Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated feasibility study. Century released the results of its 2026 NI 43-101 feasibility study for the 100%-owned Angel Island Lithium Project in Esmeralda County, Nevada. The updated study reflects engineering optimization and improvements that materially strengthen the project’s economic profile and highlight Angel Island as one of the most significant and economically robust sedimentary lithium developments in the United States.

Lower initial capital expenditures. Phase I initial capital expenditures are estimated to be $997 million, a significant reduction from the $1.5 billion outlined in the 2024 Study. The updated study streamlines development into a two-phase approach. Phase I contemplates 7,500 tonnes per day (tpd) of mill feed, expanding to 15,000 tpd in Phase II beginning in Year 5. Phase II expansion capital is estimated at $660 million. A previously planned third expansion phase has been eliminated, lowering overall capital requirements. The economic analysis is based on a 40-year production schedule, with planned life-of-mine average production of 26,500 tonnes per annum of battery-grade lithium carbonate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)—a high–grade Copper–PGE, Nickel, gold and silver system—toward Canada’s next polymetallic mine. On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~212.86 km² and roughly 50 km of prospective basin margins. Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs. Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025. It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s JabalSaid Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Expanding the High-Grade Core at Lion. Summer-Fall 2025 drilling successfully extended high-grade mineralization down plunge at the Lion Zone, with impressive intercepts including 8.40 meters grading 8.05% copper equivalent recovered, and 5.10 meters grading 9.86% copper equivalent recovered, reinforcing strong vertical continuity.

Precious Metals Significantly Enhance Value. Assays revealed substantial palladium, platinum, and gold contributions, materially boosting copper-equivalent grades and highlighting the robust polymetallic nature of the deposit.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

TORONTO, Feb. 18, 2026 /CNW/ – Power Metallic Mines Inc. (the “Company” or “Power Metallic”) (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt: IVV1) is pleased to provide a release of assays from its fall drill program

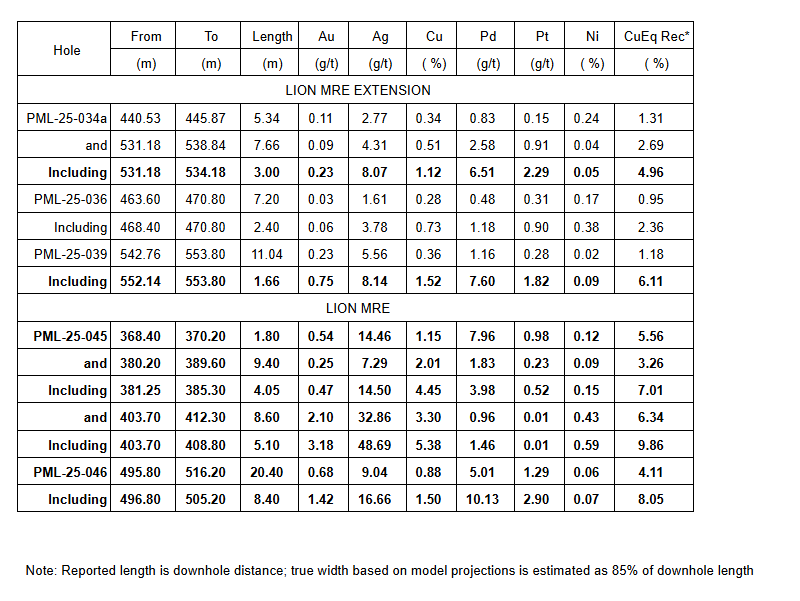

Summer-Fall Drilling Release 4 – Lion

Figure 1 – Lion Drill holes reported in this news release, with off-hole BHEM anomalies from recent drilling (see Lion- Tiger Deep discussion below) (CNW Group/Power Metallic Mines Inc.)Figure 2 – Exploration target areas currently being explored on the Nisk Project. (CNW Group/Power Metallic Mines Inc.)

The summer-fall 2025 drilling program was designed to search for extensions to the Lion Zone, specifically down plunge from known mineralization, and to infill drilling the Lion deposit to define the zone geometry to a confidence level that would allow a future mineral resource estimate to be carried out to an Indicated Resource classification.

As assay results are returned from this exploration drilling, they have continued to successfully define the Lion mineralization. The holes in this release are extensions down-plunge from high-grade shoots that are internal to the Lion zone for future MRE modelling. Drilling reported here intersected mineralization below the central high-grade zone of Lion, including a high-grade palladium-platinum-gold-copper intersection of 8.40m @ 8.05% CuEqRec1 included within 20.40m @ 4.11% CuEqRec1 in hole PML-25-046; and 5.10m @ 9.86% CuEqRec1 included in 8.60m of 6.34% CuEqRec1 in hole PML-25-045.

Highlighting the polymetallic nature of Lion the reported results from hole PML-25-046 was expected to be a relatively low-grade hole based on initial observations based on the amount of copper mineralization in the core (veins, stringers, and disseminations). Subsequently the assay results indicated that the 20.4m of moderate copper mineralization (0.88% Cu) carried high values of Pd (5.01 g/t) as well as Pt and Au. Power Metallic is now developing logging procedures to help identify these higher-grade precious metal zones that form part of this orthomagmetic polymetallic deposit.

Extensional intersections on the west side of Lion included 7.66m @ 2.69% CuEqRec1in hole PML-25-34a, again with significant metal value carried by Pd-Pt. These holes have largely confirmed the grade of the Lion zone as well as increasing the size of the interpreted higher-grade lodes.

Hole PML-25-036 is approximately 150m west of the main Lion zone. This intersection is indicative of another lens of polymetallic mineralization west of Lion and will be followed up by future drilling to expand this zone.

Table 1 – Lion Zone Intersections reported in this News Release

1Copper Equivalent Rec Calculation (CuEqRec1) CuEqRec in represents CuEq calculated based on the following metal prices (USD) : 2,360.15 $/oz Au, 27.98 $/oz Ag, 1,215.00 $/oz Pd, 1000.00 $/oz Pt, 4.00 $/lb Cu, 10.00 $/lb Ni and 22.50 $/lb Co., and recovered grades based on recent locked-cycle metallurgical recoveries by SGS Canada Inc (see press release Jan 21, 2026).

“We have made a lot of progress on the Lion Zone. The continuity and growth of the higher-grade core of Lion zone with in-fill drill holes (MRE holes), coupled with our amazing metal recovery numbers that we reported a couple of weeks ago puts us in great shape to ramp up exploration this year. Commented Power Metallic Ceo Terry Lynch

Exploration Update

Power Metallic is expecting to receive the balance of the fall drill holes within the month of February. It will provide a detailed update on the exploration the company is conducting on Lion West, The Hydro lands, Tiger Deep and the Elephant exploration plays as well as initial exploration on the Li-FT acquisition ground. In addition, there will be further updates on the Lion Zone East expansion drilling following the recently recognized high grade east plunging mineralization structures extending from the Lion main zone.

Qualified Person

Joseph Campbell, P. Geo, VP Exploration at Power Metallic, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Metallic Mines Inc.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)–a high–grade Copper–PGE, Nickel, gold and silver system–toward Canada’s next polymetallic mine.

On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~212.86 km² and roughly 50 km of prospective basin margins.

Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs.

Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025.

It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s JabalSaid Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

For further information, readers are encouraged to contact: Power Metallic Mines Inc. The Canadian Venture Building 82 Richmond St East, Suite 202 Toronto, ON

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

QAQC and Sampling

GeoVector Management Inc (“GeoVector”) is the Consulting company retained to perform the actual drilling program, which includes core logging and sampling of the drill core.

All samples were submitted to and analyzed at Activation Laboratories Ltd (“Actlabs”), an independent commercial laboratory for both the sample preparation and assaying. Actlabs is a commercial laboratory independent of Power Metallic with no interest in the Project. Actlabs is an ISO 9001 and 17025 certified and accredited laboratories. Samples submitted through Actlabs are run through standard preparation methods and analysed using RX-1 (Dry, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 μm) preparation methods, and using 1F2 (ICP-OES) and 1C-OES – 4-Acid near total digestion + Gold-Platinum-Palladium analysis and 8-Peroxide ICP-OES, for regular and over detection limit analysis. Pegmatite samples are analyzed using UT7 – Li up to 5%, Rb up to 2% method. Actlabs also undertake their own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibr

Gold tumbled sharply Thursday in a sudden wave of selling that swept across financial markets, as traders liquidated metal positions to cover mounting losses in equities. The sharp decline underscores how even traditional safe-haven assets can be caught in broader risk-off moves when volatility spikes.

Bullion fell as much as 4.1% during the session before trimming some losses, while silver plunged as much as 11% in one of its steepest drops in recent memory. Copper also slid, declining nearly 3% on the London Metal Exchange. The move came amid renewed pressure on U.S. technology stocks, where concerns resurfaced about whether massive artificial intelligence investments will generate the expected returns.

As equity markets weakened, some investors were forced to raise cash quickly. In moments of intense stress, even defensive assets such as gold can be sold to meet margin calls or offset losses elsewhere. Rather than serving purely as a haven, gold briefly became a source of liquidity.

The speed of the decline suggested systematic and momentum-driven selling. Analysts noted that algorithmic strategies and commodity trading advisors likely accelerated the drop as key technical levels gave way. Such strategies often amplify moves in either direction, particularly when market sentiment shifts abruptly.

Part of Thursday’s pressure also stemmed from profit-taking. Gold and silver have been on a powerful rally since 2024, with momentum-driven buying pushing both metals to repeated record highs. That advance stalled abruptly late last month, when gold posted its largest one-day drop in more than a decade and silver recorded a historic plunge. Since then, both metals have traded in a volatile but relatively tight range, lacking fresh catalysts to sustain the upward momentum.

The latest decline does not necessarily signal the beginning of a sustained downtrend. Instead, it highlights heightened volatility in a market where positioning had become crowded. When sentiment-driven trades unwind, price swings can be exaggerated.

Despite the recent rout, many major banks remain bullish on gold’s longer-term outlook. Analysts continue to point to structural drivers that supported the earlier rally, including persistent geopolitical tensions, concerns about central bank independence, and a broader shift by some investors away from traditional assets such as currencies and sovereign bonds. Several institutions maintain ambitious year-end targets for bullion, arguing that underlying demand remains intact.

Silver faced additional pressure from options-related activity tied to the iShares Silver Trust, the world’s largest silver exchange-traded fund. Investors who had previously accumulated bullish positions near recent highs were seen selling contracts, potentially intensifying downside momentum.

Market participants are now turning their attention to upcoming U.S. economic data, including core consumer price figures, for signals about the Federal Reserve’s interest-rate trajectory. Precious metals typically benefit from lower borrowing costs, as they do not offer interest payments and tend to compete with yield-bearing assets.

By early afternoon in New York, spot gold was down nearly 3% at $4,938.38 an ounce. Silver had dropped more than 9% to $76.34, while platinum and palladium also declined. The Bloomberg Dollar Spot Index edged slightly higher.

The episode serves as a reminder that in periods of extreme market stress, no asset class is immune from volatility. Even gold, long regarded as a financial safe haven, can fall sharply when liquidity becomes the priority.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 2025 Estimate Revisions. We are adjusting Q4 estimates to reflect softer commodity pricing, with WTI averaging $59.10 per barrel versus our prior $60.00 estimate and wider differentials reducing realized Canadian pricing. We are lowering our revenue, adjusted funds flow (AFF), and AFF per share estimates to C$80.7 million, C$29.1 million, and C$1.04, respectively, from C$88.8 million, C$35.8 million, and C$1.28. Our production estimate remains unchanged at 19,419 boe/d.

FY 2025 Estimate Revisions. We are modestly lowering our full-year revenue, AFF, and AFF per share estimates to reflect lower fourth-quarter estimates. We now forecast revenue of C$290.6 million, AFF of C$112.9 million, and AFF per share of C$4.58, down from C$298.7 million, C$119.5 million, and C$4.85, respectively. Our outlook continues to assume average 2025 production of approximately 17,000 boe/d. We will update our 2026 estimates following the release of InPlay’s 2026 guidance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Advancing a multi-project portfolio. Aurania is advancing two projects in France: a gold exploration project in Brittany and a nickel recovery project in Corsica. Aurania is also evaluating the recovery of nickel and cobalt from the waste tailings of the former Balangero asbestos mine near Turin, Italy. The projects in Corsica and Italy offer significant environmental benefits for the nearby communities, along with the economic benefit of recovering valuable critical metals. In Ecuador, the company is having productive discussions with government officials to advance its project while pursuing potential strategic partnerships.

Exploration Licenses in Brittany. Aurania, through a wholly owned French subsidiary, was granted three exploration licenses for polymetallic metals, including gold, in the Brittany Peninsula of northwestern France. The three license areas, Epona, Taranis, and Belenos, are in southern Brittany and northern Pays de la Loire in France. Aurania is in the process of identifying all the landowners to seek their support for exploration.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Transocean Ltd. (NYSE: RIG), a leading international provider of offshore contract drilling services, announced today that it has entered into a definitive agreement to acquire Valaris Limited (NYSE: VAL) in an all-stock transaction valued at approximately $5.8 billion. The transaction creates one of the largest and most diversified offshore drilling companies in the world, with a pro forma enterprise value of approximately $17 billion.

Under the terms of the agreement, Valaris shareholders will receive a fixed exchange ratio of 15.235 shares of Transocean stock for each Valaris common share. Based on the companies’ closing prices on February 6, 2026, Transocean shareholders will own approximately 53% of the combined company on a fully diluted basis, with Valaris shareholders owning the remaining 47%.

A Strategic Combination of Premium Offshore Assets

Transocean is widely recognized for operating the highest-specification floating offshore drilling fleet in the world, with a strong focus on ultra-deepwater and harsh-environment drilling. The company currently owns or operates a fleet of 27 mobile offshore drilling units, including 20 ultra-deepwater floaters and seven harsh-environment floaters.

Valaris brings complementary strengths, operating a high-quality fleet of ultra-deepwater drillships, versatile semisubmersibles, and modern shallow-water jackups. With operations spanning nearly every major offshore basin globally, Valaris has established itself as an industry leader across all water depths and geographies, emphasizing safety, operational excellence, and technological innovation.

On a pro forma basis, the combined company will own 73 rigs, including 33 ultra-deepwater drillships, nine semisubmersibles, and 31 modern jackups, significantly expanding its ability to serve customers in deepwater, harsh-environment, and shallow-water markets worldwide.

Financial and Operational Benefits

The transaction is expected to deliver substantial financial and operational benefits. The combined company will have an industry-leading contract backlog of approximately $10 billion, enhancing cash flow visibility and providing a strong foundation for long-term planning.

Transocean has identified more than $200 million in incremental cost synergies related to the transaction, additive to its ongoing cost-reduction program, which is expected to reduce costs by more than $250 million in aggregate through 2026. Management expects the stronger pro forma cash flow to accelerate debt reduction, targeting a leverage ratio of approximately 1.5x within 24 months of closing.

“This transaction creates a very attractive investment in the offshore drilling industry, differentiated by the best fleet, proven people, leading technologies, and unequalled customer service,” said Keelan Adamson, Transocean’s President and Chief Executive Officer. “The powerful combination is well-timed to capitalize on an emerging, multi-year offshore drilling upcycle.”

The combined company is expected to have an estimated pro forma market capitalization of approximately $12.3 billion, improved trading liquidity, and a stronger capital markets profile, potentially enabling broader equity index inclusion.

Leadership and Transaction Structure

Following the close of the transaction, Transocean’s senior management team will continue to lead the combined company, with Keelan Adamson serving as Chief Executive Officer. Jeremy Thigpen will assume the role of Executive Chairman of the Board. The board will consist of nine current Transocean directors and two current Valaris directors.

Transocean will remain incorporated in Switzerland, with its primary administrative office in Houston. Valaris Limited is a Bermuda exempted company, and the transaction will be completed through a court-approved scheme of arrangement under Bermuda’s Companies Act.

The transaction has been unanimously approved by the boards of directors of both companies and is expected to close in the second half of 2026, subject to regulatory approvals, customary closing conditions, and approval by shareholders of both companies. Shareholder support agreements have already been secured from Perestroika AS, which owns approximately 9% of Transocean’s outstanding shares, and from Famatown Finance Limited and Oak Hill Advisors, which collectively own approximately 18% of Valaris’ outstanding shares.

Industry Context and Recent Trends

The offshore drilling industry has been undergoing a period of consolidation following years of financial stress, bankruptcies, and asset rationalization. In recent years, the number of offshore drillers operating globally has declined sharply, leaving a smaller group of companies with increasingly high-quality fleets.

At the same time, energy producers have become more disciplined with capital spending, prioritizing returns over aggressive production growth. This has favored offshore projects with long reserve lives and lower decline rates, particularly in deepwater basins such as the Gulf of Mexico, Brazil, and offshore West Africa.

Oilfield service providers, including offshore drillers, have increasingly pursued mergers to improve scale, reduce costs, and enhance pricing power amid ongoing operational and pricing pressures. As available high-specification rigs remain constrained, leading contractors have been better positioned to benefit from improving dayrates and utilization.

Against this backdrop, the Transocean–Valaris combination reflects a broader industry trend toward creating larger, financially stronger players capable of supporting complex offshore developments while delivering improved returns to shareholders.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Bond offering details. InPlay announced a senior unsecured bond issuance in Israel for up to 550 million New Israeli Shekels (NIS), or approximately C$241 million. Three amortization payments of 6% of the principal amount of the bonds will be due on December 15 of 2027, 2028, and 2029, and the fourth and last amortization payment of the remaining 82% will be due on December 15, 2030. The offering is expected to close on or around February 12, 2026, subject to certain conditions.

Expanding capital market access. Beyond the financing itself, we view the transaction as a strategic expansion of InPlay’s funding base outside of Canada. InPlay received interest from over 40 institutional investors in the oversubscribed offering and, to date, has accepted tenders for NIS 550 million of the bonds. The transaction further strengthens InPlay’s diversified financing sources while reducing its overall cost of capital.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kodiak Gas Services, Inc. (NYSE: KGS) announced it has entered into a definitive agreement to acquire Distributed Power Solutions, LLC (DPS) in a transaction valued at approximately $675 million, marking a strategic expansion beyond traditional contract compression into the rapidly growing distributed power market. The acquisition, which includes $575 million in cash and roughly $100 million in Kodiak equity, is expected to close in early April 2026, subject to regulatory approvals and customary conditions.

DPS is a leading provider of turnkey, scalable, and highly reliable distributed power solutions, serving customers across energy, industrial, and digital infrastructure end markets. Its fleet includes approximately 384 megawatts of modern generation capacity powered by Caterpillar reciprocating engines and turbines, positioning it as a premium platform in a market increasingly constrained by grid limitations.

The strategic rationale for the deal centers on strong operational and commercial synergies. Kodiak brings deep expertise in operating and maintaining large-horsepower equipment, supported by more than 700 Caterpillar-certified technicians, advanced fleet monitoring systems, and embedded maintenance processes. Management expects these capabilities to enhance the reliability and uptime of DPS’s generation assets while supporting future fleet expansion.

Financially, the acquisition is expected to be immediately accretive to earnings and discretionary cash flow per share. The transaction values DPS at approximately 7.4x estimated 2026 adjusted EBITDA, a compelling multiple given the business’s contracted revenue profile and exposure to high-growth end markets. Notably, DPS has secured long-term contracts, including roughly 100 megawatts serving a large data center operator with demonstrated 99.9% reliability for over a year.

The deal also expands Kodiak’s customer reach. While the company has historically focused on upstream and midstream oil and gas customers, DPS adds exposure to digital infrastructure clients, including data centers increasingly adopting “bring-your-own-power” solutions. With power grid constraints intensifying and data center demand accelerating, distributed power is emerging as a primary, long-term energy solution rather than a temporary backup option.

Kodiak President and CEO Mickey McKee described distributed power as a natural extension of the company’s core competencies, noting that the acquisition enhances Kodiak’s ability to deliver critical energy infrastructure while opening new avenues for growth. DPS President Scott Milligan echoed that sentiment, highlighting the cultural alignment between the two companies and the opportunity to scale DPS’s high-quality fleet on a larger operational platform.

From a strategic perspective, the transaction positions Kodiak at the intersection of energy reliability and digital growth. As data centers, industrial users, and energy customers seek faster deployment and greater control over power supply, the combined Kodiak-DPS platform is well positioned to meet rising demand.

With an experienced management team joining Kodiak and a strong backlog of contracted cash flows, the acquisition represents a meaningful step in Kodiak’s evolution from a pure-play compression provider into a broader provider of mission-critical energy infrastructure solutions.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Industry-scale facility fully permitted. Comstock has received all required regulatory approvals for its first industry-scale solar recycling facility in Silver Springs, Nevada, including the Written Determination Permit and the Air Quality Permit from the Nevada Division of Environmental Protection. The permits cover the full scope required to commission a facility designed to process more than 3.0 million panels per year, representing up to 100 thousand tons of end-of-life solar materials. Installation, testing, and commissioning are expected to occur during the first quarter of 2026.

Unit economics. Comstock’s recycling process is certified as a zero-landfill solution and designed to handle all major solar panel types, eliminating contaminants and recovering aluminum, glass, and metal-rich tailings. Comstock estimates that facility-level economics reflect a combination of upfront processing fees and proceeds from recovered materials, resulting in revenue of ~$750 per ton against all-in operating costs of roughly $150 per ton. Based on current operating data, profitability is achievable at relatively low utilization levels.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

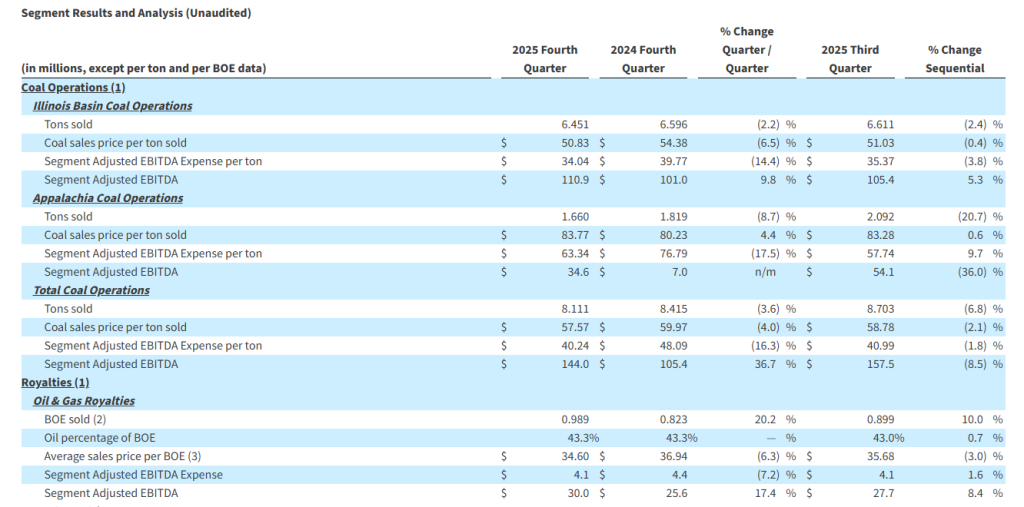

Fourth quarter and full year 2025 financial results. Alliance reported adjusted fourth quarter revenue, adj. EBITDA and earnings per unit (EPU) of $535.5 million, $191.1 million, and $0.64, respectively, compared to $590.1 million, $124.0 million, and $0.12 during the prior year period. We had forecast revenue, adj. EBITDA and EPU of $560.1 million, $182.9 million, and $0.57, respectively. While the quarter was impacted by lower coal sales, which impacted revenue, operating expenses were lower, and net income on equity method investments exceeded our estimate. Full year 2025 adj. EBITDA and EPU of $698.7 million and $2.40, respectively, were above our estimates of $690.5 million and $2.33, respectively.

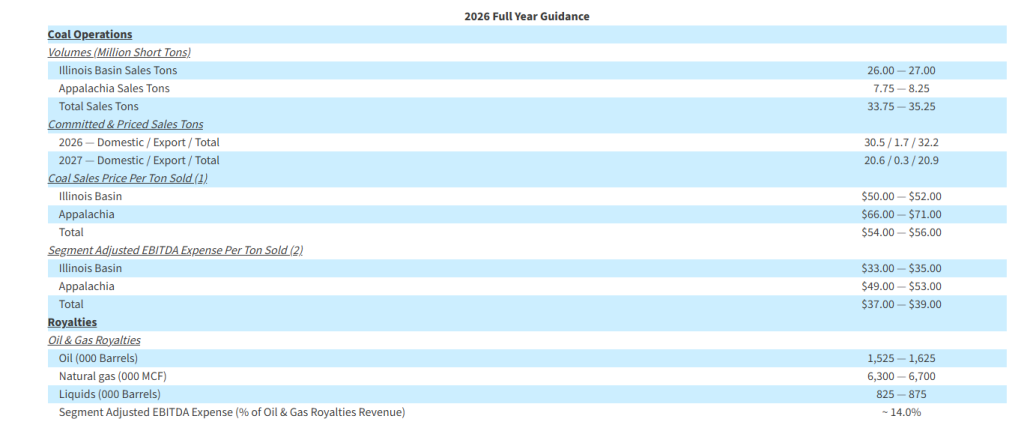

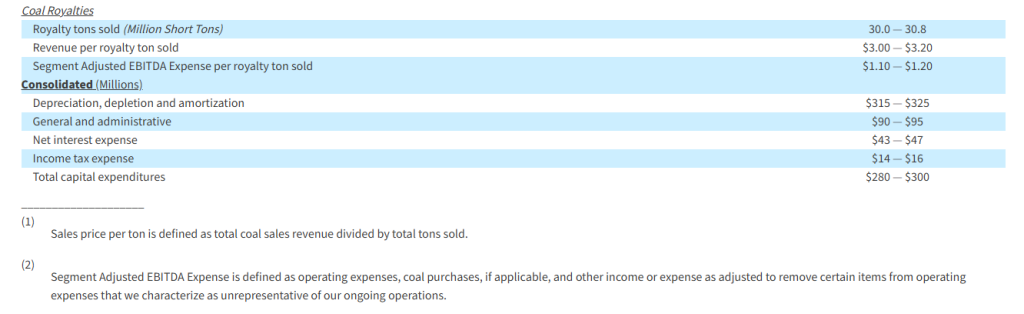

Management guidance for 2026. Total coal sales are expected to be in the range of 33.75 million to 35.25 million tons, while the sales price of coal per ton is expected to be in the range of $54.00 to $56.00. Segmented adjusted EBITDA expense per ton sold is expected to be $37.00 to $39.00. ARLP has committed and priced 32.2 million tons of its 2026 sales volume, including 30.5 million tons for the domestic market and 1.7 million tons for the export market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The U.S. government is making its most aggressive move yet to secure critical mineral supply chains—and small-cap mining stocks may be the biggest beneficiaries.

President Donald Trump is preparing to launch Project Vault, a first-of-its-kind $12 billion strategic stockpile of critical minerals designed to break America’s dependence on China. Modeled after the Strategic Petroleum Reserve, the initiative will target minerals essential to modern industry: rare earths, cobalt, gallium, nickel, and antimony—materials that power electric vehicles, semiconductors, defense systems, jet engines, and consumer electronics.

For investors focused on small-cap and emerging resource companies, this announcement represents more than a policy shift. It’s a potentially transformative multi-year demand catalyst.

Why Project Vault Changes the Game

Project Vault pools $10 billion in financing from the U.S. Export-Import Bank with $1.67 billion in private capital, creating a centralized procurement system that will buy and store minerals on behalf of major manufacturers including General Motors, Boeing, Stellantis, Google, and GE Vernova. Three global commodities trading firms—Hartree, Traxys, and Mercuria—will manage sourcing and logistics.

Unlike traditional defense-focused stockpiles, this program explicitly targets civilian supply chains. It offers participating manufacturers two critical advantages: price stability and guaranteed access during supply disruptions. Companies commit to purchasing materials at a predetermined price and can later buy them back at the same cost—a mechanism designed to eliminate volatility and enable long-term production planning.

The implications for upstream producers are significant. Government-backed demand provides the certainty mining companies need to justify capital investment, accelerate development timelines, and secure project financing.

The Small-Cap Advantage

Markets responded immediately. Shares of USA Rare Earth, Critical Metals Corp., United States Antimony, and NioCorp Developments all surged following the announcement, signaling investor recognition of a fundamental truth: supply security requires actual production, not just strategic intent.

This creates a disproportionate opportunity for small-cap miners.

Large diversified mining companies already generate stable cash flow from multiple commodities. Smaller miners, by contrast, often operate single-asset projects concentrated in exactly the minerals Project Vault prioritizes. For these companies, government-backed offtake agreements and improved access to financing could fundamentally alter project economics—transforming marginal assets into commercially viable operations.

Put simply: Project Vault de-risks production at the precise stage where small mining companies struggle most—the transition from exploration to commercial scale.

The timing reflects geopolitical reality. China’s export restrictions last year exposed the brittleness of Western supply chains, forcing some U.S. manufacturers to curtail production. Project Vault is Washington’s financial response—a clear signal that the federal government will actively intervene to reshape critical mineral markets.

The U.S. has also established cooperation agreements with key allies including Australia, Japan, and Malaysia, reinforcing a non-China supply network. This geopolitical alignment strengthens the long-term investment case for North American and allied-jurisdiction producers, who now benefit from both policy support and structural demand shifts.

Project Vault is more than a stockpile—it’s a demand guarantee underwritten by the U.S. government. For small-cap investors, this could mark the start of a sustained revaluation cycle for select critical mineral producers, particularly those nearing production or capable of supplying rare earths and strategic metals domestically.

The framework changes the risk-reward equation. Companies with credible projects in favorable jurisdictions now have a potential counterparty whose commitment extends beyond market cycles. That’s a fundamentally different investment environment than what existed even six months ago.

Bottom Line

Selectivity remains essential—not every critical mineral stock will benefit equally. But the broader narrative is unmistakable: critical minerals have moved from niche sector to national priority, and the market is already repricing accordingly.

For investors positioned in quality small-cap producers, Project Vault may prove to be the catalyst they’ve been waiting for.

Fourth quarter 2025 net income of $82.7 million and Adjusted EBITDA of $191.1 million, up 406.2% and 54.1%, respectively, year-over-year

Record full year and fourth quarter 2025 oil & gas royalty volumes, up 7.2% and 20.2%, respectively, year-over-year

Fourth quarter 2025 coal production volumes increased to 8.2 million tons produced, representing a year-over-year increase of 18.7%

Full year 2025 total revenue of $2.2 billion, net income of $311.2 million, and Adjusted EBITDA of $698.7 million

Total and net leverage ratios as of December 31, 2025, were 0.66 times and 0.56 times, respectively

On January 27, 2026, declared quarterly cash distribution of $0.60 per unit, or $2.40 per unit annualized

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter and full year ended December 31, 2025 (the “2025 Quarter” and “2025 Full Year”, respectively). This release includes comparisons of results to the quarter and year ended December 31, 2024 (the “2024 Quarter” and “2024 Full Year”, respectively), as well as to the quarter ended September 30, 2025 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of Adjusted EBITDA and Segment Adjusted EBITDA Expense and related reconciliations to comparable GAAP financial measures, please see the end of this release.

For the 2025 Quarter net income increased $66.3 million to $82.7 million, or $0.64 per basic and diluted limited partner unit, compared to $16.3 million, or $0.12 per basic and diluted limited partner unit for the 2024 Quarter as a result of reduced operating expenses, lower impairment charges and increased investment income, partially offset by lower revenues and a decrease in the fair value of our digital assets during the 2025 Quarter. Total revenues decreased 9.2% to $535.5 million in the 2025 Quarter compared to $590.1 million for the 2024 Quarter primarily due to lower coal sales and transportation revenues, partially offset by record oil & gas royalty volumes. Adjusted EBITDA increased 54.1% to $191.1 million in the 2025 Quarter compared to $124.0 million in the 2024 Quarter.

Compared to the Sequential Quarter, total revenues decreased by 6.3% due to lower coal sales volumes and prices, partially offset by higher other revenues. Net income decreased by 13.1% compared to the Sequential Quarter as a result of lower revenues and a decrease in the fair value of our digital assets, partially offset by reduced operating expenses and increased investment income. Adjusted EBITDA for the 2025 Quarter increased by 2.8% compared to the Sequential Quarter.

Total revenues decreased 10.4% to $2.19 billion for the 2025 Full Year compared to $2.45 billion for the 2024 Full Year primarily due to lower coal sales pricing and transportation revenues. Net income for the 2025 Full Year was $311.2 million, or $2.40 per basic and diluted limited partner unit, compared to $360.9 million, or $2.77 per basic and diluted limited partner unit, for the 2024 Full Year as a result of lower revenues and a decrease in the fair value of our digital assets in the 2025 Full Year, partially offset by reduced operating expenses and increased investment income. Adjusted EBITDA for the 2025 Full Year was $698.7 million compared to $714.2 million for the 2024 Full Year.

CEO Commentary

“Our team delivered solid performance to close out the fourth quarter and full year,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “We achieved record Oil & Gas royalty volumes, underscoring the quality of our minerals portfolio. In our coal operations, the Illinois Basin continued to perform well, highlighted by Hamilton’s record year for clean tons and yield. While Appalachia costs increased sequentially primarily due to an unplanned outage at a key customer’s plant that required production adjustments at Mettiki and lower recoveries at Tunnel Ridge, we expect Appalachia costs to improve in 2026 as mining progresses in the new district at Tunnel Ridge.”

Mr. Craft continued, “Industry fundamentals strengthened during the quarter. The December 2025 PJM capacity auction for 2027-2028 delivery years cleared at the FERC‑approved cap across the entire region, with every megawatt of coal capacity selected. At the same time, reserve margins fell below PJM targets, reinforcing the critical need to keep existing, reliable baseload resources online as data center and industrial load growth accelerates. The Trump administration this month reestablished the National Coal Council, citing coal’s critical importance to our country’s economic competitiveness and national security, warning that the United States cannot win the global AI race without coal.”

Mr. Craft concluded, “During the fourth quarter, we also recognized investment income of $17.5 million related to our share of the increase in the fair value of a coal-fired power plant indirectly owned and operated by an equity method investee. This investment aligns with our strategy to allocate a portion of excess cash flows into investments that we believe will generate attractive returns for our unitholders.”

Coal Operations

Coal sales volumes decreased by 2.2% and 2.4% in the Illinois Basin compared to the 2024 Quarter and Sequential Quarter, respectively, due primarily to decreased tons sold from our River View mine as a result of transportation delays and the timing of committed sales. Reduced export sales volumes from Gibson South also contributed to the reduction in coal sales volumes in the Illinois Basin compared to the 2024 Quarter. In Appalachia, tons sold decreased by 8.7% and 20.7% compared to the 2024 Quarter and Sequential Quarter, respectively, due to reduced sales volumes across the region, primarily caused by timing of committed sales at our Mettiki mine, a longwall move at Tunnel Ridge and lower recoveries at Tunnel Ridge and Mettiki. Coal sales price per ton sold decreased by 6.5% in the Illinois Basin compared to the 2024 Quarter as a result of the expiration of higher priced legacy contracts. In Appalachia, coal sales price per ton sold increased by 4.4% compared to the 2024 Quarter primarily due to higher domestic and export pricing as well as an increased sales mix of higher priced MC Mining and Mettiki sales volumes in the 2025 Quarter. ARLP ended the 2025 Quarter with total coal inventory of 1.1 million tons, representing an increase of 0.4 million tons and 0.1 million tons compared to the end of the 2024 Quarter and Sequential Quarter, respectively.

Segment Adjusted EBITDA Expense per ton in the Illinois Basin decreased by 14.4% and 3.8% compared to the 2024 Quarter and Sequential Quarter, respectively, due primarily to increased production at our Hamilton mine resulting from fewer longwall move days and improved recoveries during the 2025 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton for the 2025 Quarter decreased by 17.5% compared to the 2024 Quarter due to increased production at our Mettiki and MC Mining operations and higher recoveries at MC Mining and Tunnel Ridge. Compared to the Sequential Quarter, Segment Adjusted EBITDA Expense per ton increased by 9.7% in Appalachia primarily due to reduced recoveries across the region and lower production at our Mettiki and Tunnel Ridge operations.

Royalties

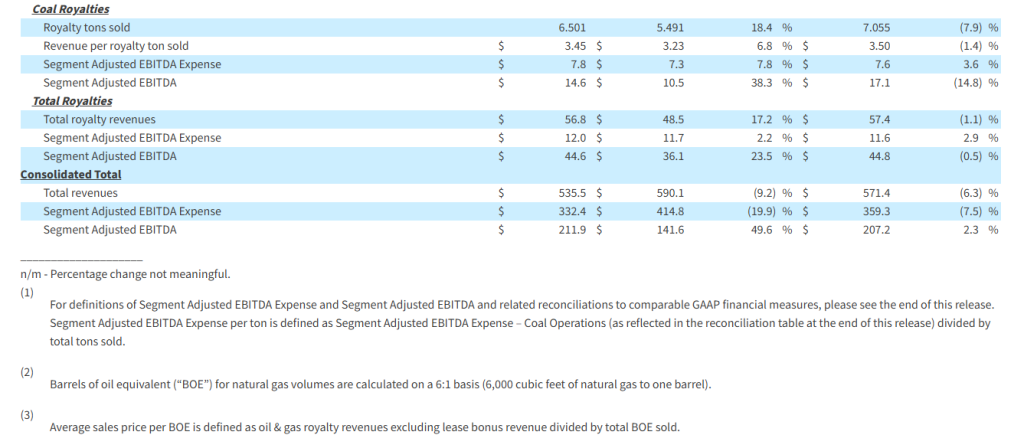

Segment Adjusted EBITDA for the Oil & Gas Royalties segment increased to $30.0 million in the 2025 Quarter compared to $25.6 million and $27.7 million in the 2024 Quarter and Sequential Quarter, respectively, due to record oil & gas royalty volumes, which increased 20.2% and 10.0%, respectively, partially offset by lower average sales price per BOE.

Segment Adjusted EBITDA for the Coal Royalties segment increased to $14.6 million in the 2025 Quarter compared to $10.5 million in the 2024 Quarter due to higher royalty tons sold, primarily from Tunnel Ridge, and higher average royalty rates per ton received from the Partnership’s mining subsidiaries. Compared to the Sequential Quarter, Segment Adjusted EBITDA for the Coal Royalties segment decreased 14.8% as a result of lower royalty tons sold and royalty rates per ton.

Growth Investments

During the 2025 Quarter, equity method investment income increased $22.0 million primarily driven by a higher increase in the value of our share of the net assets of the companies in which we hold interests. This included approximately $17.5 million related to our share of the increase in the fair value of a coal-fired power plant indirectly owned and operated by an equity method investee.

Balance Sheet and Liquidity

As of December 31, 2025, total debt and finance leases were outstanding in the amount of $463.7 million. The Partnership’s total and net leverage ratios were 0.66 times and 0.56 times debt to trailing twelve months Adjusted EBITDA, respectively, as of December 31, 2025. ARLP ended the 2025 Quarter with total liquidity of $518.5 million, which included $71.2 million of cash and cash equivalents and $447.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities. ARLP also held 592 bitcoins valued at $51.8 million as of December 31, 2025.

Distributions

On January 27, 2026, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2025 Quarter of $0.60 per unit (an annualized rate of $2.40 per unit), payable on February 13, 2026, to all unitholders of record as of the close of trading on February 6, 2026.

Outlook

“Looking ahead to 2026, oil & gas royalty volumes are expected to be near 2025 Full Year record levels at the high end of our 2026 guidance,” commented Mr. Craft. “Over the past week, commodity benchmark pricing has been volatile, with 2026 oil futures down 3-8% and natural gas futures up 10-15% compared to 2025 averages. February Henry Hub futures climbed to $7.46 per MMBtu on its final trading day compared to $3.68 per MMBtu at the beginning of this year. Lower crude oil prices have created a softer backdrop for acquisition activity. However, we were successful in completing $14.4 million in oil & gas mineral acquisitions during the 2025 Quarter and we remain committed to growing our minerals portfolio moving forward. At the midpoint of our 2026 guidance, coal royalty tons sold are expected to be six million tons, or 25% above 2025, reflecting higher volumes at our Hamilton and Tunnel Ridge mines.”

“Turning to our coal operations, we expect another year of strong operational and financial performance as we build on the progress achieved in 2025,” continued Mr. Craft. “Our 2026 guidance reflects the anticipated impact of reduced coal sales volumes at our Mettiki mine as disclosed in last week’s WARN Act notices. Notwithstanding these reductions, our guidance reflects higher planned coal sales tons in 2026, where previous capital investments in equipment and mine development are driving meaningful productivity gains with total sales tons expected to exceed 2025 levels by 0.8 million to 2.3 million tons, primarily across the Illinois Basin and at Tunnel Ridge. Customer demand across our core markets remains strong, and we have already committed and priced more than 93% of our 2026 sales tons guidance range at the midpoint.”

Mr. Craft added, “We expect improved operating expenses per ton sold in the Illinois Basin and at Tunnel Ridge to help offset lower coal sales prices per ton sold year-over-year, supporting our efforts to preserve margins while maintaining our focus on cost discipline and execution.”

Mr. Craft concluded, “With tightening domestic coal supply, robust contracting activity, and growing electricity demand, our longer-term outlook continues to be promising. Supported by our logistical advantages, cost structure, and strong balance sheet, we believe Alliance will continue to demonstrate its ability to serve as a reliable supply partner and is preparing to meet increased customer demand.”

ARLP is providing the following guidance for the full year ending December 31, 2026:

Conference Call

A conference call regarding ARLP’s 2025 Quarter and Full Year financial results and 2026 guidance is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13757920.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as a reliable energy partner for the future by pursuing opportunities that support the growth and development of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial and operational performance, coal and oil & gas consumption and expected future prices, our ability to increase or maintain unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, infrastructure projects at our existing properties, growth in domestic electricity demand, preserving liquidity and maintaining financial flexibility, our future repurchases of units, and the impact of recently announced tax legislation. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; our ability to provide fuel for growth in domestic energy demand, should it materialize; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the effects of a prolonged government shutdown; impacts of geopolitical events, including the conflicts in Ukraine and in the Middle East and the potential for conflict in Venezuela; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers and operators, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices and the direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by the operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of and investments into the infrastructure of our operations and properties, including the timing of such investments coming online; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging and other infrastructure and technology companies; dependence on significant customer contracts, and failure of customers to renew existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, and the results of central bank policy actions including interest rates, bank failures, and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted or threatened by the United States and foreign governments, including the imposition of or increase in tariffs on steel and/or other raw materials; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, such as the Environmental Protection Agency’s emissions regulations for coal-fired power plants, and state legislation seeking to impose liability on a wide range of energy companies under greenhouse gas “superfund” laws, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2024, filed on February 27, 2025, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2025, June 30, 2025 and September 30, 2025, filed on May 9, 2025, August 7, 2025 and November 7, 2025, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

")

(CNW Group/Power Metallic Mines Inc.)")

")