Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mining. Bit Digital had a decrease in BTC production in September, producing 130.2 BTC, a 7% decrease compared to the prior month of 133.0. The decrease was primarily driven by an increase in network difficulty and a reduction in active hash rate that occurred towards the end of the month. The active hash rate was approximately 1.19 EH/s as of September 30, 2023, as roughly 600 PH/s of miners went offline due to a power utility mandated maintenance outage from September 26, 2023, to October 6, 2023 with an additional 250 PH/s of miners going offline towards the end of the month following the conclusion of a hosting contract at one facility. The Company is in the process of relocating those miners to alternative hosting sites.

Staking. The Company had approximately 13,594 ETH (13,188 last month) actively staked in native and liquid staking protocols as of September 30, 2023, with 11,200 natively staked and 2,394 ETH deployed in liquid staking protocols. The Company has 512 ETH (16 Nodes) deposited but in queue to be activated on the Ethereum staking network, which are estimated to come online by the end of October 2023. The blended APY for the month was roughly 4.1%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The biotechnology sector has seen a flurry of activity recently, with major drugmakers looking to acquire smaller biotech firms to boost their pipelines. According to a recent Bloomberg News report, French pharmaceutical giant Sanofi is in talks to acquire Mirati Therapeutics, a clinical-stage biotech focused on developing novel cancer treatments.

While negotiations are still ongoing, this potential deal highlights the enormous value being seen in emerging biotech firms like Mirati that are pioneering cutting-edge medicines. Mirati’s lead drug candidate is a treatment for non-small cell lung cancer, one of the most common and deadly forms of cancer.

These mergers and acquisitions underscore the biotech sector’s immense growth prospects. With novel approaches to treating cancer, genetic diseases, and other unmet medical needs, biotechs have become hotbeds for innovation. And major drugmakers are increasingly looking to tap into these scientific advancements through strategic deals.

For investors, the busy M&A environment highlights the potential windfalls in identifying and investing in promising biotech firms early on. While risky, buying shares in companies with disruptive technologies before they are on Big Pharma’s radar can result in exponential returns.

With science rapidly advancing, the coming decades are likely to see huge leaps in biomedical innovations. The recent wave of pharma-biotech mergers shows large drugmakers recognize the future potential of biotech. Savvy investors who spot these opportunities stand to profit as more biotech firms are snatched up or grow into full-fledged pharmaceutical leaders themselves.

Biotechnology represents an exciting new frontier in drug development. Unlike traditional pharmaceuticals derived from chemical compounds, biotech drugs utilize living organisms and biological molecules to treat disease.

Some key innovations driving growth in biotech include:

Gene therapy – Altering genes to treat genetic conditions. Gene editing tools like CRISPR have made gene therapy more precise and scalable.

Cell therapy – Using modified human cells as treatments, such as CAR T-cell therapy for blood cancers.

RNA interference – Silencing specific genes by blocking mRNA translation through RNAi mechanisms.

Monoclonal antibodies – Targeted antibodies cloned from immune cells are blockbuster therapies for cancer, autoimmunity, and more.

Vaccines – Novel vaccine platforms like mRNA vaccines are enabling rapid development of new vaccines.

These advanced technologies promise to revolutionize medicine and usher in an era of personalized, precision medicine. The possibilities span from regenerative medicine to reversing aging. For investors, biotech represents enormous growth potential.

Biotech Deal Frenzy

Given the vast promise of biotech, it is no surprise that pharmaceutical giants have been scooping up biotech firms at a fierce clip. Small promising biotechs are prime targets for acquisition.

Big Pharma companies like Sanofi, Merck, and Bristol-Myers need to refill drying pipelines. Revenue-generating biotech drugs can also help offset losses from older medications losing patent protection.

For the acquiring company, buying a biotech with an innovative drug candidate eliminates the risks and costs of developing a new medicine from scratch. And the more established resources and expertise of a pharma giant can help push novel therapies through late-stage trials and regulatory approvals.

Meanwhile, being acquired provides biotech startups with an influx of funds and resources to continue advancing their pipeline. It also offers a lucrative exit for early investors.

As the healthcare needs of the global population increase, larger pharmaceutical companies will likely continue acquiring emerging biotechs to remain competitive. This M&A frenzy shows no signs of slowing down.

Investment Opportunities

For investors, the busy biotech M&A environment provides exciting opportunities to profit. Here are some tips:

Seek out early-stage biotechs with promising technologies before they become acquisition targets. The ideal scenario is investing pre-IPO.

Focus on firms with advanced clinical pipelines addressing urgent unmet needs like cancer, rare diseases, neurodegeneration, etc.

Evaluate the strength of a biotech’s intellectual property and licensing agreements for its core technology.

Assess the management team’s experience in drug development and commercialization.

Consider biotechs focused on next-gen platforms like gene editing, cell therapy, RNAi, etc which are garnering lots of interest.

Be prepared to hold for longer time horizons and have a higher risk tolerance. Clinical trials have high failure rates.

For investors comfortable with risk, the payoffs for spotting the next potential biotech star could be immense as entire new markets for cutting-edge medicines continue to emerge.

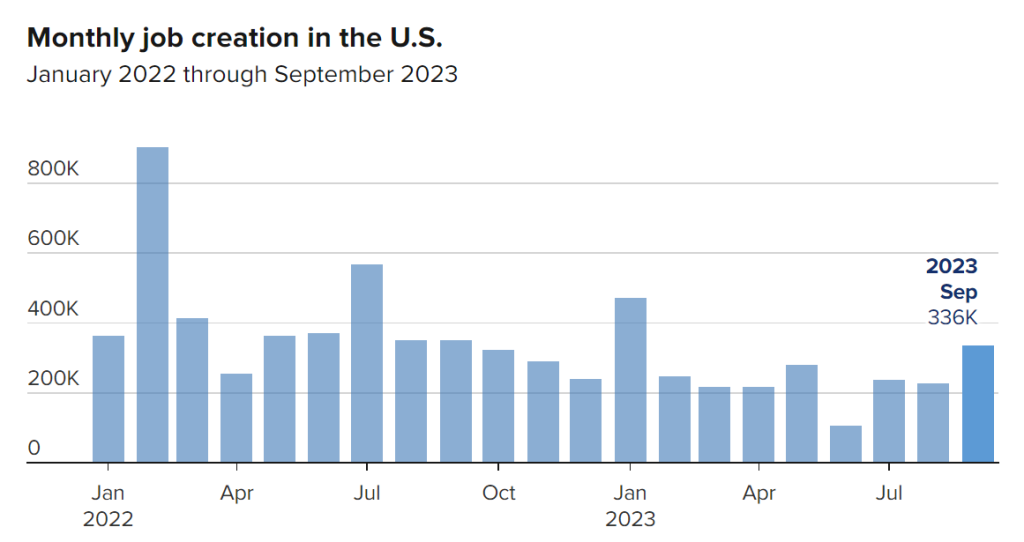

The September jobs report revealed the U.S. economy added 336,000 jobs last month, nearly double expectations. The data highlights the resilience of the labor market even as the Federal Reserve aggressively raises interest rates to cool demand.

Economists surveyed by Bloomberg had forecast 170,000 job additions for September. The actual gain of 336,000 jobs suggests the labor market remains strong despite broader economic headwinds.

The unemployment rate held steady at 3.8%, unchanged from August and still near historic lows. This shows employers continue hiring even amid rising recession concerns.

Wage growth moderated but still increased 0.3% month-over-month and 5.0% year-over-year. Slowing wage gains may reflect reduced leverage for workers as economic uncertainty increases.

The report reinforces the tight labor market conditions the Fed has been hoping to loosen with its restrictive policy. Rate hikes aim to reduce open jobs and slow wage growth to contain inflationary pressures.

Yet jobs growth keeps exceeding forecasts, defying expectations of a downshift. The Fed wants to see clear cooling before it eases up on rate hikes. This report suggests its work is far from done.

The September strength was broad-based across industries. Leisure and hospitality added 96,000 jobs, largely from bars and restaurants staffing back up. Government employment rose 73,000 while healthcare added 41,000 jobs.

Upward revisions to July and August payrolls also paint a robust picture. An additional 119,000 jobs were created in those months combined versus initial estimates.

Markets are now pricing in a reduced chance of another major Fed rate hike in November following the jobs data. However, resilient labor demand will keep pressure on the central bank to maintain its aggressive tightening campaign.

While the Fed has raised rates five times this year, the benchmark rate likely needs to go higher to materially impact hiring and wage trajectories. The latest jobs figures support this view.

Ongoing job market tightness suggests inflation could become entrenched at elevated levels without further policy action. Businesses continue competing for limited workers, fueling wage and price increases.

The strength also hints at economic momentum still left despite bearish recession calls. Job security remains solid for many Americans even as growth slows.

Of course, the labor market is not immune to broader strains. If consumer and business activity keep moderating, job cuts could still materialize faster than expected.

For now, the September report shows employers shaking off gloomier outlooks and still urgently working to add staff and retain workers. This resiliency poses a dilemma for the Fed as it charts the course of rate hikes ahead.

The unexpectedly strong September jobs data highlights the difficult balancing act the Fed faces curbing inflation without sparking undue economic damage. For policymakers, the report likely solidifies additional rate hikes are still needed for a soft landing.

Apple CEO Tim Cook raised eyebrows this week after disclosing the sale of over $88 million worth of company shares, his largest stock sale in over two years. While insider transactions are common, the considerable size and timing of Cook’s liquidation stokes fears amid a bearish environment for tech stocks.

Cook offloaded 511,000 Apple shares at prices between $171-173 per share according to regulatory filings. The sale equates to about 15% of his total vesting this year of over 3.4 million shares. However, it still reduces his exposure as he now holds around 3.28 million shares remaining.

The sale comes at a precarious time for Apple and the broader tech sector. After rallying strongly for most of 2022, the stock has declined nearly 20% from highs since peaking in late July. Concerns over slowing iPhone sales due to macro headwinds have plagued Apple lately.

With the economy potentially heading into recession and inflation hurting consumer budgets, investors have grown nervous over Apple’s prospects. The company also faces supply chain constraints impacting production capacity.

Cook choosing this period to materially reduce his Apple holdings could signal diminished confidence in near-term performance. Even scheduled sales through preset plans evoke questions on timing and motivation when executed amid market turbulence.

While Cook still maintains substantial skin in the game, the optics of a CEO offloading large share blocks matter. Apple also reports quarterly earnings at the end of this month, adding significance to the sale’s proximity.

Any hint of caution from Cook on the conference call risks further rattling shareholders. The considerable size of his stock sale suggests a more defensive posture than his typical modest liquidations.

The move follows similar trends of tech leaders diversifying holdings away from their own companies’ stocks. Meta’s Mark Zuckerberg sold off over $4 billion in shares in recent months. Amazon’s Jeff Bezos and Google’s founders have executed multi-billion dollar sales as well.

With valuations under pressure after a massive bull run, insiders seem intent on locking in gains. But it also betrays their lack of confidence in stock upside ahead. This compounds fears of slowing growth and execution challenges in the sector.

Cook’s sale in particular cuts deep given his influential leadership and long tenure at Apple. As a revered figure, actions speak loudly, and his uncharacteristic liquidation risks sending the wrong signal.

It may suggest that even entrenched tech stalwarts see limits to future gains amid rising macro uncertainty. The instinct to diversify out of FAANG names reinforces the sense that a pivot is underway.

For Apple specifically, Cook’s historic payday casts doubt ahead of the crucial holiday season. It may indicate softer demand for new iPhone models and other products as consumers tighten budgets.

With the stock down nearly 40% from highs, any wavering commitment from icons like Cook further spooks investors. For now, he retains substantial direct ownership, but the considerable cash-out still feels ill-timed given the challenges.

Cook’s sale exemplifies the broader pivot away from high-flying tech as economic conditions worsen. But his influential role means the signal cuts even deeper. Anxious Apple shareholders now await the next earnings results.

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, said today it will release its third-quarter financial results on Thursday, November 2, 2023, at approximately 4:15 p.m., U.S. Eastern Time.

The firm will host a conference call with investors and industry analysts at 9 a.m., U.S. Eastern Time, the following day, Friday, November 3. Dial-in details are as follows:

The dial-in number for U.S. participants is +1 (888) 330-2057.

International participants should call +1 (646) 960-0203.

The security code to access the call is 1482106.

Participants are requested to dial in at least five minutes before the scheduled start time.

A recording of the conference call will be accessible on ISG’s website (www.isg-one.com) for approximately four weeks following the call.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

ATLANTA, GA, October 5, 2023 – GeoVax Labs, Inc. (Nasdaq: GOVX), a biotechnology company developing immunotherapies and vaccines against cancers and infectious diseases, today announced that the U.S. Patent and Trademark Office has issued a Notice of Allowance for Patent Application No. 17/409,574 titled “Multivalent HIV Vaccine Boost Compositions and Methods of Use.” The allowed claims generally cover a priming vaccination with a DNA vector encoding multiple HIV antigens in virus-like particles (VLPs), followed by a boost vaccination with GeoVax’s vector platform for expressing HIV-1 antigens in VLPs utilizing an MVA viral vector.

David Dodd, GeoVax President and CEO, commented, “Our development priorities continue to be our next-generation COVID-19 vaccine, currently in Phase 2 clinical trials, and our cancer immunotherapy program, with Gedeptin® as our lead product in a Phase 1/2 clinical trial for advanced head and neck cancer. While we are focusing on these two products in the near-term, our long-term vision includes developing vaccines against other global public health threats such as HIV. Although not currently under active development, our HIV program forms an important part of the dataset underpinning all of our MVA-based development programs. The patent protection associated with the use of this vaccine is an important part of this product platform.”

Mr. Dodd continued, “Earlier this year, data were presented from a clinical study of a combinational HIV therapy that included GeoVax’s HIV vaccine candidate, MVA62B. The goal of the trial was to reduce or eliminate viral replication in the absence of antiviral medications in HIV-positive individuals (a “functional cure”). The data indicated very high levels of immunogenicity of the treatment, particularly the induction of T cell immunity, even though HIV infection compromises the immune system. We are pleased that GeoVax’s MVA-vectored HIV vaccine was selected to be a part of the experimental combination therapy and contributed to the positive findings. MVA62B was also previously tested in multiple clinical trials as a component of vaccine regimens designed to induce immune responses that prevent HIV infection. The team here at GeoVax is committed to help end the HIV epidemic worldwide and recognizes that the consistent results of MVA62B reflected in clinical trials to date may offer promise towards achieving this goal. We remain committed to supporting corporate and/or academic collaborations or partnering of this potentially critically important vaccine.”

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel therapies and vaccines for solid tumor cancers and many of the world’s most threatening infectious diseases. The company’s lead program in oncology is a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, presently in a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax’s lead infectious disease candidate is GEO-CM04S1, a next-generation COVID-19 vaccine targeting high-risk immunocompromised patient populations. Currently in three Phase 2 clinical trials, GEO-CM04S1 is being evaluated as a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, and as a booster vaccine in patients with chronic lymphocytic leukemia (CLL). In addition, GEO-CM04S1 is in a Phase 2 clinical trial evaluating the vaccine as a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. GeoVax has a leadership team who have driven significant value creation across multiple life science companies over the past several decades. For more information, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

LOS ANGELES, Oct. 05, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Twin Peaks, Fazoli’s, Smokey Bones and 11 other restaurant concepts, announced today that its Board of Directors has declared the Company’s fiscal 2023 fourth quarter cash dividend of $0.14 per share on each outstanding share of Class A common stock and Class B common stock. The dividend is payable on December 1, 2023 to holders of record of Class A common stock and Class B common stock as of the close of business on November 15, 2023.

The declaration and payment of future dividends, as well as the amounts thereof, are subject to the discretion of the Company’s Board of Directors. The amount and size of any future dividends will depend upon the Company’s future results of operations, financial condition, capital levels, cash requirements and other factors. There can be no assurance that the Company will declare and pay dividends in future periods.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands Inc. (NASDAQ: FAT) (the Company) is a leading global franchising company that strategically acquires, markets and develops quick service, fast casual and casual dining restaurant concepts around the world. The Company currently owns eighteen restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Smokey Bones, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean, Ponderosa and Bonanza Steakhouses and franchises and owns over 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these risks, uncertainties and contingencies. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

Conference Call to be held Thursday, October 26 at 8:00 a.m. Central Time

HOUSTON, Oct. 05, 2023 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, today announced that it will issue its financial results for the third quarter ended September 30, 2023, on Wednesday, October 25, 2023, after the close of the stock market.

A conference call and audio webcast with analysts and investors will be held the next day, October 26, at 8:00 a.m. Central Time to discuss the results and answer questions.

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Hawaii, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design, and specialty services. Its concrete segment provides turnkey concrete construction services including place and finish, site prep, layout, forming, and rebar placement for large commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices throughout its operating areas (oriongroupholdingsinc.com)

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Amended PIPE Funding Agreement. The company announced that it is amending its PIPE agreement, which was established when it went public through a SPAC. The amendment allows several private investors to purchase roughly 3.4 million Series A Convertible Preferred shares from the original PIPE investor.

PIPE agreement. In accordance with the agreement, 4.3 million Convertible Preferred shares and 0.7 million common shares and $50 million cash ($10 pre share) were held in trust. After going public, the company received cash per share from the trust at the volume weighted average price (VWAP) of the shares (rather than $10/share). The shares would settle in increments over several reference periods. The PIPE investor would receive a cash redemption for the difference between $10 and the VWAP of the shares for a given reference period. For example, if the VWAP was $3 for a reference period, the company would receive $3 per share and the trust would return $7 per share to the PIPE investor.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Sells Church Products. On September 29, 2023, the company entered into an agreement to sell the Salem Church Products business to Gloo LLC for $22.5 million in cash and a promissory note in the principal amount of $7.5 million. Additionally, the company announced entering into membership unit purchase agreement with Gloo in exchange for an advertising credit. In our view, the sale is attractive and provides a timely influx of cash that assuages liquidity concerns.

Membership unit purchase agreement. As stipulated in the agreement, the company entered into a put agreement with Gloo Holdings for 833,333 series A membership units, which are redeemable after January 1, 2027 for a minimum price of $10 million. In exchange for the units, the company will provide an advertising credit of $10 million to Gloo Holdings that expires on December 31, 2028.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Japan-based pharma Kyowa Kirin has agreed to acquire gene therapy specialist Orchard Therapeutics in a deal worth up to $477.6 million. The buyout aims to strengthen Kyowa Kirin’s emerging presence in the high-potential genetic medicine field.

Under the terms, Kyowa Kirin will pay $16 per Orchard ADS in cash upfront, representing a 144% premium to Orchard’s recent share price. Orchard shareholders will also receive a contingent value right worth an additional $1 per ADS if certain regulatory milestones are met.

The total potential payout values the deal at $477.6 million. Kyowa Kirin expects the acquisition to close in Q1 2024 pending approvals.

Orchard focuses on developing therapies using genetically modified hematopoietic stem cells (HSCs) taken from patients themselves. Its treatments aim to correct the underlying genetic cause of diseases in a single administration.

The company’s lead asset is Libmeldy, approved in Europe for treating a rare metabolic disorder called MLD. It also has two other programs for pediatric neurological conditions in late-stage testing.

Beyond the commercial and near-term pipeline assets, Kyowa Kirin gains Orchard’s HSC gene therapy platform. This technology can be leveraged to develop new treatments for diseases in Kyowa Kirin’s wheelhouse like oncology, autoimmune disorders, and others.

Kyowa Kirin has made gene and cell therapy a priority as part of its vision to deliver transformative new medicines. Orchard’s proven development capabilities and leadership position in HSC gene therapy make it an ideal fit for this strategy.

The high premium paid reflects Orchard’s status as a pioneer in the burgeoning field of genetic medicine. The deal provides Kyowa Kirin immediate scale and expertise in leveraging gene therapy.

Kyowa Kirin also gains commercial infrastructure to support the global launch of Libmeldy. The FDA is currently reviewing Libmeldy for approval in the U.S. with a decision date in March 2024.

Orchard’s two other clinical programs in development also address rare pediatric neurological disorders with immense unmet need. Additional earlier stage preclinical assets add further upside to the pipeline.

The deal continues biotech industry consolidation as large players acquire innovators to reinforce their drug development pipelines. The competition among pharmas for gene therapy assets has intensified as the field matures.

For Orchard investors, the buyout represents a significant premium after a long stretch of the stock languishing. But with cash running low, the company faced challenges transitioning its pipeline programs to commercial status alone.

The deal provides ample resources to continue advancing Orchard’s mission of tackling rare genetic diseases. Kyowa Kirin expects to hit $1 billion in sales from the MLD treatment alone if approved in the U.S.

Gene therapy has disrupted drug development over the past decade with its potential to deliver curative, lifelong treatment through a single administration. As technology improves, dealmaking and R&D in the space continues gaining steam.

Kyowa Kirin is the latest pharma to bet big on gene therapy’s possibilities. If it can successfully harness Orchard’s specialized platform and assets, the deal may pave the way to developing life-changing genetic medicines while delivering solid returns to shareholders.

Standard BioTools and SomaLogic have announced plans to unite through an all-stock merger aimed at creating a diversified life sciences tools platform with over $1 billion in equity value. The deal brings together technologies, expertise and customer bases across genomics, proteomics and other omics fields.

Standard BioTools provides genomic analysis tools catering to academic and clinical research settings. SomaLogic specializes in proteomics technology that profiles proteins for biopharmaceutical drug discovery. Their complementary offerings provide scale, synergies, and cross-selling opportunities.

Under the merger agreement, SomaLogic shareholders will receive 1.11 shares of Standard BioTools stock for each SomaLogic share they own. This values SomaLogic at over $370 million based on recent Standard BioTools share prices.

The combined company expects to generate $80 million in cost synergies by 2026 through optimization of its integrated operations. It will also hold over $500 million in cash to fund growth initiatives and new product development.

Standard BioTools CEO Michael Egholm touted SomaLogic’s proteomics capabilities as an ideal fit to accelerate his company’s strategy in the over $100 billion life science tools industry. The deal diversifies Standard BioTools’ portfolio beyond genomics while leveraging its global commercial infrastructure.

SomaLogic provides proteomic analysis that reveals functional expressions of genes, filling a key gap left by genomics. Its SOMAscan platform uses aptamer-based technology to measure thousands of proteins in biological samples.

The technology has become an industry leader in enabling biopharma researchers to identify and validate new drug targets. SomaLogic has relationships with nine of the ten largest pharma companies along with partnerships like its recently launched proteogenomics offering with Illumina.

Standard BioTools plans to tap into these biopharma relationships to cross-sell its genomic analysis tools. Meanwhile, SomaLogic can leverage Standard BioTools’ strong presence selling to academic labs. The combined customer base spans nearly all major end markets.

SomaLogic interim CEO Adam Taich called the merger an opportunity to better serve translational and clinical research customers while creating shareholder value. The healthy $500 million cash position provides ample capital to fund the commercial ramp.

Standard BioTools increased its 2023 revenue outlook to $100-105 million following the merger news. SomaLogic maintained its full-year guidance of $80-84 million. Together, the combined entity expects to generate over $180 million this year.

The boards of both companies have unanimously approved the transaction. Major shareholders holding around 16% of Standard BioTools stock and 1% of SomaLogic have also committed support through voting agreements.

The deal is expected to close in the first quarter of 2024 after securing shareholder and antitrust regulatory approvals. The combined company will operate under the Standard BioTools name and stock ticker, with dual headquarters in South San Francisco and Boulder, Colorado.

Standard BioTools has undergone major changes after a period of underperformance, divesting its sequencing business earlier this year. The merger with SomaLogic continues its strategic shift toward life science research tools.

Together, the companies aim to accelerate development of new diagnostics and precision medicines through their multi-omics technology. Providing genomics, proteomics and other readouts on disease samples provides deeper insights to researchers.

With scale, synergies, ample resources, and multi-pronged revenue opportunities, the combined Standard BioTools and SomaLogic expects to occupy a strengthened position in the competitive life science tools space. Their integration marks the continued consolidation in the industry amid rising demand for omics-based research capabilities.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today that it entered into an agreement to sell its Salem Church Products business to Gloo, LLC for $30 million. When the transaction closes, scheduled for November 1, the parties will also enter into a $10 million multi-year agreement for Salem to advertise the Gloo platform’s products and services across Salem’s radio and digital platform that serves the Christian audience.

Salem Church Products creates and distributes resources for churches and ministries in the areas of church media, worship, children’s ministry, preaching, teaching and employment through online resources including WorshipHouse Media, SermonSearch, ChurchStaffing, Children’s Ministry Deals and many others.

Salem’s Chief Operating Officer David Evans said, “We are proud of the Church Products business we have built over the years. What started with a single website – SermonSearch – has grown into a successful organization providing valuable resources and services to local churches and their pastors. Any time we look to sell a business, we look for organizations that share our passion and that can take that business to the next level. Gloo is just such an organization and we couldn’t be more thrilled.”

Scott Beck, Chief Executive Officer of Gloo, said, “Salem has been a tremendous partner for several years. We share their mission to equip and support the mission of the Church. Welcoming the Salem Church Products collection of brands to the Gloo platform will accelerate our ability to connect churches with a broad network of great products and producers in everything from Sunday weekend experiences, children’s resourcing, staffing and digital evangelism/discipleship. We are excited to support the Salem Church Products’ great leadership team as they accelerate their ability to serve and expand their network.”

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.