CHELMSFORD, MA / ACCESSWIRE / September 16, 2024 / Harte Hanks, Inc. (NASDAQ:HHS), a global leader in customer experience for over 100 years, today announced a leadership transition within its sales organization.

Jason Chapman, a seasoned executive known for driving business transformation and leading global go-to-market teams, has been appointed as Interim Global Head of Sales and Marketing. Chapman takes over for Kelly Waller, who has stepped down as part of a planned departure due to personal reasons.

Kirk Davis, Chief Executive Officer, remarked: “The entire Harte Hanks team fully supports Kelly in her decision and wishes her the best as she moves forward. Kelly’s leadership has been instrumental in reshaping and expanding our sales organization. She fostered a customer-centric approach, enhanced accountability, and implemented a modern framework for success measurement. Thanks to her efforts, our sales pipeline has grown significantly, and we enter this transition and the final stretch of 2024 from a position of strength. We are well positioned for an executive of Jason’s caliber.”

Jason Chapman brings a wealth of experience from renowned organizations such as Bain & Company, SAP SE, Skillsoft, and most recently, Infor. In his previous roles, he successfully led large global go-to-market teams, introduced advanced productivity tools, developed partnership programs, restructured teams, and launched new go-to-market strategies. His efforts have consistently resulted in successful turnarounds, measurable transformations, and sustainable growth. Chapman holds an MBA from MIT Sloan School of Management and a bachelor’s degree from Williams College.

Chapman commented on his new role: “Kelly’s initiatives have refocused Harte Hanks’ sales organization around the customer, creating a unified reporting structure to drive cross-selling and growth. I am eager to build on her accomplishments and leverage these improvements to accelerate sustainable growth. Harte Hanks has an exciting array of near-term opportunities, with solutions tailored to address the persistent challenges our customers face.”

In her parting remarks, Kelly Waller stated: “This past year at Harte Hanks has been incredibly rewarding. I am confident that we have built a formidable team, with the right structure to drive long-term growth. While a personal matter requires me to step aside, I believe in the strength of our executive team under Kirk’s leadership and the company’s ability to carry forward the progress we’ve made. I will do everything I can to ensure a smooth and successful transition.”

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including GlaxoSmithKline, Unilever, Pfizer, Warner Bros Discovery, Volvo, Ford, FedEx, Midea, and IBM, among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,000 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks, Inc.

Our press release and related earnings conference call contain “forward-looking statements” within the meaning of U.S. federal securities laws. All such statements are qualified by this cautionary note, provided pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements other than historical facts are forward-looking and may be identified by words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “seeks,” “could,” “intends,” or words of similar meaning. These forward-looking statements are based on current information, expectations and estimates and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to vary materially from what is expressed in or indicated by the forward-looking statements. In that event, our business, financial condition, results of operations or liquidity could be materially adversely affected and investors in our securities could lose part or all of their investments. These risks, uncertainties, assumptions and other factors include: (a) local, national and international economic and business conditions, including (i) the outbreak of diseases, such as the COVID-19 coronavirus, which has curtailed travel to and from certain countries and geographic regions, created supply chain disruption and shortages, disrupted business operations and reduced consumer spending, (ii) market conditions that may adversely impact marketing expenditures, (iii) the impact of the Russia/Ukraine conflict on the global economy and our business, including impacts from related sanctions and export controls and (iv) the impact of economic environments and competitive pressures on the financial condition, marketing expenditures and activities of our clients and prospects; (b) the demand for our products and services by clients and prospective clients, including (i) the willingness of existing clients to maintain or increase their spending on products and services that are or remain profitable for us, and (ii) our ability to predict changes in client needs and preferences; (c) economic and other business factors that impact the industry verticals we serve, including competition and consolidation of current and prospective clients, vendors and partners in these verticals; (d) our ability to manage and timely adjust our facilities, capacity, workforce and cost structure to effectively serve our clients; (e) our ability to improve our processes and to provide new products and services in a timely and cost-effective manner though development, license, partnership or acquisition; (f) our ability to protect our facilities against security breaches and other interruptions and to protect sensitive personal information of our clients and their customers; (g) our ability to respond to increasing concern, regulation and legal action over consumer privacy issues, including changing requirements for collection, processing and use of information; (h) the impact of privacy and other regulations, including restrictions on unsolicited marketing communications and other consumer protection laws; (i) fluctuations in fuel prices, paper prices, postal rates and postal delivery schedules; (j) the number of shares, if any, that we may repurchase in connection with our repurchase program; (k) unanticipated developments regarding litigation or other contingent liabilities; (l) our ability to complete anticipated divestitures and reorganizations, including cost-saving initiatives; (m) our ability to realize the expected tax refunds; and (n) other factors discussed from time to time in our filings with the Securities and Exchange Commission, including under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022 which was filed on March 31, 2023. The forward-looking statements in this press release and our related earnings conference call are made only as of the date hereof, and we undertake no obligation to update publicly any forward-looking statement, even if new information becomes available or other events occur in the future.

Investor Relations Contact:

Rob Fink or Tom Baumann 646.809.4048/646.349.6641 FNK IR HHS@fnkir.com

Median Overall Survival remains at 30 months; Objective Response Rate of 36% and Disease Control Rate of 77%

11/53 (21%) of patients experienced 90-100% tumor shrinkage

VERSATILE-003 Phase 3 clinical trial planned to begin this year

PRINCETON, N.J., Sept. 16, 2024 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (“PDS Biotech” or the “Company”), a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers and the development of infectious disease vaccines, today announced updated data from the VERSATILE-002 trial evaluating Versamune® HPV (formerly PDS0101) in combination with KEYTRUDA® (pembrolizumab) as a first-line (1L) treatment for patients with HPV16-positive recurrent/metastatic (R/M) head and neck squamous cell carcinoma (HNSCC). The data were presented during a poster session on September 14 at the European Society for Medical Oncology (ESMO) Congress 2024 in Barcelona, Spain.

As of the latest data cut of the VERSATILE-002 single-arm, Phase 2 trial on May 17, 2024, Versamune® HPV plus pembrolizumab continued to be well tolerated in this 1L R/M HPV16-positive HNSCC population. Enrollment in the trial (n=53) is complete, 10 patients remain on study treatment and 27 patients (including the 10 on treatment) continue to be followed for survival. Median patient follow-up is 16 months. The data demonstrated the following:

Median Overall Survival (mOS) was 30 months with a lower 95% confidence interval of 19.7 months; Published mOS for pembrolizumab is 12-18 months1,2

Objective Response Rate (ORR) of 36% (19/53); Published ORR for pembrolizumab is 19-25%1,2

Disease Control Rate (DCR) is 77% (41/53)

21% (11/53) of patients had deep tumor responses and shrinkage of 90-100%

9% (5/53) of patients had a complete response

Treatment-related adverse events of Grade ≥3 were seen in 9 patients (Grade 3, n=8 and Grade 4, n=1)

“The updated response data we presented at ESMO show the strong clinical activity and durability of Versamune® HPV plus pembrolizumab,” said Jared Weiss, M.D., Section Chief of Thoracic and Head/Neck Oncology, Professor of Medicine at the University of North Carolina, and principal investigator of the VERSATILE-002 clinical trial. “Continued evaluation shows the promise of this combination in improving survival for patients with HPV16-positive HNSCC.”

A global, randomized, controlled Phase 3 clinical trial, VERSATILE-003, that will evaluate Versamune® HPV plus pembrolizumab vs. pembrolizumab monotherapy as 1L treatment in patients with HPV16-positive R/M HNSCC with CPS ≥1 is planned to start this year.

“We’re encouraged to see that as the data from our VERSATILE-002 clinical trial have matured, responses continue to improve, suggesting durability of the Versamune® HPV induced anti-tumor immune response,” said Dr. Kirk Shepard, M.D., Chief Medical Officer of PDS Biotech. “The encouraging patient survival and clinical responses coupled with promising tolerability as seen in the VERSATILE-002 trial underscore our belief in the potential of the combination to be the first HPV-targeted immunotherapy for HNSCC, and a significant advancement in the treatment of the growing population of patients with HPV16-positive HNSCC. We are working toward initiating the VERSATILE-003 Phase 3 study this year.”

Versamune® HPV has been granted Fast Track designation by the FDA.

Licitra L. et al. 2024, International Journal of Radiation Oncology Volume 118, Issue 5e2-e3April 01

No head-to-head studies have been performed comparing Versamune® HPV with other treatments

About PDS Biotechnology PDS Biotechnology is a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers and the development of infectious disease vaccines. The Company plans to initiate a pivotal clinical trial in 2024 to advance its lead program in advanced HPV16-positive head and neck squamous cell cancers. PDS Biotech’s lead investigational targeted immunotherapy Versamune® HPV is being developed in combination with a standard-of-care immune checkpoint inhibitor, and also in a triple combination including PDS01ADC, an IL-12 fused antibody drug conjugate (ADC), and a standard-of-care immune checkpoint inhibitor.

Forward Looking Statements This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS01ADC, Versamune® HPV (formerly PDS0101), PDS0203 and other Versamune® and Infectimune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS01ADC, Versamune® HPV, PDS0203 and other Versamune® and Infectimune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; the Company’s ability to continue as a going concern; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® and Infectimune® are registered trademarks of PDS Biotechnology Corporation.

Keytruda® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

The World Health Organization (WHO) released its preferred target product profile (TPP) criteria for mpox vaccines at its Mpox Research and Innovation Scientific Conference held August 29-30

TNX-801, Tonix’s attenuated live-virus vaccine candidate, has characteristics that align closely with WHO’s TPP

On August 14, 2024, the WHO determined that the upsurge of mpox in a growing number of countries in Africa constitutes a public health emergency of international concern1–4: cases of the potentially lethal new Clade I mpox also detected in Sweden, Thailand and Singapore

CHATHAM, N.J., Sept. 16, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a fully-integrated biopharmaceutical company with marketed products and a pipeline of development candidates, announced today that the World Health Organization’s (WHO’s) preferred target product profile (TPP), released at the WHO sponsored Mpox Research and Innovation Scientific Conference held August 29-30, 2024, aligns with the characteristics of TNX-801 (horsepox, live virus) vaccine, which is being developed for preventing mpox (formerly known as monkeypox). Key elements of the WHO draft TPP include single-dose, durable protection, administration without special equipment, and stability at ambient temperature. Other potential beneficial characteristics include the ability to limit forward transmission, use in case-contact vaccination strategies and suitability for use in immunocompromised individuals.

“The characteristics of TNX-801 align with the draft TPP released at the WHO sponsored Mpox Research and Innovation Scientific Conference,” said Seth Lederman, M.D., Chief Executive Officer of Tonix. “In animal studies TNX-801 has shown single dose protection against a lethal challenge of Clade I monkeypox virus administered by intratracheal route.5 In addition, protected animals did not produce any infectious virus suggesting TNX-801 has the potential to block forward transmission as expected with live-virus vaccines. TNX-801 is designed for percutaneous administration using a bifurcated needle, like the products and delivery used in WHO’s accelerated smallpox eradication project. Since TNX-801 is a live-virus vaccine, we expect the stability of lyophilized TNX-801 at ambient temperature to be similar to live vaccinia virus vaccines including ACAM2000. We believe TNX-801 can be shipped and stored without the need for a costly and cumbersome ultra-cold supply chain, a particular advantage in lesser developed parts of the world. The stability of live virus vaccines eliminates the need for ultra-cold storage which complicates the widespread use of mRNA vaccines in Africa, where they are needed most right now. Finally, studies on immunocompromised animals6 suggest that TNX-801 may be given to persons with immunocompromising conditions such as HIV, which is another property that will be essential for public health.”

Dr. Lederman continued, “The recent WHO declaration of a Public Health Emergency of International Concern (PHEIC) underscores the urgent need for new vaccines to control this outbreak and save lives. We have been motivated to develop TNX-801 because single-dose vaccines simplify logistics of administration, achieve higher coverage by reducing vaccinee dropout between doses and allow for case-contact or “ring” strategies to vaccinate the contacts of confirmed mpox patients.7,8 Ring vaccination is deemed essential for controlling mpox but requires single-dose vaccines that interrupt forward transmission.”7,8

On August 26, 2024, Tonix announced a collaboration with Bilthoven Biologics (Bbio) to develop GMP manufacturing processes for its mpox vaccine. Bbio is part of the world’s largest vaccine manufacturer, the Cyrus Poonawalla Group, which also includes the Serum Institute of India.

The U.S. Food and Drug Administration (FDA) approved vaccines for mpox are a two-dose non-replicating vaccine called Jynneos® from Bavarian Nordic9 and a one-dose live-virus vaccine from Emergent for people at high risk for mpox infection.10 WHO recently authorized Jynneos for use in adults.11 Recently data in animals have been reported for a two-dose mRNA vaccine from Moderna.12

About TNX-801*

TNX-801 is a live replicating attenuated vaccine based on horsepox that is believed to provide immune protection with better tolerability than 20th Century vaccinia viruses. As previously disclosed, TNX-801 protected animals against lethal challenge with intratracheal Clade I monkeypox virus.5 After a single dose vaccination, TNX-801 prevented clinical disease and lesions and also decreased shedding in the mouth and lungs of non-human primates.6 The Findings are consistent with mucosal immunity and suggest the ability to block forward transmission, similar to Dr. Edward Jenner’s vaccinia vaccine, which eradicated smallpox and kept mpox out of the human population. TNX-801 combines immune protection with improved tolerability compared to other vaccines based on orthopoxviruses and is administered with a single dose which has advantages over two-dose regimens. The focus on single-dose vaccines confirms early recommendations by the Bipartisan Commission on Biodefense, 7 and the U.S. National Academies of Science.7,8 The National Academies of Science (NAS) report highlights the difficulty of a ring vaccination strategy with even a two-dose regimen. 7 The U.S. National Institutes of Health (NIH) selected Tonix’s COVID-19 vaccine, TNX-1800 for Project NextGen. TNX-1800 is an engineered version of horsepox that expresses the spike protein of SARS-CoV-2. 13,14

About Mpox* On August 14, 2024, the WHO determined that the upsurge of mpox in a growing number of countries in Africa constitutes a PHEIC the second such declaration in the past two years called in response to an mpox outbreak.1 The current outbreak is caused by Clade I monkeypox virus, while the 2022 outbreak was Clade 2 monkeypox virus. The global mpox outbreak, which commenced in 2022 has affected over 90,000 persons in countries where mpox had previously not been endemic, including Europe and the US. The spread of Clade IIb strain mpox in 2022 underscores the pandemic potential of mpox. Unlike Clade IIb mpox, the Clade I strain of mpox appears to be spreading to countries neighboring the Democratic Republic of the Congo, including Burundi, Rwanda, Uganda and Kenya. Clade I mpox is typically associated with approximately twenty times the case fatality rates than Clade IIb mpox in Africa. According to the U.S. Centers for Disease Control and Prevention (CDC), and other experts, there is a significant risk that the deadlier Clade I strain may appear in the U.S.2,3

Tonix Pharmaceuticals Holding Corp.* Tonix is a fully-integrated biopharmaceutical company focused on developing, licensing and commercializing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s priority is to submit a New Drug Application (NDA) to the FDA in October of 2024 for TNX-102 SL, a product candidate for which two statistically significant Phase 3 studies have been completed for the management of fibromyalgia. The FDA has granted Fast Track designation to TNX-102 SL for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction. Tonix recently announced the U.S. Department of Defense (DoD), Defense Threat Reduction Agency (DTRA) awarded it a contract for up to $34 million over five years in an Other Transaction Agreement (OTA) to develop TNX-4200 small molecule broad-spectrum antiviral agents targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, MD. The company’s Good Manufacturing Practice (GMP)-capable advanced manufacturing facility in Dartmouth, MA was purpose-built to manufacture TNX-801 and the GMP suites are ready to be reactivated in case of a national or international emergency. Tonix’s development portfolio is focused on central nervous system (CNS) disorders. Tonix’s CNS portfolio includes TNX-1300 (cocaine esterase), a biologic in Phase 2 development designed to treat cocaine intoxication that has Breakthrough Therapy designation. Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix also has product candidates in development in the areas of rare disease and infectious disease. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

1WHO Press Release August 14, 2024. “WHO Director-General declares mpox outbrfeak a public health emergency of international concern”. URL: www.who.int/news/item/14-08-2024-who-director-general-declares-mpox-outbreak-a-public-health-emergency-of-international-concern (accessed 8-15-24) 2McQuiston JH, et al. U.S. Preparedness and Response to Increasing Clade I Mpox Cases in the Democratic Republic of the Congo. 2024, MMWR Morbi Mortal Wkly Rep: United States. p. 435-440 3CDC. 2022-2023 Mpox: US Map and Case Count. https://www.cdc.gov/poxvirus/mpox/response/2022/us-map.html 4World Health Organization SAGE meeting highlights on updated mpox vaccine recommendations. 2024, March 5Noyce RS, et al. Viruses. 2023 Jan 26;15(2):356. Doi: 10.3390/v15020356. PMID: 36851570; PMCID: PMC9965234 6Trefry, SV et al. bioRxiv 2023.10.25.564033; doi: https://doi.org/10.1101/2023.10.25.564033 7Bipartisan Commission on Biodefense. Box the Pox: Reducing the risk of Smallpox and Other Ortho poxviruses, Washington:2024 8U.S. National Academies of Science. Future State of Smallpox Medical Countermeasures. Washington:2024 9Zaeck LM, et al. Low levels of monkeypox virus-neutralizing antibodies after MVA-BN vaccination in healthy individuals. Nat Med. 2023 Jan;29(1):270-278. doi: 10.1038/s41591-022-02090-w. Epub 2022 Oct 18. PMID: 36257333; PMCID: PMC9873555. 10August 30, 2024. Reuters. “US FDA approves Emergent’s smallpox vaccine for people at high risk of mpox”. https://www.msn.com/en-us/health/other/us-fda-approves-emergent-s-smallpox-vaccine-for-people-at-high-risk-of-mpox/ 11Keaton, J. Sept. 13, 2024. Associated Press. “WHO grants first mpox vaccine approval to ramp up response to disease in Africa.” URL: https://bit.ly/4e4yyeb 12Mucker et al., (in press) Comparison of protection against mpox following mRNA or modified vaccinia Ankara vaccination in nonhuman primates, Cell (2024), https://doi.org/10.1016/j.cell.2024.08.043 13Awasthi M, et al. Viruses. 2023 Oct 21;15(10):2131. Doi: 10.3390/v15102131. PMID: 37896908; PMCID: PMC10612059. 14Awasthi M, et al. Vaccines (Basel). 2023 Nov 2;11(11):1682. Doi: 10.3390/vaccines11111682.PMID: 38006014

Forward Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Toni’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 1, 2024, and periodic reports filed with the SEC on or after the date thereof. All of Toni’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Key Points: – An assassination attempt on former President Donald Trump adds to the volatility surrounding the 2024 U.S. presidential election. – Investors fear increased political instability, which could impact market sentiment, particularly in small and micro-cap stocks. – Market movements highlight the fragile balance between politics and economic confidence as election tensions rise.

The recent assassination attempt on Donald Trump, the Republican presidential nominee, underscores a key theme in this year’s U.S. election cycle: rising political tensions and their impact on financial markets. On Sunday, Secret Service officers thwarted an apparent assassination attempt at Trump’s West Palm Beach golf course, shaking both political and economic spheres. The event further exacerbates an already turbulent election year, where unpredictable developments have consistently affected investor sentiment.

Political uncertainty is a well-known driver of market volatility, and this incident amplifies the existing concerns. With both parties engaged in heated battles, any threat to a high-profile candidate like Trump has a significant ripple effect on investor confidence. The attempted assassination, while fortunately thwarted, introduces fears of escalating political violence, which could weigh heavily on market behavior, particularly as the election draws near.

In fact, political instability tends to trigger risk aversion among investors, who seek safer assets in uncertain times. The U.S. stock market’s reaction to political events often involves a flight to quality, with investors moving toward bonds, precious metals, or large-cap stocks, while small and micro-cap companies tend to bear the brunt of the volatility. These companies, which rely more heavily on investor confidence and market stability, can see exaggerated price swings during periods of uncertainty.

Small and micro-cap stocks are especially vulnerable in uncertain political environments. These companies often have more limited access to capital and are more sensitive to market fluctuations. Historically, political risks, particularly those involving threats to major candidates, have led to a pullback in smaller stocks as investors pivot toward safer, more liquid assets.

If market anxiety continues to rise over the course of the election season, small-cap stocks could see increased volatility. Investors may start to question how the election’s outcome, influenced by these dramatic events, will impact regulatory frameworks, tax policies, and economic growth. This is especially true for sectors tied closely to government policies, such as healthcare, energy, and technology.

The 2024 election cycle has been unusual, marked by extraordinary levels of polarization, political violence, and uncertainty. The July assassination attempt on Trump in Pennsylvania, coupled with Sunday’s incident, only serves to escalate concerns. Political violence, if it continues, may raise questions about the security and stability of the election process itself, further unsettling markets.

While the S&P 500 and other major indices have shown resilience so far, the small and micro-cap sectors remain more fragile. Any further threats to political figures or destabilizing events could drive more dramatic responses from these stocks. The next few weeks are likely to be crucial as investors digest the implications of these incidents alongside expected changes in monetary policy and global economic developments.

As the FBI continues its investigation into the latest assassination attempt, the political climate will likely remain in focus for investors. While larger companies with diversified portfolios may weather the storm, smaller and more speculative investments will require greater scrutiny. In an unpredictable election cycle like this, market participants may look for safer opportunities and hedge against the risks of political violence or upheaval.

Ultimately, the intersection of political drama and market dynamics this year serves as a reminder that investors should stay agile and informed. Whether these assassination attempts will influence the broader market remains to be seen, but in this highly charged environment, investors will be watching closely for any signs of escalation as the election unfolds.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong fiscal Q4. SelectQuote’s fiscal Q4 revenue of $307.2 million and adj. EBITDA of $14.4 million exceeded our estimates of $271.3 million and a loss of $2.2 million, respectively. In our view, the strong performance demonstrated the power of the company’s synergistic business model, which serves consumers’ needs both for insurance policies and pharmacy services.

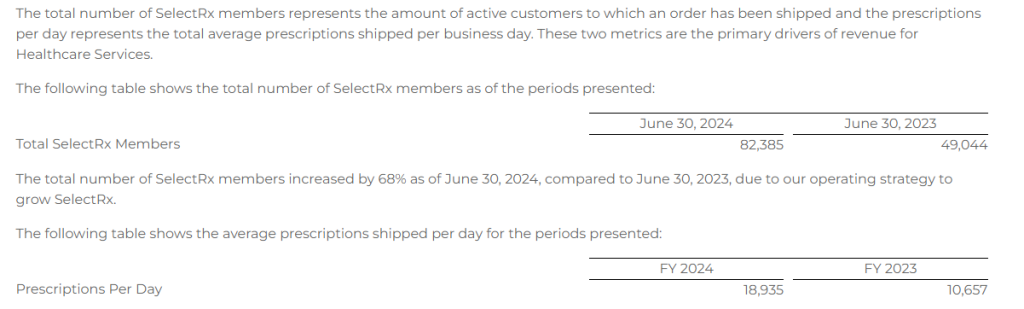

Pharmacy momentum. Total revenue grew an impressive 38% over the prior year period, driven largely by the company’s Healthcare Services segment, which is comprised primarily of SelectRx (home-direct pharmacy business). Healthcare Services revenue was up roughly 75%, year-over-year with SelectRx membership growing to approximately 82,000, up from roughly 75,000 at the end of fiscal Q3.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 results. The company reported Q2 revenue of $105.8 million, which was in line with our $105.0 million estimate. Due to lower than expected Selling & Marketing Expenses and efficiency initiatives, adj. EBITDA was $16.2 million, far better than our $0.9 million estimate. Selling & Marketing expenses were roughly $11 million lower than expected, accounting for the largest portion of the sizable “beat”.

PC picking up Steam. Notably, management highlighted the launch of Pixel Gun 3D PC Edition to the Steam platform, the largest digital distribution platform for PC gaming. The launch of Pixel Gun 3D on Steam and a solid quarter for Hero Wars: Dominion Era led to PC revenue accounting for 42% of total revenue, up from 38% in the prior year period. The addition of Steam is viewed favorably given that PC players tend to spend more money and time playing than mobile users.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Pure play manufacturer. FreightCar America, Inc. is a diversified manufacturer of railroad cars and rail car components. The company designs and manufactures a broad variety of railroad car types for the transportation of bulk commodities and containerized freight products primarily in North America. The company recently reported strong second-quarter financial results and appears poised for greater scale and margin expansion as it increases its market share and expands its product suite.

Expected redemption of high-cost preferred stock. We have assumed the company could redeem its high-cost preferred shares using a private credit term loan. For the sake of simplicity, we have assumed this occurs just prior to 2025. Based on the company’s strong cash flow profile and outlook, we estimate the rate on a $100 million private credit term loan could approximate the secured overnight financing rate (SOFR) plus 600 basis points or 11.33%. We note that the amount of the term loan and the interest rate could vary from our estimates. If the loan amount or interest rate is lower, interest expense could be lower.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Fourth Quarter of Fiscal Year 2024 – Consolidated Earnings Highlights

Revenue of $307.2 million

Net loss of $31.0 million

Adjusted EBITDA* of $14.4 million

Fiscal Year 2025 Guidance Ranges:

Revenue expected in a range of $1.4 billion to $1.5 billion

Net loss expected in a range of $42 million to $6 million

Adjusted EBITDA* expected in a range of $90 million to $120 million

Fourth Quarter Fiscal Year 2024 – Segment Highlights

Senior

Revenue of $114.1 million

Adjusted EBITDA* of $27.9 million

Approved Medicare Advantage policies of 107,272

Healthcare Services

Revenue of $145.2 million

Adjusted EBITDA* of $0.9 million

Approximately 82,000 SelectRx members

Life

Revenue of $42.1 million

Adjusted EBITDA* of $7.2 million

Auto & Home

Revenue of $7.6 million

Adjusted EBITDA* of $2.5 million

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) reported consolidated revenue for the fourth quarter of fiscal year 2024 of $307.2 million compared to consolidated revenue for the fourth quarter of fiscal year 2023 of $221.8 million. Consolidated net loss for the fourth quarter of fiscal year 2024 was $31.0 million compared to consolidated net loss for the fourth quarter of fiscal year 2023 of $47.8 million. Finally, consolidated Adjusted EBITDA* for the fourth quarter of fiscal year 2024 was $14.4 million compared to consolidated Adjusted EBITDA* for the fourth quarter of fiscal year 2023 of $(5.8) million.

Consolidated revenue for the fiscal year ended June 30, 2024, was $1.3 billion compared to consolidated revenue for the fiscal year ended June 30, 2023, of $1.0 billion. Consolidated net loss for the fiscal year ended June 30, 2024, was $34.1 million compared to consolidated net loss for the fiscal year ended June 30, 2023, of $58.5 million. Finally, consolidated Adjusted EBITDA* for the fiscal year ended June 30, 2024, was $117.0 million compared to consolidated Adjusted EBITDA* of $74.3 million for the fiscal year ended June 30, 2023.

SelectQuote Chief Executive Officer, Tim Danker, commented, “2024 was another successful and strong year for SelectQuote across both Senior Medicare Advantage distribution and our Healthcare Services business, driven by SelectRx. On a consolidated basis our fiscal year revenue and Adjusted EBITDA outperformed the midpoint of our original forecast by 17% and 26%, respectively. This marks the 10th consecutive quarter of outperformance versus our internal expectations, reaffirming our strategy to prioritize profitability and cash efficiency over volume growth. Revenue growth was driven primarily by 68% growth in SelectRx members and increasing utilization. Our profitability was driven by another strong year of execution in Senior, which achieved a 25% Adjusted EBITDA margin, similar to a very strong fiscal 2023. Additionally, our Healthcare Services segment achieved its 5th straight quarter of profitability ending the year with Adjusted EBITDA of $7.8 million, which compares to an Adjusted EBITDA loss of $22.8 million in fiscal 2023. Lastly, SelectQuote has signed a non-binding letter of intent to complete an initial commissions receivable securitization of approximately $100 million with certain of our term lenders. Provided this deal closes in the coming weeks, we believe this will be an important first step in our strategic imperative to optimizing our balance sheet capacity, lowering our funding costs, and extending our debt maturities.”

Mr. Danker continued, “SelectQuote’s unique healthcare information platform remains best positioned as a value creation conduit, efficiently connecting a large and growing population of Americans in need of coverage and care with the best providers, based on each of their distinct personal needs.”

Segment Results

We currently report on four segments: 1) Senior, 2) Healthcare Services, 3) Life, and 4) Auto & Home. The performance measures of the segments include total revenue and Adjusted EBITDA*. Costs of commissions and other services revenue, cost of goods sold-pharmacy revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses that are directly attributable to a segment are reported within the applicable segment. Indirect costs of revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses are allocated to each segment based on varying metrics such as headcount. Adjusted EBITDA is our segment profit measure to evaluate the operating performance of our business. We define Adjusted EBITDA as net loss plus: (i) interest expense, net; (ii) benefit for income taxes; (iii) depreciation and amortization; (iv) share-based compensation; (v) goodwill, long-lived asset, and intangible assets impairments; (vi) transaction costs; (vii) loss on disposal of property, equipment and software, net; and (viii) other non-recurring expenses and income. Adjusted EBITDA Margin is calculated as Adjusted EBITDA divided by revenue.

Senior

Financial Results

Operating Metrics

Submitted Policies

Approved Policies

Lifetime Value of Commissions per Approved Policy

Healthcare Services

Financial Results

Operating Metrics

Members

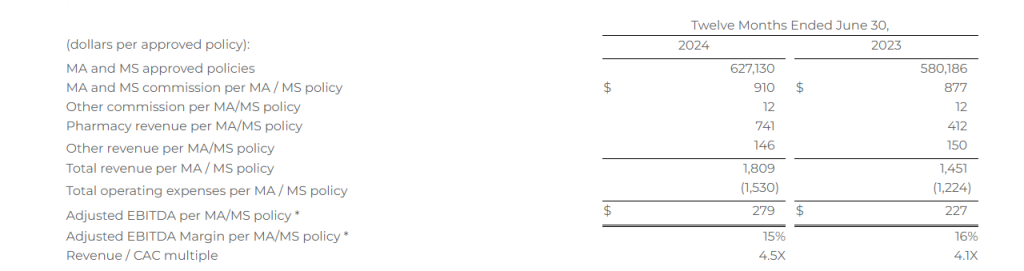

Combined Senior and Healthcare Services – Consumer Per Unit Economics

The opportunity to leverage our existing database and distribution model to improve access to healthcare services for our consumers has created a need for us to review our key metrics related to our per unit economics. As we think about the revenue and expenses for Healthcare Services, we note that they are derived from the marketing acquisition costs associated with the sale of an MA or MS policy, some of which costs are allocated directly to Healthcare Services, and therefore determined that our per unit economics measure should include components from both Senior and Healthcare Services. See details of revenue and expense items included in the calculation below.

Combined Senior and Healthcare Services consumer per unit economics represents total MA and MS commissions; other product commissions; other revenues, including revenues from Healthcare Services; and operating expenses associated with Senior and Healthcare Services, each shown per number of approved MA and MS policies over a given time period. Management assesses the business on a per-unit basis to help ensure that the revenue opportunity associated with a successful policy sale is attractive relative to the marketing acquisition cost. Because not all acquired leads result in a successful policy sale, all per-policy metrics are based on approved policies, which is the measure that triggers revenue recognition.

The MA and MS commission per MA/MS policy represents the LTV for policies sold in the period. Other commission per MA/MS policy represents the LTV for other products sold in the period, including DVH prescription drug plan, and other products, which management views as additional commission revenue on our agents’ core function of MA/MS policy sales. Pharmacy revenue per MA/MS policy represents revenue from SelectRx, and other revenue per MA/MS policy represents revenue from Population Health, production bonuses, marketing development funds, lead generation revenue, and adjustments from the Company’s reassessment of its cohorts’ transaction prices. Total operating expenses per MA/MS policy represents all of the operating expenses within Senior and Healthcare Services. The revenue to customer acquisition cost (“CAC”) multiple represents total revenue as a multiple of total marketing acquisition cost, which represents the direct costs of acquiring leads. These costs are included in marketing and advertising expense within the total operating expenses per MA/MS policy.

The following table shows combined Senior and Healthcare Services consumer per unit economics for the periods presented. Based on the seasonality of Senior and the fluctuations between quarters, we believe that the most relevant view of per unit economics is on a rolling 12-month basis. All per MA/MS policy metrics below are based on the sum of approved MA/MS policies, as both products have similar commission profiles.

Total revenue per MA/MS policy increased 25% for the twelve months ended June 30, 2024, compared to the twelve months ended June 30, 2023, primarily due to the increase in pharmacy revenue. Total operating expenses per MA/MS policy increased 25% for the twelve months ended June 30, 2024, compared to the twelve months ended June 30, 2023, driven by an increase in cost of goods sold-pharmacy revenue for Healthcare Services due to the growth of the business, offset by a decrease in our marketing and advertising costs.

Life

Financial Results

The following table provides the financial results for the Life segment for the periods presented:

Operating Metrics

Life premium represents the total premium value for all policies that were approved by the relevant insurance carrier partner and for which the policy document was sent to the policyholder and payment information was received by the relevant insurance carrier partner during the indicated period. Because our commissions are earned based on a percentage of total premium, total premium volume for a given period is the key driver of revenue for our Life segment.

Auto & Home

Financial Results

Operating Metrics

Auto & Home premium represents the total premium value of all new policies that were approved by our insurance carrier partners during the indicated period. Because our commissions are earned based on a percentage of total premium, total premium volume for a given period is the key driver of revenue for our Auto & Home segment.

Earnings Conference Call

SelectQuote, Inc. will host a conference call with the investment community on September 13, 2024, beginning at 8:30 a.m. ET. To register for this conference call, please use this link: https://www.netroadshow.com/events/login?show=7297aa9f&confId=70516 . After registering, a confirmation will be sent via email, including dial-in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call we suggest registering at least 10 minutes before the start of the call. The event will also be webcasted live via our investor relations website https://ir.selectquote.com/investor-home/default.aspx .

Non-GAAP Financial Measures

This release includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. To supplement our financial statements presented in accordance with GAAP and to provide investors with additional information regarding our GAAP financial results, we have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin, which are non-GAAP financial measures. These non-GAAP financial measures are not based on any standardized methodology prescribed by GAAP and are not necessarily comparable to similarly titled measures presented by other companies. We define Adjusted EBITDA as net income (loss) before interest expense, income tax expense (benefit), depreciation and amortization, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. The most directly comparable GAAP measure is net income (loss). We define Adjusted EBITDA Margin as Adjusted EBITDA divided by revenue. The most directly comparable GAAP measure is net income margin. We monitor and have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin because they are key measures used by our management and Board of Directors to understand and evaluate our operating performance, to establish budgets, and to develop operational goals for managing our business. In particular, we believe that excluding the impact of these expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core operating performance. We believe that these non-GAAP financial measures help identify underlying trends in our business that could otherwise be masked by the effect of the expenses that we exclude in the calculations of these non-GAAP financial measures. Accordingly, we believe that these financial measures provide useful information to investors and others in understanding and evaluating our operating results, enhancing the overall understanding of our past performance and future prospects. Reconciliations of net income (loss) to Adjusted EBITDA are presented below beginning on page 13.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: impacts of the COVID-19 pandemic and any other significant public health events; our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; our ability to regain and maintain compliance with NYSE listing standards; potential litigation and other legal proceedings or inquiries; our existing and future indebtedness; our ability to maintain compliance with our debt covenants; access to additional capital; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in the most recent Annual Report on Form 10-K (the “Annual Report”) and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) provides solutions that help consumers protect their most valuable assets: their families, health, and property. The company pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads.

With an ecosystem offering high touchpoints for consumers across Insurance, Medicare, Pharmacy, and Value-Based Care, the company now has four core business lines: SelectQuote Senior, SelectQuote Healthcare Services, SelectQuote Life, and SelectQuote Auto and Home. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a specialized medication management pharmacy, and Population Health which proactively connects its members with best-in-class healthcare services that fit each member’s unique healthcare needs. The platform improves health outcomes and lowers healthcare costs through proactive engagement and access to high-value healthcare solutions.

Key Points: – Investors now expect a potential 50-basis point Fed rate cut next week, up from prior expectations of a 25-basis point reduction. – Gold reaches a record high, supported by dollar weakness and looming rate cuts. – Crude oil continues its rally as hurricane-related supply concerns rise.

U.S. stocks opened higher on Friday, and gold surged to a record high, as investors grew increasingly optimistic about the Federal Reserve’s potential for a 50-basis point interest rate cut next week. Earlier, market expectations had pointed to a smaller 25-basis point reduction, but reports from The Financial Times and The Wall Street Journal suggested the decision might be more evenly split than previously thought. These reports have caused a sharp change in market sentiment, driving gains in multiple sectors.

In early trading, all three major U.S. stock indexes saw positive movements, with the Dow Jones Industrial Average up 0.36%, the S&P 500 gaining 0.26%, and the Nasdaq Composite climbing 0.16%. Investors are now positioning themselves for potential rate cuts, encouraged further by influential voices like former New York Federal Reserve President Bill Dudley, who said during a forum in Singapore that “there’s a strong case for 50,” referencing a more significant rate cut.

Beyond the scope of next week’s interest rate decision, market participants are also closely watching the Federal Reserve’s forward guidance, particularly its dot plot projections and the statements from Chair Jerome Powell at the post-meeting press conference. According to analysts at TD Securities, the decision could be more contentious than anticipated, with the Fed expected to maintain a broadly dovish tone moving forward.

Gold Prices Surge on Dollar Weakness

Gold prices soared to a record high of $2,579.61 per ounce, marking its strongest weekly gain since mid-August. Investors flocked to the safe-haven asset, which benefits from a weakening U.S. dollar and expectations of further rate cuts. Gold’s appeal tends to rise when interest rates are cut, as lower rates reduce the opportunity cost of holding non-yielding assets like gold.

The U.S. dollar saw significant declines, dropping as much as 1% against the yen to 140.36, its weakest level since December 2023. The dollar index, which tracks the currency against major global counterparts, fell to a one-week low at 101.00. The Japanese yen’s strength was also bolstered by hawkish comments from Bank of Japan officials, signaling potential policy tightening in Japan.

Treasury Yields and Crude Oil React

In the bond market, U.S. Treasury prices rose, causing yields to fall. The benchmark 10-year Treasury yield dropped 2.1 basis points to 3.659%, while rate-sensitive two-year yields fell 6.8 basis points to 3.5803%. The rally in Treasuries indicates growing market confidence in further rate cuts by the Federal Reserve.

Crude oil prices continued to climb, with prices reaching $69.51 per barrel as producers assess the impact of Hurricane Francine, which tore through the Gulf of Mexico. The storm has raised concerns over potential disruptions in oil production, further supporting the upward trend in oil prices.

Market Outlook

As the week progresses, investors will be closely monitoring the Fed’s rate decision and the accompanying guidance on future monetary policy. With inflation easing and economic indicators pointing to slower growth, the market anticipates that further rate cuts may follow throughout the rest of the year. This sentiment has helped lift stocks, gold, and oil, creating a more bullish outlook for the markets in the short term.

Key Points: – MBX Biosciences raised $163.2 million, focusing on metabolic and endocrine disorders. – Bicara Therapeutics and Zenas BioPharma raised $315M and $225M, respectively. – These IPOs reflect renewed investor interest in biotech amid a sluggish broader market.

In a significant boost to the biotech IPO market, three emerging biotech companies—MBX Biosciences, Bicara Therapeutics, and Zenas BioPharma—collectively raised over $700 million through initial public offerings (IPOs). This surge in biotech IPOs, after a quiet summer, underscores the sector’s ability to attract investor attention despite broader market challenges.

MBX Biosciences successfully raised $163.2 million by pricing 10.2 million shares at $16 each, the high end of its expected range. MBX is developing peptide-based therapies for treating metabolic and endocrine disorders, including its lead candidate, MBX 2109, which targets chronic hypoparathyroidism. The company is also developing a preclinical therapy, MBX 4291, aimed at treating obesity by mimicking the effects of gut hormones GLP-1 and GIP. These advances in weight-loss therapies have garnered significant investor interest, especially as obesity treatments like Eli Lilly’s Zepbound and Novo Nordisk’s Wegovy continue to show potential for reducing risks such as stroke and heart attacks.

Another notable IPO, Bicara Therapeutics, raised $315 million, positioning itself as the third-largest biotech IPO of the year. Bicara is focused on developing bifunctional antibody drugs for treating cancers, including head and neck cancers. With plans to launch a late-stage trial alongside Merck’s Keytruda, Bicara is well-positioned to explore treatments for other solid tumors as well.

Zenas BioPharma raised $225 million through its IPO and is gaining traction in the immunology space. Zenas is developing a dual-targeting antibody currently in Phase 3 testing for treating IgG4-related diseases and anemia. With potential applications for multiple sclerosis and lupus, the company is riding a wave of enthusiasm for immune therapies, contributing to its successful public offering.

These IPOs reflect a growing interest in later-stage biotech companies, with all three firms advancing drugs already in human testing. The renewed confidence in the sector could also signal more biotech IPOs on the horizon, particularly as companies look to capitalize on robust investor demand for novel therapies in metabolic diseases, cancer, and immunology.

In a market that has been challenging for biotech firms, these successful IPOs highlight the resilience of companies with strong pipelines and innovative approaches to medical treatment. With MBX Biosciences set to trade under the symbol “MBX” on the Nasdaq Global Select Market, investors are closely watching the sector, hopeful that this uptick in activity is a sign of better things to come for biotech in 2025.

Key Points: – Wall Street’s main indexes rose after August producer price data reinforced expectations of a 25-basis point rate cut. – Moderna shares tumbled following a weak revenue forecast, while communication services led sector gains. – Gold miners surged, benefiting from record-high gold prices.

Wall Street’s major indexes climbed Thursday, buoyed by producer price index (PPI) data that met expectations, pointing to a smaller interest rate cut by the Federal Reserve. The PPI for August showed a 0.2% increase, slightly higher than the anticipated 0.1%, while core prices (excluding volatile food and energy) rose 0.3%, indicating that inflation pressures are continuing to ease but remain a concern. This data has solidified investor expectations of a 25-basis point rate cut at the Fed’s September 17-18 meeting, as opposed to a more aggressive 50-basis point cut.

The stock market responded positively, with the Dow Jones Industrial Average up 0.40%, the S&P 500 gaining 0.70%, and the Nasdaq Composite rising 1.04%. The report also showed initial claims for unemployment benefits at 230,000, aligning with estimates and signaling that the labor market is cooling but remains stable.

Investors remain optimistic despite concerns over inflation, with some bargain hunting occurring in the more economically sensitive small-cap Russell 2000 index, which outperformed with a 1.4% rise. According to Chuck Carlson, CEO of Horizon Investment Services, “There’s a willingness among investors to buy on declines,” highlighting growing confidence in a more controlled inflation environment.

However, Moderna faced significant losses, dropping over 11.5% after issuing a disappointing revenue forecast for fiscal year 2025, citing a lower-than-expected demand for vaccines. This dragged down the healthcare sector, although the rest of the market showed strength in communication services and gold mining stocks. Shares of Warner Bros. Discovery surged nearly 9% following news of a strategic partnership with Charter Communications, further boosting investor sentiment in the media and communications space.

The gold mining sector was another bright spot in the market, with spot gold prices reaching new highs, driving up the Arca Gold BUGS index by 6.3%. Investors flocked to gold as a safe-haven asset amid global economic uncertainties, propelling mining stocks like Newmont Corporation and Barrick Gold.

The backdrop of cooling inflation is encouraging for investors who anticipate that the Fed will begin a more dovish monetary policy cycle. A quarter-point rate cut would mark the first reduction since March 2020, when the pandemic triggered rapid monetary easing. With the U.S. central bank likely to cut rates next week, expectations for further rate reductions in 2024 are growing, depending on how inflation and labor market data evolve.

Looking ahead, investors will continue to monitor economic indicators closely, especially as concerns about the health of the U.S. economy persist. While inflation appears to be retreating, the possibility of a broader economic slowdown could influence market sentiment in the coming months. For now, the stock market is riding high on the belief that the Federal Reserve’s actions will continue to support growth while taming inflation.

High-Performance, USA-Made Engines Now Available with No Lead Time

SAN DIEGO, Sept. 12, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced that Technical Directions, Inc. (TDI), a business unit within Kratos’ Unmanned Systems Division, now offers four classes of its low-cost, high-performance turbojet engines with immediate availability. These engines, ranging from 30 to 200 pounds of thrust, are designed and manufactured in the United States at TDI’s facility in Oxford, Michigan, with all parts and components sourced from U.S. companies.

Known for their compact size and reliable performance, TDI’s turbojets are ideal for use in cruise missiles, loitering munitions systems, and other critical defense systems. Kratos’ commitment to affordability and innovation is at the forefront of this announcement, ensuring that customers can quickly access these engines without lead times—a vital factor for time-sensitive defense projects.

The four classes of TDI’s turbojet engines now available are:

“We understand the importance of rapidly fielding cost-effective solutions in today’s fast-paced defense environment,” said Steve Fendley, President of Kratos Unmanned Systems Division. “With the large number of programs and technology efforts underway in the affordable weapons classes, by building ahead and having these affordable and high-performance engines stocked on our shelves in Michigan, we enable rapid evaluation, test, integration, and ultimately, all up round delivery without the traditional front end lead-time delays.”

Each TDI engine is 100% USA-designed, sourced, and manufactured, ensuring both quality and security. TDI has developed and refined turbine engine technologies for military applications in Michigan since 1983—providing unique features in support of low-cost, high-production, expendable turbojet engine applications, such as small cruise missiles and other Unmanned Aerial Vehicles (UAVs). With the engineering, manufacturing, and system integration employees in the Oxford, Michigan facility, TDI’s subject matter experts leverage Michigan’s deep automotive expertise and apply it to the defense sector and have experience that encompasses all aspects of this turbine engine class, from clean-sheet design, through performance testing, vehicle integration, flight testing, and production manufacturing.

To learn more about TDI’s turbojet engines and their immediate availability, visit our booth at the upcoming Air Force Association’s Air, Space & Cyber Conference or www.tdi-engines.com.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 31, 2023, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.