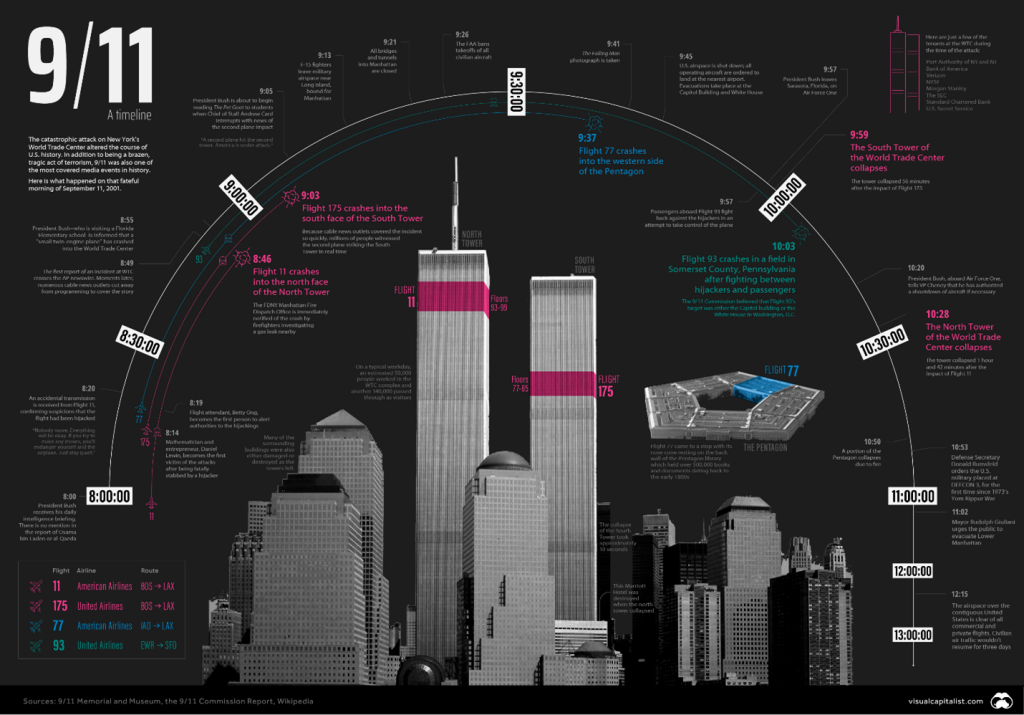

September 11, a Retrospective Account of Investment Fallout and Recovery

I wasn’t in New York City on September 11, 2001. Just prior to 911, I had taken a position as CIO for a major Wall Street firm headquartered in lower Manhattan; however, the trading floor I was responsible for was about 50 miles east of ground zero. I took the position outside NYC to be closer to my home and family – the benefit of my decision became apparent all at once, at 8:45 am that Tuesday morning, then reinforced 18 minutes later.

Twenty-one years have passed since then, the children of the deceased are now adults, and financial activity is spread much further than one small area in lower Manhattan. Although much has changed, it’s important to look back and recognize how the investment markets handle devastation and, at the same time, recognize how humans here and around the world will band together when others need help.

The opening bells at the New York Stock Exchange (NYSE) and Nasdaq were silent at 9:30 that morning. They remained silent until September 17, as traders and investors feared what their positions would be worth upon the reopening of the financial markets after the longest close on record.

Once reopened, the Dow Jones fell 7.1% or 684 points, setting a record at the time for the highest one-day loss in the exchange’s history. By Friday, the NYSE had experienced the greatest one-week decline in its history. The Dow 30 was down more than 14%, the S&P 500 plunged 11.6%, and the Nasdaq dropped 16%. In all, about $1.4 trillion in wealth disappeared during the five trading days. Since then, this record has only been surpassed once at the early stages of the pandemic.

In hindsight, the industries most negatively impacted make sense. Airlines and the insurance sectors lost tremendous value. A flight to quality made gold popular as the price per ounce leaped 6% to $287.

Gas and oil prices quickly rose as fears that oil imports from the Middle East would be slowed or stopped altogether. Those fears lasted about a week; then, after no new attacks and a clearer understanding of the intentions of government officials, index levels returned to near their pre-911 levels.

The sectors that experienced major gains after the attacks include technology companies and certainly defense and weapons contractors. Investors anticipated a huge increase in government borrowing and spending as the country prepared to root out terror around the world. Stock prices also spiked for communications and pharmaceutical companies.

On the U.S. options exchanges, volatility in the markets caused put and call volume to increase. Put options, designed to allow an investor to profit if a specific stock declines in price, were purchased in large numbers on airline, banking, and publicly traded insurance companies. Call options, designed to allow an investor to profit from stocks that go up in price, were purchased on defense and military-related companies. Short-term profits were made by investors who were quick to execute.

The terrorism of September 11 will, doubtless, have significant effects on the U.S. economy over the short term. An enormous effort will be required on the part of many to cope with the human and physical destruction. But as we struggle to make sense of our profound loss and its immediate consequences for the economy, we must not lose sight of our longer-run prospects, which have not been significantly diminished by these terrible events. – Fed Chairman Alan Greenspan, September 20, 2001

Since September 11

Over the following 21 years, the major U.S. stock exchanges have taken steps to make physical disruption of trading more difficult. This includes dramatically increasing the percentage of trading that is electronic. While this has made the U.S. markets less vulnerable to physical attacks, it is feared that there is increased potential for cyberattacks. “As we have digitized our lives, which has generally been a great blessing, we have sown the seeds for even greater destruction in terms of the ability to hack into our systems,” said former Securities and Exchange Commission Chairman Harvey Pitt, who led the agency on Sept. 11, 2001. “That is today’s equivalent of a 9/11 attack. There is a potential ‘black swan’ event every single day.”

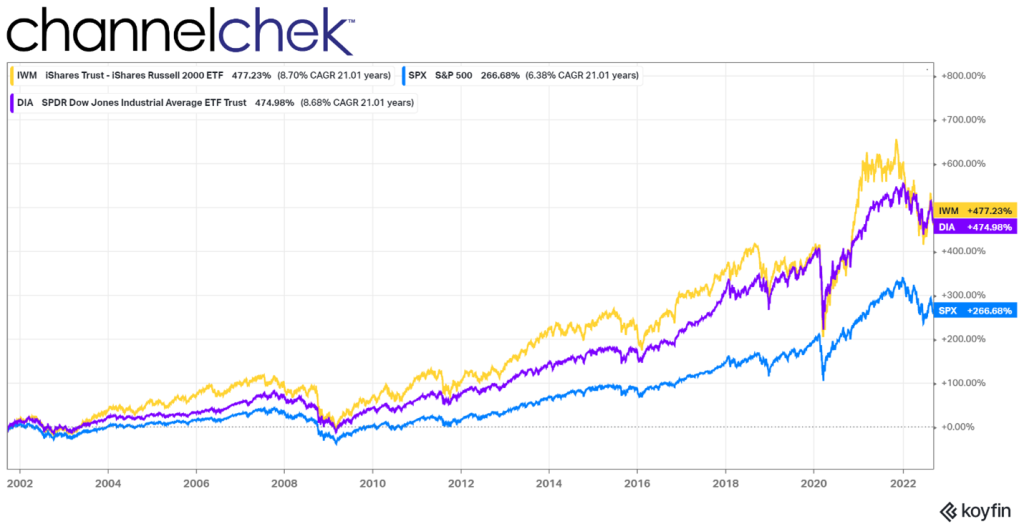

Major Market Indices Since September 11, 2001 (Source: Koyfin)

The investment markets have enjoyed above-average upward movement, despite the negative short-term impact of the black swan event. In the nearly 20 years since Sept. 11, the S&P 500, Nasdaq 100, and Russell 2000 Small-Cap index has risen more than four-fold. The bond market has also been strong (persistent low rates) despite increased borrowing to fund defense operations to finance America’s 911 response.

The U.S. economy itself has had long periods of expansion since 2021, even with the mortgage market crisis from December 2007 to June 2009, and the economic challenges from the response to the COVID-19 pandemic.

The costs, however, are likely to continue to be borne by taxpayers for generations. Interest-related costs alone on debt which financed military operations, including the long Afghanistan war, which was resolved last year when the U.S. withdrew after 20 years, and the protracted conflict in Iraq from 2003 to 2011, are high. The economic drag of these costs, while not fully measurable, are real.

The U.S. government financed the wars with debt, not taxes. Interest rates have been low, but taxpayers have already helped pay approximately $1 trillion in interest costs on the debt incurred to finance the two wars. These interest costs are expected to balloon to $2 trillion by 2030 and to $6.5 trillion by 2050 (according to the Watson Institute at Brown University). This places upward pressure on interest rates and places downward pressure on economic activity. One reason is that taxes used to fund interest costs take money from the economy without providing any stimulus or new material benefit.

Off Wall Street

September 11 radically changed the national mood and political environment. Polls and surveys taken just before the 911 attacks found Americans growing less certain about the direction of the country as a recession began to weigh down the ability to be optimistic. A full 44 percent of the country thought it was headed in on the wrong direction, according to the August 29-30, 2001 New Models survey.

Logic might suggest that after a successful attack, people’s attitudes toward the direction of the country would trend toward a worse future. Reporters, politicians, and spokespeople all predicted a terrible economic shock; their forecast seemed supported by the first week’s plunge in markets. But the events of that day seemed to give citizens purpose. In fact, statistics that indicated the “direction of the country” showed that optimism surged. An October 25-28 CBS/NY Times survey reported that people felt the country was headed in the right direction by a two-to-one margin. A sense of pride in who we are as a country and as individuals overcame negative economic news in an unprecedented way.

Take Away

It has been over two decades since what many of us think of as recent. The truth is, children born on September 11, 2021 or before are now of drinking age. But history can prepare us for new events. The market’s first reaction to tragic news is always down; when proven temporary, bargain hunters come in, then the market has always resumed its historical growth trend upward.

The markets now trade more digitally with almost no need for runners in lower Manhattan and far less open-outcry and paper jockeying by masses of people working for companies in one small section of Manhattan island. But the new threats are also real, a cyber attack on electronic records or transactions could be devastating in its own way.

Challenges even those caused by tragedy provide opportunity and even purpose. September 11, and its aftermath are proof of this.

MIAMI, Sept. 09, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, today announced that its Chief Executive Officer, Dmitry Kozko, will present at the H.C. Wainwright 24th Annual Global Investment Conference at 11:30 a.m. ET on September 14, 2022.

Participants may access a live webcast of the presentation on the Motorsport Games Investor Relations site at https://ir.motorsportgames.com/ under “News & Events.” A replay will be archived online for 90-days.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. RFactor 2 also serves as the official sim racing platform of Formula E, while also powering Formula 1™ centers through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on these websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent drill results. Labrador Gold released results from recent drilling associated with its 100,000-meter drill program at its 100%-owned Kingsway gold project targeting the Appleton Fault Zone over a 12-kilometer strike length.A total of 52,648 meters have been drilled to date with assays pending for samples from approximately 3,343 meters of core. The company has four drill rigs operating, including two at the Big Vein target, one rig at the Golden Glove target, and one at the CSAMT target. Till sampling and prospecting continues to generate new drill targets along the Appleton Fault Zone and the gabbro trend north and south of Midway. Drilling on these targets will commence once initial drilling at the CSAMT target is complete.

Big Vein results continue to impress. At the Big Vein target, Hole K-22-177 returned 2.02 grams of gold per tonne over 32 meters from 134 meters depth that included 18.08 grams of gold per tonne over 0.63 meters and 11.42 grams of gold per tonne over 1.05 meters. It represents the longest mineralized intersection on the property to date. Hole K-22-187 at Big Vein southwest intersected 12.84 grams of gold per tonne over 0.8 meters from 341 meters depth.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ark Invest’s Cathie Wood Finds the Federal Reserve Quixotic

On Wall Street, staying with the herd guarantees average gains or losses. Wandering far from the herd adds two more possibilities. You may still have average performance, you may exceed the averages, or you may get slaughtered. ARK Invest’s Cathie Wood likes to explore her own field in which to graze, far from the herd. This preference shows in her funds performance. At times her returns have far exceeded competing hedge funds, and at other times they fall well below the pack.

In October of 2021, before Fed Chairman Powell changed his thinking that inflation may not be transitory, the renowned hedge fund manager, and market guru, Cathie Wood began sounding alarm bells about her fear of deflationary pressures. At the same time, she warned of job losses due to displacement as technology would reduce costs and the need for the current skill sets in the labor force.

For months renowned investor Cathie Wood has said that the Federal Reserve should stop raising interest rates, that the economy is seeing deflation rather than inflation, and that it is in a recession.

Even as others in the”transitory” camp have come more in line with the official position of the Fed on inflation, she has remained steadfast to her idea that new technology will solve supply issues. Supply is an important inflation input, and that innovation may oversupply to a point where the economy may struggle with falling prices.

This week she tweeted a few reasons for her forecast and shared her thoughts on Jerome Powell’s address at the Jackson Hole Economic Symposium.

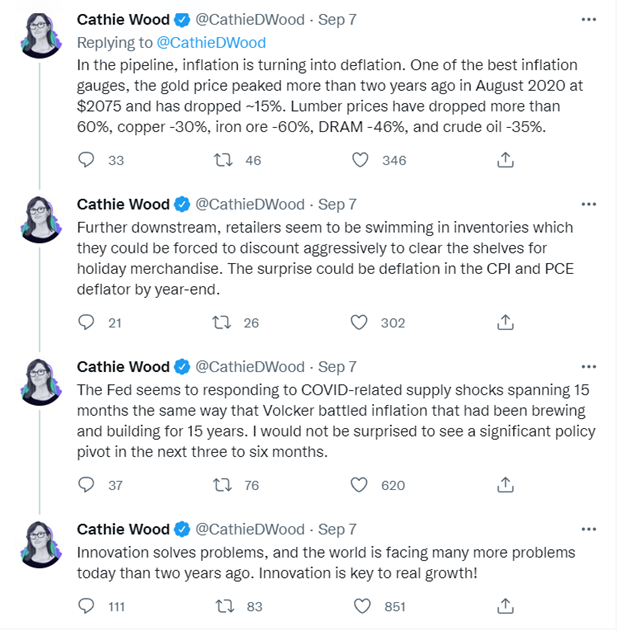

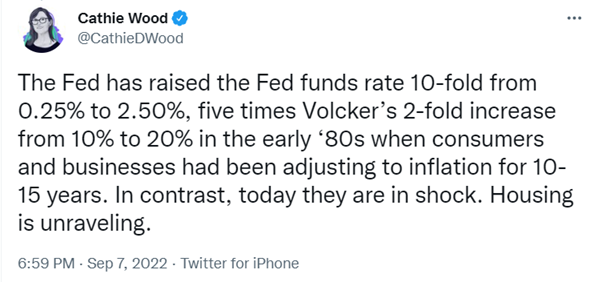

Her view is that the Fed has overshot the target. Wood, who was already working on Wall Street during the high inflation 1970’s, tweeted her reasons for this belief. High on her list is the price of gold (expressed in dollars) which she says is one of the best inflation gauges. Gold, she tweeted, “peaked more than two years ago.”

She also reminded followers of the price movements of other commodities, all down. These include lumber’s price decrease of 60%, iron ore 60%, oil 35%, and copper 30%. Much closer to final consumer prices, she highlighted that retailers are flush with inventories that don’t match the selling season. They’re discounting to clear shelves which could result in a deflation print in one of the more popular inflation gauges.

The Fed chairman who last fought inflation with unblinking resolve is Paul Volcker. Ms. Wood reminded her Twitter followers that the inflation he was battling had been “brewing and building for 15 years.” In comparison, she said inflation under Jay Powell’s watch is only 15 months old and Covid-related. She thinks the current Fed Chair has gone too far, and “I wouldn’t be surprised to see a significant policy pivot over the next three to six months,” Wood said.

A Quixotic Fed?

Powell and his colleagues are looking at the wrong data, Wood tweeted. “The Fed is basing monetary policy decisions on backward indicators: employment and core inflation,” she tweeted. “Inflation is turning into deflation,” she said in another tweet.

Wood said, comparing the two Fed chairpersons, Powell invoked Volcker’s name four times in the Jackson Hole speech. Her tweets explained inflation was much higher in Volker’s era. “Until Volker took over [of the Fed] In 1979, 15 years after the start of the Vietnam War and the Great Society, did the Fed launch a decisive attack on inflation,” Wood detailed.

“Conversely, in the face of two-year supply-related inflationary shocks, Powell is using Volker’s sledgehammer and, I believe, is making a mistake.”

Take Away

Without different opinions and different investment holding periods, there would be no market. We’d all speculate on the same things, and they’d continue upward until the last dollar was invested.

Ark Invest’s flagship Arc Innovation ETF (arkk) has fallen 55% this year, more than double the fall-off of the indexes. When discussing current performance Wood has defended her strategy by reminding others that she has an investment horizon of five years. As of Sept. 7, Arc Innovation’s five-year annualized return was 5.81%.

Cathie Wood has continued an almost year-long campaign warning of deflation and saying the Federal Reserve should stop raising interest rates, and that the economy is in a recession. If she is right and has selected the investments that benefit from being correct, then those invested in her funds will be glad they placed some of their investment funds away from the herd.

Making EVs Without China’s Supply Chain is Hard, But Not Impossible – 3 Supply Chain Experts Outline a Strategy

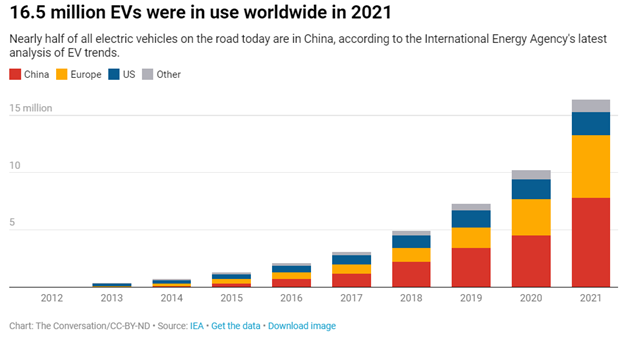

Two electrifying moves in recent weeks have the potential to ignite electric vehicle demand in the United States. First, Congress passed the Inflation Reduction Act, expanding federal tax rebates for EV purchases. Then California approved rules to ban the sale of new gasoline-powered cars by 2035.

The Inflation Reduction Act extends the Obama-era EV tax credit of up to US$7,500. But it includes some high hurdles. Its country-of-origin rules require that EVs – and an increasing percentage of their components and critical minerals – be sourced from the U.S. or countries that have free-trade agreements with the U.S. The law expressly forbids tax credits for vehicles with any components or critical minerals sourced from a “foreign entity of concern,” such as China or Russia. That’s not so simple when China controls 60% of the world’s lithium mining, 77% of battery cell capacity and 60% of battery component manufacturing. Many American EV makers, including Tesla, rely heavily on battery materials from China.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It was written by and represents the research-based opinions of Ho-Yin Mak, Associate Professor in Operations & Information Management, Georgetown University – Christopher S. Tang, Professor of Supply Chain Management, University of California, Los Angeles – Tinglong Dai, Professor of Operations Management & Business Analytics, Carey Business School, Johns Hopkins University.

The U.S. needs a national strategy to build an EV ecosystem if it hopes to catch up. As experts in supply chain management, we have some ideas.

Why the EV Industry Depends Heavily on China

How did the U.S. fall so far behind?

Back in 2009, the Obama administration pledged $2.4 billion to support the country’s fledgling EV industry. But demand grew slowly, and battery manufacturers such as A123 Systems and Ener1 failed to scale up their production. Both succumbed to financial pressure and were acquired by Chinese and Russian investors.

China took the lead in the EV market through an aggressive mix of carrots and sticks. Its consumer subsidies raised demand at home, and Beijing and other major cities set licensing quotas mandating a minimum share of EV sales.

China also established a world-dominating battery supply chain by securing overseas mineral supplies and heavily subsidizing its battery manufacturers.

Today, the U.S. domestic EV supply chain is far from adequate to meet its goals. The new U.S. tax credits are designed to help turn that around, but building a resilient EV supply chain will inevitably entail competing with China for limited resources.

A comprehensive national strategy entails measures for the short, medium and long term.

Short-Term: What Can be Done Now?

Six of the 10 best-selling EV models in 2022 are already assembled in the U.S., fulfilling the Inflation Reduction Act’s final assembly location clause. The Hyundai-Kia alliance, which has three of the other four bestsellers, plans to open an EV assembly line in Georgia. Volkswagen has also started assembling its ID.4 electric SUV in Tennessee.

The challenge is batteries. Besides the Tesla-Panasonic factories in Nevada and planned in Kansas, U.S.-based battery manufacturers trail their Chinese counterparts in both size and growth.

For the U.S. to scale up its own production, it needs to rely on strategic partners overseas. The Inflation Reduction Act allows imports of critical minerals from countries with free trade agreements to still qualify for incentives, but not imports of battery components. This means overseas suppliers like Korea’s “Big Three” – LG Chem, SK Innovation and Samsung SDI – which supply 26% of the world’s EV batteries, are shut out, even though the U.S. and Korea have a free trade agreement.

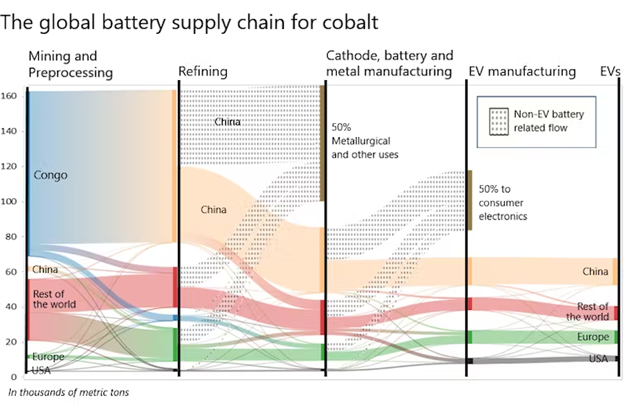

The bulk of the world’s cobalt is mined in the Democratic Republic of Congo but processed and turned into lithium-ion battery components by Chinese companies. This chart shows the pathways from mining to EVs.

The Korea Automobile Manufacturers Association has asked Congress to make an exception for Korean-made EVs and batteries.

In the spirit of “friend-shoring,” the Biden administration could think of a temporary waiver as a stopgap measure that makes it easier for Korean battery makers to move more of their supply chain to the U.S., such as LG’s planned battery plants in partnerships with GM and Honda.

The 2021 Infrastructure Act also provided $5 billion to expand charging infrastructure, which surveys show is critical to bolstering demand.

Medium-Term: Diversifying Lithium and Cobalt Supplies

A strong and concerted effort in trade and diplomacy is necessary for the U.S. to secure critical mineral supplies.

As EV sales rise, the world is expected to face a lithium shortage by 2025. In addition to lithium, cobalt is needed for high-performance battery chemistries.

The problem? The Democratic Republic of the Congo is where 70% of the world’s cobalt is mined, and Chinese companies control 80% of that. The distant second-largest producer is Russia.

The Biden administration’s “friend-shoring” vision has a chance only if it can diversify the lithium and cobalt supply chains.

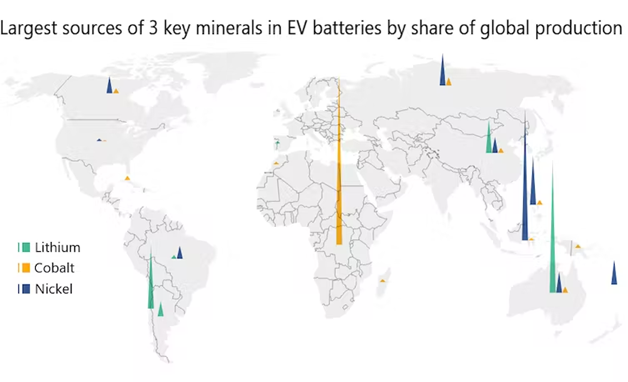

Lithium, cobalt and nickel are critical components in many EV batteries. The largest 2021 production sources included the Democratic Republic of Congo for cobalt; Australia, Chile and China for lithium; and Indonesia, the Philippines and Russia for nickel.

The “Lithium Triangle” of South America is one region to invest in. Also, Australia, a key U.S. ally, leads the world in lithium production and possesses rich cobalt deposits. Waste from many of Australia’s copper mines also contains cobalt, lowering the cost. GM has reached an agreement with the Australian mining giant Glencore to mine and process cobalt in Western Australia for its Ohio battery plant with LG Chem, bypassing China.

A way to avoid cobalt altogether also exists: lithium-iron-phosphate batteries are about 30% cheaper to make because they use minerals that are easy to find and plentiful. However, LFP batteries are heavier and have less power and range per unit.

For years, Chinese companies like CATL and BYD were the only ones making LFP batteries. But the patent rights associated with LFP batteries expire this year, opening up an important opportunity for the U.S.

Since not everyone needs a high-end electric supercar, affordable EVs powered by LFP batteries are an option. In fact, Tesla now offers Model 3s with LFP batteries that can travel about 270 miles on a charge.

The 2021 Bipartisan Infrastructure Law set aside $3.16 billion to support domestic battery supply chains. With the Inflation Reduction Act’s emphasis on supporting more affordable EVs – it has price caps for vehicles to qualify for incentives – these funds will be needed to help scale up domestic LFP manufacturing.

Long-Term: US Critical Mineral Production

Replacing overseas critical materials with domestic mining falls under long-term planning.

The scale of current domestic mining is minuscule, and new mining operations can take seven to 10 years to establish because of the lengthy permitting process. Lithium deposits exist in California, Maine, Nevada and North Carolina, and there are cobalt resources in Minnesota and Idaho.

Finally, to build an industrial commons for EVs, the U.S. must continue to invest in research and development of new battery technologies.

Pools of brine containing lithium carbonate stretch across a lithium mine in the Atacama Desert of Chile. Local opposition can be a challenge to mining proposals. Nuno Luciano (Flickr)

Also, end-of-life battery recycling is essential to the sustainability of EVs. The industry has been kicking the can down the road on this, as recycling demand has been minuscule thus far given the longevity of batteries. Yet, as a proactive step, the Inflation Reduction Act specifically permits battery content recycled in North America to qualify for the critical mineral clause.

To make this happen, the federal and state governments could use takeback legislation similar to producer responsibility laws for electronic waste enacted in more than 20 states, which stipulate that producers bear the responsibility for collecting, transporting and recycling end-of-cycle electronic products.

What’s Ahead

With the new law, the Biden administration has set its sights on a future transportation system that is built in the U.S. and runs on electricity. But there are supply chain obstacles, and the U.S. will need both incentives and regulations to make it happen.

California’s announcement will help. Under the Clean Air Act, California has a waiver that allows it to set policies more strict than federal law. Other states can choose to follow California’s policies. Seventeen other states have adopted California’s emissions standards. At least three, New York, Washington and Massachusetts, have already announced plans to also phase out new gas-powered cars and light trucks by 2035.

CALGARY, AB, Sept. 8, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV); (OTCQX: ALVOF) announces a discovery at our 49.1% Caburé Unit C well, record August sales volumes and an operational update.

7-CARN-2D-BA Well (“Unit-C Well”)

The Unit-C well at the Caburé Unit (49.1% Alvopetro) was spud in July and drilled to a total measured depth (“MD”) of 2,096 metres. Based on Alvopetro’s analysis of open hole logs and fluid samples confirming hydrocarbons, the well has potential net pay in multiple formations using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off. The well was drilled with development objectives in the Pojuca and Marfim sands that are producing from, or tested hydrocarbons in, the offsetting Unit well (IMET-10). The well was also drilled with exploratory objectives in the deeper Maracangalha sands that are producing on the eastern side of the bounding fault. The well encountered a total of 52.6 metres of potential net hydrocarbon pay at an average 37.2% water saturation and average porosity of 16.8% in multiple formations. Fluid samples were also collected using a formation testing tool with natural gas being recovered from a sand in the Maracangalha Formation at 1,443.5 metres total vertical depth and oil from a deeper sand at 1,633.6 metres total vertical depth. Potential net pay is summarized, by formation, as follows:

Formation

Objective

Net Pay (metres)

Water Saturation (%)

Porosity (%)

Pojuca

Development

19.9

31.9

24.6

Marfim

Development

3.9

30.4

12.1

Maracangalha

Exploration

28.8

41.7

12.1

Total

52.6

37.2

16.8

August 2022 Sales Volumes

Our August daily sales volumes averaged 2,727 boepd, including natural gas sales of 15.6 MMcfpd, and associated natural gas liquids sales from condensate of 120 bopd, based on field estimates. Our August sales volumes are a record for Alvopetro, 8% above July sales volumes of 2,514 boepd and 16% above average volumes in the second quarter of 2022 of 2,359 boepd.

Operational Update

On August 26th, we spud our 182-C2 well on Block 182 (100% Alvopetro). The 182-C2 well is a follow-up well to our 182-C1 well drilled earlier this year and targets the Agua Grande and Sergi Formations further east from the bounding fault encountered during drilling of the 182-C1 well.

On our Murucututu project, the ANP inspection of our fiscal meter station at our 183-1 location was completed last week and, subject to receipt of all finalized reports, we expect to commence production from our 183-1 well this month.

Corporate Presentation

Alvopetro’s updated corporate presentation is available on our website at:

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the Unit C well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities, should be considered to be preliminary until testing, detailed analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the Unit C well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Cautionary statements regarding the filing of a Notice of Discovery. The unit operator has submitted a Notice of Discovery of Hydrocarbons to the Agência Nacional do Petróleo, Gás Natural e Biocombustíveis (the “ANP”) with respect to the Unit C well. All operators in Brazil are required to inform the ANP, through the filing of a Notice of Discovery, of potential hydrocarbon discoveries. A Notice of Discovery is required to be filed with the ANP based on hydrocarbon indications in cuttings, mud logging or by gas detector, in combination with wire-line logging. Based on the results of open-hole logs, a Notice of Discovery has been filed for the Unit C well. These routine notifications to the ANP are not necessarily indicative of commercial hydrocarbons, potential production, recovery or reserves.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential hydrocarbon pay in the Unit C well, exploration and development prospects of Alvopetro and the expected timing of certain of Alvopetro’s testing and operational activities. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning results of the Unit C well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

MALVERN, Pa., Sept. 08, 2022 (GLOBE NEWSWIRE) — Baudax Bio, Inc. (NASDAQ:BXRX), a pharmaceutical company focused on innovative products for acute care settings, today announced that Gerri Henwood, the Company’s President and Chief Executive Officer, will present at the 24th Annual H.C. Wainwright Healthcare Conference, taking place in New York, New York on Wednesday, September 14, 2022 at 3:00 p.m. Eastern Time.

A webcast of the presentation will be available on the “Events” page within the investors section of the Baudax Bio website at https://www.baudaxbio.com/news-and-investors. The webcast will be archived on the company’s website for 90 days following the event.

About Baudax Bio

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. Baudax Bio markets ANJESO®, the first and only 24-hour, non-opioid, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two clinical-stage, novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Alliance Resource Partners, L.P. 2021 Schedule K-3 Now Available

Company Release – 9/8/2022 3:30 PM ET

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ “ARLP”) today announced that its 2021 Schedule K-3 reflecting items of international tax relevance is available online. Unitholders requiring this information may access their Schedule K-3 at www.taxpackagesupport.com/arlp.

A limited number of unitholders (primarily foreign unitholders, unitholders computing a foreign tax credit on their tax return and certain corporate and/or partnership unitholders) may need the detailed information disclosed on Schedule K-3 for their specific reporting requirements. To the extent Schedule K-3 is applicable to your federal income tax return filing needs, we encourage you to review the information contained on this form and refer to the appropriate federal laws and guidance or consult with your tax advisor.

To receive an electronic copy of your Schedule K-3 via email, unitholders may call Tax Package Support toll free at (800) 485-6875.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

Brian L. Cantrell Alliance Resource Partners, L.P. (918) 295-7673

2022 Restructuring Program designed to improve Profitability and Cash Flow – Expected to generate approximately $4 millionin Annualized Cost Reductions by the end of 2023

Financing Commitment will Improve Capital Structure and Deliver New Funding for the Business

Planned Reverse Stock Split Expected to Allow Motorsport Games to Re-gain Compliance with NASDAQ’s Continued Listing Standards

MIAMI, Sept. 08, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ:MSGM) (“Motorsport Games” or the “Company”) today announced several important steps forward in strengthening the Company’s business, capital structure and foundation for achieving future growth.

First, the Company executed a Support Agreement with its majority stockholder, Motorsport Network, LLC (“Motorsport Network”), pursuant to which Motorsport Network recently paid a $3 million cash advance to Motorsport Games under the terms of the parties’ pre-existing line of credit.

Second, the Company announced a new organizational restructuring program (the “2022 Restructuring Program”) that is expected to generate material annualized cost reductions of approximately $4 million by the end of 2023. The goal of the 2022 Restructuring Program is to build a stronger global business operation, enhance the Company’s cost efficiency and improve the Company’s operating margins.

In an effort to re-gain compliance with NASDAQ’s continued listing standards, the Company also announced its plans to effect a 1-for-10 reverse stock split during the fourth quarter of 2022, following stockholder approval. Motorsport Network agreed to exercise its combined 94% voting power to support the reverse stock split at a special meeting expected to be held shortly.

Dmitry Kozko, the Company’s CEO, stated, “Today’s announcement represents an important, necessary, and logical next step forward for Motorsport Games. The financing commitment and the launch of the new restructuring program represent our plans to optimize our business for the future and create a more optimal business structure that is designed to achieve success in terms of long-term profitability. The 2022 Restructuring Program, which we are implementing immediately, is expected to create a stronger global business operating model, enhance cost efficiency and improve profit margins to drive growth in operating income and Adjusted EBITDA. With the increased liquidity, and a more efficient and streamlined business, we are taking steps to becoming a stronger, more financially sound organization, while being in a better position to take on opportunities within the gaming industry and continuing to deliver for our key stakeholders and, most importantly, our deeply dedicated racing fans. That said, we recognize that we have additional work to do in terms of reinforcing our liquidity for the long-term and managing our business in these volatile markets.”

Oliver Ciesla, CEO of Motorsport Network, said, “At Motorsport Network, we are proud of the recent progress the Motorsport Games team has been making, especially on the game development side, thus, we decided to provide additional working capital to Motorsport Games. In addition, Motorsport Games has an exclusive promotion agreement with Motorsport Network under which Motorsport Games can exclusively advertise its products on our Motorsport Network channels in front of up to 62 million monthly unique users. To all motorsport series that are partners of Motorsport Games, this offers a unique marketing advantage. Also, our recent Global fan surveys with Formula 1, INDYCAR and MotoGP show the significant crossover of young gamers with motorsport fans, who desire interactive entertainment such as Motorsport Games strives to provide. With this, Motorsport Network is a strong believer in Motorsport Games’ future to successfully produce and market great interactive entertainment for the global motorsport fans and beyond.”

2022 Restructuring Program and Cost Reductions

The 2022 Restructuring Program is designed to reduce the Company’s marketing, general and administrative expenses, improve the Company’s profit and Adjusted EBITDA and maximize efficiency, cash flow and liquidity.

Through the 2022 Restructuring Program, the Company expects to eliminate approximately 20% of its overhead costs worldwide, including budgeted open positions, and deliver approximately $4 million of total annualized cost reductions by the end of 2023. The immediate headcount cost reductions are expected to deliver annualized cost reductions of approximately $2.5 million by the end of 2022, with additional actions to be taken during 2022 expected to generate an additional $1.5 million of annualized cost reductions by the end of 2023.

The 2022 Restructuring Program includes right-sizing the organization and operating with more efficient workflows and processes. The primary components of the organizational restructuring involve consolidating certain functions; reducing layers of management, where appropriate, to increase accountability and effectiveness; and streamlining support functions to reflect the new organizational structure. The leaner organizational structure is also expected to improve communication flow and cross-functional collaboration, leveraging the more efficient business processes. In addition, given the ongoing uncertain economic environment and the potential effect that it could have on net sales, this action will also provide the Company with additional flexibility.

In connection with implementing the 2022 Restructuring Program, the Company expects to recognize during 2022 approximately $0.1 million to $0.3 million of total pre-tax restructuring and related charges, consisting primarily of employee-related costs, such as severance, retention and other contractual termination benefits. The Company expects that substantially all of these restructuring charges will be paid in cash during 2022, with the balance, if any, expected to be paid in 2023. The amounts and timing of all estimates are subject to change until finalized and may vary materially based on various factors. See “Forward-Looking Statements” below.

Financing Commitment

The agreement reached with Motorsport Network will provide the Company with $3 million in cash which the Company plans to use for general corporate purposes and working capital. As a result of such cash funding, the Company has on hand approximately $4.5 million of cash. The Company continues to work with its financial advisors on longer-term solutions to its liquidity needs.

Reverse Stock Split

The Company also announced today that its Board of Directors approved a reverse split of its Class A and Class B common stock at a 1-for-10 split ratio. Pursuant to the Support Agreement, Motorsport Network agreed to vote all of its shares of Class A and Class B common stock, representing approximately 94% of the combined voting power of the Company’s Class A and Class B common stock, in favor of the reverse stock split and in favor of any required actions related to such reverse stock split. With Motorsport Network’s agreement to provide its approval, the Company will have adequate shareholder support to approve the split at the special meeting of stockholders.

The reverse stock split would be intended to increase the per share trading price of the Company’s Class A common stock, which the Company believes may make it more attractive to a broader range of institutional and other investors. The reverse stock split would also reduce certain of the Company’s compliance costs, such as NASDAQ’s listing fees, and would be intended to satisfy the Company’s compliance with the NASDAQ’s minimum closing bid price requirement for continued listing. The same reverse split ratio will be used to effect the reverse stock split of both the Company’s Class A and Class B common stock; accordingly all stockholders will be affected proportionately.

No fractional shares will be issued in connection with the reverse stock split. Shares that would otherwise have resulted in fractional shares from the reverse stock split will be collected and pooled by the Company’s transfer agent and sold in the open market. The proceeds will be allocated to the stockholders’ respective accounts who are entitled to receive cash in lieu of fractional shares. The number of common shares subject to the Company’s outstanding employee and director stock options and restricted stock, as well as the relevant exercise price per share, will be proportionately adjusted to reflect the reverse stock split. The number of shares authorized for issuance under the Company’s stock plan will also be reduced by the same reverse stock split ratio.

The Company plans to file shortly with the SEC a proxy statement which will include additional information about the reverse stock split and requesting stockholders to vote for the reverse stock split at an upcoming special meeting, which proxy statement will be available on the SEC’s website at www.sec.gov. The Company expects the reverse stock split to be consummated during the fourth quarter of 2022.

FORWARD-LOOKING STATEMENTS

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements.

These forward-looking statements include, but are not limited to, statements concerning:

(i) the Company’s plans to secure the $3 million cash advance as contemplated by the Support Agreement, to use the proceeds thereof for general corporate purposes and working capital and to reinforce its liquidity for the long-term and managing its business in these volatile markets;

(ii) the Company’s plans to implement the 2022 Restructuring Program and the expected benefits therefrom;

(iii) the Company’s expectation that it will substantially complete the employee-related actions by the end of September 2022;

(iv) the Company’s expectations regarding the amount and timing of the charges and payments related to the 2022 Restructuring Program;

(v) the Company’s expectations that as a result of the 2022 Restructuring Program, the Company will deliver approximately $4 million of total annualized cost reductions by the end of 2023, with the immediate headcount reductions expected to deliver annualized cost reductions of approximately $2.5 million by the end of 2022 and additional actions to be taken during 2022 expected to generate an additional $1.5 million of annualized cost reductions by the end of 2023; and

(vi) the Company’s plans to consummate the reverse stock split, its expected terms, conditions and timing, as well as the intended benefits of the reverse stock split.

All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to:

(i) difficulties, delays or the inability of the Company to use the proceeds thereof as intended and/or in reinforcing its liquidity for the long-term and managing its business in these volatile markets, such as due to tightening credit and equity markets, less than anticipated consumer acceptance of the Company’s games and events and/or recessionary factors in the broader economy that causes consumers to alter their purchasing habits in ways that the Company did not predict;

(ii) difficulties, delays or the inability of the Company to successfully complete the 2022 Restructuring Program, in whole or in part, which could result in less than expected operating and financial benefits from such actions;

(iii) delays in completing the 2022 Restructuring Program, which could reduce the benefits realized from such activities;

(iv) higher than anticipated restructuring charges and/or payments and/or changes in the expected timing of such charges and/or payments;

(v) less than anticipated annualized cost reductions from the 2022 Restructuring Program and/or changes in the timing of realizing such cost reductions, such as due to less than anticipated liquidity to fund such activities and/or more than expected costs to achieve the expected cost reductions; and/or

(vi) difficulties, delays, unanticipated costs or the Company’s inability to consummate the reverse stock split on the expected terms and conditions or timeline, as well as future decreases in the price of the Company’s Class A common stock whether due to, among other things, the announcement of the reverse stock split, the Company’s inability to make its Class A common stock more attractive to a broader range of institutional or other investors or an inability to increase the stock price in an amount sufficient to satisfy compliance with the NASDAQ’s minimum closing bid price requirement for continued listing.

Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. RFactor 2 also serves as the official sim racing platform of Formula E, while also powering Formula 1™ centers through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Hole K-22-177 intersected 2.02 g/t Au over 32 metres including 18.08 g/t Au over 0.63 metres and 11.42 g/t Au over 1.05 metres.

Mineralization at Big Vein remains open along strike to the southwest and northeast.

Drilling also intersected high-grade mineralization at Big Vein southwest grading 12.84 g/t Au over 0.8 metres.

TORONTO, Sept. 08, 2022 (GLOBE NEWSWIRE) — Labrador Gold Corp. (TSX.V:LAB | OTCQX:NKOSF | FNR: 2N6) (“LabGold” or the “Company”) is pleased to announce results from recent drilling targeting the prospective Appleton Fault Zone over a 12km strike length. The drilling is part of the Company’s ongoing 100,000 metre diamond drilling program at its 100% owned Kingsway Project.

Highlights of the drilling include an intersection of 2.02 g/t Au over 32 metres from 134 metres that included 18.08 g/t Au over 0.63 metres and 11.42 g/t Au over 1.05 metres in Hole K-22-177 from the north end of Big Vein. The intersection is approximately 75 metres north of the discovery outcrop. In addition, Hole K-22-187 at Big Vein southwest intersected 12.84 g/t Au over 0.8 metres from 341 metres.

The last results from initial drilling at Midway showed an intersection of 5.69 g/t Au over 1.33 metres in Hole K-22-171. Further drilling is planned at Midway to test the continuity of gabbro-hosted mineralization along strike towards Cracker.

“Drilling at Big Vein continues to deliver excellent results with the longest mineralized intersection of 32 metres grading 2.02 g/t gold drilled on the property to date. We are currently testing this intersection down dip. The intersection is approximately 30 metres north of another long intercept of 6.07 g/t Au over 19m in hole K-21-111.” said Roger Moss, President and CEO. “Big Vein has now been drilled over a strike length of approximately 520 metres and remains open both to the northeast and southwest. Two rigs continue drilling at Big Vein to test for extensions of the mineralization in both directions.”

Hole ID

From (m)

To (m)

Interval (m)

Au (g/t)

Zone

K-22-187

157.80

158.25

1.20

1.08

Big Vein SW

328.55

328.85

0.30

3.27

341.00

341.80

0.80

12.84

K-22-184

140.26

140.59

0.33

2.89

Big Vein SW

336.25

337.89

1.64

2.69

K-22-180

nsv

CSAMT

K-22-179

72.00

72.76

0.76

1.08

Golden Glove

K-22-178

nsv

Big Vein SW

K-22-177

8.00

9.00

1.00

1.01

Big Vein

93.74

94.55

0.81

1.11

134.00

166.00

32.00

2.02

including

142.77

143.40

0.63

18.08

and

158.95

160.00

1.05

11.42

212.00

215.00

3.00

2.63

245.00

248.00

3.00

3.60

265.00

266.00

1.00

1.73

K-22-176

nsv

Golden Glove

K-22-175

63.00

65.00

2.00

1.48

Big Vein

230.00

232.00

2.00

2.87

K-22-174

296.00

297.49

1.49

3.65

Big Vein SW

407.00

407.30

0.30

3.24

K-22-173

11.00

12.00

1.00

1.04

Big Vein

16.00

17.00

1.00

1.38

50.00

51.00

1.00

2.23

K-22-172

nsv

CSAMT

K-22-171

194.50

198.00

3.50

1.44

Midway

201.17

202.50

1.33

5.69

K-22-170

11.00

12.00

1.00

1.10

HTC

35.00

44.00

9.00

1.42

218.00

219.00

1.00

1.01

K-22-169

nsv

Golden Glove

K-22-168

165.91

166.21

0.30

1.01

Midway

217.90

218.40

0.50

1.82

K-22-167

57.00

62.00

5.00

1.90

Big Vein

K-22-166

nsv

Midway

K-22-165

243.00

244.00

1.00

1.05

Golden Glove

Table 1. Summary of assay results. All intersections are downhole length as there is insufficient Information to calculate true width.

A total of 52,648 metres have been drilled to date out of the planned 100,000 metre program. Assays are pending for samples from approximately 3,343 metres of core (11% of the total submitted).

Drilling at Kingsway continues with four drill rigs, two working at Big Vein, one at Golden Glove and one at the CSAMT target. Ongoing detailed till sampling and prospecting continues to generate new drill targets along the Appleton Fault Zone and the gabbro trend north and south of Midway. Drilling will begin on these targets once initial drilling at CSAMT is complete.

The Company has $23.6 million in cash and is well funded to carry out the remaining 47,000 metres of the planned drill program as well as further target generation on the property.

True widths of the reported intersections have yet to be calculated. Assays are uncut. Samples of HQ split core are securely stored prior to shipping to Eastern Analytical Laboratory in Springdale, Newfoundland for assay. Eastern Analytical is an ISO/IEC17025 accredited laboratory. Samples are routinely analyzed for gold by standard 30g fire assay with atomic absorption finish as well as by ICP-OES for an additional 34 elements. Samples containing visible gold are assayed by metallic screen/fire assay, as are any samples with fire assay results greater than 1g/t Au. The company submits blanks and certified reference standards at a rate of approximately 5% of the total samples in each batch.

Qualified Person

Roger Moss, PhD., P.Geo., President and CEO of LabGold, a Qualified Person in accordance with Canadian regulatory requirements as set out in NI 43-101, has read and approved the scientific and technical information that forms the basis for the disclosure contained in this release.

The Company gratefully acknowledges the Newfoundland and Labrador Ministry of Natural Resources’ Junior Exploration Assistance (JEA) Program for its financial support for exploration of the Kingsway property.

About Labrador Gold Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada.

Labrador Gold’s flagship property is the 100% owned Kingsway project in the Gander area of Newfoundland. The three licenses comprising the Kingsway project cover approximately 12km of the Appleton Fault Zone which is associated with gold occurrences in the region, including those of New Found Gold immediately to the south of Kingsway. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water. LabGold is drilling a projected 100,000 metres targeting high-grade epizonal gold mineralization along the Appleton Fault Zone with encouraging results. The Company has approximately $23.6 million in working capital and is well funded to carry out the planned program.

The Hopedale property covers much of the Florence Lake greenstone belt that stretches over 60 km. The belt is typical of greenstone belts around the world but has been underexplored by comparison. Work to date by Labrador Gold show gold anomalies in rocks, soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt in the vicinity of the known Thurber Dog gold showing where grab samples assayed up to 7.8g/t gold. In addition, anomalous gold in soil and lake sediment samples occur over approximately 40 km along the southern section of the greenstone belt (see news release dated January 25 th 2018 for more details). Labrador Gold now controls approximately 40km strike length of the Florence Lake Greenstone Belt.

The Company has 169,189,979 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release .

Forward-Looking Statements: This news release contains forward-looking statements that involve risks and uncertainties, which may cause actual results to differ materially from the statements made. When used in this document, the words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” and similar expressions are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. Many factors could cause our actual results to differ materially from the statements made, including those factors discussed in filings made by us with the Canadian securities regulatory authorities. Should one or more of these risks and uncertainties, such as actual results of current exploration programs, the general risks associated with the mining industry, the price of gold and other metals, currency and interest rate fluctuations, increased competition and general economic and market factors, occur or should assumptions underlying the forward looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, or expected. We do not intend and do not assume any obligation to update these forward-looking statements, except as required by law. Shareholders are cautioned not to put undue reliance on such forward-looking statements .

SAN DIEGO, Sept. 08, 2022 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leading National Security Solutions provider and industry-leading provider of high-performance, jet-powered unmanned aerial systems, announced today that its Kratos Unmanned Aerial Systems unit has received a Cost-Plus-Fixed-Fee Indefinite Delivery Indefinite Quantity contract award for $14,748,648 from the U.S. Navy for five year ordering period to continue software maintenance and updates of the BQM-177A Subsonic Aerial Targets (SSAT).

Steve Fendley, President of the Kratos Unmanned Systems Division, said, “This award provides the foundation to continue our work with the Navy, maturing and evolving the SSAT aircraft on pace with the threat environment. This enables us to collectively provide the training to stress and exercise our fleet prior to their deployments to increasingly challenging theaters of operation, ultimately strengthening our nation’s defense and helping protect the warfighter. Consistent with our corporate motto, we continue our trend to be ready for what’s next.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technology for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training, combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations, and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 26, 2021, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

MALVERN, Pa., Sept. 08, 2022 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that the Company’s Chief Scientific Officer, Arun Upadhyay, PhD, will be among the featured speakers at the 3rd Annual Gene Therapy for Ophthalmic Disorders conference, which is being held Sept. 13-16 in Danvers, Massachusetts.

Details regarding Dr. Upadhyay’s presentation are as follows:

Event:

3rd Annual Gene Therapy for Ophthalmic Disorders Conference

Topic:

Highlighting the Modifier Gene Therapy Approach for the Treatment of Retinitis Pigmentosa

Date:

September 14, 2022

Time:

9:15 a.m. ET

Location:

DoubleTree by Hilton Boston North Shore, Danvers, Mass.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Contact: Tiffany Hamilton Head of Communications IR@ocugen.com

PHOENIX, Sept. 08, 2022 (GLOBE NEWSWIRE) — Planet MicroCap today published a new Video Interview with Dave Shworan, CEO of QuoteMedia Ltd. (OTCQB: QMCI), discussing how the company is disrupting the financial data markets and competing with established industry giants, and also offers insights into the directions the company is taking moving forward.

About QuoteMedia QuoteMedia is a leading software developer and cloud-based syndicator of financial market information and streaming financial data solutions to media, corporations, online brokerages, and financial services companies. The Company licenses interactive stock research tools such as streaming real-time quotes, market research, news, charting, option chains, filings, corporate financials, insider reports, market indices, portfolio management systems, and data feeds. QuoteMedia provides industry leading market data solutions and financial services for companies such as the Nasdaq Stock Exchange, TMX Group (TSX Stock Exchange), Canadian Securities Exchange (CSE), London Stock Exchange Group, FIS, U.S. Bank, Broadridge Financial Systems, JPMorgan Chase, CI Financial, Canaccord Genuity Corp., Hilltop Securities, HD Vest, Stockhouse, TheStreet.com, Zacks Investment Research, The Motley Fool, General Electric, Boeing, Bombardier, Telus International, Business Wire, PR Newswire, FolioFN, Regal Securities, ChoiceTrade, Cetera Financial Group, Dynamic Trend, Inc., Qtrade Financial, CNW Group, IA Private Wealth, Ally Invest, Inc., Suncor, Virtual Brokers, Leede Jones Gable, Firstrade Securities, Charles Schwab, First Financial, Cirano, Equisolve, Stock-Trak, Mergent, Cision, Day Trade Dash and others. Quotestream®, QMod™ and Quotestream Connect™ are trademarks of QuoteMedia. For more information, please visit www.quotemedia.com.

About Planet Microcap Planet MicroCap is a global multimedia and publishing financial news investor portal specifically focused on covering the MicroCap market by providing news, insights, education tools and expert commentary. We have cultivated an active and engaged community of folks that are interested in learning about and to stay ahead of the curve in the MicroCap space. Planet MicroCap is your go-to destination for unfettered access to the world of MicroCap stocks and investing.