Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter financial results. FreightCar America generated adjusted net income of $3.8 million or $0.11 per share, compared to our estimate of $2.0 million or $0.06 per share. Second quarter revenue of $118.6 million exceeded our estimate of $100.6 million. Rail car deliveries were 939 units compared to 1,159 units during the prior year period and our estimate of 850. The year-over-year decline was attributed to a strategic shift in the product mix toward higher-margin rail cars. As a percentage of revenue, second quarter gross margin increased to 15.0% compared to 12.5% during the prior year period and our 12.7% estimate. Adjusted EBITDA amounted to $10.0 million compared to our $8.8 million estimate and represented an EBITDA margin of 8.4%. RAIL generated adjusted free cash flow of $7.9 million and ended the quarter with $61.4 million in cash and cash equivalents.

Favorable outlook. During the second quarter, RAIL received 1,226 new rail car orders valued at $106.9 million. With a backlog of 3,624 units valued at $316.9 million, we expect deliveries to accelerate throughout the year. During the quarter, RAIL increased utilization across its four production lines, enhanced productivity, and benefited from a higher-margin product mix. The company is advancing its growth strategy by investing in its tank car capabilities, which it expects to strengthen its cost position and support long-term accretive growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

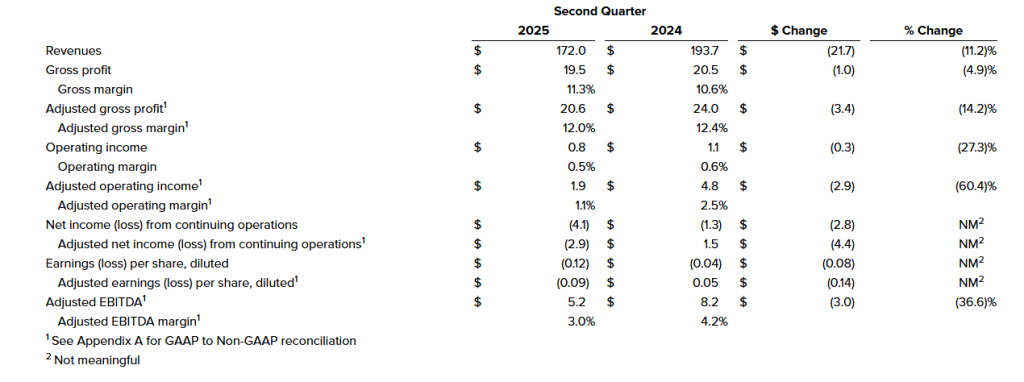

2Q25 Results. Revenue came in at $172 million, down from $193.7 million a year ago, but above our $158 million estimate. Adjusted EBITDA was $5.2 million, down from $8.2 million a year ago, and in-line with our $5 million estimate. Net loss from continuing operations was $4.1 million, or a loss of $0.12/sh, versus $1.3 million, or a loss of $0.04/sh in 2Q24. Adjusted net loss was $0.09/sh in 2Q25 versus adjusted EPS of $0.05 last year. We had forecasted a net loss of $2 million, or a loss of $0.06/sh.

Highlights. Gross margin improved 80 bp sequentially to 11.3% due to operational efficiency improvements. Free cash flow was $17.3 million, up $16.5 million, due to better working capital management. Net debt decreased $31.8 million compared to the year end 2024 level.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – U.S. plans to impose steep pharmaceutical import tariffs starting at 150%, eventually rising to 250%. – Industry analysts warn of price shocks, supply disruptions, and increased pressure on U.S. manufacturing. – The tariffs come amid broader U.S. trade actions targeting semiconductors, copper, and EU goods.

The U.S. pharmaceutical industry is bracing for major potential disruption following the announcement of proposed import tariffs on foreign-made drugs. The new tariffs, set to begin at 150% and rise to 250% within 18 months, signal a dramatic policy shift intended to reduce reliance on overseas pharmaceutical manufacturing and boost domestic production.

The move is part of a broader effort by the U.S. government to reassert control over critical supply chains. Alongside pharmaceuticals, new duties are also targeting semiconductors, copper, and goods from multiple trading partners, including the European Union, Canada, Brazil, and India.

While the intention is to bolster U.S. drug manufacturing and reduce vulnerability during global health crises, some experts caution that the aggressive timeline and steep rates could create short-term turbulence in pricing and availability. A significant portion of both generic and brand-name pharmaceuticals sold in the U.S. are either manufactured or sourced from foreign plants — particularly in India, China, and parts of Europe.

Economists warn that higher tariffs could increase costs for American consumers and health systems. “Any sudden increase in tariffs on widely used medications will likely lead to a ripple effect — from importers to hospitals and pharmacies, and ultimately to patients,” said one analyst at a Washington-based policy institute. In an industry already grappling with rising R&D costs and supply chain stressors, the added tariff burden may push smaller pharmaceutical companies to the brink or force them to pass costs along to consumers.

Large U.S.-based manufacturers with strong domestic infrastructure may benefit from reduced competition and new federal incentives aimed at onshoring production. However, the buildout of new facilities and regulatory approvals for domestic production can take years — potentially creating a supply-demand gap in the interim.

Global reactions have been swift. India, a leading supplier of generic drugs to the U.S., criticized the planned tariff hikes as discriminatory, especially in light of existing tensions over oil trade. Meanwhile, trade partners in the EU and Brazil are closely monitoring developments, particularly as the U.S. continues to renegotiate trade terms and tariff structures across multiple sectors.

The pharmaceutical tariffs are just one facet of a broader strategy that also includes revoking the de minimis rule on small imports and instituting high duties on copper and semiconductor products. Each of these actions represents a clear shift toward protectionist policies and reshoring of critical industries.

For the pharmaceutical sector, the coming months could be pivotal. Companies may accelerate reshoring strategies or lobby for exemptions on essential or life-saving drugs. With implementation expected to begin soon, the industry — and the patients who rely on it — may be facing an era of significant transition.

HNI Corporation has announced a definitive agreement to acquire Steelcase Inc. in a cash-and-stock deal valued at approximately $2.2 billion. The strategic acquisition unites two iconic names in workplace furniture and design, combining their strengths in innovation, manufacturing, and dealer networks to form a dominant force in the commercial interiors market.

Under the terms of the deal, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each Steelcase share they own. Based on HNI’s stock price as of August 1, 2025, the total purchase price comes to about $18.30 per share. Once finalized, HNI shareholders will own roughly 64% of the combined entity, while Steelcase shareholders will hold the remaining 36%.

HNI Chairman and CEO Jeffrey Lorenger emphasized the complementary nature of the merger, stating, “This acquisition brings together two respected companies with strong brands and decades of leadership in the industry.” Lorenger will continue to lead the combined company, which will retain HNI’s headquarters in Muscatine, Iowa, and keep Steelcase’s base in Grand Rapids, Michigan.

The new entity will have a pro forma annual revenue of $5.8 billion and adjusted EBITDA of approximately $745 million, with anticipated annual cost synergies of $120 million. Financially, the acquisition positions the company for long-term earnings growth, with projections for accretive non-GAAP EPS by 2027 and a return to pre-acquisition leverage within 18 to 24 months.

The companies’ combined strengths span across corporate, healthcare, education, hospitality, and small-to-midsize business markets. With their complementary product portfolios and broad dealer networks, the merger enhances their ability to serve a wider range of customers with innovative solutions for modern workspaces. Both firms bring decades of product design expertise and a shared commitment to purpose-driven leadership and environmental stewardship.

Steelcase CEO Sara Armbruster called the merger a “bold step” that ushers in a new era for the company, employees, and customers. “Together, we will redefine what’s possible in the world of work, workers, and workplaces,” she said.

The transaction has received strong early support from key stakeholders. Some Steelcase shareholders have already agreed to vote in favor of the deal, and committed financing is in place from JPMorgan Chase and Wells Fargo. The merger is expected to close by the end of 2025, pending shareholder and regulatory approvals.

Advisors for the deal include J.P. Morgan Securities for HNI, and Goldman Sachs and BofA Securities for Steelcase. Legal counsel is being provided by Davis Polk & Wardwell for HNI and Skadden, Arps, Slate, Meagher & Flom for Steelcase.

The deal signals a major consolidation in the commercial furniture sector and positions the combined company to lead the evolution of the workplace at a time when hybrid work, digital transformation, and sustainable design continue to reshape business environments.

Delivered GrossMargin of 15%, Expansion of 250Basis Points OperatingCashFlowof$8.5 Million andAdjustedFreeCashFlowof$7.9Million Strong Order Intake Driven by Operational Flexibility, Reaffirmed Full Year Guidance

CHICAGO, Aug. 04, 2025 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the second quarter ended June 30, 2025.

SecondQuarter 2025Highlights

Revenues of $118.6 million, compared to $147.4 million in the second quarter of 2024, with railcar deliveries of 939 units compared to 1,159 units in the prior year period

Gross margin of 15.0% with gross profit of $17.8 million, compared to gross margin of 12.5% with gross profit of $18.4 million in the second quarter of 2024

Net income of $11.7 million, or $0.34 per share, and Adjusted net income of $3.8 million, or $0.11 per share, reflecting a $51.9 million benefit from a valuation allowance release, partially offset by a $47.6 million non-cash adjustment from the change in warrant liability due to share price appreciation

Adjusted EBITDA was $10.0 million, representing a margin of 8.4%, compared to $12.1 million and a margin of 8.2% in the second quarter of 2024

Received new orders for 1,226 railcars within the quarter valued at $106.9 million

Ended the quarter with a backlog of 3,624 units valued at $316.9 million, up approximately 300 units from prior quarter, reflecting strong order activity and healthy demand

“In the second fiscal quarter, we delivered on our commercial excellence initiatives across the business, supported by strong order intake and healthy customer demand,” said Nick Randall, President and Chief Executive Officer of FreightCar America. “We increased utilization across our four production lines, delivered improved productivity, and benefited from a richer product mix from disciplined pricing. Our ability to remain agile and responsive to customer needs continues to be a key differentiator, particularly in rebuilds and conversions, enabling us to capture meaningful opportunities in a dynamic market.”

Randall continued, “While broader market uncertainty earlier in the year delayed some order activity, we believe the underlying fundamentals point to a meaningful replacement cycle ahead. As that takes shape, our agile manufacturing presence positions us well to capture incremental demand and grow our share. At the same time, we continue to advance our growth strategy by investing in our tank car capabilities, which we expect will strengthen our cost position and support long-term value creation.”

FiscalYear2025 Outlook

The Company has reaffirmed outlook for fiscal year 2025 as follows:

Fiscal2025 Outlook

Year-over-Year GrowthatMidpoint

Railcar Deliveries

4,500 – 4,900 Railcars

7.7%

Revenue

$530 – $595 million

0.6%

AdjustedEBITDA1

$43 – $49 million

7.0%

1. The Company does not provide a reconciliation of forward-looking Adjusted EBITDA guidance due to the inherent difficulty in forecasting and quantifying adjustments necessary to calculate such non-GAAP measure without unreasonable effort. Material changes to such adjustments, including warrant liability and non-core operating items, could affect future GAAP results.

Mike Riordan, Chief Financial Officer of FreightCar America, added, “We’re pleased to reaffirm our full-year guidance, supported by strong margin performance and continued commercial execution across the business, with order activity supporting our healthy backlog. In addition, this quarter marked our fifth consecutive quarter of positive operating cash flow, reflecting the consistency and sustainability of our cash generation engine. Our focus on working capital discipline and operational efficiency has positioned us well to maintain momentum and invest in growth opportunities as we deliver strong performance in the second half of the year.”

SecondQuarter 2025 ConferenceCall&Webcast Information

The Company will host a conference call and live webcast on Tuesday, August 5, at 11:00 a.m. (Eastern Time) to discuss its second quarter 2025 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call. Teleconference details are as follows:

An audio replay of the conference call will be available beginning at 3:00 p.m. (Eastern Time) on Tuesday, August 5, 2025, until 11:59 p.m. (Eastern Time) on Tuesday, August 19, 2025. To access the replay, please dial (844) 512-2921 or (412) 317-6671. The replay passcode is 13754875. An archived version of the webcast will also be available on the FreightCar America Investor Relations website.

AboutFreightCarAmerica

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-LookingStatements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse geopolitical, economic and market conditions, including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials, including steel and aluminum; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion; delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings; potential unexpected changes in laws, rules, and regulatory requirements, including tariffs and trade barriers (including recent United States tariffs imposed or threatened to be imposed on China, Canada, Mexico and other countries and any retaliatory actions taken by such countries); and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAPFinancialMeasures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted EPS, Free cash flow and Adjusted free cash flow. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.

Second quarter sales of $172 million, EPS of $(0.12), Adjusted EBITDA of $5.2 million Continued strong free cash flow generation Updates full year 2025 guidance

NEW ALBANY, Ohio, Aug. 04, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its second quarter ended June 30, 2025.

Second Quarter 2025 Highlights(Results from Continuing Operations; compared with prior year, where comparisons are noted)

Revenues of $172.0 million, down 11.2%, primarily due to softening in global demand.

Operating income of $0.8 million, adjusted operating income of $1.9 million, down compared to operating income of $1.1 million and adjusted operating income of $4.8 million. The decrease in operating income was driven primarily by lower sales volumes.

Net loss from continuing operations of $4.1 million, or $(0.12) per diluted share and adjusted net loss of $2.9 million, or $(0.09) per diluted share, compared to net loss from continuing operations of $1.3 million, or $(0.04) per diluted share and adjusted net income of $1.5 million, or $0.05 per diluted share.

Adjusted EBITDA of $5.2 million, down 36.6%, with an adjusted EBITDA margin of 3.0%, down from 4.2%.

Free cash flow of $17.3 million, up $16.5 million, due to better working capital management. Net debt decreased $31.8 million compared to the year end 2024 level.

Gross margin expansion of 80 basis points versus Q1 2025 due to operational efficiency improvements.

James Ray, President and Chief Executive Officer, said, “Despite continued macroeconomic volatility, particularly a softening in Construction and Agriculture and Class 8 end markets and ongoing concerns around tariff impacts, we were pleased with continued momentum in our second quarter results, which were highlighted by strong free cash generation. During the quarter, we made progress in implementing operational improvements and right sizing our manufacturing footprint, which drove sequential gross margin improvement for the second consecutive quarter. Additionally, as part of our efforts to preserve margin performance, we are continuing our efforts to further reduce our targeted SG&A levels, and we are having constructive negotiations with customers as it relates to mitigating tariff impacts.”

Mr. Ray continued, “We are encouraged by the improved performance in our Global Electrical Systems segment, driven by new business wins outside of the Construction and Agriculture end markets, which continue to see lower demand. The Global Electrical Systems segment also saw margin expansion despite revenues being flat year-over-year. Across our enterprise, we remain focused on execution, delivery, and driving operational efficiency, while managing the potential impact of trade policy.”

Andy Cheung, Chief Financial Officer, added, “We were pleased to see continued strong free cash generation in the quarter, as well as continued improvement in gross margin, as the benefits of our strategic initiatives take hold. Given our successful working capital initiatives, we are raising our free cash outlook to at least $30 million for the full fiscal year. Continued free cash generation and debt paydown remain key focus areas moving forward. During the quarter, we completed the refinancing of our credit facilities, which will further benefit our strategic initiatives and provide increased financial flexibility as we look to drive further cost reductions, margin improvement, and overall operational efficiency.”

Second Quarter Financial Results from Continuing Operations (amounts in millions except per share data and percentages)

Consolidated Results from Continuing Operations

Second Quarter 2025 Results

Second quarter 2025 revenues were $172.0 million, compared to $193.7 million in the prior year period, a decrease of 11.2%. The overall decrease in revenues was due to lower sales as a result of a softening in customer demand across all segments.

Operating income in the second quarter 2025 was $0.8 million compared to $1.1 million in the prior year period. The decrease in operating income was attributable to the impact of lower sales volumes. Second quarter 2025 adjusted operating income was $1.9 million, compared to $4.8 million in the prior year period.

Interest associated with debt and other expenses was $2.3 million and $2.4 million for the second quarter 2025 and 2024, respectively.

Net loss from continuing operations was $4.1 million, or $(0.12) per diluted share, for the second quarter 2025 compared to net loss of $1.3 million, or $(0.04) per diluted share, in the prior year period. Second quarter 2025 adjusted net loss from continuing operations was $2.9 million, or $(0.09) per diluted share, compared to adjusted net income of $1.5 million, or $0.05 per diluted share.

On June 30, 2025, the Company had $30.3 million of outstanding borrowings on its U.S. revolving credit facility and $4.2 million outstanding borrowings on its China credit facility, $45.3 million of cash and $90.6 million of availability from the credit facilities (subject to customary borrowing base and other conditions), resulting in total liquidity of $135.9 million.

Second Quarter 2025 Segment Results

Global Seating Segment

Revenues were $74.5 million compared to $82.4 million for the prior year period, a decrease of 9.6%, due to lower sales volume as a result of decreased customer demand.

Operating income was $2.7 million, compared to $2.1 million in the prior year period, an increase of 29.1%, primarily attributable to lower SG&A expenses. Second quarter 2025 adjusted operating income was $3.1 million compared to $2.9 million in the prior year period.

Global Electrical Systems Segment

Revenues were $53.6 million compared to $53.6 million in the prior year period, essentially flat.

Operating income was $0.7 million compared to an operating loss of $0.5 million in the prior year period. The increase in operating income was primarily attributable to lower salary expense and lower restructuring costs in the current period compared to the prior period. Second quarter 2025 adjusted operating income was $1.2 million compared to $0.8 million in the prior year period.

Trim Systems and Components Segment

Revenues were $43.9 million compared to $57.6 million in the prior year period, a decrease of 23.8%, primarily as a result of decreased customer demand.

Operating income was $0.1 million compared to $2.3 million in the prior year period, a decrease of $2.2 million. The decrease in operating income was primarily attributable to lower sales volumes. Second quarter 2025 adjusted operating income was $0.3 million compared to $4.0 million in the prior year period.

Outlook

CVG updated the Company’s outlook for the full year 2025, based on current market conditions:

Metric

Prior 2025 Outlook ($ millions)

2025 Outlook ($ millions)

Net Sales

$660- $690

$650- $670

Adjusted EBITDA

$22 – $27

$21 – $25

Free Cash Flow

> $20

> $30

This outlook reflects, among others, current industry forecasts for North America Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 252,000 units. The 2024 actual Class 8 truck builds according to the ACT Research was 332,372 units.

Construction and Agriculture end markets are projected to decline approximately 5-15% in 2025. However, we expect the contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, August 5, 2025, at 8:30 a.m. ET. Management intends to reference the Q2 2025 Earnings Call Presentation during the conference call. To participate, dial (800) 549-8228 using conference code 72110. International participants dial (289) 819-1520 using conference code 72110.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 72110#.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions, production of new products, plans for capital expenditures, and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Other Information

Throughout this document, certain numbers in the tables or elsewhere may not sum due to rounding. Rounding may have also impacted the presentation of certain year-on-year percentage changes.

Revenue of $1.08 billion and net income of $22.4 million

Adjusted net income1 of $42.3 million, up 61% y/y

Adjusted EBITDA1 of $82.4 million, with a margin of 7.6%

Diluted EPS of $0.70; Adjusted diluted EPS1 of $1.33, up 59% y/y

Improved net debt by $200 million y/y

Established $100 million share repurchase authorization

Awarded $4.3 billion T-6 aircraft program

RESTON, Va., Aug. 4, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) announced second quarter 2025 financial results. “Our second quarter results reflect V2X’s ability to execute in all market environments and further demonstrate the resiliency of our business,” said Jeremy C. Wensinger, President and Chief Executive Officer. “We believe the overall trends in our market remain positive and that V2X is well positioned to leverage our mission expertise and full lifecycle capabilities to deliver next generation data-enabled solutions that enhance readiness and customer outcomes.”

Mr. Wensinger continued, “We are bringing innovation and new approaches to rapidly deploy solutions for improved readiness, which was exemplified by the recent $4.3 billion T-6 program award. The T-6 aircraft is widely used in a multi-service aviation training program that is critical to ensure new pilot readiness. This award is an example of the strategy we are executing and it’s an honor to have been selected to help ensure that pilots in the U.S. Air Force, Navy, and Army will be trained and ready for their next mission. V2X will use commercial-based approaches to provide full spectrum supply chain management solutions to enable this essential training-mission for over 700 aircraft.”

“I’d like to thank all our employees for their contributions during the quarter and specifically recognize the recent success achieving full operational capability on the Army’s largest training program. This is a remarkable accomplishment, which will ensure the delivery of critical training related services to Army warfighters worldwide by infusing cutting-edge innovations to meet ever-evolving needs.”

Mr. Wensinger concluded, “We are transforming V2X to be a leader in data-enabled mission solutions across all domains. The growth initiatives fueling this advancement include optimizing our core for on contract growth, leveraging capabilities into adjacent markets, extending new offerings, and strategically investing both internally and externally. We are executing on these initiatives today and believe they will accelerate growth, create differentiation, and yield value in the years to come.”

Second Quarter 2025 Results

“V2X reported revenue of $1.08 billion in the quarter,” said Shawn Mural, Senior Vice President and Chief Financial Officer. “The performance in the second quarter was strong and provides additional confidence to deliver on our full year commitments. The second quarter results reflect the great job our team has done in optimizing and refining our processes and procedures. I’m very proud of what we have been able to achieve over the past year.”

“For the quarter, the Company reported operating income of $52.9 million and adjusted operating income1 of $77.3 million, increasing $11.5 million dollars or 18% from the prior year. V2X delivered adjusted EBITDA1 of $82.4 million, with a margin of 7.6%. Net income for the quarter was $22.4 million dollars. Adjusted net income1 was $42.3 million dollars, increasing $16.1 million dollars or 61% year-over-year. Second quarter GAAP diluted EPS was $0.70. Adjusted diluted EPS1 for the quarter was $1.33, increasing 59% year-over-year.”

“Second quarter net cash provided by operating activities was $28.5 million. Adjusted net cash provided by operating activities1 increased $112.1 million year-over-year to $58.3 million.”

Mr. Mural continued, “During the quarter we further progressed our capital allocation strategy by establishing a $100 million share repurchase authorization. We believe the strong cash flow characteristics of our business support V2X’s ability to create additional long-term value through the efficient deployment of capital. The core tenets of our deployment strategy include opportunistically repurchasing shares, strategic acquisitions, internal investments for growth, and reducing leverage via debt reduction.”

Increasing 2025 Adjusted EPS1 Guidance

Mr. Mural concluded, “Given the year-to-date performance and trends in our business, the Company is increasing its adjusted EPS guidance for 2025 and reaffirming its revenue, adjusted EBITDA, and adjusted net cash1 ranges.”

Guidance is as follows:

$ millions, except for per share amounts

Prior 2025 Guidance

Updated 2025 Guidance

Revenue

$4,375

$4,500

$4,375

$4,500

Adjusted EBITDA1

$305

$320

$305

$320

Adjusted Diluted Earnings Per Share1

$4.45

$4.85

$4.65

$4.95

Adjusted Net Cash Provided by Operating Activities1

$150

$170

$150

$170

The Company is not providing a quantitative reconciliation with respect to the foregoing forward-looking non-GAAP measures in reliance on the “unreasonable efforts” exception set forth in the SEC rules because certain financial information, the probable significance of which cannot be determined, is not available and cannot be reasonably estimated. For example, unusual, one-time, non-ordinary, or non-recurring costs, which relate to mergers and acquisitions (“M&A”), integration and related activities cannot be reasonably estimated. Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Second Quarter Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Monday, August 4, 2025. U.S.-based participants may dial in to the conference call at 877-300-8521, while international participants may dial 412-317-6026. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/MPvl2xBdpg3

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through August 18, 2025, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10200918.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the Company’s website at https://gov2x.com. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management. Forward-looking statements in this press release, include, but are not limited to our future performance and capabilities; all of the statements and items listed under “Increasing 2025 Adjusted EPS Guidance” above and other assumptions contained therein for purposes of such guidance; our belief that prior performance provides substantial visibility for future performance; market trends; our expectations that the foreign military sales and international markets represent a large and growing addressable opportunity; and our belief that our strategy, visibility, and targeted growth opportunities provide substantial opportunities for value creation.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

Highly Complementary Brand Portfolios, Dealer Networks, and Industry Segments will Enhance Customer Reach

Combined Capabilities to Drive Accretion and Accelerate Strategic Initiatives to Better Serve Customers

HNI and Steelcase to Host Conference Call and Webcast at 8:30 AM ET Today

MUSCATINE, Iowa & GRAND RAPIDS, Mich.–(BUSINESS WIRE)– HNI Corporation (NYSE: HNI) and Steelcase Inc. (NYSE: SCS) today announced that they have entered into a definitive agreement under which HNI will acquire Steelcase in a cash and stock transaction, with a total consideration of approximately $2.2 billion to Steelcase common shareholders.

Under the terms of the agreement, Steelcase shareholders will receive $7.20 in cash and 0.2192 shares of HNI common stock for each share of Steelcase they own. The implied per share purchase price of $18.30 is based on HNI’s closing share price of $50.62 on Friday, August 1, 2025, reflecting a valuation multiple at transaction close1 for Steelcase of approximately 5.8x TTM2 Adjusted EBITDA, inclusive of run-rate cost synergies of $120 million. Upon closing, HNI shareholders will own approximately 64% and Steelcase shareholders will own approximately 36% of the combined company.

“This acquisition brings together two respected companies with complementary strengths and represents an exciting milestone in HNI’s growth journey,” said Jeffrey Lorenger, HNI’s Chairman, President, and Chief Executive Officer. “We have long admired Steelcase for its insight-led approach, which has helped shape our industry for decades. With the Steelcase portfolio of brands and as in-office work trends accelerate, we will be even better positioned to meet the evolving needs of the workplace, enhance dealer and customer relationships, unlock new opportunities for growth, and create compelling value for the combined company’s shareholders.”

“Joining with HNI is a bold step that marks the next era for Steelcase, our customers, dealers, and employees,” said Sara Armbruster, President and Chief Executive Officer of Steelcase. “Together, we will be positioned to redefine what’s possible in the world of work, workers, and workplaces. Like Steelcase, HNI is an organization that leads with purpose, shares similar values, and puts the customer at the center of everything they do. I’m excited to see this combination shape our industry.”

Compelling Strategic Benefits

Combines Complementary Portfolios and Dealer Networks to Enhance Customer Reach: HNI’s and Steelcase’s geographic footprints and dealer networks are highly complementary, which bolsters the combined company’s ability to serve more customers across diverse industry segments, including small and medium business, large corporate, healthcare, education, and hospitality customers. The companies have the industry’s most respected and widely recognized brands, allowing the combined company to better support an expanded customer base and capture growth opportunities from industry tailwinds.

Brings Together World-Class Capabilities: Uniting a strong innovation engine with operational excellence, the combined organization will accelerate delivery of more advanced solutions to customers, while increasing value for shareholders.

Strong Financial Profile: The combined company will have pro forma annual revenue of approximately $5.8 billion, pro forma Adjusted EBITDA of approximately $745 million, and 2.1x net leverage. 3 These metrics are based on each company’s respective last reported 12-month results and are inclusive of annual run-rate synergies. Net leverage is expected to return to pre-acquisition levels within 18-24 months.

Highly Synergistic Combination: With recent experience in M&A execution and a disciplined integration approach, HNI’s proven ability to successfully combine core capabilities and deliver cost synergies will maximize the new organization’s future success. Annual run-rate synergies are expected to total $120 million when fully mature. The company projects the combination will be highly accretive to non-GAAP earnings per share beginning in 2027.

Accelerates Strategic Framework: The acquisition is fully aligned with HNI’s strategic framework focused on driving long-term profitable growth. With an enhanced financial profile, the new company will also be better positioned to accelerate and increase investments in long-term operational enhancements, digital transformation, and customer-centric buying experiences.

HNI and Steelcase share a deep commitment to respecting people, protecting the planet, operating with excellence, and acting with integrity. As a stronger and more diversified organization, the combined company will bring together the strengths of both HNI and Steelcase to create new career growth opportunities for team members, deliver more value for customers, and further support and invest in the communities where they operate.

Following the close of the transaction, the combined company will continue to be led by Jeffrey Lorenger, HNI’s Chairman, President, and Chief Executive Officer. HNI will continue to operate its corporate headquarters in Muscatine, Iowa, and Steelcase will maintain its headquarters in Grand Rapids, Michigan. HNI will maintain the Steelcase brand following the transaction’s close. In addition, post-closing, HNI’s Board of Directors will expand from 10 directors to 12, to include two of Steelcase’s current independent board members.

Approvals, Financing, and Timing to Close

The transaction, which is expected to close by the end of calendar year 2025, is subject to approval by HNI and Steelcase shareholders, the receipt of required regulatory clearances, and the satisfaction of other customary closing conditions.

Certain shareholders of Steelcase have entered into a voting agreement to vote in favor of the transaction at the special meeting of Steelcase shareholders to be held in connection with the transaction.

In support of the transaction, JPMorgan Chase Bank, N.A. and Wells Fargo Bank, N.A. have executed a commitment letter to provide committed financing to HNI, subject to the terms and conditions therein.

Advisors

J.P. Morgan Securities LLC is serving as exclusive financial advisor to HNI, and Davis Polk & Wardwell LLP is serving as legal counsel. Goldman Sachs & Co. LLC and BofA Securities are serving as financial advisors to Steelcase, and Skadden, Arps, Slate, Meagher & Flom LLP is serving as legal counsel.

Conference Call, Webcast and Presentation

HNI and Steelcase will hold a conference call to discuss the transaction today, August 4, 2025 at 8:30 a.m. Eastern Time. To listen, call (855) 761-5600 and use conference ID number 7006893. Access to a live audio webcast and slide presentation will be available on the Events & Presentations page of the Investor Relations section of HNI Corporation’s website or at the following link: https://events.q4inc.com/attendee/369737700 [events.q4inc.com].

About HNI Corporation

HNI Corporation (NYSE: HNI) has been improving where people live, work, and gather for more than 75 years. HNI is a manufacturer of workplace furnishings and residential building products, operating under two segments. The Workplace Furnishings segment is a leading global designer and provider of commercial furnishings, going to market under multiple unique brands. The Residential Building Products segment is the nation’s leading manufacturer and marketer of hearth products, which include a full array of gas, electric, wood, and pellet-burning fireplaces, inserts, stoves, facings, and accessories. More information can be found on the Corporation’s website at www.hnicorp.com.

About Steelcase

Steelcase (NYSE: SCS) is a global design and thought leader in the world of work. Our purpose is to help the world work better. Along with more than 30 creative and technology partner brands, we research, design and manufacture furnishings and solutions for many of the places where work happens — including offices, homes, and learning and health environments. Together with our 11,300 employees, we’re working toward better futures for the wellbeing of people and the planet. Our solutions come to life through our global community of expert Steelcase dealers in approximately 790 locations, store.steelcase.com and other retail partners. For more information, visit Steelcase.com.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934 and Section 27A of the Securities Act of 1933, which involve risks and uncertainties. Any statements about HNI’s, Steelcase’s or the combined company’s plans, objectives, expectations, strategies, beliefs, or future performance or events and any other statements to the extent they are not statements of historical fact are forward-looking statements. Words, phrases or expressions such as “anticipate,” “believe,” “could,” “confident,” “continue,” “estimate,” “expect,” “forecast,” “hope,” “intend,” “likely,” “may,” “might,” “objective,” “plan,” “possible,” “potential,” “predict,” “project”, “target,” “trend” and similar words, phrases or expressions are intended to identify forward looking statements but are not the exclusive means of identifying such statements. Forward-looking statements are based on information available and assumptions made at the time the statements are made. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Forward-looking statements in this communication include, but are not limited to, statements about the benefits of the transaction between HNI and Steelcase (the “Transaction”), including future financial and operating results, the combined company’s plans, objectives, expectations and intentions, and other statements that are not historical facts.

The following Transaction-related factors, among others, could cause actual results to differ materially from those expressed in or implied by forward-looking statements: the occurrence of any event, change, or other circumstance that could give rise to the right of one or both of the parties to terminate the definitive merger agreement between HNI and Steelcase; the outcome of any legal proceedings that may be instituted against HNI or Steelcase; the possibility that the Transaction does not close when expected or at all because required regulatory, shareholder, or other approvals and other conditions to closing are not received or satisfied on a timely basis or at all (and the risk that seeking or obtaining such approvals may result in the imposition of conditions that could adversely affect the combined company or the expected benefits of the Transaction); the risk that the benefits from the Transaction may not be fully realized or may take longer to realize than expected, including as a result of changes in, or problems arising from, general economic and market conditions, interest and exchange rates, monetary policy, trade policy (including tariff levels), laws and regulations and their enforcement, and the degree of competition in the geographic and business areas in which HNI and Steelcase operate; any failure to promptly and effectively integrate the businesses of HNI and Steelcase; the possibility that the Transaction may be more expensive to complete than anticipated, including as a result of unexpected factors or events; reputational risk and potential adverse reactions of HNI’s or Steelcase’s customers, employees or other business partners, including those resulting from the announcement, pendency or completion of the Transaction; the dilution caused by HNI’s issuance of additional shares of its capital stock in connection with the Transaction; and the diversion of management’s attention and time to the Transaction from ongoing business operations and opportunities.

Additional important factors relating to Steelcase that could cause actual results to differ materially from those in forward-looking statements include, but are not limited to, competitive and general economic conditions domestically and internationally; acts of terrorism, war, governmental action, natural disasters, pandemics and other Force Majeure events; cyberattacks; changes in the legal and regulatory environment; changes in raw material, commodity and other input costs; currency fluctuations; changes in customer demand; and the other risks and contingencies detailed in Steelcase’s most recent Annual Report on Form 10-K and its other filings with the U.S. Securities and Exchange Commission (the “SEC”).

Additional important factors relating to HNI that could cause actual results to differ materially from those in forward-looking statements include, but are not limited to, HNI’s ultimate realization of the anticipated benefits of the acquisition of Kimball International; disruptions in the global supply chain; the effects of prolonged periods of inflation and rising interest rates; labor shortages; the levels of office furniture needs and housing starts; overall demand for HNI’s products; general economic and market conditions in the United States and internationally; industry and competitive conditions; the consolidation and concentration of HNI’s customers; HNI’s reliance on its network of independent dealers; change in trade policy, including with respect to tariff levels; changes in raw material, component, or commodity pricing; market acceptance and demand for HNI’s new products; changing legal, regulatory, environmental, and healthcare conditions; the risks associated with international operations; the potential impact of product defects; the various restrictions on HNI’s financing activities; an inability to protect HNI’s intellectual property; cybersecurity threats, including those posed by potential ransomware attacks; impacts of tax legislation; and force majeure events outside HNI’s control, including those that may result from the effects of climate change, a description of which risks and uncertainties and additional risks and uncertainties can be found in HNI’s most recent Annual Report on Form 10-K and its other filings with the SEC.

These factors are not necessarily all of the factors that could cause HNI’s, Steelcase’s or the combined company’s actual results, performance, or achievements to differ materially from those expressed in or implied by any forward-looking statements. Other unknown or unpredictable factors also could harm HNI’s, Steelcase’s or the combined company’s results.

All forward-looking statements attributable to HNI, Steelcase, or the combined company, or persons acting on HNI’s or Steelcase’s behalf, are expressly qualified in their entirety by the cautionary statements set forth above. Forward-looking statements speak only as of the date they are made, and HNI and Steelcase do not undertake or assume any obligation to update publicly any of these statements to reflect actual results, new information or future events, changes in assumptions, or changes in other factors affecting forward-looking statements, except to the extent required by applicable law. If HNI or Steelcase updates one or more forward-looking statements, no inference should be drawn that HNI or Steelcase will make additional updates with respect to those or other forward-looking statements. Further information regarding HNI, Steelcase and factors that could affect the forward-looking statements contained herein can be found in HNI’s Annual Report on Form 10-K, its Quarterly Reports on Form 10-Q, and its other filings with the SEC, and in Steelcase’s Annual Report on Form 10-K, its Quarterly Reports on Form 10-Q, and its other filings with the SEC.

No Offer or Solicitation

This communication is not an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

Important Information and Where to Find It

In connection with the Transaction, HNI will file with the SEC a Registration Statement on Form S-4 to register the shares of HNI common stock to be issued in connection with the Transaction. The Registration Statement will include a joint proxy statement of HNI and Steelcase that also constitutes a prospectus of HNI. The definitive joint proxy statement/prospectus will be sent to the shareholders of each of HNI and Steelcase.

INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT ON FORM S-4 AND THE JOINT PROXY STATEMENT/PROSPECTUS WHEN THEY BECOME AVAILABLE, AS WELL AS ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN CONNECTION WITH THE TRANSACTION OR INCORPORATED BY REFERENCE INTO THE JOINT PROXY STATEMENT/PROSPECTUS, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION REGARDING HNI, STEELCASE, THE TRANSACTION AND RELATED MATTERS.

Investors and security holders may obtain free copies of these documents and other documents filed with the SEC by HNI or Steelcase through the website maintained by the SEC at http://www.sec.gov or from HNI at its website, www.hnicorp.com, or from Steelcase at its website, www.steelcase.com (information included on or accessible through either of HNI’s or Steelcase’s website is not incorporated by reference into this communication).

Participants in the Solicitation

HNI, Steelcase, their respective directors and certain of their respective executive officers may be deemed to be participants in the solicitation of proxies in connection with the Transaction under the rules of the SEC. Information about the interests of the directors and executive officers of HNI and Steelcase and other persons who may be deemed to be participants in the solicitation of proxies in connection with the Transaction and a description of their direct and indirect interests, by security holdings or otherwise, will be included in the joint proxy statement/prospectus related to the Transaction, which will be filed with the SEC. Information about the directors and executive officers of HNI and their ownership of HNI common stock is set forth in the definitive proxy statement for HNI’s 2025 Annual Meeting of Shareholders, filed with the SEC on March 11, 2025; in Table I (Information about our Executive Officers) at the end of Part I of HNI’s Annual Report on Form 10 K for the fiscal year ended December 28, 2024, filed with the SEC on February 25, 2025; in HNI’s Current Report on Form 8 K filed with the SEC on June 20, 2025; in the Form 3 and Form 4 statements of beneficial ownership and statements of changes in beneficial ownership filed with the SEC by HNI’s directors and executive officers; and in other documents filed by HNI with the SEC. Information about the directors and executive officers of Steelcase and their ownership of Steelcase common stock can be found in Steelcase’s definitive proxy statement in connection with its 2025 Annual Meeting of Shareholders, filed with the SEC on May 28, 2025; under the heading “Supplementary Item. Information About Our Executive Officers” in Steelcase’s Annual Report on Form 10 K for the fiscal year ended February 28, 2025, filed with the SEC on April 18, 2025; in Steelcase’s Amendment No. 1 to Current Report on Form 8-K/A filed with the SEC on July 11, 2025; in the Form 3 and Form 4 statements of beneficial ownership and statements of changes in beneficial ownership filed with the SEC by Steelcase’s directors and executive officers; and in other documents filed by Steelcase with the SEC. Free copies of the documents referenced in this paragraph may be obtained as described above under the heading “Important Information and Where to Find It.”

____________________

1 Assumes transaction close at 12/31/2025 with $21 million of net debt; equity consideration is at time of announcement

2 TTM as of 05/30/2025

3 Includes EBITDA add-backs, which encompass two-year look-forward run-rate synergies, as defined within the credit agreement

HNI Corporation

Investors Vincent P. Berger Executive Vice President and Chief Financial Officer (563) 272-7400

Matthew S. McCall Vice President, Investor Relations and Corporate Development (563) 275-8898

Media Lauren Odell / Felipe Ucrós Gladstone Place Partners hni@gladstoneplace.com (212) 230-5930

HOUSTON, Aug. 4, 2025 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”) and Orange 142, LLC (“Orange 142”), today announced that the Company will report financial results for the second quarter ended June 30, 2025 on Tuesday, August 5, 2025 after the U.S. stock market closes.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT) combines cutting-edge sell-side and buy-side advertising solutions, providing data-driven digital media strategies that enhance reach and performance for brands, agencies, and publishers of all sizes. Our sell-side platform, Colossus SSP, offers curated access to premium, growth-oriented media properties throughout the digital ecosystem. On the buy-side, Orange 142 delivers customized, audience-focused digital marketing and advertising solutions that enable mid-market and enterprise companies to achieve measurable results across a range of platforms, including programmatic, search, social, CTV, and influencer marketing. With extensive expertise in high-growth sectors such as Energy, Healthcare, Travel & Tourism, and Financial Services, our teams deliver performance strategies that connect brands with their ideal audiences.

At Direct Digital Holdings, we prioritize personal relationships by humanizing technology, ensuring each client receives dedicated support and tailored digital marketing solutions regardless of company size. This empowers everyone to thrive by generating billions of monthly impressions across display, CTV, in-app, and emerging media channels through advanced targeting, comprehensive data insights, and cross-platform activation. DDH is “Digital advertising built for everyone.”

CALGARY, AB, Aug. 3, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces that Obsidian Energy Ltd. (“Obsidian“) has entered into a definitive agreement with Delek Group Ltd. (“Delek“) in respect of the sale of all 9,139,784 common shares (“Common Shares“) in the capital of InPlay currently held by Obsidian (the “Transaction“).

“We are thrilled to welcome the Delek Group to our organization as part of their impressive oil and gas portfolio,” said Doug Bartole, President and CEO of InPlay Oil Corp. “Delek holds a 45% working interest in the largest natural gas field in the Mediterranean, with an estimated 23 TCF of recoverable natural gas. They have also played a key role in the growth of Ithaca Energy plc, where they hold a 52% equity stake, increasing production from 30,000 boe/d to over 120,000 boe/d since their initial investment. We look forward to partnering with Delek to continue building InPlay into a long-term, sustainable, growth-oriented Canadian oil and gas producer, with a strong focus on per-share growth and consistent returns to shareholders.”

“Delek is excited to partner with InPlay as our investment in the Canadian energy sector,” said Ehud (Udi) Erez, Chairman of the Board of the Delek Group. “We identified Canada as a strong and stable jurisdiction for our oil and gas investment, and InPlay stood out with its dynamic team and deep expertise in the Canadian market. InPlay has built a formidable track record through strong operational performance and strategic, accretive acquisitions. We look forward to seeing InPlay’s continued growth and continued success.”

The Transaction is expected to occur in the first half of August 2025 and remains subject to customary conditions to closing.

In connection with the Transaction, InPlay has entered into a registration rights agreement with Delek (the “Registration Rights Agreement“) and an investor rights agreement (the “Investor Rights Agreement“) substantially in the forms entered into between InPlay and Obsidian. The Registration Rights Agreement and Investor Rights Agreement are conditional upon closing of the Transaction.

The Investor Rights Agreement provides that, conditional upon closing of the Transaction, InPlay will appoint two nominees of Delek to the Board of Directors of InPlay (the “Board“) immediately following closing of the Transaction. For so long as Delek holds 20% or more of the issued and outstanding Common Shares and the Board is comprised of eight (8) members, Delek will be entitled to maintain two (2) board nominees. Delek has agreed that, subject to certain conditions, in respect of the election of directors and the appointment of the auditor’s at InPlay’s annual general meeting to be held in 2026 and the appointment of the auditor’s at InPlay’s annual general meeting to be held in 2027, Delek will vote (or, at Delek’s discretion, abstain or cause to be abstained from voting) all Common Shares held by it in accordance with the recommendations of the Board or management of InPlay. Additionally, the Investor Rights Agreement provides Delek with certain pre-emptive and participation rights with respect to certain equity offerings undertaken by InPlay.

The Registration Rights Agreement and the Investor Rights Agreement will be filed on InPlay’s SEDAR+ profile at www.sedarplus.com in due course.

About InPlay Oil Corp.

InPlay is a growth-oriented, sustainable oil and gas producer focused on long-term value creation for its shareholders. The Company’s operations are centered in the Western Canadian Sedimentary Basin, where InPlay holds a diverse portfolio of oil and natural gas assets. InPlay is committed to delivering strong per-share growth, maintaining a disciplined approach to capital investment, and providing consistent returns to shareholders.

About Delek Group

Delek is an independent E&P and the pioneering visionary behind the development of the East Med. With major finds in the Levant Basin, including Leviathan (21.4 TCF) and Tamar (11.2 TCF no longer owned by Delek) and others, Delek is leading the region’s development into a major natural gas export hub. In addition, Delek has invested in the North Sea, with its subsidiary, Ithaca Energy. Delek is one of Israel’s largest and most prominent companies with a consistent track record of growth. Its shares are traded on the Tel Aviv Stock Exchange (TASE:DLEKG) and are part of the TA 35 Index.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President, Business & Corporate Development, InPlay Oil Corp., Telephone: (587) 893-6804

Key Points: – Global M&A value reaches $2.6 trillion YTD, the highest since the 2021 post-pandemic surge. – AI, big tech, and private equity lead activity despite fewer total deals and tariff tensions. – U.S. megadeals and renewed corporate confidence drive optimism for more deals ahead.

Global mergers and acquisitions (M&A) activity has surged to $2.6 trillion year-to-date, making 2025 the most active year since the 2021 boom, as companies aggressively pursue growth and innovation—particularly in artificial intelligence. The total value of deals has risen 28% from the same period last year, even though the actual number of transactions is down 16%, according to data from Dealogic.

Several U.S. megadeals have fueled the resurgence, including Union Pacific’s proposed $85 billion acquisition of Norfolk Southern and OpenAI’s massive $40 billion funding round led by Japan’s SoftBank. These transactions signal a bold appetite for scale and future-proofing in the face of evolving technologies and regulatory dynamics.

What’s driving this momentum? Experts say companies are seeking to stay ahead in a transformative AI race, while adapting to a more settled political and regulatory environment following the initial uncertainties surrounding the Trump administration’s trade tariffs and antitrust posture.

Private equity has also re-entered the scene with major moves. Examples include Sycamore Partners’ $10 billion buyout of Walgreens Boots Alliance and Advent’s revised $6.4 billion bid for UK firm Spectris. These moves show that buyout firms are growing confident in valuations and exit opportunities once again.

While healthcare led the charge in previous years, technology and electronics are now driving deal volume, especially in the U.S. and UK. Notable moves include Samsung’s $1.7 billion acquisition of FlaktGroup, which specializes in data center cooling—an essential infrastructure for AI systems.

The largest deal in EMEA this year came from Palo Alto Networks, which acquired Israeli cybersecurity company CyberArk for $25 billion. Rising AI-driven threats have made cybersecurity a top priority, prompting record valuations in the space.

Looking ahead, dealmakers at JPMorgan and other institutions remain bullish. The combination of AI demand, digital infrastructure needs, and steady leadership in corporate boardrooms suggests that the second half of 2025 could see even more high-profile M&A activity.

LOS ANGELES, Aug. 04, 2025 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (the “Company”) announced today that it has entered into a stipulation of settlement to resolve two stockholder derivative lawsuits pending in the Court of Chancery of the State of Delaware (the “Court”) on behalf of the Company against certain current and former directors and officers of the Company. The stockholder derivative claims were filed in June 2021 (Case No. 2021-0511-NAC, relating to the Company’s December 2020 merger with Fog Cutter Capital Group), and March 2022 (Case No. 2022-0254-NAC, relating to the Company’s June 2021 recapitalization).

The settlement will resolve all claims asserted against the named defendants in the derivative lawsuits without any liability or wrongdoing attributed to them personally or the Company. Under the terms of the proposed settlement, the Company’s Board of Directors agreed to adopt and implement certain corporate governance modifications. In addition, the Company’s insurers will pay to the Company $10 million, from which fees and expenses of plaintiffs’ counsel will be deducted, and Fog Cutter Holdings LLC will contribute 200,000 shares of Twin Hospitality Group Inc. (NASDAQ: TWNP), to the Company.

The settlement is subject to approval of the Court, and non-objection by the United States.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit fatbrands.com.

Forward Looking Statements

This news release contains forward-looking statements within the meaning of certain securities laws, including the Private Securities Litigation Reform Act of 1995, including statements regarding the agreement to settle the pending derivative lawsuits, and other statements that are not purely historical facts. These statements involve risks and uncertainties, including, among others, the uncertainty of obtaining court approval and non-objection by the United States of the proposed settlement, whether any proposed settlement is appealed, and the timing of the settlement payment. There can be no assurance that the litigation will be finally resolved in accordance with the agreement or at all. For a further description of additional risks and uncertainties relating to the business of the Company, see the Company’s filings with the Securities and Exchange Commission, including the Company’s Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. Any forward-looking statements are made only as of the date hereof and the Company does not intend to update or revise any of them, except as required by law.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Product Updates All Three Trials Are On Schedule. Ocugen reported a 2Q25 loss of $14.7 million or $(0.05) per share. During the quarter, the clinical trials made progress to keep the products on schedule for 3 BLA filings beginning in 2026. The quarter also included a licensing agreement covering OCU400 in South Korea and the reverse merger to form OthroCellix, a new company focused on regenerative medicine.

OrthoCellix Has Been Formed To Develop NeoCart. Ocugen and Carisma Therapeutics, Inc. announced a reverse merger that will create a new company developing regenerative cellular therapies. As discussed in our Research Note on June 24, NeoCart cellular therapy is outside its main focus. The transaction is expected to close in September-October with the new company valued at $150 million. The Phase 3 pivotal trial is expected to begin in FY2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")