HOUSTON, June 1, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit,” “SMC” or the “Company”) today announced that its Board of Directors has authorized the Company’s inaugural stock repurchase program to repurchase up to $35 million of the Company’s outstanding common stock.

Heath Deneke, President, Chief Executive Officer and Chairman, commented, “The authorization of our inaugural share repurchase program reflects the Board’s confidence in Summit’s financial strength and the significant progress we have made over the past year in simplifying our balance sheet and strengthening our platform. Having repaid all arrears on our Series A Preferred Stock and supported by our improving free cash flow profile and financial flexibility, we are now in a position to utilize a common stock buyback program as a tool to ensure liquidity and support the secondary market of the shares. We believe our common stock represents an attractive opportunity at current levels, and we intend to be opportunistic in executing any repurchases.”

Under the program, repurchases of shares of the Company’s common stock may be made from time to time in the open market, through privately negotiated transactions, block purchases, or otherwise, including through a Rule 10b5-1 trading plan, in compliance with applicable federal and state securities laws, including Rule 10b-18 under the Securities Exchange Act of 1934, as amended. The timing and amount of any repurchases will be determined by management at its discretion based on a variety of factors, including business and market conditions, the trading price of the Company’s common stock, compliance with debt covenants, and certain other considerations. The program does not obligate the Company to repurchase any specific number of shares, has no fixed expiration date, and may be suspended or discontinued at any time.

About Summit Midstream Corporation

SMC is a value-driven corporation focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in the core producing areas of unconventional resource basins, primarily shale formations, in the continental United States. SMC provides natural gas, crude oil and produced water gathering, processing and transportation services pursuant to primarily long-term, fee-based agreements with customers and counterparties in five unconventional resource basins: (i) the Williston Basin, which includes the Bakken and Three Forks shale formations in North Dakota; (ii) the Denver-Julesburg Basin, which includes the Niobrara and Codell shale formations in Colorado and Wyoming; (iii) the Fort Worth Basin, which includes the Barnett Shale formation in Texas; (iv) the Arkoma Basin, which includes the Woodford and Caney shale formations in Oklahoma; and (v) the Piceance Basin, which includes the Mesaverde formation as well as the Mancos and Niobrara shale formations in Colorado. SMC has an equity method investment in Double E Pipeline, LLC, which provides interstate natural gas transportation service from multiple receipt points in the Delaware Basin to various delivery points in and around the Waha Hub in Texas. SMC is headquartered in Houston, Texas.

Forward-Looking Statements

This press release includes certain statements concerning expectations for the future that are forward-looking within the meaning of the federal securities laws. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements and may contain the words “expect,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result,” and similar expressions, or future conditional verbs such as “may,” “will,” “should,” “would” and “could.” In addition, any statement concerning future financial performance (including future revenues, earnings or growth rates), repurchases of the Company’s common stock, payment of dividends on any series of stock, ongoing business strategies and possible actions taken by SMC or its subsidiaries are also forward-looking statements. Forward-looking statements also contain known and unknown risks and uncertainties (many of which are difficult to predict and beyond management’s control) that may cause SMC’s actual results in future periods to differ materially from anticipated or projected results. An extensive list of specific material risks and uncertainties affecting SMC is contained in its 2025 Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission on March 16, 2026, as amended and updated from time to time. Any forward-looking statements in this press release are made as of the date of this press release and SMC undertakes no obligation to update or revise any forward-looking statements to reflect new information or events.

NCS Multistage is not a generalist oilfield services company. It operates in a specific and technically demanding niche: highly engineered products and support services that optimize well construction, completion, and field development strategies — primarily in horizontal wells drilled in unconventional oil and gas formations. Its technology is designed to improve reliability and production performance across the full well lifecycle, from initial completion design through late-stage production optimization and intervention.

The company operates primarily across North American basins and has established a presence in select international markets including the North Sea, the Middle East, and Argentina. That international footprint, while smaller than Weatherford’s, gives the combined company immediate leverage to cross-sell NCS Multistage’s technology into Weatherford’s six-continent global customer base — which is one of the most compelling near-term value creation levers in the deal.

Why This Deal Makes Sense Right Now

Weatherford is making a direct bet on two intersecting trends. The first is the sustained relevance of unconventional resource development. Despite the ongoing shift toward energy transition narratives, horizontal drilling and hydraulic fracturing in unconventional formations remain the backbone of North American oil and gas production. NCS Multistage’s core technology sits squarely in that production stream, and demand for completion optimization tools that improve per-well economics has not softened.

The second trend is consolidation driven economics. Smaller, specialized oilfield technology companies with strong engineering capabilities but limited distribution reach are increasingly attractive acquisition targets for larger platforms that can scale those technologies globally. NCS Multistage had the technology and the reputation. Weatherford has the footprint and the financial capacity to take it international.

Piper Sandler served as financial advisor to NCS Multistage in the transaction.

The Broader Signal for Small Cap Energy Services

For investors tracking the sub-$2 billion oilfield services and energy technology space, the Weatherford-NCS deal continues a pattern worth monitoring. Specialized completion technology, production optimization tools, and unconventional resource services companies have been consistent acquisition targets as larger players look to deepen technical differentiation rather than compete purely on scale.

The Iran conflict has kept oil prices elevated despite recent ceasefire negotiations, and sustained prices above $90 WTI support the capital spending levels that drive demand for exactly the kind of completion technology NCS Multistage provides. In that environment, companies with defensible technology niches and proven field performance records are not staying independent for long.

The most consequential macro story of 2026 may be moving toward resolution. The United States and Iran are now describing a draft memorandum of understanding to end their three-month conflict as “largely negotiated,” and oil markets are responding decisively. West Texas Intermediate crude fell to $89.97 per barrel Wednesday and Brent dropped to approximately $95, with both benchmarks down more than 10% since President Trump called off an imminent military strike on Iran ten days ago. That is a significant and rapid repricing for a commodity that was trading above $107 as recently as last week.

What the Draft Deal Actually Says

Iran’s state television and multiple US officials briefed on the talks have outlined the framework of the proposed MOU, which was brokered through indirect negotiations with Pakistan playing a central mediating role. Under the draft terms, Iran would restore commercial shipping through the Strait of Hormuz to pre-war levels within 30 days, and would clear the mines it deployed in the waterway. In exchange, the United States would lift its naval blockade of Iranian ports, withdraw military forces from Iran’s vicinity, and issue sanctions waivers allowing Iran to sell oil on global markets during a 60-day negotiating period.

The framework also includes the release of approximately $12 billion in frozen Iranian assets as part of a wider $25 billion package under discussion, and envisions Iran managing ship traffic through the strait in cooperation with Oman. If a final agreement is reached within the 60-day window, the MOU could be elevated to a binding UN Security Council resolution.

Trump described the deal as “largely negotiated” over the weekend after consulting with leaders from Saudi Arabia, the UAE, Qatar, Pakistan, Turkey, Egypt, Jordan, Bahrain, and Israel. Secretary of State Marco Rubio confirmed “good signs” and “progress” earlier this week. The deal has not yet been signed and Trump’s formal approval is still pending, while Iran has stated it will take no steps without “tangible verification” of US commitments.

Why This Matters for the Small Cap Universe

The Strait of Hormuz conflict has functioned as a slow-moving tax on the entire small and microcap economy since February 28. Oil above $100 compressed margins for consumer-facing companies, accelerated inflation, pushed Treasury yields to 19-year highs, and sharply reduced the probability of Fed rate cuts that smaller, variable-rate borrowers were counting on. The gradual unwinding of that pressure, if the deal holds, is not a single-day event. It plays out over weeks and quarters.

The most immediate beneficiaries are consumer-facing small caps in transportation, logistics, food service, and retail that have been absorbing elevated fuel costs with limited ability to pass them through to customers. Diesel prices remain significantly elevated, but a sustained move toward $80 WTI would represent meaningful operating cost relief for companies in these sectors.

The flip side is domestic energy producers. Independent oil and gas operators that benefited from WTI above $100 face a direct revenue headwind as prices normalize. Energy services companies and oilfield operators in the small cap space will need to watch production economics carefully if crude continues its descent.

The deal is not yet done. Multiple rounds of progress have collapsed in this conflict before, and outstanding issues including Iran’s nuclear program and enriched uranium stockpile remain unresolved. Energy executives have cautioned that full normalization of Middle East oil supply may not occur until 2027 given the scale of infrastructure disruption caused by the three-month closure. The IEA has also warned that global oil inventories remain dangerously depleted and markets could enter a supply “red zone” as summer travel demand builds.

A deal at $90 oil is not the same as a deal at $75 oil. But the direction of travel is clear, and for the half of the small cap economy that has been squeezed by elevated energy costs since late February, every dollar WTI moves lower is a dollar back in the margin structure.

Americans hitting the road this Memorial Day weekend are paying the highest prices at the pump in nearly four years and the bill is coming due for small and microcap companies across the consumer economy whether they are behind the wheel or not.

The national average for a gallon of regular gasoline reached $4.56 on Thursday according to AAA, up more than $1.38 from this time last year and more than 50% since the US and Israel launched strikes on Iran on February 28. Every single US state has now crossed the $4 threshold. Seven states are posting averages above $5, with California topping the national rankings at $6.16 per gallon. The last time Memorial Day fuel costs were this elevated was 2022, in the wake of Russia’s full-scale invasion of Ukraine, when the national average peaked at $4.61.

The summer outlook is not encouraging. GasBuddy projects the national average will run at approximately $4.80 per gallon across the full summer driving season from Memorial Day through Labor Day and warns prices could test the all-time record of $5.02 per gallon if the Strait of Hormuz remains effectively closed deep into the season. GasBuddy’s head of petroleum analysis attributes more than 90% of the year-over-year gap at the pump directly to the Iran conflict and the resulting disruption to the strait, which normally handles roughly one-fifth of global oil supply and has now been compromised for twelve consecutive weeks.

Record Travel, Real Costs

The timing could not be more pointed. AAA projects a record 45 million Americans will travel at least 50 miles this Memorial Day weekend, up from 44.8 million in 2025 and nearly 5% above pre-pandemic 2019 levels. Of those travelers, 87% will be driving. Gasoline demand ticked higher last week to 8.76 million barrels per day even as total domestic supply fell to 214.2 million barrels and production slipped to 9.3 million barrels per day. Demand rising into a tightening supply picture is not a recipe for relief at the pump.

The Small Cap Exposure

For investors in the sub-$2 billion market cap space, this is not an abstract macro story, it is an active margin event playing out across multiple sectors simultaneously. Regional trucking companies, last-mile delivery operators, and logistics providers are absorbing diesel costs that have risen sharply alongside gasoline, with limited ability to push surcharges through in a competitive environment. Consumer-facing small caps in food service, casual dining, and retail are getting squeezed from two directions: higher distribution and operating costs on one side, and a consumer with less disposable income after filling the tank on the other.

Travel-adjacent small caps, regional hospitality operators, independent hotel brands, and leisure-focused consumer companies face a more nuanced picture. Record travel volumes represent a genuine demand tailwind, but margin pressure from elevated fuel and labor costs can quickly offset volume gains for operators without significant pricing power.

The companies best positioned on the other side of this trade remain domestic energy producers. With WTI holding above $100 and summer demand accelerating into a supply-constrained market, independent oil and gas operators in the small cap space continue to benefit from a price environment that shows no structural signs of easing before fall.

The pump price this weekend is $4.56. If the Strait of Hormuz stays closed, it may look cheap by August.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lowering 1Q26 estimates. We have reduced our 1Q26 revenue, adjusted EBITDA, adjusted net income attributable to common shareholders, and EPS estimates to $42.9 million, $23.5 million, $9.5 million, and $0.45, respectively, from prior estimates of $43.9 million, $24.8 million, $10.1 million, and $0.48. The revisions primarily reflect a modest reduction in operating days to 1,696 from 1,700, a lower average daily TCE rate of $24,200 versus $25,100, and higher voyage and G&A expenses, including non-cash stock compensation.

FY26 estimates are mostly unchanged. We now project FY26 revenue, adjusted EBITDA, adjusted net income attributable to common shareholders, and EPS of $182.1 million, $106.7 million, $50.4 million, and $2.40, respectively, compared with prior estimates of $183.2 million, $105.2 million, $50.4 million, and $2.40.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

TSX approves share repurchase program. InPlay Oil Corp. announced that the Toronto Stock Exchange has approved its normal course issuer bid (NCIB), allowing the company to repurchase and cancel up to 1.79 million common shares, representing 10% of its public float. Purchases may be made through the TSX and other Canadian trading systems beginning May 25, 2026, and ending May 24, 2027, subject to daily purchase limits and applicable securities regulations.

Automatic repurchase plan provides flexibility. An automatic share purchase plan allows for repurchases to continue during self-imposed blackout periods. Outside of blackout periods, management will retain discretion over the timing and amount of share repurchases. Any shares acquired under the program will be canceled, reducing the company’s overall share count.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, May 20, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (TASE: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) is pleased to announce that the Toronto Stock Exchange (“TSX“) has accepted InPlay’s notice of intention to make a normal course issuer bid (the “NCIB“).

Under the NCIB, InPlay may purchase for cancellation, from time to time, as InPlay considers advisable, up to a maximum of 1,793,976 common shares (“Common Shares“), which represents 10% of the Company’s public float of 17,939,761 Common Shares as at May 14, 2026. As of the same date, InPlay had 28,006,416 Common Shares issued and outstanding. Purchases of Common Shares may be made on the open market through the facilities of the TSX and through other alternative Canadian trading systems at the prevailing market price at the time of such transaction. The actual number of Common Shares that may be purchased for cancellation and the timing of any such purchases will be determined by InPlay, subject to a maximum daily purchase limitation of 23,004 Common Shares which equates to 25% of InPlay’s average daily trading volume on the TSX of 92,017 Common Shares for the six months ended April 30, 2026. InPlay may make one block purchase per calendar week which exceeds the daily repurchase restrictions. Any Common Shares that are purchased by InPlay under the NCIB will be cancelled.

InPlay has entered into an automatic share purchase plan (“ASPP“) with a broker to facilitate repurchases of the Common Shares. Under the Corporation’s ASPP, the broker may repurchase Common Shares under the NCIB during the Corporation’s self-imposed blackout periods. Purchases will be made by the broker based upon the parameters prescribed by the TSX and applicable securities laws, as well as the terms of the ASPP and the parties’ written agreement. Outside of these blackout periods, Common Shares may be purchased under the NCIB in accordance with management’s discretion.

The NCIB will commence on May 25, 2026 and will terminate on May 24, 2027 or such earlier time as the NCIB is completed or terminated at the option of InPlay.

InPlay’s free cash flow has increased significantly in the current crude oil pricing environment. The Company believes renewing the NCIB is a prudent step in a volatile energy market, particularly during periods when the prevailing market price does not reflect the underlying intrinsic value of its Common Shares. The repurchase and cancellation of Common Shares demonstrates management’s confidence in the Company’s long-term prospects and the sustainability of its business model. By reducing the share count, the NCIB enhances per share metrics for shareholders and provides management with an additional tool within its disciplined capital allocation and shareholder return strategy.

About InPlay Oil Corp.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The Company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The Common Shares trade on the Toronto Stock Exchange under the symbol “IPO”, the Tel-Aviv Stock Exchange under the symbol “IPO” and the OTCQX under the symbol “IPOOF”.

For further information please contact:

Doug Bartole

Kevin Leonard

President and Chief Executive Officer

Vice President Corporate & Business Development

InPlay Oil Corp.

InPlay Oil Corp.

Telephone: (587) 955-0632

Telephone: (587) 955-0635

Caution Regarding Forward-Looking Statements

This news release contains certain statements that may constitute forward-looking information within the meaning of applicable securities laws. This information includes, but is not limited to InPlay’s intentions with respect to the NCIB and purchases thereunder and the effects of repurchases under the NCIB. Although InPlay believes that the expectations and assumptions on which the forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because InPlay can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions by their very nature they involve inherent risks and uncertainties. Actual results could defer materially from those currently anticipated due to a number of factors and risks. Certain of these risks are set out in more detail in InPlay’s Annual Information Form which has been filed on SEDAR+ and can be accessed at www.sedarplus.com.

The forward-looking statements contained in this press release are made as of the date hereof and InPlay undertakes no obligation to update publically or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Oil markets whipsawed Tuesday after President Trump announced he had called off a planned military strike on Iran scheduled for that morning, citing active negotiations brokered by Gulf allies. The announcement briefly pulled crude prices lower, but the relief was short-lived. The underlying supply crisis has not been resolved, and the data emerging from global inventory trackers suggests the window for a clean diplomatic outcome is narrowing fast.

Brent crude slipped to around $110 per barrel following Trump’s announcement while West Texas Intermediate pulled back to approximately $103. Both contracts had been climbing sharply the session prior, with Brent settling above $112 and WTT rising more than 3% on Monday alone. The combined 54% rise in both benchmarks since the US-Iran conflict began February 28 represents one of the most sustained energy price shocks in recent memory.

What Trump Said — and What It Means

Trump posted on Truth Social Monday evening that the leaders of Saudi Arabia, Qatar, and the United Arab Emirates personally requested he hold off on the strike while serious negotiations proceed. He confirmed the military had been placed on full alert and instructed to act on short notice if a deal is not reached. A senior US official told reporters that Iran’s latest proposal remains insufficient, and no framework has been announced. The ceasefire is intact — but barely.

The Inventory Problem

The diplomatic pause may have eased prices temporarily, but the physical oil market tells a more urgent story. The International Energy Agency warned Monday at the G7 finance ministers meeting in Paris that global commercial oil inventories are depleting at a record pace. Stockpiles fell 129 million barrels in March and another 117 million barrels in April. At the current rate of depletion, inventories will approach all-time lows of approximately 7.6 billion barrels by end of May — a timeline measured in days, not months.

Complicating matters further, Iran has effectively converted the strait into a toll-collecting operation. Reports indicate the Iranian Revolutionary Guards are charging vessels fees for passage, with nearly two dozen tankers sitting idle around Kharg Island. Traffic through the strait last week totaled just 55 vessels — still well below pre-conflict norms and only a marginal recovery from the wartime low of 19 crossings the prior week.

The Small Cap Exposure

For investors in the sub-$2 billion market cap space, the Iran situation is an active P&L event. Consumer-facing small caps in transportation, logistics, food services, and manufacturing continue absorbing elevated fuel costs that compress margins in real time. Limited pricing power and thin operating margins make smaller companies structurally more vulnerable to a prolonged energy shock than large cap counterparts.

The counterweight remains domestic energy producers. With WTI holding above $100 despite Tuesday’s pullback, the economics for independent US oil and gas operators remain highly favorable. Energy services companies and midstream operators in the small cap space are direct beneficiaries — and a negotiated resolution that reopens the strait would not necessarily collapse prices overnight given how severely inventories have been drawn down.

Trump’s call to stand down bought time. Whether that time produces a deal or simply delays the next escalation remains the most consequential open question in global energy markets right now.

The artificial intelligence boom just claimed its biggest infrastructure deal yet — and it has nothing to do with chips or software. NextEra Energy announced Monday it will acquire Virginia-based Dominion Energy in an all-stock transaction valued at approximately $66.8 billion, creating the world’s largest regulated electric utility by market capitalization and marking one of the most significant utility mergers in a generation.

The deal values Dominion at $75.97 per share — a roughly 23% premium to its last close — structured as an exchange of 0.8138 NextEra shares for each outstanding Dominion share. Dominion stock jumped nearly 15% on the announcement. NextEra shares slipped about 2% as investors digested the scale of the acquisition. The combined entity will carry a market cap of approximately $249 billion and an enterprise value of $420 billion, making it the third-largest company in the US energy sector behind only ExxonMobil and Chevron. The transaction is expected to close within 12 to 18 months.

Why This Deal Happened Now

The answer is straightforward: AI is consuming electricity at a pace the existing power grid was never built to handle. Dominion is the utility responsible for powering Northern Virginia’s “Data Center Alley” — the world’s largest concentration of data centers — with roughly 51 gigawatts of contracted data center capacity already on the books. Its customer list reads like a who’s who of hyperscale computing: Alphabet, Amazon, Microsoft, Meta, Equinix, CoreWeave, and CyrusOne all depend on Dominion’s grid.

Across both companies’ service territories, data centers proposing to connect to the combined grid represent approximately 130 gigawatts of future electricity demand. To put that in perspective, one gigawatt powers roughly 750,000 homes. NextEra’s CEO framed the acquisition plainly: electricity demand is rising faster now than it has in decades, and scale is the only way to meet it. The company plans to build more than 30 dedicated data center hubs across the US as part of its post-merger strategy.

Power prices nationally have already climbed roughly 40% over the past five years, with the sharpest increases concentrated in AI-heavy states including Virginia, Maryland, and Pennsylvania — the exact markets this merger is designed to dominate.

What It Means for Smaller Energy Players

A merger of this magnitude reshapes competitive dynamics across the entire energy infrastructure ecosystem, and the ripple effects reach well into the small and microcap space. The buildout required to serve 130 gigawatts of incremental data center demand cannot be executed solely through internal resources — it requires a network of suppliers, contractors, and technology providers operating at every layer of the grid.

Companies involved in grid modernization, high-voltage transformer manufacturing, power management systems, substation equipment, and renewable energy development are all positioned to benefit from the infrastructure spending surge that a combined NextEra-Dominion will need to execute. Many of the companies operating in these niches sit well below the $2 billion market cap threshold.

Independent power producers and smaller regional renewable developers face a more complex picture — a utility giant with NextEra’s capital base and Dominion’s existing relationships creates a formidable competitor for new generation contracts. But for those on the supply side of the infrastructure buildout, the pipeline just got significantly larger.

The AI energy trade is no longer a theme. It is the defining structural force reshaping American power markets — and Monday’s deal is the clearest evidence yet of just how seriously the biggest players are taking it.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

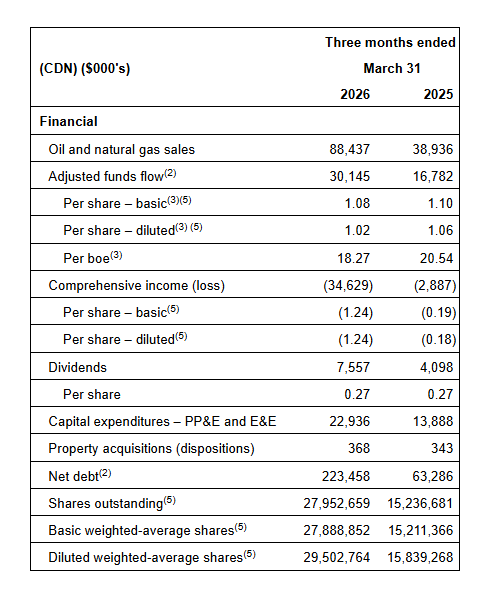

1Q 2026 financial results. InPlay Oil generated first-quarter 2026 adjusted funds flow (AFF) of C$30.1 million, or C$1.08 per share, above our estimate of C$27.4 million, or C$0.98 per share. Oil and natural gas sales revenue totaled C$88.4 million, ahead of our C$79.9 million forecast, due to stronger commodity prices. First quarter production averaged 18,337 barrels of oil equivalent per day (boe/d), modestly below our estimate. Compared to the prior year period, production, oil and natural gas sales revenue, operating income, and AFF increased 127.1%, 102.0%, 116.9%, and 79.6%, respectively. Average production more than doubled due to the successful integration of the company’s 2025 acquisition and strong results from its Pembina drilling program. Liquids production increased significantly, improving the overall production mix and supporting stronger corporate netbacks.

Outlook for the remainder of 2026. Supported by stronger oil prices, the Company increased its adjusted funds flow and free adjusted funds flow guidance to a range of C$143.0 to C$151.0 million, compared to previous expectations of C$122.0 million to C$129.0 million, while maintaining a disciplined production target of 18,600 to 19,200 boe/d and capital spending in the range of C$66.0 to C$74.0 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

HOUSTON, May 11, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit”, “SMC” or the “Company”) announced today its financial and operating results for the three months ended March 31, 2026.

Highlights

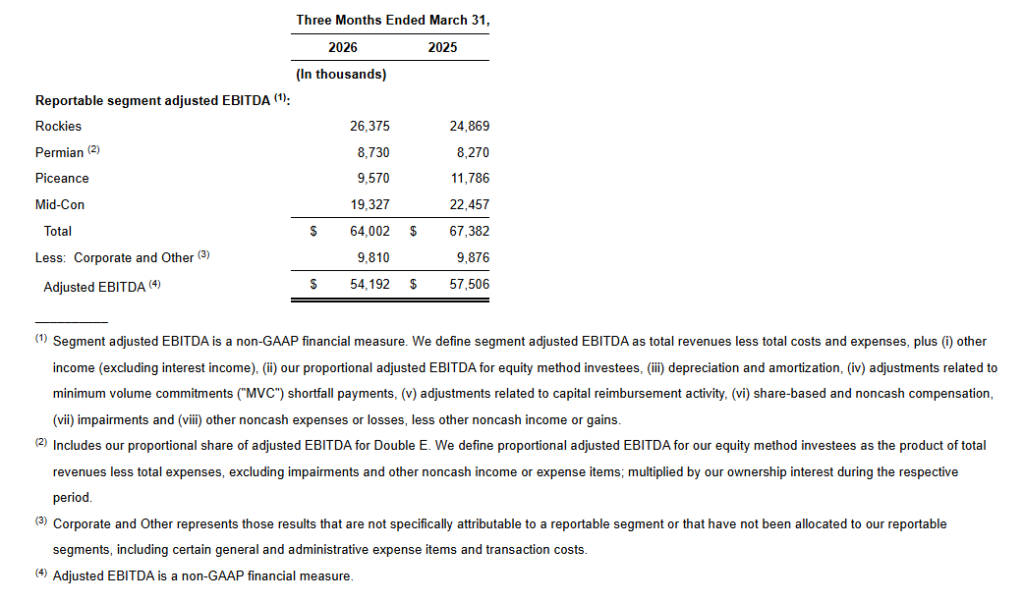

First quarter 2026 net loss of $3.2 million, Adjusted EBITDA of $54.2 million, cash flow available for distributions (“Distributable Cash Flow” or “DCF”) of $26.9 million and free cash flow (“FCF”) of $11.4 million

Connected 37 wells during the first quarter, including four Williston wells from the new 10-year crude gathering agreement; five rigs currently running with approximately 80 DUCs behind the systems

Executed a new precedent agreement for 100 MMcf/d of firm capacity on the Double E Pipeline, with Q1 2027 expected in-service date and 10-year term

Repaid all $45 million of accrued Series A Preferred Stock dividends clearing a key milestone toward reinstating a common dividend

Completed a $42 million private placement of common stock to an affiliate of Tailwater Capital LLC, Summit’s largest shareholder, providing additional financial flexibility to execute on high-return growth projects and reduce ABL borrowings

Reiterating 2026 full-year Adjusted EBITDA guidance of $225 million to $265 million, supported by accelerating producer activity in the Rockies and anticipated Mid-Con volume ramp

Management Commentary

Heath Deneke, President, Chief Executive Officer and Chairman, commented, “First quarter results reflected favorable crude oil prices primarily impacting our Rockies segment, offset by lower realized residue gas prices and lower than expected volumes in the Mid-Con Segment. We continue to expect the business to trend toward the midpoint of our original guidance range and are seeing a lot of momentum across our portfolio, particularly in the Permian and Rockies segments.

“Subsequent to quarter end, Double E executed another new 10-year take-or-pay precedent agreement for 100 MMcf/d of firm capacity behind an operational processing plant in Eddy County, New Mexico, with the lateral connecting the plant expected to be in-service in the first quarter of 20271. This agreement, along with those previously announced, brings total contracted volume on Double E to 1.755 Bcf/d, and we remain encouraged by the continued commercial progress on the pipeline. We are evaluating significant shipper interest in the recently launched open season, and remain optimistic there will be sufficient commercial support to make a final investment decision on the approximately 800 MMcf/d mid-point compression expansion project.

“In the Rockies Segment, the favorable crude oil price environment is expected to improve our product margin over the coming quarters and several customers are actively working to accelerate and increase activity beyond our original expectations. We are also encouraged by the preliminary results of four wells behind the new Williston Basin commercial contract we secured last quarter. We have 40 new wells expected across the portfolio in the second quarter, including 20 in the Mid-Con segment.”

__________________________

1 The agreement is contingent upon satisfaction of certain customary conditions, including Double E board approval.

First Quarter 2026 Business Highlights

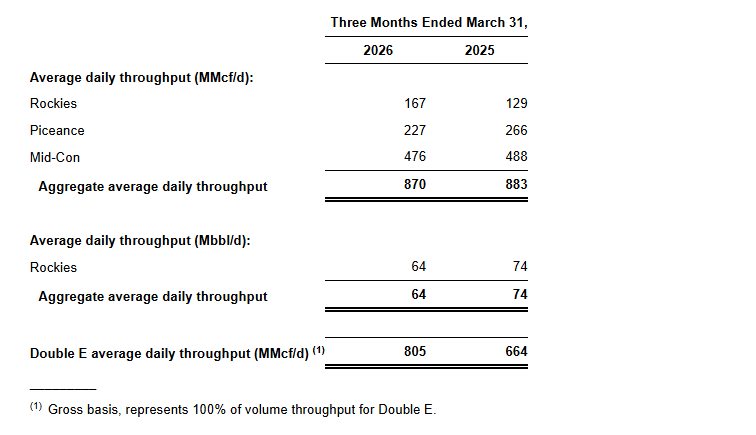

SMC’s average daily natural gas throughput on its wholly owned, operated systems decreased 2.7% to 870 MMcf/d, while liquids volumes decreased 3.0% to 64 Mbbl/d, relative to the fourth quarter of 2025. Double E Pipeline averaged 805 MMcf/d and contributed $8.7 million in Adjusted EBITDA, net to SMC, for the first quarter of 2026.

Natural gas price-driven segments:

Natural gas price-driven segments generated $28.9 million in combined Segment Adjusted EBITDA, a $2.6 million decrease relative to the fourth quarter of 2025, with combined capital expenditures of $7.6 million

Mid-Con Segment Adjusted EBITDA totaled $19.3 million, a decrease of $2.1 million relative to the fourth quarter of 2025, primarily due to lower natural gas throughput as a result of natural production declines, partially offset by six new Arkoma well connections. Subsequent to quarter end, three additional Arkoma wells were connected to the system and there are currently 17 Barnett DUCs expected to come online in the second quarter of 2026.

Piceance Segment Adjusted EBITDA totaled $9.6 million, a decrease of $0.4 million relative to the fourth quarter of 2025, primarily due to a 7.3% decline in volume throughput driven by temporary shut-ins of approximately 8.0 MMcf/d, natural production declines, and no new well connections during the quarter. Customers currently have ~20 MMcf/d of natural gas shut-in as a result of low regional gas prices. Based on current forecasted prices in the region, we expect this production to resume beginning in the third quarter of 2026.

Oil price-driven segments:

Oil price-driven segments generated $35.1 million in combined Segment Adjusted EBITDA, a $1.5 million decrease relative to the fourth quarter of 2025, with combined capital expenditures of $11.0 million

Rockies Segment Adjusted EBITDA totaled $26.4 million, a decrease of $1.5 million relative to the fourth quarter of 2025, driven by a $1.2 million non-cash imbalance, lower realized residue gas prices negatively impacting percent-of-proceeds contracts and lower fresh water sales, partially offset by a 4.4% increase in natural gas volume throughput and higher realized crude oil and NGL prices beginning in March 2026. 18 wells were connected in the DJ Basin and 13 in the Williston Basin, including the first four 3-mile lateral wells under the new 10-year crude gathering agreement. Five rigs are currently running with approximately 60 DUCs behind the system.

Permian Segment Adjusted EBITDA totaled $8.7 million, flat relative to the fourth quarter of 2025.

The following table presents average daily throughput by reportable segment for the periods indicated:

The following table presents adjusted EBITDA by reportable segment for the periods indicated:

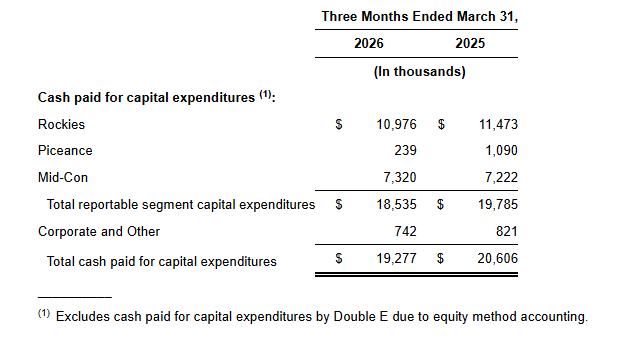

Capital Expenditures

Capital expenditures totaled $19.3 million in the first quarter of 2026, inclusive of maintenance capital expenditures of $3.7 million. Capital expenditures in the first quarter of 2026 were primarily related to pad connections in the Rockies and Mid-Con segments.

Capital & Liquidity

As of March 31, 2026, SMC had $43.4 million in unrestricted cash on hand and $116 million drawn under its $500 million ABL Revolver with $381 million of borrowing availability, after accounting for $2.7 million of issued, but undrawn letters of credit. As of March 31, 2026, SMC’s gross availability based on the borrowing base calculation in the credit agreement was $802 million, which is $302 million greater than the $500 million of lender commitments to the ABL Revolver. As of March 31, 2026, SMC was in compliance with all financial covenants, including interest coverage of 2.7x relative to a minimum interest coverage covenant of 2.0x and first lien leverage ratio of 0.4x relative to a maximum first lien leverage ratio of 2.5x. As of March 31, 2026, SMC reported a total leverage ratio of approximately 4.2x.

During the first quarter, Summit Permian Transmission, LLC entered into a new $440 million senior secured term facility, which includes a $50 million committed accordion feature and a $50 million uncommitted accordion feature (the “Term Facility”) maturing in March 2031. Proceeds from the Term Facility were used to refinance Summit Permian Transmission’s existing credit facility, redeem Summit Permian Transmission Holdco’s preferred units, fund an $85 million restricted payment to SMC, provide liquidity to fund SMC’s share of capital expenditures including those associated with the recently announced expansion projects, and pay other fees and expenses.

As of March 31, 2026, the Summit Permian Transmission Term Loan Facility had a balance of $340 million. Summit Midstream Permian has $6.1 million of cash-on-hand as of March 31, 2026. The Permian Transmission Term Loan remains non-recourse to SMC.

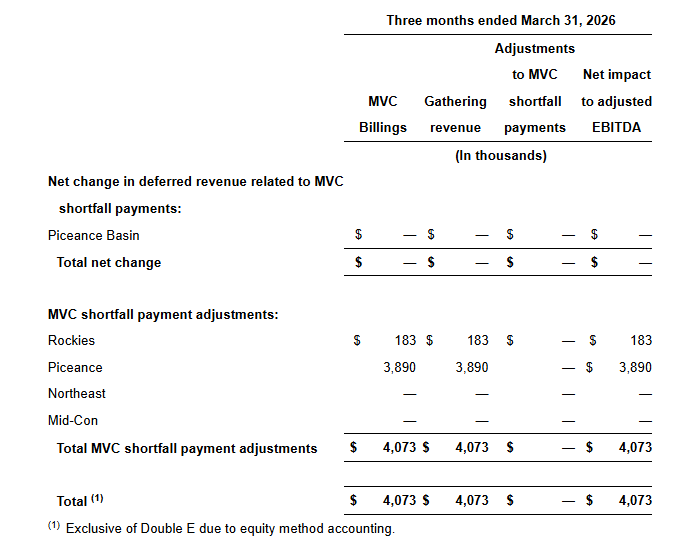

MVC Shortfall Payments

SMC billed its customers $4.1 million in the first quarter of 2026 related to MVC shortfalls. For those customers that do not have MVC shortfall credit banking mechanisms in their gathering agreements, the MVC shortfall payments are accounted for as gathering revenue in the period in which they are earned. In the first quarter of 2026, SMC recognized $4.1 million of gathering revenue associated with MVC shortfall payments. SMC had no adjustments to MVC shortfall payments in the first quarter of 2026. SMC’s MVC shortfall payment mechanisms contributed $4.1 million of total Adjusted EBITDA in the first quarter of 2026.

Quarterly Dividend

The Board of Directors of Summit Midstream Corporation continued to suspend cash dividends payable on the common stock for the period ended March 31, 2026. The quarterly cash dividend on the Series A Preferred Stock, for the period ended June 14, 2026, will be paid to preferred shareholders of record as of the close of business on June 1, 2026.

On March 27, 2026, all unpaid dividends of $46.3 million on the Series A Preferred Stock were paid to holders of record as of the close of business on March 17, 2026.

First Quarter 2026 Earnings Call Information

SMC will host a conference call at 10:00 a.m. Eastern on May 12, 2026, to discuss its quarterly operating and financial results. The call can be accessed via teleconference at the following link: Q1 2026 Summit Midstream Corporation Earnings Conference Call (https://register-conf.media-server.com/register/BI874f39fdf8c54b499c4ac477755fbcad). Once registration is completed, participants will receive a dial-in number along with a personalized PIN to access the call. While not required, it is recommended that participants join 10 minutes prior to the event start. The conference call, live webcast and archive of the call can be accessed through the Investors section of SMC’s website at www.summitmidstream.com.

Upcoming Investor Conferences

Members of SMC’s senior management team will attend the 2026 Energy Infrastructure CEO & Investor Conference which will take place on May 18–20, 2026, the 2026 RBC Capital Markets Global Energy, Power & Infrastructure Conference taking place on June 2–3, 2026, and the BofA Energy and Power Credit Conference on June 3–4, 2026. The presentation materials associated with each event will be accessible through the Investors section of SMC’s website at www.summitmidstream.com prior to the beginning of the conference.

Use of Non-GAAP Financial Measures

We report financial results in accordance with U.S. generally accepted accounting principles (“GAAP”). We also present adjusted EBITDA, segment adjusted EBITDA, Distributable Cash Flow, and Free Cash Flow, non-GAAP financial measures.

Adjusted EBITDA

We define adjusted EBITDA as net income or loss, plus interest expense, income tax expense, depreciation and amortization, our proportional adjusted EBITDA for equity method investees, adjustments related to MVC shortfall payments, adjustments related to capital reimbursement activity, share-based and noncash compensation, impairments, items of income or loss that we characterize as unrepresentative of our ongoing operations and other noncash expenses or losses, income tax benefit, income (loss) from equity method investees and other noncash income or gains. Because adjusted EBITDA may be defined differently by other entities in our industry, our definition of this non-GAAP financial measure may not be comparable to similarly titled measures of other entities, thereby diminishing its utility.

Management uses adjusted EBITDA in making financial, operating and planning decisions and in evaluating our financial performance. Furthermore, management believes that adjusted EBITDA may provide external users of our financial statements, such as investors, commercial banks, research analysts and others, with additional meaningful comparisons between current results and results of prior periods as they are expected to be reflective of our core ongoing business.

Adjusted EBITDA is used as a supplemental financial measure to assess:

the ability of our assets to generate cash sufficient to make future potential cash dividends and support our indebtedness;

the financial performance of our assets without regard to financing methods, capital structure or historical cost basis;

our operating performance and return on capital as compared to those of other entities in the midstream energy sector, without regard to financing or capital structure;

the attractiveness of capital projects and acquisitions and the overall rates of return on alternative investment opportunities; and

the financial performance of our assets without regard to (i) income or loss from equity method investees, (ii) the impact of the timing of MVC shortfall payments under our gathering agreements or (iii) the timing of impairments or other income or expense items that we characterize as unrepresentative of our ongoing operations.

Adjusted EBITDA has limitations as an analytical tool and investors should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. For example:

certain items excluded from adjusted EBITDA are significant components in understanding and assessing an entity’s financial performance, such as an entity’s cost of capital and tax structure;

adjusted EBITDA does not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments;

adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; and

although depreciation and amortization are noncash charges, the assets being depreciated and amortized will often have to be replaced in the future, and adjusted EBITDA does not reflect any cash requirements for such replacements.

We compensate for the limitations of adjusted EBITDA as an analytical tool by reviewing the comparable GAAP financial measures, understanding the differences between the financial measures and incorporating these data points into our decision-making process.

Distributable Cash Flow

We define Distributable Cash Flow as adjusted EBITDA, as defined above, less cash interest paid, cash paid for taxes, net interest expense accrued and paid on the senior notes, and maintenance capital expenditures.

Free Cash Flow

We define free cash flow as distributable cash flow attributable to common and preferred shareholders less growth capital expenditures, less investments in equity method investees, less dividends to common and preferred shareholders. Free cash flow excludes proceeds from asset sales and cash consideration paid for acquisitions.

We do not provide the GAAP financial measures of net income or loss or net cash provided by operating activities on a forward-looking basis because we are unable to predict, without unreasonable effort, certain components thereof including, but not limited to, (i) income or loss from equity method investees and (ii) asset impairments. These items are inherently uncertain and depend on various factors, many of which are beyond our control. As such, any associated estimate and its impact on our GAAP performance and cash flow measures could vary materially based on a variety of acceptable management assumptions.

About Summit Midstream Corporation

SMC is a value-driven corporation focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in the core producing areas of unconventional resource basins, primarily shale formations, in the continental United States. SMC provides natural gas, crude oil and produced water gathering, processing and transportation services pursuant to primarily long-term, fee-based agreements with customers and counterparties in five unconventional resource basins: (i) the Williston Basin, which includes the Bakken and Three Forks shale formations in North Dakota; (ii) the Denver-Julesburg Basin, which includes the Niobrara and Codell shale formations in Colorado and Wyoming; (iii) the Fort Worth Basin, which includes the Barnett Shale formation in Texas; (iv) the Arkoma Basin, which includes the Woodford and Caney shale formations in Oklahoma; and (v) the Piceance Basin, which includes the Mesaverde formation as well as the Mancos and Niobrara shale formations in Colorado. SMC has an equity method investment in Double E Pipeline, LLC, which provides interstate natural gas transportation service from multiple receipt points in the Delaware Basin to various delivery points in and around the Waha Hub in Texas. SMC is headquartered in Houston, Texas.

Forward-Looking Statements

This press release includes certain statements concerning expectations for the future that are forward-looking within the meaning of the federal securities laws. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements and may contain the words “expect,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result,” and similar expressions, or future conditional verbs such as “may,” “will,” “should,” “would” and “could.” In addition, any statement concerning future financial performance (including future revenues, earnings or growth rates), payment of dividends on any series of stock, ongoing business strategies and possible actions taken by SMC or its subsidiaries are also forward-looking statements. Forward-looking statements also contain known and unknown risks and uncertainties (many of which are difficult to predict and beyond management’s control) that may cause SMC’s actual results in future periods to differ materially from anticipated or projected results. An extensive list of specific material risks and uncertainties affecting SMC is contained in its 2025 Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 16, 2026, as amended and updated from time to time. Any forward-looking statements in this press release are made as of the date of this press release and SMC undertakes no obligation to update or revise any forward-looking statements to reflect new information or events.

CALGARY, AB, May 8, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (TASE: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three months ended March 31, 2026. InPlay’s unaudited interim financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the three months ended March 31, 2026 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated corporate presentation will be available on our website in due course.

First Quarter 2026 Highlights:

Closed an oversubscribed offering of senior unsecured bonds for total gross proceeds of C$244 million maturing on December 15, 2030 at an attractive interest rate of 6.23%. InPlay has fully hedged all cashflows relating to the New Israeli Shekel denominated bonds over the next four years.

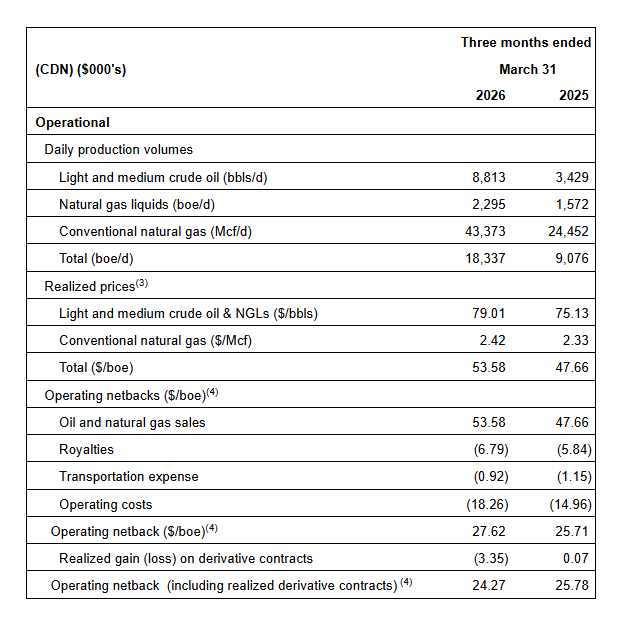

Achieved average quarterly production of 18,337 boe/d(1) (61% light crude oil and NGLs), a 102% increase from Q1 2025.

Improved light oil production to 8,813 bbl/d, a 157% increase from Q1 2025. Light crude oil weighting improved by 10% from Q1 2025 driving stronger per boe netbacks and returns.

Realized strong operating income of $45.6 million, a 117% increase from Q1 2025 and a 20% increase from Q4 2025. This resulted in an operating income profit margin(4) of 52%, an 11% improvement from Q4 2025.

Enhanced field operating netbacks(3) to $27.62/boe, an increase of 31% compared to Q4 2025.

Generated AFF(2) of $30.1 million ($1.08 per weighted average basic share(3)), an 80% increase from Q1 2025.

Returned $7.6 million to shareholders via monthly dividends (6.4% yield relative to current share price). Since November 2022, InPlay has distributed $75 million in dividends, including dividends declared to date in the second quarter.

Message to Shareholders:

The ongoing conflict in the Middle East and associated uncertainty has driven extreme and unprecedented volatility in oil and gas commodity prices. Concerns surrounding the largest oil supply shock in recent history has led to significantly higher crude oil prices. The Company believes this supply shortfall, combined with years of underinvestment and relatively modest global reserve additions compared to global consumption of approximately 38 billion barrels per year, supports a higher WTI pricing environment going forward relative to the ~US$60 WTI prices experienced in recent years.

InPlay has maintained a smart and disciplined business approach through the previous US$60 WTI pricing environment, achieving one of the highest free cash flow yields amongst our peers, which is expected to increase materially in a US $70+ WTI price environment. This increase is anticipated to drive meaningful net debt reduction, further strengthening the Company’s ability to execute our strategy of disciplined organic growth coupled with our strong track-record of accretive acquisitions, while reinforcing our focus on Free Adjusted Funds Flow and delivering strong returns to shareholders.

Our strategically aligned relationship with Delek Group Ltd. (“Delek”), who have a solid track record of value creation in the oil and gas industry, puts us in an advantageous position to execute our strategy. This relationship has already created meaningful value through Delek’s support in facilitating the successful issuance of unsecured bonds on the Tel Aviv Stock Exchange (“TASE”). The bonds were issued at favorable rates and terms, and we are confident we will have continued access to this advantageous cost of capital resource going forward.

During the first quarter, InPlay continued to build on the strong momentum generated from our transformational 2025 acquisition and results. The Company executed an active drilling program in the first quarter with five (5.0 net) Pembina Extended Reach Horizontal (“ERH”) wells drilled. The first two wells were brought on production in mid-February and have delivered strong results ahead of internal expectations. Initial production (“IP”) rates for these two wells were 333 boe/d (88% light oil and NGLs) per well over the first 60 days of production (45% above type curve) and they are currently producing at a rate of 278 boe/d (83% light oil and NGLs) per well. The last three wells were brought on production in April and are currently in the clean-up phase. These wells have delivered initial production (“IP”) rates of 351 boe/d (91% light oil and NGLs) per well over the first 27 days of production and are currently producing at a rate of 462 boe/d (90% light oil and NGLs) per well. To date, results indicate performance is significantly ahead of internal estimates.

The Company was able to access the field early in the second quarter during spring break-up, allowing us to accelerate our capital program. Drilling operations recently finished three (3.0 net) ERH Pembina wells that are expected to be on-production in early June, approximately 40 days earlier than originally planned. Unlimited use of access roads that are owned and maintained by the Company and unrestricted entry to surface locations with minimal road bans in effect allowed us to advance drilling operations in response to the significantly improved crude oil commodity price environment. Given the Company’s financial flexibility and ability to quickly adjust operations, further modifications to upcoming capital programs can be made in response to changing market conditions.

Driven by strong production exiting the first quarter, InPlay reiterates its 2026 average annual production guidance of 18,600 boe/d – 19,200 boe/d(1) (60% – 62% light oil and NGLs). The Company is now forecasting WTI prices to average US$81.50 for the remainder of the year (compared to our previous estimate of US$63.00). This results in an increase in AFF(2) from $125 million (mid-point) to $147 million (mid-point), with estimated FAFF(3) increasing from $55 million (mid-point) to $77 million (mid-point), equating to a FAFF yield(3) of 15% (mid-point). The Company’s leverage metrics are projected to remain strong with net debt to EBITDA(3) forecasted to be 1.1x for 2026 (mid-point).

The Company continues to monitor the evolving pricing environment and remains focused on disciplined but flexible capital allocation and maintaining financial strength to support long-term sustainability and returns to shareholders.

First Quarter 2026 Financial & Operations Overview:

InPlay completed an active capital program during the first quarter investing $22.9 million in drilling five (5.0 net) Pembina ERH wells and related infrastructure. Operational execution remained strong during the quarter, with drilling and completion operations on budget and consistent with recent capital programs. Some service equipment delays and unseasonably warm weather in March impacted completion operations on the three-well pad, resulting in a three-week delay in bringing these wells on production. The Company benefitted from new flush production coming on-line into a favorable oil pricing environment, with WTI prices averaging US $91.00 and US $98.06 in March and April respectively, compared to approximately US $62.50 during the first two months of 2026.

Quarterly production averaged 18,337 boe/d(1) (61% light crude oil and NGLs), representing a 102% increase from the first quarter of 2025. Quarterly crude oil production averaged 8,813 bbl/d, a 157% increase from the first quarter of 2025. The Company forecasts an estimate of 3% – 5% of downtime per month, the first quarter was impacted by some extraordinary one-time events, resulting in incremental downtime of approximately 475 boe/d (47% light oil and NGLs). This included a severe windstorm in March which damaged power infrastructure affecting the Company’s core Pembina properties, resulting in downtime of approximately 300 boe/d (55% light oil and NGLs) for the quarter. The low-decline nature of the Company’s base production, combined with strong performance of recently drilled wells, continues to benefit the Company.

Quarterly operating costs decreased on an absolute basis compared to the fourth quarter of 2025, but were slightly higher on a per boe basis reflecting the impact of fixed operating costs on per boe metrics due to production downtime from the one-time events described above. In addition, the Company performed service operations on five low-rate wells that have been offline for up to three years. At current crude oil prices, these wells are estimated to payout in 6 – 9 months and are anticipated to produce without issues for an additional 5 – 10 years with minimal decline. InPlay will look to complete similar well servicing operations in the upcoming months given the current pricing environment.

InPlay generated AFF of $30.1 million ($1.08 per basic share), representing an 80% increase from the first quarter of 2025. These results were achieved despite $5.5 million in realized hedging losses, primarily due to the significant increase in WTI in March relative to the hedges required by our first lien bank lenders to facilitate the acquisition in 2025. The Company has significantly less crude oil volumes hedged in the second half of 2026 and all of 2027 and intends to remain opportunistic with future hedging activity while monitoring the current backwardation in the WTI forward price curve. Details of the Company’s current hedges are provided in the “Hedging Summary” section of the Reader Advisories.

During the quarter, InPlay paid dividends of $7.6 million to shareholders, representing a 6.1% yield relative to our current share price. Since November 2022, InPlay has distributed $75 million in dividends, including dividends declared to date in the second quarter.

The Company realized a net loss of $34.6 million ($1.24 per basic share; $1.24 per diluted share), which includes a $39 million impact from the unrealized future mark-to-market value of the Company’s hedges required by our first lien bank lenders to facilitate our acquisition in 2025.

Financial and Operating Results:

On behalf of our employees, management team and Board of Directors, we thank our shareholders for their continued support and look forward to providing updates on our progress throughout the year.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0635

Notes:

1.

See “Production Breakdown by Product Type” at the end of this press release.

2.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

3.

Supplementary financial measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

4.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release and in our most recently filed MD&A.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President Corporate & Business Development, InPlay Oil Corp., Telephone: (587) 955-0635

May 4, 2026 – Vancouver, Canada – Century Lithium Corp. (TSXV: LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or the “Company”) is pleased to announce the following management appointments. These individuals will reinforce the Company’s technical, environmental, and operational capabilities as it advances its 100%-owned Angel Island Lithium Project (“Angel Island”) in Esmeralda County, Nevada, USA through permitting and pre-construction development programs.

“Century Lithium’s leadership and success to date in bringing forward our Angel Island lithium project has been greatly due to the expertise and contributions of the individuals recognized today,” said Bill Willoughby, President and CEO of Century Lithium. “These appointments reflect our commitment to continue to advance Angel Island and the Company to achieve the milestones ahead, while driving active engagement with our communities, regulators, and investors.”

Management Appointments

Todd Fayram was appointed CTO of the Company, effective April 9, 2026. Mr. Fayram is a metallurgical engineer with over 40 years of experience leading process design, construction, start-up, and operations improvement on mineral projects across North and South America. He is a Qualified Person under NI 43-101 through Registered Member status with MMSA, and a member of SME and CIM. He holds a Master of Science (M.Sc.) degree in Mineral Processing/Metallurgical Engineering and a Bachelor of Science (B.Sc.) degree in Mineral Processing Engineering, Metallurgy from Montana Technology University. Since 2018, Mr. Fayram has played a key role in developing the Company’s chloride leaching process, related intellectual property, and the engineering and operations programs that have advanced Angel Island, joining the Company in 2023 as Senior Vice President, Metallurgy. As CTO, he will lead the technical direction of the Company’s metallurgy, process development, engineering, and the continued advancement of Century Lithium’s patent-pending chloride leaching and direct lithium extraction flowsheet.

Daniel Kalmbach is appointed Vice President, Exploration and Resource Development. Mr. Kalmbach is a geologist with 26 years of experience in the minerals industry. Since 2017, Mr. Kalmbach has led the Company’s mineral resource development, technical reporting, and permitting activities for Angel Island. Mr. Kalmbach holds a B.Sc. degree in Geology from the University of Idaho and is a Certified Professional Geologist with the American Institute of Professional Geologists. He is a Qualified/Competent Person under CRIRSCO-recognized reporting standards. He will lead the Company’s geological operations including exploration and resource development efforts, overseeing resource modeling, drill program design, and resource expansion at Angel Island and across the Company’s portfolio.

Teresa Conner is appointed Director of Permitting and Environmental Affairs. Ms. Conner has 45 years of experience in both the mining and oil and gas industries. Since 2021, Ms. Conner has led the Company’s permitting activities and strategy, environmental planning, regulatory coordination, and compliance activities for Angel Island. Ms. Conner holds a B.Sc. degree in Mining and Geological Engineering and a M.L.S. degree in Legal Studies with a focus in Mining Law and Policy from the University of Arizona. Ms. Conner is a member of the Society for Mining, Metallurgy, and Exploration, and a member and former Trustee of the American Exploration & Mining Association. Ms. Conner brings extensive experience in permitting, federal land management coordination, and environmental baseline programs in the western United States. She will lead the Company’s permitting activities and engagement with public and regulatory interests.

Adam Knight is appointed General Manager. Mr. Knight is a mining engineer with 31 years of experience in the mining industry. Since 2020, Mr. Knight has managed project operations and field programs supporting the pilot plant program, infrastructure development, mine planning, and community liaison for Angel Island. Mr. Knight holds a B.Sc. degree in Mining Engineering from the University of Nevada, Reno and is a Licensed Professional Engineer in the State of Nevada. He is a Qualified/Competent Person under CRIRSCO-recognized reporting standards. He will oversee the implementation of Angel Island’s development plan, including coordination of engineering, procurement, and construction activities, contractor management, and project controls as the Company progresses toward construction readiness.

Richard Alberthal is appointed Manager, Technical Services. Mr. Alberthal has over 30 years of experience in the mechanical and process disciplines, including leadership roles in management, design and operations. Since 2020, Mr. Alberthal has worked directly with the construction and operation of the Company’s Pilot and Demonstration Plants, and the chlor-alkali and lithium carbonate processes for Angel Island. He will oversee technical services for Angel Island, including process plant commissioning readiness, operator training, and integration of the lithium carbonate and chlor-alkali process flowsheets developed for Angel Island.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced-stage lithium development company focused on its 100%-owned Angel Island lithium project in Esmeralda County, Nevada. Angel Island hosts one of the largest known sedimentary lithium deposits in the United States and is designed with an integrated, end-to-end process for the on-site production of battery-grade lithium carbonate to support the electric vehicle and battery storage markets.

The Company has developed a patent-pending process that incorporates hydrochloric acid leaching combined with direct lithium extraction to produce battery-grade lithium carbonate. As part of the integrated chlor-alkali process, Angel Island is designed to produce sodium hydroxide as a co-product, with planned surplus sales expected to lower operating costs, reduce reliance on externally sourced reagents, and minimize environmental impacts.

Century Lithium is currently advancing Angel Island through the permitting process.

Century Lithium trades on the TSX Venture Exchange under the symbol “LCE” the OTCQX under the symbol “CYDVF”, and on the Frankfurt Stock Exchange under the symbol “C1Z”.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.ca. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

")