Apple Inc. (AAPL) is ramping up its domestic investment strategy with a newly announced $100 billion commitment to U.S. manufacturing and infrastructure, expanding its total U.S. investment to $600 billion over the next four years. The announcement comes just hours ahead of a scheduled White House event where Apple CEO Tim Cook will join President Donald Trump in the Oval Office.

The announcement is viewed as both a response to and a strategic buffer against mounting trade tensions. The Trump administration has signaled its intent to impose a 25% tariff on iPhones imported from India, where Apple now manufactures the majority of U.S.-bound iPhones after shifting production away from China.

These escalating tariff threats are already hitting the bottom line. In its most recent quarterly earnings report, Apple disclosed an $800 million tariff-related impact and forecasted another $1.1 billion in related costs this quarter. The company’s shift toward increased U.S. investment appears aimed at minimizing long-term exposure to geopolitical trade risks while addressing growing political pressure to manufacture more within the United States.

The centerpiece of this new initiative is the American Manufacturing Program, which will involve expanded partnerships with U.S.-based suppliers, additional AI-focused data centers, and a potential new semiconductor facility. These moves reflect a broader trend in tech: companies are reassessing global supply chains not just for efficiency, but for resiliency.

Apple’s share price responded sharply to the news, jumping more than 5% in midday trading. The stock move reflects both investor confidence in Apple’s ability to navigate regulatory challenges and the perceived benefits of deeper integration into the U.S. industrial base.

For Apple, this could be a turning point. The tech giant has long relied on overseas manufacturing for its scale, efficiency, and cost advantages. But the dual pressures of tariffs and supply chain vulnerabilities exposed during the COVID-19 pandemic have reshaped that calculus. Bringing more production stateside not only helps Apple hedge against future tariffs—it may also give the company greater control over component access and intellectual property protections.

Still, scaling U.S.-based iPhone production remains a complex challenge. Industry experts warn that building out sufficient infrastructure, skilled labor pools, and logistical networks could take years. Apple’s long-term strategy may involve a hybrid model, combining strategic U.S. investments with continued production in global hubs like India and Vietnam.

With the 2026 presidential election already on the horizon, companies like Apple are likely to face increased scrutiny over domestic job creation and industrial policy alignment. This latest move positions Apple as both a responsive corporate citizen and a resilient global operator—prepared for whatever comes next in an increasingly fragmented trade landscape.

– Total net sales of $144.0 million, up 9% over $131.7 million in prior year second quarter –

– Net income of $1.6 million, up from $0.6 million in prior year second quarter –

– EBITDA of $6.1 million, up 9% over $5.6 million in prior year second quarter –

– Continued to execute on stock repurchase plan –

– Board of Directors approves $0.14 per share quarterly dividend –

ST. PETERSBURG, Fla., Aug. 05, 2025 (GLOBE NEWSWIRE) — Superior Group of Companies, Inc. (NASDAQ: SGC) (the “Company”), today announced its second quarter 2025 results.

“We were able to grow revenue 9% over the prior year, led by Branded Products sales climbing a very healthy 14%, resulting in strong sequential improvement from the first quarter,” said Michael Benstock, Chief Executive Officer. “We are experiencing modest improvement in client sentiment and we will continue to leverage our diverse sourcing channels and marketing strategies to make the most of market conditions. With our strong balance sheet and cost actions taken during the year, we’re able to navigate changing market conditions, invest for future growth and return capital to shareholders whenever possible. In addition to our consistent dividend, during the quarter we also continued to repurchase shares which we consider a compelling value.”

Second Quarter Results

For the second quarter ended June 30, 2025, net sales were $144.0 million, up from second quarter 2024 net sales of $131.7 million. Pretax earnings of $1.8 million were up from $0.7 million in the second quarter of 2024. Net earnings of $1.6 million or $0.10 per diluted share were up from net income of $0.6 million or $0.04 per diluted share for the second quarter of 2024.

Second Quarter 2025 Dividend

The Board of Directors declared a quarterly dividend of $0.14 per share, payable August 29, 2025 to shareholders of record as of August 18, 2025.

Share Repurchase Update

The Company allocated $4.0 million to repurchasing approximately 390,000 shares during the second quarter, resulting in $12.3 million remaining under its existing repurchase authorization at quarter end.

2025 Full-Year Outlook

The Company is maintaining its full-year revenue outlook range of $550 million to $575 million.

Webcast and Conference Call

The Company will host a webcast and conference call at 5:00 pm Eastern Time today. The live webcast and archived replay can be accessed in the investor relations section of the Company’s website at https://ir.superiorgroupofcompanies.com/Presentations. Interested individuals may also join the teleconference by dialing 1-844-861-5505 for U.S. dialers and 1-412-317-6586 for International dialers. The Canadian Toll-Free number is 1-866-605-3852. Please ask to be joined to the Superior Group of Companies call. A telephone replay of the teleconference will be available through August 19, 2025. To access the replay, dial 1-877-344-7529 in the United States or 1-412-317-0088 from international locations. Canadian dialers can access the replay at 855-669-9658. Please reference conference number 7254182 for replay access.

Certain matters discussed in this press releaseare “forward-looking statements“ intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified by use of the words “may,” “will,” “should,” “could,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “project,” “potential,“ or “plan“ or the negative of these words or other variations on these words or comparable terminology. Forward-looking statements in this press releasemay include, without limitation:(1)projections of revenue, income, and other items relating to our financial position and results of operations, including short term and long term plans for cash,(2) statements of our plans, objectives, strategies, goals and intentions, (3) statements regarding the capabilities, capacities, market position and expected development of our business operations and (4) statements of expected industry and general economic trends.

Such forward-looking statements are subject to certain risks and uncertainties that may materially adversely affect the anticipated results. Such risks and uncertainties include, but are not limited to, the following: the impact of competition;the effect of existing and/or new or expanded tariffs, uncertainties related to supply disruptions, inflationary environment (including with respect to the cost of finished goods and raw materials and shipping costs), employment levels (including labor shortages), and general economic and political conditions in the areas of the world in which the Company operates or from which it sources its supplies or the areas of the United States of America (“U.S.“ or “United States“) in which the Company‘s customers are located;changes in the healthcare,retail chain,food service, transportation and other industrieswhere uniforms and service apparel are worn; our ability to identify suitable acquisition targets, discover liabilities associated with such businesses during the diligence process, successfully integrate any acquired businesses, or successfully manage our expanding operations; the price and availability of raw materials; attracting and retaining senior management and key personnel; the effect of the Company‘s previously disclosed material weaknessin internal control over financial reporting; the Company may identify a material weakness in internal control in the future, which could result in us notpreventing or detecting on a timely basis a material misstatement of the Company‘s financial statements and to maintain effective internal control over financial reporting;and other factors described in the Company‘s filings with the Securities and Exchange Commission, including those described in the “Risk Factors“ section ofour Annual Report on Form 10-K for the fiscal year ended December 31, 2024and the Quarterly Report on Form 10-Q for the quarter ended June 30, 2025. Shareholders, potential investors and other readers are urged to consider these factors carefully in evaluating the forward-looking statements made herein and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements made herein are only made as of the date of this press releaseand we disclaim any obligation to publicly update such forward-looking statements to reflect subsequent events or circumstances, except as may be required by law.

About Superior Group of Companies, Inc. (SGC):

Established in 1920, Superior Group of Companies is comprised of three attractive business segments each serving large, fragmented and growing addressable markets. Across Healthcare Apparel, Branded Products and Contact Centers, each segment enables businesses to create extraordinary brand engagement experiences for their customers and employees. SGC’s commitment to service, quality, advanced technology, and omnichannel commerce provides unparalleled competitive advantages. We are committed to enhancing shareholder value by continuing to pursue a combination of organic growth and strategic acquisitions. For more information, visit www.superiorgroupofcompanies.com.

Alcon (NYSE: ALC), a global leader in eye care, has signed a definitive agreement to acquire STAAR Surgical Company (NASDAQ: STAA) in a cash transaction valued at approximately $1.5 billion. The acquisition is aimed at bolstering Alcon’s position in the surgical vision correction market, particularly in addressing the growing global demand for alternatives to LASIK.

The deal will see Alcon purchasing all outstanding shares of STAAR common stock at $28 per share, representing a 59% premium to STAAR’s 90-day volume-weighted average price and a 51% premium over its August 4 closing price.

STAAR Surgical is best known for its EVO family of Implantable Collamer Lenses (ICLs), which offer minimally invasive, reversible vision correction for patients with moderate to high myopia, including those with astigmatism. These lenses are implanted behind the iris and in front of the eye’s natural lens, offering a surgical option that avoids corneal tissue removal.

For Alcon, the acquisition is a strategic complement to its existing laser vision correction business. By incorporating STAAR’s EVO ICL technology, the company aims to provide a broader spectrum of refractive solutions for patients, especially those who are not ideal candidates for LASIK or other laser procedures.

The need for such alternatives is expanding rapidly. Global studies suggest that by 2050, half of the world’s population will be myopic, with approximately 500 million people falling into the high myopia category—a group that often requires advanced vision correction techniques.

Alcon expects the acquisition to be accretive to earnings by the second year post-closing. The company plans to finance the purchase through short- and long-term credit facilities and noted that the transaction is not subject to a financing condition.

STAAR has faced recent market challenges, including fluctuating demand in key international markets such as China. By joining Alcon, STAAR is expected to benefit from increased operational scale and broader global distribution, which could accelerate the adoption of its EVO ICLs.

The transaction has received unanimous approval from both companies’ boards of directors. It is expected to close within six to twelve months, pending customary closing conditions, including regulatory clearances and approval by STAAR shareholders.

Financial advisors on the deal include Morgan Stanley for Alcon and Citi for STAAR, while legal counsel was provided by Gibson, Dunn & Crutcher LLP and Wachtell, Lipton, Rosen & Katz, respectively.

As part of ongoing developments, STAAR is scheduled to release its Q2 2025 earnings on August 6, though it will not hold an investor conference call due to the pending acquisition.

PURCHASE, N,Y., Aug. 05, 2025 (GLOBE NEWSWIRE) — Townsquare Media, Inc. (NYSE: TSQ) (“Townsquare” or the “Company”), a leader in digital advertising and marketing solutions focused on markets outside of the Top 50 in the United States, announced today a strategic digital advertising partnership with Renda Media, a local media company with a strong presence in six U.S. cities (including Ft. Myers/Naples, FL; Jacksonville, FL; Pittsburgh, PA; Indiana, PA; Greensburg, PA; and Punxsutawney, PA) that do not overlap with Townsquare’s market footprint.

“We’re excited to partner with Renda Media to bring our market-leading digital advertising solutions to their expansive client base,” said Todd Lawley, President of Townsquare Ignite, the Company’s Digital Advertising division. “Our success stems from a deep expertise in leveraging our proprietary in-house programmatic platform and data-driven strategies to deliver measurable value. Through this partnership, we look forward to equipping Renda Media with the tools, insights, and proven strategic approach needed to strengthen their digital capabilities and accelerate client growth.”

Townsquare announced the launch of their Media Partnerships division in 2024. As part of the Company’s Digital Advertising segment (also called Townsquare Ignite), the Media Partnerships division provides a white-label service that equips other local media companies with the digital advertising solutions that have fueled Townsquare’s own growth and success, with digital now comprising over 50% of Townsquare’s total revenue and profit. With this alliance with Renda Media, Townsquare now has six media partners, reaching 19 incremental markets that do not overlap with Townsquare’s own footprint. Through this partnership, Townsquare will share its expertise and resources with Renda Media, focusing on customized, data-driven strategies that meet the unique needs of local, regional and national businesses, helping Renda Media grow its digital business alongside its respected broadcast presence.

“Years ago, I heard of a radio company that was getting more involved with the digital business. Through the years, I have watched and admired Townsquare as they grew their digital business into a media leader,” said Tony Renda, Sr., CEO of Renda Media. “Renda Media is proud to announce our partnership with Townsquare. They bring years of digital experience, knowhow, and professionalism to this partnership.”

About Townsquare Media, Inc. Townsquare is a community-focused digital and broadcast media and digital marketing solutions company principally focused outside the top 50 markets in the U.S. Townsquare Ignite, our robust digital advertising division, specializes in helping businesses of all sizes connect with their target audience through data-driven, results based strategies, by utilizing a) our proprietary digital programmatic advertising technology stack with an in-house demand and data management platform and b) our owned and operated portfolio of more than 400 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data. Townsquare Interactive, our subscription digital marketing services business, partners with SMBs to help manage their digital presence by providing a SAAS business management platform, website design, creation and hosting, search engine optimization and other digital services. And through our portfolio of local radio stations strategically situated outside the Top 50 markets in the United States, we provide effective advertising solutions for our clients and relevant local content for our audiences. For more information, please visit www.townsquaremedia.com, www.townsquareinteractive.com, and www.townsquareignite.com.

About Renda Media Renda Media is a privately held radio broadcasting company with its corporate office located in Pittsburgh, PA. The company manages affiliates, operating 18 radio stations in 6 markets: Ft. Myers/Naples, FL, Jacksonville, FL, Pittsburgh, PA, Indiana, PA, Greensburg, PA and Punxsutawney, PA. Everyday Renda Media delivers Entertainment, Information and News to thousands of listeners. For more information, visit www.rendabroadcasting.com.

LIMASSOL, Cyprus, Aug. 05, 2025 (GLOBE NEWSWIRE) — GDEV Inc. (Nasdaq: GDEV), a global gaming and entertainment company, today announced the acquisition of Light Hour Games, a privately held mobile studio based in Cyprus.

Light Hour Games is a full-stack studio that builds and markets mobile casual games using AI-first workflows — enabling rapid iteration without compromising high-quality execution. Founded by industry veterans Konstantin Mitrofanov and Ilya Nikitin, the studio operates as a 15-person team with deep expertise across game development, art, and live operations.

The acquisition represents a strategic partnership that will grant the Light Hour Games studio the opportunity for continued creative freedom and long-term upside through a share in the future success of its games, while securing the necessary funding for its operations through GDEV. As part of GDEV’s ecosystem, Light Hour Games will gain access to GDEV’s knowledge and data platforms.

“By welcoming Light Hour Games into the GDEV family we secure a talented crew whose lean structure, deep industry experience and advanced AI-driven toolset perfectly complement our growth strategy. Our philosophy has always been about enabling the best creators with the resources and freedom they need to succeed,” said Andrey Fadeev, CEO of GDEV. “With Light Hour Games, we see an opportunity to bring fresh ideas and approaches to a proven genre – and we believe this team has the experience and ambition to build something truly special.”

Konstantin Mitrofanov, CEO of Light Hour Games, shared: “Partnering with GDEV gives our studio both the financial runway and the strategic reach to realise our ambitions. With GDEV’s support, we can focus on crafting a casual experience that not only engages players from day one, but grows over time into a meaningful part of their everyday lives.”

About GDEV Inc.

GDEV is a gaming and entertainment holding company, focused on development and growth of its franchise portfolio across various genres and platforms. With a diverse range of subsidiaries including Nexters and Cubic Games, among others, GDEV strives to create games that will inspire and engage millions of players for years to come. Its franchises, such as Hero Wars, Island Hoppers, Pixel Gun 3D and others have accumulated over 550 million installs and $2.7 billion of bookings worldwide. For more information, please visit www.gdev.inc.

About Light Hour Games

Light Hour Games is an AI-first game development studio and a part of GDEV. Based in Cyprus and founded by industry veterans, the company combines deep production expertise with cutting-edge AI workflows to accelerate development and enhance game quality. The studio focuses on creating mobile casual experiences that are emotionally engaging, scalable, and built to evolve with their players over time.

Contacts:

Investor Relations Roman Safiyulin | Chief Corporate Development Officer investor@gdev.inc

Certain statements in this press release may constitute “forward-looking statements” for purposes of the federal securities laws. Such statements are based on current expectations that are subject to risks and uncertainties. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The forward-looking statements contained in this press release are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that the Company has anticipated. Forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Company’s control) or other assumptions. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of the Company’s 2024 Annual Report on Form 20-F, filed by the Company on March 31, 2025, and other documents filed by the Company from time to time with the SEC. Should one or more of these risks or uncertainties materialize, or should any of the Company’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Second quarter net income of $9.7 million Second quarter Adjusted EBITDA of $28.0 million Dredging backlog of $1 billion at June 30, 2025

HOUSTON, Aug. 05, 2025 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (Nasdaq: GLDD), the largest provider of dredging services in the United States, today reported financial results for the second quarter ended June 30, 2025.

Second Quarter 2025 Highlights

Revenue was $193.8 million

Total operating income was $17.1 million

Net income was $9.7 million

Adjusted EBITDA was $28.0 million

Backlog as of June 30, 2025, was $1.0 billion

Management Commentary

Lasse Petterson, President and Chief Executive Officer, commented, “Great Lakes delivered a solid second quarter, driven by strong project execution and high equipment utilization. We ended the quarter with revenue of $193.8 million, net income of $9.7 million, and adjusted EBITDA of $28.0 million, despite four dredges undergoing their regulatory drydocking. Our substantial dredging backlog stood at approximately $1.0 billion as of the end of the second quarter, with an additional $215.4 million in low bids and options pending award, providing expected revenue visibility for the remainder of 2025 and well into 2026. Capital and coastal protection projects account for 93% of our dredging backlog, which typically yield higher margins.

Dredging activity for private clients in the Liquefied Natural Gas (LNG) sector remains strong. In the second quarter, we received notice to proceed for dredging operations on the Woodside Louisiana LNG project. This project has been added to our Q2 2025 backlog, along with two additional options currently included in our Q2 2025 options pending award. Dredging for this project is scheduled to begin in early 2026.

Our current backlog also includes two additional major LNG projects awarded in 2023: the Port Arthur LNG Phase 1 Project and the Brownsville Ship Channel Project, part of NextDecade Corporation’s Rio Grande LNG initiative, the latter marking the largest project in our Company’s history. Dredging operations for both projects began in Q3 2024 and are actively ongoing.

In the first quarter of 2025, we initiated a $50 million share repurchase program, as we believed our share price did not appropriately reflect the Company’s financial performance and long-term outlook. As of June 30, 2025, we have repurchased 1.3 million shares under the program for a total spend of $11.6 million.

In addition, on May 2, 2025, we executed an amendment to our Revolving Credit Facility, increasing the size from $300 million to $330 million, further enhancing our liquidity. All other terms remained the same.

Our newbuild program is coming towards completion with our newest hopper dredge, the Amelia Island, expected to be delivered within the next few weeks and plans to immediately go to work when she leaves the shipyard. The Amelia Island and her sister ship, the Galveston Island, which was delivered in early 2024, will primarily work on projects aimed at the redevelopment and enhancement of our shorelines, which are consistently impacted by severe weather.

The Acadia, the first U.S.-flagged, Jones Act-compliant subsea rock installation vessel, hit a key milestone with her launch from drydock in July with expected completion in the first quarter of 2026. Upon delivery, the Acadia is expected to immediately commence operations, first on Equinor’s Empire Wind I project and then onto Orsted’s Sunrise Wind project, which will provide full utilization for the vessel for 2026. The Acadia is designed to serve projects in both domestic and international markets focused on safeguarding critical subsea infrastructure, including subsea cables for power transmission, telecommunications cables, oil and gas pipelines and offshore wind developments.

The Company had an exceptional first half of 2025, which we expect to continue for the remainder of this year and into 2026 driven by a modernized fleet, superior project execution, and a robust backlog.”

Operational Update

Second Quarter 2025

Revenue was $193.8 million, an increase of $23.7 million from the second quarter of 2024. The higher revenue in the second quarter of 2025 was due primarily to higher capital project revenue as compared to the same period in the second quarter last year, partially offset by lower coastal protection and maintenance project revenue.

Gross profit was $36.6 million, an improvement of $6.8 million compared to the gross profit from the second quarter of 2024 and gross margin percentage increased to 18.9% in the second quarter of 2025 from 17.5% in the second quarter of 2024 primarily due to improved utilization and project performance and a larger number of capital and coastal protection projects which typically yield higher margins, partially offset by higher drydocking cost.

Operating income was $17.1 million, which increased from $14.6 million in the prior year second quarter primarily driven by higher gross profit partially offset by an increase in general and administrative expenses primarily from higher incentive compensation due to the increased results in the first half of 2025.

Net income for the quarter was $9.7 million, which is a $2.0 million increase compared to net income of $7.7 million in the prior year second quarter. The increase is mostly driven by improved operating results partially offset by an increase in income tax provision.

Balance Sheet, Dredging Backlog & Capital Expenditures

At June 30, 2025, the Company had $2.9 million in cash and cash equivalents and total long-term debt of $419.6 million including $5.0 million drawn on our $330 million revolver. As of June 30, 2025, our liquidity was $272 million.

At June 30, 2025, the Company had $1.0 billion in dredging backlog as compared to $1.2 billion at December 31, 2024. Dredging backlog as of June 30, 2025 does not include approximately $215.4 million of awards and options pending.

Total capital expenditures for the second quarter of 2025 were $64.6 million including $28.7 million for the construction of the Acadia, $19.8 million for the Amelia Island, $8.8 million for support equipment, and $7.3 million for maintenance and growth.

Market Update

The Administration continues to demonstrate strong and consistent support for the dredging industry. The U.S. Army Corps of Engineers (the “Corps”) is operating in fiscal year 2025 under a continuing resolution, enacted on March 15, 2025, which sustains the funding levels established in the prior fiscal year’s record-setting budget through September 30, 2025. Our $1 billion project backlog and the inclusion of resources from the 2023 Disaster Relief Supplemental Appropriations should enable us to continue to deliver on a very busy 2025.

The Water Resources Development Act (WRDA), reauthorized every two years, funds the Corps’ projects related to flood protection, dredging, and ecosystem restoration. On January 4, 2025, WRDA 2024 was signed into law, authorizing new capital investments to enhance flood protection, coastal resilience, and ecosystem restoration. Previously, WRDA 2022 authorized deepening shipping channels in New York and New Jersey to 55 feet and advanced the Coastal Texas Protection and Restoration Program. In addition to the planned New York and New Jersey deepening, additional large-scale projects are expected to commence in the next two to three years in Tampa Bay, New Haven, Baltimore, among others.

Following the resolution of the temporary pause from the Bureau of Ocean Management, Equinor’s Empire Wind I project, which is part of our Offshore Energy backlog, has resumed in accordance with its schedule. We have secured full utilization of the Acadia for 2026 and are currently bidding work for 2027 and beyond.

In anticipation of potential delays in U.S. offshore wind projects, we proactively expanded the Acadia’s strategic target markets to include oil and gas pipeline protection, power and telecommunications cable protection, and international offshore wind. This diversification increases our opportunities into a broader range of services we now refer to as Offshore Energy. Our strategy is supported by a global shortage of rock placement vessels, and we are actively pursuing opportunities across these sectors to ensure strong and sustained utilization of the Acadia well into the future.

Conference Call Information

The Company will conduct a quarterly conference call, which will be held on Tuesday, August 5, 2025, at 9:00 a.m. C.D.T (10:00 a.m. E.D.T.). Investors and analysts are encouraged to pre-register for the conference call by using the link below. Participants who pre-register will be given a unique PIN to gain immediate access to the call. Pre-registration may be completed at any time up to the call start time.

The live call and replay can also be heard at https://edge.media-server.com/mmc/p/e9ususwz or on the Company’s website, www.gldd.com, under Events on the Investor Relations page. A copy of the press release will be available on the Company’s website.

Use of Non-GAAP Measures

Adjusted EBITDA, as provided herein, represents net income from continuing operations, adjusted for net interest expense, income taxes, depreciation and amortization expense, debt extinguishment, accelerated maintenance expense for new international deployments, goodwill or asset impairments and gains on bargain purchase acquisitions. Adjusted EBITDA is not a measure derived in accordance with GAAP. The Company presents Adjusted EBITDA as an additional measure by which to evaluate the Company’s operating trends. The Company believes that Adjusted EBITDA is a measure frequently used to evaluate the performance of companies with substantial leverage and that the Company’s primary stakeholders (i.e., its stockholders, bondholders and banks) use Adjusted EBITDA to evaluate the Company’s period to period performance. Additionally, management believes that Adjusted EBITDA provides a transparent measure of the Company’s recurring operating performance and allows management to readily view operating trends, perform analytical comparisons and identify strategies to improve operating performance. For this reason, the Company uses a measure based upon Adjusted EBITDA to assess performance for purposes of determining compensation under the Company’s incentive plan. Adjusted EBITDA should not be considered an alternative to, or more meaningful than, amounts determined in accordance with GAAP including: (a) net income as an indicator of operating performance or (b) cash flows from operations as a measure of liquidity. As such, the Company’s use of Adjusted EBITDA, instead of a GAAP measure, has limitations as an analytical tool, including the inability to determine profitability or liquidity due to the exclusion of accelerated maintenance expense for new international deployments, goodwill or asset impairments, gains on bargain purchase acquisitions, net interest expense and income tax expense and the associated significant cash requirements and the exclusion of depreciation and amortization, which represent significant and unavoidable operating costs given the level of indebtedness and capital expenditures needed to maintain the Company’s business. For these reasons, the Company uses net income to measure the Company’s operating performance and uses Adjusted EBITDA only as a supplement. Adjusted EBITDA is reconciled to net income in the table of financial results. For further explanation, please refer to the Company’s SEC filings.

The Company

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States, which is complemented with a long history of performing significant international projects. In addition, Great Lakes is fully engaged in expanding its core business into the offshore energy industry. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 135-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Certain statements in this press release may constitute “forward-looking” statements, as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “may,” “would,” “could,” “should,” “seeks,” “are optimistic,” “commitment to” or “scheduled to,” or other similar words, or the negative of these terms or other variations are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining of these terms or comparable language, or by discussion of strategy or intentions. These cautionary statements have the benefit of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future performance. Important assumptions and other important factors that could cause actual results to differ materially from those forward-looking statements with respect to Great Lakes include, but are not limited to: a reduction in government funding for dredging and other contracts, or government cancellation of such contracts, or the inability of the Corps to let bids to market; our ability to qualify as an eligible bidder under government contract criteria and to compete successfully against other qualified bidders in order to obtain government dredging and other contracts; the political environment and governmental fiscal and monetary policies; cost over-runs, operating cost inflation and potential claims for liquidated damages, particularly with respect to our fixed price contracts; the timing of our performance on contracts and new contracts being awarded to us; significant liabilities that could be imposed were we to fail to comply with government contracting regulations; project delays related to the increasingly negative impacts of climate change or other unusual, non-historical weather patterns; costs necessary to operate and maintain our existing vessels and the construction of new vessels, including with respect to changes in applicable regulations or standards; equipment or mechanical failures; pandemic, epidemic or outbreak of an infectious disease; disruptions to our supply chain for procurement of new vessel build materials or maintenance on our existing vessels; capital and operational costs due to environmental regulations; market and regulatory responses to climate change, including proposed regulations concerning emissions reporting and future emissions reduction goals; contract penalties for any projects that are completed late; force majeure events, including natural disasters, war and terrorists’ actions; changes in the amount of our estimated backlog; significant negative changes attributable to large, single customer contracts; our ability to obtain financing for the construction of new vessels, including our new offshore energy vessel; our ability to secure contracts to utilize our new offshore energy vessel; unforeseen delays and cost overruns related to the construction of our new vessels; any failure to comply with the Jones Act provisions on coastwise trade, or if those provisions were modified, repealed or interpreted differently; our ability to comply with anti-discrimination laws, including those pertaining to diversity, equity and inclusion programs; fluctuations in fuel prices, particularly given our dependence on petroleum-based products; impacts of nationwide inflation on procurement of new build and vessel maintenance materials; our ability to obtain bonding or letters of credit and risks associated with draws by the surety on outstanding bonds or calls by the beneficiary on outstanding letters of credit; acquisition integration and consolidation, including transaction expenses, unexpected liabilities and operational challenges and risks; divestitures and discontinued operations, including retained liabilities from businesses that we sell or discontinue; potential penalties and reputational damage as a result of legal and regulatory proceedings; any liabilities imposed on us for the obligations of joint ventures, and similar arrangements and subcontractors; increased costs of certain material used in our operations due to newly imposed tariffs; unionized labor force work stoppages; any liabilities for job-related claims under federal law, which does not provide for the liability limitations typically present under state law; operational hazards, including any liabilities or losses relating to personal or property damage resulting from our operations; our substantial amount of indebtedness, which makes us more vulnerable to adverse economic and competitive conditions; restrictions on the operation of our business imposed by financing terms and covenants; impacts of adverse capital and credit market conditions on our ability to meet liquidity needs and access capital; limitations on our hedging strategy imposed by statutory and regulatory requirements for derivative transactions; foreign exchange risks, in particular, related to the new offshore energy vessel build; losses attributable to our investments in privately financed projects; restrictions on foreign ownership of our common stock; restrictions imposed by Delaware law and our charter on takeover transactions that stockholders may consider to be favorable; restrictions on our ability to declare dividends imposed by our financing agreements or Delaware law; significant fluctuations in the market price of our common stock, which may make it difficult for holders to resell our common stock when they want or at prices that they find attractive; changes in previously recorded net revenue and profit as a result of the significant estimates made in connection with our methods of accounting for recognized revenue; maintaining an adequate level of insurance coverage; our ability to find, attract and retain key personnel and skilled labor; disruptions, failures, data corruptions, cyber-based attacks or security breaches of the information technology systems on which we rely to conduct our business; impairments of our goodwill or other intangible assets; and failure of our share repurchase program to be fully implemented or enhance long-term shareholder value. For additional information on these and other risks and uncertainties, please see Item 1A. “Risk Factors” of Great Lakes’ Annual Report on our most recent Form 10-K, Item 1A. “Risk Factors” of Great Lakes’ Quarterly Report on Form 10-Q for the quarter ended June 30, 2025 and in other securities filings by Great Lakes with the SEC.

Although Great Lakes believes that its plans, intentions and expectations reflected in or suggested by such forward-looking statements are reasonable, actual results could differ materially from a projection or assumption in any forward-looking statements. Great Lakes’ future financial condition and results of operations, as well as any forward-looking statements, are subject to change and inherent risks and uncertainties. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

Orchestrated Software Solution Will Eliminate the Need for On-site Hub Hardware and Enhance Flexibility for Customers

SAN DIEGO, Aug. 05, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, and hiSky, a leading provider of industrial satellite communications solutions, announced today a partnership that will enable the delivery of hiSky satellite network services, including Industrial Internet of Things (IoT) as a fully orchestrated capability using Kratos’ OpenSpace® dynamic, software-defined ground system. The partnership will allow satellite and other communications network operators to offer IoT connectivity services to their commercial and government customers, taking advantage of the scale, economics and operational benefits of a modern, cloud-enabled network architecture.

According to ABI Research, the global IoT market for supply-side software and service revenue will grow in value from US$277 billion in 2024 to US$606 billion by 2030, and that IoT will play an increasing role in all industries. Satellite connectivity can contribute mightily to this growth with its ability to reach remote, mobile, disaster-affected and other unconnected environments. The partnership between Kratos and hiSky will advance this capability by enabling IoT services employing virtual and cloud-native network architectures, thereby reducing costs and greatly increasing scalability and service flexibility.

hiSky’s solution provides customers around the globe an exceptionally agile answer for satellite IoT applications with easy-to-deploy Smartellite™ terminals today connecting to a conventional hardware-based hub. “Kratos is working closely with hiSky to fully virtualize the hiSky hub within the OpenSpace platform, enabling it to run in the mainstream public cloud,” said Greg Quiggle, SVP of Product Management at Kratos. “Doing so will enable hiSky and Kratos customers to offer a new breed of on-demand and dynamically scalable IoT services at a much lower cost than conventional hardware-based systems.”

According to Shahar Kravitz, co-founder and CEO at hiSky, “With the results of this partnership, satellite operators will be able to spin-up new carriers upon demand at any enabled teleport with a touch of a button, without the need for new hardware at the teleport and the associated plumbing. It’s a new era of flexibility, scalability, speed of service enablement and redundancy.”

About Kratos OpenSpace Kratos’ OpenSpace family of solutions enables the digital transformation of satellite ground systems to become a more dynamic and powerful part of the space network. Today’s ground systems are still based upon legacy hardware architectures that are inflexible, difficult and expensive to manage, and slow to adapt to evolving customer needs. As the first and only commercially available, fully orchestrated, software-defined ground system, the OpenSpace Platform enhances satellite network operations, reducing costs and mainstreaming satellite connectivity to work seamlessly with the rest of the world’s global communications infrastructure, which long ago adopted modern software-defined networking principles. For more information about the OpenSpace family visit www.KratosDefense.com/OpenSpace.

About hiSky Founded in 2015, hiSky is a leading provider of satellite communication solutions, offering innovative and reliable connectivity for government and industrial IoT applications.

hiSky is the only commercially available, satellite-agnostic end-to-end system focused on mid-range bitrates. Its technology ensures secure and reliable connectivity through private networks, addressing critical connectivity challenges across multiple sectors.

hiSky’s competitive edge is driven by its proprietary, in-house-developed firmware and a unified software solution, enabled across GEO, MEO, and LEO satellite networks over high-speed Ka/Ku frequencies. The company’s technology stack provides a cost-effective, small, lightweight, ruggedized and adaptable solution. For more information visit: www.hiskysat.com.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

All CDI-988 doses, ranging from 100 mg to 1200 mg, in the Phase 1 study were well tolerated

Company expects to initiate Phase 1b study with CDI-988 in norovirus-infected healthy subjects later this year

Lack of approved norovirus treatments or vaccines creates critical unmet medical need

BOTHELL, Wash., Aug. 05, 2025 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) announces the presentation of favorable safety and tolerability data from a randomized, double-blinded, placebo-controlled Phase 1 study with its oral, direct-acting pan-viral inhibitor CDI-988 at the 2025 Military Health System Research Symposium (MHSRS), being held August 4-7 in Kissimmee, Florida. The results support Cocrystal’s continued clinical development of CDI-988 as a potential norovirus prophylaxis and treatment.

In An Oral Pan-viral Protease Inhibitor for the Prevention and Treatment of Norovirus and Coronavirus Infections: Mechanism of Action and Phase 1 Study Results, Sam Lee, Ph.D., Cocrystal President and co-CEO, discussed findings from the CDI-988 Phase 1 single-ascending (SAD) and multiple-ascending (MAD) cohorts. Data indicate that all doses, ranging from 100 mg to 1200 mg, were well tolerated. Overall treatment-emergent adverse events among CDI-988 subjects were 28% (10/36) compared with 40% (4/10) among placebo subjects for the SAD cohorts, and 53% (19/36) and 92% (11/12), respectively, for the MAD cohorts. Headache was the most common adverse event. All subjects in the SAD cohorts and all but one in the MAD cohorts completed the study. No severe treatment-emergent adverse events, no clinically relevant ECG changes and no clinically significant pathology results were reported from the CDI-988 Phase 1 single-ascending (SAD) and multiple-ascending (MAD) cohorts.

“Consistent with interim results from the Phase 1 study, CDI-988 was well-tolerated with a favorable safety profile across all dose levels tested in this study,” said Dr. Lee. “Our plan to continue CDI-988’s clinical development for norovirus is particularly relevant for the military, where this highly transmissible pathogen poses significant operational and economic risks. In confined settings such as naval vessels and military installations, norovirus can rapidly spread, causing debilitating gastrointestinal symptoms that could compromise mission readiness.

“The absence of approved norovirus treatments or vaccines creates a critical unmet medical need,” he added. “Norovirus presents significant vaccine development challenges due to its high genetic variability and mutation rate. CDI-988’s mechanism of action targeting viral replication and its broad-spectrum coverage offers a promising solution as a potential prophylactic and therapeutic intervention across all norovirus genogroups including GII.4 and GII.17. This could be a new approach to outbreak prevention and management. We expect to initiate a Phase 1b challenge study with CDI-988 in norovirus-infected healthy subjects later this year.”

MHSRS is an annual educational symposium with approximately 4,000 attendees that provides a collaborative environment for military medical care providers with deployment experience, research and academic scientists, international partners and industry on research and related healthcare initiatives falling under the topic areas of combat casualty care, military operational medicine, clinical and rehabilitative medicine, information sciences, military infectious diseases and radiation health effects. More information is available here.

Pan-viral Protease Inhibitor CDI-988 CDI-988 was designed and developed with Cocrystal’s proprietary structure-based platform technology as a broad-spectrum inhibitor to a highly conserved region in the active site of 3CL viral proteases. Based on a novel mechanism of action and superior broad-spectrum antiviral activity, CDI-988 represents a compelling first potential oral treatment for noroviruses, and for coronaviruses.

Norovirus Infection Norovirus is a common and highly contagious virus that afflicts people of all ages and causes symptoms of acute gastroenteritis including nausea, vomiting, stomach pain and diarrhea, as well as fatigue, fever and dehydration. Norovirus outbreaks occur most commonly in semi-closed communities such as hospitals, nursing homes, childcare facilities, cruise ships, schools and disaster relief sites. Norovirus infections are estimated to cost society approximately $60 billion annually worldwide.

Structure-Based Drug Discovery Platform Technology Cocrystal’s proprietary structural biology, along with its expertise in enzymology and medicinal chemistry, enable its development of novel antiviral agents. The Company’s platform provides a three-dimensional structure of inhibitor complexes at near-atomic resolution, providing immediate insight to guide Structure Activity Relationships. This helps to identify novel binding sites and allows for a rapid turnaround of structural information through highly automated X-ray data processing and refinement. The goal of this technology is to facilitate the development of novel broad-spectrum antivirals for the treatment of acute and chronic viral diseases.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), noroviruses and hepatitis C viruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Cautionary Note Regarding Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the potential efficacy of CDI-988 as a potential breakthrough for norovirus prophylaxis and treatment, and the potential characteristics of and market for such product candidate and the Company’s plan to initiate a Phase 1b study in 2025. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, our need for additional capital to fund our operations over the next 12 months, risks relating to our ability to obtain regulatory approval for and proceed with clinical trials including recruiting volunteers and procuring materials for such studies by our clinical research organizations and vendors, the results of such studies, our and our collaboration partners’ technology and software performing as expected, general risks arising from clinical studies, receipt of regulatory approvals, regulatory changes, and potential development of effective treatments and/or vaccines by competitors, potential mutations in a virus we are targeting that may result in variants that are resistant to a product candidate we develop, the impact of the Trump Administration’s policies and actions on regulation affecting the FDA and other healthcare agencies and potential staffing issues resulting therefrom, as well as other government actions such as tariffs which may cause delays or force us to incur additional costs to proceed without development programs. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2024. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

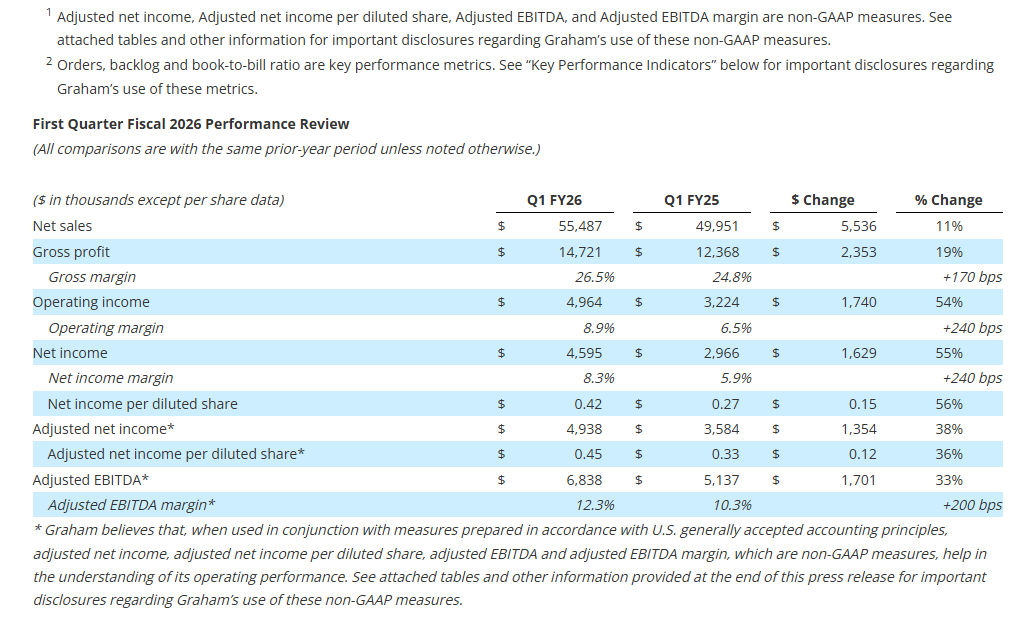

Revenue increased 11% to $55.5 million, reflecting the strength of the Company’s product portfolio and diversified revenue base

Gross profit increased 19% to $14.7 million; Gross margin improved 170 basis points to 26.5%

Net income per diluted share increased 56% to $0.42; adjusted net income per diluted share1 increased 36% to $0.45

Net income increased 55% to $4.6 million; Adjusted EBITDA1 increased 33% to $6.8 million; Adjusted EBITDA margin1 improved 200 basis points to 12.3%

Orders2 were $125.9 million, driven by large defense orders; Book-to-Bill ratio2 of 2.3x and backlog2 of $482.9 million

Strong balance sheet with no debt, $10.8 million in cash, and access to $44.3 million under its revolving credit facility at quarter end to support growth initiatives

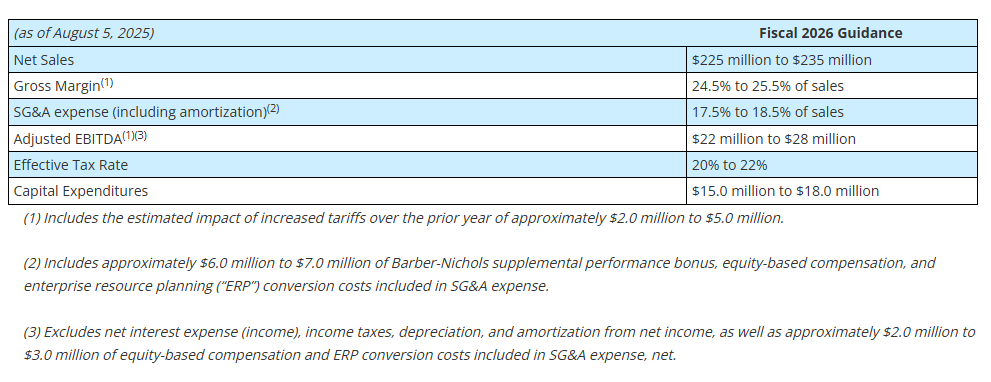

Reiterating full year fiscal 2026 guidance for all metrics provided; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its first quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “The start of fiscal 2026 demonstrates continued strength across our diversified product portfolio. We delivered strong growth in our Energy & Process markets, driven by execution on major commercial projects and robust aftermarket demand, along with increasing momentum in emerging energy segments such as small modular reactors (“SMRs”) and cryogenics. In addition, our Defense business continues to perform well, supported by recent follow-on orders, including $86.5 million to support the Virginia Class submarine program in May and $25.5 million for the MK48 Mod 7 Heavyweight Torpedo program in July, reaffirming our position as a trusted supplier to the U.S. Navy.”

Mr. Malone continued, “We remain focused on high-return initiatives that drive long-term value creation, including numerous in-process capital investments expected to generate returns above 20%. These initiatives include automated welding, enhanced radiographic testing technologies, and our new cryogenic testing facility in Florida, which we expect will improve margins and create new revenue opportunities. I’m also pleased to announce that we’ve completed the expansion of our Batavia defense facility this month. With these investments, we believe Graham is well-positioned to drive sustainable growth, deliver for our customers, and continue expanding margins.”

Quarterly net sales of $55.5 million increased 11%, or $5.5 million. Sales to the Energy & Process market contributed $5.7 million to growth driven by increased sales in the Chemical/Petrochemical and New Energy industries. The increase in Chemical/Petrochemical sales was largely due to a surface condenser order for a North American net-zero carbon emissions ethylene cracker received in June 2024, while the increase in New Energy sales was driven by increased sales to the hydrogen and SMR markets. Aftermarket sales to the Energy & Process and Defense markets of $10.4 million remained strong and were 33% higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $2.4 million to $14.7 million compared to the prior-year period of $12.4 million. As a percentage of sales, gross profit margin increased 170 basis points to 26.5%, compared to the first quarter of fiscal 2025. Increased leverage on fixed overhead costs due to the higher volume of sales discussed above, as well as an improved mix of sales related to higher margin aftermarket sales, and better execution and pricing on defense contracts were the primary drivers of this increase. For the first quarter of fiscal 2026, the impact of tariffs was not material to our consolidated financial statements in comparison to the prior year. However, we still estimate the range of potential impact of increased tariffs for the full year to be between $2 million to $5 million.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $9.8 million, an increase of $0.6 million compared with the prior year. This increase reflects the investments we are making in our operations, our employees, and our technology. As a percentage of sales, SG&A, including amortization, of 17.7% decreased 90 basis points compared to the prior year period, reflective of our financial discipline.

Cash Management and Balance Sheet As expected, cash used by operating activities totaled $2.3 million for the quarter-ending June 30, 2025, primarily due to the payment of fiscal 2025 bonuses including the supplemental Barber-Nichols earnout bonus of $4.3 million in connection with the acquisition. As of June 30, 2025, cash and cash equivalents were $10.8 million, compared with $21.6 million as of March 31, 2025.

Capital expenditures for the first quarter fiscal 2025 were $7.0 million, focused on capacity expansion, increasing capabilities, and productivity improvements. All major capital projects are on time.

The Company had no debt outstanding as of June 30, 2025, with $44.3 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the first quarter of fiscal 2026 increased to $125.9 million, including the remaining $86.5 million of a $136.5 million follow-on order in support of the U.S. Navy’s Virginia Class Submarine program. Aftermarket orders for the Energy & Process and Defense markets remained strong and totaled $10.5 million for the first quarter of fiscal 2026, increasing 16% over the prior year. Book-to-bill for the first quarter of fiscal 2026 was 2.3x. Note that orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was $482.9 million, a 22% increase over the prior-year period. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 87% of our backlog at June 30, 2025, was to the Defense industry, which we believe provides stability and visibility to our business.

Fiscal 2026 Outlook Based upon the results for the first quarter of fiscal 2026, as well as our expectations for the remainder of the fiscal year, we are reiterating our full year fiscal 2026 guidance provided earlier this year as follows:

Our expectations for sales and profitability assume that we will be able to operate our production facilities at planned capacity, have access to our global supply chain including our subcontractors, do not experience any global disruptions, and experience no impact from any other unforeseen events.

Webcast and Conference Call GHM’s management will host a conference call and live webcast on August 5, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (412)-317-5195. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Tuesday, August 12, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 10201479 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expects,” “future,” “outlook,” “believes,” “could,” “guidance,” “may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the Defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures Adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent written communications received from customers requesting the Company to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

Advances knowledge about the use of tecarfarin in patients with severe kidney impairment, including dialysis

Pivotal step forward in pursuit of ESKD + Atrial Fibrillation (AFib) registration trial

Addresses a critical current treatment gap in patients with ESKD

PONTE VEDRA, Fla. – Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a biopharmaceutical company focused on developing transformative therapeutics that specifically address limitations of current anticoagulation therapy, today announced clinical trial initiation plans for its lead late-stage drug candidate, tecarfarin, in patients with ESKD who are transitioning to dialysis. Enrollment is planned to begin later this year and will include patients with and without atrial fibrillation (AFib).

Patients with severe kidney disease are already at high risk for thrombotic cardiovascular events such as myocardial infarction and stroke, along with a much greater risk of AFib and venous thromboembolism compared to subjects with normal kidney function. When ESKD patients require dialysis, their transition period comes with even greater risk of myocardial infarction, stroke, and a substantial increase in mortality.

“There is a critical need for safe, effective anticoagulants for use in ESKD patients,” said Quang X. Pham, Chairman and CEO of Cadrenal Therapeutics. “Tecarfarin’s orphan drug and fast-track designations in ESKD patients with AFib underscore this need, and we are excited to advance this program. This study will be an important step forward for the continued development of tecarfarin in ESKD and in other areas with real opportunities to improve patient outcomes with a potentially better vitamin K antagonist.”

Currently, there is limited evidence supporting the use of anticoagulant therapy in dialysis patients. Dialysis patients are often excluded from clinical trials due to their high underlying risk profile, and studies of direct oral anticoagulants (DOACs) in this patient population have not provided clear answers. Furthermore, a recent Phase 2 trial of chronic hemodialysis patients sponsored by a global company showed no benefit from the new class of Factor XI inhibitors in maintaining vascular access graft patency. To date, no prospective studies have examined the benefit of oral anticoagulation in preventing thrombotic events at the time of dialysis initiation.

“Initiating dialysis carries substantial excess risk of cardiovascular events and mortality, and to date, this risk has not been sufficiently addressed. Tecarfarin, a next-generation Vitamin K antagonist with a unique metabolism pathway that is not significantly affected by kidney impairment, has potential promise in this area of unmet need,” said Wolfgang Winkelmayer, Professor of Medicine and Chief of Nephrology at Baylor College of Medicine in Houston, Texas.

About Cadrenal Therapeutics, Inc.

Cadrenal Therapeutics, Inc. is a biopharmaceutical company developing transformative therapeutics to address limitations of current anticoagulation therapy specifically. Cadrenal’s lead investigational product is tecarfarin, a novel oral vitamin K antagonist anticoagulant that is designed to address unmet needs in anticoagulation therapy. Tecarfarin is a reversible anticoagulant (blood thinner) designed to prevent heart attacks, strokes, and deaths due to blood clots in patients requiring chronic anticoagulation. Although warfarin is widely used off-label for several indications, extensive clinical and real-world data have shown it can have significant, serious side effects. With tecarfarin, Cadrenal is advancing an innovative solution to address the unmet needs in anticoagulation therapy, aiming to reduce the clinical complexities of managing Vitamin K antagonists and where DOACs remain inadequate or unproven.