Novartis made a big move this week to expand its oncology portfolio, announcing plans to acquire German biotech MorphoSys in an all-cash deal valued at approximately $2.9 billion. The proposed acquisition continues Novartis’ strategy of striking deals and partnerships to enhance its drug development capabilities, especially in cancer.

Under the terms of the agreement, Novartis will pay $73 per share to purchase all outstanding ordinary shares of MorphoSys, representing a premium of 37% over the biotech’s closing price on February 3rd. The deal has been unanimously approved by MorphoSys’ board and is expected to close in the first half of 2024, pending regulatory and shareholder approval.

Driving Novartis’ interest is MorphoSys’ lead pipeline candidate pelabresib, an investigational BET inhibitor being studied for myelofibrosis. Myelofibrosis is a type of bone marrow cancer that disrupts the body’s normal production of blood cells.

Pelabresib is currently in the Phase 3 MANIFEST-2 trial in combination with Incyte’s Jakafi for first-line myelofibrosis patients. While the trial posted mixed results in November, Novartis believes the data support a regulatory submission in the second half of 2024. The pharma giant sees pelabresib as having potential to be a “practice changing” myelofibrosis treatment.

Beyond pelabresib, MorphoSys brings other early-stage oncology assets that could strengthen Novartis’ position in blood cancers. However, the crown jewel of MorphoSys’ portfolio – its approved non-Hodgkin’s lymphoma drug Monjuvi – is not included in the acquisition. Just before the Novartis deal was announced, MorphoSys sold the global rights to Monjuvi to Incyte for $1.5 billion.

Novartis has been actively hunting for new drug programs and technology platforms to replenish its pipeline as patents expire over the next decade on blockbuster brands like Cosentyx and Entresto. The patent cliff threatens over 50% of Novartis’ current sales.

In 2022, the pharma giant established a $1 billion fund to invest in startups focused on potentially transformational medicines. It has also been open to large M&A, as seen last year with the $20.7 billion purchase of gene therapy biotech The Medicines Company.

The MorphoSys deal reinforces Novartis’ commitment to growing its oncology division, which accounted for over 30% of total sales in 2023. Earlier this year, Novartis acquired the oncology biotech Calypso for $335 million upfront.

From an investor perspective, the MorphoSys acquisition provides Novartis with multiple shots on goal in blood cancers. If pelabresib hits, it could generate peak sales above $1 billion annually according to analysts. And with MorphoSys trading at multi-year lows, Novartis appears to have struck at an opportune time.

However, the mixed clinical data keeps pelabresib’s commercial prospects uncertain. And with most of MorphoSys’ value residing in the newly divested Monjuvi, it remains to be seen if Novartis overpaid. Investors reacted with caution on Tuesday, with Novartis shares falling 1% on news of the acquisition.

But with MorphoSys providing additional expertise in hematology R&D and a foothold in the German biotech scene, Novartis can justify the deal as a strategic move to reinforce oncology leadership. The pharma giant has the resources to continue its shopping spree, with around $9 billion in annual free cash flow.

If Novartis can successfully integrate MorphoSys’ personnel and drug candidates into its pipeline, while achieving cost synergies, the acquisition could pay dividends over time as new oncology drugs emerge. But executing large M&A successfully is always challenging, and investors will watch closely how Novartis leverages its new MorphoSys assets.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference on April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available…Read More

Atlanta, GA, February 6, 2024 – GeoVax Labs, Inc. (Nasdaq: GOVX), a biotechnology company developing immunotherapies and vaccines against cancers and infectious diseases, today announced positive initial safety and immune response findings from its Phase 2 clinical trial at one month following administration of its Covid-19 vaccine, GEO-CM04S1. The trial, evaluating GEO-CM04S1 as a heterologous booster in 63 healthy adults who had previously received the Pfizer or Moderna mRNA vaccine (ClinicalTrials.gov Identifier: NCT04639466), was fully enrolled at the end of Sept 2023.

The study is designed to evaluate the safety and immunogenicity of two GEO-CM04S1 dose levels. The trial remains blinded to dose of vaccine received, with study subjects being followed for a total of one year. To date, there have been no serious adverse events, and adverse events were in line with other routine vaccinations. The immunological responses measured throughout the study period include both neutralizing antibodies against SARS-CoV-2 variants and specific T-cell responses. Consolidated data from all subjects tested one-month post-vaccination, documented statistically significant increases in neutralizing antibody responses against multiple SARS-CoV-2 variants, ranging from the original Wuhan strain through Delta and Omicron XBB 1.5; additional testing against the JN.1 variant is underway.

GEO-CM04S1 is a next-generation Covid-19 vaccine based on GeoVax’s MVA viral vector platform, which supports the presentation of multiple vaccine antigens to the immune system in a single dose. GEO-CM04S1 encodes for both the spike (S) and nucleocapsid (N) antigens of SARS-CoV-2 and is specifically designed to induce both antibody and T cell responses to those parts of the virus less likely to mutate over time. The more broadly functional engagement of the immune system is designed to protect against severe disease caused by continually emerging variants of Covid-19. Vaccines of this format should not require frequent and repeated modification or updating. These latest findings lend support to previously published findings in cell transplant patients of the ability of GEO-CM04S1 to stimulate functional antibody responses against a broad array of evolving SARS-CoV-2 virus variants (Chiuppesi et al, Vaccines, Sept 2023).

Kelly McKee, Jr., MD, MPH, GeoVax Chief Medical Officer, stated, “There is a critical need to address the recognized shortcomings of currently approved SARS-CoV-2 vaccines. Annual (or even more frequent) vaccination in a seemingly never-ending race to keep pace with this rapidly evolving virus is an unsustainable strategy. GEO-CM04S1 continues to demonstrate the ability to elicit broadly reactive functional antibodies in conjunction with robust and durable T-cell responses, offering the prospect of a next-generation solution to address these shortcomings.”

“We are thrilled by these data and our investigational vaccine designed to protect against severe disease caused by emerging variants of Covid-19,” said David Dodd, GeoVax Chairman and CEO. “These interim data reinforce our resolve to bring our expertise in the development of innovative vaccines to address critical public health needs using new approaches and technologies. We look forward to providing further updates regarding the successful progress of the clinical development of GEO-CM04S1.”

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel therapies and vaccines for solid tumor cancers and many of the world’s most threatening infectious diseases. The company’s lead program in oncology is a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, presently in a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax’s lead infectious disease candidate is GEO-CM04S1, a next-generation Covid-19 vaccine targeting high-risk immunocompromised patient populations. Currently in three Phase 2 clinical trials, GEO-CM04S1 is being evaluated as a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized Covid-19 vaccines are insufficient, and as a booster vaccine in patients with chronic lymphocytic leukemia (CLL). In addition, GEO-CM04S1 is in a Phase 2 clinical trial evaluating the vaccine as a more robust, durable Covid-19 booster among healthy patients who previously received the mRNA vaccines. GeoVax has a leadership team who have driven significant value creation across multiple life science companies over the past several decades. For more information, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

SAN DIEGO, Feb. 06, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets and an industry-leading provider of high-performance, jet-powered unmanned aerial systems, recently welcomed U.S. Senator Gary Peters (D-MI) and U.S. Representative Lisa McClain (R-MI-9) to Technical Directions Inc. (TDI) headquartered in Oxford, Michigan, to showcase Kratos’ family of affordable turbine engines and turbogenerators.

Steve Fendley, President of Kratos Unmanned Systems Division, said, “TDI’s engines are a key enabler for producing small cruise missile and loitering munitions in mass, thanks to our laser-focus on manufacturability for scale with an incredibly high performance-to-cost ratio. These characteristics mirror the Kratos’ corporate strategy, but more importantly, provide a U.S. designed, manufactured, integrated, and tested affordable small-thrust-class turbine engine solution which has effectively been unachievable from U.S. manufacturers in recent years. We’re very proud of the products we’ve developed and proud to be growing in Michigan where we are able to leverage the deep experience of the automotive industry. We appreciate the opportunity to show them firsthand to Sen. Peters and Rep. McClain.”

TDI has developed and refined turbine engine technologies for military applications in Michigan since 1983—providing unique features in support of low-cost, high-production, expendable turbojet engine applications, such as small cruise missiles and other Unmanned Aerial Vehicles (UAVs). With the engineering, manufacturing, and system integration employees in the Oxford, Michigan facility, TDI’s subject matter experts leverage Michigan’s deep automotive expertise and apply it to the defense sector and have experience that encompasses all aspects of this turbine engine class, from clean-sheet design, through performance testing, vehicle integration, flight testing, and production manufacturing. By making its own internally funded investments that are not tied to any specific customer or budget process, TDI is able to rapidly develop and be first to market with its engines.

In 2023, Kratos received a $9 million contract award from the Department of Defense that, in addition to current and near-term program plans, is expected to rapidly increase TDI’s job, capability, and capacity growth trajectories, and advance TDI’s work bringing small engine turbine manufacturing back to the U.S. with the production rate and cost levels to support the DoD’s affordable mass needs of today and tomorrow.

Senator Peters, a member of the Senate Armed Services and Appropriations Committees, said, “Michigan defense manufacturers excel at producing innovative solutions to our most pressing national security challenges, and Kratos and the TDI team here in Oxford are a key partner in that success. It was great to see firsthand the important work they are doing to build the next-generation of defense technologies that protect our men and women in uniform, and to celebrate this new contract that will support Michigan-made products and jobs.”

“Touring the Kratos TDI facility this morning was a terrific experience that gave me a first-hand perspective of the work that goes into creating turbine engines and turbogenerators,” said Representative McClain. “I am proud that Kratos continues to call Oxford home, and I am excited to see their impact in the community grow throughout this year and beyond.”

About Kratos Defense & Security Solutions, Inc. Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

SAN DIEGO, Feb. 06, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the fourth quarter and fiscal year 2023 after the close of market on Tuesday, February 13th. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

MustGrow has received The State of Oregon Agriculture approval to commence sales of TerraSanteTM, an organic biofertility product, in Oregon State.

MustGrow’s recently-awarded organic compliance certification from the USDA National Organic Program (OMRI Listed®) will apply to this Registration.

Mustard-derived TerraSanteTMfocuses on soil microbiome health, nutrient/water use efficiencies, and plant yields.

SASKATOON, Saskatchewan, Canada, February 6, 2024 – MustGrow Biologics Corp. (TSXV:MGRO) (OTC:MGROF) (FRA:0C0) (the “Company” or “MustGrow”) is pleased to announce receipt of The State of Oregon Agriculture Fertilizer Registration Certificate for its mustard plant-based TerraSanteTM, an organic biofertility product. TerraSanteTM’s recently-awarded organic compliance certification from the USDA National Organic Program (OMRI Listed®) will apply to TerraSanteTM product sales in Oregon State.

TerraSanteTM product sales may now commence in Oregon State, with a sales and marketing commercialization strategy already underway with BioAg Product Strategies for the 2024 planting season. In addition to Oregon State and recently-awarded Washington State, further state-level registrations are progressing in other key U.S. states.

In 2021, Oregon State recorded $5.0 billion USD in agriculture production on 16 million acres of farmland and contributed $2.6 billion USD in agriculture exports.(1) Agriculture plays a critical role in the state’s economy, generating 13% of the state’s gross product and $30 billion USD in wages.(1) Oregon farmers grow a wide variety of fruits and vegetables, including potatoes, tomatoes, strawberries, wine-making grapes, cherries, pears, and apples. Oregon farmers are regarded for their innovative commitment to sustainable agriculture with a rising trend toward organic and sustainable farming practices.(2) MustGrow believes its organic TerraSanteTM product will position Oregon farmers to meet increasing demand for organic, local, and healthy produce.

The MustGrow organic biofertility product will complement the Company’s existing biocontrol programs in preplant soil fumigation, postharvest food preservation, and bioherbicide, which are currently under development with four global partners: Bayer, Sumitomo Corporation, Janssen PMP, and NexusBioAg. These four partnered programs continue to achieve performance milestones and expand globally in scope and investment.

TerraSanteTM for Soil and Ecological Health

MustGrow’s soil amendment and biofertility development programs focus on soil microbiome health, nutrient and water use efficiencies, and plant yields. Soil is a farmer’s most valuable asset, and MustGrow’s mustard plant-based technologies are being developed with the intention to improve not only the health of the soil, but also the surrounding ecological environment.

As an organic biofertilizer in soluble mixable form, TerraSanteTM contains nutritious plant proteins and carbohydrates that feed soil microbes, potentially improving beneficial microbial activity and ensuring long-term sustainable soil health. These targeted micro-communities have been shown to work to improve nutrient availability, which can potentially increase plant vigor and yields, while reducing plant stress. TerraSanteTM has the potential to improve crop nutrient uptake and, hence, overall crop performance. There are no artificial additives or preservatives used during its manufacturing.

MustGrow is an agriculture biotech company developing organic biocontrol and biofertility products by harnessing the natural defense mechanism and organic materials of the mustard plant to sustainably protect the global food supply and help farmers feed the world. MustGrow and its leading global partners — Bayer, Janssen PMP (pharmaceutical division of Johnson & Johnson), Sumitomo Corporation, and Univar Solutions’ NexusBioAg — are developing mustard-based organic solutions for applications in biocontrol to potentially replace harmful synthetic chemicals in preplant soil treatment and weed control, to postharvest disease control and food preservation. Bayer has a commercial agreement to develop and commercialize MustGrow’s biocontrol soil applications in Europe, Africa, and the Middle East. Concurrently, with new formulations derived from food-grade mustard, the Company is pursuing the adoption and use of its first registered and OMRI Listed® product, TerraSanteTM, in key U.S. states. Over 150 independent tests have been completed, validating MustGrow’s safe and effective approach to crop and food protection and yield enhancements. Pending regulatory approval, MustGrow’s patented liquid technologies could be applied through injection, standard drip or spray equipment, improving functionality and performance features. MustGrow has approximately 51.5 million basic common shares issued and outstanding and 54.2 million shares fully diluted. For further details, please visit www.mustgrow.ca.

Contact Information

Corey Giasson Director & CEO Phone: +1-306-668-2652 info@mustgrow.ca

MustGrow Forward-Looking Statements

Certain statements included in this news release constitute “forward-looking statements” which involve known and unknown risks, uncertainties and other factors that may affect the results, performance or achievements of MustGrow.

Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects”, “is expected”, “budget”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved”. Examples of forward-looking statements in this news release include, among others, statements MustGrow makes regarding: the commencement of TerraSanteTM product sales in Oregon State; the progress of state-level registrations of TerraSanteTM products in other states; whether the TerraSanteTM product will position Oregon farmers to meet increasing demand for organic, local, and healthy produce; whether MustGrow’s organic biofertility product will complement the Company’s existing biocontrol programs in preplant soil fumigation, postharvest food preservation, and bioherbicide; whether MustGrow’s four partnered programs will continue to achieve performance milestones and expand globally in scope and investment; whether targeted micro-communities can increase plant vigor and yields, while reducing plant stress; and the potential for TerraSanteTM to improve crop nutrient uptake and, hence, overall crop performance. Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual results of MustGrow to differ materially from those discussed in such forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, MustGrow. Important factors that could cause MustGrow’s actual results and financial condition to differ materially from those indicated in the forward-looking statements include market receptivity to investor relations activities as well as those risks described in more detail in MustGrow’s Annual Information Form for the year ended December 31, 2022 and other continuous disclosure documents filed by MustGrow with the applicable securities regulatory authorities which are available at www.sedar.com. Readers are referred to such documents for more detailed information about MustGrow, which is subject to the qualifications, assumptions and notes set forth therein.

This release does not constitute an offer for sale of, nor a solicitation for offers to buy, any securities in the United States.

Neither the TSXV, nor their Regulation Services Provider (as that term is defined in the policies of the TSXV), nor the OTC Markets has approved the contents of this release or accepts responsibility for the adequacy or accuracy of this release.

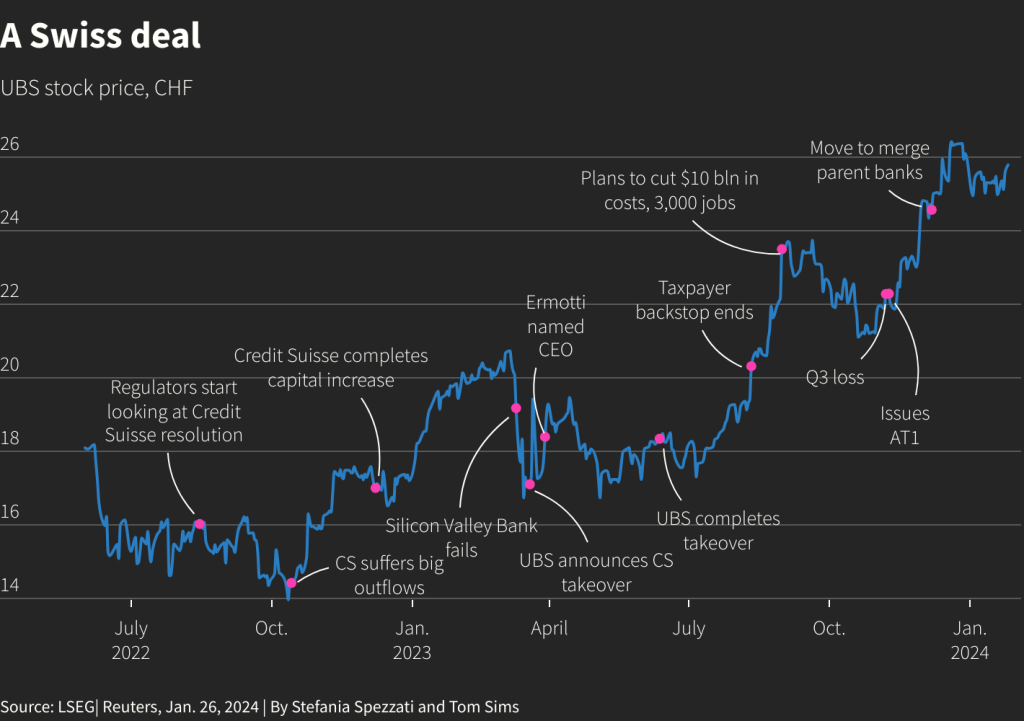

Swiss banking giant UBS announced several major strategic updates on Tuesday, including resuming share buybacks and increasing cost-cutting targets related to its takeover of Credit Suisse last year. The bank’s shares fell nearly 4% as investors reacted to financial results and the roadmap ahead.

UBS said it plans up to $1 billion in share repurchases in 2024, restarting its buyback program which was halted during the acquisition of Credit Suisse in March 2023. The deal, valued at nearly $16 billion, was the first ever merger between two global systemically important banks. It significantly expanded UBS’s wealth management operations and investment banking capabilities.

Integrating Credit Suisse is expected to generate major cost synergies over the next several years. UBS now estimates total savings of $13 billion by the end of 2026, up from the previous target of over $10 billion. Around half of the savings will come from headcount reductions, according to CFO Todd Tuckner.

While UBS said the initial phase of integration is complete, CEO Sergio Ermotti warned there is still significant restructuring ahead. The next few years will involve job cuts, combining IT systems, and optimizing operations. Ermotti cautioned that progress “will not be measured in a straight line” and the trickier parts of integration have yet to occur.

The bank reaffirmed its key financial targets, including for return on capital and cost-income ratios. It also set new ambitions, such as growing assets under management in its wealth management division to $5 trillion by 2028, up from $3.85 trillion currently.

For 2024, UBS proposed boosting its dividend by 27% compared to 2023. This comes as many European banks have been rewarding shareholders through dividends and buybacks.

UBS posted a small net loss of $279 million in the fourth quarter of 2023. The loss was attributed to Credit Suisse integration costs. However, the bank sees profitability improving in early 2024 amid better market activity and progress on merging operations.

Image Credit: Reuters Graphics

The wealth management unit reported $22 billion in net new money growth during the quarter. However, a change in metrics makes the figure not directly comparable to previous periods. The investment bank posted a pre-tax loss of $169 million but is expected to return to profitability soon.

Shares fell due to concerns around UBS’s near-term profitability as integration costs weigh on performance. While cost savings are substantial over the long run, analysts pointed out revenue will likely drop in the next couple years before synergies are fully realized.

There are also lingering concerns around integrating such large banking operations smoothly. Regulators are keeping a close eye given the combined balance sheet is nearly twice the size of Switzerland’s GDP. However, UBS maintains only around one-third of assets are illiquid.

Overall, UBS remains confident in achieving strategic goals from its takeover of Credit Suisse, even if the next few years involve headaches from combining staff, technology, and business lines. Execution risks remain but cost cuts could significantly boost profitability down the line. Tuesday’s announcements provided investors more clarity around buybacks, dividends, and the path forward.

Haynes International, Inc. is a leading developer, manufacturer and marketer of technologically advanced, nickel and cobalt-based high-performance alloys, primarily for use in the aerospace, industrial gas turbine and chemical processing industries.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Haynes to be acquired by Acerinox, S.A. Haynes International entered into a definitive agreement to be acquired in an all-cash transaction by Acerinox’s wholly owned U.S. subsidiary, North American Stainless, Inc. Acerinox is a leader in the manufacturing and distribution of stainless steel and high-performance alloys and will acquire all the outstanding shares of Haynes for $61.00 per share valuing Haynes at an enterprise value of approximately $970 million and a fully diluted equity value of $798 million. The shares are trading close to the proposed transaction price per share.

Closing is expected in the third calendar quarter. The transaction has been unanimously approved by the board of directors of both companies and is expected to close in the third calendar quarter of 2024, subject to the satisfaction of closing conditions, including receipt of regulatory approvals and approval by Haynes stockholders. Because the Haynes shareholder meeting is tentatively planned for April 2024, we think the transaction could close sooner than later.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Washington Extension. The State of Washington awarded Comtech a $48 million contract extension to continue providing Next Generation 911 (NG911) services over the next five years, with the option to extend through 2034. This is a key extension, in our view, with a number of other NG911 state contracts up, or coming up, for renewal.

A Key Partnership. Washington State is a national leader in the application of NG911 services and, beginning in 2016, Comtech designed, deployed, and operated next generation public safety technologies for the state. Under Comtech, Washington has one of the most robust and advanced NG911 systems in the country.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported Q2 revenue of $305.7 million, beating our estimate of $295.5 million by 3.4%.. Adj. EBITDA of $103.1 million was 3.6% higher than our estimate of $99.5 million. Notably, acquisitions and new builds contributed $41 million of revenue in the quarter and event revenue was up over 30% from the prior year period.

Expanding growth initiatives. Management highlighted the company’s increased investment guidance for 2024. Notably, $190.0 million is allocated for acquisitions, up from $160.0 million, and $80.0 million is allocated to conversions, up from $75.0 million. Additionally, $40.0 million is allocated to new builds and $45.0 million in maintenance expenditures are expected in 2024. We view the company’s increased investment favorably.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Shares of data analytics company Palantir Technologies soared over 25% on Tuesday after the company reported fourth-quarter results that beat expectations, driven by strong demand for its artificial intelligence capabilities.

Palantir said revenue in the fourth quarter increased 20% year-over-year to $608.4 million, surpassing Wall Street estimates of $602.4 million. The revenue growth was led by the company’s commercial business, especially in the U.S., where Palantir has been rapidly building out its AI platform known as AIP.

In a letter to shareholders, Palantir CEO Alex Karp provided color on the ongoing demand for AI capabilities, stating that appetite for large language models in the U.S. “continues to be unrelenting.” Karp noted that Palantir conducted nearly 600 pilots of its AIP platform with customers last year.

The AI platform allows Palantir customers to build their own AI models specific to their business using the company’s robust data management and analytics capabilities. This enables tailored AI applications across a variety of industries and use cases, from risk modeling in financial services to supply chain optimization and more.

Analyst Commentary on AI Momentum

Multiple analysts upgraded Palantir stock and raised price targets following the strong quarterly showing, which provided tangible evidence of the company’s AI platform gaining traction with customers.

Citi analysts upgraded Palarntir to a Neutral rating from Sell, saying the results demonstrated “breakthrough momentum” for the commercial business driven by AI adoption. They see the momentum in AIP balancing out risks related to guidance for the non-U.S. commercial business.

Meanwhile, Jefferies analysts admitted they were previously wrong to downplay the impact AI could have for Palantir. They now believe the company is at an “inflection point” as the AIP platform ramps faster than their initial expectations.

Bank of America also noted that while still early, AIP is already having a meaningful impact on Palantir’s growth. They expect the AI momentum to continue and see significant opportunities in the U.S. government sector as well.

Concerns Around Valuation Remain

Despite the more constructive view on AI traction, some analysts still harbor concerns around Palantir’s valuation. Jefferies pointed out the stock trades at a 23% premium to large cap peers, leading them to remain sidelined for now despite the growth signals.

Citi also raised its target to $20, which offers upside from current levels but is likely still conservative relative to more bullish Street views. The premium multiple encapsulates the potential rewards and risks at this stage of Palantir’s expansion within AI.

Path Forward for AI Business

The fourth quarter results provided promising evidence that Palantir’s investments in AI and its unified data platform are allowing it to capitalize on the surging demand. But the company will likely need to maintain the commercial momentum and continue gaining AI adoption to justify a higher valuation.

If Palantir can consistently grow revenue, especially within the U.S. commercial landscape, while expanding AIP pilots into long-term customers, it could support a durable growth trajectory. Government work also offers a steady revenue stream to complement the more volatile commercial business over time.

Overall, Palantir’s latest quarter showcased its potential as an AI leader. But realizing the full upside will depend on smart and consistent execution across geographies and industries. The positive analyst reactions and stock move indicate investors are gaining confidence in Palantir’s ability to capture the AI opportunity.

BY THE COMTECH EDITORIAL TEAM – FEB 5, 2024 | 3 MIN READ

MELVILLE, N.Y. – February 5, 2024– Comtech (NASDAQ: CMTL) announced today that Washington State recently awarded the company a $48 million contract extension to continue providing Next Generation 911 (NG911) services over the next five years, with the option to extend through 2034.

Washington State initially contracted Comtech to design, deploy and operate next generation public safety technologies and secure and reliable communications capabilities in 2016, making Washington a national leader in the application of NG911 services.

“We value our continued partnership with Washington State and have worked collaboratively over the past eight years to deploy one of the most robust and advanced NG911 systems in the United States,” said Ken Peterman, President and CEO, Comtech. “This contract extension award further demonstrates the state of Washington’s trust of our NG911 capabilities to support the state’s public safety mission. As we continue to support the state of Washington, we look forward to exploring emerging capabilities like artificial intelligence to equip first responders with life-saving insights at the speed of relevance.”

“The Washington State NG911 enterprise system provides people in crisis with a more effective 911 service and has saved countless lives in the eight years since we initially partnered with Comtech,” said Adam Wasserman, Assistant Director for Emergency Communications, Washington State Emergency Management Division. “Our NG911 system keeps pace with the ever-evolving communications technologies used by the citizens in our state. In addition, due to the increased reliability, resilience and security, as well as the designed interoperability with other 911 centers – intrastate, interstate, and international (Canada) – the Washington State NG911 enterprise system is more effective at collecting and disseminating initial situational awareness during major emergencies and disasters.”

As one of the most trusted providers of public safety technologies, Comtech is continuing to expand its NG911 offerings for governments and emergency response providers around the world. The company’s NG911 systems are designed to adapt and continuously evolve over time to meet the needs of emerging use cases as well as future applications.

About the State of Washington 911 Coordination Office

The 911 Unit of the Emergency Management Division works to ensure the seamless operation of the statewide 911 communications system, ensuring uniform, prompt, and efficient access to public safety services for the citizens and visitors to the state of Washington.

Washington has 86 Public Safety Answering Points (911 centers) that cover all 39 counties within the state. The PSAPs are connected to the statewide Emergency Services IP Network (ESInet), which delivers location information of the 911 caller as well as other data needed.

In addition to contracting for the statewide 911 network, the 911 Unit provides fiscal and technical assistance to counties and PSAPs to support 911 operations. The 911 Unit continues to drive the evolution of the 911 network to accommodate the advances in communication technologies such as wireless, VoIP-based communications and the myriad of upcoming non-traditional technologies.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 911 emergency services, satellite and space communications technologies, and cloud native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results and performance could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

CHELMSFORD, MA / ACCESSWIRE / February 5, 2024 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for 100 years, today announced the appointment of two senior executives to newly-created roles reporting to Kelly Waller, Senior Vice President of Sales and Marketing.

Varsha Tomar was named Vice President, Partnerships, and will oversee the identification, cultivation, and management of strategic B2B sales partnerships that will enable Harte Hanks to drive incremental revenue. She will oversee joint alliances, resellers/white labelers of Harte Hanks services and manage a team of Inside Partner Account Managers. Ms. Tomar joins Harte Hanks from HealthEquity, where she was Director of Business Operations after previously serving as Global Head of Go-To-Market Strategy for Finastra.

Luke Kenny was named Sr. Director of International Sales and Client Expansion. Based in Portugal, Mr. Kenny has nearly two decades of experience as a sales director and demand generation expert across EMEA and APAC for B2B organizations, including Finastra and FIS. At Harte Hanks, he will focus on sales as well as supporting and growing business from existing European clients. He is also tasked with overseeing the growth of the sales teams throughout the region. Harte Hanks has offices in the UK, Romania and Belgium.

“As we continue to implement our transformation growth plan, these two strategic hires will help us meet our goals of expanding our sales and marketing organization routes to market and expanding our global footprint,” commented Ms. Waller.

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Certain statements discussed in this release as well as in other reports, materials and oral statements that the Company releases from time to time to the public may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Generally, words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “believe,” “plan,” “target,” “forecast” and similar expressions are intended to identify forward- looking statements. Such forward-looking statements concern management’s expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters. Forward-looking statements are inherently uncertain and subject to a variety of assumptions, risks and uncertainties that could cause actual results to differ materially from those anticipated or expected by the management of the Company. These statements are not guarantees of future performance and actual events or results may differ significantly from these statements. Given these risk factors, investors and analysts should not place undue reliance on forward-looking statements. Forward-looking statements speak only as of the date of the document in which they are made. The Company disclaims any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in the Company’s expectations or any change in events, conditions or circumstances on which the forward-looking statement is based, except as required by law. It is advisable, however, to consult any further disclosures the Company makes in its filings with the Securities and Exchange Commission, including Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K (if any). These statements constitute the Company’s cautionary statements under the Private Securities Litigation Reform Act of 1995.

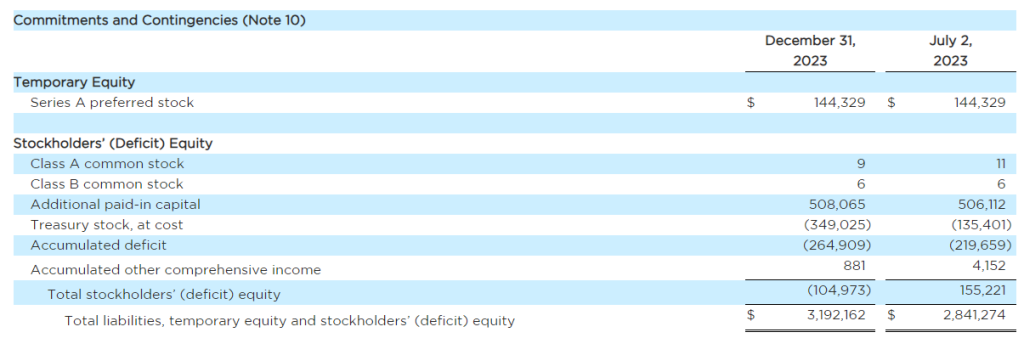

RICHMOND, Va.–(BUSINESS WIRE)– Bowlero Corp. (NYSE: BOWL) (“Bowlero” or the “Company”), one of the world’s premier operators of location-based entertainment, today provided financial results for the second quarter of the 2024 Fiscal Year, which ended on December 31, 2023.

Quarter Highlights:

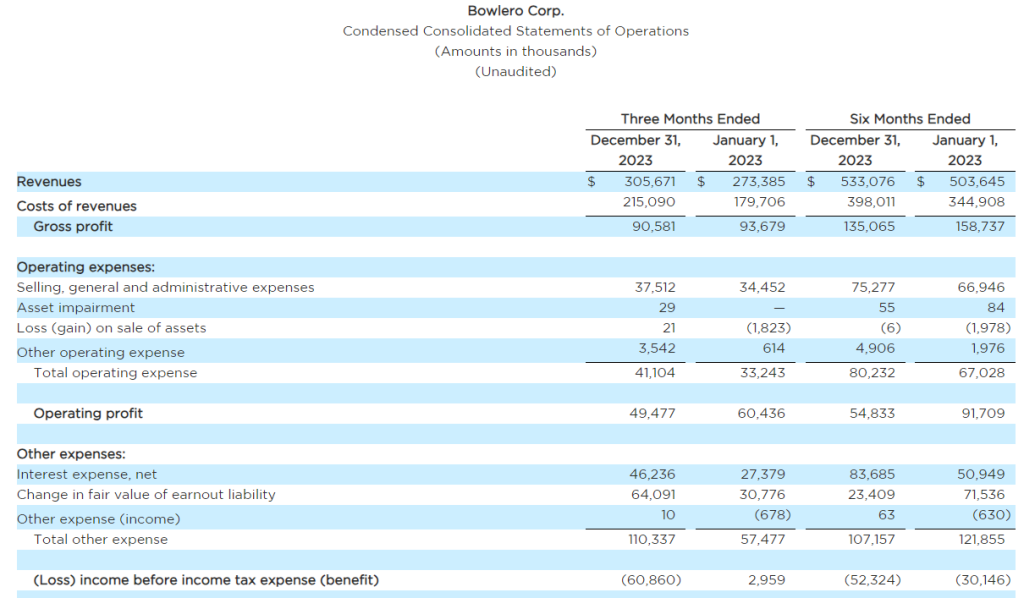

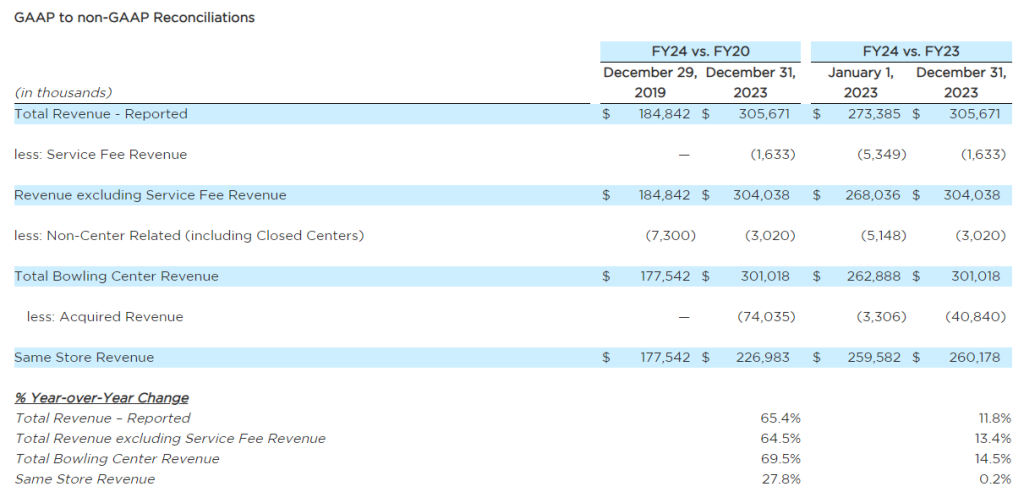

Revenue increased 11.8% to $305.7 million versus the prior year and increased 65.4% versus 2QFY20 (quarter ended December 29, 2019)

Revenue excluding Service Fee Revenue increased 13.4% to $304.0 million versus the prior year and was up 64.5% versus 2QFY20

Total Bowling Center Revenue increased 14.5% versus the prior year and was up 69.5% versus 2QFY20

Same Store Revenue increased 0.2% versus the prior year and grew 27.8% versus 2QFY20

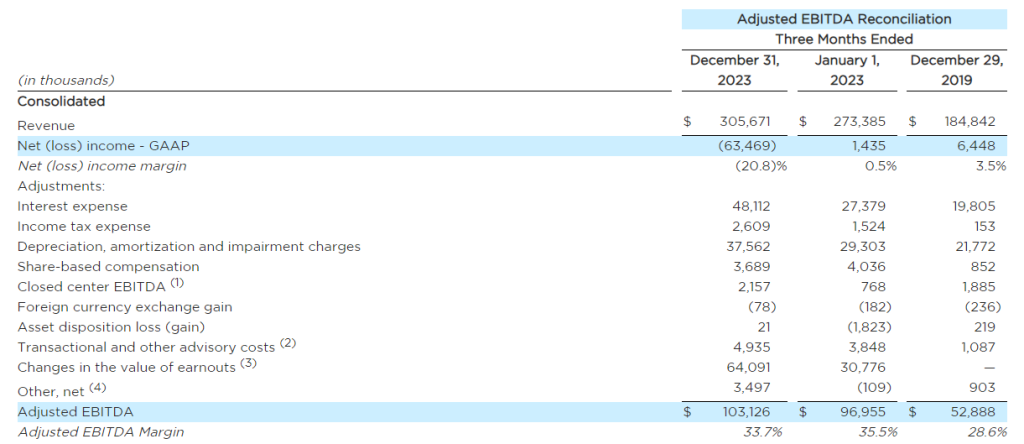

Net loss of $63.5 million versus prior year income of $1.4 million and income of $6.4 million in 2QFY20, which includes $64.1 million of expense from the non-cash impact of the earnouts for the current period

Adjusted EBITDA of $103.1 million versus prior year of $97.0 million and $52.9 million in 2QFY20

Added 3 locations during the quarter, 2 from acquisitions and 1 new build-out, bringing year-to-date new centers to 21

Total locations in operation as of February 5, 2024 is 350

“Second quarter fiscal year 2024 saw double-digit total growth, amplifying our ability to grow the business despite difficult comparatives as we come out of the record-breaking COVID rebound. Our acquisition of Lucky Strike represents a major milestone for the Company as we focus on higher revenue properties and continue to grow our location count. That deal brought together flagship properties with our best-in-class operators and event sales platform, driving results higher than expectations. We are expanding the well-known Lucky Strike brand by opening our first Lucky Strike new build in Moorpark, California, and the new Lucky Strike Miami will soon follow.,” said Thomas Shannon, Founder and Chief Executive Officer of Bowlero.

Mr. Shannon continued, “In the quarter, our event business was up over thirty percent and continues to drive the strength of our overall business. Same-store revenue was positive in the quarter, driven by the reset of mid-week promotions, improved pricing dynamics on the weekend, and strong execution from our events team. Acquisitions and new builds contributed $41 million of revenue in the quarter and the Lucky Strike acquisition is ahead of our profitability targets. We are taking a cautious approach to the third quarter due to meaningful weather headwinds in the first three weeks of January but expect to make up that softness in the rest of the third quarter and fourth quarter and continue to expect double-digit revenue growth in fiscal year 2024.”

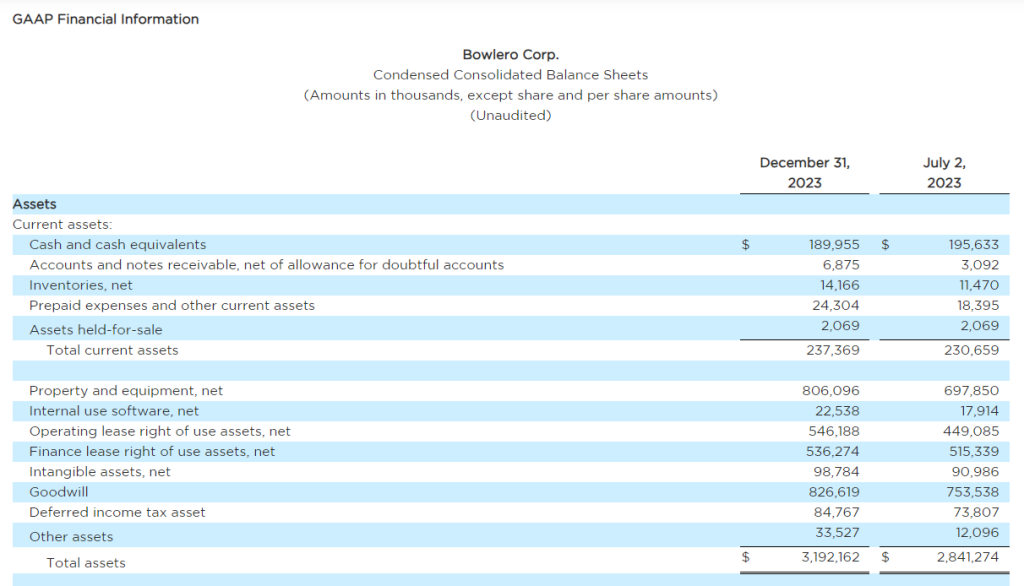

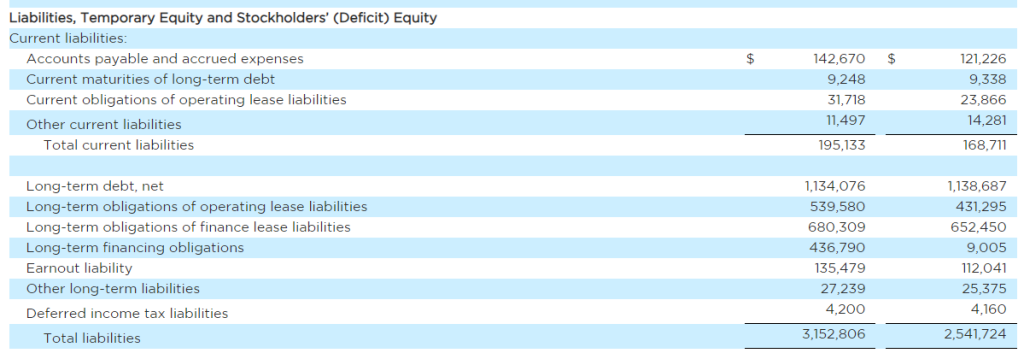

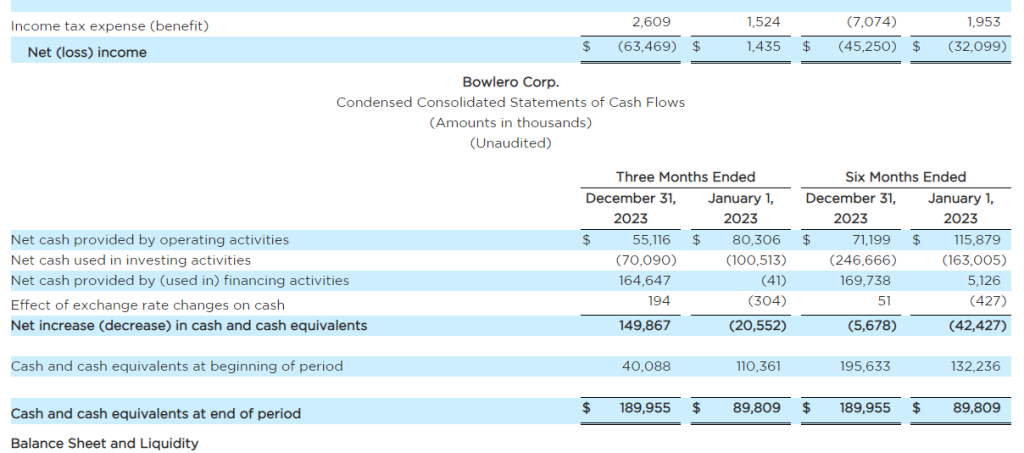

Bobby Lavan, Chief Financial Officer, added, “In the quarter, we received $409 million net proceeds from our sale-leaseback transaction with Vici. We used proceeds to pay down our revolver balance in full, fund acquisitions including Lucky Strike, and accelerate our capital investment plan. We ended the quarter with $190 million of cash and $412 million of total liquidity.”

Share Repurchases

During the quarter, the Company repurchased approximately 7.5 million shares of Class A common stock for approximately $80 million. In the first quarter of fiscal year 2024, the company repurchased approximately 12.1 million shares for approximately $131 million, bringing total repurchases in the first half of fiscal year 2024 to approximately 19.6 million. Since 2021, the Company has spent approximately $432 million retiring all SPAC-related warrants, repurchasing 31.0 million shares of common stock, and 4.9 million as-converted preferred shares, reducing common stock outstanding by about 20%.

On February 2, 2024, the Board of Directors authorized a time extension and an increase to the share repurchase program, replenishing the authorized repurchase amount to $200 million and removing the program expiration date. The timing of the repurchases and the actual amount repurchased will depend on a variety of factors, including the market price of the Company’s shares, general market and economic conditions, and other factors.

Dividend

The Board of Directors of the Company has approved the initiation of a quarterly dividend program. The Board of Directors declared an initial quarterly cash dividend of $0.055 per share of common stock for the third quarter of fiscal 2024. The dividend will be payable on March 8, 2024, to stockholders of record on February 23, 2024. The Company intends to pay a cash dividend on a quarterly basis going forward, subject to market conditions and approval by the Company’s Board of Directors.

Fiscal Year 2024 and Third Quarter 2024 Guidance

The Company reiterated financial guidance for fiscal year 2024. The Company expects Revenue to be up 10% to 15% in fiscal year 2024, excluding the $21 million of Service Fee Revenue1 from prior year revenue, equating to $1.14 billion to $1.19 billion. Adjusted EBITDA margin is expected to be 32% to 34%, which equates to Adjusted EBITDA of $365 million to $405 million. The Company expects the third quarter of fiscal year 2024 to have Revenue Excluding Service Fee Revenue of $335 million to $350 million and Adjusted EBITDA of $128 million to $143 million.

The Company is updating its investment guidance based on expanding growth opportunities in fiscal year 2025. The Company expects to reinvest heavily in the business in fiscal year 2024, with more than $190 million allocated to acquisitions (up from $160 million), $40 million to new builds, and $80 million to conversions and growth (up from $75 million). Maintenance capital expenditures are expected to be $45 million.

Investor Webcast Information

Listeners may access an investor webcast hosted by Bowlero. The webcast and results presentation will be accessible at 10:00 AM ET on February 5, 2024, in the Events & Presentations section of the Bowlero Investor Relations website at https://ir.bowlerocorp.com/overview/default.aspx.

About Bowlero Corp.

Bowlero Corporation is one of the world’s premier operators of location-based entertainment. With approximately 350 locations across North America, the Company serves more than 40 million guest visits annually through a family of brands that include Lucky Strike, Bowlero and AMF. In 2019, Bowlero acquired the Professional Bowlers Association, the major league of bowling and a growing media property that boasts millions of fans around the globe. For more information on Bowlero, please visit BowleroCorp.com.

Forward Looking Statements

Some of the statements contained in this press release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that involve risk, assumptions and uncertainties, such as statements of our plans, objectives, expectations, intentions and forecasts. These forward-looking statements are generally identified by the use of forward-looking terminology, including the terms “anticipate,” “believe,” “confident,” “continue,” “could,” “estimate,” “expect,” “intend,” “likely,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other various or comparable terminology. These forward-looking statements reflect our views with respect to future events as of the date of this release and are based on our management’s current expectations, estimates, forecasts, projections, assumptions, beliefs and information. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. All such forward-looking statements are subject to risks and uncertainties, many of which are outside of our control, and could cause future events or results to be materially different from those stated or implied in this document. It is not possible to predict or identify all such risks. These risks include, but are not limited to: our ability to design and execute our business strategy; changes in consumer preferences and buying patterns; our ability to compete in our markets; the occurrence of unfavorable publicity; risks associated with long-term non-cancellable leases for our centers; our ability to retain key managers; risks associated with our substantial indebtedness and limitations on future sources of liquidity; our ability to carry out our expansion plans; our ability to successfully defend litigation brought against us; our ability to adequately obtain, maintain, protect and enforce our intellectual property and proprietary rights and claims of intellectual property and proprietary right infringement, misappropriation or other violation by competitors and third parties; failure to hire and retain qualified employees and personnel; the cost and availability of commodities and other products we need to operate our business; cybersecurity breaches, cyber-attacks and other interruptions to our and our third-party service providers’ technological and physical infrastructures; catastrophic events, including war, terrorism and other conflicts; public health emergencies and pandemics, such as the COVID-19 pandemic, or natural catastrophes and accidents; changes in the regulatory atmosphere and related private sector initiatives; fluctuations in our operating results; economic conditions, including the impact of increasing interest rates, inflation and recession; and other factors described under the section titled “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) by the Company on September 11, 2023, as well as other filings that the Company will make, or has made, with the SEC, such as Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this press release and in other filings. We expressly disclaim any obligation to publicly update or review any forward-looking statements, whether as a result of new information, future developments or otherwise, except as required by applicable law.

Non-GAAP Financial Measures

To provide investors with information in addition to our results as determined under Generally Accepted Accounting Principles (“GAAP”), we disclose Revenue Excluding Service Fee Revenue, Total Bowling Center Revenue, Same Store Revenue and Adjusted EBITDA as “non-GAAP measures”, which management believes provide useful information to investors because each measure assists both investors and management in analyzing and benchmarking the performance and value of our business. Accordingly, management believes that these measurements are useful for comparing general operating performance from period to period, and management relies on these measures for planning and forecasting of future periods. Additionally, these measures allow management to compare our results with those of other companies that have different financing and capital structures. These measures are not financial measures calculated in accordance with GAAP and should not be considered as a substitute for revenue, net income, or any other operating performance or liquidity measure calculated in accordance with GAAP, and may not be comparable to a similarly titled measure reported by other companies. Our third quarter and fiscal year 2024 guidance measures (other than revenue) are provided on a non-GAAP basis without a reconciliation to the most directly comparable GAAP measure because the Company is unable to predict with a reasonable degree of certainty certain items contained in the GAAP measures without unreasonable efforts. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Such items include, but are not limited to, acquisition related expenses, stock-based compensation and other items not reflective of the company’s ongoing operations.

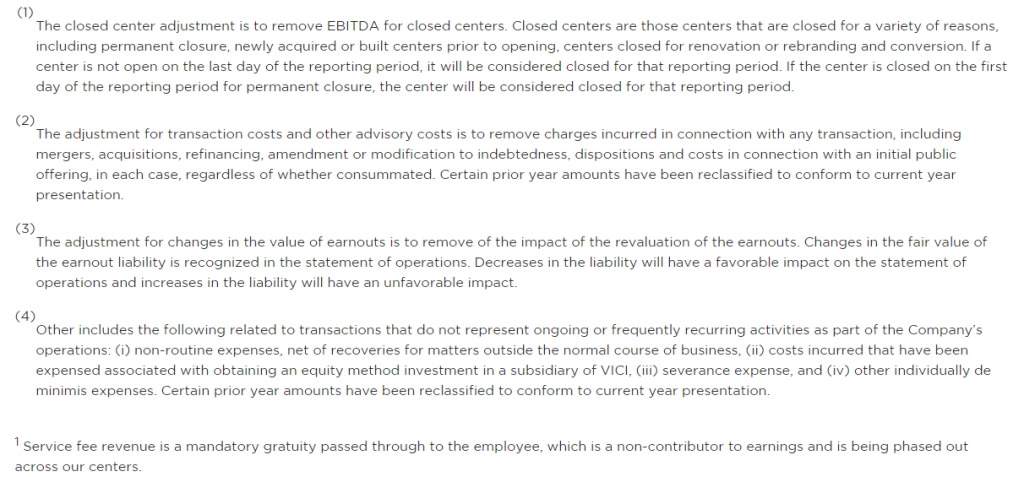

Revenue Excluding Service Fee Revenue represents Total Revenue less Service Fee Revenue. Total Bowling Center Revenue represents Total Revenue less Non-Center Related Revenue, Revenue from Closed Centers (as defined below), and Service Fee Revenue, if applicable. Same Store Revenue represents Total Revenue less Non-Center Related Revenue, Revenue from Closed Centers, Service Fee Revenue, if applicable, and Acquired Revenue. Adjusted EBITDA represents Net Income (Loss) before Interest Expense, Income Taxes, Depreciation and Amortization, Share-based Compensation, EBITDA from Closed Centers, Foreign Currency Exchange Loss (Gain), Asset Disposition Loss (Gain), Transactional and other advisory costs, changes in the value of earnouts, and other.

The Company considers Revenue Excluding Service Fee Revenue as an important financial measure because provides a financial measure of revenue directly associated with consumer discretionary spending and Total Bowling Center Revenue as an important financial measure because it provides a financial measure of revenue directly associated with bowling center operations. The Company also considers Same Store Revenue as an important financial measure because it provides comparable revenue for centers open for the entire duration of both the current and comparable measurement periods.

The Company considers Adjusted EBITDA as an important financial measure because it provides a financial measure of the quality of the Company’s earnings. Other companies may calculate Adjusted EBITDA differently than we do, which might limit its usefulness as a comparative measure. Adjusted EBITDA is used by management in addition to and in conjunction with the results presented in accordance with GAAP. We have presented Adjusted EBITDA solely as a supplemental disclosure because we believe it allows for a more complete analysis of results of operations and assists investors and analysts in comparing our operating performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are that Adjusted EBITDA:

do not reflect every expenditure, future requirements for capital expenditures or contractual commitments;

do not reflect changes in our working capital needs;

do not reflect the interest expense, or the amounts necessary to service interest or principal payments, on our outstanding debt;

do not reflect income tax (benefit) expense, and because the payment of taxes is part of our operations, tax expense is a necessary element of our costs and ability to operate;

do not reflect non-cash equity compensation, which will remain a key element of our overall equity based compensation package; and

do not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations.