Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

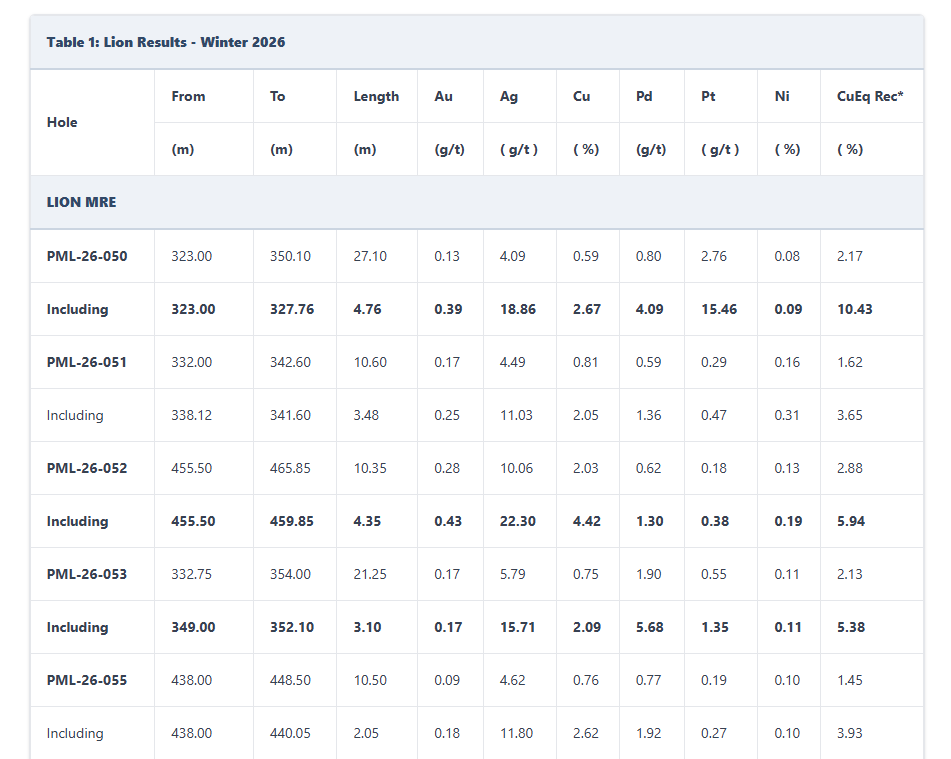

Continued drilling success in the Lion Zone. Recent Winter 2026 drill results further defined the high-grade Lion Zone ahead of a planned 2026 Mineral Resource Estimate (MRE) for the Nisk project that will incorporate Lion Zone mineralization. Infill drilling confirmed continuity of mineralization, highlighted by notable intercepts, including 4.76 meters grading 10.43% copper equivalent (CuEq) and 4.35 meters at 5.94% CuEq, along with broad intervals including 27.1 meters at 2.17% CuEq. These results reinforce confidence in the geological model and support potential resources in the Indicated category.

Near-surface drilling reinforces development potential. Shallow drilling continues to demonstrate strong near-surface mineralization that may be suitable for open-pit extraction, enhancing the project’s development potential. Additional noteworthy results, including 3.10 meters at 5.38% CuEq, further validate the presence of consistent high-grade zones that could underpin future economic studies, including a preliminary economic assessment (PEA).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VANCOUVER, BC, April 14, 2026 – Nicola Mining Inc. (the “Company” or “Nicola”) (NASDAQ: NICM) (TSX.V: NIM) (FSE: HLIA) is pleased to announce the closing of its underwritten public offering in the United States (the “Offering”). The Offering consisted of 930,233 American Depositary Shares (“ADSs”) and warrants to purchase 930,233 ADSs at an offering price of US$6.45 per ADS and accompanying warrant. Each ADS offered represents 12 common shares of Nicola. The gross proceeds, before deducting underwriter discounts, and commissions and offering expenses, were US$6.0 million. The warrants have an exercise price of CAD$12.2213 per ADS, are exercisable immediately upon issuance and will expire on the fifth anniversary of the original issuance date. The ADSs began trading on the Nasdaq Capital Market under the ticker symbol “NICM” on April 14, 2026 and the warrants are not listed for trading.

In addition, Nicola granted the underwriters a 45-day option to purchase up to an additional 139,534 ADSs and/or up to an additional 139,534 warrants to purchase up to 139,534 ADSs, which was partially exercised to purchase 139,534 warrants.

The Company intends to use the net proceeds from the Offering for mill expansion, property, plant and equipment expenditures and general and administrative and working capital.

Maxim Group LLC acted as sole book-running manager for the Offering.

The Offering was made pursuant to an effective shelf registration statement on Form F-10 (File No. 333-293048) previously filed with the U.S. Securities and Exchange Commission (the “SEC”) and became effective on January 29, 2026. Nicola may offer and sell securities in both the United States and other jurisdictions outside of Canada. No securities were offered or sold to Canadian purchasers under the Offering. A final prospectus supplement and accompanying prospectus relating to the Offering and describing the terms thereof was filed with the SEC and forms a part of the effective registration statement and is available on the SEC’s website at www.sec.gov. Copies of the final prospectus supplement and accompanying prospectus may be obtained by contacting Maxim Group LLC, at 300 Park Avenue, 16th Floor, New York, NY 10022, Attention: Syndicate Department, or by telephone at (212) 895-3745 or by email at [email protected]. The final prospectus supplement is available for free on the SEC’s website at www.sec.gov and is also available on the Company’s profile on the SEDAR+ website at www.sedarplus.ca.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the Nasdaq Capital Market, TSX Venture Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high-grade BC-based gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a property that hosts historical high-grade copper mineralization and covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

This news release contains “forward-looking statements” within the meaning of applicable securities laws. All statements, other than statements of present or historical facts, are forward-looking statements. Forward-looking statements in this news release include, but are not limited to, statements relating to the expected use of proceeds of the Offering.

Forward-looking statements are based upon certain assumptions and other key factors that, if untrue, could cause actual results to be materially different from future results expressed or implied by such statements. Key assumptions upon which the Company’s forward-looking information is based include, without limitation, that required regulatory approvals and authorizations (including approvals, if any, of applicable stock exchanges and securities regulatory authorities) will be obtained in a timely manner; that the depositary and other service providers will be able to perform as contemplated; that there will be no material adverse change in the Company’s business, financial condition or prospects; and that the Company will be able to use the net proceeds of the Offering substantially as described.

Forward-looking statements involve known and unknown risks, uncertainties, and assumptions and accordingly, actual results could differ materially from those expressed or implied in such statements. Such risks and uncertainties include, without limitation: the risk that the Company may be unable to satisfy applicable regulatory requirements; and the risk that the Company’s planned use of proceeds may change due to operational requirements, business opportunities or other factors. Investors are cautioned not to place undue reliance on forward-looking statements.

There can be no assurance that forward-looking statements will prove to be accurate, and even if events or results described in the forward-looking statements are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, Nicola. Investors are cautioned against attributing undue certainty to forward-looking statements.

THE FORWARD-LOOKING INFORMATION CONTAINED IN THIS PRESS RELEASE REPRESENTS THE EXPECTATIONS OF NICOLA AS OF THE DATE OF THIS PRESS RELEASE AND, ACCORDINGLY, IS SUBJECT TO CHANGE AFTER SUCH DATE. READERS SHOULD NOT PLACE UNDUE IMPORTANCE ON FORWARD- LOOKING INFORMATION AND SHOULD NOT RELY UPON THIS INFORMATION AS OF ANY OTHER DATE. WHILE NICOLA MAY ELECT TO, IT DOES NOT UNDERTAKE TO UPDATE THIS INFORMATION AT ANY PARTICULAR TIME, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE, EXCEPT AS REQUIRED IN ACCORDANCE WITH APPLICABLE LAWS.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

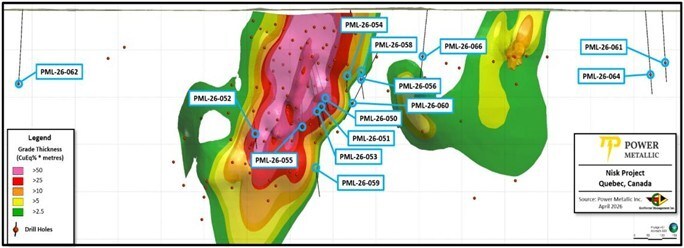

TORONTO, April 15, 2026 / PRNewswire / – Power Metallic Mines Inc. (the “Company” or “Power Metallic”) (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt: IVV1) is pleased to provide a release of assays from its Winter 2026 drill campaign.

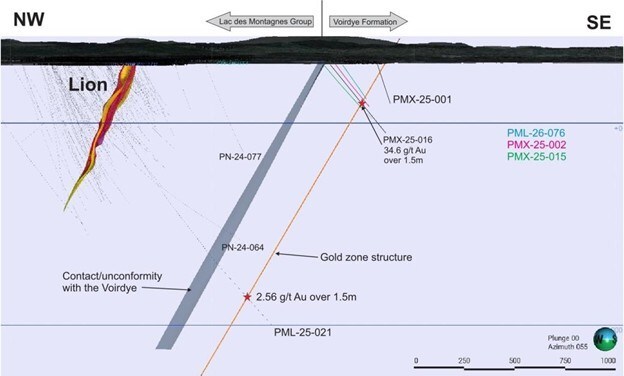

Lion MRE In-fill program Drilling continued to define the high-grade Lion Zone in preparation for a 2026 Mineral Resource Estimate (MRE). The majority of infill drill holes in this release are for holes that are mostly defining the eastern side of the Lion zone (Figure 1) for future mineral resource estimates to an Indicated Resource classification. The 2026 winter drill campaign continues to support the modelled interpretation of the Lion Zone based on earlier wider spaced drilling and includes PML-26-050 intersected the Lion Zone and confirmed the eastern edge of the high-grade copper shoot with 4.76m @ 10.43% CuEqRec1 (Table 1).

Hole PML-26-052 tested the eastern edge of the western high-grade shoot 4.35m @ 5.94% CuEqRec1) and confirmed the expected mineralization modeled from the wider spaced earlier drilling in this area.

Figure 1 – Lion Drill holes reported in this news release (CNW Group/Power Metallic Mines Inc.)

Note: Reported length is downhole distance; true width based on model projections is estimated as 85% of downhole length

1Copper Equivalent Rec Calculation (CuEqRec1) CuEqRec represents CuEq calculated based on the following metal prices (USD) : 2,360.15 $/oz Au, 27.98 $/oz Ag, 1,215.00 $/oz Pd, 1000.00 $/oz Pt, 4.00 $/lb Cu, 10.00 $/lb Ni and 22.50 $/lb Co., and recovered grades based on recent locked-cycle metallurgical recoveries by SGS Canada Inc (see press release Jan 21, 2006).

Current MRE drilling has concentrated on the Lion zone near surface that may be amenable to early open pit extraction in a possible future mining operation. This drilling continues to intersect strong copper sulphide mineralization (Figures 2 and 3).

Exploratory Drilling – East and West of Lion Drill holes PML-26-056, 058, 059 and 060 were designed to define the eastern edge of the Lion Zone, which is interpreted as possibly being fault controlled. All these holes (Figure 1) encountered low grade mineralization, Cu (up to 0.22%), Au (up to 0.20 g/t Au), Pd (up to 0.60 g/t Pd), and Pt (0.21 g/t Pt) and effectively define the eastern boundary of the Lion Zone.

Holes PML-26-060 and 064 were drilled 400-450 meters west of the Tiger Zone (Figure 1) and failed to intersect any sulphide mineralization or the ultramafic unit that occurs at Lion.

Hole PML-26-066 was designed to test above an interpreted arm of the Tiger Zone. The hole collared in mineralization (0.27% Cu, 0.17 g/t Pd) at the overburden bedrock contact before intersecting 2 wide ultramafic units of the type found at Lion. Between these two units 1.31m @ 32.9 g/t Ag was intersected. It is unknown how this may relate to the Tiger mineralization down dip of this intersection. When ground conditions permit, testing behind the initial Cu, Pb mineralization will be done.

Hole PML-26-062 was drilled 800m to the west of Lion. Although the favourable ultramafic unit was encountered over a wide intersection, no significant mineralization was encountered.

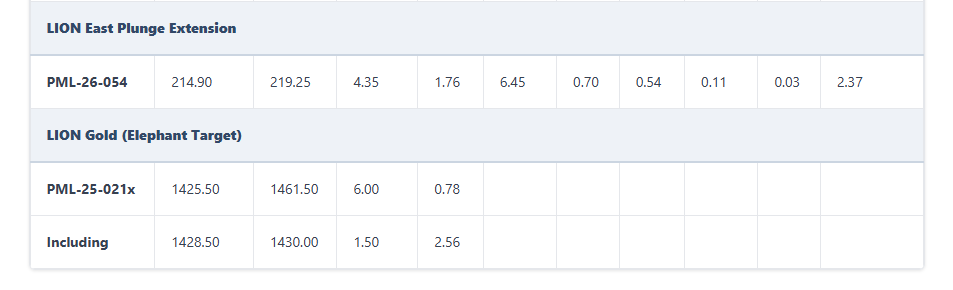

Exploratory Drilling – Elephant Target Hole PML-25-021 was extended (PML-25-021x) to test a large BHEM anomaly detected in PN-24-064. Hole PML-25-021x failed to explain the BHEM anomaly, and work is continuing to refine this target area for further drilling.

PML-25-021x entered the paragneiss formation that define the footwall of Power Metallic’s Nisk Ni-Cu-Pd deposit to the west of Lion. This formation was intersected more than a kilometer below surface and contained recognizable favourable geological units (Figure 4) that had hosted a high-grade gold intersection in PMX-25-016 (1.5m @ 34.6 g/t). Assay results from PML-25-021x returned 6m @ 0.78 g/t Au, including 1.5m @ 2.56 g/t Au. Although low grade, this intersection establishes a large sized area of gold structure. Associated with wide anomalous Au, As and W, summer surface mapping, prospecting and re-interpretation of geophysics will be done to localize this recognizable unit and determine whether this gold target requires more drill follow-up.

Figure 4 – Lion Drill hole PML-25-021x intersecting the gold zone discovered in PMX-25-016 (CNW Group/Power Metallic Mines Inc.)

“Lion MRE drilling continues to deliver as or better than expected. The shallow hole success, which we expect assays to confirm what we are seeing in the cores, should be very supportive to the starter open pit. This all will support the upcoming MRE and PEA. On the exploration side the drill bit continues to give us clues and points us to more structures to test. We have 37 holes in for assay and we’re drilling our last few holes of the winter campaign. The team remains very bullish on our discovery process”, commented Terry Lynch, CEO & Director.

Qualified Person

Joseph Campbell, P. Geo, VP Exploration at Power Metallic, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Metallic Mines Inc.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)—a high–grade Copper–PGE, Nickel, gold and silver system—toward Canada’s next polymetallic mine.

On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~330 km² and roughly 50 km of prospective basin margins.

Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs.

Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025.

It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s Jabal Said Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

For further information, readers are encouraged to contact: Power Metallic Mines Inc. The Canadian Venture Building 82 Richmond St East, Suite 202 Toronto, ON

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

QAQC and Sampling

GeoVector Management Inc (“GeoVector”) is the Consulting company retained to perform the actual drilling program, which includes core logging and sampling of the drill core.

All core in this news release is NQ sized core. Drill core is re-fitted and measured. Geotech on core includes photographs (wet & dry), rock quality index, magnetic susceptibility, conductivity, and recovery estimates. Core is logged for lithology, mineralogy, and structural features, and sample intervals are delineated and tagged.

Sampled core is mechanically sawn, and half-core is retained for future reference. GeoVector’s QAQC program includes regular insertion of CRM standards, duplicates, and blanks into the sample stream with a stringent review of all results. QAQC and data validation was performed, and no material errors were observed.

All samples were submitted to and analyzed at Activation Laboratories Ltd (“Actlabs”), a commercial laboratory independent of Power Metallic with no interest in the Project. Actlabs is an ISO 9001 and 17025 certified and accredited laboratories. Samples submitted through Actlabs are run through standard preparation methods and analysed using RX-1 (Dry, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 μm) preparation methods, and using 1F2 (ICP-OES) and 1C-OES – 4-Acid near total digestion + Gold-Platinum-Palladium analysis and 8-Peroxide ICP-OES, for regular and over detection limit analysis. Pegmatite samples are analyzed using UT7 – Li up to 5%, Rb up to 2% method. Actlabs also undertake their own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibration.

This message contains certain statements that may be deemed “forward-looking statements” concerning the Company within the meaning of applicable securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential,” “indicates,” “opportunity,” “possible” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, are subject to risks and uncertainties, and actual results or realities may differ materially from those in the forward-looking statements. Such material risks and uncertainties include, but are not limited to, among others; the timing for various drilling plans; the ability to raise sufficient capital to fund its obligations under its property agreements going forward and conduct drilling and exploration; to maintain its mineral tenures and concessions in good standing; to explore and develop its projects; changes in economic conditions or financial markets; the inherent hazards associates with mineral exploration and mining operations; future prices of nickel and other metals; changes in general economic conditions; accuracy of mineral resource and reserve estimates; the potential for new discoveries; the ability of the Company to obtain the necessary permits and consents required to explore, drill and develop the projects and if accepted, to obtain such licenses and approvals in a timely fashion relative to the Company’s plans and business objectives for the applicable project; the general ability of the Company to monetize its mineral resources; and changes in environmental and other laws or regulations that could have an impact on the Company’s operations, compliance with environmental laws and regulations, dependence on key management personnel and general competition in the mining industry.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Advancing financing efforts with international support. First Phosphate has secured a letter of interest (LOI) from the Export and Investment Fund of Denmark (EIFO) for up to €170 million to support equipment and service purchases for its Begin-Lamarche igneous phosphate project in Saguenay–Lac-Saint-Jean, Quebec. EIFO, owned and backed by the Danish government and effectively AAA-rated, would provide a guarantee to participating banks, with its involvement expected to be pro rata and pari passu alongside other senior lenders.

Global experience in export and project finance. EIFO brings extensive global experience in export and project finance, having supported numerous international transactions. The proposed guarantee remains subject to EIFO’s internal credit approvals and completion of project due diligence. The LOI is non-binding pending finalization of borrower, guarantor, and security arrangements, and will be governed by Danish law.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saguenay, Québec–(Newsfile Corp. – April 13, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce that it has finalized a letter of Intent (“LOI”) from the Danish Export Credit Agency (“EIFO”) for up to EUR 170 Million in equipment and services purchases for its igneous phosphate mine project in Saguenay-Lac-St-Jean, Quebec, Canada.

EIFO is backed by the Danish state, and as such, the EIFO guarantee can be considered AAA rated. The guarantee is provided to one or more banks providing the funding and EIFO participation can be expected to be pro rata and pari passu with other senior lenders.

“We look forward to continuing to work with First Phosphate and the other parties involved in this transaction,” says Jens Hestbech, Director of EIFO. “We can assure First Phosphate that we will work with a constructive approach towards the project, in order to reach a successful result.”

EIFO has been involved in the financing of a significant number of transactions and projects around the world and has extensive experience within the field of export and project finance.

Issuance of an EIFO guarantee is subject to EIFO internal credit approval, satisfactory documentation as well as satisfactory completion of normal and customary project due diligence, including but not limited to environmental and social matters. The LOI remains non-binding until the exact borrower/guarantor and security arrangements are established and is subject to Danish law and Danish jurisdiction.

About First Phosphate Corp

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay-Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

Forward-Looking Information and Cautionary Statements

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, this press release contains forward-looking information relating to, among other things: the Company’s ability to meet EIFO review and approval requirements, the engagement of participating banks, and onshoring a vertically integrated mine-to-market LFP battery supply chain for North America. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things, assumptions regarding general business and economic conditions; there being no significant disruptions affecting the activities of the Company or inability to access required project inputs; permitting and development of the projects being consistent with the Company’s expectations; the accuracy of the current mineral resource estimates for the Company and results of metallurgical testing; certain price assumptions for P2O5 and Fe2O3; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the Company’s relationship with First Nations and other Indigenous parties remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

Toronto, Ontario–(Newsfile Corp. – April 13, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) announces that it has elected to rely on Coordinated Blanket Order 51-933 – Exemptions to Permit Semi-Annual Reporting for Certain Venture Issuers (the “Order“) and move to semi-annual financial reporting (“SAR“).

The Order allows eligible venture issuers listed on the TSX Venture Exchange (the “TSXV“) to voluntarily move from a quarterly to a semi-annual financial reporting framework. The Company’s fiscal year ends on December 31. Under the SAR pilot program, the Company will be exempt from filing interim financial reports and related Management’s Discussion & Analysis (MD&A) for its first and third quarters.

Interim Period: The Company will not file an interim report for the first quarter (Q1) ending March 31 and the third quarter (Q3) ending September 30; and

Ongoing Reporting: The Company will continue to file audited financial statements (due within 120 days of December 31) and six-month interim financial reports (due within 60 days of June 30).

The Company confirms it meets the pilot program’s eligibility criteria, which include being a venture issuer with annual revenues of less than $10 million, having a disclosure record of over 12 months and having filed all required periodic and timely continuous disclosure documents.

The first period for which the Company will not file an interim financial report and related MD&A will be for the three-month period ended March 31, 2026.

This news release is being filed pursuant to Coordinated Blanket Order 51-933 Exemptions to Permit Semi-Annual Reporting for Certain Venture Issuers.

In addition, the Company announces that, further to the Company’s press release dated January 29, 2026, pursuant to which the Company announced a $750,000 loan (the “Loan“) from Dr. Keith Barron, CEO of the Company, the Company and Dr. Barron have agreed to amend the Loan to increase the amount of the Loan to C$1,000,000 to be advanced from time to time in principal amounts as agreed by the parties. All other terms of the Loan, as previously announced, remain the same.

Dr. Keith Barron is a related party of the Company by virtue of the fact that he is the Chairman, the President and Chief Executive Officer, a promoter and a principal shareholder of the Company, and as a result, each advance and repayment under the Loan constitutes a “Related Party Transaction” for the purposes of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101“). The Company is relying upon an exemption from the formal valuation and minority shareholder approval requirements under MI 61-101 in respect of the Related Party Transactions, in reliance on Sections 5.5(a) and 5.7(1) of MI 61-101, respectively, as the fair market value of the Related Party Transaction, collectively, does not exceed 25% of the Company’s market capitalization, as determined in accordance with MI 61-101. The Company did not file a material change report related to the Loan more than 21 days before the expected closing of the Loan as required by MI 61-101, as the Company wished to organize the Loan on an expedited basis for sound business reasons. The amendment to the Loan was approved by the members of the board of directors of the Company who are independent for purposes of the related party transaction, being all directors other than Dr. Barron. No special committee was established in connection with the amendment to the Loan, and no materially contrary view or abstention was expressed or made by any director of the Company in relation thereto.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes Aurania’s objectives, goals, future plans or other statements of intent, Aurania’s ongoing engagement in the identification, evaluation, acquisition and exploration of mineral property interests, and any potential exploration results or potential mineralization resulting therefrom, Aurania’s ongoing exploration efforts in France, Italy, Ecuador and abroad, potential additional advances pursuant to the Loan, eventual repayment of the Loan or any part thereof by Aurania, and the use by Aurania of funds received pursuant to the Loan. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that, there will be no material adverse change in metal prices and all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things, the state of the capital markets generally and of the mining markets more particularly, any commodity prices supply chain disruptions, restrictions on labour and workplace attendance and local and international travel due to war, weather, pandemics or otherwise; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed, including pursuant to the Loan; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals, copper and critical minerals; and those risks set out in the Company’s public documents filed on SEDAR+. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fast-41 Designation. Resolution Minerals Ltd (OTCQB: RLMLF, ASX: RML) is advancing its Antimony Ridge Project in Idaho as a strategically significant source of antimony within the United States, reinforced by its recent inclusion in the Federal FAST 41 Permitting Transparency Program. This designation underscores the project’s importance to national security and critical mineral supply chains while supporting accelerated permitting, enhanced regulatory coordination, and increased visibility with investors and strategic partners.

Large-Scale Potential. The project demonstrates strong large-scale potential, with recent modeling defining an extensive and expanding mineralized system hosting high grade antimony and silver across a substantial footprint. Historical production and recent sampling confirm exceptionally high grades, while mineralization remains open in multiple directions, indicating considerable upside and resource growth potential.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

While Wall Street fixates on gold, lithium, and rare earth elements, a lesser-known critical mineral is quietly becoming one of the most strategically important materials in the world — and a growing opportunity in the small and microcap space. The mineral is antimony, and the race to secure domestic supply is accelerating fast.

Antimony sits at the intersection of defense, energy, and advanced technology. It hardens ammunition and military alloys, serves as a key component in flame-retardant materials protecting electronics and aircraft wiring, and plays a critical role in semiconductors, infrared sensors, and night-vision systems. The U.S. Department of Defense has identified it as one of the most critical minerals in its supply chain — and for good reason. Without antimony, a significant portion of America’s weapons systems simply don’t function.

The problem is stark. The United States has not mined antimony domestically since the early 1990s. China controls roughly 60% of global production and has enacted increasingly aggressive export restrictions, including an outright ban on shipments to the U.S. in late 2024. A Govini supply chain analysis found that more than 80,000 individual weapons parts across nearly 1,900 DoD weapon systems incorporate antimony or related critical minerals. That is not a supply chain vulnerability — that is a national security exposure.

Washington has responded with urgency. The Department of Defense has deployed nearly $400 million in investments and stockpile contracts around domestic antimony production, the most concentrated federal mobilization around a single critical mineral in recent memory. Earlier this year, the DoD disbursed $27 million under the Defense Production Act directly to United States Antimony Corporation (NYSE American: UAMY) — the only domestic processor and finished antimony product manufacturer in the country — to modernize and expand its refining facility in Thompson Falls, Montana, with capacity expected to double to 320 tons per month by year-end.

The other name drawing serious institutional attention is Perpetua Resources (NASDAQ: PPTA). The company broke ground on its Stibnite Gold Project in Idaho in October 2025 after years of permitting work. The project holds 148 million pounds of antimony and is positioned to become the only domestically mined source of the mineral, potentially supplying 35% of annual U.S. antimony demand in its first six years of production. Perpetua has already secured over $70 million in DoD awards and a preliminary $2 billion financing term sheet from the Export-Import Bank of the United States.

From a market standpoint, the global antimony market is currently valued at roughly $2.4 to $2.5 billion. Analysts project it could reach $4.1 to $4.4 billion by the mid-2030s, representing steady annual growth of 5% to 6% over the next decade. Prices have moderated from a record high of nearly $60,000 per tonne reached in mid-2025 following China’s export ban, settling around $25,000 per tonne — still nearly double where they sat two years ago.

The broader context matters here. With the Iran conflict still rattling global supply chains and reshoring emerging as a defining economic policy, the U.S. government’s push to develop domestic critical mineral production is not a trend — it is a structural shift backed by federal dollars and bipartisan political will. For small and microcap investors, that combination of government demand, supply scarcity, and growing commercial applications across defense and advanced technology creates a genuinely compelling long-term setup in a sector that most of the market is still sleeping on.

Antimony may not be a household name yet. It probably will be.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated feasibility study. Century recently filed its updated 2026 NI 43-101 feasibility study for its 100%-owned Angel Island Lithium Project in Nevada. The updated study reflects engineering optimization and improvements that materially strengthen the project’s economic profile and highlight Angel Island as one of the most significant and economically robust sedimentary lithium developments in the United States.

Next steps. With the completion and filing of the 2026 Feasibility Study and the recent C$7 million financing, the company is well positioned to advance the Angel Island project to its next development stages. Planned activities include submitting a Plan of Operations to the Bureau of Land Management to initiate the National Environmental Policy Act (NEPA) review process, advancing Nevada state permitting, progressing detailed engineering, and continuing engagement with strategic and downstream partners. Century also intends to further evaluate the rate of earth element recovery at Angel Island and continue discussions with potential offtake and project finance partners.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating 1Q 2026 estimates. We have lowered our 1Q and FY 2026 EPU estimates to $(0.02) and $2.20, respectively, from $0.61 and $2.60. We have marked-to-market ARLP’s holding of bitcoins, which amounted to 592 bitcoins as of year-end 2025. The price of bitcoin closed at $87,508.83 on December 31, 2025, compared to $68,233.31 on March 31. We anticipate that the value of digital assets in Q1 2026 could decrease by approximately $11.4 million if all bitcoins were held through the end of the first quarter. Because it would represent a non-cash unrealized loss, it has no impact on our adjusted EBITDA estimate. Moreover, our EPU estimate reflects a non-cash impairment charge of $43 million related to a decision to cease longwall production at the Mettiki Mining complex, although it has no impact on our adjusted EBITDA estimate.

FY 2026 estimates. We have also adjusted the cadence of coal sales throughout the year, with lower volumes in the first quarter, along with higher segment adjusted EBITDA expense per ton. While we have lowered our FY 2026 EPU estimates, our adjusted EBITDA estimate declined only modestly to $708.3 million from $708.4 million due, in part, because our estimates reflect greater tonnage in the second half of the year when adjusted EBITDA expense per ton is lower, and margins are stronger. Quarterly coal sales volume is expected to be lowest in the first quarter, increase modestly in the second, and peak in the back half as longwall move disruptions abate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Toronto, Ontario–(Newsfile Corp. – April 1, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (Frankfurt: 20Q) (“Aurania” or the “Company”) announces that certain of its directors have agreed to receive their quarterly director fees in the form of stock options in lieu of cash for the first quarter of 2026. In addition, the Company wishes to grant the directors additional stock options due to the expiration of out-of-the-money stock options previously granted to the directors in lieu of cash for director fees.

An aggregate of 203,000 stock options was granted to directors on March 31, 2026, having an exercise price of $0.205. All such stock options will be exercisable for a period of three years from the date of grant and vested immediately upon grant. In the event a director intends to exercise such stock options, such director shall be solely responsible for paying the entirety of the exercise price.

Aurania also granted 40,000 stock options to a consultant of the Company on March 31, 2026, at an exercise price of $0.205. These options are exercisable for a period of one year from the date of grant and vested immediately upon grant.

The Company also announces that the Company and Dr. Keith Barron, CEO of the Company, have agreed to an amendment to a previously issued loan from Dr. Barron to the Company in the amount of up to US$2,094,500 (the “Loan“) originally announced on April 30, 2025, pursuant to which the term of the Loan has been amended such that the Loan matures twelve months and one day after repayment notice is given by Dr. Barron to the Company.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

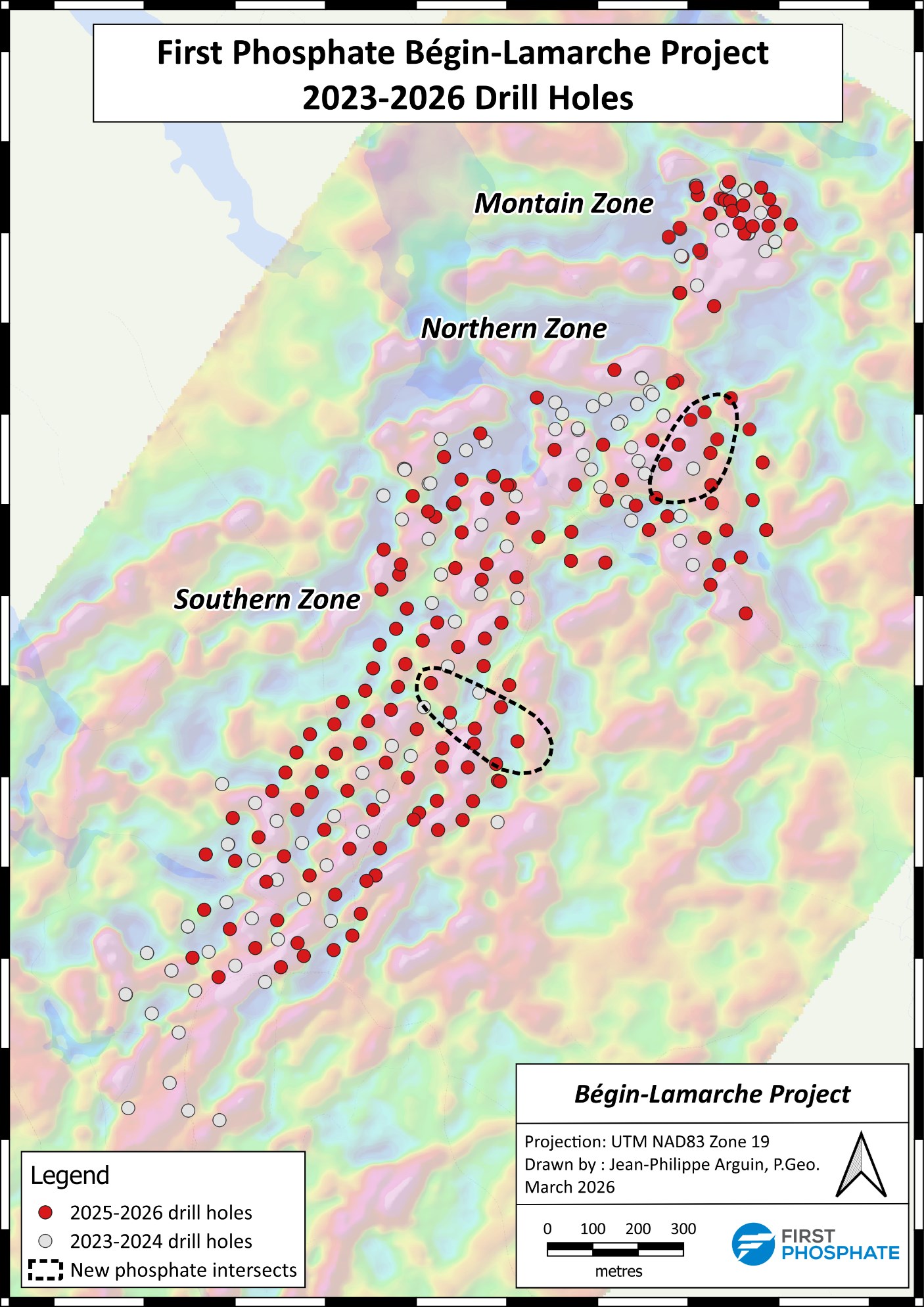

Expanded infill drill program. First Phosphate completed an expanded infill drill program, totaling approximately 40,000 meters, that was launched in October at its Begin-Lamarche property in Saguenay-Lac-St. Jean, Quebec. The drilling program, which was expanded from 30,000 meters of drilling, confirmed continuity of phosphate mineralization across the existing resource horizon and discovered two new mineralized intersects in the Northern and Southern zones.

Updated geological model. The incremental 10,000 meters of drilling was designed to better understand the new intersects and test mineralization at depth in areas across the Northern and Southern zones. The company is processing the full set of drill results from its original and expanded drill program with the goal of updating the geological model in the coming weeks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saguenay-Lac-Saint-Jean, Quebec–(Newsfile Corp. – March 31, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the completion of its infill drill program launched on October 21, 2025 at its Bégin-Lamarche property in Saguenay-Lac-St-Jean, Quebec.

The drilling campaign has confirmed extensive, continuous mineralization across the existing horizon of the initial resource estimate. The drill program has also discovered two new phosphate intersects located in the Northern Zone and in the Southern Zone on the eastern side of the existing mineralized zone. An additional 10,000 meters of targeted drilling was added to the initial drill program of 30,000 meters to solidify an understanding of these new intersects as well as to test additional mineralization located at depth in various areas across the Northern and Southern Zones.

The Company is currently processing the full set of drill results from its original and expanded drill campaign which totalled about 40,000 m with the goal of upgrading the geological model for the Bégin-Lamarche property in the coming weeks.

“We were able to discover, drill and create a significant geological model for the Bégin-Lamarche property all within about 3.5 years,” commented Gilles Laverdiere, Chief Geologist of First Phosphate. “Such rapid progression from initial discovery reflects the exceptional continuity of the phosphate mineralization and the efficiency of our exploration approach.”

The Company also announces that Gilles Laverdiere will be retiring as Chief Geologist following 48 years of dedicated service to the mining industry. Existing team member, Steeve Lavoie, PGeo., will assume the role of Chief Geologist. Steeve has over 20 years of experience in the mineral exploration industry, having worked most recently with Agnico Eagle Mines prior to joining First Phosphate in November 2025.

“I’d like to thank Gilles Laverdière for his dedication to First Phosphate and the Bégin-Lamarche project since its early discovery and for building our strong exploration foundation,” says First Phosphate CEO, John Passalacqua. “Most importantly, we would like to thank Gilles for delaying his retirement until he could see through Bégin-Lamarche to its resource definition and geological modelling. Gilles is a man of remarkable dedication and a true role model for the industry.”

The Company also announces today a grant of 300,000 incentive stock options (the “Options”) to Steeve Lavoie in accordance with the terms of the Company’s Omnibus Equity Incentive Plan. Each Option has an exercise price of $0.98 and expires on December 29, 2028 with 25% vesting every 6 months for two years following the date of grant. All securities issued in accordance with the Option grant are subject to a hold period of four months plus one day.

First Phosphate Bégin-Lamarche Project 2023-2026 Drill Holes

The scientific and technical information relating to First Phosphate contained in this press release has been reviewed and approved by Gilles Laverdière, P.Geo., Chief Geologist of First Phosphate and Steeve Lavoie, P,Geo., Geology Manager of First Phosphate who are qualified persons within the meaning of National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay-Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

Forward-Looking Information and Cautionary Statement

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, of the GPI funding award under the contribution agreement with NRCan and the project funded thereby including the Company’s plans for building and onshoring a vertically integrated mine-to-market LFP battery supply chain for North America. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things, assumptions regarding general business and economic conditions; there being no significant disruptions affecting the activities of the Company or inability to access required project inputs; permitting and development of the projects being consistent with the Company’s expectations; the accuracy of the current mineral resource estimates for the Company and results of metallurgical testing; certain price assumptions for P2O5 and Fe2O3; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the Company’s relationship with First Nations and other Indigenous parties remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

{kind=link}