Research News and Market Data on TNXP

March 12, 2026 5:30pm EDTDownload as PDF

Related Documents

TONMYA™ (cyclobenzaprine HCl sublingual tablets) launched November 17, 2025, for the treatment of fibromyalgia; through February 27, 2026, more than 1,500 healthcare providers have prescribed TONMYA to patients, approximately 2,500 patients have initiated treatment with TONMYA, and cumulative prescriptions totaled approximately 4,200

Expect to initiate U.S. field study in 2027 for TNX-4800 for seasonal prevention of Lyme disease pending FDA clearance

Completed $20.0 million registered direct offering with Point72 on December 29, 2025

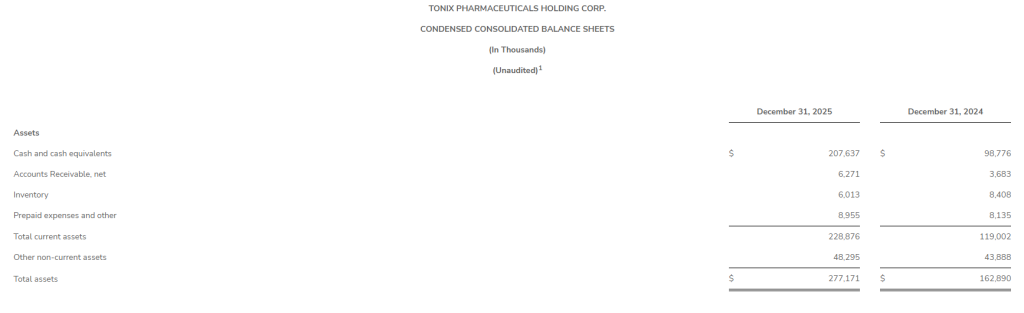

Approximately $207.6 million in cash and cash equivalents as of December 31, 2025

BERKELEY HEIGHTS, N.J., March 12, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully integrated, commercial biotechnology company, today announced financial results for the fourth quarter and full year ended December 31, 2025, and provided an overview of recent operational highlights.

“2025 was transformational for Tonix as we achieved FDA approval and began the U.S. commercial launch of TONMYA, our first fully in-house developed product and the first new medicine approved for fibromyalgia in more than 15 years,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “TONMYA is a non-opioid analgesic designed for long-term, once-daily bedtime dosing. We believe TONMYA now provides an alternative medicine for the approximately 10 million adults in the U.S. who suffer from fibromyalgia. We have the capabilities to engage healthcare providers and patients, having launched the product and an approximately 90-member salesforce. Early prescription trends reflect favorable prescriber uptake and repeat utilization consistent with our internal launch expectations. Our experienced commercial team is committed to growing awareness and adoption, facilitating patient access, and obtaining payer coverage as we strive to improve the fibromyalgia journey for patients and healthcare providers.”

Dr. Lederman continued, “We also meaningfully advanced our robust clinical pipeline in 2025. Tonix in-licensed TNX-4800, a long-acting human monoclonal antibody for the seasonal prevention of Lyme disease, for which there are no FDA-approved vaccines or prophylactics. This program, developed by researchers at UMass Chan Medical School, anchors our clinical-stage infectious disease pipeline, and we plan to discuss Phase 2/3 development with the FDA this year. An additional highlight includes FDA clearance of the Investigational New Drug application (IND) for HORIZON, a potentially pivotal Phase 2 study of TNX-102 SL (cyclobenzaprine HCl sublingual tablets) in major depressive disorder, which is expected to initiate enrollment in mid-2026. Looking ahead, our priorities are clear. We are driven to continue our momentum in 2026 as we focus on the successful commercialization of TONMYA, pipeline progress, and sustainable long-term value for patients and shareholders.”

Commercial Updates

TONMYA (cyclobenzaprine HCl sublingual tablets): a centrally acting, non-opioid analgesic for the treatment of fibromyalgia in adults

- In August 2025, the U.S. FDA approved TONMYA for the treatment of fibromyalgia in adults, making it the first new prescription medicine approved for this indication in more than 15 years. The approval was based on two double-blind, randomized, placebo-controlled Phase 3 clinical trials of nearly 1,000 patients that demonstrated statistically significant reduction in daily pain scores compared to placebo.

- On November 17, 2025, TONMYA became commercially available at pharmacies by prescription in the U.S. Approximately 90 sales representatives were deployed in the field in advance of the launch. Early prescription trends reflect favorable adoption rates by prescribers and patients, with prescription volumes increasing each full month post launch. Launch metrics for the period November 17, 2025–February 27, 2026 (launch-to-date), are as follows:

- More than 1,500 healthcare providers have prescribed TONMYA to patients.

- Approximately 2,500 patients have initiated treatment with TONMYA.

- Cumulative prescriptions totaled approximately 4,200. This includes bridge prescriptions that are facilitated through the Company’s specialty pharmacy channel. Bridge prescriptions represent initial patient fills provided while coverage determinations are pending and do not immediately generate net product revenue.

- The Company has contracted with existing wholesalers and specialty pharmacies for distribution and with companies to assist with prescription fulfillment and patient access. Tonix also has a robust patient access program and support services in place, including TONMYA savings card, copay assistance, and prior authorization support, intended to reduce access barriers during early commercialization.

- The Company is prioritizing expanding payer engagement and establishing contracts with commercial payers, while also progressing discussions with Medicare and Medicaid.

Key Product Pipeline Candidates: Recent Highlights

Infectious Disease Pipeline

TNX-4800 (anti-OspA mAb): long-acting human monoclonal antibody in development for the seasonal prevention of Lyme disease, which has no FDA-approved vaccines or prophylactics

- In December 2025, Tonix announced plans to meet with the FDA in 2026 to explore Phase 2/3 development options, including a Phase 2 field study and a Phase 2 controlled human infection model (CHIM) study, which is also called a human challenge study. The Company expects to have GMP investigational product available for clinical testing in early 2027. Pending FDA clearances, the field study is expected to initiate enrollment in 2027 and the CHIM study in 2028.

Central Nervous System (CNS) Pipeline

TNX-102 SL (cyclobenzaprine HCl sublingual tablets): in development for major depressive disorder (MDD)

- In November 2025, the FDA cleared the IND for TNX-102 SL 5.6 mg for the treatment of MDD in adults. The IND clearance enables Tonix to proceed with the HORIZON study, a potentially pivotal Phase 2, 6-week, randomized, double-blind, placebo-controlled study of TNX-102 SL as a first-line monotherapy in adults with MDD. About 360 patients will be enrolled at approximately 30 U.S. sites, with the primary endpoint being the MADRS total score change from baseline at Week 6. Tonix plans to initiate enrollment in mid-2026.

- Prior studies of TNX-102 SL in fibromyalgia and post-traumatic stress disorder (PTSD) showed promising signals for improvement of depressive symptoms. TNX-102 SL treatment has been associated with a low incidence of side effects common with traditional antidepressants, including weight gain, blood pressure changes, sexual dysfunction, and cognitive issues.

TNX-102 SL for the treatment of acute stress reaction (ASR) and acute stress disorder (ASD), and prophylaxis against development of PTSD

- The U.S. Department of Defense-funded Optimizing Acute Stress Reaction Interventions (OASIS) trial is being conducted by the University of North Carolina under an investigator-initiated IND application. The OASIS trial examines the safety and efficacy of TNX-102 SL to reduce adverse posttraumatic neuropsychiatric sequelae among patients in the emergency department after a motor vehicle collision. Topline data is expected to be reported in the second half of 2026.

Immunology Pipeline

TNX-1500 (dimeric Fc modified anti-CD40L, humanized monoclonal antibody): third generation anti-CD40L for prophylaxis of kidney transplant rejection and treatment of autoimmune disorders

- In November 2025, Tonix announced a collaboration with Massachusetts General Hospital to advance a Phase 2 open-label, investigator-initiated clinical trial of TNX-1500 in kidney transplant recipients, planned for initiation mid-year 2026 pending FDA clearance of the IND. The study is expected to enroll five adult kidney transplant recipients.

- In October 2025, Tonix presented an update at the Japan Society for Transplantation annual congress, highlighting Phase 1 safety and pharmacokinetic and pharmacodynamic results and outlining next steps toward Phase 2 evaluation in allogenic kidney transplantation.

Rare Disease Pipeline

TNX-2900 (intranasal potentiated oxytocin): in development for Prader-Willi syndrome, with Orphan Drug designation as well as Rare Pediatric Disease designation that could make Tonix eligible for a Priority Review Voucher upon approval

- In September 2025, Tonix announced plans to initiate a Phase 2, randomized, double-blind, placebo-controlled trial in children and adolescents with Prader-Willi syndrome. The study is expected to initiate in the first quarter of 2027.

Financial: Recent Highlights

Tonix had approximately $207.6 million of cash and cash equivalents as of December 31, 2025, compared to approximately $98.8 million as of December 31, 2024. Net cash used in operations was approximately $99.8 million for the full year ended December 31, 2025, compared to $60.9 million for the same period in 2024. Cash paid for capital expenditures for the full year ended December 31, 2025, were approximately $3.4 million compared to $0.1 million for the same period in 2024.

In December 2025, Tonix completed a $20.0 million registered direct offering with Point72 Asset Management. The net proceeds are being used to fund commercialization of marketed products, pipeline development, and general working capital. TD Cowen acted as sole placement agent for the offering. A.G.P./Alliance Global Partners acted as a financial advisor.

Subsequent to year-end, the Company has raised $8.6 million proceeds using its at-the-market (ATM) facility.

The Company believes that its cash resources at December 31, 2025, will meet its planned operating and capital expenditure requirements into the first quarter of 2027.

As of March 11, 2026, the Company had 13,405,401 shares of common stock outstanding.

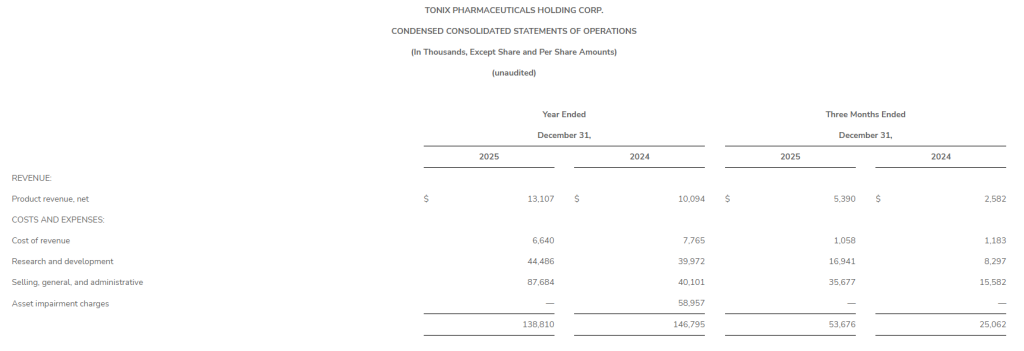

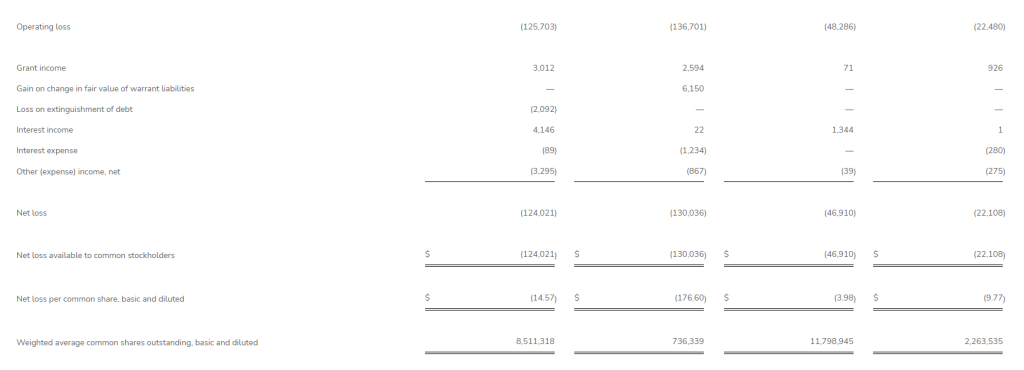

Full Year 2025 Financial Results

Net product revenue for the full year 2025 was approximately $13.1 million, compared to $10.1 million in 2024. Net revenue from sales of Zembrace®, SymTouch®, and Tosymra® for the full year 2025 was approximately $11.7 million, compared to $10.1 million in 2024. Net revenue from sales of TONMYA for the period from launch on November 17, 2025, to December 31, 2025, was approximately $1.4 million. Cost of sales for the full year 2025 was approximately $6.6 million, compared to $7.8 million in 2024.

Research and development expenses for the full year 2025 were approximately $44.5 million, compared to $40.0 million in 2024. This increase is predominately due to pipeline prioritization period over period, and increased headcount.

Selling, general, and administrative expenses for the full year 2025 were $87.7 million, compared to $40.1 million in 2024. The increase is predominately due to spending on sales and marketing related to TONMYA as well as increased headcount.

Net loss available to common stockholders was approximately $124.0 million, or $14.57 per basic and diluted share, for the full year 2025, compared to net loss available to common stockholders of $130.0 million, or $176.60 per basic and diluted share, in 2024. The basic and diluted weighted average common shares outstanding for the full year 2025 was 8,511,318 compared to 736,339 shares for 2024.

Fourth Quarter 2025 Financial Results

Net product revenue for the fourth quarter 2025 was approximately $5.4 million, compared to $2.6 million for the same period in 2024, and consisted of combined net sales of TONMYA™, Zembrace® SymTouch®, and Tosymra®. Cost of sales for the fourth quarter 2025 was approximately $1.1 million, compared to $1.2 million for the same period in 2024.

Research and development expenses for the fourth quarter 2025 were approximately $16.9 million, compared to $8.3 million for the same period in 2024. This increase is predominately due to pipeline prioritization period over period and increased headcount.

Selling, general, and administrative expenses for the fourth quarter 2025 were $35.7 million, compared to $15.6 million for the same period in 2024. The increase is predominately due to spending on sales and marketing related to TONMYA and increased headcount.

Net loss available to common stockholders was $46.9 million, or $3.98 per basic and diluted share, for the fourth quarter 2025, compared to net loss available to common stockholders of $22.1 million, or $9.77 per basic and diluted share, for the same period in 2024. The basic and diluted weighted average common shares outstanding for the fourth quarter 2025 was 11,798,945 compared to 2,263,535 shares for the same period in 2024.

Tonix Pharmaceuticals Holding Corp.

Tonix Pharmaceuticals* is a fully-integrated, commercial-stage biotechnology company focused on central nervous system (CNS) and immunology treatments in areas of high unmet medical need. TONMYATM (cyclobenzaprine HCl sublingual tablets 2.8mg), the Company’s recently approved flagship medicine, is the first new treatment for fibromyalgia in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® and Tosymra®. Tonix is maximizing the science behind TONMYA in Phase 2 clinical trials to evaluate its potential in major depressive disorder and acute stress disorder. In addition, the Company’s CNS portfolio includes TNX-2900, which is Phase 2 ready for the treatment of Prader-Willi syndrome, a rare disease. Tonix is also advancing a pipeline of immunology programs, including monoclonal antibody TNX-4800 for Lyme disease prophylaxis and TNX-1500, a third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. To learn more, visit www.tonixpharma.com and follow the Company on LinkedIn and X.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. TONMYA is a trademark of Tonix Pharma Limited. All other marks are property of their respective owners.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the completion of the offering, the satisfaction of customary closing conditions, the intended use of proceeds from the offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially as a result of a number of factors, including the ability of the Company to satisfy the conditions to the closing of the offering and the timing thereof, as well as those described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on March 12, 2026, and periodic reports filed with the SEC on or after the date thereof. Tonix does not undertake an obligation to update or revise any forward-looking statement. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Investor Contacts

Jessica Morris

Tonix Pharmaceuticals

(862) 799-8599

investor.relations@tonixpharma.com

Brian Korb

astr partners

(917) 653-5122

brian.korb@astrpartners.com

Media Contacts

Deborah Elson

Tonix Pharmaceuticals

deborah.elson@tonixpharma.com

Ray Jordan

Putnam Insights

ray@putnaminsights.com

INDICATION

TONMYA is indicated for the treatment of fibromyalgia in adults.

CONTRAINDICATIONS

TONMYA is contraindicated:

In patients with hypersensitivity to cyclobenzaprine or any inactive ingredient in TONMYA. Hypersensitivity reactions may manifest as an anaphylactic reaction, urticaria, facial and/or tongue swelling, or pruritus. Discontinue TONMYA if a hypersensitivity reaction is suspected. With concomitant use of monoamine oxidase (MAO) inhibitors or within 14 days after discontinuation of an MAO inhibitor. Hyperpyretic crisis seizures and deaths have occurred in patients who received cyclobenzaprine (or structurally similar tricyclic antidepressants) concomitantly with MAO inhibitors drugs.

During the acute recovery phase of myocardial infarction, and in patients with arrhythmias, heart block or conduction disturbances, or congestive heart failure. In patients with hyperthyroidism.

WARNINGS AND PRECAUTIONS

Embryofetal toxicity: Based on animal data, TONMYA may cause neural tube defects when used two weeks prior to conception and during the first trimester of pregnancy. Advise females of reproductive potential of the potential risk and to use effective contraception during treatment and for two weeks after the final dose. Perform a pregnancy test prior to initiation of treatment with TONMYA to exclude use of TONMYA during the first trimester of pregnancy.

Serotonin syndrome: Concomitant use of TONMYA with selective serotonin reuptake inhibitors (SSRIs), serotonin norepinephrine reuptake inhibitors (SNRIs), tricyclic antidepressants, tramadol, bupropion, meperidine, verapamil, or MAO inhibitors increases the risk of serotonin syndrome, a potentially life-threatening condition. Serotonin syndrome symptoms may include mental status changes, autonomic instability, neuromuscular abnormalities, and/or gastrointestinal symptoms. Treatment with TONMYA and any concomitant serotonergic agent should be discontinued immediately if serotonin syndrome symptoms occur and supportive symptomatic treatment should be initiated. If concomitant treatment with TONMYA and other serotonergic drugs is clinically warranted, careful observation is advised, particularly during treatment initiation or dosage increases.

Tricyclic antidepressant-like adverse reactions: Cyclobenzaprine is structurally related to TCAs. TCAs have been reported to produce arrhythmias, sinus tachycardia, prolongation of the conduction time leading to myocardial infarction and stroke. If clinically significant central nervous system (CNS) symptoms develop, consider discontinuation of TONMYA. Caution should be used when TCAs are given to patients with a history of seizure disorder, because TCAs may lower the seizure threshold. Patients with a history of seizures should be monitored during TCA use to identify recurrence of seizures or an increase in the frequency of seizures.

Atropine-like effects: Use with caution in patients with a history of urinary retention, angle-closure glaucoma, increased intraocular pressure, and in patients taking anticholinergic drugs.

CNS depression and risk of operating a motor vehicle or hazardous machinery: TONMYA monotherapy may cause CNS depression. Concomitant use of TONMYA with alcohol, barbiturates, or other CNS depressants may increase the risk of CNS depression. Advise patients not to operate a motor vehicle or dangerous machinery until they are reasonably certain that TONMYA therapy will not adversely affect their ability to engage in such activities. Oral mucosal adverse reactions: In clinical studies with TONMYA, oral mucosal adverse reactions occurred more frequently in patients treated with TONMYA compared to placebo. Advise patients to moisten the mouth with sips of water before administration of TONMYA to reduce the risk of oral sensory changes (hypoesthesia). Consider discontinuation of TONMYA if severe reactions occur.

ADVERSE REACTIONS

The most common adverse reactions (incidence ≥2% and at a higher incidence in TONMYA-treated patients compared to placebo-treated patients) were oral hypoesthesia, oral discomfort, abnormal product taste, somnolence, oral paresthesia, oral pain, fatigue, dry mouth, and aphthous ulcer.

DRUG INTERACTIONS

MAO inhibitors: Life-threatening interactions may occur.

Other serotonergic drugs: Serotonin syndrome has been reported.

CNS depressants: CNS depressant effects of alcohol, barbiturates, and other CNS depressants may be enhanced.

Tramadol: Seizure risk may be enhanced.

Guanethidine or other similar acting drugs: The antihypertensive action of these drugs may be blocked.

USE IN SPECIFIC POPULATIONS

Pregnancy: Based on animal data, TONMYA may cause fetal harm when administered to a pregnant woman. The limited amount of available observational data on oral cyclobenzaprine use in pregnancy is of insufficient quality to inform a TONMYA-associated risk of major birth defects, miscarriage, or adverse maternal or fetal outcomes. Advise pregnant women about the potential risk to the fetus with maternal exposure to TONMYA and to avoid use of TONMYA two weeks prior to conception and through the first trimester of pregnancy. Report pregnancies to the Tonix Medicines, Inc., adverse-event reporting line at 1-888-869-7633 (1-888-TNXPMED).

Lactation: A small number of published cases report the transfer of cyclobenzaprine into human milk in low amounts, but these data cannot be confirmed. There are no data on the effects of cyclobenzaprine on a breastfed infant, or the effects on milk production. The developmental and health benefits of breastfeeding should be considered along with the mother’s clinical need for TONMYA and any potential adverse effects on the breastfed child from TONMYA or from the underlying maternal condition.

Pediatric use: The safety and effectiveness of TONMYA have not been established.

Geriatric patients: Of the total number of TONMYA-treated patients in the clinical trials in adult patients with fibromyalgia, none were 65 years of age and older. Clinical trials of TONMYA did not include sufficient numbers of patients 65 years of age and older to determine whether they respond differently from younger adult patients.

Hepatic impairment: The recommended dosage of TONMYA in patients with mild hepatic impairment (HI) (Child Pugh A) is 2.8 mg once daily at bedtime, lower than the recommended dosage in patients with normal hepatic function. The use of TONMYA is not recommended in patients with moderate HI (Child Pugh B) or severe HI (Child Pugh C). Cyclobenzaprine exposure (AUC) was increased in patients with mild HI and moderate HI compared to subjects with normal hepatic function, which may increase the risk of TONMYA-associated adverse reactions.

Please see additional safety information in the full Prescribing Information.

To report suspected adverse reactions, contact Tonix Medicines, Inc. at 1-888-869-7633, or the FDA at 1-800-FDA-1088 or www.fda.gov/medwatch.

Indication and Usage

Zembrace® SymTouch® (sumatriptan succinate) injection (Zembrace) and Tosymra® (sumatriptan) nasal spray are prescription medicines used to treat acute migraine headaches with or without aura in adults who have been diagnosed with migraine.

Zembrace and Tosymra are not used to prevent migraines. It is not known if Zembrace or Tosymra are safe and effective in children under 18 years of age.

Important Safety Information

Zembrace and Tosymra can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop use and get emergency help if you have any signs of a heart attack:

- discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

- severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

- pain or discomfort in your arms, back, neck, jaw or stomach

- shortness of breath with or without chest discomfort

- breaking out in a cold sweat

- nausea or vomiting

- feeling lightheaded

Zembrace and Tosymra are not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam shows no problem.

Do not use Zembrace or Tosymra if you have:

- history of heart problems

- narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

- uncontrolled high blood pressure

- hemiplegic or basilar migraines. If you are not sure if you have these, ask your provider.

- had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

- severe liver problems

- taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, or dihydroergotamine. Ask your provider for a list of these medicines if you are not sure.

- are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

- an allergy to sumatriptan or any of the components of Zembrace or Tosymra

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Zembrace and Tosymra can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Zembrace and Tosymra may cause serious side effects including:

- changes in color or sensation in your fingers and toes

- sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

- cramping and pain in your legs or hips; feeling of heaviness or tightness in your leg muscles; burning or aching pain in your feet or toes while resting; numbness, tingling, or weakness in your legs; cold feeling or color changes in one or both legs or feet

- increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

- medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

- serotonin syndrome, a rare but serious problem that can happen in people using Zembrace or Tosymra, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

- hives (itchy bumps); swelling of your tongue, mouth, or throat

- seizures even in people who have never had seizures before

The most common side effects of Zembrace and Tosymra include: pain and redness at injection site (Zembrace only); tingling or numbness in your fingers or toes; dizziness; warm, hot, burning feeling to your face (flushing); discomfort or stiffness in your neck; feeling weak, drowsy, or tired; application site (nasal) reactions (Tosymra only) and throat irritation (Tosymra only).

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Zembrace and Tosymra. For more information, ask your provider.

This is the most important information to know about Zembrace and Tosymra but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit https://www.tonixpharma.com or call 1-888-869-7633.

You are encouraged to report adverse effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

Source: Tonix Pharmaceuticals Holding Corp.

Released March 12, 2026