Gold prices pulled back as financial markets reassessed the likelihood of another Federal Reserve rate cut in December, following a US jobs report that delivered a blend of strength and weakness. The data added another layer of uncertainty to an already murky policy outlook, prompting traders to dial back expectations for imminent easing and pressuring precious metals in the process.

The September jobs report showed stronger-than-expected hiring, signaling that parts of the labor market still retain momentum. At the same time, the unemployment rate continued drifting upward, reinforcing concerns that underlying conditions may be gradually softening. The combination of firm job creation and rising unemployment has made it harder for investors to predict how the Fed will interpret the data heading into its December 9–10 meeting.

This jobs report will be the last major labor market reading the central bank receives before making its next policy decision. With no October report released due to government delays, policymakers are entering December with limited visibility, relying heavily on data that may not fully reflect current conditions. That uncertainty has fed directly into market expectations for precious metals.

Traders had already stepped back from the idea of a December rate cut even before the employment data was released. The cancellation of the October jobs report raised doubts about whether the Fed would feel confident enough to ease further without fresh, reliable readings. After the September data, market activity briefly nudged probability forecasts slightly higher, but not enough to shift the broader view: investors still see less than a 50% chance of a cut next month.

Gold typically struggles in environments where rate cuts are uncertain. Higher interest rates lift Treasury yields and strengthen the US dollar — both of which reduce the appeal of non-yielding assets like bullion. That dynamic weighed on the metal after the jobs report, contributing to the latest pullback.

Fed officials also remain divided in their public remarks. Some members have expressed caution about further easing, citing concerns that recent inflation progress may have stalled. That has fueled additional skepticism among traders and added pressure across the precious metals complex. Broad-based losses in silver, platinum, and palladium further reflected the market’s defensive posture.

Despite the recent dip, gold remains one of the year’s strongest-performing major assets. The metal has surged more than 50% year-to-date, boosted by the Fed’s earlier rate cuts, persistent central bank demand, and strong inflows into bullion-backed ETFs. Prices hit a record high in October before moderating as policy uncertainty grew. Even with the latest volatility, gold remains firmly supported by longer-term structural drivers, including geopolitical tensions and ongoing diversification efforts among global reserve managers.

As of early afternoon in New York, gold was trading around $4,059 an ounce, while the US dollar saw modest gains. With inflation concerns stirring again and the labor market sending mixed signals, traders are preparing for a December decision that could go either way — and gold is likely to remain sensitive to every shift in the outlook.

In a landmark week for U.S.–Saudi relations, Washington has secured $1 trillion in Saudi spending commitments, dramatically expanding the scope of agreements announced just six months ago. The visit of Crown Prince Mohammed bin Salman—paired with President Donald Trump’s high-profile welcome—signaled a strategic deepening of political, economic, and defense ties between the two countries.

The new commitment, up from the previously announced $600 billion, underscores Saudi Arabia’s broad push to accelerate technological modernization, diversify its economy, and cement key alliances as global power centers shift. The Crown Prince is expected to meet with top U.S. corporate leaders, further strengthening private-sector alignment across both nations.

Nuclear Energy Becomes a Central Pillar

One of the most consequential announcements is the signing of a bilateral nuclear cooperation pact, laying the foundation for decades of collaboration in civilian nuclear infrastructure. Although progress had long stalled due to U.S. restrictions on uranium enrichment, the deal approved this week does not allow enrichment, sticking to strict nonproliferation requirements.

For Saudi Arabia, nuclear power is a cornerstone of its long-term energy transition strategy. For the U.S., the agreement secures American firms as preferred partners—locking out geopolitical competitors seeking influence in the region.

In parallel, Saudi Aramco revealed 17 new agreements with major U.S. companies, worth more than $30 billion, expanding joint ventures across refining, chemicals, and cutting-edge energy technologies.

Critical Minerals: A Geopolitical Priority

A new U.S.–Saudi critical minerals framework marks another major strategic milestone. As the U.S. works to reduce dependency on China for rare earth elements, the Saudis are emerging as a key partner in building diversified, secure supply chains.

Complementing the pact, MP Materials announced plans—backed by the U.S. Department of Defense and Saudi mining giant Maaden—to construct a rare earths refinery in the kingdom. This positions Saudi Arabia as a future hub for minerals essential to EVs, clean energy, and advanced defense technologies.

AI and Supercomputing Collaboration Expands

Artificial intelligence took center stage as the two nations signed a broad AI memorandum of understanding. The agreement grants Saudi Arabia access to U.S. AI capabilities at a scale previously unmatched.

Technology leader Nvidia confirmed that it will collaborate with Saudi Arabia to develop new supercomputing infrastructure—a critical building block for advanced AI research, autonomous systems, and next-generation digital industries.

Defense: A Major Realignment

A new strategic defense agreement reaffirms the 80-year U.S.–Saudi alliance while easing operational barriers for American defense firms. Although it falls short of a NATO-style treaty, the pact introduces new burden-sharing commitments and modernizes joint security frameworks.

Perhaps most notably, the U.S. approved future deliveries of F-35 fighter jets to Saudi Arabia—marking the first time the aircraft will be sold to a Middle Eastern nation other than Israel. Riyadh will also purchase 300 American tanks as part of a broader defense modernization push.

Trade, Finance, and Capital Markets

Additional accords strengthen cooperation on trade, capital markets technology, financial regulations, and cross-border investment standards. These agreements aim to expand U.S. exports while opening new pathways for American companies operating in global markets.

Collectively, the $1 trillion package represents one of the most sweeping and strategically significant investment commitments ever exchanged between the two countries—reshaping global alliances in energy, technology, defense, and economic policy for years to come.

SKYX is Expected to Supply 15,000 Units Including its Advanced Smart Plug & Play Technologies comprising Ceiling Lighting, Ceiling Fans, Recessed Lights, Down Lights, EXIT Signs, Emergency Lights, Indoor and Outdoor Wall Lights Among Other Advanced Smart Products

Landmark Companies are Prominent Developers with 27 Years of Experience Building Tens of Thousands of Units, Specializing in Modern Homes and Buildings with Over 3,000 Units in Development in Texas, Florida, and Colorado, Among Other Locations

SKYX and Landmark are Expected to Collaborate on Additional Upcoming Landmark Projects

SKYX’s Technologies Expansion Provides Additional Opportunities for Future Recurring Revenues Through Interchangeability, Upgrades, AI Services, Monitoring and Subscriptions, Among Others

MIAMI, Nov. 19, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced that it will supply its advanced smart plug and play technologies to a 340 unit residential development project in San Antonio, Texas. The project will include 88 townhomes and 252 apartments. The development is led by prominent developers Landmark Companies. Amenities will include swimming pools, a state-of-the-art gym, modern meeting and conference facilities, landscaped green spaces, and more.

SKYX is expected to provide over 15,000 units of its advanced and smart plug & play technologies, including ceiling lighting, recessed lights, downlights, wall lights, EXIT, and EMERGENCY lights, plug-in LED backlight mirrors among other SKYX products.

Landmark Companies are prominent developers with 27 years of experience building tens of thousands of units specializing in modern homes and buildings in Texas, Florida and Colorado, among other locations.

Julia Baytler, CEO of Landmark Companies, said; “We are excited to continue collaborating with SKYX and bring their innovative technologies into our Austin Manor project. At Landmark, our focus has always been on creating modern, high-quality living spaces that enhance the daily lives of our residents. By integrating SKYX’s advanced plug-and-play solutions, we are raising the standard of safety, convenience, and design for our communities, and we look forward to expanding this collaboration across future developments.”

Rani Kohen, Founder and Executive Chairman, of SKYX Platforms, said; “We are very happy to be working with prominent developers like Landmark Companies. We look forward to collaborating with them to enhance home values while creating safer, more advanced, and smarter buildings for the future.”

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Adobe’s latest acquisition marks one of the most significant moves yet in the evolution of how brands manage visibility, discoverability, and customer engagement in an AI-driven world. On November 19, 2025, Adobe announced a definitive agreement to acquire Semrush Holdings, Inc. in an all-cash deal valued at approximately $1.9 billion, or $12.00 per share. The acquisition unites Adobe’s expansive customer experience and content orchestration tools with Semrush’s deep capabilities in search engine optimization (SEO) and the rapidly emerging field of generative engine optimization (GEO).

Adobe has been at the forefront of enabling enterprises to reimagine their customer experience workflows through agentic AI—AI that can plan, initiate, and optimize tasks autonomously. Tools such as Adobe Experience Manager (AEM), Adobe Analytics, and the newly introduced Adobe Brand Concierge reflect the company’s commitment to helping brands create, manage, and deliver content at scale. These products support a content supply chain that aligns with the needs of enterprises navigating new customer interfaces powered by large language models (LLMs).

Semrush’s inclusion strengthens Adobe’s position dramatically. As brands increasingly confront the challenge of remaining visible across traditional search engines and emerging AI-driven discovery channels, Semrush provides a powerful layer of intelligence and optimization. The company is widely known for its decade-long leadership in SEO analytics and has recently become a leading force in GEO—an emerging discipline focused on helping brands remain discoverable within AI-powered platforms, from LLMs to generative search engines.

The acquisition comes at a time when consumer behavior is rapidly shifting. With more customers receiving answers, recommendations, and purchase guidance from platforms like ChatGPT and Google Gemini, brand visibility is no longer confined to search engine rankings or owned channels. It now includes how a brand appears within LLM outputs, conversational AI systems, and algorithm-driven summaries. Organizations that fail to adapt to these dynamics risk losing relevance across key digital touchpoints.

Semrush brings enterprise-grade capabilities and impressive momentum to Adobe’s ecosystem. Its generative marketing tools are already being used by major brands, and the company recently reported 33% year-over-year Annual Recurring Revenue growth in its enterprise segment. This traction reflects a growing need among marketers who now rely on SEO and GEO teams to drive visibility strategies in generative environments.

Together, Adobe and Semrush will offer marketers a unified solution that spans the entire spectrum of brand exposure—owned websites, search engines, LLM responses, and the broader web. By integrating Semrush’s data intelligence into Adobe’s customer experience tools, the combined platform is designed to give organizations a holistic, real-time understanding of how their brand appears and performs across both traditional and AI-driven discovery channels.

This acquisition positions Adobe to become a central player in helping enterprises navigate the next phase of AI-enabled marketing. As AI continues reshaping how consumers gather information, evaluate options, and make buying decisions, Adobe’s expanded ecosystem aims to ensure that brands remain both discoverable and competitive in an increasingly complex digital landscape.

Bitcoin’s recent sharp downturn has become one of the most talked-about developments in global markets, not only because of the scale of the decline but because of how dramatically it diverges from the performance of nearly every major asset class. While the world’s largest cryptocurrency has fallen close to 30% from its highs, traditional investments such as gold, long-term Treasuries, and several equity sectors have moved in the opposite direction, highlighting a shift in risk appetite that is challenging assumptions about Bitcoin’s role within a diversified portfolio.

Gold has been one of the clearest contrasts. For years, Bitcoin supporters positioned the asset as “digital gold,” a modern alternative that could offer the same inflation-hedging and store-of-value qualities while delivering far stronger growth potential. Yet 2025 has told a different story. As Bitcoin has weakened, gold has steadily climbed, supported by falling interest rates, macroeconomic caution, and investors reverting to the familiarity of a centuries-old safe haven. Instead of moving in tandem, the two assets have decoupled, with gold benefiting from fear while Bitcoin has absorbed the pressure of risk-off sentiment.

Bonds have also outperformed Bitcoin, despite being viewed as some of the most conservative instruments available. With global central banks shifting toward lower rates and expectations for slower economic growth building, long-term Treasuries have enjoyed a meaningful rally. These gains have been especially striking when compared with Bitcoin, which has struggled to attract inflows in an environment where investors are prioritizing stability over high-volatility assets. The comparison underscores how Bitcoin’s risk profile still aligns more with speculative tech than with defensive or income-generating investments.

Tech stocks offer another dimension to the divergence. Despite pockets of volatility tied to earnings and shifting valuations, many tech names—especially large-cap leaders—have held up better than Bitcoin. Lower rates have helped the sector maintain some resilience, and tech remains a favored destination for investors seeking long-term growth. Bitcoin, however, has not benefited from the same support, partly due to the lingering psychological effects of October’s steep liquidation event, where billions in leveraged crypto positions were wiped out in a matter of hours.

Even sectors traditionally considered slow or predictable have outpaced Bitcoin. Utilities, often ignored during high-growth periods, have returned to favor as investors shift toward assets offering stability and lower correlation with market swings. Their ability to outperform Bitcoin reinforces the degree to which risk sentiment has changed during the year. Emerging market equities have also benefited from global rate moves and a refreshed appetite for select developing economies, adding another category that has outperformed the cryptocurrency.

This multi-asset comparison paints a clear picture: Bitcoin is still functioning as a high-beta asset closely tied to speculative momentum rather than acting as a hedge or a defensive anchor. When markets favor safety, income, or measured growth, gold, bonds, and stable equity sectors take the lead. When markets are optimistic and liquidity is abundant, Bitcoin tends to outperform. In 2025, the tide has shifted toward caution, and Bitcoin’s performance reflects that shift more starkly than ever.

Although the longer-term narrative for Bitcoin remains intact for many investors, the current landscape shows that the cryptocurrency continues to behave as a risk-sensitive asset rather than a universal hedge. As the year progresses, Bitcoin’s next major move will likely depend on whether global markets transition back toward risk-on sentiment or continue rewarding defensive positioning across traditional asset classes.

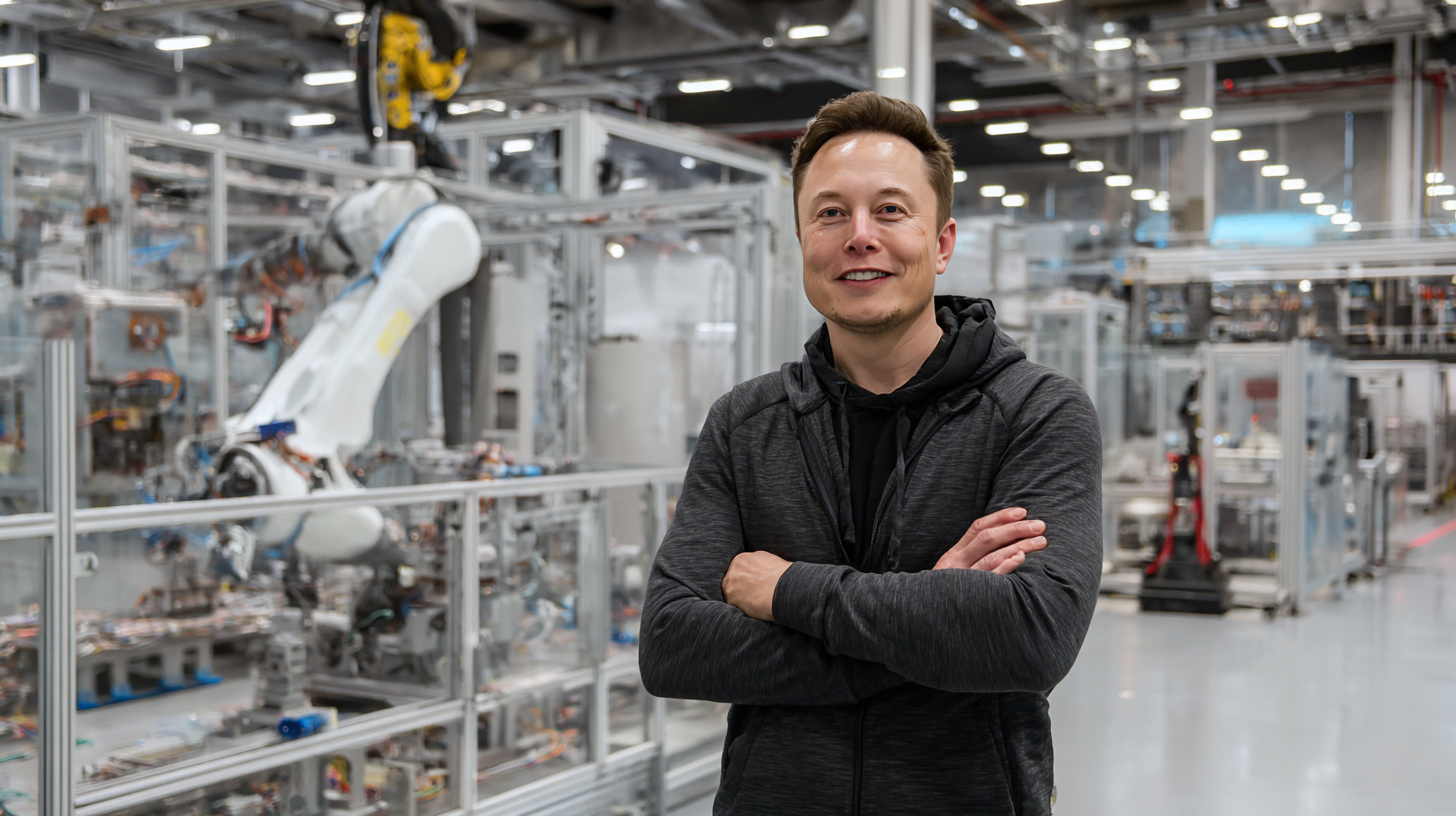

Tesla shares recovered on Friday after an early slide, signaling some stabilization in a tech sector that has been under stress for several days. The stock opened lower as markets continued reacting to Thursday’s broad sell-off, but sentiment gradually improved as investors returned to growth names. Despite the bounce, Tesla remains roughly 9 percent lower since CEO Elon Musk secured his record-setting $1 trillion compensation package, a milestone that has introduced additional volatility into an already sensitive market.

For the week, Tesla is still on track for a significant decline, trading about 7 percent lower as of Friday morning. The stock also dropped below a key technical support level at $400 earlier in the week before finding some footing. Thursday’s downturn marked Tesla’s weakest price since September, driven largely by shifting expectations around Federal Reserve policy. With odds of a December rate cut fading, investors have been reassessing their exposure to high-valuation technology stocks, creating pressure on both mega-cap growth names and companies tied to the accelerating artificial intelligence cycle.

Concerns about the pace and sustainability of AI spending have also contributed to a rotation into sectors viewed as more reasonably priced. Still, long-term Tesla supporters remain focused on the company’s innovation roadmap, pointing to autonomous driving, robotics, and next-generation AI systems as core drivers of future value. This outlook is being reinforced by new analyst projections that indicate Tesla may be approaching major milestones in key technology programs.

One of the most closely watched developments is Tesla’s effort to advance its Robotaxi initiative. Analysts expect the company to proceed with removing human safety drivers from its autonomous trials in Texas and at least one additional state. If executed, this would represent a pivotal step toward launching commercial autonomous mobility services. Tesla has also highlighted several cities—including Miami, Dallas, Phoenix, and Las Vegas—as upcoming expansion zones for Robotaxi testing, suggesting broader deployment is on the horizon.

Tesla’s deepening relationship with xAI, Musk’s artificial intelligence company, is another major area fueling investor interest. Industry observers anticipate Tesla will integrate xAI’s computational capabilities to accelerate Optimus, its humanoid robot platform. This collaboration could significantly enhance Optimus’s learning speed, coordination, and operational reliability, strengthening Tesla’s position in the rapidly emerging robotics sector.

The company has outlined ambitious production plans for Optimus, beginning with a target of manufacturing one million units at its Fremont facility, followed by a long-term expansion to a ten-million-unit line at Giga Texas. Optimus is currently in pilot production, and investors are closely watching for signs that Tesla can scale the platform to commercial volume. Many believe humanoid robots could eventually become one of Tesla’s largest business lines, potentially surpassing automotive revenue in the long run.

Although recent market volatility has pressured the stock, several analysts remain constructive on Tesla’s long-term outlook, citing its advancements in AI, robotics, and autonomous transportation as foundational pillars for future growth. Investors are now closely monitoring technology updates, regulatory progress, and production milestones to evaluate how quickly these innovations can begin contributing meaningful earnings.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 below estimates. Sky Harbour reported Q3 revenue of $7.3 million (+78% Y/Y) trailing our estimate of $9.3 million. An adj. EBITDA loss of $2.3 million was below our forecast of a $0.2 million gain, illustrated in Figure #1 Q3 Results. Management noted that the company is within $1 million of a cash break-even run-rate and expects to achieve positive operating cash flow before year-end.

Site acquisition on target. Sky Harbour now holds 19 airport ground leases (nine operating, ten in development) and remains on pace to reach 23 by year-end. The company announced a site acquisition at Long Beach Airport, while pre-leasing at Dulles and Bradley supports pricing power and visibility into 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Another Sale. Yesterday, V2X announced the sale of 2.25 million shares of its common stock on an underwritten basis by Vertex Aerospace Holdco LLC. V2X is not selling any shares of common stock in the offering, and V2X will not receive any proceeds from the offering by Vertex Aerospace. The offering is expected to close on or about November 13, 2025, subject to customary closing conditions. The sale is another in a series as Vertex Aerospace continues to liquidate its V2X holding acquired in the merger between Vectrus and Vertex.

V2X To Participate. Under its existing share repurchase authorization, V2X has agreed to purchase 363,638 shares of common stock that are subject to the offering at a price per share of common stock equal to the price to be paid to Vertex Aerospace by the underwriter. V2X intends to fund the repurchase of its common stock with cash on hand. At the current price, the 363,638 shares would cost approximately $20 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q25 Reported With OLC Update. Unicycive reported a 3Q25 loss of $6.0 million or $(0.33) per share, below our expectations of $(8.4) million. Importantly, the company confirmed previous plans to resubmit its NDA for OLC (oxylanthanum citrate) by the end of the year, implying a new PDUFA date during 1H26. Cash at the end of the quarter was $42.7 million.

OLC Resubmission Planned Before Year-End. Unicycive previously announced that it held a meeting with the FDA to discuss the issue with a third-party manufacturer cited as a deficiency in the Complete Response Letter (CRL) received in June 2025. After the FDA meeting and an inspection of the third-party manufacturer by EU regulators, the company plans to resubmit the NDA. Assuming a PDUFA (Prescription Drug User Fee Act) review time of 6 months, an answer could be received during 1H26.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 results. The company reported Q3 revenue of $13.8 million and an adj. EBITDA loss of $9.6 million, both of which were lower than our estimates of $22.0 million and a loss of $2.0 million, respectively. The weaker than expected results were largely attributed to moderately higher than expected operating expenses and a $10.9 million increase in deferred revenue, which currently has a balance of $36.4 million. Notably, while revenue and adj. EBITDA were softer than anticipated, bookings increased a solid 9.3%, y-o-y, to $17.6 million.

Favorable release roadmap. The company has a busy release roadmap in Q4 and 2026. Notably, in Q4, the company plans to release the ARK: Survival Ascended (ASA) Lost Colony DLC, which is expected to unlock $5.8 million in deferred revenue. Looking ahead to 2026, the release roadmap includes Honeycomb, Bellwright on PlayStation and Xbox, and two DLCs for ASA, Genesis Part 1 and Part 2, which are tied to $10.3 million in deferred revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 on target. SKYX reported Q3 revenue of $23.9 million versus our estimate of $23.5 million and an adj. EBITDA loss of $2.3 million versus our forecasted loss of $2.1 million. Revenue rose 4% over Q2, while gross margin improved to 32% from 30% in Q2, reflecting an increased mix of higher-margin proprietary products.

B2B pipeline building. SKYX’s new partnership with Global Ventures Group expands its footprint into the Middle East, including projects in Saudi Arabia and Egypt. Alongside Landmark Companies, Forte Developments, Cavco Homes, and the Miami Smart City, these relationships reinforce multi-year B2B growth potential as deployments scale through 2026 and beyond.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third-quarter 2025 results. InPlay reported third-quarter results, with production averaging 18,970 barrels of oil equivalent per day (boe/d), up 7% from Q2 and 131% higher than Q3 2024. This was above our forecast of 18,695 boe/d, due to continued outperformance of wells drilled in the first quarter of 2025 and low decline base production. Revenue totaled C$79.3 million, below our forecast of C$86.8 million due to lower natural gas pricing. Adjusted funds flow (AFF) came in at C$26.8 million, or C$0.96 per share, modestly below our C$28.0 million, or $1.00 per share estimate, mainly due to the variance in revenue.

Market outlook. We think 2026 will offer a more favorable environment for InPlay. It will mark the first full year of results post-Pembina acquisition, unlocking the benefits of greater scale, infrastructure control, and an expanded drilling inventory. While near-term pricing remains soft, we expect stronger demand, slower supply growth, and potential for tighter oil and gas markets to support improved realizations and higher netbacks through 2026. With enhanced gas processing capacity and capital flexibility, InPlay remains well-positioned to capitalize on an improving macro backdrop.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overachieves fiscal first quarter. Total revenues increased a solid 10.9% to $253.9 million, better than our $244.0 million estimate, bolstered by a 59% increase in movie sales. In addition, adj. EBITDA of $12.2 million, up roughly 260% y-o-y, was better than our $9.5 million estimate, reflecting a 330 basis point improvement in margins. Figure #1 Q3 Results highlights our estimates and the recent results.

Strong movie sales likely to continue. Movie sales revenues increased 59% to $84.0 million, well above our $74.9 million estimate, a reflection of a recent licensing agreement with Paramount Pictures, and, to a smaller extent, strong Steelbook sales. The Paramount Pictures licensing revenue lift is likely to bolster total company revenues for the next few quarters.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.