Stratasys Ltd. (Nasdaq: SSYS), a Minnesota and Israel-based leader in additive manufacturing solutions, announced Wednesday it has entered into a definitive agreement to acquire MarkForged, Inc. in an all-cash transaction valued at $42.5 million, subject to customary adjustments. MarkForged is currently a wholly owned subsidiary of Nano Dimension (Nasdaq: NNDM), which will retain MarkForged’s Metal Binder Jetting product line as part of the deal structure. The transaction is expected to close in the second half of 2026, subject to regulatory approvals and customary closing conditions.

At $42.5 million for a business that generated approximately $70 million in revenue in 2025, the transaction reflects an implied revenue multiple of roughly 0.6 times trailing sales. Stratasys expects the deal to be accretive to gross margins and generate positive adjusted EBITDA contribution within the first year following close, though actual results may differ from these forward-looking projections.

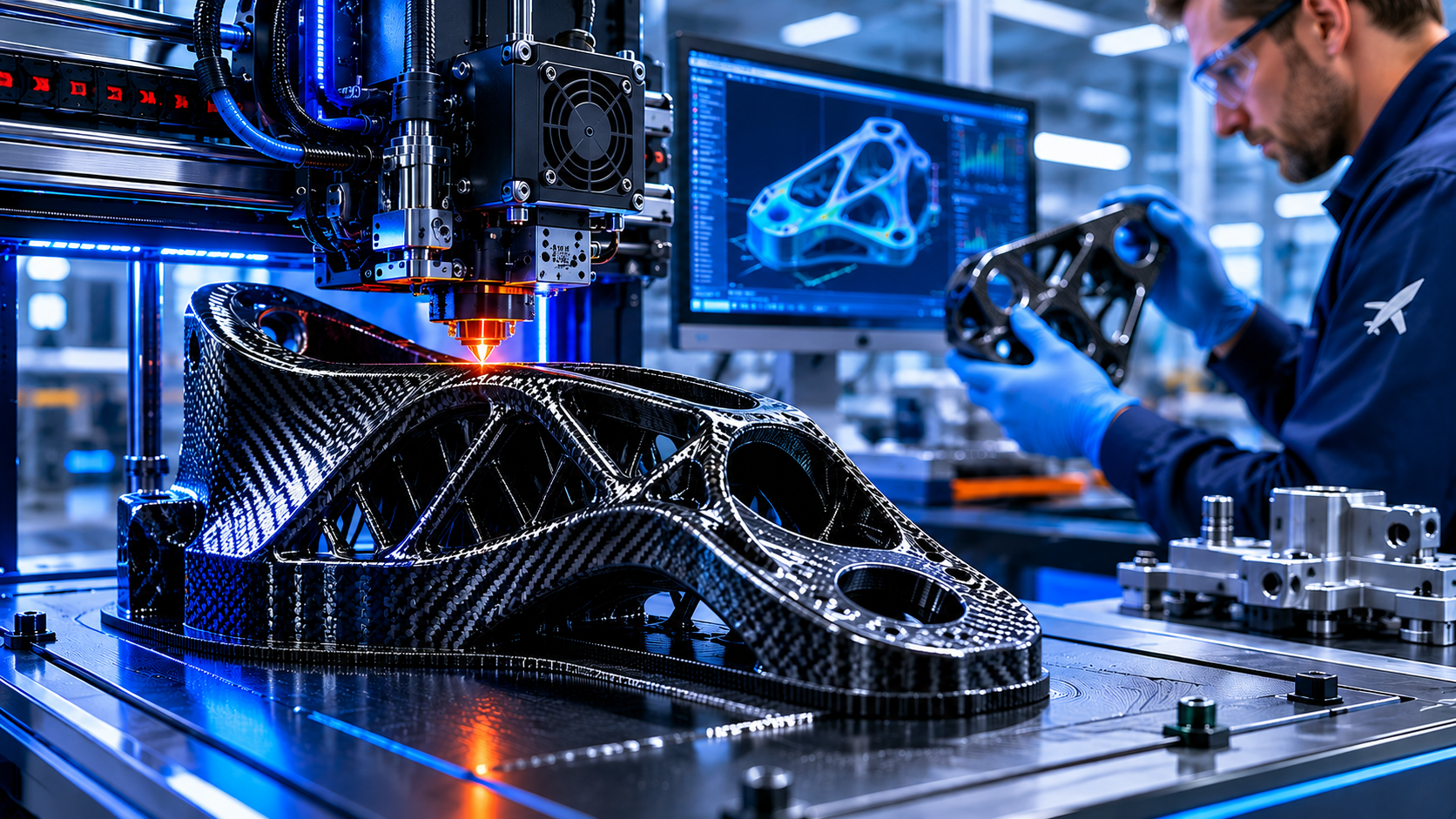

What Stratasys Is Acquiring

MarkForged built its core technology around Continuous Carbon Fiber Fused Filament Fabrication, a manufacturing approach that enables production of parts that are lighter and stronger than traditional alternatives. Its integrated platform, the Digital Forge, combines 3D printing hardware, proprietary high-performance materials, and a software ecosystem that includes simulation, part management, and automated print optimization designed with security and compliance requirements in mind.

The acquisition adds a broad portfolio of high-performance polymer and metal filaments to Stratasys’ existing materials capabilities, expanding the combined company’s addressable market across aerospace, defense, automotive, and industrial production verticals. MarkForged’s partner and reseller network is also expected to generate cross-selling opportunities across both companies’ existing customer bases.

The Industry Context

The additive manufacturing sector has been undergoing consolidation as demand for production-grade 3D printing grows in defense and aerospace applications. Government agencies including the Air Force Research Laboratory, DARPA, and the Space Force have expanded procurement of components produced through additive manufacturing for tooling, fixtures, ground support equipment, and select production parts.

Supply chain resilience has emerged as a structural driver of this demand. The ability to produce certified, production-ready components digitally on demand reduces dependence on traditional global supply chains, a priority that has gained urgency across both commercial and defense manufacturing environments since 2020. Stratasys positions this acquisition as a response to that demand shift, strengthening its capabilities in sectors where performance, reliability, and manufacturing agility are operational requirements.

Key Risks to Monitor

As with any acquisition, execution risk exists. The successful integration of MarkForged’s operations, technology, and personnel into Stratasys is not guaranteed. Stratasys is itself a small cap company operating in a competitive and evolving technology sector. The additive manufacturing market continues to face headwinds including longer-than-anticipated enterprise adoption cycles, pricing pressure from emerging competitors, and macroeconomic factors that can compress capital equipment budgets at customer organizations. The projected synergies and EBITDA accretion within the first year are forward-looking estimates and may not materialize as projected.

Stratasys has indicated it will update its financial guidance following the closing of the transaction.