Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

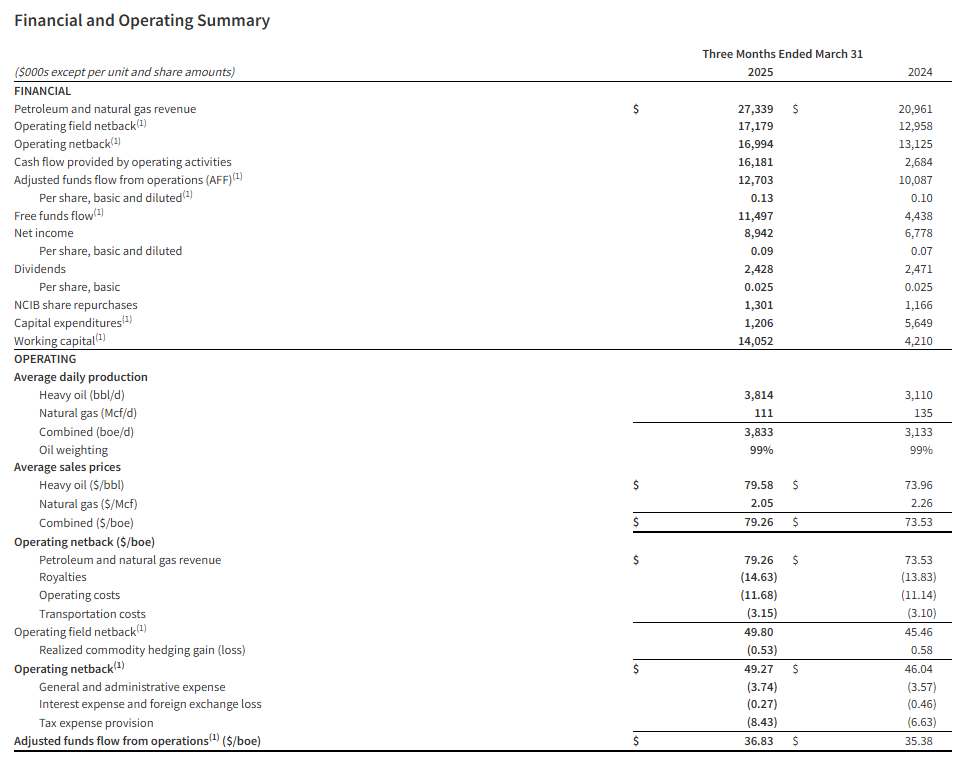

First quarter financial results. Hemisphere generated first quarter oil and gas revenue of C$27.3 million, an increase of 30.4% year-over-year, and above our estimate of C$24.4 million. Net income amounted to C$8.9 million or C$0.09 per share compared to C$6.8 million or C$0.07 per share during the prior year period and our estimates of C$8.2 million or C$0.08 per share. The strong earnings were reflective of a 22.3% year-over-year increase in production to 3,833 barrels of oil equivalent per day (boe/d) from 3,133 boe/d, along with better-than-expected commodity pricing due to the company’s strategic hedging. Adjusted funds flow (AFF) amounted to C$12.7 million or C$0.13 per diluted share compared to C$10.1 million or C$0.10 per diluted share during the prior year period. We had forecasted AFF of C$11.2 million.

Updating estimates. Based on first quarter results and management’s production guidance of 3,800 boe/d for the second quarter, we are raising our 2025 revenue estimates to C$98.2 million from C$94.8 million. We have modestly increased our operating expense estimate to C$38.4 million from C$37.6 million. Additionally, we are raising our net income and earnings per share (EPS) estimates to C$31.3 million and C$0.30, from C$30.3 million and C$0.29. We expect full year 2025 AFF of C$44.7 million, up from our previous estimate of C$43.0 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – May 22, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the first quarter ended March 31, 2025, declares a quarterly dividend payment to shareholders, renews credit facility, and provides operations update.

Q1 2025 Highlights

Attained record quarterly production of 3,833 boe/d (99% heavy oil), a 21% increase over the same period of last year.

Generated $27.3 million in revenue, a 30% increase over the first quarter of 2024.

Achieved total operating and transportation costs of $14.63/boe.

Delivered an operating netback1 of $17.0 million, or $49.27/boe.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $12.7 million, or $36.83/boe, a 26% increase over the first quarter of 2024.

Generated free funds flow1 of $11.5 million, or $0.12 per share.

Distributed $2.4 million, or $0.025 per share, in dividends to shareholders during the quarter.

Purchased and cancelled 709,700 shares for $1.3 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Exited the first quarter with positive working capital1 of $14.1 million, compared to $4.2 million at the end of March 2024.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditure, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited condensed interim consolidated financial statements and related notes, and the Management’s Discussion and Analysis for the three months ended March 31, 2025 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on June 30, 2025 to shareholders of record as of the close of business on June 19, 2025. The dividend is designated as an eligible dividend for income tax purposes.

Including Hemisphere’s special dividend of $0.03 per common share paid in April and base quarterly dividends of $0.025 per common share in February and June, Hemisphere will have paid its shareholders $0.08 per common share in dividends during the first half of 2025.

Credit Facility

The Company has completed its annual bank review and renewed its $35.0 million two-year extendible credit facility with the same key terms, and the next annual review date set for May 31, 2026.

Operations Update

With the majority of Hemisphere’s 2025 capital spending scheduled for the latter half of the year, the Company generated $11.5 million in free funds flow during the first quarter. Current second quarter production of approximately 3,800 boe/d (99% heavy oil, field estimates between April 1 – May 15, 2025) is consistent with that of the first quarter, and represents an increase of 13% over fourth quarter production of 3,359 boe/d (99% heavy oil), due both to downtime in November and continued injection support from Hemisphere’s polymer floods at its Atlee Buffalo projects in southeast Alberta.

At Hemisphere’s Marsden pilot polymer flood project, injection continues to repressure the reservoir. Management anticipates that polymer response could take until late 2025, at which time the Company will determine economics of further development.

Management continues to closely monitor the volatility of the oil market and will adjust capital spending accordingly. With over $14 million in working capital and an undrawn credit line, Hemisphere will prioritize shareholder returns, share buybacks, and potential acquisition activity over accelerated capital spending.

Annual General and Special Meeting of Shareholders

Hemisphere’s Annual General and Special Meeting of Shareholders will be held at 10:00 am (Pacific Daylight Time) on June 2, 2025 in the Walker Room of the Terminal City Club located at 837 West Hastings Street, Vancouver, British Columbia.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor webinar. Century Lithium recently discussed the Angel Island Lithium project during an insightful investor webinar. Key highlights included: 1) Angel Island is an advanced project with one of the largest lithium deposits in the United States, 2) the project employs a proven patent-pending process for chloride leaching, along with direct lithium extraction to produce lithium carbonate, 3) Century has a secured a 1,770 acre-feet per year water rights permit, and 4) the company has demonstrated its ability to consistently produce battery grade lithium carbonate on-site at its pilot plant in Amargosa Valley, Nevada.

Nearing completion of a Plan of Operations. Management expects to submit a Plan of Operations to the Bureau of Land Management within the next few months, which would enable the company to initiate the National Environmental Policy Act (NEPA) permitting process. We anticipate the NEPA permitting process could take between 12 and 24 months, depending on whether an environmental assessment or environmental impact statement is required. An environmental impact statement generally takes longer.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

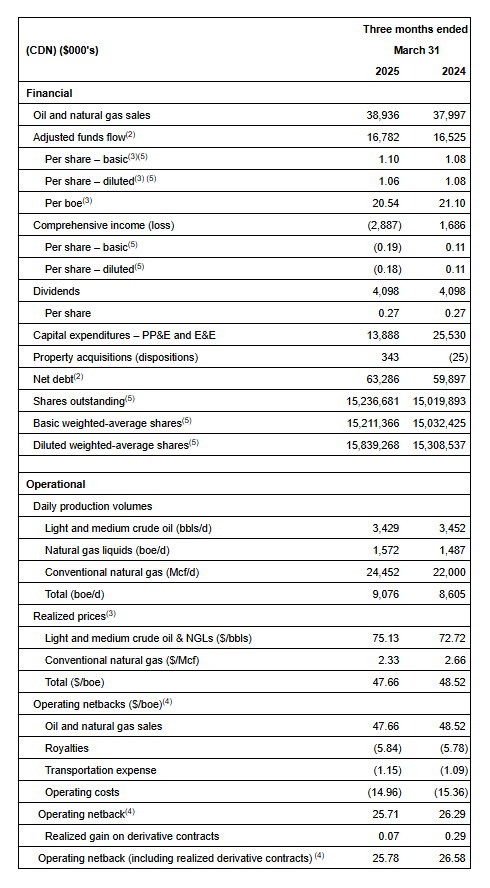

First quarter financial results. InPlay Oil reported a first quarter net loss of C$2.9 million or C$0.18 per share compared to net income of C$1.7 million or C$0.02 per share during the prior year period. This was below our net income estimate of C$4.2 million or C$0.15 per share, primarily due to an unrealized loss on derivative contracts of C$4.6 million and higher-than-expected expenses. Moreover, commodity prices declined slightly during the first quarter, leading to lower revenues of C$38.4 million compared to our estimate of C$40.4 million.

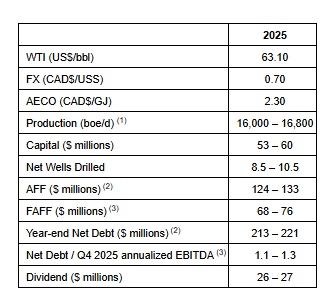

Corporate 2025 guidance. The company generated quarterly production of 9,076 barrels of oil equivalent per day (boe/d), a 5% increase year-over-year and above our expectations of 8,800 boe/d. The company is raising its estimated field production expectations to 21,500 boe/d, a marked increase from 18,750 boe/d, and expects 2025 full year production to be in the range of 16,000 to 16,800 boe/d. Revenue guidance has been adjusted downward to C$46.75 to C$51.75 boe/d from C$56.50 to C$61.50 boe/d. Adjusted funds flow is expected to be between C$124 million and C$133 million, down from $204 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, May 8, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces its financial and operating results for the three months ended March 31, 2025 and an updated 2025 capital budget following the successful completion of the strategic acquisition of Cardium light oil focused assets (the “Acquired Assets“) in the Pembina area of Alberta (the “Acquisition“) from Obsidian Energy Ltd. And certain of its affiliates (collectively “Obsidian“). InPlay’s condensed unaudited interim financial statements and notes, as well as Management’s Discussion and Analysis (“MD&A”) for the three months ended March 31, 2025 will be available at “www.sedarplus.ca” and on our website at “www.inplayoil.com“. All figures presented herein reflect the Company’s six (6) to one (1) share consolidation, which was effective April 14, 2025. An updated corporate presentation will be available on our website shortly.

First Quarter 2025 Highlights

Achieved average quarterly production of 9,076 boe/d(1) (55% light crude oil and NGLs), a 5% increase over Q1 2024 and ahead of internal forecasts.

Generated strong quarterly Adjusted Funds Flow (“AFF”)(2) of $16.8 million ($1.10 per basic share(3)).

Returned $4.1 million to shareholders by way of monthly dividends, equating to a 16% yield relative to the current share price. Since November 2022 InPlay has distributed $44 million in dividends including dividends declared to date.

Maintained a strong operating income profit margin(3) of 54%.

Improved field operating netbacks(3) to $25.71/boe, an increase of 3% compared to Q4 2024.

First quarter results exceeded expectations, driven in part by the outperformance of newly drilled wells at Pembina Cardium Unit #7 (PCU#7). A two well pad delivered average initial production (“IP”) rates of 677 boe/d (75% light oil and NGLs) over the first 30 days and 492 boe/d (66% light oil and NGLs) over the first 60 days, both significantly above expectations. Over the initial two-month period, production from these wells was more than 100% above our type curve. These wells ranked in the top-ten for production rates for all Cardium wells in the basin for the month of March.

Complementing InPlay’s strong operational momentum, Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which started production mid quarter, are outperforming our internal type curve by approximately 50% with average IP rates of 304 boe/d (91% light oil and NGLs) over the first 30 days and 295 boe/d (85% light oil and NGLs) over the first 60 days. The remaining two wells, brought online in the final days of the first quarter, are performing more than 350% above our internal type curve, with average IP rates per well of 887 boe/d (88% light oil and NGLs) over their initial 30 day period.

The Company is very excited about the highly accretive Pembina Acquisition announced February 19, 2025 and had anticipated strong results from the combined assets. The exceptional results from the first quarter drilling program, combined with the outperformance of base production, have driven current field estimated production to approximately 21,500 boe/d (64% light oil and NGLs) significantly exceeding what we had initially forecasted at the announcement of the Acquisition. Given the current volatility in commodity prices, this material outperformance provides the Company with significant flexibility to scale back our capital program, providing “more for less” while maintaining our production forecasts, allowing for more aggressive debt repayment even in a lower pricing environment.

2025 Capital Budget and Associated Guidance

Following the closing of the highly accretive Acquisition on April 7, 2025, InPlay is pleased to provide initial pro forma guidance inclusive of the Acquired Assets. This guidance reflects the exceptional operational performance across the Company’s expanded asset base, while taking into account the current volatile commodity price environment. It also underscores InPlay’s continued commitment to maximizing free cash flow to support ongoing debt reduction, while positioning the Company to support its return to shareholder strategy.

InPlay’s Board has approved an updated capital program of $53 – $60 million for 2025. InPlay plans to drill approximately 5.5 – 7.5 net Extended Reach Horizontal (“ERH”) Cardium wells over the remainder of the year. A significant portion of the remaining 2025 capital budget is expected to be directed toward the Acquired Assets, which (as outlined above) continue to materially outperform internally modelled type curves. Cost efficiencies realized through InPlay’s recent drilling program, combined with the application of InPlay’s drilling and completion techniques to the Acquired Assets, are expected to further enhance well economics. Capital will also be spent tying in certain InPlay assets into the newly acquired facilities, eliminating significant trucking costs, and marks the first step in our synergy cost savings strategy. Due to the outperformance of production across our asset base, InPlay has reduced total capital spending for the remainder of 2025 by approximately 30% (relative to initial expectations) without reducing production estimates.

Key highlights of the updated 2025 capital program include:

Production per Share Growth:

Forecasted average annual production of 16,000 – 16,800 boe/d(1) (60% – 62% light oil and NGLs), a 15% increase (based on mid-point) in production per weighted average share compared to 2024 despite 30% less capital spending than initially expected, driven by:

Lower corporate base decline rate of 24% due to the favorable decline profile of the Acquired Assets;

Improved corporate netbacks driven by the higher oil and liquids weighting of the Acquired Assets; and

Enhanced capital efficiencies from high graded drilling inventory of the pro forma assets.

FAFF Generation and Dividend Sustainability:

AFF(2) per weighted average share(4) of $5.00 – $5.35, a 13% increase (based on mid-point) compared to 2024.

Free adjusted funds flow (“FAFF”)(3) of $68 – $76 million equating to a 35% – 40% FAFF Yield(3), a 10x increase (based on mid-point) in FAFF per share compared to 2024 despite a 17% year over year reduction in forecasted WTI price.

Top Tier Returns:

Total return of 50% – 55% after combining FAFF Yield and production per share growth(4), which is expected to be at the high end of our peer group.

Debt Reduction:

Excess FAFF(3) is planned to be used to reduce debt.

Projected year-end Net Debt(2) of $213 – $221 million equating to a $31 – $39 million reduction from closing of the Acquisition.

Year-end Net Debt to Q4 2025 annualized EBITDA(3) ratio of 1.1x – 1.3x.

InPlay continues to monitor global trade and commodity dynamics, including United States tariffs on Canada. Capital spending will be weighted towards the back end of the year with drilling expected to resume again in August, providing ample time to finalize capital spending allocation depending on commodity pricing and continued asset performance. As a result of minimal capital spending in the second quarter, InPlay anticipates generating significant FAFF which will be directed to reducing debt. InPlay will remain flexible and will make decisions based on our core strategy of disciplined capital allocation, maintaining financial strength to ensure the long term sustainability of our strategy and return to shareholder program.

Updated 2025 Guidance Summary:

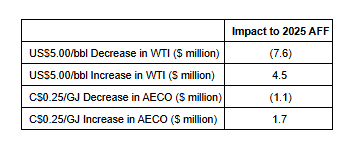

Following closing of the Acquisition, a significant hedging program was undertaken to help provide downside commodity price protection. As further detailed in the hedging summary section in this press release, InPlay has hedged approximately 75% of its net after royalty oil production and 67% of its net after royalty production on a BOE basis for the remainder of 2025. InPlay’s strong hedge book provides insulation to the current commodity price volatility which is highlighted in the sensitivity table below.

With low decline high netback assets, a flexible budget, a resilient balance sheet, and becoming a larger company, InPlay remains well positioned to sustainably navigate future commodity price cycles. Adhering to this disciplined strategy has allowed the Company to navigate previous commodity price cycles including the COVID-19 pandemic price environment.

Financial and Operating Results:

First Quarter 2025 Financial & Operations Overview:

The year has begun with strong momentum as production for the quarter exceeded internal forecasts, largely due to the outperformance of new ERH wells in PCU#7. Three (3.0 net) ERH wells were brought online at the end of February as part of a $13.9 million capital program, inclusive of $1.4 million invested in well optimization initiatives which continues to lower corporate declines. Production averaged 9,076 boe/d(1) (55% light crude oil and NGLs) in the quarter, a 5% increase from 8,605 boe/d(1) in the first quarter of 2024.

Notably, a two well pad drilled in PCU#7 exceeded expectations, delivering average IP rates of 677 boe/d (75% light oil and NGLs) and 492 boe/d (66% light oil and NGLs) per well over their first 30 and 60 days, respectively, which is over 100% above our internally modeled type curve for these wells.

Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which came on production mid quarter, are outperforming the internal type curve with IP rates averaging 304 boe/d (91% light oil and NGLs) and 295 boe/d (85% light oil and NGLs) over the first 30 and 60 days, respectively (approximately 50% above our internally modelled type curve). The last two wells were brought online in the final days of the quarter and are performing significantly above internal forecasts with IP rates averaging 887 boe/d (88% light oil and NGLs) per well over their first 30 days (more than 350% above our type curve).

AFF for the quarter was $16.8 million. In addition, the Company returned $4.1 million ($0.09 per share) in base dividends to shareholders which equates to a yield of 16% based on the current share price. Net debt at quarter-end totaled $63 million, with a net debt to EBITDA ratio(3) of 0.8x, reflecting a healthy financial position.

On behalf of the entire InPlay team and the Board of Directors, we thank our shareholders for their continued support as we advance our strategy of disciplined growth, returns, and long-term value creation. We are excited to report our progress with respect to the strategic Acquisition.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Watch the replays from the Noble Capital Markets Emerging Growth Virtual Equity Conference. Replays are available to Channelchek registered members. Registration is free and easy. Simply click the Join button in the upper right to get started.

Key Points – US plans tariffs up to 3,521% on solar panel imports from four Southeast Asian nations. – Domestic solar stocks surged, led by First Solar and Sunnova Energy. – The move could revive US-based solar manufacturing and reshape the industry.

Solar stocks rallied Tuesday after the US Department of Commerce unveiled plans to impose massive tariffs — as high as 3,521% — on solar panel imports from four Southeast Asian countries. The move sent shares of domestic solar manufacturers sharply higher as investors bet on a wave of renewed demand for American-made panels.

First Solar (FSLR) led the charge, soaring more than 9%, while Sunnova Energy (NOVA) jumped over 12%. Other solar-related names like SolarEdge Technologies (SEDG), Array Technologies (ARRY), and Enphase Energy (ENPH) also posted notable gains. The Invesco Solar ETF (TAN), a barometer for the sector, rose nearly 5% on the day, signaling a broad-based rally.

The proposed duties follow a yearlong investigation into claims that Chinese solar manufacturers were using proxy operations in Southeast Asia to circumvent earlier trade restrictions. The Commerce Department concluded that imports from Cambodia, Malaysia, Thailand, and Vietnam were being “dumped” into the US market — sold at artificially low prices — with the backing of Chinese state subsidies. Companies in Cambodia that failed to cooperate with the probe face the stiffest penalties.

If approved by the International Trade Commission (ITC), the tariffs could reshape the competitive landscape for solar panel manufacturing, providing a significant tailwind for US-based producers. The ITC has until June 2 to determine whether the subsidized imports harmed the domestic solar industry — a key requirement before the Commerce Department can implement the levies.

The decision is a major victory for the American Alliance for Solar Manufacturing, a coalition of US-based producers that pushed for the trade probe. The group has long argued that Chinese-headquartered firms have gamed the system by establishing operations in neighboring countries while continuing to benefit from Chinese subsidies. Advocates say the resulting price suppression has undermined domestic companies and led to job losses across the sector.

For US manufacturers, the announcement caps years of efforts to shift production closer to home — a trend first accelerated by the Biden administration’s Inflation Reduction Act, which offered tax incentives for domestic clean energy development. Companies like Enphase and First Solar have been actively reshoring production. First Solar, for example, opened a new facility in Alabama last year and now boasts a sizable manufacturing footprint in Ohio and Louisiana.

Despite Tuesday’s rally, solar stocks have struggled in 2025. Rising interest rates have increased financing costs for consumers, putting downward pressure on demand. The sector was also rattled by political headwinds following President Trump’s return to the White House and his vocal support for traditional energy. The tariffs, however, may signal a shift — a more nuanced approach to energy independence that could favor domestic solar even under a fossil fuel-friendly administration.

While the solar ETF TAN remains down more than 13% year to date and 27% lower over the past 12 months, the tariff announcement could serve as a turning point. Investors appear to be recalibrating their expectations for the space, betting that the tariff protections will help stabilize margins and renew growth.

If finalized, the tariffs could usher in a new chapter for American solar, one where domestic innovation and manufacturing play a central role in the industry’s expansion.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Share consolidation. As of April 21, 2025, InPlay Oil shares are trading on a post-consolidation basis, with 27,939,437 common shares outstanding. The terms of the share consolidation were one post-consolidation common share per six pre-consolidation common shares. Fractional shares resulting from the consolidation were rounded down to the nearest whole number.

Updating estimates and price target. We are updating our 2025 estimates to reflect fewer shares outstanding and lower crude oil price estimates. For 2025, we are lowering our oil and gas revenue and earnings per share estimates to C$318.7 million and C$1.34, from C$333.5 million and C$1.46, both adjusted for the share consolidation. Moreover, we have lowered our adjusted funds flow (AFF) to C$149.5 million from C$161.6 million. We are maintaining our production estimate of 18,750 barrels of oil equivalent per day (boe/d) post the Pembina acquisition, which averages 15,816 boe/d for the full-year 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

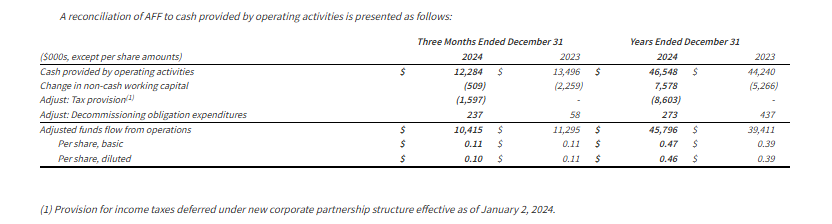

Full-year 2024 financial results. Hemisphere Energy reported full-year net income and earnings per share of C$33.1 million and C$0.33, respectively, slightly above our estimates of C$32.3 million and C$0.32. The variance is mainly due to stronger oil pricing of $79.48, compared to our estimate of $76.31. Year-over-year, oil and natural gas revenue increased ~18% to C$79.7 million from C$67.7 million. This increase was driven by increased production and more robust pricing of 3,436 barrels of oil equivalent per day (boe/d) and $79.48, respectively, compared to 3,125 boe/d and $74.07. Likewise, adjusted funds flow (AFF) increased 16% in 2024 to C$45.8 million from C$39.4 million in 2023. We had forecast AFF of C$45.4 million.

Updating estimates. Based on lower crude oil price estimates, we are lowering our 2025 net income and earnings per share estimates to C$30.3 million and C$0.29, respectively, from C$37.2 million and C$0.37. Additionally, we are decreasing our adjusted funds flow estimate to C$42.9 million from C$50.6 million. We are maintaining our 2025 average daily production estimate of 3,900 boe/d, an increase of ~14% over 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – April 17, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the fourth quarter and year ended December 31, 2024.

2024 Highlights

Increased annual production by 10% to a record of 3,436 boe/d (99% heavy oil).

Generated annual revenue of $99.9 million, an 18% increase over the previous year.

Achieved a 16% increase in annual adjusted funds flow from operations (“AFF”)(1) to $45.8 million.

Invested $22 million to drill nine wells, upgrade facilities, and purchase land at Atlee Buffalo in Alberta, as well as drill five wells (three production wells and two injection wells) and build the facilities required to test a pilot polymer flood at Marsden, Saskatchewan.

Generated $23.9 million of annual free funds flow (“FFF”)(1), a 6% increase over annual FFF reported for 2023.

Achieved robust operating and transportation costs of $15.60/boe.

Distributed $9.8 million in quarterly base dividends to shareholders during the year.

Distributed $5.9 million in special dividends to shareholders during the year.

Purchased and cancelled 3.4 million shares at an average price of $1.62 per share under the Company’s normal course issuer bid (“NCIB”), returning $5.5 million to shareholders during the year.

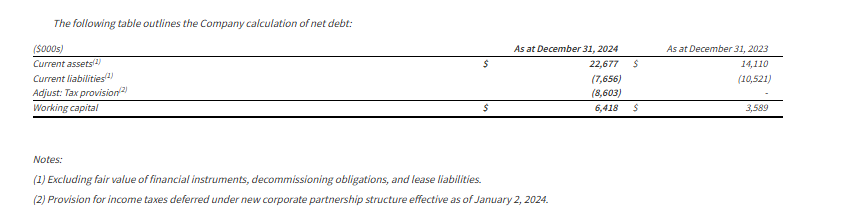

Exited 2024 with a positive working capital(1) position of $6.4 million compared to $3.6 million at December 31, 2023.

Note: (1)Non-IFRS financial measure that is not a standardized financial measure under International Financial Reporting Standards (“IFRS”) and may not be comparable to similar financial measures disclosed by other issuers. Refer to “Non-IFRS and Other Financial Measures” section below.

Financial and Operating Summary

Selected financial and operational highlights should be read in conjunction with Hemisphere’s audited consolidated financial statements and related Management’s Discussion and Analysis for the year ended December 31, 2024. These reports, including the Company’s Annual Information Form for the year ended December 31, 2024, are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Operations Update and Outlook

2024 marked another strong year for Hemisphere, with record production levels of over 3,400 boe/d (99% heavy oil), near record AFF of $45.8 million, record shareholder returns of over $21 million ($0.21/share) through dividends and share buybacks, and an increase in its net cash position at year end to $6.4 million. The Company’s first quarter 2025 field estimated production has since grown to 3,800 boe/d (99% heavy oil) through continued success of its polymer floods, despite no new wells being drilled since the third quarter of 2024.

Given the strong financial position and performance outlook of the Company, Hemisphere recently announced a special dividend of C$0.03 per common share to be paid on April 28, 2025 to shareholders of record on April 17, 2025. In 2024, Hemisphere’s total dividend payments to shareholders of C$0.16 per common share included two special dividends of C$0.03 per common share (in each of July and November), in addition to the base annual dividend of C$0.10 per common share. These special dividends are an important part of Hemisphere’s overall shareholder return model.

As seen over the first two weeks of April, pricing outlook for the oil market is experiencing significant volatility influenced by geopolitical developments, supply-demand dynamics, and trade tensions. Hemisphere’s 2025 budget is extremely flexible with minimal capital spending planned until summer. The Company’s robust balance sheet, ultra-low decline assets, and limited sustaining capital requirements for 2025 position Hemisphere well to withstand these economic headwinds.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-Looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements that a special dividend will be paid to shareholders on April 28, 2025 to shareholders of record on April 17, 2025; Hemisphere’s intention to have minimal capital spending until summer; and the Company’s view that its robust balance sheet, ultra-low decline assets, and limited sustaining capital requirements for 2025 position Hemisphere well to withstand economic headwinds.

Forward‐Looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; current budgets; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; trade and tariff matters, including the impacts on costs and supply chains; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, changes in Hemisphere’s budget, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

This MD&A contains the terms adjusted funds flow from operations, free funds flow, operating field netback and operating netback, capital expenditures and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

a)Adjusted funds flow from operations “AFF“ (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for tax provision and decommissioning expenditures, and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculatedusing the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

b)Free funds flow (“FFF”) (Non-IFRS Financial Measures): Calculated by taking adjusted funds flow and subtracting capital expenditures, excluding acquisitions and dispositions. Management believes that free funds flow provides a useful measure to determine Hemisphere’s ability to improve returns and to manage the long-term value of the business.

c)Capital Expenditures (Non-IFRS Financial Measure): Management uses the term “capital expenditures” as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities. A summary of the reconciliation of cash flow used in investing activities to capital expenditures is set forth below:

d)Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): A benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses, and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e)Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): Calculated as the operating field netback plus the Company’s realized gain (loss) on derivative financial instruments on an absolute and per barrel of oil equivalent basis.

f)Working capital/Net debt (Non-IFRS Financial Measure): Closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding derivative financial instruments, decommissioning obligations, and lease liabilities, adjusted for tax provision and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

g)Supplementary Financial Measures and Ratios

“Adjusted Funds Flow from operations per basic share” is comprised of funds from operations divided by basic weighted average common shares. “Adjusted Funds Flow from operations per diluted share” is comprised of funds from operations divided by diluted weighted average common shares. “Annual Free Funds Flow” is comprised of free funds flow from the current three-month period multiplied by four. “Operating expense per boe” is comprised of operating expense, as determined in accordance with IFRS, divided by the Company’s total production. “Realized heavy oil price” is comprised of heavy crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. “Realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. “Realized combined price” is comprised of total commodity sales from production, as determined in accordance with IFRS, divided by the Company’s total production. “Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the Company’s total production. “Transportation costs per boe” is comprised of transportation expenses, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2024, which is available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to initial production rates (including as a result of recent water or polymer flood activities) are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

WCS

Western Canadian Select

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Mboe

thousand barrels of oil equivalent

C$

Canadian Dollar

MMboe

million barrels of oil equivalent

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transformative acquisition closed. InPlay Oil recently closed its acquisition of Cardium light oil focused assets in the Pembina area of Alberta from Obsidian Energy for net consideration of approximately $301 million. The transaction more than doubles InPlay’s total output to 18,750 barrels of oil equivalent per day (boe/d). The assets are 68% weighted in oil and natural gas liquids (NGLs) and have a low decline rate of 22%. Management expects greater production, a lower decline rate, and enhanced operational efficiency. Following the completion of the acquisition, InPlay had 167,636,627 shares issued and outstanding.

Share consolidation. Effective April 14, InPlay will implement a share consolidation based on one common share for six common shares. The consolidation was unanimously approved by the company’s board and by 96.56% of the votes cast during a special meeting of shareholders. Post-consolidation, InPlay will have approximately 27,939,438 common shares issued and outstanding. The shares are expected to begin trading on a post-consolidation basis two to three trading days following the effective date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY AB, April 7, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) is pleased to announce that it has closed the previously announced strategic acquisition of Cardium light oil focused assets in the Pembina area of Alberta (the “Acquired Assets“) from Obsidian Energy Ltd. (the “Vendor“) for net consideration of approximately $301 million (the “Acquisition“).

The highly accretive Acquisition was funded by a combination of net proceeds released to InPlay pursuant to its previously announced $32.8 million bought deal subscription receipt financing (the “Financing“), an amended $330 million credit facility with a $190 million revolving credit facility, a letter of credit facility of up to $30 million, a fully drawn $110 million two-year amortizing term loan and the issuance of 54,838,709 InPlay common shares to the Vendor at a deemed price of $85 million or $1.55 per share (the “Share Consideration“). The Share Consideration is subject to a six-month lock up period, which may be shortened in certain circumstances.

In accordance with their terms, each one (1) subscription receipt issued pursuant to the Financing was automatically exchanged for one (1) InPlay Share concurrently with the completion of the Acquisition, and the net proceeds were released to InPlay from escrow and used to fund a portion of the cash consideration payable to the Vendor under the Acquisition. Previous holders of subscription receipts of InPlay are not required to take any action to receive the underlying InPlay Shares. Trading in the subscription receipts on the Toronto Stock Exchange is expected to be halted today and the subscription receipts delisted in due course.

Immediately following completion of the Acquisition, InPlay has 167,636,627 InPlay Shares issued and outstanding, inclusive of the underlying 21,145,625 InPlay Shares issued upon conversion of subscription receipts previously issued pursuant to the Financing and the Share Consideration issued to the Vendor.

Concurrent with completion of the Acquisition, InPlay entered into an amended and restated credit agreement with a syndicate of lenders (the “Lenders“) pursuant to which the aggregate available borrowing capacity under InPlay’s Senior Credit Facility has been increased from $110 million to $330 million by way of an increased $190 million revolving credit facility with a term out date extended to June 30, 2026, a fully drawn $110 million two-year amortizing term loan (the “Term Loan“) and a letter of credit facility of up to $30 million. The Term Loan includes quarterly amortization payments of $4.1 million. The covenant and security package under the new Term Loan is substantially the same as the revolving credit facility, with the exception of an additional affirmative covenant to satisfy certain prescribed hedging requirements during the period the Term Loan remains outstanding.

In accordance with a shareholder rights agreement between InPlay and the Vendor, the Vendor nominated Stephen E. Loukas, President and Chief Executive Officer and Peter D. Scott, Senior Vice President and Chief Financial Officer, both of Obsidian Energy Ltd., for election to the InPlay Board of Directors at the Special Meeting. Both nominees were elected as directors of InPlay to serve until the next annual meeting of shareholders or until their successors are elected or appointed. The Vendor nominees have agreed to support the resolutions brought before InPlay shareholders at the 2025 annual general meeting of shareholders.

Reader Advisories

Forward-Looking Information and Statements

This document contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this document contains forward-looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives; light crude oil and NGLs weighting estimates; expectations regarding future commodity prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures; the amount and timing of capital projects; and methods of funding our capital program.

The internal projections, expectations, or beliefs underlying our Board approved 2025 capital budget and associated guidance are subject to change in light of, among other factors, changes to U.S. economic, regulatory and/or trade policies (including tariffs), the impact of world events including the Russia/Ukraine conflict and war in the Middle East, ongoing results, prevailing economic circumstances, volatile commodity prices, and changes in industry conditions and regulations. InPlay’s 2025 financial outlook and revised guidance provides shareholders with relevant information on management’s expectations for results of operations, excluding any potential acquisitions or dispositions, for such time periods based upon the key assumptions outlined herein. Readers are cautioned that events or circumstances could cause capital plans and associated results to differ materially from those predicted and InPlay’s revised guidance for 2025 may not be appropriate for other purposes. Accordingly, undue reliance should not be placed on same.

Forward-looking statements or information are based on a number of material factors, expectations or assumptions of InPlay which have been used to develop such statements and information, but which may prove to be incorrect. Although InPlay believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because InPlay can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current U.S. economic, regulatory and/or trade policies; the impact of increasing competition; the general stability of the economic and political environment in which InPlay operates; the timely receipt of any required regulatory approvals; the ability of InPlay to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which InPlay has an interest in to operate the field in a safe, efficient and effective manner; the ability of InPlay to obtain debt financing on acceptable terms; the anticipated tax treatment of the monthly base dividend; that other than the tariffs that came into effect on March 4, 2025 (some of which were subsequently paused on March 6, 2025), neither the U.S. nor Canada (i) increases the rate or scope of such tariffs (if they come into effect in the future), or imposes new tariffs, on the import of goods from one country to the other, including on oil and natural gas, and/or (ii) imposes any other form of tax, restriction or prohibition on the import or export of products from one country to the other, including on oil and natural gas; the potential scope and duration of tariffs, export taxes, export restrictions or other trade actions; magnitude and duration of potential new or increased tariffs may be imposed on goods imported from Canada into the United States, which could adversely impact InPlay’s revenues; the potential for new and increased U.S. tariffs and protectionist trade measures on Canadian oil and gas imports; changes in political and economic conditions, including risks associated with tariffs, export taxes, export restrictions or other trade actions; impacts of any tariffs imposed on Canadian exports into the United States by the Trump administration and any retaliatory steps taken by the Canadian federal government; that InPlay’s results and operations could be adversely affected by economic or geopolitical developments, including protectionist trade policies such as tariffs, or other events; conditions in international markets, including social and political conditions, civil unrest, terrorist activity, governmental changes, restrictions on the ability to transfer capital across borders, tariffs and other protectionist measures; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and the ability of InPlay to secure adequate product transportation; future commodity prices; that various conditions to a shareholder return strategy can be satisfied; the ongoing impact of the Russia/Ukraine conflict and war in the Middle East; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which InPlay operates; and the ability of InPlay to successfully market its oil and natural gas products.

Without limitation of the foregoing, readers are cautioned that the Company’s future dividend payments to shareholders of the Company, if any, and the level thereof will be subject to the discretion of the Board of Directors of InPlay. The Company’s dividend policy and funds available for the payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to pay dividends will be subject to applicable laws, including satisfaction of solvency tests under the Business Corporations Act (Alberta), and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness. Further, the actual amount, the declaration date, the record date and the payment date of any dividend are subject to the discretion of the InPlay Board of Directors. There can be no assurance that InPlay will pay dividends in the future.

The forward-looking information and statements included herein are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); the risk that the Pembina Cardium asset acquisition may not be completed on the anticipated terms or timing; risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for InPlay’s products and/or otherwise adversely affects InPlay, or lead to the termination of InPlay’s financing arrangements for the Pembina Cardium asset acquisition, including specifically that the imposition of tariffs or similar measures in excess of 10% would be an adverse tariff event for the purposes of InPlay’s new credit facilities to be entered into in connection with the transaction and that the lenders thereunder may choose not to fund the transaction; the continuing impact of the Russia/Ukraine conflict and war in the Middle East; potential changes to U.S. economic, regulatory and/or trade policies as a result of a change in government; inflation and the risk of a global recession; changes in our planned 2025 capital program; changes in our approach to shareholder returns; changes in commodity prices and other assumptions outlined herein; the risk that dividend payments may be reduced, suspended or cancelled; the potential for variation in the quality of the reservoirs in which InPlay operates; changes in the demand for or supply of InPlay’s products; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans or strategies of InPlay or by third party operators of InPlay’s properties; changes in InPlay’s credit structure, increased debt levels or debt service requirements; inaccurate estimation of InPlay’s light crude oil and natural gas reserve and resource volumes; limited, unfavorable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in InPlay’s continuous disclosure documents filed on SEDAR+ including InPlay’s Annual Information Form dated March 27, 2024 and the annual management’s discussion & analysis for the year ended December 31, 2024.

This document contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about InPlay’s financial and leverage targets and objectives, potential dividends, and beliefs underlying our Board approved 2025 capital budget and associated guidance, all of which are subject to the same assumptions, risk factors, limitations, and qualifications as set forth in the above paragraphs. The actual results of operations of InPlay and the resulting financial results will likely vary from the amounts set forth in this document and such variation may be material. InPlay and its management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s reasonable estimates and judgments. However, because this information is subjective and subject to numerous risks, it should not be relied on as necessarily indicative of future results. Except as required by applicable securities laws, InPlay undertakes no obligation to update such FOFI. FOFI contained in this document was made as of the date of this document and was provided for the purpose of providing further information about InPlay’s anticipated future business operations and strategy. Readers are cautioned that the FOFI contained in this document should not be used for purposes other than for which it is disclosed herein.

The forward-looking information and statements contained in this document speak only as of the date hereof and InPlay does not assume any obligation to publicly update or revise any of the included forward-looking statements or information, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Risk Factors to FLI

Risk factors that could materially impact successful execution and actual results of the Company’s 2025 capital program and associated guidance and estimates include:

risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for the Company’s products and/or otherwise adversely affects the Company;

volatility of petroleum and natural gas prices and inherent difficulty in the accuracy of predictions related thereto;

the extent of any unfavourable impacts of wildfires in the province of Alberta.

changes in Federal and Provincial regulations;

the Company’s ability to secure financing for the Board approved 2025 capital program and longer-term capital plans sourced from AFF, bank or other debt instruments, asset sales, equity issuance, infrastructure financing or some combination thereof; and

those additional risk factors set forth in the Company’s MD&A and most recent Annual Information Form filed on SEDAR+.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President, Business Development, InPlay Oil Corp., Telephone: (587) 893-6804

Vancouver, British Columbia–(Newsfile Corp. – April 3, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that its board of directors has approved the declaration of a special dividend to shareholders.

Special Dividend

Given the strong financial position and performance outlook of the Company, Hemisphere’s board of directors has approved the declaration of a special dividend of C$0.03 per common share, in accordance with its dividend policy. The special dividend will be paid on April 28, 2025, to shareholders of record on April 17, 2025, and is designated as an eligible dividend for Canadian income tax purposes. It is in addition to the Company’s quarterly base dividend of C$0.025 per common share.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation, or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a special dividend will be paid to shareholders on April 28, 2025, to shareholders of record on April 17, 2025.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the timing for payment of the special dividend; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in project timelines and workstreams; changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

")