Pangaea Logistics Solutions Ltd. (NASDAQ: PANL) provides logistics services to a broad base of industrial customers who require the transportation of a wide variety of dry bulk cargoes, including grains, pig iron, hot briquetted iron, bauxite, alumina, cement clinker, dolomite, and limestone. The Company addresses the transportation needs of its customers with a comprehensive set of services and activities, including cargo loading, cargo discharge, vessel chartering, and voyage planning. Learn more at www.pangaeals.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are adjusting our models to reflect lower shipping rates in the third quarter. Although shipping rates remains high relative to historical levels, they have decreased relative to peak levels reached this spring.

We are lowering our revenue, cashflow and earnings estimates in response. We now project third-quarter and 2022 revenues of $158.6 million an $714.1 million, respectively, down from our previous estimates of $182.3 million and $752.2 million. Our new EBITDA estimates are $9.6 million and $112.2 million, down from $33.31 million and $142.4 million. We now estimate earnings per share of $(0.08) and $1.27 as compared to $0.45 and $1.93.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Drilling continues at the Big Vein target. Labrador Gold released results from recent drilling associated with its 100,000-meter drill program at its 100%-owned Kingsway gold project targeting the Appleton Fault Zone over a 12-kilometer strike length. A total of 58,265 meters have been drilled to date with assays pending for samples from approximately 3,100 meters of core. Currently, one rig is drilling at the Golden Glove target while two rigs are drilling at Big Vein to test for extensions of mineralization in both directions. With drilling at the CSAMT target completed, a third rig is being deployed at Big Vein.

High grade assay results. Hole K-22-190 from the north end of Big Vein returned an intersection of 30.67 grams of gold per tonne over 1.1 meters from 208.85 meters depth that included 99.31 grams of gold over 0.3 meters. At Big Vein Southwest, Hole K-22-184 intersected 4.67 grams of gold per tonne over 1.64 meters from 336.25 meters depth that included 8.97 grams of gold per tonne over 0.75 meters. Drilling has returned several significant intercepts at the north end of Big Vein, including 6.07 grams of gold per tonne over 19 meters in Hole K-21-111. Results from Hole K-22-190 underscore the high-grade prospectivity of the area.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Kruh Well 28 finds oil formation in addition to previously announced gas reservoir. Indo reported reaching final depth in its fourth well in the Kruh field. As has been the case with the other three wells, oil has been discovered, this time with a wider oil band that had been expected. The company previously reported discovering natural gas at shallower levels as had been the case in Kruh Well 27. We view drilling in the Kruh Field as largely developmental so the successful discovery of hydrocarbons was not a surprise. It will take at least a month to complete the well before we can learn flow rate information, but management maintains that the wells have a twelve-month payback at current oil prices.

Well success prompts further seismic studies. Indo is planning to conduct new seismic operations across the entire Kruh Block to optimize drilling locations. The company still plans on drilling 18 wells in the block (four have been completed). Seismic studies will push back the drilling program twelve months into the 2024-25 time frame and will not begin until Kruh 27 and 28 have been brought on line. We had modeled six wells in 2023 and eight in 2024 and are pushing all drilling back a year. Indonesia Energy has faced a series of delays in its drilling program due to COVID, weather, and other factors.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Genco Shipping & Trading Limited, incorporated on September 27, 2004, transports iron ore, coal, grain, steel products and other drybulk cargoes along shipping routes through the ownership and operation of drybulk carrier vessels. The Company is engaged in the ocean transportation of drybulk cargoes around the world through the ownership and operation of drybulk carrier vessels. As of December 31, 2016, its fleet consisted of 61 drybulk carriers, including 13 Capesize, six Panamax, four Ultramax, 21 Supramax, two Handymax and 15 Handysize drybulk carriers, with an aggregate carrying capacity of approximately 4,735,000 deadweight tons (dwt). Of the vessels in its fleet, 15 are on spot market-related time charters, and 27 are on fixed-rate time charter contracts. As of December 31, 2016, additionally, 19 of the vessels in its fleet were operating in vessel pools.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are adjusting in response to lower third-quarter shipping rates. Our third-quarter and 2022 revenues estimates for Genco have been modestly reduced to $130.6 million and $535.2 million. Our third-quarter and 2022 EBITDA estimates are now $68.7 million and $258.0 million, down from $70.8 million and $264.3 million. Our third-quarter and 2022 EPS estimates are now $1.21 and $4.52, down from $1.25 and $4.66.

Our rating on the shares of Genco remains Outperform with a $28 price target. Lower shipping rates will adversely affect near-term results but does not change our long-term positive view of the shipping industry and Genco, in specific.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are lowering our assumed TCE shipping rate for non-fixed vessels. We are lowering third-quarter TCE rates to $20,000/day from $23,000/day to reflect weaker shipping rates in the quarter. The impact on EuroDry cash flow and earnings is somewhat muted relative to other shipping companies given fixed rates for the bulk of its fleet. Nevertheless, we are adjusting downward our estimates to reflect the impact on ships tied to market prices.

Revenues, EBITDA and EPS estimate all come down slightly. Our new third quarter and 2022 revenues estimates are $25.4 million and $96.3 million, down from $26.1 million and $98.4 million. Our new third quarter and 2022 EBITDA estimates are $13.1 million and $55.5 million, down from $13.7 million and $57.1 million. Our new third quarter and 2022 EPS estimates are $3.27 and $14.88, down from $3.48 and $15.44.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Eagle Bulk Shipping Inc. (“Eagle”) is a US-based drybulk owner-operator focused on the Supramax/Ultramax mid-size asset class, which ranges from 50,000 and 65,000 deadweight tons in size; these vessels are equipped with onboard cranes allowing for the self-loading and unloading of cargoes, a feature which distinguishes them from the larger classes of drybulk vessels and provides for greatly enhanced flexibility and versatility- both with respect to cargo diversity and port accessibility. The Company transports a broad range of major and minor bulk cargoes around the world, including coal, grain, ore, pet coke, cement, and fertilizer. Eagle operates out of three offices, Stamford (headquarters), Singapore, and Hamburg, and performs all aspects of vessel management in-house including: commercial, operational, technical, and strategic.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are lowering our estimates for Eagle Bulk Shipping to reflect lower shipping rates. We have lowered our assumed TCE shipping rates to reflect recent pricing. In response, we are lowering our third quarter and 2022 revenue estimates to $168.9 million and $710.9 million respectively, down from $193.2 million and $760.0 million.

Lower revenues means lower EBITDA and EPS estimates. Adjusting our models for lower pricing and revenues results in a decline in third quarter and 2022 EBITDA to $93.2 million and $362.7 million, down from $117.6 million and $411.8 million. EPS for the quarter and year are reduced to $4.24 and $15.55, down from $5.49 and $18.07.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. Coal prices continued to exhibit strength during the third quarter and we believe the outlook for oil and gas prices remains favorable. We have increased our 2022 adjusted EBITDA and adjusted EPU estimates to $951.9 million and $4.90 from $945.3 and $4.85, respectively. Our 2023 estimates remain unchanged. We have assumed the partnership declares third and fourth quarter per unit cash distributions of $0.45 and $0.50, respectively.

New Ventures team. Alliance recently announced the formation of a New Ventures team, led by Andrew Woodward and Matthew Lewis, to make strategic investments in energy and infrastructure that promote decarbonization. The team will identify, develop, and execute commercial opportunities outside of the company’s existing businesses to enhance growth and the company’s ability to serve the evolving energy needs of the market.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Will the November Fed rate announcement cause a stock market rally?

The next time the Federal Reserve is expected to adjust the target range of the Fed Funds overnight lending rate is Wednesday, November 2nd. Few have doubt at this point that this will again be a 0.75% increase. That level is already baked into equities. Stock market strength and direction shouldn’t veer much from the rate move but could dramatically turn as a result of the Fed’s forward guidance. If Chairman Powell & Co. suggests a slower benchmark lending rate increase, it would be a very welcome sign for investors.

Focus on the Post Meeting Announcement

There are already signs the Fed may slow the pace of Fed Funds increases. There are also indications it may alter its quantitative tightening (QT) in a way that could quicken a yield curve steepening. In other words, the speed of QT may increase. To date, the real rate of return on bonds, of most all maturities, is viewed as unnatural as they are below zero (Yield – Inflation = Real Rate). While an increase in QT may do more to raise rates and reduce the money supply, the effect is stealthier; it doesn’t provide a panicky headline for investors to react to abruptly.

Some Fed governors have already shown signs that they believe the best course from here is to slow the ratcheting up of the funds level and perhaps even stop raising Fed Funds rates early next year. A hiatus would allow them time to see if the moves have had an impact and give members a chance to see if further moves are prudent. The Fed always runs the risk of overreacting and going too far when tightening; this “oversteering” by previous Feds has occurred a high percentage of the time as they contend with a lag between monetary policy shifts and economic reaction.

Where We Are, Where We’re Going

In the most aggressive pace since early 1980, so far in 2022, the Fed raised its benchmark federal-funds rate by 0.75 points at each of its past three meetings. The most recent move was in late September. This left the overnight interest rate at a range between 3% and 3.25%.

The stock market wants the Fed to slow down. It rallied in July and August on expectations that the Fed might slow the pace of increase. Slowing, at least at the time, would have conflicted with the central bank’s inflation target because easy financial conditions stimulate spending, economic growth, and related inflation pressures. This rally in stocks may have prompted Powell to redraft a very public speech to economists in late August. He spoke about nothing else for eight minutes at Jackson Hole except for his resolve to win the fight against higher prices.

But sentiment related to how forceful the FOMC now needs to be may be shifting. Fed Vice Chairwoman Lael Brainard, joined by other officials, have recently hinted they are uneasy with raising rates by 0.75 points beyond next month’s meeting. In a speech on Oct. 10th, Brainard laid out a case for pausing rate rises, noting how they impact the economy over time.

Others that are concerned about the danger of raising rates too high include Chicago Fed President Charles Evans. Evans told reporters on Oct. 10th that he was worried about assumptions that the Fed could just cut rates if it decided they were too high. He felt a need to share his thought that promptly lowering rates is always easier in theory than in practice. The Chicago Fed President said he would prefer to find a rate level that restricted economic growth enough to lower inflation and hold it there even if the Fed faced “a few not-so-great reports” on inflation. “I worry that if the way you judge it is, ‘Oh, another bad inflation report—it must be that we need more [rate hikes],’… that puts us at somewhat greater risk of responding overly aggressive,” Evans said.

Kansas City Fed President Esther George also had something to say on this topic last week. She said she favored moving “steadier and slower” on rate increases. “A series of very super-sized rate increases might cause you to oversteer and not be able to see those turning points,” according to the Kansas City Fed President.

Others like Fed governor Waller don’t view steady 0.75% increases as a done deal but instead something to be reviewed, “We will have a very thoughtful discussion about the pace of tightening at our next meeting,” Waller said in a speech earlier this month.

The caution surrounding oversteering isn’t unanimous; at least one Fed official wants to see proof that inflation is falling before easing up on the economic brake pedal. “Given our frankly disappointing lack of progress on curtailing inflation, I expect we will be well above 4% by the end of the year,” said Philadelphia Fed President Patrick Harker.

The ultimate result is likely to come down to what Mr. Powell decides as he seeks to fashion a consensus. In the past, votes, while not always unanimous, tend to defer to the Chairperson at the time.

Take-Away

If, after the next FOMC meeting, the Fed is entertaining a lower 0.50% rate rise in December (not 0.75%), they will prepare the markets (bond, stock, and foreign exchange) for the decision in the moments and weeks following their Nov. 1-2 meeting. If this occurs, it could cause stocks to perform well just before election day and perhaps make up some lost ground in the year’s final two months.

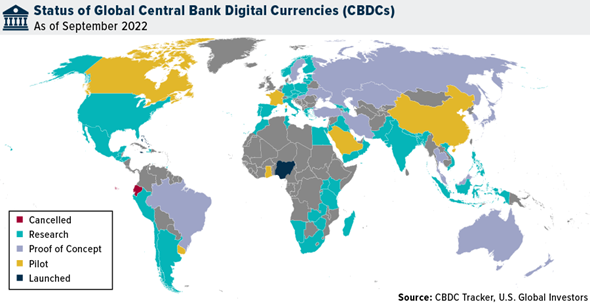

Central Bank Digital Currencies May Be Inevitable, And That’s a Problem

Readers of a certain age will remember Carnac the Magnificent, Johnny Carson’s recurring alter ego. As Carnac, the late-night host would list off three seemingly unrelated words, all of which answered a question that was sealed in an envelope that he held to his forehead.

Today we’re going to play the same game, with the answers being PayPal, Kanye (or Ye, as he’s now known) and central bank digital currencies (CBDCs). And the question: What are the consequences of financial hyper-centralization?

Some of you will make the connections immediately. For everyone else, let me explain.

PayPal, the financial technology (fintech) firm cofounded over 20 years ago by Peter Thiel, Elon Musk and others, was roundly criticized last week after an update to its terms of service showed that the company would fine users $2,500 for, among other things, spreading “misinformation.” A PayPal spokesperson was quick to walk back the update, even claiming that the language “was never intended to be inserted in our policy,” but the damage was done. #DeletePayPal started trending on Twitter, and the company’s stock tanked nearly 12%.

As for Ye, he and his apparel brand Yeezy were reportedly dropped last week by JPMorgan Chase. In a letter widely shared on social media, JPMorgan says Ye has until November 21 to move his business finances elsewhere.

No reason was given by the bank to cut ties with the billionaire rapper, but it’s easy to surmise that Ye was targeted for his political beliefs and outspokenness. I don’t agree with everything he says, nor should you. He’s a controversial figure, and his comments are often erratic and designed to get a rise out of his critics. I’m not sure, though, that this should have anything to do with his access to banking services.

The two cases of PayPal and Ye represent what I believe are legitimate and mounting concerns surrounding centralized finance. Admittedly, Ye is an extreme example. He’s a multiplatinum recording artist with tens of millions of social media followers. But there’s a real fear among everyday people that they too can be fined or have their accounts frozen or canceled at any time for expressing nonconformist views.

This article was republished with permission from Frank Talk, a CEO Blog by Frank Holmes of U.S. Global Investors (GROW). Find more of Frank’s articles here – Originally published October 19, 2022

CBDCs Are Inevitable

That brings me to CBDCs. I was in Europe last week where I attended the Bitcoin Amsterdam conference, and I was honored to participate on a lively panel that was aptly titled “The Specter of CBDCs.”

As I told the audience, I believe CBDCs are inevitable, ready or not. There are too many perceived benefits. These currencies offer broad public access and instant settlements, streamline cross-border payments, preserve the dominance of a nation’s currency and reduce the operational costs of maintaining physical cash. Here in the U.S., millions upon millions of dollars’ worth of bills and coins are lost or accidentally thrown away every year. CBDCs would solve this problem.

An estimated 90% of the world’s central banks currently have CBDC plans somewhere in the pipeline. As I write this, only two countries have officially launched their own digital currencies—the Bahamas with its Sand Dollar, and Nigeria with its eNaira—but expect many more to follow in the coming years. China, the world’s second largest economy, has been piloting its own CBDC for a couple of years now, and India, the seventh largest, released a report last week laying out the “planned features of the digital Rupee.” A pilot program of the currency is expected to begin “soon.” And speaking at an annual International Monetary Fund (IMF) meeting, Treasury Secretary Janet Yellen said that the U.S. should be “in a position where we could issue” a CBDC.

CBDCs Improve Bitcoin’s Use Case

Due to the centralized nature of CBDCs, however, there are a number of concerns that give many people pause. Unlike Bitcoin, which is decentralized and anonymous, CBDCs raise questions about privacy, government interference and manipulation.

In the White House’s own review of digital currencies, issued last month, policymakers write that a potential U.S. coin system should “promote compliance with” anti-money laundering (AML) and counter-terrorist financing (CFT) laws. Such a system should also “prevent the use of CBDC in ways that violate civil or human rights.” Further, it should be sustainable; that is, it should “minimize energy use, resources use, greenhouse gas emissions, other pollution and environmental impacts on local communities.”

Nothing about this sounds inherently nefarious, but then, some of us may have said the same thing about PayPal’s “misinformation” policy (whether intended or not) and JPMorgan’s decision to end its relationship with a polarizing celebrity.

I believe this only improves Bitcoin’s use case, especially if we’re headed for a digital future.

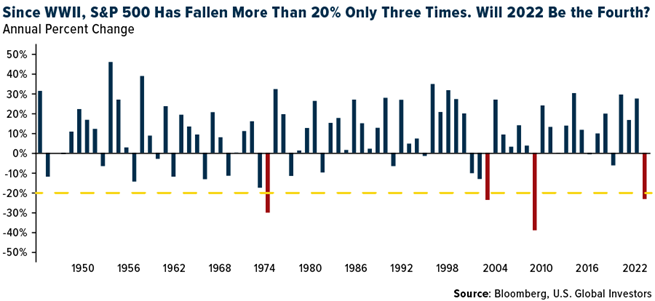

Worst 60/40 Portfolio Returns In 100 Years

With only a little over 50 trading days left in 2022, it looks more and more likely that this will be among the very worst years in history for investing. Since World War II, there have been only three instances, in 1974, 2002 and 2008, when the S&P 500 ended the year down more than 20%. If 2022 ended today, it would mark only the fourth time.

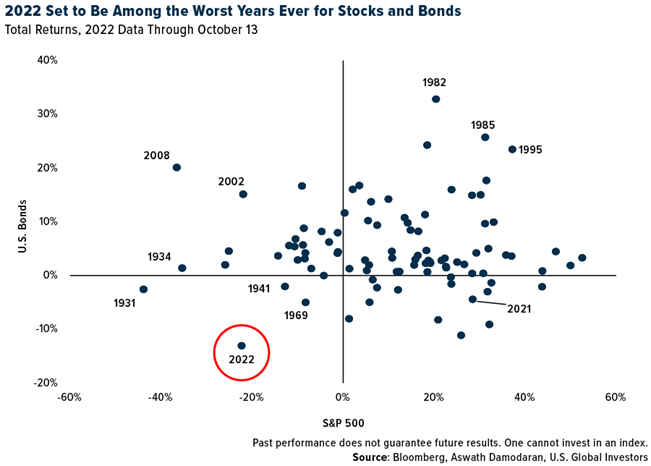

Here’s another way to visualize it. The scatter plot below shows annual returns for the S&P 500 (horizontal axis) and U.S. bonds (vertical axis). As you can see, 2022 falls in the most undesirable quadrant along with the years 1931, 1941 and 1969. Not only have stocks been knocked down, but so have bond prices as the Fed continues to hike rates at an historically fast pace.

What this means is that the traditional “60/40” portfolio—composed of 60% stocks and 40% bonds—now faces its worst year in 100 years, according to Bank of America.

My takeaway is that diversification matters more now than perhaps in any other time in recent memory. Real assets like gold and silver look very attractive right now. Real estate is an option. And Bitcoin continues to trade at a discount. Diversification doesn’t ensure a positive return, but it could potentially spell the difference between losing a little and losing a lot.

You can watch the panel discussion at Bitcoin Amsterdam featuring Frank Holmes by clicking here!

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. Diversification does not protect an investor from market risks and does not assure a profit.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. None of the securities mentioned in the article were held by any accounts managed by U.S. Global Investors as of 9/30/2022.

RICHMOND, Va.–(BUSINESS WIRE)– Bowlero Corp. (NYSE: BOWL), the world’s leader in bowling entertainment, announced today that Thomas Shannon, Founder & Chief Executive Officer of Bowlero Corp., will be interviewed by Jim Cramer on tonight’s edition of Mad Money with Jim CrameronCNBC.

The interview is scheduled to air tonight during the 6:00 PM ET showing of Mad Money. To view the interview, please visit CNBC’s website at www.cnbc.com/live-tv/ or visit the CNBC channel anywhere you get live TV.

About Bowlero Corp

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 27 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM), announced today that it will present at the Annual LD Micro Main Event XV investor conference at 4:00 P.M. Central Time on October 26, 2022. The presentation will be available on the investor relations portion of the company’s website www.salemmedia.com prior to the company’s presentation.

ABOUT LD MICRO/SEQUIRE:

LD Micro began in 2006 with the sole purpose of being an independent resource to the microcap world. What started as a newsletter highlighting unique companies, has transformed into the pre-eminent event platform in the space. For more information, please visit ldmicro.com.

In September 2020, LD Micro was acquired by SRAX, a financial technology company that unlocks data and insights for publicly traded companies. Through its premier investor intelligence and communications platform, Sequire, companies can track their investors’ behaviors and trends and use those insights to engage current and potential investors across marketing channels. For more information on SRAX, visit srax.com and mysequire.com.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Marks the Company’s 10th, 11th, and 12th Completed Acquisitions of 2022

Robust Pipeline of Definitive Agreements Remain

RICHMOND, Va., Oct. 20, 2022 /PRNewswire/ — Bowlero Corp., (NYSE: BOWL) the world’s leader in bowling entertainment, announced today that it has completed three more acquisitions from its pipeline of definitive agreements in 2022. This marks the Company’s 7th completed acquisition of FY23.

Brett Parker, President & Chief Financial Officer of Bowlero Corp stated, “We are delighted with the pace and quality of our acquisitions so far in 2022, with these completions marking our 45th location in California and expanding our presence in Wisconsin from three to five.”

On the West Coast, Strikes Unlimited is a 50-lane center in Sacramento, CA with state-of-the-art technology, arcade games, an on-site pro-shop and home to the Halftime Bar and Grill.

Super Bowl Family Entertainment Center, located in Wisconsin, is a 48-lane center featuring a wide selection of arcade games, blacklight bowling, leagues and a sports bar and grill. Additionally, located minutes away from downtown Milwaukee, is JB’s on 41. With 10 private luxury suites, 35 modern bowling lanes, 40 arcade games and much more, this location is a nationally and locally ranked top bowling and entertainment destination.

All three locations will officially open under Bowlero Corp management the weekend of October 21st.

“Our pipeline for additional deals remains robust, and we will continue to pursue accelerated growth through our proven strategy of acquisitions and new builds,” said Parker in closing.

About Bowlero Corp

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 27 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NYC NDRS. We spent Tuesday with Comtech CEO Ken Peterman and CFO Michael Bondi in a series of NDRS meeting with institutional investors. Mr. Peterman outlined his transformative vison for the Company to capitalize on significant end market opportunities that play to Comtech’s existing leadership positions in both the terrestrial wireless and satellite communications spaces.

One Comtech. Step one is the implementation of a “One Comtech” vision, dismantling the prior siloed approach. We believe the Company could begin to see the fruits of this change as soon as two or three quarters, with enhanced efficiencies and synergies dropping to the bottom line or, potentially, re-invested in the business.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.