Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Concession renewal in Ecuador. In March, Aurania filed the appropriate documentation for the 2025 renewal of its 42 mineral exploration concessions in southeastern Ecuador, along with a request to enter into an agreement for payment of the annual concession fees. The request was accepted, and the company is working with various governmental departments to negotiate an agreement. Aurania considers that by filing the concession renewals prior to the March 31 deadline, it maintains its property in Ecuador in good standing while a payment agreement is being finalized.

Kuri-Yawi IP geophysical survey. An induced polarization survey was completed at the Kuri-Yawi epithermal gold target in late 2024. The survey confirmed the presence of a conductive area, which could be an epithermal conduit that Aurania has been targeting. Aurania’s geologists are currently studying and comparing data compiled to date from the IP survey, an airborne magnetic survey, field work, previous drilling data, and a MobileMT survey to define the best possible drill hole locations for a future drilling program.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Gold prices hit a record $3,128.06 per ounce, driven by geopolitical risks and economic uncertainty. – Investors are bracing for new U.S. tariffs, which could further fuel safe-haven demand. – Analysts expect gold to reach $3,300 per ounce by the end of 2025.

Gold prices have skyrocketed to record highs, surpassing $3,100 per ounce as a wave of economic and geopolitical uncertainty fuels demand for the precious metal. Spot gold hit a new all-time high of $3,128.06 on Monday, marking one of the most significant rallies in its history. The surge comes amid expectations of fresh U.S. tariffs, a shifting Federal Reserve policy, and persistent global tensions, all of which have reinforced gold’s role as a safe-haven asset.

The metal has posted 19 all-time highs in 2025, with seven exceeding the unprecedented $3,000 mark. Prices are up 18% this year, following a 27% surge in 2024. The sharp rise has been attributed to strong central bank purchases, heightened inflation concerns, and a growing shift toward gold-backed exchange-traded funds (ETFs). Analysts believe the rally has momentum, given the broader macroeconomic environment.

Investors are closely watching upcoming U.S. trade policy decisions. President Donald Trump is set to announce new reciprocal tariffs on April 2, with automobile tariffs following on April 3. The prospect of escalating trade tensions is further amplifying gold’s appeal as a hedge against economic instability. “Gold’s rally has been fueled by escalating geopolitical tensions, inflation concerns, and strong investor demand,” said Alexander Zumpfe, a precious metals trader at Heraeus Metals Germany. “Given the current macroeconomic environment—particularly trade war uncertainties and central bank policies—this trend appears sustainable in the near term.”

Geopolitical instability has played a crucial role in gold’s ascent. With ongoing hostilities in the Middle East and no clear resolution to the Russia-Ukraine conflict, safe-haven demand remains strong. Trump’s recent remarks regarding Russia, Iran, and even Greenland have further unsettled markets, driving additional inflows into gold. “Geopolitical uncertainty is high, and Trump’s weekend comments have only increased the global risk environment, enhancing gold’s appeal,” said Nikos Tzabouras, senior market analyst at Tradu.com.

The Federal Reserve’s monetary policy shift is also contributing to gold’s strength. The central bank cut interest rates by 50 basis points last September, and officials anticipate two more rate cuts by the end of 2025. A lower rate environment tends to weaken the U.S. dollar, making gold more attractive as an alternative store of value. Despite this, some analysts argue that central banks’ rising gold purchases are less about losing confidence in the dollar and more about diversification. “Whilst buying gold may reduce central banks’ overall exposure to the dollar, we don’t think this surge reflects a severe loss of confidence in the greenback,” analysts at Capital Economics noted. They predict gold will reach $3,300 per ounce by year-end.

Investor appetite for gold remains strong, with ETFs seeing their largest weekly inflows since March 2022. While North American ETFs have benefited, demand from European investors has also surged due to political uncertainties. With gold’s record-breaking rally showing no immediate signs of slowing, market participants continue to seek safety in the metal amid a turbulent economic landscape.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor webinar. Century Lithium recently discussed the Angel Island Lithium project during an insightful investor webinar. Key highlights included: 1) Angel Island is an advanced project with one of the largest lithium deposits in the United States, 2) the project employs a proven patent-pending process for chloride leaching, along with direct lithium extraction to produce lithium carbonate, 3) Century has a secured a 1,770 acre-feet per year water rights permit, and 4) the company has demonstrated its ability to consistently produce battery grade lithium carbonate on-site at its pilot plant in Amargosa Valley, Nevada.

Updated feasibility study. Century Lithium recently completed an initial internal optimization study of the project and identified potential cost reductions of up to 25%, or $395.2 million, associated with the project’s Phase I capital expenditures totaling $1,580.7 billion. We think additional cost-reduction measures could apply to the second and third production phases of the project. Century expects to complete an updated feasibility study as early as by year-end.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Oil prices remain vulnerable to the global trade war, impacting Gulf economies dependent on crude exports. – Currency pegs to the U.S. dollar pose challenges, particularly for countries with high external debt. – New trade corridors, particularly between the Gulf and Asia, offer potential opportunities amid shifting global supply chains.

The Middle East has largely avoided direct tariffs in the ongoing global trade war, but its economies remain vulnerable to broader economic shifts. With oil demand at risk, currency pressures mounting, and global trade flows changing, the region must navigate an increasingly uncertain landscape while also seizing new opportunities.

One of the most immediate concerns for the Middle East is oil. While a weaker U.S. dollar initially benefits oil-exporting nations by making crude cheaper for foreign buyers, tariffs and economic slowdowns could lead to lower global demand. Brent crude prices remain sensitive to global trade conditions, and a prolonged trade war could weigh on revenues for major producers like Saudi Arabia and the UAE. Despite efforts to diversify their economies, oil remains the backbone of many Gulf nations, making them particularly exposed to shifts in global demand.

Another challenge comes from currency pegs. Several Gulf states, including Saudi Arabia, the UAE, Qatar, Oman, and Bahrain, have their currencies tied to the U.S. dollar. As the dollar fluctuates in response to tariffs and economic policies, these countries face higher import costs. This could lead to inflationary pressures, especially in economies heavily reliant on imported goods. At the same time, countries with significant external debt, such as Lebanon, Jordan, and Egypt, could struggle with higher debt-servicing costs if the dollar strengthens further.

Trade tensions also pose risks to regional trade hubs like the UAE, which depend on global trade flows. As a logistics and financial center, Dubai has built its economy around international commerce, meaning a prolonged global slowdown could impact its growth. Economists warn that while Gulf economies have taken steps to diversify, the effects of reduced trade volumes could still be felt.

However, the situation is not entirely negative. The trade war has also encouraged the creation of new trade corridors, particularly between the Gulf and Asia. The GCC-Asia trade relationship has seen sustained growth, with increasing investment and business ties. China’s Belt and Road Initiative has already deepened economic connections, and as global supply chains shift, Middle Eastern economies could benefit from a larger role in these emerging trade networks.

Political factors could also play a role in shaping the region’s economic resilience. U.S. President Donald Trump has maintained strong ties with Gulf nations, particularly Saudi Arabia, and has shown an interest in keeping them aligned with U.S. economic and geopolitical priorities. This relationship may provide some buffer against trade war fallout, as evidenced by Jordan’s ability to secure exemptions from certain U.S. tariffs due to its strategic importance.

Looking ahead, Middle Eastern economies must continue to adapt to changing global conditions. Strengthening domestic demand, securing diversified trade partnerships, and managing currency risks will be key strategies for mitigating potential downturns. While challenges remain, opportunities exist for the region to carve out a more influential role in global trade as supply chains and economic alliances shift.

Key Points Summary: – Waraba Gold is acquiring up to an 80% stake in Somaco Global Resources, gaining access to prospective gold and manganese licences in northern Ivory Coast. – The deal involves a $500,000 initial payment, $1.5 million over two years, and $5 million in exploration commitments, alongside issuing six million common shares. – Waraba has suspended operations in Mali due to security concerns but remains committed to resuming activities when conditions improve.

Canadian mineral exploration company Waraba Gold has entered into an earn-in agreement to acquire up to an 80% stake in Somaco Global Resources, a move that strengthens its footprint in the West African mining sector. Somaco Global holds two highly prospective gold licence applications in northern Ivory Coast, a region known for its rich mineral deposits. These include the Sirasso licence and the Tengrela & Tiegba licences, both located near existing gold mines and mineralized shear zones.

One of the most significant assets in this deal is the Sirasso licence, covering 369.34km² in the Senoufou greenstone belt, an area recognized for its high gold potential. This licence was previously held in a joint venture (JV) with Barrick Gold, one of the world’s leading gold producers. Historically, greenstone belts have yielded high-grade gold deposits, and the Senoufou belt is no exception. Waraba’s investment signals confidence in the region’s potential for large-scale gold discoveries.

In addition to Sirasso, Waraba Gold gains access to the Tengrela & Tiegba licences, which span a combined area of nearly 767km². These licences are not only prospective for gold but also manganese, a critical mineral in steel production and battery technologies. The proximity of these licences to existing gold mines further enhances their exploration potential.

Under the terms of the agreement, Waraba Gold will gradually acquire an 80% stake in Somaco Global Resources over four years. The investment involves an initial payment of $500,000 to Somaco’s shareholders within the next two months, an additional $1.5 million to be paid over a two-year period, exploration commitments totaling $5 million over the next four years, and the issuance of six million common shares to Somaco shareholders upon the signing of a definitive joint venture agreement.

To finance the initial commitments, Waraba Gold announced plans to raise up to $500,000 through non-convertible unsecured debentures. These funds will also provide general working capital for the company’s operations. In addition, Waraba Gold will appoint two Somaco nominees as directors, further integrating the companies and ensuring a strategic partnership moving forward.

Alongside the Ivory Coast expansion, Waraba Gold provided an update on its Mali operations, revealing that it has temporarily suspended activities at the Fokolore Gold Project due to security concerns. Despite setbacks, Waraba remains committed to the Malian mining sector, having submitted a letter of intent for a mining permit in June 2024. However, with ongoing political instability, the company is waiting for conditions to improve before resuming full-scale operations.

West Africa has emerged as one of the fastest-growing gold mining regions globally, attracting major industry players. However, political uncertainties in countries like Mali have raised concerns among investors. Recently, CEOs of leading gold mining companies stated that Mali’s new mining code requires adjustments to encourage further foreign investment. Regulatory changes will play a crucial role in shaping the future of the region’s mining industry.

Waraba Gold’s agreement with Somaco Global Resources marks a strategic expansion into the Ivory Coast, an increasingly important gold-producing nation. By securing access to high-potential licences, Waraba is positioning itself for long-term growth in the West African mining sector. With ongoing fundraising efforts and a commitment to exploration, Waraba Gold aims to unlock significant value from its new assets. However, challenges in Mali and broader market uncertainties may still impact the company’s overall trajectory in the coming years.

VIRGINIA CITY, NEVADA, March 25, 2025 – Comstock Inc. (NYSE: LODE) (“Comstock,” “our” and the “Company”), today announced the timely completion of two successful settlements of prior outstanding strategic commitments. These commitments originated from prior acquisitions of foundational assets and intellectual property that have been instrumental in advancing Comstock’s renewable fuels and metals businesses. Comstock has eliminated regular cash payments and reinforced its financial position to support the Company’s long-term commercialization strategy.

“Both of these equity-based settlements were with the original founders and resulted in material, restructured savings, enhanced liquidity and increased financial flexibility,” said Corrado De Gasperis, Comstock’s Executive Chairman and CEO. “We are grateful to the founders, their innovations, partnering, flexibility, and confidence in our equity and its value.”

The settlements align with Comstock’s ongoing efforts to simplify and strengthen its balance sheet, enhance liquidity, and position its differentiated technology and businesses for rapid, scalable, and long-term growth. With the metals segment achieving full operational status and remarkable, real-time revenue growth and the fuels segment securing multiple commercial, operational and jurisdictional support agreements, and direct strategic investments, both businesses remain focused on driving continued revenue generation and expanding their globally relevant network of supply chain partners.

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies that are deployable across entire industries to contribute to energy abundance by efficiently extracting and converting under-utilized natural resources, such as waste and other forms of woody biomass into renewable fuels, and end-of-life electronics into recovered electrification metals. Comstock’s innovations group is also developing and using artificial intelligence technologies for advanced materials development and mineral discovery for sustainable mining. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: RB Milestone Group LLC Tel (203) 487-2759 ir@comstockinc.com

For media inquiries or questions: Comstock Inc., Tracy Saville Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future market conditions; future explorations or acquisitions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; business opportunities, growth rates, future working capital, needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; operational or technical difficulties in connection with exploration, metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious and other metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; challenges to, or potential inability to, achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology and efficacy, quantum computing and generative artificial intelligence supported advanced materials development, development of cellulosic technology in bio-fuels and related material production; commercialization of cellulosic technology in bio-fuels and generative artificial intelligence development services; ability to successfully identify, finance, complete and integrate acquisitions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Key Points: – Gold miners’ equity funds are seeing their largest net inflows in over a year as gold prices reach record highs. – After years of cost struggles, major miners like Newmont and Barrick Gold are benefiting from increased profitability and stronger cash flows. – Investors are turning back to mining stocks as a hedge against inflation and market uncertainty.

After months of outflows, investors are returning to gold mining stocks, buoyed by record-high gold prices that have improved the profit outlook for mining firms. With gold surpassing $3,000 an ounce this year—a gain of more than 15%—funds investing in gold miners saw their first net monthly inflow in six months this March, totaling $555.3 million, according to LSEG Lipper data.

While gold prices also climbed in 2024, gold miners faced mounting cost pressures from rising labor and fuel expenses, as well as regulatory setbacks like tax disputes in Mali and project delays in Canada. These challenges pushed many investors toward traditional gold funds instead of equities, leading to a net $4.6 billion outflow from gold miner-focused funds in 2024—the highest in a decade. Conversely, physical gold and gold derivative funds attracted $17.8 billion, the most in five years.

With rising gold prices boosting profitability, mining stocks are once again attracting investor interest. Leading companies like Newmont and Barrick Gold have recovered from last year’s declines, posting year-to-date gains of 27% and 21.5%, respectively. After facing cost pressures in recent years, gold mining firms are now in a stronger position to capitalize on higher gold prices, making them more appealing to investors.

The improved market conditions are prompting major gold miners to reward shareholders. Barrick Gold recently announced a $1 billion share buyback after reporting strong profits and doubling its free cash flow in Q4 2024. Similarly, AngloGold Ashanti declared a final dividend of 91 U.S. cents per share—nearly five times higher than the previous year—while Gold Fields hinted at a potential share buyback in 2025. Harmony Gold also revealed plans to self-fund the construction of a new copper mine in Australia.

With miners stabilizing operations and benefiting from higher gold prices, mining equities are increasingly viewed as an attractive investment. As market uncertainty and inflation persist, investors are showing renewed interest in gold mining stocks as a potential hedge and diversification strategy.

Given the miners’ historically low valuations, some analysts argue that gold mining stocks may present even better opportunities than gold itself. As confidence in gold miners grows alongside surging gold prices, these stocks may continue to attract investors seeking stability in an unpredictable market.

Smaller and junior gold mining companies stand to benefit significantly from this renewed investor interest in mining stocks. Unlike major miners, which already have strong cash flows and established operations, junior miners often struggle with financing new projects and navigating regulatory hurdles. However, with gold prices at record highs, investor appetite for higher-risk, high-reward opportunities may increase, providing these smaller companies with much-needed capital.

Higher gold prices also make previously unviable mining projects more attractive, allowing junior miners to push forward with exploration and development. Companies with promising gold reserves but lacking production capabilities may now find it easier to secure funding through equity offerings or partnerships with larger mining firms.

Additionally, with major miners focusing on share buybacks and dividends, they may look to acquire smaller mining companies to replenish their reserves, driving M&A activity in the sector. This could create lucrative exit opportunities for junior miners and early-stage investors.

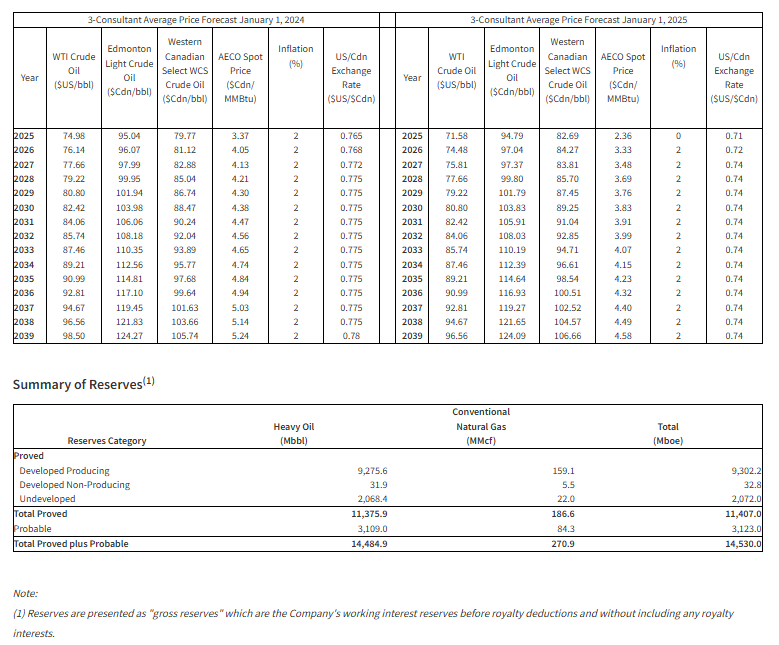

Vancouver, British Columbia–(Newsfile Corp. – March 19, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce highlights from its independent reserves evaluation (the “Reserve Report”), prepared by McDaniel & Associates Consultants Ltd. (“McDaniel”) and effective as at December 31, 2024.

Hemisphere’s estimated 2024 capital expenditures1 of approximately $22 million grew year-end Proved Developed Producing (“PDP”) reserves by 13%, increased annual production by 10%, added required infrastructure, and commenced testing a new resource play in Saskatchewan with an enhanced oil recovery (“EOR”) polymer pilot project. These investments were funded entirely by cash flow from the Company’s long-life reserve base and ultra-low production decline rates in the Atlee Buffalo oil assets. Hemisphere’s current quarterly production is trending at 3,800 boe/d (99% heavy oil and based on field estimates between January 1 – March 15, 2025).

During the year, Hemisphere also distributed over $21 million in shareholder returns, made up of $15.7 million in base and special dividends and $5.5 million of share purchases under its normal course issuer bid (“NCIB”). The Company exited the year in a cash position with estimated working capital1 of over $5 million.

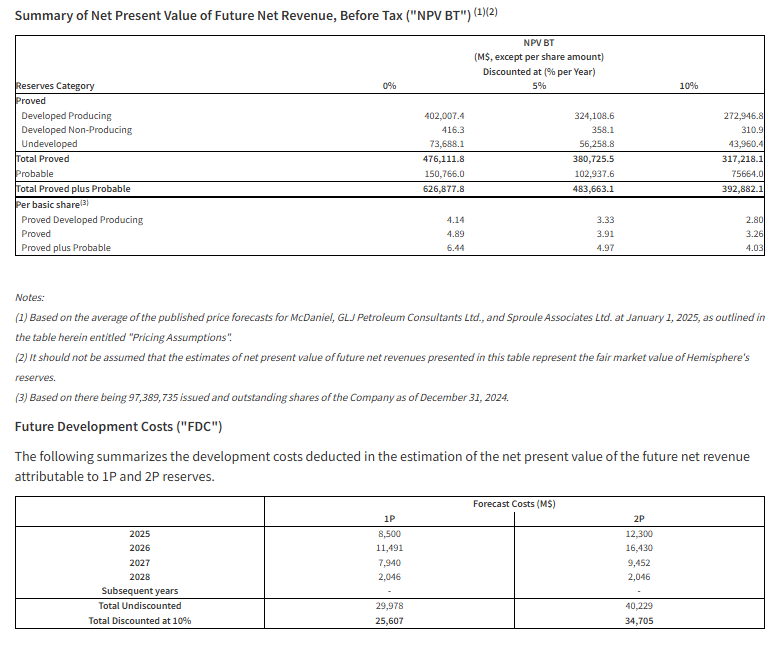

The Company’s continued success in the development of its EOR projects was recognized again by McDaniel in the Reserve Report. In the PDP category, Hemisphere replaced 186% of 2024 production and increased reserve value by 10% to $273 million NPV10 BT. In addition, Hemisphere’s Proved (“1P”) reserve value at year-end was $317 million NPV10 BT and Proved plus Probable (“2P”) reserve value was $393 million NPV10 BT.

The Company’s new Saskatchewan lands currently account for only 3% of 1P and 6% of 2P reserves, while making up only 3% of 1P and 5% of 2P NPV10 BT valuations of Hemisphere’s reserves. Significant potential reserve upside remains on Hemisphere lands if the play proves successful over the course of 2025 and beyond.

Consistent with McDaniel’s 2023 year-end evaluation, the Reserve Report incorporates full corporate abandonment, decommissioning, and reclamation costs (“ADR”) in the PDP category. Hemisphere has always been cautious of acquiring additional wellbore and facility liabilities. A direct result of this strategy is that Hemisphere’s reserves retain more comparative value per barrel than companies with additional ADR liabilities that must be deducted from their base valuations. Management estimates that total undiscounted and uninflated existing ADR is $8.1 million ($2.1 million NPV10 BT, with costs inflated at 2%/yr), which includes all ADR associated with both active and inactive wells, pipelines, and facilities regardless of whether such wells, pipelines, and facilities had any attributed reserves.

Hemisphere’s low decline, long life, and high value reserves are indicative of the unique resource the Company has been developing over the past number of years. These valuable assets are the backbone of Hemisphere and are expected to generate significant free cash flow as they continue to grow with planned additional development and optimization of EOR techniques.

2024 Reserve Highlights

Proved Developed Producing (“PDP”) Reserves

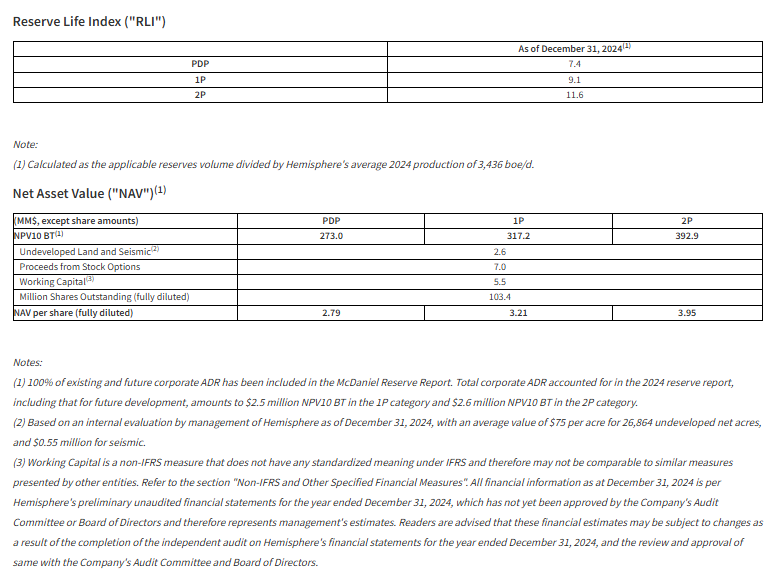

NPV10 BT of $273 million, an increase of approximately 10% over year-end 2023 and equivalent to $2.80 per basic share.

Replaced 186% of 2024 production through organic development.

Recognized reserve volumes of 9.3 MMboe (99.7% heavy crude oil), an increase of 13% year-over-year.

RLI of 7.4 years based on 2024 production.

NAV of $2.79 per fully diluted share based on reserve report pricing assumptions.

Proved (“1P”) Reserves

NPV10 BT of $317 million, equivalent to $3.26 per basic share.

Recognized reserve volumes of 11.4 MMboe (99.7% heavy crude oil).

RLI of 9.1 years based on 2024 production.

NAV of $3.21 per fully diluted share based on reserve report pricing assumptions.

Proved plus Probable (“2P”) Reserves

NPV10 BT of $393 million, equivalent to $4.03 per basic share.

Recognized reserve volumes of 14.5 MMboe (99.7% heavy crude oil).

RLI of 11.6 years based on 2024 production.

NAV of $3.95 per fully diluted share based on reserve report pricing assumptions.

2024 Independent Qualified Reserve Evaluation

The reserves data set forth below is based upon an independent reserves evaluation prepared by McDaniel dated March 18, 2025 with an effective date of December 31, 2024, and is in accordance with definitions, standards, and procedures contained within COGEH and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in Hemisphere’s Annual Information Form which will be filed on SEDAR+ on or before April 30, 2025. Due to rounding, certain totals in the columns may not add in the following tables. All dollar values are in Canadian dollars, unless otherwise noted.

Pricing Assumptions

McDaniel’s independent evaluation was based on the average of the published price forecasts for McDaniel, GLJ Petroleum Consultants Ltd., and Sproule Associates Ltd. (the “3-Consultant Average Price Forecast”) at January 1, 2025, with the following table detailing pricing and foreign exchange rate assumptions. Hemisphere’s corporate production historically averages a discount of approximately $4.10 to WCS pricing. When compared to last year’s 3-Consultant Average Price Forecast dated January 1, 2024, the current WCS pricing outlook is up approximately 4% in 2025, and up 1% thereafter over the next 15-year period. The 2025 3-Consultant Average Price Forecast uses a 5-year 2025-2029 WTI price of US$75.75/bbl and WCS price of Cdn$84.78/bbl.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Forward-looking Statements

This news release contains certain forward-looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this news release contains forward-looking information and statements pertaining to the following: Significant potential reserve upside remains on Hemisphere lands if the play proves successful over the course of 2025 and beyond, the Company’s expectations that its assets are expected to generate significant free funds flow as they continue to grow with planned additional development and optimization of enhanced oil recovery techniques; the volumes of Hemisphere’s oil and gas reserves and the estimated net present values of the future net revenues of such reserves; the Company’s estimates of ADR; the Company’s anticipated filing date for its annual information form for the year ending December 31, 2024; and any upside potential on Hemisphere’s Saskatchewan properties in 2024 and beyond. In addition, statements relating to “reserves” are deemed to be forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the reserves described can be profitably produced in the future.

The estimates of Hemisphere’s reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. In addition, forward-looking statements or information are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: that Hemisphere will continue to conduct its operations in a manner consistent with past operations; the effects of tariffs (or similar trade measures) on Hemisphere’s future results, operations, and cash flows; results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; inflation rates and cost escalations; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward-looking information and statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: changes in commodity prices; changes in applicable tariff rates and trade agreements; regulatory risks, including penalties or other remedial action; the ability of the Company to maintain legal title to its properties; changes to, or restrictions of, labour, supplies, and infrastructure; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties; changes in budgets; increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s annual information form).

The forward-looking information and statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward-looking statements or information, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Oil and Gas Advisories

All reserve references in this news release are “gross” or “Company interest reserves”. Such reserves are the Company’s total working interest reserves before the deduction of any royalties and without including any royalty interests of the Company.

It should not be assumed that the net present value of the estimated net revenues presented in this news release represent the fair market value of the reserves. There is no assurance that the forecast prices and costs assumptions will be attained, and variances could be material. The recovery and reserve estimates of Hemisphere’s crude oil, natural gas liquids and natural gas reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual crude oil, natural gas and natural gas liquids reserves may be greater than or less than the estimates provided herein. Estimates of net present value and future net revenue contained herein do not necessarily represent fair market value. Estimates of reserves and future net revenue for individual properties may not reflect the same level of confidence as estimates of reserves and future net revenue for all properties, due to the effect of aggregation. There is no assurance that the forecast price and cost assumptions in evaluating Hemisphere’s reserves will be attained and variances could be material.

All future net revenues are estimated using forecast prices, arising from the anticipated development and production of our reserves, net of the associated royalties, operating costs, development costs and abandonment and reclamation costs and are stated prior to provision for interest and general and administrative expenses. Future net revenues have been presented in this news release on a before tax basis.

“Boe” means barrel of oil equivalent on the basis of 6 mcf of natural gas to 1 bbl of oil. Boe’s may be misleading, particularly if used in isolation. A boe conversion ratio of 6 mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Oil and Gas Metrics

This news release contains metrics commonly used in the oil and natural gas industry, such as “reserve life index (“RLI”)” and “NAV”. These terms do not have a standardized meaning and the Company’s calculation of such metrics may not be comparable to the calculation method used or presented by other companies for the same or similar metrics, and therefore should not be used to make such comparisons.

“Reserve life index” is calculated as total company interest reserves divided by annual production, for the year indicated.

“NAV per fully diluted share” is calculated using the respective net present values of 1P and 2P reserves, before tax and discounted at 10%, plus internally valued undeveloped land & seismic and proceeds from warrants and stock options, plus working capital, and divided by fully diluted outstanding shares. Net present values are shown at the 3-Consultant Average Price Forecast used in the McDaniel Reserve Report. Management uses NAV per share as a measure of the relative change of Hemisphere’s net asset value over its fully diluted shares over a period of time.

Management uses these oil and gas metrics for its own performance measurements and to provide shareholders with measures to compare the Company’s operations over time. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this news release, should not be relied upon for investment or other purposes.

Financial Information

Certain financial information included in this news release is per Hemisphere’s preliminary unaudited financial statements for the year ended December 31, 2024, which have not yet been approved by the Company’s Audit Committee or Board of Directors and therefore represents management’s estimates. Readers are advised that these financial estimates may be subject to change as a result of the completion of the independent audit on Hemisphere’s financial statements for the year ended December 31, 2024, and the review and approval of same with the Company’s Audit Committee and Board of Directors. All amounts are expressed in Canadian dollars unless otherwise noted.

Non-IFRS and Other Specified Financial Measures

Certain measures commonly used in the oil and natural gas industry referred to herein, including “Capital expenditures” and “Working capital”, do not have standardized meanings prescribed by IFRS and therefore may not be comparable with the calculation of similar measures by other companies. These non-IFRS measures are further described and defined below. Investors are cautioned that these measures should not be construed as alternatives to or more meaningful than the most directly comparable IFRS measures as indicators of Hemisphere’s performance. Set forth below are descriptions of the non-IFRS financial measures used in this news release.

“Capital expenditures” is used by management as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities.

“Working capital” is closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working Capital is used in this document in the context of liquidity and is calculated as the total of the Company’s bank debt plus current assets, less current liabilities, excluding the fair value of financial instruments, lease and decommissioning liabilities. There is no IFRS measure that is reasonably comparable to working capital.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and analysis for the year ended December 31, 2023 and for the three and nine month periods ended September 30, 2024, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

1Capital expenditures and Working capital are non-IFRS measures that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Refer to the sections “Non-IFRS and Other Specified Financial Measures” and “Financial Information”.

VIRGINIA CITY, NEVADA, March 19, 2025 – Comstock Inc. (NYSE: LODE) (“Comstock,” “our” and the “Company”), today announced its 2025 Annual Meeting of shareholders will be held online May 22, 2025 in a virtual-only format via webcast.

Comstock shareholders as of the record date of March 25, 2025, can participate in the online annual meeting, including to vote their shares electronically and/or submit questions during the meeting. The Company’s proxy statement will be sent to shareholders of record and will describe the matters to be voted upon.

Electronic entry to the meeting will begin at 8:45 a.m. PDT / 11:45 a.m. EDT and the meeting will begin promptly at 9:00 a.m. PDT / 12:00 p.m. EDT.

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies that are deployable across entire industries to contribute to energy abundance by efficiently extracting and converting under-utilized natural resources, such as waste and other forms of woody biomass into renewable fuels, and end-of-life electronics into recovered electrification metals. Comstock’s innovations group is also developing and using artificial intelligence technologies for advanced materials development and mineral discovery for sustainable mining. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: RB Milestone Group LLC Tel (203) 487-2759 ir@comstockinc.com

For media inquiries or questions: Comstock Inc., Tracy Saville Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future market conditions; future explorations or acquisitions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; business opportunities, growth rates, future working capital, needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; operational or technical difficulties in connection with exploration, metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious and other metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; challenges to, or potential inability to, achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology and efficacy, quantum computing and generative artificial intelligence supported advanced materials development, development of cellulosic technology in bio-fuels and related material production; commercialization of cellulosic technology in bio-fuels and generative artificial intelligence development services; ability to successfully identify, finance, complete and integrate acquisitions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Key Points: – Gold futures have surpassed $2,990 per ounce, with Wall Street forecasts predicting prices could reach $3,500 later this year. – Geopolitical uncertainty, inflation concerns, and central bank purchases are fueling demand for the precious metal. – Rising gold prices may signal investor caution, monetary policy shifts, and potential market volatility.

Gold has once again proven its status as a safe-haven asset, reaching new record highs as economic and geopolitical uncertainties continue to mount. The latest surge has pushed gold futures above $2,990 per ounce, with some analysts now predicting that prices could hit $3,500 by the third quarter of 2025.

A primary driver of gold’s rally has been increased geopolitical tensions and uncertainty surrounding global trade policies. The Trump administration’s latest tariff measures and ongoing shifts in international relations have created an environment of heightened risk, prompting investors to flock toward assets perceived as stable. Macquarie Group recently raised its gold price forecast, citing trade instability and inflationary pressures as key factors supporting higher prices. Similarly, BNP Paribas and Goldman Sachs have also adjusted their targets, expecting gold to trade above $3,100 an ounce in the near term.

Inflation expectations have played a significant role in gold’s rapid ascent. With the Federal Reserve facing ongoing pressure regarding interest rate policy, the release of softer inflation data has fueled speculation that the central bank may eventually cut rates to support economic growth. Historically, lower interest rates tend to weaken the U.S. dollar and make gold a more attractive investment, further fueling its rally. However, if inflation remains persistent, the Fed may be forced to maintain a more restrictive stance, potentially slowing gold’s upward momentum.

Another major factor driving gold’s price surge is continued central bank buying. Institutional investors and sovereign wealth funds have been stockpiling physical gold as a hedge against currency volatility and economic downturns. Reports indicate that significant amounts of gold have been shipped to vaults in New York in anticipation of potential trade restrictions and price disparities between London and U.S. markets. This surge in demand has tightened supply and contributed to rising prices.

Mark Reichman, research analyst for industrials and basic industries at Noble Capital Markets, highlighted the growing appeal of gold as a safe-haven investment. “Gold’s appeal as a safe-have asset has only grown stronger as investors fear an escalating trade war could trigger both inflation and an economic slowdown. Growing market volatility, along with anxiety associated with geopolitical tensions and the perception of chaotic policy execution in Washington and its attendant consequences, have all contributed to growing demand for gold as a hedge against uncertainty. While some of these catalysts could unwind over time, we think there are several underlying factors, including central bank buying, that could offer support for the gold price..”

The broader economic implications of gold’s record-breaking rally are worth considering. Historically, sharp increases in gold prices have often coincided with periods of financial instability or economic slowdowns. Investors tend to turn to gold during times of uncertainty, viewing it as a hedge against inflation, currency depreciation, and stock market volatility. If gold continues its upward trajectory, it could signal growing concerns over the stability of the global economy and financial markets.

For investors, the question now becomes whether gold’s rally is sustainable. While some analysts believe the precious metal still has room to run, others caution that the current surge could lead to increased volatility. If economic conditions stabilize, or if the Federal Reserve takes a more aggressive stance against inflation, gold prices could face downward pressure. On the other hand, if geopolitical risks escalate further, gold could remain a preferred asset for investors seeking protection against uncertainty.

As gold flirts with record highs, all eyes will be on central banks, inflation data, and geopolitical developments. Whether prices continue climbing or experience a pullback, gold’s performance will serve as an important barometer for global economic sentiment in the months ahead.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor webinar. On March 6, Comstock hosted a webinar to discuss the company’s full year 2024 results and provided a comprehensive business update. Management highlighted significant accomplishments achieved in 2024 and its plans for 2025.

Upcoming events. While Comstock summarized corporate and subsidiary-level objectives for 2025, we view several as significant. These include: 1) Comstock Fuels’ completion of offtake, joint development, and warrant agreements with Marathon Petroleum Corporation on or before June 30, 2025, 2) completion of a Comstock Fuels Series A financing during the second quarter, 3) construction of Comstock Metals’ first large-scale recycling facility at a cost of $6 million, 4) advancement of project level financing for subsidiary projects, and 5) the sale of Comstock’s properties and water rights in Silver Springs, Nevada in the latter part of 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY AB, March. 3, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on March 31, 2025, to shareholders of record at the close of business on March 14, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Marathon investment in Comstock Fuels. Comstock Fuels entered into definitive agreements with subsidiaries of Marathon Petroleum Corporation, including the purchase of $14.0 million in Comstock Fuels equity as part of Comstock’s planned Series A preferred equity financing. Consideration includes $13.0 million in payment-in-kind (PIK) assets comprised of equipment, intellectual property, and other materials at Marathon’s former renewable fuel demonstration facility in Madison, WI. While the PIK assets were transferred as of the February 28 effective date, the cash portion will be received within five business days of Comstock Fuels’ execution of third-party Series A financing agreements totaling at least $25.0 million.

Key elements of the agreements. The agreements included: 1) an agreement for future equity governing the portion of the investment issued in exchange for the PIK assets, 2) an asset transfer agreement to assign the PIK assets, 3) a license agreement covering applicable intellectual property, 4) an agreement to provide post-closing conditions, and 5) a board observer agreement executed as of the effective date. Separately, Comstock executed a commercial lease for the Madison facility at a rate of $44,000 per month.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")