Key Points: – Alphabet gained ahead of its quarterly report, seen as a key influencer for the tech-driven “Magnificent Seven” group. – Companies like VF Corp and D.R. Horton had earnings-driven movements that affected sectors such as retail and housing. – U.S. job openings fell, while consumer confidence exceeded expectations, suggesting mixed signals on economic resilience.

Ahead of Alphabet’s highly anticipated earnings report, Wall Street’s main indexes remained mixed on Tuesday. Alphabet, a top tech leader and a key part of the so-called “Magnificent Seven” group of mega-cap stocks, traded up by 1.8% in anticipation of the report, set to be released after the market close. As one of the top-performing tech stocks, Alphabet’s performance will influence the broader market’s direction and its ongoing focus on artificial intelligence investments, which have driven much of the tech sector’s gains this year.

Alphabet’s performance comes amid a heavy week for S&P 500 earnings reports. This week, five of the “Magnificent Seven” companies, which have been instrumental in boosting the market, are scheduled to report quarterly results. Investors and analysts alike view these results as key indicators for whether Wall Street’s tech-driven momentum can continue through year-end.

Beyond Alphabet, other large tech players displayed a mixed performance, with Nvidia gaining 0.6% and Apple adding 0.2%, while Tesla fell 1.4%. The performance of these stocks is closely monitored, as they collectively represent a substantial portion of the S&P 500’s market capitalization. The potential for a leveling-off in growth between these “high fliers” and the rest of the market is increasingly under scrutiny by investors.

Adding to the mix, several other corporations released quarterly earnings reports. VF Corp, the parent company of Vans, saw a notable 22.2% jump in its stock price following the announcement of its first profit in two quarters. Conversely, D.R. Horton, the major U.S. homebuilder, dropped 8.5% after delivering revenue forecasts below market expectations. Other homebuilders also declined, with the PHLX Housing index on track for its largest single-day drop since April. Meanwhile, Ford reported that it expects to achieve the lower end of its annual profit target, sending its shares down by over 8%. Chipotle also saw a decrease ahead of its report later in the day.

In economic news, recent data from the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS) revealed that job openings in September came in at 7.44 million, lower than the expected 8 million, suggesting a possible cooling in labor market demand. Additionally, a report on consumer confidence exceeded expectations, reaching 108.7 in October compared to the estimated 99.5, indicating continued consumer resilience.

The benchmark U.S. 10-year Treasury yield also reached a high of 4.3%, marking the first time since early July it hit this level. The rise in bond yields led to a decline in bond-linked sectors, with utilities dropping 1.8% as they tend to respond inversely to yield changes. Bond market dynamics have placed added pressure on stocks with bond-like characteristics, such as utilities.

With the Federal Reserve’s upcoming policy meeting, rising Middle East tensions, and the Nov. 5 U.S. elections looming, investors are bracing for volatility in the weeks ahead. The potential for shifts in monetary policy and new geopolitical developments could further influence market performance and investor sentiment.

– Two Publications Recently Issued Featuring OLC and UNI-494 –

LOS ALTOS, Calif., Oct. 28, 2024 (GLOBE NEWSWIRE) — Unicycive Therapeutics, Inc. (Nasdaq: UNCY), a clinical-stage biotechnology company developing therapies for patients with kidney disease (the “Company” or “Unicycive”), today announced that multiple presentations were delivered at the American Society of Nephrology (ASN) Kidney Week 2024 that highlighted the extensive development progress for both oxylanthanum carbonate (OLC) and UNI-494.

“Kidney Week was extremely productive for us featuring a late-breaking presentation on our OLC pivotal trial, and our numerous data presentations were well received by the medical community,” said Shalabh Gupta, MD, Chief Executive Officer of Unicycive. “We were excited to present our positive pivotal clinical trial data demonstrating that OLC enabled adequate control of serum phosphate in more than 90% of patients with chronic kidney disease (CKD) on dialysis who entered the maintenance phase of the trial. OLC preclinical data was also presented at the conference and recently published. This data supports our recently submitted New Drug Application as we seek U.S. Food and Drug Administration (FDA) approval to bring OLC to the millions of CKD patients with hyperphosphatemia on dialysis.”

Dr. Gupta continued, “Earlier this month, we announced the successful competition of our UNI-494 Phase 1 study and were pleased to present the safety and tolerability data at ASN. We plan to request a meeting with the FDA before the end of the year to review these Phase 1 results and a potential Phase 2 study design.”

“For patients with CKD on dialysis, achieving adequate serum phosphate control is critically important because it can lead to other major complications including cardiovascular disease. I am encouraged by the results from the OLC pivotal trial presented at Kidney Week, and I believe that a product like OLC could have a meaningful impact on the overall care of CKD patients on dialysis,” added Dr. Pablo Pergola, MD, PhD, Research Director of the Clinical Advancement Center, PLLC, and a member of Renal Associates PA, San Antonio, Texas.

PUBLICATIONS

In addition to the presentations at ASN, preclinical studies for both OLC and UNI-494 were recently featured in two publications.

“Systemic Absorption of Oxylanthanum Carbonate is Minimal in Preclinical Models” was published in the Pharmaceutical Chemistry Journal.

“Evaluation of UNI-494 in Acute Kidney Injury Treatment Efficacy When Administered After Ischemia-Reperfusion in a Rat Model” was published in EC Pharmacology and Toxicology.

ASN KIDNEY WEEK PRESENTATIONS

Title:

Effects of Oxylanthanum Carbonate in Patients Receiving Maintenance Hemodialysis with Hyperphosphatemia

Lead Author:

Geoffrey A. Block, MD, FASN, Associate Chief Medical Officer & Senior Vice President, Clinical Research & Medical Affairs, U.S. Renal Care

Summary:

This late-breaking poster describes the pivotal Phase 2 open-label, single-arm, multicenter, multidose study in adult patients with CKD with hyperphosphatemia receiving maintenance hemodialysis. The aim of the study was to assess the tolerability and safety of OLC at doses that achieve satisfactory serum phosphate control of ≤5.5 mg/dl. Most patients (69%) who achieved the target serum phosphate did so with ≤1500 mg/day and the percent of patients with serum phosphate ≤5.5 mg/dl increased from 59% at Screening to 91% at the end of titration. OLC was safe and well-tolerated with adverse events commonly seen in this patient population and with other phosphate binders. The use of OLC enabled adequate control of serum phosphate in >90% of patients who entered maintenance.

Title:

Combination Oxylanthanum Carbonate and Tenapanor Lowers Urinary Phosphate Excretion in Rat

This study evaluated the effects of OLC plus tenapanor on urinary phosphate excretion in rats on a high phosphorus diet. The study showed that the combination of OLC and tenapanor may support a pronounced inhibition of intestinal phosphate absorption by leveraging two distinct mechanisms of action: OLC, an intestinal phosphate binder, and tenapanor, a sodium/hydrogen exchanger (NHE3) blocker that diminishes transcellular phosphate absorption. The results demonstrated that the OLC plus tenapanor combination achieved a much more pronounced reduction in urinary phosphate excretion as compared to OLC alone and 3.3 times greater than tenapanor alone. In addition, the OLC plus tenapanor combination exhibited four- to seven-fold more synergistic effects compared to the sevelamer plus tenapanor combination. The study demonstrated potent effects of the novel lanthanum-based phosphate binder OLC and found that OLC plus tenapanor has synergistic, rather than additive, effects in rats.

Title:

UNI-494 Phase I Safety, Tolerability, and Pharmacokinetics

Lead Author:

Guru Reddy, PH.D., Vice President of Preclinical R&D, Unicycive

Summary:

The poster described the results from the single ascending dose (SAD) cohorts from the Phase 1 study evaluating safety, tolerability, and pharmacokinetics (PK) of UNI-494 capsules administered to healthy volunteers. The study was a single-center, double-blind, placebo-controlled, randomized study that enrolled up to 40 subjects in 5 cohorts of 8 subjects each (6 active/2 placebo per cohort). Safety assessments and pharmacokinetics and systemic exposure of UNI-494 and its metabolites (nicorandil and CHEA) were evaluated. The data demonstrated that a single dose of 10-160 mg of UNI-494 capsules were safe and well-tolerated, and that UNI-494 was rapidly converted to nicorandil and the exposure to nicorandil increased in a dose-proportional manner. Therapeutic levels (AUC >200 hour*ng/mL) of nicorandil were achieved at 160 mg of UNI-494. This rapid conversion of UNI-494 to nicorandil and 1-cyclohexylethylamine indicates a potential for a fast-acting therapy for the prevention of Delayed Graft Function (DGF) and other acute kidney injury (AKI) clinical conditions.

Title:

Intravenous UNI-494 Slows the Progression or Halts/Reverses Acute Kidney Injury When Administered After Ischemia/Reperfusion in Rats

The poster presented the results from a study evaluating the in vivo efficacy of intravenous (IV) UNI-494 when administered therapeutically after unilateral renal ischemia-reperfusion (I/R) in a rat model of AKI, which is a well-established model of DGF. The study showed that single IV doses of 10 mg/kg of UNI-494 administered after I/R significantly reduced serum and urinary AKI markers and improved proximal tubular injury scores. Specifically, a single IV dose of 10 mg/kg of UNI-494 improved key kidney functional markers (serum creatinine, blood urea nitrogen, urinary samples collected for albumin-creatinine ratio), the tubular injury marker neutrophil gelatinase-associated lipocalin, and proximal tubular injury scores. These data indicate therapeutic administration of UNI-494 slows down and may even halt or reverse AKI progression.

The posters and publications can be found on the Unicycive Therapeutics website here.

About Oxylanthanum Carbonate (OLC)

Oxylanthanum carbonate is a next-generation lanthanum-based phosphate binding agent utilizing proprietary nanoparticle technology being developed for the treatment of hyperphosphatemia in patients with chronic kidney disease (CKD). OLC has over forty issued and granted patents globally. Its potential best-in-class profile may have meaningful patient adherence benefits over currently available treatment options as it requires a lower pill burden for patients in terms of number and size of pills per dose that are swallowed instead of chewed. Based on a survey conducted in 2022, Nephrologists stated that the greatest unmet need in the treatment of hyperphosphatemia with phosphate binders is a lower pill burden and better patient compliance.1 The global market opportunity for treating hyperphosphatemia is projected to be in excess of $2.5 billion in 2023, with the United States accounting for more than $1 billion of that total. Despite the availability of several FDA-cleared medications, 75 percent of U.S. dialysis patients fail to achieve the target phosphorus levels recommended by published medical guidelines.

Unicycive is seeking FDA approval of OLC via the 505(b)(2) regulatory pathway. As part of the clinical development program, two clinical studies were conducted in over 100 healthy volunteers. The first study was a dose-ranging Phase I study to determine safety and tolerability. The second study was a randomized, open-label, two-way crossover bioequivalence study to establish pharmacodynamic bioequivalence between OLC and Fosrenol. Based on the results of the bioequivalence study, pharmacodynamic (PD) bioequivalence of OLC to Fosrenol was established. A pivotal clinical trial was also conducted in CKD patients on hemodialysis that achieved the study objective and established favorable tolerability of OLC at clinically effective doses.

Fosrenol® is a registered trademark of Shire International Licensing BV. 1Reason Research, LLC 2022 survey. Results here.

About Hyperphosphatemia

Hyperphosphatemia is a serious medical condition that occurs in nearly all patients with End Stage Renal Disease (ESRD). If left untreated, hyperphosphatemia leads to secondary hyperparathyroidism (SHPT), which then results in renal osteodystrophy (a condition similar to osteoporosis and associated with significant bone disease, fractures and bone pain); cardiovascular disease with associated hardening of arteries and atherosclerosis (due to deposition of excess calcium-phosphorus complexes in soft tissue). Importantly, hyperphosphatemia is independently associated with increased mortality for patients with chronic kidney disease on dialysis. Based on available clinical data to date, over 80% of patients show signs of cardiovascular calcification by the time they become dependent on dialysis.

Dialysis patients are already at an increased risk for cardiovascular disease (because of underlying diseases such as diabetes and hypertension), and hyperphosphatemia further exacerbates this. Treatment of hyperphosphatemia is aimed at lowering serum phosphate levels via two means: (1) restricting dietary phosphorus intake; and (2) using, on a daily basis, and with each meal, oral phosphate binding drugs that facilitate fecal elimination of dietary phosphate rather than its absorption from the gastrointestinal tract into the bloodstream.

About UNI-494

UNI-494 is a novel nicotinamide ester derivative and a selective ATP-sensitive mitochondrial potassium channel activator. Mitochondrial dysfunction plays a critical role in the progression of acute kidney injury and chronic kidney disease. UNI-494 has a novel mechanism of action that restores mitochondrial function and may be beneficial for the treatment of several diseases including kidney disease. Unicycive has completed enrollment in the UNI-494 Phase 1 dose-ranging safety study in healthy volunteers in the United Kingdom. UNI-494 is protected by issued patent(s) in the U.S. and Europe and a wide range of patent applications worldwide. UNI-494 has been granted orphan drug designation (ODD) by the U.S. Food and Drug Administration (FDA) for the prevention of Delayed Graft Function (DGF) in kidney transplant patients.

About Acute Kidney Injury

Acute kidney injury (AKI) is defined as a sudden loss of kidney function that is determined based on increased serum creatinine levels and decreased urine output and is limited to a duration of 7 days. The primary causes of AKI include sepsis, ischemia, hypoxia, and drug-induced nephrotoxicity. Delayed Graft Function is a type of acute kidney injury that occurs in the first week after kidney transplantation. AKI is estimated to occur in 20-200 per million population in the community, 7-18% of patients in the hospital, and approximately 50% of patients admitted to the intensive care unit. Importantly AKI is associated with morbidity and mortality; an estimated 2 million people die of AKI worldwide every year whereas survivors of AKI are at increased risk of chronic kidney disease and end stage renal disease.

About Unicycive Therapeutics

Unicycive Therapeutics is a biotechnology company developing novel treatments for kidney diseases. Unicycive’s lead drug candidate, oxylanthanum carbonate (OLC), is a novel investigational phosphate binding agent being developed for the treatment of hyperphosphatemia in chronic kidney disease patients on dialysis. UNI-494 is a patent-protected new chemical entity in clinical development for the treatment of conditions related to acute kidney injury. For more information, please visit Unicycive.com and follow us on LinkedIn, X, and YouTube.

Forward-looking statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified using words such as “anticipate,” “believe,” “forecast,” “estimated” and “intend” or other similar terms or expressions that concern Unicycive’s expectations, strategy, plans or intentions. These forward-looking statements are based on Unicycive’s current expectations and actual results could differ materially. There are several factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, clinical trials involve a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results; our clinical trials may be suspended or discontinued due to unexpected side effects or other safety risks that could preclude approval of our product candidates; risks related to business interruptions, which could seriously harm our financial condition and increase our costs and expenses; dependence on key personnel; substantial competition; uncertainties of patent protection and litigation; dependence upon third parties; and risks related to failure to obtain FDA clearances or approvals and noncompliance with FDA regulations. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including: the uncertainties related to market conditions and other factors described more fully in the section entitled ‘Risk Factors’ in Unicycive’s Annual Report on Form 10-K for the year ended December 31, 2023, and other periodic reports filed with the Securities and Exchange Commission. Any forward-looking statements contained in this press release speak only as of the date hereof, and Unicycive specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise.

Third quarter 2024 total revenue of $613.6 million, net income of $86.3 million, and EBITDA of $170.7 million

Increased oil & gas royalty volumes to 864 MBOE, up 11.9% year-over-year

Completed $10.5 million in oil & gas mineral interest acquisitions

Declares quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized

Increased committed & priced sales tons for the 2025 full year by 5.9 million tons to 22.5 million tons

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the three and nine months ended September 30, 2024 (the “2024 Quarter” and “2024 Period,” respectively). This release includes comparisons of results to the three and nine months ended September 30, 2023 (the “2023 Quarter” and “2023 Period,” respectively) and to the quarter ended June 30, 2024 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.

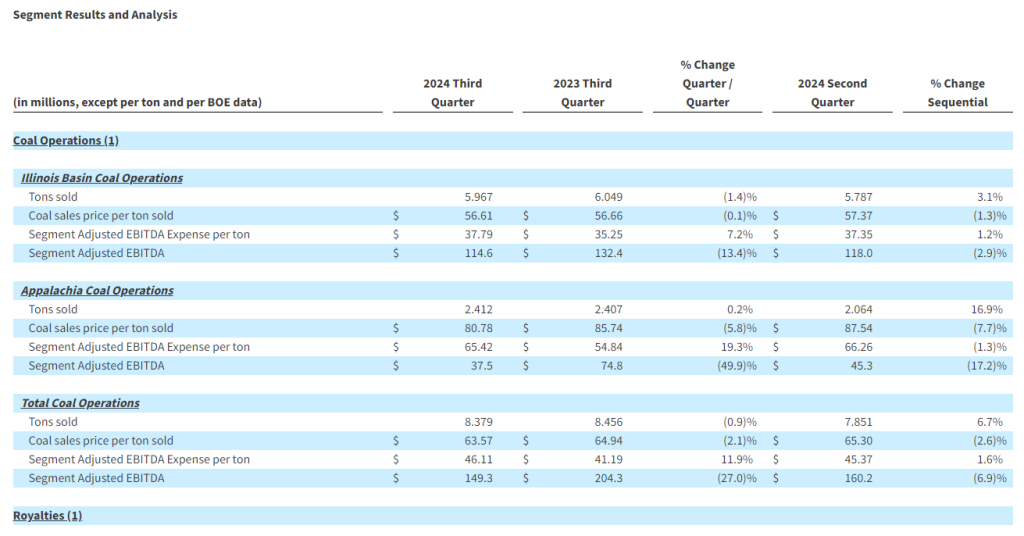

Total revenues in the 2024 Quarter decreased 3.6% to $613.6 million compared to $636.5 million for the 2023 Quarter primarily as a result of reduced coal sales prices, which declined 2.1% due in part to lower export pricing in Appalachia, and lower transportation revenues. Net income for the 2024 Quarter was $86.3 million, or $0.66 per basic and diluted limited partner unit, compared to $153.7 million, or $1.18 per basic and diluted limited partner unit, for the 2023 Quarter as a result of lower revenues and increased total operating expenses. EBITDA for the 2024 Quarter was $170.7 million compared to $227.6 million in the 2023 Quarter.

Total revenues in the 2024 Quarter increased 3.4% compared to $593.4 million in the Sequential Quarter primarily as a result of increased coal sales volumes, which rose 6.7% to 8.4 million tons sold compared to 7.9 million tons sold. Net income and EBITDA for the 2024 Quarter decreased by 13.9% and 3.9%, respectively, compared to the Sequential Quarter as a result of higher total operating expenses, partially offset by increased revenues.

Total revenues decreased 4.3% to $1.86 billion for the 2024 Period compared to $1.94 billion for the 2023 Period primarily due to lower coal sales and transportation revenues, partially offset by higher oil & gas royalties and other revenues. Net income for the 2024 Period was $344.5 million, or $2.64 per basic and diluted limited partner unit, compared to $514.7 million, or $3.93 per basic and diluted limited partner unit, for the 2023 Period as a result of lower revenues and increased total operating expenses, partially offset by an increase in the fair value of our digital assets. EBITDA for the 2024 Period was $583.4 million compared to $747.7 million in the 2023 Period.

CEO Commentary

“We delivered sequential improvement in revenue, coal sales, and minerals volumes during the third quarter, however revenues were lower than our expectations primarily due to lower coal sales volumes and pricing related to export sales from our MC Mining, Mettiki and Hamilton operations, as well as shipping deferrals on some of our higher priced domestic contracted commitments,” commented Joseph W. Craft III, Chairman, President, and CEO. “Segment Adjusted EBITDA Expense per ton sold was $46.11 during the 2024 Quarter, slightly higher than the Sequential Quarter and increasing 11.9% year-over-year due to a longwall move at our Tunnel Ridge operations and challenging mining conditions at all three Appalachia operations that lowered recoveries and increased costs related to roof control and maintenance. We took proactive steps during the 2024 Quarter to more closely align production with shipments at our MC Mining, Mettiki and Hamilton operations by reducing production due to high stockpile levels at each operation which also impacted our costs. As a result, coal inventory levels declined by over 0.5 million tons in the 2024 Quarter.”

Mr. Craft added, “We are pleased to report that all of the major capital and mine infrastructure projects we have been investing in over the last several years are wrapping up and are projected to be on schedule to deliver lower mining expenses beginning next year.”

Mr. Craft concluded, “We realized another solid quarter of year-over-year volumetric growth in our Oil & Gas Royalties business. We continue to reap the benefits of a minerals portfolio that is heavily weighted towards the Permian Basin, where top-tier upstream operators are actively drilling and completing new wells on our mineral acreage. Additionally, we continued to add to our position in the Permian, successfully closing $10.5 million of ground game acquisitions during the 2024 Quarter. As we have mentioned previously, we believe the value and prospects for our oil and gas royalty segment was a major contributor to the success of our Senior Notes offering earlier this year. We remain committed to growing this segment as a complement to our core coal operations, and as we scale the business, we believe investors will continue to recognize the intrinsic value the segment possesses as a growth vehicle.”

Coal Operations

Total coal sales volumes for the 2024 Quarter increased 6.7% compared to the Sequential Quarter while remaining relatively consistent compared to the 2023 Quarter. Sequentially, tons sold increased by 3.1% in the Illinois Basin due to higher sales volumes from our River View and Hamilton mines. In Appalachia, tons sold increased by 16.9% in the 2024 Quarter compared to the Sequential Quarter primarily due to improved conditions on the Ohio River allowing for higher shipments from our Tunnel Ridge operation. Coal sales price per ton decreased by 5.8% in Appalachia compared to the 2023 Quarter as a result of reduced export price realizations from our Mettiki and MC Mining operations. Compared to the Sequential Quarter, coal sales prices decreased by 7.7% in Appalachia primarily due to reduced domestic price realizations across the region. ARLP ended the 2024 Quarter with total coal inventory of 2.0 million tons, representing an increase of 0.2 million tons and a decrease of 0.5 million tons compared to the end of the 2023 Quarter and Sequential Quarter, respectively.

Segment Adjusted EBITDA Expense per ton for the 2024 Quarter increased by 7.2% in the Illinois Basin compared to the 2023 Quarter due primarily to reduced production and higher beginning inventory cost per ton at our Hamilton and River View mines. Increased expenses and lower production at our Hamilton mine during the 2024 Quarter was partially attributable to increased longwall move days compared to the 2023 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton for the 2024 Quarter increased by 19.3% compared to the 2023 Quarter due to a longwall move at our Tunnel Ridge operation, increased subsidence related expenses and challenging mining conditions at all three operations that lowered recoveries, and increased costs related to roof control and maintenance.

Royalties

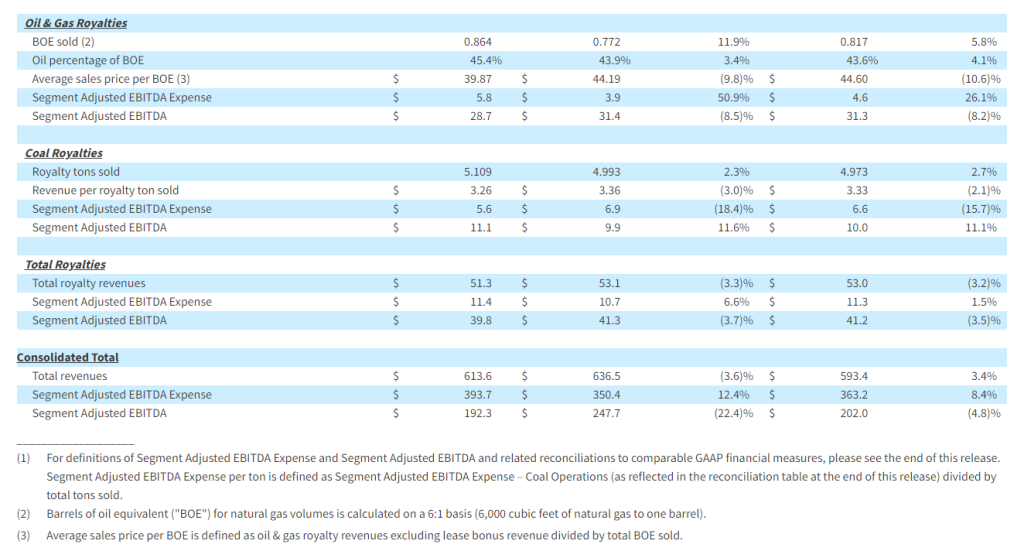

Oil & gas volumes increased to 864 MBOE in the 2024 Quarter, representing an 11.9% and a 5.8% increase compared to the 2023 Quarter and Sequential Quarter, respectively, due to increased drilling and completion activities on our interests and acquisitions of additional oil & gas mineral interests. Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased 8.5% and 8.2% in the 2024 Quarter compared to the 2023 Quarter and Sequential Quarter, respectively, primarily due to reduced average realized sales prices per BOE.

Segment Adjusted EBITDA for the Coal Royalties segment in the 2024 Quarter increased by $1.2 million and $1.1 million compared to the 2023 Quarter and Sequential Quarter, respectively, as a result of increased royalty tons sold and reduced expenses, partially offset by reduced prices.

Balance Sheet and Liquidity

As of September 30, 2024, total debt and finance leases outstanding were $497.4 million, including $400 million in recently issued Senior Notes due 2029. The Partnership’s total and net leverage ratios were 0.64 times and 0.39 times debt to trailing twelve months Adjusted EBITDA, respectively, as of September 30, 2024. ARLP ended the 2024 Quarter with total liquidity of $657.7 million, which included $195.4 million of cash and cash equivalents and $462.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

ARLP is also announcing today that the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2024 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on November 14, 2024, to all unitholders of record as of the close of trading on November 7, 2024. The announced distribution is consistent with the cash distributions for the 2023 Quarter and Sequential Quarter.

Outlook

“We have repeatedly warned about the impact of federal regulations on grid reliability, influencing what we believe to be the premature retirement of essential baseload power sources even as significant demand growth from AI, data centers, and manufacturing onshoring is being projected,” commented Mr. Craft. “This summer’s PJM capacity auction results highlight these concerns. Recognizing a potential crisis due to unexpectedly high demand growth, the delayed construction of new generation, and planned capacity retirements, particularly in our served markets, PJM prioritized baseload capacity over interruptible sources. This further supports recent third-party sources which indicate that greater than 40% of previously announced baseload power plant retirement dates have been deferred nationwide.”

Mr. Craft concluded, “Many of our largest domestic customers have been active on the contracting side of late. Since our last update, we are in the process of finalizing commitments for 21.7 million tons over the 2025 to 2030 time period. We are also in active discussions with other customers to add to future commitments, that if secured, will lift our 2025 domestic sales order book to a level near our historical contracted position heading into the new calendar year. Looking longer-term, the underlying coal demand fundamentals of non-traditional demand growth is accelerating, particularly in the markets we serve in the Midwest, Mid-Atlantic, and Southeast.”

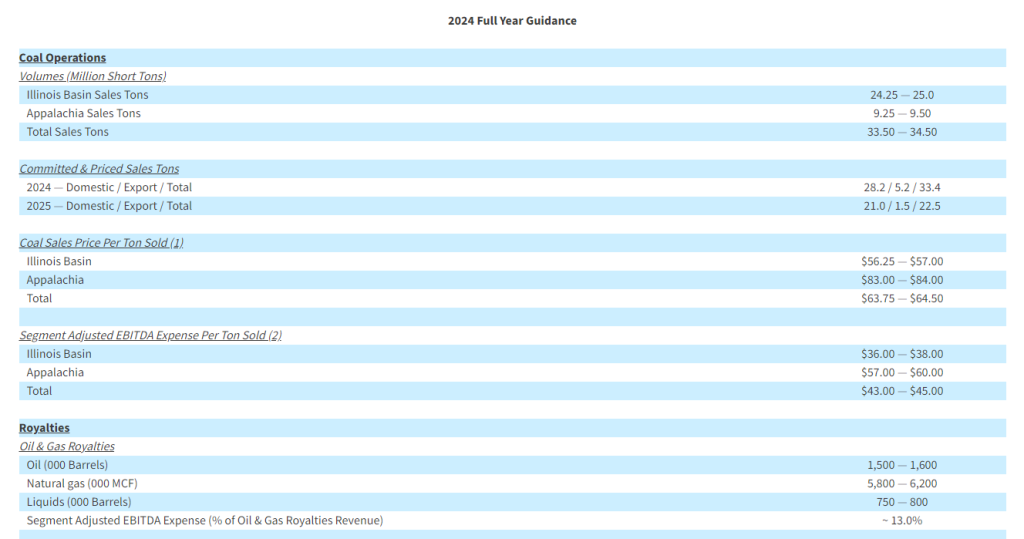

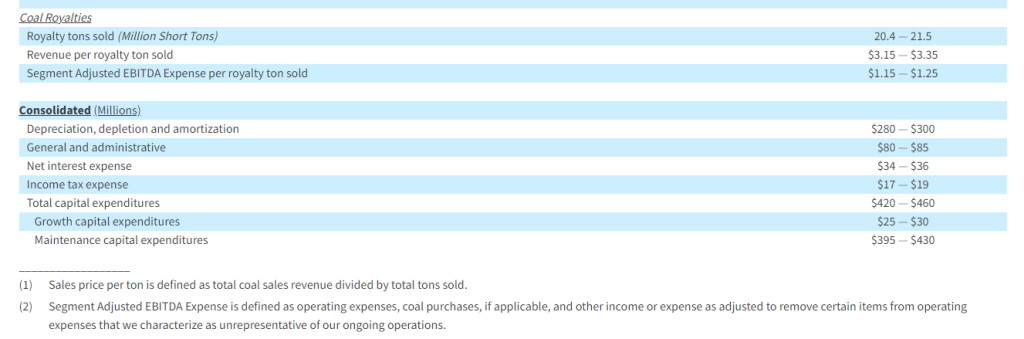

ARLP is maintaining the following guidance for the full year ended December 31, 2024 (the “2024 Full Year”) and updating our committed and priced sales tons:

Conference Call

A conference call regarding ARLP’s 2024 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13749425.

Concurrent with this announcement we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, infrastructure projects at our existing properties, growth in domestic electricity demand, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; our ability to provide fuel for growth in domestic energy demand, should it materialize; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers and operators, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by the operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of and investments into the infrastructure of our operations and properties, including the timing of such investments coming online; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, and the results of central bank policy actions, including interest rates, bank failures, and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, such as the Environmental Protection Agency’s recently promulgated emissions regulations for coal-fired power plants, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2023, filed on February 23, 2024,and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2024 and June 30, 2024, filed on May 9, 2024 and August 7, 2024, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Progress on OCU400 Phase 3 liMeliGhT clinical trial for retinitis pigmentosa (RP) and new data from Phase 1/2

Preliminary safety and efficacy update on OCU410 Phase 1/2 ArMaDa clinical trial for geographic atrophy (GA)

Clinical update on OCU410ST Phase 1/2 GARDian clinical trial for Stargardt disease

Featuring patients, investigators and thought leaders

MALVERN, Pa., Oct. 28, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced that it will host an in-person Clinical Showcase on Tuesday, November 12, 2024. The event will take place from 10 a.m.-noon ET at the Nasdaq MarketSite in Times Square, New York City.

The event will focus on encouraging updates from Ocugen’s ongoing gene therapy trials, including:

Clinical update on Phase 3 liMeliGhT clinical trial for retinitis pigmentosa along with data updates from Phase 1/2 RP and Leber congenital amaurosis (LCA)

Preliminary safety and efficacy data from Phase 1/2 OCU410 ArMaDa clinical trial for GA

Clinical trial progress from Phase 1/2 OCU410ST GARDian study for Stargardt disease

In addition, background on Ocugen’s biologic candidate, OCU200 for diabetic macular edema, will be presented. The Company is planning to initiate the OCU200 Phase I clinical trial this quarter.

Ocugen presenters will include:

Dr. Shankar Musunuri, Chairman, CEO & Co-founder

Dr. Huma Qamar, Chief Medical Officer

Dr. Arun Upadhyay, Chief Scientific Officer & Head of R&D

Mike Shine, Senior Vice President, Commercial

Joining the Ocugen team will be study investigators:

Dr. Benjamin Bakall, Director of Clinical Research at Associated Retina Consultants (ARC) and Clinical Assistant Professor at University of Arizona, College of Medicine – Phoenix

Dr. Lejla Vajzovic, Professor of Ophthalmology, Pediatrics, and Biomedical Engineering with Tenure at Duke Eye Center and Duke University School of Medicine

Dr. Syed M. Shah, Vice Chair for Research and Digital Health, Director of Retina Service at Gundersen Health – La Crosse, Wisconsin

The program will conclude with a patient panel representing participants in Ocugen’s ongoing clinical trials.

Advance registration is required and can be done by contacting Tiffany Hamilton at Tiffany.Hamilton@ocugen.com.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, including, but not limited to, strategy, business plans and objectives for Ocugen’s clinical programs, plans and timelines for the preclinical and clinical development of Ocugen’s product candidates, including the therapeutic potential, clinical benefits and safety thereof, expectations regarding timing, success and data announcements of current ongoing preclinical and clinical trials, the ability to initiate new clinical programs; statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including, but not limited to, the risks that preliminary, interim and top-line clinical trial results may not be indicative of, and may differ from, final clinical data; that unfavorable new clinical trial data may emerge in ongoing clinical trials or through further analyses of existing clinical trial data; that earlier non-clinical and clinical data and testing of may not be predictive of the results or success of later clinical trials; and that that clinical trial data are subject to differing interpretations and assessments, including by regulatory authorities. These and other risks and uncertainties are more fully described in our annual and periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

CHICAGO, Oct. 28, 2024 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today announced that it will release its third quarter 2024 financial results on Tuesday, November 12, 2024 before the market opens.

The conference call and live webcast will be held on Tuesday, November 12 at 11:00 a.m. (ET), and will be available on the Investor Relations page of the Company’s website at https://viavid.webcasts.com/starthere.jsp?ei=1693396&tp_key=feca4932b6 or by dialing (877) 407-0789 or (201) 689-8562. It is recommended that listeners log on or dial in approximately 10 to 15 minutes prior to the start of the call.

An audio replay of the conference call will be available shortly after the call has ended on the Company’s Investor Relations website until November 26, 2024.

About FreightCar America

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

SAN DIEGO, Oct. 28, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the third quarter 2024 after the close of market on Thursday, November 7th. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Key Points: – AbbVie acquires Aliada Therapeutics, adding ALIA-1758 and its unique drug-delivery platform. – Expands AbbVie’s neuroscience pipeline with advanced Alzheimer’s treatments. – Aliada’s MODEL platform enhances drug delivery across the blood-brain barrier.

AbbVie has strategically bolstered its Alzheimer’s portfolio by acquiring Boston-based Aliada Therapeutics in a deal valued at $1.4 billion. The acquisition brings AbbVie ALIA-1758, a Phase I anti-amyloid antibody targeting Alzheimer’s disease, along with Aliada’s novel Modular Delivery (MODEL) platform. This technology aims to improve the delivery of therapeutics across the blood-brain barrier (BBB), a significant challenge in developing drugs for the central nervous system.

With Alzheimer’s becoming a critical area for biotech and pharma innovation, AbbVie’s acquisition comes amid heightened interest in anti-amyloid therapies. The recent successes of Biogen and Eisai’s Leqembi and Eli Lilly’s Kisunla, the first FDA-approved disease-modifying treatments for Alzheimer’s, have demonstrated the potential of anti-amyloid treatments, though they come with risks. ALIA-1758 is designed to target pyroglutamate amyloid beta, an epitope similar to that in Kisunla, and leverages Aliada’s MODEL platform to improve therapeutic delivery.

The MODEL platform is engineered to transport therapeutic agents across the BBB by targeting transferrin and CD98 receptors, both of which are abundantly expressed in brain endothelial cells. The technology effectively carries antibodies across the BBB, allowing higher therapeutic concentrations in the brain to address amyloid plaques associated with Alzheimer’s. This targeted approach has the potential to provide superior treatment efficacy compared to previous approaches.

This acquisition aligns with AbbVie’s strategy of expanding its presence in neuroscience. The company already has a robust portfolio that includes experimental therapies like ABBV-916, another anti-amyloid antibody; ABBV-552, which targets nerve terminals to enhance synaptic function; and AL002, an antibody developed in partnership with Alector Therapeutics. With the addition of ALIA-1758, AbbVie strengthens its position in the field and continues to invest in innovation that could transform the treatment landscape for neurodegenerative diseases.

While the Alzheimer’s market is promising, AbbVie’s expansion comes with some caution. Analysts have noted that investor sentiment in anti-amyloid drugs is mixed, given the high cost and developmental challenges. However, AbbVie’s investment signals confidence in the MODEL platform’s potential to enhance drug delivery, particularly in addressing diseases with significant unmet needs like Alzheimer’s. AbbVie is optimistic that Aliada’s technology will complement its existing assets and support long-term growth in the neuroscience sector.

Expected to close by the end of 2024, the acquisition of Aliada Therapeutics is subject to regulatory approvals and standard closing conditions. The deal underscores AbbVie’s ongoing commitment to innovation and its mission to bring novel treatments to patients suffering from Alzheimer’s and other neurological disorders.

Key Points: – DJT shares soar on investor optimism around Trump’s 2024 election chances. – Rally at Madison Square Garden and support from figures like Elon Musk bolster stock. – While stock rises, Trump Media’s underlying financial challenges could impact long-term performance.

Donald Trump’s Trump Media & Technology Group (DJT) stock has seen a surge following his rally at Madison Square Garden, as market excitement and the election’s proximity drive interest. Over the weekend, DJT shares rose by as much as 20%, boosted by investor anticipation surrounding the former president’s election chances. The stock now trades at its highest point since July, marking a substantial 235% increase from September’s lows.

This surge wasn’t limited to DJT stock alone. Related companies like Phunware (PHUN), which provides mobile advertising services connected to Trump, and conservative video platform Rumble (RUM) also experienced gains of over 3% and 6%, respectively. Market analysts suggest that DJT’s stock performance hinges largely on the election, making it highly volatile in the face of public opinion shifts.

Investors betting on DJT stock see the upcoming election as a major catalyst. If Trump wins, the stock is likely to benefit from positive sentiment and speculation around Truth Social, his social media platform under Trump Media & Technology. Trump’s recent rally, while controversial, has further stoked investor sentiment as prediction markets shift more favorably towards his presidential bid. Betting markets, such as PredictIt and Kalshi, have shown Trump gaining ground against Democratic nominee Kamala Harris, adding to the optimism fueling DJT’s stock momentum.

However, experts warn of potential volatility. With a highly polarized market reaction to Trump’s campaign, a loss in the election could drive DJT’s stock down dramatically. Investment fund CEO Matthew Tuttle, who currently holds put options on DJT stock, predicts that a Trump loss could send the stock’s value tumbling to zero. Analysts advise caution, citing a “buy the rumor, sell the fact” approach for DJT stock tied to the November results.

The uptick in DJT’s value comes after a volatile period that included a drop in share price following the end of a lockup period for some early investors. Trump’s presence on Truth Social, which he launched post-2021 after being removed from traditional platforms, has continued to fuel speculation on the stock. Elon Musk, a known supporter of Trump, attended Trump’s rally alongside other influential figures, creating a spectacle that resonated with supporters and media alike. Trump and Musk’s association has generated media buzz, with Trump even suggesting a potential cabinet position for Musk, though the Tesla CEO’s involvement remains unofficial.

Despite recent stock performance, Trump Media’s fundamentals raise concerns. For the quarter ending June 30, DJT reported a $16.4 million net loss, with revenue down 30% year-over-year to $837,000. Half of these losses were linked to expenses associated with the company’s SPAC (Special Purpose Acquisition Company) deal. DJT also disclosed earlier in the month that its COO had stepped down in September, indicating potential instability within its management team.

As Trump Media gains attention in the market, its financial landscape remains a key factor for investors who are looking beyond the election.

Key Points: – Chinese autonomous vehicle company WeRide raised $440.5 million through a U.S. IPO and private placement. – WeRide is valued at over $4 billion and begins trading on the Nasdaq, signaling improved investor sentiment in Chinese tech IPOs. – The autonomous driving sector faces challenges, particularly in robotaxi safety and regulatory barriers.

WeRide, a prominent Chinese self-driving technology company, has successfully raised a combined $440.5 million through its initial public offering (IPO) in the United States and a private placement. The Guangzhou-based firm sold 7.74 million American Depositary Shares (ADS) at $15.50 each, reaching the lower end of its targeted range and securing roughly $120 million from the IPO. In addition, WeRide raised $320.5 million through a concurrent private placement, valuing the company at over $4 billion. Trading on the Nasdaq is expected to start later today, marking a significant milestone for WeRide and a notable increase in Chinese company IPO activity on American exchanges.

The interest in U.S.-listed Chinese IPOs has seen a resurgence after years of regulatory uncertainty that culminated in the delisting of ride-hailing giant Didi Global following scrutiny by Chinese regulators. Recent easing of regulatory barriers by Beijing, paired with a resolution on audit access between the U.S. and China in 2022, has allowed for renewed activity. The reopening of the U.S. IPO market has also been welcomed by tech startups that faced a downturn over the past two years due to cash burn concerns and volatile valuations. With investor sentiment improving, WeRide’s successful listing follows the IPO of EV manufacturer Zeekr earlier in the year and could pave the way for additional Chinese tech companies to pursue U.S. listings. Autonomous vehicle firm Pony AI, backed by Toyota, is one such company with its Nasdaq filing earlier this month.

WeRide’s operations include testing and commercial trials of autonomous taxis, buses, vans, and street sweepers across 30 cities in seven countries. As robotaxi technology continues to evolve, analysts note that establishing widespread autonomous taxi services may still require years of technological refinement to meet safety and reliability standards. Accidents involving autonomous vehicles remain a primary concern, as challenges such as adverse weather, complex intersections, and unexpected pedestrian behavior still pose obstacles to self-driving technology. Despite these hurdles, China has taken a more proactive stance on authorizing self-driving trials compared to the U.S., allowing firms like WeRide greater flexibility for experimentation and commercialization within their domestic market.

WeRide’s expansion into the U.S. market, however, may be influenced by a proposed regulation from the Biden administration that seeks to limit Chinese software and hardware in American-connected and autonomous vehicles due to national security concerns. Such regulatory measures may shape the future landscape of cross-border collaboration in autonomous technology. However, companies remain optimistic that continued advancements in the sector will transform urban transportation. Notably, Tesla has recently revealed its own robotaxi and robovan concept as the competition within the EV and autonomous vehicle industries intensifies.

The underwriters for WeRide’s IPO include major players Morgan Stanley, J.P. Morgan, and China International Capital Corp. With proceeds potentially reaching $458.5 million if underwriters exercise options for additional shares, WeRide’s public listing aims to bolster its financial base for continued development and expansion, setting it on a path toward establishing a robust presence in the global autonomous driving market.

Key Points: – Nvidia’s stock reached a market value of $3.53 trillion, overtaking Apple’s $3.52 trillion temporarily. – AI-driven demand has significantly boosted Nvidia’s stock, leading to an 18% increase in October alone. – The company remains a leader in AI chip production, benefiting from strong market optimism for artificial intelligence applications.

The rally in Nvidia’s stock underscores the growing dominance of tech firms in financial markets, especially companies that drive the AI sector. For several months, Nvidia, Apple, and Microsoft have held the top spots in market capitalization, reflecting their massive influence on Wall Street.

Following a record year driven by its specialized processors, Nvidia has become indispensable for companies investing in AI computing power. The firm’s AI processors, essential for complex computing tasks, have cemented Nvidia’s status as a key player in the competitive race to shape the future of artificial intelligence. The company’s market trajectory gained momentum in recent weeks after OpenAI, developer of the popular ChatGPT, announced a significant funding round of $6.6 billion. This news fueled optimism for Nvidia as its AI-related products are essential to the operations of companies like Microsoft, Alphabet, and Meta, who are vying for AI dominance.

The semiconductor market experienced a broader lift this week after chipmaker Western Digital reported better-than-expected quarterly earnings. This optimism added to Nvidia’s upswing, especially as companies look to integrate AI into their workflows.

Nvidia, a company known initially for its graphic processing units (GPUs) for gaming, has effectively transformed its focus to capitalize on the AI wave. The company’s shares climbed roughly 18% this October, following a record-breaking year-to-date performance. The firm has set a high bar with projections of nearly 82% year-over-year revenue growth, significantly outpacing the 5.5% projected growth for Apple, which faces headwinds in China, where iPhone sales dropped by 0.3% last quarter.

The AI boom has also made Nvidia a top choice for options traders, with its stock among the most actively traded. Nvidia’s price surge, nearly 190% year-to-date, demonstrates the confidence in AI’s potential for reshaping industries. However, some analysts, like Rick Meckler of Cherry Lane Investments, caution that while Nvidia’s financials are strong, long-term growth in the AI space may need to prove itself beyond current enthusiasm.

Meanwhile, Apple continues to face mixed projections. Analysts forecast the tech giant’s quarterly revenue to reach $94.5 billion, which, although solid, reflects slower growth than Nvidia’s. Apple’s challenges, including stiffer competition in international markets from brands like Huawei, underscore the shifting landscape. Nonetheless, both Nvidia and Apple, along with Microsoft, account for about 20% of the S&P 500 index, underscoring the tech sector’s influence on broader U.S. markets.

As AI investments surge and technology companies cement their place at the forefront of the market, Nvidia’s recent ascent highlights the rapidly changing dynamics of tech valuation. Investors are keeping a close watch on whether Nvidia can sustain its growth trajectory, particularly as new earnings data, interest rate changes, and evolving AI applications continue to impact the financial landscape.

LAKE ZURICH, Ill–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on December 11, 2024, to stockholders of record as of the close of business on November 15, 2024.

“This is the Company’s 28 th quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy, and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an approximate 6% yield on their investment,” said Tom Tedford, President, and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn and play. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Chris McGinnis Investor Relations (847) 796-4320

Kori Reed Media Relations (224) 501-0406Source: ACCO Brands Corporation

Key Points: – Ingram Micro’s shares jumped 15% in its NYSE debut, pushing the company’s valuation to $6 billion. – The IPO raised $409.2 million, with shares priced at $22, exceeding market expectations as they opened at $25.28. – Ingram is investing heavily in cloud services and digital transformation, positioning itself for growth as AI-driven consumer electronics expand.

Ingram Micro, one of the world’s largest technology distributors, made a strong return to public markets on Thursday, achieving a valuation of $6 billion after its shares surged 15% on the New York Stock Exchange (NYSE). The company’s shares opened for trading at $25.28 apiece, exceeding the initial public offering (IPO) price of $22 per share. This solid market debut signals strong investor demand, marking a successful IPO for Ingram and its private-equity owner, Platinum Equity.

The IPO raised $409.2 million through the sale of 18.6 million shares, valuing Ingram at $5.18 billion at the time of pricing. The offering priced within the targeted range of $20 to $23 per share, reflecting investor confidence as U.S. stock markets continue to hover near record highs. Analysts believe the positive investor sentiment, coupled with the easing of election-related uncertainties and potential interest rate cuts next year, will encourage more companies to move forward with IPOs in the coming months.

Ingram Micro is well-positioned to capitalize on the anticipated global upgrade cycle in consumer electronics, driven by increasing demand for artificial intelligence (AI) features in a wide range of products, from smartphones to household appliances. The company distributes a broad portfolio of IT products, including Apple’s iPhone, Cisco’s network equipment, and solutions from big-tech giants like Microsoft and Nvidia.

Paul Bay, Ingram Micro’s CEO, emphasized the company’s forward-looking strategy in an interview with Reuters. “One of those things we’ve done, and we continue to do under Platinum … is investing ahead of the curve,” Bay said. He highlighted that Ingram has invested over $600 million into its cloud business, accelerating its focus on advanced solutions, specialty services, and digital capabilities.

The company’s history has seen several ownership changes. Ingram originally went public in 1996 and traded on the NYSE until 2016, when it was acquired by Chinese conglomerate HNA Group for $6 billion. Platinum Equity purchased Ingram Micro in a $7.2 billion deal in 2020, and it remains the company’s controlling shareholder. With this IPO, Ingram returns to the public market under the ownership of Platinum Equity, benefiting from its support and resources while continuing to grow in key technology segments.

The offering was managed by a syndicate of major Wall Street investment banks, reflecting the high-profile nature of Ingram’s return to the NYSE. As the company continues to expand its cloud business and build out digital competencies, investors appear confident in its ability to maintain its leadership in the technology distribution sector.

Ingram Micro’s strong debut on the stock exchange showcases both its current market strength and the optimistic outlook investors have for the tech sector, especially as AI integration becomes increasingly prevalent across consumer electronics. The company’s continued focus on innovation and strategic investments should position it well for future growth in a rapidly evolving industry.

LOS ANGELES, Oct. 23, 2024 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 13 other restaurant concepts, today announced that the Company will host a conference call to review its third quarter 2024 financial results on Wednesday, October 30, 2024 at 5:00 PM ET. A press release with third quarter 2024 financial results will be issued prior to the conference call that day.

The conference call can be accessed live over the phone by dialing 1-877-704-4453 from the U.S. or 1-201-389-0920 internationally. A replay will be available after the call until Wednesday, November 20, 2024, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 13748855. Hosting the call will be Andy Wiederhorn, Chairman, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call will also be webcast live from the corporate website at www.fatbrands.com, under the “Investors” section. A replay of the webcast will be available through the corporate website shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.