NEW ALBANY, Ohio, Feb. 06, 2026 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI), a diversified industrial products and services company, today announced that its Board of Directors (“Board”) appointed Ari Levy of Lakeview Investment Group (“Lakeview”) as an independent director. Lakeview owns approximately 8.9% of the outstanding shares of the Company. In connection with Mr. Levy’s appointment, the Board was expanded to 7 members. Mr. Levy will serve on the Board’s Nominating, Governance and Sustainability, and Audit Committees.

Mr. Levy is the founder, President, and Chief Investment Officer of Lakeview Investment Group, a Chicago based Investment Manager focused on the public markets. Mr. Levy was the President of Levy Acquisition Corp, a NASDAQ listed acquisition vehicle, and subsequently served on the Board of the resulting public company, Del Taco, until it was acquired by Jack in the Box in early 2022. Ari holds a B.A. in International Relations from Stanford University.

“We are excited to welcome Ari to the Board,” said William Johnson, Chair of the Board of Directors. “His background and experience as a founder, operator, and investor will be valuable assets as we look to drive long-term value creation.”

“I am thrilled to join the CVG Board of Directors,” Ari Levy said. “I look forward to working alongside my fellow board members to help guide the Company into the future and maximize value for all stakeholders.”

Mr. Levy will stand for re-election at the Company’s 2026 Annual Meeting of Stockholders.

In connection with the appointment of Mr. Levy to the Board, the Company and Lakeview entered into a support agreement that contains customary standstill provisions.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Nathan Skown Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

BOCA RATON, Fla.–(BUSINESS WIRE)–Jan. 22, 2026– The GEO Group, Inc. (NYSE: GEO) (“GEO” or the “Company”) announced today the closing of an amendment to the Company’s Amended Credit Agreement to increase GEO’s Revolving Credit Facility commitments from $450 million to $550 million, effective January 20, 2026.

George C. Zoley, Executive Chairman of GEO, said, “We are pleased with this recent amendment to upsize our Revolving Credit Facility, which provides us with enhanced balance sheet flexibility while remaining positioned for future growth needs and long-term shareholder value creation, including through our expanded stock repurchase authorization announced in November. This important amendment also continues to demonstrate the growing support from our banking partners.”

About The GEO Group

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 95 facilities totaling approximately 75,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 20,000 employees.

Use of forward-looking statements

This news release may contain “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the U.S. Private Securities Litigation Reform Act of 1995. Readers are cautioned not to place undue reliance on these forward-looking statements and any such forward-looking statements are qualified in their entirety by reference to the cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission including its Form 10-K, 10-Q and 8-K reports. All forward-looking statements speak only as of the date of this news release and are based on current expectations and involve a number of assumptions, risks and uncertainties that could cause the actual results to differ materially from such forward-looking statements. Readers are strongly encouraged to read the full cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission, including those referenced above. GEO disclaims any obligation to update or revise any forward-looking statements, except as required by law.

Announces Cooperation Agreement with Legion Partners

CHARLOTTE, N.C., Jan. 20, 2026 (GLOBE NEWSWIRE) — NN, Inc. (“NN” or the “Company”) (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, today announced that it has appointed Ted White to its Board of Directors (the “Board”), effective immediately. In connection with this appointment, the Company has entered into a cooperation agreement (the “Cooperation Agreement”) with Legion Partners Asset Management, LLC (together with its affiliates, “Legion”), one of the Company’s largest shareholders.

Mr. White, Legion’s co-founder and Managing Director, is an experienced institutional investor and has corporate governance and capital markets expertise. He will join the Board’s Strategic Committee, which was formed to evaluate a broad range of strategic, financing and other alternatives to enhance shareholder value.

“We are pleased to welcome Ted to the Board,” said Harold Bevis, President and Chief Executive Officer of NN. “Over the last few years, we have transformed NN’s business profile while evolving our Board to ensure that we have the right skills and experience to help capitalize on the Company’s opportunities for profitable growth. We look forward to working alongside Ted to complete our transformation plan and deliver value for shareholders.”

Mr. White added, “I am excited to be joining the Board at this critical juncture as the Company continues to drive organic growth and profitability. I look forward to working with my fellow directors to unlock the significant upside in NNBR’s shares for the benefit of all shareholders.”

Mr. White’s addition to the Board was completed following constructive engagement with another of the Company’s largest shareholders, Corre Partners Management, LLC (“Corre”). Corre has informed the Company that it is supportive of the appointment, including Mr. White’s membership on the Board’s Strategic Committee.

Pursuant to the Cooperation Agreement, Legion has agreed to a customary standstill, voting commitment, and related provisions. The full Cooperation Agreement will be filed as an exhibit to a Current Report on Form 8-K with the U.S. Securities and Exchange Commission.

About Ted White

Ted White is co-founder and a Managing Director of Legion Partners Asset Management, an institutional asset management firm. Prior to founding Legion Partners, Mr. White served in various functions with Knight Vinke Asset Management, a European-based investment management firm. Positions included Managing Director and Chief Operating Officer, where he was responsible for finance, operations, legal, marketing and client service functions. He is a former Deputy Director of the Council of Institutional Investors (CII), where responsibilities included policy development and implementation. Earlier in his career, Mr. White was a Portfolio Manager, Director of Corporate Governance, for the California Public Employees’ Retirement System (“CalPERS”), where he was responsible for all components of its Governance Program, including $3 billion in active management, policy development and implementation, proxy voting and focused engagement activities. Prior to CalPERS, Mr. White was an Investment Officer – Deputy State Treasurer at the California State Treasurer’s Office, where his duties included fixed income portfolio analysis and trading, among other responsibilities. He has served as a director of Clear Channel Outdoor Holdings, Inc. (NYSE: CCO) since 2024.

Mr. White earned an MBA from California State University in Sacramento with a concentration in finance. He is also a Chartered Financial Analyst Charterholder.

About NN

NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and China. For more information about the company and its products, please visit www.nninc.com.

Investor Relations: Joseph Caminiti or Stephen Poe NNBR@alpha-ir.com 312-445-2870

Forward-Looking Statements

This press release contains express and implied forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including, but not limited to, statements regarding the Company’s previously announced review of strategic, financing and other alternatives, including the timing and outcome of such review, our long-term financial profile and other statements that are not historical fact. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “growth,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project”, “trajectory” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of management’s control and that may cause actual results to be materially different from such statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector; material changes in the costs and availability of raw materials; the level of our indebtedness; our ability to secure, maintain or enforce patents or other appropriate protections for our intellectual property; and cyber liability or potential liability for breaches of our or our service providers’ information technology systems or business operations disruptions. The foregoing factors should not be construed as exhaustive and should be read in conjunction with the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s filings made with the U.S. Securities and Exchange Commission. The Company undertakes no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law. New risks and uncertainties may emerge from time to time, and it is not possible for the Company to predict their occurrence or how they will affect the Company. The Company qualifies all forward-looking statements by these cautionary statements.

Closes its First Prepaid Long-Term Hangar Lease with a $5.9 million Upfront Cash Payment

WEST HARRISON, N.Y.–(BUSINESS WIRE)– Sky Harbour Group Corporation (NYSE: SKYH, SKYH WS) (“SHG” or the “Company”), an aviation infrastructure company building the first nationwide network of Home Base Operator (HBO) campuses for business aircraft, announced today that its indirect, wholly-owned subsidiary Sky Harbour Capital III LLC (“SKYH Capital III”) is filing today with the Municipal Securities Rulemaking Board through its Electronic Municipal Market Access system (“EMMA”) a Preliminary Limited Offering Memorandum relating to the offering of $100 million of tax-exempt fixed rate bonds with a 5-year mandatory tender date (the “Series 2026 Bonds”), which are proposed to be issued by the Public Finance Authority of Wisconsin, a multi-jurisdictional conduit issuer. Through underwriters Barclays Capital, J.P. Morgan, and Academy Securities, SKYH Capital III expects to price the Series 2026 Bonds during the week of January 26th, after a two-week investor marketing period. The proceeds of the Series 2026 Bonds are expected to be used to finance the development of certain of the Company’s hangar campuses, as described below. The principal amount, structure, tenor and timing are preliminary and subject to change. Any such offering is dependent on market and other conditions, and there is no assurance that all or any of the Series 2026 Bonds will be offered.

Separately, Sky Harbour Capital II (“SKYH Capital II”) completed the onboarding of subsidiaries owning its hangar campuses at Camarillo Airport and Bradley International Airport to the borrowing base of its committed warehouse bank facility with JPMorgan Chase Bank, N.A. on January 8, 2026 (the “JPM Facility”). The Company also amended the JPM Facility in order to facilitate the flow of funds securing the proposed Series 2026 Bonds. These amendments have been filed under Form 8-K with the SEC. On the same date, SKYH Capital II drew funds of approximately $13 million to reimburse the Company for prior advances associated with capital expenditures at Bradley International Airport and certain costs of issuance and fund certain reserves for the JPM Facility.

Update on Leasing Activities

Stabilized campuses: The Company expects revenue per square foot at its stabilized campuses to increase as legacy hangar leases turn over or are renewed and through the annual rent escalators embedded in all tenant leases.

Recently opened campuses: As of January 9, 2026, Dallas Addison (ADS) Phase 1, Phoenix Deer Valley (DVT) and Denver Centennial (APA) have reached 87% ,73% and 27% occupancy levels, respectively.

Pre-leasing: We continue our pre-lease activities at Washington Dulles (IAD), Bradley International Airport (BDL), and have begun pre-leasing at Miami-Opa Locka (OPF) Phase 2 and Addison (ADS) Phase 2. The latter two projects are under construction following the success of their respective Phase 1 developments, which are now nearly fully leased.

Selective long-term partnerships: We have extended our documentation negotiation period under the letter of intent with a potential joint-venture partner leasing a single SH34 hangar at OPF Phase 2 through mid-March 2026, in order to address certain operational requirements. Separately, we continue discussions for similar joint ventures at other locations in the network with other parties.

Ultra-long tenant leases: In late December, we entered into an amended lease with an existing tenant at OPF Phase 1 for a 15-year lease term in exchange for an upfront lump sum rent payment of $5.9 million.

Update on Capital Formation

The proposed Series 2026 Bonds, if completed, would raise $100 million, reducing the need for additional equity contributions associated with the $200 million JPM Facility. As previously disclosed, the JPM Facility has a 5-year term commencing September 2025 with an interest rate of 80% of the sum of daily SOFR + 0.10%, plus 200 basis points. The Company subsequently entered into a floating-to-fixed interest rate swap, with a notional schedule based on the anticipated draws under the JPM Facility and a 4.73% fixed rate for the duration of the term of the JPM Facility. Proceeds from the JPM Facility and the Series 2026 Bonds are expected to be used to fund construction projects at Bradley International Airport (BDL), Salt Lake City International (SLC), Orlando Executive Airport (ORL), Hudson Valley Regional Airport (POU), Trenton-Mercer Airport (TTN), Chicago Executive Airport (PWK) and Dulles International Airport (IAD). The JPM Facility is expandable to $300 million subject to credit approval.

If completed as planned, the $100 million raised from the Series 2026 Bond issuance and the $200 million of borrowing capacity available from the JPM Facility and other existing Company resources are expected to fully fund approximately 1.1 million rentable square feet of new hangars, for a total of approximately 2.1 million rentable square feet portfolio-wide.

Selective long-term partnerships: Should the company enter selective long-term partnerships or ultra long-term tenant leases as described above, the Company expects to use the proceeds for the satisfaction of any of its future capital needs and for general corporate purposes.

Internal Cash Flow Generation. The Company expects that between its leasing activities in Q4 2025, Q1 2026, and the anticipated opening of its OPF Phase 2 campus in Q2 2026, the Company will now be able to reinvest internally generated cash flows as equity for its future developments.

About Sky Harbour

Sky Harbour Group Corporation is an aviation infrastructure company developing the first nationwide network of Home-Basing campuses for business aircraft. The company develops, leases, and manages general aviation hangar campuses across the United States. Sky Harbour’s Home-Basing offering aims to provide private and corporate residents with the best physical infrastructure in business aviation, coupled with dedicated service, tailored specifically to based aircraft, offering the shortest time to wheels-up in business aviation. To learn more, visit www.skyharbour.group.

Forward Looking Statements

Certain statements made in this release are “forward looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including statements about the financial condition, results of operations, earnings outlook and prospects of SHG, including statements regarding our expectations for future results, our expectations for future ground leases, our plans for future capital raising activity, the transactions contemplated by the letter of intent, our expectations on future construction and development activities and lease renewals, and our plans for future financings. When used in this press release, the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The forward-looking statements are based on the current expectations of the management of Sky Harbour Group Corporation (the “Company”) as applicable and are inherently subject to uncertainties and changes in circumstances. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. For more information about risks facing the Company, see the Company’s annual report on Form 10-K for the year ended December 31, 2024 and other filings the Company makes with the SEC from time to time. The Company’s statements herein speak only as of the date hereof, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators

We use a number of metrics, including annualized revenue run rate per leased rentable square foot, to help us evaluate our business, measure our performance, identify trends affecting our business, formulate business plans, and make strategic decisions. Our key performance indicators may be calculated in a manner different than similar key performance indicators used by other issuers. These metrics are estimated operating metrics and not projections, nor actual financial results, and are not indicative of current or future performance.

Disclaimer

This Notice does not constitute an offer to sell Series 2026 Bonds or the solicitation of an offer to buy, nor shall there be any sale of the Series 2026 Bonds by any person in any state or other jurisdiction to any person to whom it is unlawful to make such offer, solicitation or sale in such state or jurisdiction. No dealer, broker, salesperson or any other person has been authorized to give any information or to make any representation other than those contained in the Preliminary Limited Offering Memorandum in connection with the contemplated offering of the Series 2026 Bonds, and, if given or made, such information or representation must not be relied upon.

BOCA RATON, Fla.–(BUSINESS WIRE)–Dec. 22, 2025– The GEO Group, Inc. (NYSE: GEO) (“GEO” or the “Company”) announced today that its wholly-owned subsidiary, BI Incorporated (“BI”), has been awarded a contract by U.S. Immigration and Customs Enforcement (“ICE”) for the provision of skip tracing services. Skip tracing services entail enhanced location research with identifiable information, commercial data verification, and physical observation to verify current address information and investigate alternative address information for individuals on the federal government’s non-detained docket.

The new contract has a term of two years, with an initial term of one year, effective December 16, 2025, and an additional one-year period. The estimated revenue value of the two-year contract is up to approximately $121 million.

George C. Zoley, Executive Chairman of GEO, said, “The expansion of our services addressing the non detained docket through this new contract is a testament to the high-quality solutions BI has provided to ICE for more than 21 years. We appreciate the confidence that ICE and the U.S. Department of Homeland Security have continued to place in our company.”

About The GEO Group

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 95 facilities totaling approximately 75,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 20,000 employees.

Use of forward-looking statements

This news release may contain “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the U.S. Private Securities Litigation Reform Act of 1995. Readers are cautioned not to place undue reliance on these forward-looking statements and any such forward-looking statements are qualified in their entirety by reference to the cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission including its Form 10-K, 10-Q and 8-K reports. All forward-looking statements speak only as of the date of this news release and are based on current expectations and involve a number of assumptions, risks and uncertainties that could cause the actual results to differ materially from such forward-looking statements. Readers are strongly encouraged to read the full cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission, including those referenced above. GEO disclaims any obligation to update or revise any forward-looking statements, except as required by law.

BRENTWOOD, Tenn., Dec. 12, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic” or the “Company”) announced today that CoreCivic’s Board of Directors (the “Board”) has appointed Daren Swenson, who currently serves as CoreCivic’s Senior Vice President and Chief Corrections Officer, to Executive Vice President and Chief Corrections and Reentry Officer (CCRO), effective January 1, 2026, overseeing the operations for our corrections, detention, and reentry facilities.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “Daren is an exceptional leader whose decades of service within the organization has allowed him to develop an in-depth knowledge of our business. I am confident that Daren’s demonstrated abilities will serve us well in the midst of a period of rapid growth.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “I look forward to Daren’s continued contributions to operational excellence, drawing on his extensive experience with the Company, as we tend to the growing needs of our government partners.”

Mr. Swenson said, “I am deeply honored by the trust CoreCivic’s Board and executive leadership have placed in me with this new role. Having spent my career with CoreCivic since 1992, I have witnessed firsthand the dedication and professionalism of our team as we work to serve our government partners and the public good. I am grateful for the opportunity to continue helping individuals on their path to reentry and addressing the complex needs of our government partners. As we move forward during this exciting period of growth, I look forward to working alongside my colleagues to deliver innovative solutions and uphold the high standards that define CoreCivic.”

Mr. Swenson began his career with CoreCivic in 1992 at our Prairie Correctional Facility in Appleton, Minnesota as a Correctional Sergeant. Before becoming Senior Vice President and Chief Corrections Officer of the Company, Mr. Swenson progressed through multiple leadership positions including Warden, Managing Director, and Vice President. Mr. Swenson holds bachelor’s degrees in psychology and sociology from North Dakota State University and a master’s degree in management with a concentration in Organizational Leadership from Middle Tennessee State University.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes forward-looking statements concerning executive leadership positions at CoreCivic and prospects of growth in CoreCivic’s business. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

Committee to Evaluate a Broad Range of Strategic, Financing and Other Alternatives to Enhance Shareholder Value

CHARLOTTE, N.C., Dec. 12, 2025 (GLOBE NEWSWIRE) — NN, Inc. (“NN” or the “Company”) (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, today announced that the Board of Directors (the “Board”) has formed a Strategic Committee to oversee a review of strategic and financial alternatives to further enhance shareholder value.

The Strategic Committee is comprised of three independent directors, Raynard Benvenuti, Jeri Harman and Thomas Wilson, and has been tasked with evaluating a broad spectrum of strategic, financial and business configuration options for the Company. The Board has engaged Houlihan Lokey, a leading independent investment bank, as the Company’s financial advisor.

“The Board’s decision to form a Strategic Committee reflects our commitment to maximizing value for NN’s shareholders and evaluating potential avenues to achieve this objective,” said Ms. Harman, independent Chair of NN. Ms. Harman continued, “Over the past several years, we have strengthened our executive team, sharpened our strategic focus, expanded operating income and EBITDA, built a new sales pipeline of more than $800 million, secured approximately $200 million in new business, entered the medical and data center markets, developed a healthy M&A pipeline, and positioned the Company to scale up to its next stage of growth. These accomplishments have improved our earnings quality and enhanced our free cash flow generation profile. With this stronger foundation in place, we believe now is the right time to take a fresh, comprehensive look at additional ways to unlock value for our shareholders.”

Harold Bevis, President and Chief Executive Officer of NN, added, “As the Committee conducts its review, the Company remains focused on advancing its transformation plan and delivering the high-quality products, engineering support and service that our customers expect from NN.”

There can be no assurance that the process will result in any particular outcome. NN has not set a timetable for the completion of the review, and the Company does not intend to provide further updates unless and until the Board has approved a specific course of action or determines additional disclosure is appropriate or necessary.

ABOUT NN

NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and China. For more information about the company and its products, please visit www.nninc.com.

Forward-Looking Statements

This press release contains express and implied forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including, but not limited to, statements regarding the strategic review, including the timing and outcome of such review, our long-term financial profile and other statements that are not historical fact. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “growth,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project”, “trajectory” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of management’s control and that may cause actual results to be materially different from such statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector; material changes in the costs and availability of raw materials; the level of our indebtedness; our ability to secure, maintain or enforce patents or other appropriate protections for our intellectual property; and cyber liability or potential liability for breaches of our or our service providers’ information technology systems or business operations disruptions. The foregoing factors should not be construed as exhaustive and should be read in conjunction with the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s filings made with the U.S. Securities and Exchange Commission. The Company undertakes no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law. New risks and uncertainties may emerge from time to time, and it is not possible for the Company to predict their occurrence or how they will affect the Company. The Company qualifies all forward-looking statements by these cautionary statements.

Investor Relations: Joseph Caminiti or Stephen Poe, Investors NNBR@alpha-ir.com 312-445-2870

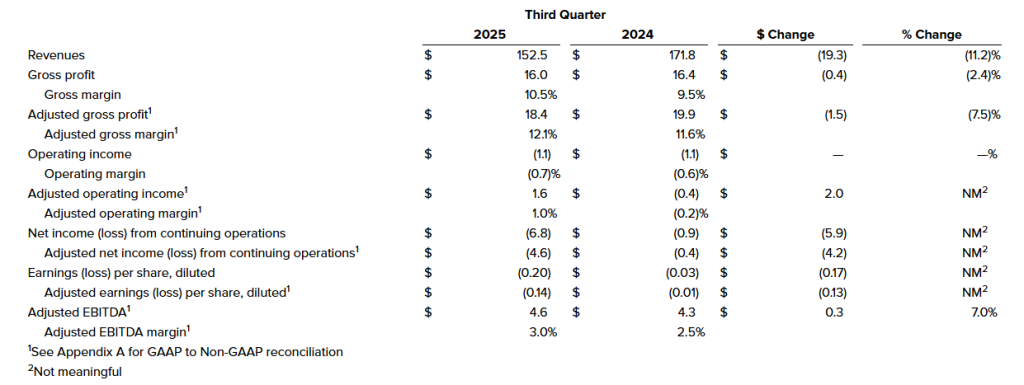

Third quarter sales of $152 million, EPS of $(0.20), Adjusted EBITDA of $4.6 million Returns to growth in Global Electrical Solutions segment Updates full year 2025 guidance

NEW ALBANY, Ohio, Nov. 10, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its third quarter ended September 30, 2025.

Third Quarter 2025 Highlights(Results from Continuing Operations; compared with prior year, where comparisons are noted)

Revenues of $152.5 million, down 11.2%, primarily due to softening in North American demand.

Operating loss of $1.1 million, flat compared to operating loss of $1.1 million. Adjusted operating income of $1.6 million, compared to adjusted operating loss of $0.4 million. The increase in adjusted operating income was primarily attributable to improved gross margin performance and lower SG&A expenses.

Net loss from continuing operations of $6.8 million, or $(0.20) per diluted share and adjusted net loss of $4.6 million, or $(0.14) per diluted share, compared to net loss from continuing operations of $0.9 million, or $(0.03) per diluted share and adjusted net loss of $0.4 million, or $(0.01) per diluted share.

Adjusted EBITDA of $4.6 million, up 7.0%, with an adjusted EBITDA margin of 3.0%, up from 2.5%.

James Ray, President and Chief Executive Officer, said, “In the face of ongoing lower demand in our key Construction, Agriculture, and Class 8 truck end markets, we were pleased with the resilience seen in our third quarter results. We continued to benefit from our operational efficiency improvement and right sizing our manufacturing footprint and enterprise structural cost, evidenced by the continued sequential expansion in our adjusted gross margin in the quarter, despite the lower demand environment. Furthermore, as part of our efforts to preserve margins and position CVG for an eventual end market recovery, we remain focused on reducing SG&A expenses, and we have made demonstrable progress with customers as it relates to mitigating tariff impacts. I want to sincerely thank every member of the CVG team for their commitment, resilience, and focus on execution.”

Mr. Ray continued, “We are encouraged by the continued improvement in Global Electrical Systems segment performance, which returned to year-over-year revenue growth in third quarter, driven by new business wins outside of the Construction and Agriculture end markets, which continue to see lower demand. This segment also saw continued margin expansion year-over-year. In addition, our Global Seating segment expanded margins, as we see the benefits of our operational efficiency improvements, even in a softer demand environment. Our North American-focused Trim Systems and Components segment continues to see weakness as Class 8 production declines year-over year. However, we are taking proactive actions to improve profitability in the face of lower production levels. As an organization, we remain laser-focused on the levers we can control to improve financial performance, drive operational efficiency, and while continuing to launch previously won new customer programs across all segments to best position CVG for the future.”

Andy Cheung, Chief Financial Officer, added, “We are encouraged by our margin performance in the quarter, particularly against a difficult demand backdrop. We continue to optimize our operations to account for individual end market outlooks, particularly in the North American Class 8 truck market. While softer orders led to an inventory increase in the third quarter, we expect to reduce working capital in the fourth quarter. We remain focused on cash generation, with an expectation to drive at least $30 million in free cash flow for the full fiscal year. Continued free cash generation and debt paydown remain our near-term focus areas as we look to drive further cost reductions and improve overall operational efficiency.”

Third Quarter Financial Results from Continuing Operations (amounts in millions except per share data and percentages)

Consolidated Results from Continuing Operations

Third Quarter 2025 Results

Third quarter 2025 revenues were $152.5 million, compared to $171.8 million in the prior year period, a decrease of 11.2%. The overall decrease in revenues was due to lower sales as a result of a softening in customer demand, primarily in the Global Seating and Trim Systems & Components segments.

Operating loss in the third quarter 2025 was flat compared to the prior year period at $1.1 million. Third quarter 2025 adjusted operating income was $1.6 million, compared to loss of $0.4 million in the prior year period. The increase in adjusted operating income was primarily attributable to improved gross margin performance and lower SG&A expenses.

Interest associated with debt and other expenses was $4.1 million and $2.4 million for the third quarter 2025 and 2024, respectively, due to higher interest rates.

Net loss from continuing operations was $6.8 million, or $(0.20) per diluted share, for the third quarter 2025 compared to net loss of $0.9 million, or $(0.03) per diluted share, in the prior year period. Third quarter 2025 adjusted net loss from continuing operations was $4.6 million, or $(0.14) per diluted share, compared to adjusted net loss of $0.4 million, or $(0.01) per diluted share.

On September 30, 2025, the Company had $20.2 million of outstanding borrowings on its U.S. revolving credit facility and $4.2 million outstanding borrowings on its China credit facility, $31.3 million of cash and $96.5 million of availability from the credit facilities (subject to customary borrowing base and other conditions), resulting in total liquidity of $127.8 million.

Third Quarter 2025 Segment Results

Global Seating Segment

Revenues were $68.7 million compared to $76.6 million for the prior year period, a decrease of 10.4%, due to lower sales volume as a result of decreased customer demand.

Operating income was $1.4 million, compared to loss of $1.5 million in the prior year period, an increase of $2.9 million, driven by improved gross margin performance and lower SG&A expenses. Third quarter 2025 adjusted operating income was $2.9 million compared to loss of $0.8 million in the prior year period.

Global Electrical Systems Segment

Revenues were $49.5 million compared to $46.7 million in the prior year period, an increase of 5.9%, primarily as a result of ramping new business wins.

Operating income was $0.8 million compared to loss of $1.5 million in the prior year period, an increase of $2.3 million. The increase in operating income was primarily attributable to higher sales volumes. Third quarter 2025 adjusted operating income was $1.4 million compared to loss of $0.2 million in the prior year period.

Trim Systems and Components Segment

Revenues were $34.3 million compared to $48.4 million in the prior year period, a decrease of 29.2%, primarily due to lower sales volume.

Operating loss was $0.9 million compared to an operating income of $5.4 million in the prior year period. The decrease in operating income was primarily attributable to lower demand and a gain on a facility sale in the prior period. Third quarter 2025 adjusted operating loss was $0.3 million compared to income of $4.1 million in the prior year period.

Outlook

CVG updated the Company’s outlook for the full year 2025, based on current market conditions:

This outlook reflects, among others, current industry forecasts for North America Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 239,000 units, down 28% versus the 2024 actual Class 8 truck builds of 332,372 units and down 5% from the time of our second quarter 2025 earnings release, when ACT Research was forecasting 252,000 units for 2025 North American Class 8 truck production.

Construction and Agriculture end markets are projected to decline approximately 5-15% in 2025. However, we expect the contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, November 11, 2025, at 8:30 a.m. ET. Management intends to reference the Q3 2025 Earnings Call Presentation during the conference call. To participate, dial (800) 549-8228 using conference code 19689. International participants dial (289) 819-1520 using conference code 19689.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 19689#.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Nathan Skown Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions, production of new products, plans for capital expenditures, and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Other Information

Throughout this document, certain numbers in the tables or elsewhere may not sum due to rounding. Rounding may have also impacted the presentation of certain year-on-year percentage changes.

BRENTWOOD, Tenn., Nov. 10, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that its Board of Directors authorized an increase to its existing share repurchase program pursuant to which CoreCivic may purchase up to an additional $200 million in shares of CoreCivic’s outstanding common stock. As a result of the increase, the aggregate authorization under CoreCivic’s repurchase program increased from up to $500.0 million shares of common stock to up to $700.0 million shares of common stock.

Since the share repurchase program was authorized in May 2022, through November 7, 2025, we have repurchased a total of 21.5 million shares of our common stock at an aggregate cost of $322.1 million, or $14.98 per share, excluding fees, commissions and other costs related to the repurchases. As of November 7, 2025, including the additional authorization, we have $377.9 million of repurchase authorization available under the share repurchase program.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “We are pleased to announce an increase to our stock repurchase authorization. We remain committed to deploying capital in ways that we believe will enhance long-term shareholder value. While our share price is influenced by many factors outside our control, we believe our current valuation does not fully reflect the progress and opportunities we see in our business.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “We believe our recently announced contract awards and the overall strength of our business position us well to execute on our capital allocation strategy. Given our earnings trajectory, alternative opportunities to deploy capital, and our current share price, we are prioritizing the allocation of our cash flows to our share repurchase program.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

Strong grossmargins of 15.1%, expansion of 80basis points

Reaffirming Adjusted EBITDA guidance for full year

CHICAGO, Nov. 10, 2025 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the third quarter ended September 30, 2025.

ThirdQuarter 2025Highlights

Revenues of $160.5 million, compared to $113.3 million in the third quarter of 2024, with railcar deliveries of 1,304 units compared to 961 units in the prior year period

Gross margin of 15.1% with gross profit of $24.2 million, compared to gross margin of 14.3% with gross profit of $16.2 million in the third quarter of 2024

Recorded a $17.6 million non-cash adjustment due to share price appreciation resulting in a Net loss of $(7.4) million, or $(0.23) per share, and Adjusted net income of $7.8 million, or $0.24 per share

Adjusted EBITDA was $17.0 million, representing a margin of 10.6%, compared to $10.9 million and a margin of 9.6% in the third quarter of 2024

Ended the quarter with a backlog of 2,750 units valued at $222.0 million, reflecting a diversified mix of railcar conversion programs and new railcar builds

Well-positioned to deploy capital for growth, with $62.7 million in cash and equivalents and no borrowings under the company’s revolving credit facility

“Our third quarter results highlight the strength of our operating platform and the continued execution of our commercial strategy,” said Nick Randall, President and Chief Executive Officer of FreightCar America. “We delivered record third quarter Adjusted EBITDA at our new facility, reflecting the benefits of improved production efficiency and favorable product mix. Our team continues to demonstrate manufacturing flexibility which, coupled with our customer-centric approach, differentiates FreightCar America in the market. While overall industry demand remains subdued, we continue to support customers by leveraging our expertise in conversions and customized solutions to create value for our customers.”

Randall continued, “This quarter’s strong bottom line performance reflects our manufacturing discipline and commercial excellence. By building for value and meeting complex customer requirements instead of commoditized throughput, we delivered exceptional Adjusted EBITDA performance and strengthened the Company’s financial position. With this momentum, we enter the final quarter well-positioned to deliver profitable growth, generate positive free cash flow and advance our long-term growth initiatives.”

FiscalYear2025 Outlook

The Company has updated its outlook for fiscal year 2025 as follows:

Fiscal2025 Outlook

Year-over-Year ChangeatMidpoint of Range

Railcar Deliveries

4,500 – 4,900 Railcars

7.7

%

Revenue

$500 – $530 million

(7.9

)%

AdjustedEBITDA1

$43 – $49 million

7.0

%

1. The Company does not provide a reconciliation of forward-looking Adjusted EBITDA guidance due to the inherent difficulty in forecasting and quantifying adjustments necessary to calculate such non-GAAP measure without unreasonable effort. Material changes to such adjustments, including warrant liability and non-core operating items, could affect future GAAP results.

Mike Riordan, Chief Financial Officer of FreightCar America, added, “We delivered another quarter of solid financial results, including strong deliveries, margin performance and operating cash flow. Looking ahead, while our change in revenue guidance reflects product mix as we saw a larger number of conversion railcars compared to new railcars in the second half of 2025, our profitability and positive cash performance remain on track, underscoring the resilience of our business model, which fuels our capital strength and positions us to drive long-term sustainable growth.”

ThirdQuarter 2025 ConferenceCall&Webcast Information

The Company will host a conference call and live webcast on Monday, November 10, at 11:00 a.m. (Eastern Time) to discuss its third quarter 2025 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call. Teleconference details are as follows:

An audio replay of the conference call will be available beginning at 3:00 p.m. (Eastern Time) on Monday, November 10, 2025, until 11:59 p.m. (Eastern Time) on Monday, November 24, 2025. To access the replay, please dial (844) 512-2921 or (412) 317-6671. The replay passcode is 13756539. An archived version of the webcast will also be available on the FreightCar America Investor Relations website.

AboutFreightCarAmerica

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-LookingStatements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse geopolitical, economic and market conditions, including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials, including steel and aluminum; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion; delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings; potential unexpected changes in laws, rules, and regulatory requirements, including tariffs and trade barriers (including recent United States tariffs imposed or threatened to be imposed on China, Canada, Mexico and other countries and any retaliatory actions taken by such countries); the scope and duration of the government shutdown; and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAPFinancialMeasures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted EPS, Free cash flow and Adjusted free cash flow. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.

WEST CHICAGO, Ill., Oct. 28, 2025 /PRNewswire/ — Titan International, Inc. (NYSE: TWI) (“Titan” or the “Company”), a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products, today announced the closing of a strategic partnership with Rodaros Industria de Rodas Ltda. (“Rodaros”), a Brazilian manufacturer of agricultural and construction wheels. This deal was first announced during Titan’s second quarter 2025 earnings call on July 31st and has now completed formal regulatory review.

Rodaros is the second largest manufacturer of agricultural wheels in Brazil. This partnership will be forged with an initial cash investment of $4 million by Titan for a 20% ownership stake and includes commitments to acquire the remaining 80% in 2029 based on financial performance criteria for final valuation of the enterprise. Titan will obtain one Board seat within Rodaros (out of a three-member Board) and will begin providing financial leadership.

Paul Reitz, President and Chief Executive Officer of Titan stated, “This partnership reinforces Titan’s commitment to offering the best solutions for our customers’ equipment and to driving performance improvements in agriculture and construction operations. By combining Rodaros’ excellence in wheel manufacturing with Titan’s market leading tire production and distribution across the entire region, we are paving the way for the development of integrated solutions tailored to the Brazilian and South American markets.”

Mr. Reitz continued “Building on Titan’s One Stop Shop framework, this strategic partnership now gives us the opportunity to distribute wheel/tire assemblies to existing OEM customers, particularly in Brazil, the third largest agricultural market in the world. Over the years, I’ve talked to key OEMs in Brazil, and they expressed enthusiasm about the opportunity to procure wheel/tire assemblies, which is something that none of our key competitors offer in that region. I expect this partnership to be a game changer for our customers and anticipate that wheel/tire assemblies will be a successful part of our Brazilian portfolio, much like they are in the US. Additionally, it gets us one step closer to our goal of being a supplier that OEMs can rely on for both wheels and tires, for all key geographies across the globe. We are excited about the growth opportunities that this partnership will provide for Titan, and about the ability to better serve our customers.”

Ronaldo Linero, CEO of Rodaros added, “This partnership is founded on shared values and complementary technical expertise between the companies. Our goal is to generate real synergies and deliver added value to the end customer”.

About Titan

Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the Company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, announced that it will release its second quarter fiscal year 2026 financial results before financial markets open on Friday, November 7, 2025.

The Company will host a conference call and webcast to review its financial and operating results, strategy, and outlook. A question-and-answer session will follow.

Second Quarter Fiscal Year 2026 Financial Results Conference Call

Friday, November 7, 2025 11:00 a.m. Eastern Time Phone: (201) 689-8560 Internet webcast link and accompanying slide presentation: ir.grahamcorp.com

A telephonic replay will be available from 3:00 p.m. ET on the day of the teleconference through Friday, November 14, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13756267 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

ABOUT GRAHAM CORPORATION Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space, industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

WEST HARRISON, N.Y.–(BUSINESS WIRE)– Sky Harbour Group Corporation (NYSE: SKYH, SKYH WS) (“SHG” or the “Company”), an aviation infrastructure company building the first nationwide Home Base Operator (HBO) network of campuses for business aircraft, announced the release of its unaudited financial results for the three months ended June 30, 2025 on Form 10-Q. The Company also announced the filing of its unaudited financial results for the three months ended June 30, 2025 for Sky Harbour Capital (Obligated Group) with MSRB/EMMA. Please see the following links to access the filings:

Financial Highlights on a Consolidated Basis include:

Constructed assets and construction in progress reached over $295 million at quarter end, an increase of $125 million year-over-year and $18 million as compared to the prior quarter.

Q2 2025 consolidated revenues increased 82% as compared to Q2 2024 and 18% as compared to the prior quarter.

Net cash used in operating activities was approximately $0.9 million for the quarter, a significant improvement from the $5 million used in prior quarter.

Strong liquidity and capital resources as of June 30th, 2025, with consolidated cash and US Treasuries totaling nearly $75 million.

Reiterating our guidance of reaching operating cash-flow breakeven on a consolidated run-rate basis by year-end 2025, supported by the commencement of revenues from campuses in Phoenix, Denver, Dallas and Seattle.

Financial Highlights at Sky Harbour Capital (Obligated Group) include:

Q2 2025 Obligated Group Revenues increased approximately 20% as compared to the prior quarter.

Net cash from operating activities (positive) reached approximately $2.2 million in Q2 2025, a 117% increase from the prior quarter.

Cash and US Treasuries at the Obligated Group totaled $37 million as of June 30th, 2025.

Update on Site Acquisition

Sky Harbour currently has campuses operating at Houston’s Sugar Land Regional Airport (SGR), Nashville International Airport (BNA), Miami Opa-Locka Executive Airport (OPF), San Jose Mineta International Airport (SJC), Camarillo Airport (CMA), Phoenix Deer Valley Airport (DVT), Dallas’s Addison Airport (ADS), Seattle’s King County International Airport – Boeing Field (BFI); one campus nearing construction completion at Denver’s Centennial Airport (APA); campuses in pre-development at Chicago Executive Airport (PWK), Sky Harbour’s first four New-York-metro area airports – Bradley International Airport (BDL), Hudson Valley Regional Airport (POU), Trenton-Mercer Airport (TTN), and Stewart International Airport (SWF); Orlando Executive Airport (ORL), Dulles International Airport (IAD), Salt Lake City International Airport (SLC), and Portland-Hillsboro Airport (HIO).

We reiterate our prior guidance of five additional airport ground leases to be announced by the end of 2025, for a total portfolio of 23 airports by year end.

Update on Construction and Development Activities, Change in Development Leadership

As reported on our monthly activity reports filed with MSRB/EMMA, and available on our website, Dallas Addison (ADS) achieved its first Certificates of Occupancy in Q2 and has commenced resident flight operations. Denver Centennial (APA) achieved its first Certificates of Occupancy last month and will commence resident flight operations in the coming weeks. Please see the following link for the last monthly construction report:

Miami Opa Locka (OPF) Phase 2 commenced construction in Q2 and is expected to be completed by Q2 2026.

Outgoing COO, Will Whitesell, who led the Company’s construction division, has entered an amicable separation agreement with the Company and has assisted in an orderly transfer of his responsibilities. The Company is grateful for Will’s commitment and his contributions and wishes him much success in his future endeavors.

Phil Amos, a 40-year veteran of the Pre-Engineered Metal Building (PEMB) industry, and co-founder of A&F Contractors, has joined Sky Harbour as Head of Construction and President of Sky Harbour’s newly-formed, wholly-owned development subsidiary, Ascend Aviation Services (“Ascend”). Ascend brings specialized airport construction-management and in-house General Contracting capabilities to Sky Harbour. Ascend is headquartered in Houston, TX, and staffed by veterans of the airport construction industry around the United States, including legacy members of the Sky Harbour development team. In addition to its construction management and general contracting functions, Ascend oversees the operations of Stratus Building Systems, Sky Harbour’s wholly-owned PEMB manufacturing subsidiary. Ascend and Stratus together constitute a vertically-integrated, specialized airport infrastructure developer. Mr. Amos, while at A&F, served as the general contractor for Sky Harbour’s first hangar campus at Sugar Land Regional Airport, which was delivered on time and under budget.

Update on Leasing Activities

Stabilized campuses: The Company continues to enjoy higher-than-forecast revenue per square foot at its stabilized campuses. Revenue per square foot continues to grow as legacy hangar leases turn or are renewed.

New campuses: The Company has executed the first six hangar leases at its new Denver, Dallas and Phoenix campuses, and is under LOI for additional leases. The Company expects to meet its revenue run-rate targets at the new campuses within six months.

Pre-leasing: The Company has initiated a pilot project at two airports – Bradley International Airport (BDL) and Dulles International Airport (IAD) to pre-lease hangar space prior to construction commencement. The objective is to take advantage of growing awareness of the Sky Harbour HBO value proposition within the US Business Aviation industry to a) reduce lease-up times, b) better curate resident communities, and c) integrate customized resident improvements during construction (as opposed to retrofitting). Hangar leases have been executed at both airports at revenue rates that present an introductory pricing advantage to pre-lease residents while still delivering above-target per-square-foot revenue to the Company. Additional pre-leases are under LOI.

Update on Airport Operations

As of Q3, the Company is conducting flight operations at nine airports.

Under the leadership of Marty Kretchman, Senior Vice President of Airports, the company has transitioned to a centralized operating model, featuring National Directors of Line Training; Facilities; and Ground Support Equipment (GSE).

Surveys of current residents indicate that Sky Harbour’s HBO service offering has become a key differentiating component of the Sky Harbour value proposition. The Company plans to continue to invest in constant improvement in airfield operations, through selective recruiting, rigorous training, detailed and thoughtful operating procedures, and constant innovation in collaboration with Sky Harbour residents.

Update on Capital Formation

After several quarters of “dual tracking” the review of various debt funding alternatives and proposals, the Company has decided to pursue a tax-exempt bank debt facility in lieu of a bond issue.

We are currently in advanced discussions with a major US financial institution for an expected five (5) year drawdown construction facility of $200 million, with an expected indicative interest rate of 80% of 3-month SOFR plus 200 basis points (~5.47% in the current market).

Our debt financing plan is to fund the next 5-6 airport projects using this facility and internal equity. The Company expects to replace this facility with permanent tax-exempt bonds in the next 3-4 years. We expect to close the facility on or about August 28th. However, we can provide no assurance on exact terms or the timing of this facility.

Tal Keinan commented: “As Sky Harbour navigates the transition from a tactical team, emphasizing agility, innovation and flexibility, to a high-growth organization, increasingly embracing process, discipline and specialization, five constants will continue to guide our leadership: 1) Obsessive focus on the Resident, 2) Commitment to building long-term shareholder value, 3) Uncompromising pursuit of professional excellence, 4) Cost-efficiency, and 5) Individual ownership of results. We value the reputation we are building in business aviation and intend to continue building it for years to come.”

About Sky Harbour

Sky Harbour Group Corporation is an aviation infrastructure company developing the first nationwide network of Home-Basing campuses for business aircraft. The company develops, leases, and manages general aviation hangar campuses across the United States. Sky Harbour’s Home-Basing offering aims to provide private and corporate residents with the best physical infrastructure in business aviation, coupled with dedicated service, tailored specifically to based aircraft, offering the shortest time to wheels-up in business aviation. To learn more, visit www.skyharbour.group.

Forward Looking Statements

Certain statements made in this release are “forward looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including statements about the financial condition, results of operations, earnings outlook and prospects of SHG, including statements regarding our expectations for future results, our expectations for future ground leases, our expectations on future construction and development activities and lease renewals, and our plans for future financings. When used in this press release, the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The forward-looking statements are based on the current expectations of the management of Sky Harbour Group Corporation (the “Company”) as applicable and are inherently subject to uncertainties and changes in circumstances. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. For more information about risks facing the Company, see the Company’s annual report on Form 10-K for the year ended December 31, 2024 and other filings the Company makes with the SEC from time to time. The Company’s statements herein speak only as of the date hereof, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators

We use a number of metrics, including annualized revenue run rate per leased rentable square foot, to help us evaluate our business, measure our performance, identify trends affecting our business, formulate business plans, and make strategic decisions. Our key performance indicators may be calculated in a manner different than similar key performance indicators used by other issuers. These metrics are estimated operating metrics and not projections, nor actual financial results, and are not indicative of current or future performance.