LOS ANGELES, July 11, 2024 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Twin Peaks, Fazoli’s, Smokey Bones and 11 other restaurant concepts, announced today that its Board of Directors has declared the Company’s fiscal 2024 third quarter cash dividend of $0.14 per share on each outstanding share of Class A common stock and Class B common stock. The dividend is payable on August 30, 2024 to holders of record of Class A common stock and Class B common stock as of the close of business on August 15, 2024.

The declaration and payment of future dividends, as well as the amounts thereof, are subject to the discretion of the Company’s Board of Directors. The amount and size of any future dividends will depend upon the Company’s future results of operations, financial condition, capital levels, cash requirements and other factors. There can be no assurance that the Company will declare and pay dividends in future periods.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands Inc. (NASDAQ: FAT) (the Company) is a leading global franchising company that strategically acquires, markets and develops quick service, fast casual and casual dining restaurant concepts around the world. The Company currently owns eighteen restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Smokey Bones, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean, Ponderosa and Bonanza Steakhouses and franchises and owns over 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these risks, uncertainties and contingencies. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pivotal Trial Included A Patient Satisfaction Survey. In late June, Unicycive released safety, efficacy, and dosing data from its Pivotal trial for OCL. As discussed on our Research Note on June 26, over 90% of the patients were able to reach target serum phosphate levels. The trial included a pre-specified patient survey asking about ease of use, satisfaction, and overall preference that shows patients prefer OLC over their current phosphate binders. We see this as an important point that could make it the best treatment in a $1 billion drug category.

We Consider Patient Preference To Be A Strong Point. OLC was developed as an improved formulation of Fosrenol (lanthanum citrate) that would require fewer and smaller pills. This was intended to improve compliance and maintain phosphate levels in the proper range. The Pivotal study for the NDA application showed sufficient safety, tolerability, and effective dose levels, with a pre-specified patient survey to collect post-treatment opinions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. For the fiscal year (FY) 2025, AZZ reported adjusted first quarter net income of $44.0 million or $1.46 per share compared to $33.4 million or $1.14 per share during the prior year period and our estimate of $38.9 million or $1.32 per share. The consensus EPS estimate was $1.30. Adjusted EBITDA increased 10.2% to $94.1 million representing 22.8% of sales versus 21.8% of sales during the first quarter of FY 2024. Sales of $413.2 million exceeded our $402.6 million estimate and a 24.8% gross margin as a percentage of first quarter sales exceeded our estimate of 24.1%. AZZ reiterated its prior fiscal year guidance with sales expected to be in the range of $1.525 billion to $1.625 billion, adjusted EBITDA in the range of $310 million to $360 million, and adjusted diluted EPS in the range of $4.50 to $5.00.

Balance sheet continues to strengthen. During the first quarter, AZZ generated operating cash flow of $71.9 million and the company further reduced debt by $25 million and is on track to achieve or exceed its goal of reducing debt by $60 million to $90 million during the fiscal year. At quarter end, the company’s net leverage was 2.8x trailing twelve months EBITDA. Cash and cash equivalents amounted to $10.5 million. During the quarter, AZZ returned capital to common shareholders in the form of cash dividend payments totaling $4.3 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In a significant turn of events, the latest data from the Bureau of Labor Statistics (BLS) revealed that inflation cooled in June, marking the first monthly decline since 2020. The Consumer Price Index (CPI) fell by 0.1% compared to the previous month, with a year-over-year increase of just 3%, down from May’s 3.3% annual rise. This data beat economists’ expectations of a 0.1% monthly increase and a 3.1% annual gain.

The June CPI report is notable for being the first instance since May 2020 that the monthly headline CPI turned negative. Additionally, the 3% annual gain represents the slowest rate of increase since March 2021.

When excluding volatile food and gas prices, the “core” CPI showed a modest increase of 0.1% from the previous month and a 3.3% rise over the past year. These figures also came in below expectations, as economists had anticipated a 0.2% monthly increase and a 3.4% annual gain. This marks the smallest month-over-month increase in core prices since August 2021.

In response to the report, markets opened on a positive note. The yield on the 10-year Treasury note fell by approximately 10 basis points, trading around 4.2%.

Despite the positive signs, inflation remains above the Federal Reserve’s 2% annual target. However, recent economic data suggests that the central bank might consider rate cuts sooner rather than later. Following the release of the June inflation data, market analysts estimated an 89% likelihood that the Federal Reserve would begin cutting rates at its September meeting, up from 75% the previous day, according to CME Group data.

The broader economic context includes a robust labor market report from the BLS, which indicated that 206,000 nonfarm payroll jobs were added in June, surpassing the forecast of 190,000 jobs. However, the unemployment rate edged up to 4.1%, its highest level in nearly three years.

The Fed’s preferred inflation measure, the core Personal Consumption Expenditures (PCE) price index, showed a year-over-year increase of 2.6% in May, the smallest annual gain in over three years, aligning with expectations.

Ryan Sweet, Chief US Economist at Oxford Economics, noted that while the drop in CPI between May and June bolsters the argument for rate cuts, it should be interpreted cautiously. He emphasized that this single-month decline does not necessarily indicate a lasting trend.

Seema Shah, Chief Global Strategist at Principal Asset Management, echoed this sentiment, suggesting that while the current figures set the stage for a potential rate cut in September, a cut in July remains unlikely. Shah pointed out that such a premature move could raise concerns about the Fed’s insider knowledge on the economy, and more evidence is needed to confirm a sustained downward trajectory in inflation.

In the breakdown of the CPI components, the shelter index, a significant contributor to core inflation, showed signs of easing. It increased by 5.2% on an annual basis, down from May’s rate, and rose by 0.2% month-over-month. This was the smallest increase in rent and owners’ equivalent rent indexes since August 2021. Additionally, lodging away from home decreased by 2% in June.

Energy prices continued their downward trend, with the index dropping 2% from May to June, primarily driven by a notable 3.8% decline in gas prices. On an annual basis, energy prices were up 1%.

Food prices, however, remained a sticky point for inflation, increasing by 2.2% over the past year and 0.2% from May to June. The index for food at home rose by 0.1% month-over-month, while food away from home saw a 0.4% increase.

Other categories such as motor vehicle insurance, household furnishings and operations, medical care, and personal care saw price increases. Conversely, airline fares, used cars and trucks, and communication costs decreased over the month.

As inflation shows signs of cooling, the economic outlook suggests potential shifts in Federal Reserve policy, with market participants keenly watching upcoming data to gauge the next steps in monetary policy.

In a bold move that underscores its commitment to the energy transition, Honeywell International Inc. (NYSE: HON) announced on Wednesday its agreement to acquire Air Products’ (NYSE: APD) liquefied natural gas (LNG) process technology and equipment business for $1.81 billion in cash. This acquisition, Honeywell’s fourth in 2024, signals the industrial giant’s aggressive push into the burgeoning LNG market and its determination to position itself as a key player in the global energy landscape.

The deal comes at a time when LNG demand is surging, particularly in power generation and data center applications. According to the Energy Information Administration, U.S. LNG exports are projected to reach 12.2 billion cubic feet per day in 2024 and 14.3 billion cubic feet per day in 2025, up from a record 11.9 billion cubic feet per day in 2023. This growth trajectory presents a significant opportunity for Honeywell to capitalize on the increasing global appetite for cleaner energy sources.

By acquiring Air Products’ LNG unit, Honeywell gains access to cutting-edge technologies such as heat exchangers and cryogenic equipment, which complement its existing LNG pretreatment business. The addition of Air Products’ coil-wound heat exchangers, known for their efficient liquefaction capabilities and minimal space requirements, will enhance Honeywell’s competitive edge in both onshore and offshore LNG applications.

From an investor’s perspective, this acquisition aligns perfectly with Honeywell’s strategic focus on three “mega trends” identified by CEO Vimal Kapur: automation, the future of aviation, and energy transition. The LNG business acquisition squarely addresses the energy transition pillar, potentially opening up new revenue streams and market opportunities for the company.

Financially, the deal is expected to be accretive to Honeywell’s adjusted earnings per share in the first full year of ownership. Analyst Sheila Kahyaoglu from Jefferies estimates that the transaction could boost adjusted earnings by approximately 1% in 2025. Moreover, Honeywell anticipates growth opportunities in aftermarket services and digitalization through its Forge platform, which could further enhance the deal’s long-term value proposition.

The acquisition also demonstrates Honeywell’s commitment to growth through strategic M&A activity. With this latest deal, the company is on track to deploy around $15 billion in acquisitions in 2024 alone, a clear indication of its aggressive growth strategy and confidence in its ability to integrate and leverage new technologies and market positions.

For investors, Honeywell’s move into the LNG space offers exposure to a critical segment of the energy transition. As countries worldwide seek to reduce their carbon footprint while ensuring energy security, LNG is increasingly seen as a crucial “bridge fuel” in the shift from coal to renewables. Honeywell’s enhanced capabilities in LNG technology position it to benefit from this global trend.

However, investors should also consider the potential risks. The LNG market can be volatile, subject to geopolitical tensions and fluctuations in global energy demand. Additionally, the success of the acquisition will depend on Honeywell’s ability to effectively integrate Air Products’ LNG business and leverage its technologies across its existing customer base.

Honeywell’s $1.81 billion acquisition of Air Products’ LNG business represents a strategic bet on the future of energy. This move positions the company as a more comprehensive player in the LNG value chain, potentially opening up new revenue streams and market opportunities. For investors seeking exposure to the energy transition trend through a diversified industrial giant, this deal enhances Honeywell’s appeal. The company’s ability to integrate this acquisition effectively and leverage its new technologies across its existing customer base will be crucial to realizing the full value of this investment. As Honeywell continues to align itself with key technological and market trends, investors should closely monitor how this strategic move contributes to the company’s long-term growth trajectory and its role in shaping the evolving global energy landscape.

CHATHAM, N.J., July 10, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully-integrated biopharmaceutical company, today announced the closing of its public offering of 3,393,600 shares of its common stock and pre-funded warrants to purchase up to 3,703,140 shares of common stock in a public offering at an offering price of $0.57 per share of common stock and $0.569 per pre-funded warrant. The warrants have an exercise price of $0.001 per share and became exercisable upon issuance.

The gross proceeds of the offering are $4.0 million before deducting placement agent fees and other estimated offering expenses payable by the Company. The Company intends to use the net proceeds from the offering for working capital and general corporate purposes, including the preparation of the new drug application relating to its Tonmya™ product candidate in patients with fibromyalgia, and the satisfaction of any portion of its existing indebtedness.

Dawson James Securities, Inc. acted as the sole placement agent for the offering.

Lowenstein Sandler, New York, NY, represented the Company in connection with the offering, and ArentFox Schiff LLP, Washington, DC, represented the placement agent.

This offering was made pursuant to an effective shelf registration statement on Form S-3 (File No. 333-266982) previously filed with the U.S. Securities and Exchange Commission (the “SEC”). The offering was made only by means of a prospectus supplement and accompanying prospectus. A final prospectus supplement and accompanying prospectus describing the terms of the proposed offering were filed with the SEC and are available on the SEC’s website located at http://www.sec.gov. Electronic copies of the preliminary prospectus supplement may be obtained from Dawson James Securities, Inc., 101 North Federal Highway, Suite 600, Boca Raton, FL 33432 or by telephone at (561) 391-5555, or by email at investmentbanking@dawsonjames.com.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a fully-integrated biopharmaceutical company focused on developing, licensing and commercializing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s development portfolio is focused on central nervous system (CNS) disorders. Tonix’s priority is to submit a New Drug Application (NDA) to the FDA in the second half of 2024 for Tonmya1, a product candidate for which two statistically significant Phase 3 studies have been completed for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction as well as fibromyalgia-type Long COVID. Tonix’s CNS portfolio includes TNX-1300 (cocaine esterase), a biologic designed to treat cocaine intoxication that has Breakthrough Therapy designation. Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix also has product candidates in development in the areas of rare disease and infectious disease. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

1Tonmya™ is conditionally accepted by the U.S. Food and Drug Administration (FDA) as the tradename for TNX-102 SL for the management of fibromyalgia. Tonmya has not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the intended use of proceeds from the public offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 1, 2024, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Company builds on 38-year history of providing innovative Medicaid management solutions to Montana Department of Public Health and Human Services

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-led business solutions and services company, today announced a three-year Pharmacy Benefit Management (PBM) contract renewal with the Montana Department of Public Health and Human Services (MDPHHS). The renewal builds on Conduent’s nearly 38-year relationship with the MDPHHS of providing advanced Medicaid management solutions to further the agency’s mission to deliver healthcare services that help improve and protect the health and safety of Montanans.

As part of the Conduent Medicaid Suite (CMdS), the pharmacy module helps MDPHHS reduce costs and streamline operations within its PBM model with advanced applications for point of sale, prior authorization, rebate, data analytics, consumer relationship management and prospective and retrospective drug review functions. Conduent will also continue to provide medical authorization, precertification, payment method development and inpatient call center services.

The company’s comprehensive PBM system was among the first to be certified in the state of Montana and the first instance of an individual Medicaid management module to earn federal certification.

“Our successful, long-term relationship with Montana reflects our commitment to providing effective solutions and on-going innovations that enable the Montana Department of Public Health and Human Services to continue to manage pharmacy benefits with transparency and cost-effectiveness,” said Lydie Quebe, General Manager, Government Healthcare Solutions at Conduent.

In addition to supporting pharmacy benefit management and claims processing, Conduent provides a range of government solutions including Medicaid enrollment and eligibility support, critical payment disbursement solutions, and child support solutions. The company supports approximately 41 million residents across various government health programs. Visit Conduent Government Healthcare Solutions to learn more.

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 59,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $100 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com.

Trademarks Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

– Patients preferred OLC more than 4 to 1 over their prior phosphate binder therapy –

– Median daily pill burden reduced by half after switch to OLC –

LOS ALTOS, Calif., July 10, 2024 (GLOBE NEWSWIRE) — Unicycive Therapeutics, Inc. (Nasdaq: UNCY), a clinical-stage biotechnology company developing therapies for patients with kidney disease (the “Company” or “Unicycive”), today announced the initial results from the patient reported outcome survey conducted during the UNI-OLC-201 pivotal clinical trial. The positive top-line results from the oxylanthanum carbonate (OLC) trial in patients with hyperphosphatemia who have chronic kidney disease on dialysis were reported on June 25, 2024.

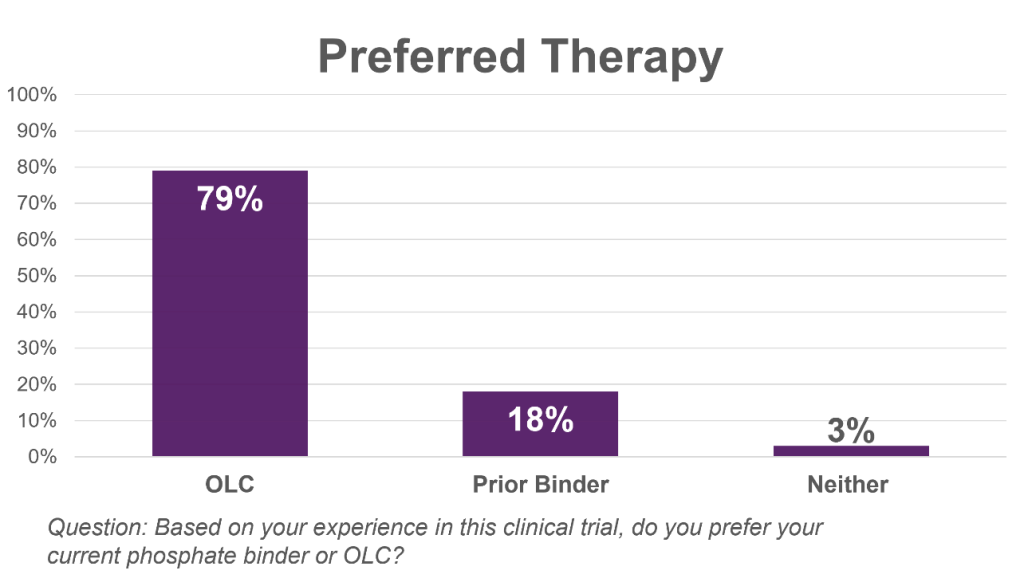

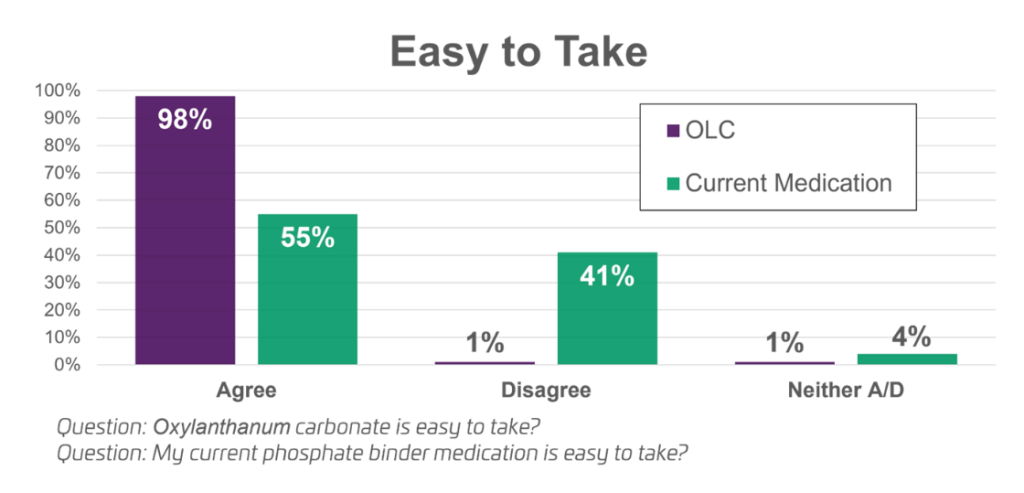

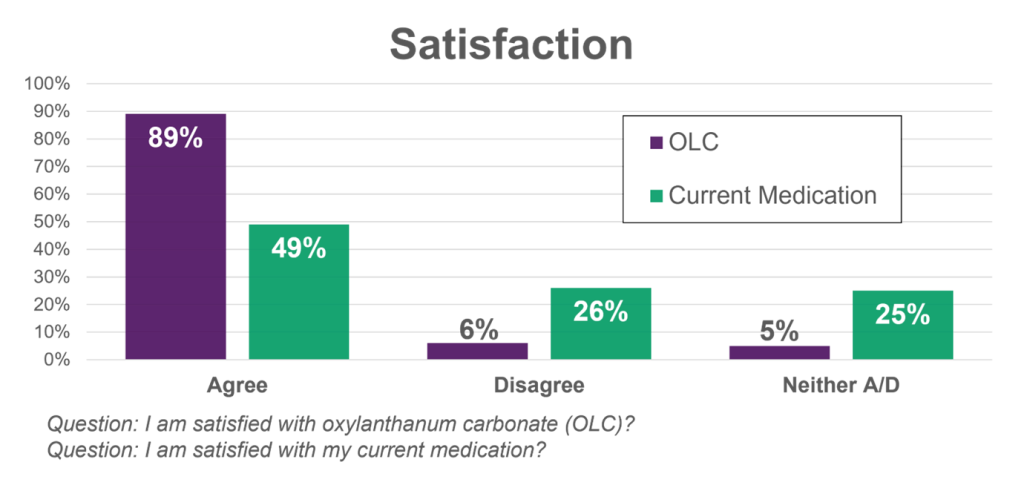

The patient reported outcomes are being evaluated from a satisfaction questionnaire that was a pre-specified exploratory objective of the study. The questionnaire surveyed patients in the UNI-OLC-201 trial to assess characteristics of their current phosphate binder as compared to OLC after switching medications. The questions included patient satisfaction, ease of use, and preferred therapy and were taken at the start and conclusion of the study. In the survey, OLC consistently outperformed the other phosphate binders in all categories: 79% of patients preferred OLC while 18% preferred their prior therapy, 98% of patients said that OLC was easy to take compared to 55% for their prior therapy, 89% of patients said they were satisfied with OLC while 49% were satisfied with their prior therapy.

“We are gratified by the encouraging patient reported findings from our pivotal trial that mirror the better-than-expected topline clinical results that we reported last month,” said, Shalabh Gupta, MD, Chief Executive Officer of Unicycive. “In the design of our pivotal clinical trial for OLC, we believed that it was important to consider the patient perspective and the personal challenges that they face in managing their hyperphosphatemia. Importantly, the results showed that patients preferred OLC greater than 4 to 1 over their prior phosphate binder therapy. Our focus is now directed toward filing our New Drug Application and making OLC available to patients who may benefit from its potential best-in-class profile, if approved.”

Pablo Pergola, MD, PhD, Research Director, Clinical Advancement Center, Renal Associates, P.A., and principal investigator for the UNI-OLC-201 trial, commented, “In this clinical study, our patients stated a clear preference for OLC over their prior phosphate lowering therapies. This positive patient reported experience with OLC is encouraging because hyperphosphatemia outcomes are often negatively impacted by non-adherence to phosphate lowering prescriptions due to side effects and high pill burden. At the end of the study, several of my patients asked not to be put back on their prior phosphate binder.”

Background

Patients screened to enter the trial were taking the following phosphate binder therapies (n=128): 52% Renvela® (sevelamer carbonate), 19% PhosLo® (calcium acetate, 15% Auryxia® (ferric citrate), 13% Velphoro® (sucroferric oxyhydroxide, and 1% Other. Once patients were enrolled into the trial, they went through a washout period for two weeks to clear their current phosphate binder from the body.

Key Findings

Preferred Therapy: In response to the question: Based on your experience in this clinical trial, do you prefer your current phosphate binder or OLC, 79% preferred OLC, 18% preferred their prior phosphate binder, and 3% preferred neither.

Ease of Use: In the trial, the median patient pill burden on OLC was reduced by half compared to their prior phosphate binder therapy. The pill burden on prior therapy at screening was a median of 6 (mean 6.5) pills per day. On OLC, the pill burden at the end of the study was a median of 3 (mean 3.9) pills per day.

In response to the question: My current phosphate binding medication is easy to take, 55% of patients agreed, 41% disagreed, and 4% neither agreed nor disagreed. In response to the question: Oxylanthanum carbonate (OLC) is easy to take, 98% of patients agreed, 1% disagreed, and 1% neither agreed nor disagreed.

Patient Satisfaction: At screening, less than half of the patients in the study agreed with the statement, I am satisfied with my current phosphate binder medication. At the end of the study and after switching to OLC, 89% of patients agreed with the statement, I am satisfied with oxylanthanum carbonate. Only 6% expressed dissatisfaction with OLC.

The initial findings from the Oxylanthanum carbonate (OLC) pivotal trial satisfaction questionnaire are preliminary and subject to change based on further detailed analysis. Full survey results are expected to be presented at a future medical conference.

About Oxylanthanum Carbonate (OLC)

Oxylanthanum carbonate is a next-generation lanthanum-based phosphate binding agent utilizing proprietary nanoparticle technology being developed for the treatment of hyperphosphatemia in patients with chronic kidney disease (CKD). OLC has over forty issued and granted patents globally. Its potential best-in-class profile may have meaningful patient adherence benefits over currently available treatment options as it requires a lower pill burden for patients in terms of number and size of pills per dose that are swallowed instead of chewed. Based on a survey conducted in 2022, Nephrologists stated that the greatest unmet need in the treatment of hyperphosphatemia with phosphate binders is a lower pill burden and better patient compliance.1 The global market opportunity for treating hyperphosphatemia is projected to be in excess of $2.5 billion in 2023, with the United States accounting for more than $1 billion of that total. Despite the availability of several FDA-cleared medications, 75 percent of U.S. dialysis patients fail to achieve the target phosphorus levels recommended by published medical guidelines.

Unicycive is seeking FDA approval of OLC via the 505(b)(2) regulatory pathway. As part of the clinical development program, two clinical studies were conducted in over 100 healthy volunteers. The first study was a dose-ranging Phase I study to determine safety and tolerability. The second study was a randomized, open-label, two-way crossover bioequivalence study to establish pharmacodynamic bioequivalence between OLC and Fosrenol. Based on the results of the bioequivalence study, pharmacodynamic (PD) bioequivalence of OLC to Fosrenol was established. A pivotal clinical trial was also conducted in CKD patients on hemodialysis that achieved the study objective and established favorable tolerability of OLC at clinically effective doses.

About Hyperphosphatemia

Hyperphosphatemia is a serious medical condition that occurs in nearly all patients with End Stage Renal Disease (ESRD). If left untreated, hyperphosphatemia leads to secondary hyperparathyroidism (SHPT), which then results in renal osteodystrophy (a condition similar to osteoporosis and associated with significant bone disease, fractures and bone pain); cardiovascular disease with associated hardening of arteries and atherosclerosis (due to deposition of excess calcium-phosphorus complexes in soft tissue). Importantly, hyperphosphatemia is independently associated with increased mortality for patients with chronic kidney disease on dialysis. Based on available clinical data to date, over 80% of patients show signs of cardiovascular calcification by the time they become dependent on dialysis.

Dialysis patients are already at an increased risk for cardiovascular disease (because of underlying diseases such as diabetes and hypertension), and hyperphosphatemia further exacerbates this. Treatment of hyperphosphatemia is aimed at lowering serum phosphate levels via two means: (1) restricting dietary phosphorus intake; and (2) using, on a daily basis, and with each meal, oral phosphate binding drugs that facilitate fecal elimination of dietary phosphate rather than its absorption from the gastrointestinal tract into the bloodstream.

About Unicycive Therapeutics

Unicycive Therapeutics is a biotechnology company developing novel treatments for kidney diseases. Unicycive’s lead drug candidate, oxylanthanum carbonate (OLC), is a novel investigational phosphate binding agent being developed for the treatment of hyperphosphatemia in chronic kidney disease patients on dialysis. UNI-494 is a patent-protected new chemical entity in clinical development for the treatment of conditions related to acute kidney injury. For more information, please visit Unicycive.com and follow us on LinkedIn, X, and YouTube.

Forward-looking statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified using words such as “anticipate,” “believe,” “forecast,” “estimated” and “intend” or other similar terms or expressions that concern Unicycive’s expectations, strategy, plans or intentions. These forward-looking statements are based on Unicycive’s current expectations and actual results could differ materially. There are several factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, clinical trials involve a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results; our clinical trials may be suspended or discontinued due to unexpected side effects or other safety risks that could preclude approval of our product candidates; risks related to business interruptions, which could seriously harm our financial condition and increase our costs and expenses; dependence on key personnel; substantial competition; uncertainties of patent protection and litigation; dependence upon third parties; and risks related to failure to obtain FDA clearances or approvals and noncompliance with FDA regulations. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including: the uncertainties related to market conditions and other factors described more fully in the section entitled ‘Risk Factors’ in Unicycive’s Annual Report on Form 10-K for the year ended December 31, 2023, and other periodic reports filed with the Securities and Exchange Commission. Any forward-looking statements contained in this press release speak only as of the date hereof, and Unicycive specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise.

Renvela®️ is a registered trademark of Sanofi. Phoslo®️ and Velphoro®️ are registered trademarks of Vifor Fresenius Auryxia®️ is a registered trademark of Akebia Therapeutics Fosrenol®️ is a registered trademark of Takeda Pharmaceutical Company Limited 1Reason Research, LLC 2022 survey. Results here.

Investor Contact: ir@unicycive.com (650) 543-5470 SOURCE: Unicycive Therapeutics, Inc.

Earnings Release Scheduled for Wednesday, August 7, 2024 Before the Market Opens

Conference Call Scheduled for Wednesday, August 7, 2024 at 11:00 AM (Eastern Time)

BOCA RATON, Fla.–(BUSINESS WIRE)–Jul. 9, 2024– The GEO Group, Inc. (NYSE:GEO) (“GEO”) will release its second quarter 2024 financial results on Wednesday, August 7, 2024 before the market opens. GEO has scheduled a conference call and simultaneous webcast for 11:00 AM (Eastern Time) on Wednesday, August 7, 2024.

Hosting the call for GEO will be George C. Zoley, Executive Chairman of the Board, Brian R. Evans, Chief Executive Officer, Mark Suchinski, Chief Financial Officer, Wayne Calabrese, President and Chief Operating Officer, and James Black, President, GEO Secure Services.

To participate in the teleconference, please contact one of the following numbers 5 minutes prior to the scheduled start time:

In addition, a live audio webcast of the conference call may be accessed on the Webcasts section of GEO’s investor relations home page at investors.geogroup.com. A webcast replay will remain available on the website for one year.

A telephonic replay will also be available through August 14, 2024. The replay numbers are 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The passcode for the telephonic replay is 4116450. If you have any questions, please contact GEO at 1-866-301-4436.

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel therapies and vaccines for solid tumor cancers and many of the world’s most threatening infectious diseases. The company’s lead program in oncology is a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, presently in a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax’s lead infectious disease candidate is GEO-CM04S1, a next-generation COVID-19 vaccine targeting high-risk immunocompromised patient populations. Currently in three Phase 2 clinical trials, GEO-CM04S1 is being evaluated as a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, and as a booster vaccine in patients with chronic lymphocytic leukemia (CLL). In addition, GEO-CM04S1 is in a Phase 2 clinical trial evaluating the vaccine as a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. GeoVax has a leadership team who have driven significant value creation across multiple life science companies over the past several decades.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

GeoVax Reached Important Milestones For Both Platforms During 1H2024. The first half of 2024 has been a transformational period for GeoVax. A Phase 2 trial testing CM04S1 as a booster vaccine for COVID-19 reported initial data in February, then received a BARDA grant to conduct a large Phase 2b in June. The Gedeptin gene therapy program in head and neck cancer reported interim Phase 1/2 data showing successful proof-of-concept. Both programs are moving forward with additional milestones in 2H24.

BARDA Grant Allocates $367 Million For A Phase 2b Trial. In June, GeoVax announced that it has received a grant from BARDA to conduct a Phase 2b trial testing CM04S1 as a booster vaccine to protect healthy patients from COVID-19. As discussed in our Research Note on June 28, the grant terms include payments to GeoVax for clinical supplies and regulatory costs of $24.3 million (which could be increased to $45 million). The balance will be payable to Allucent, the CRO that will conduct the trial.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

M/V Joanna charter. Euroseas Ltd. executed a new time charter contract for its 1,732 twenty-foot equivalent (teu) feeder containership, M/V Joanna, for a minimum period of 23 months to a maximum period of 25 months at an average gross daily rate of $16,500. The rate is higher than its current charter rate of $13,500 per day which ends in August. The charter for M/V Joanna will commence at the end of October 2024. The charter is expected to contribute EBITDA of ~$6.4 million during the minimum contracted period and increases the company’s remaining 2024 and 2025 charter coverage to 92% and 40%, respectively.

M/V Pepi Star charter. The company executed a time charter contract for the M/V Pepi Star, an 1,800 teu feeder containership currently under construction, for a minimum period of 23 to a maximum period of 25 months at a gross daily rate of $24,250. The time charter contract rate is higher than what we had previously forecast. The new charter will commence in mid-July upon delivery of the vessel from the shipyard. The charter is expected to contribute EBITDA in the amount of ~$12.3 million during the minimum contracted period.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Model Updates. We updated our model to reflect the upcoming loss of the South Texas contract in mid-August. While a significant loss, we believe the ongoing increase in ICE detainees elsewhere could help soften the South Texas blow and we remain hopeful additional state and local contracts could be signed.

Details. As a reminder, South Texas generates approximately $40 million in quarterly revenue and generates approximately $0.10 per share in quarterly EPS. We assumed half of a quarter impact for 3Q24 and a full quarter impact in 4Q24. We kept the majority of the rest of the model consistent, although there may be some cost savings initiatives CoreCivic is able to put in place. We held our 2Q24 estimates the same.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

As Tesla continues to dominate headlines with its electric vehicles and ambitious plans for autonomous driving, a less-discussed segment of the company is quietly becoming a potential game-changer. Tesla’s energy business, particularly its energy storage division, is showing signs of becoming a major contributor to the company’s bottom line and future growth prospects.

In a recent production and delivery report, Tesla revealed that it had deployed a record-breaking 9.4 GWh (gigawatt hours) of battery energy storage in the second quarter of 2024. This figure represents more than double the amount deployed in the first quarter, signaling explosive growth in this sector.

Tesla’s energy storage solutions range from residential Powerwall units to utility-scale Megapack installations. A single Powerwall can store enough energy to power a small home for a day, while a Megapack installation boasts the capacity to provide electricity to 3,600 homes for an hour. This scalability allows Tesla to cater to a wide range of customers, from individual homeowners to large utility companies and municipalities.

The financial performance of Tesla’s energy business is equally impressive. In the first quarter of 2024, the segment generated $1.6 billion in revenue and $403 million in gross profit. What’s particularly noteworthy is the gross margin of 24.6%, significantly higher than Tesla’s overall gross margin of 17.4% for the same period. This robust profitability comes at a crucial time for Tesla, as its automotive business faces margin pressure due to recent price cuts aimed at stimulating demand.

Wall Street is taking notice of this shift. Adam Jonas, an analyst at Morgan Stanley, dubbed the Q2 energy deployment figures a “show stealer” and valued Tesla Energy at $36 per Tesla share, or approximately $130 billion. This valuation suggests that the energy business could be a substantial component of Tesla’s market capitalization in the future.

The growth potential for Tesla’s energy storage business is closely tied to broader technological and infrastructure trends. The increasing adoption of artificial intelligence and the subsequent need for more data centers are expected to drive a “multigenerational increase in energy demand,” according to Jonas. This surge in electricity needs, coupled with the ongoing transition to renewable energy sources, positions Tesla’s energy storage solutions as a critical component of future power grids.

Moreover, the Inflation Reduction Act in the United States is likely to accelerate investments in grid infrastructure, potentially creating more opportunities for Tesla’s energy products. As utilities and businesses look to modernize and stabilize the power grid, Tesla’s Megapack installations could play a crucial role in load balancing and ensuring reliable power supply.

While much of the investor focus has been on Tesla’s automotive innovations, including the anticipated launch of a lower-priced electric vehicle and the reveal of its robotaxi concept, the energy business could provide a significant upside surprise in upcoming earnings reports. This diversification of revenue streams may also help to stabilize Tesla’s financial performance, reducing its reliance on the cyclical automotive market.

It’s worth noting that Tesla’s energy business isn’t limited to storage solutions. The company also produces solar roof tiles and conventional solar panels, although these products have received less attention in recent years. As the energy storage business continues to grow, it may create synergies with Tesla’s solar products, offering customers comprehensive energy solutions.

As we approach Tesla’s Q2 earnings report in July 2024, investors and analysts will be keenly watching the performance of the energy storage segment. If the strong deployment figures translate into substantial revenue and profit growth, it could mark a turning point in how the market perceives Tesla – not just as an automaker, but as a diversified energy and technology company.

In conclusion, Tesla’s energy storage business is emerging as a powerful growth driver for the company. With its impressive profit margins, scalable solutions, and alignment with global energy trends, this segment could play a crucial role in Tesla’s future success and valuation. As the world continues its transition to sustainable energy, Tesla appears well-positioned to capitalize on the growing demand for advanced energy storage solutions.