The energy sector experienced a major shakeup today as Sunoco LP announced it will acquire NuStar Energy in an all-stock deal valued at approximately $7.3 billion including debt. The blockbuster acquisition aims to create a more diversified and vertically integrated energy company with an expanded footprint across the value chain.

For Sunoco, the deal provides a number of key benefits that will strengthen its operations and financial position. Most notably, it will gain NuStar’s extensive pipeline and storage terminal network which spans over 9,500 miles across the United States. This will provide greater scale and diversification to Sunoco’s current focus on fuel distribution and retail. As pipeline assets generate steady contracted revenues, the acquisition is expected to add stability and predictability to cash flows.

The larger cash flow base will also improve Sunoco’s credit profile and enhance its financial flexibility. This will enable accelerated deleveraging while also supporting steady distribution growth. Management estimates the deal will be immediately accretive to distributable cash flow per unit by 10%+ within three years. Ongoing synergies of $150 million annually will also boost the bottom line.

Vertically integrating NuStar’s transportation and storage activities with Sunoco’s strengths in distribution and retail is another major strategic benefit. This will help optimize operations across the integrated value chain and lead to further efficiency gains over time. Cost savings are forecasted at $50 million per year.

For the energy sector overall, the deal also has important implications. The combined entity will control critical infrastructure delivering refined products across the United States. With its expanded footprint, Sunoco will play an even more pivotal role ensuring energy supplies are reliably transported to end-users nationwide.

The acquisition also arrives at a challenging time for the industry. Many energy companies are facing pressure from the transition towards renewable power. By combining forces, Sunoco and NuStar can cut costs, leverage their size and scale, and invest in new growth opportunities. This will ultimately strengthen their competitiveness and staying power.

However, the deal does raise some regulatory concerns. With its extensive control over pipelines and storage capacity, the merged company could potentially restrict competitors’ access. Watchdogs will want to ensure open access at fair rates. Still, management emphasized the acquisition will have a positive financial outlook and support continued distribution growth. This should benefit both sets of unitholders if the deal is approved as expected.

Looking ahead, the acquisition positions Sunoco and NuStar to play a pivotal role in the future of US energy infrastructure. Their integrated network will be crucial for delivering traditional and renewable fuels as the industry evolves. With enhanced financial strength and flexibility, the combined giants now have greater capacity to adapt and seize new opportunities in the years ahead.

The annual World Economic Forum concluded on Friday in Davos, Switzerland, after a week of insight from some of the biggest names in business and politics. One of the main takeaways was optimism about avoiding a recession in the U.S. this year, despite ongoing economic concerns.

Most experts and executives see steady growth continuing in 2024, believing the economy remains on solid footing. Reasons for their confidence include potential interest rate cuts by the Federal Reserve in coming months, which could further stimulate economic activity. Consumer confidence has also been rising, suggesting households are eager to keep spending. Barring any major global crises, these factors have led to consensus that a downturn is unlikely in the next year.

The optimism comes as a breath of fresh air after massive disruption from the pandemic in recent years. However, other parts of the world are facing greater struggles. China in particular is dealing with slower growth, which prompted officials to reveal at Davos that their GDP expanded by just 5.2% in 2023. That’s down significantly from the 6-7% range China was averaging pre-pandemic.

Reasons for the slowdown include an ongoing semiconductor trade battle with the U.S. that is hurting tech manufacturing. China is also losing foreign direct investment as companies eye other Asian markets with friendlier business climates. The country recently lost its spot as the world’s most populous to rival India as well. With these challenges mounting, China appears eager for overseas capital to help spur its economy. Its officials breaking precedent to announce 2023 GDP numbers hints at this thirst for foreign money.

While China scrambles, Davos remains as popular as ever, albeit with some growing pains. Several regular attendees commented that the city is having infrastructure troubles keeping up with swarming conferences like the World Economic Forum. Traffic jams of shuttles and Ubers have become constant as hotels fill up. Local government officials apparently can’t even expense rooms anymore due to astronomical prices driven by demand.

This disruption didn’t stop high-level conversations on major themes like technology and geopolitics. Artificial intelligence was one of the hottest topics this year, taking over from the crypto hype of 2022. Companies flooded Davos with advertisements for their AI products and services. Headliners like will.i.am spoke enthusiastically about AI’s potential, announcing plans for a new podcast co-hosted with an AI companion.

But among the boosterism were voices urging calm and perspective. Sam Altman of OpenAI said AI will “change the world much less than we all think.” He noted how companies are using AI as a collaborative tool alongside human employees, rather than replacing them outright. Such measured takes may ease fears about mass job losses from automation. Job postings remain high in most countries, signaling an ongoing need for human skills and oversight.

While AI took center stage this year, some pressing geopolitical matters received surprisingly little airtime. The conflict between Israel and Hamas was rarely discussed, despite its global significance. Some speculate that businesses are wary of irritating stakeholders by speaking out on the polarizing topic. Similar logic may be why few executives criticized the prospect of Donald Trump returning to power. Staying cautiously neutral, however cynical, remains the safest option for profits.

Relatedly, the rise in antisemitism worldwide was a glaring omission in Davos discussions per some attendees. Finding constructive ways to combat prejudice could have been a valuable session. But the lack of debate on this and other divisive issues speaks to a gathering that ultimately caters to the global elite.

AI and recession talk make for good business panel chatter, but taking on discrimination may be beyond Davos’s comfort zone. As the conference’s popularity increases however, pressure may mount to address the most vital social issues of the day rather than sidestep them. Navigating that tension will be key to keeping Davos a premiere gathering of thought leaders.

For now, the World Economic Forum remains sold out and buzzing. Its reputation seems secure even as conversations gravitate toward the safest corporate ground. But avoiding the divides splintering society risks making Davos an echo chamber detached from reality. If it wants to keep its relevance, future forums may need to push attendees out of their comfort zones.

Mortgage rates fell to their lowest level in seven months this past week, providing a glimmer of hope for homebuyers who have been sidelined by high borrowing costs.

The average rate on a 30-year fixed mortgage dropped to 6.60% according to Freddie Mac, down from a recent peak of nearly 8% in October 2023. While still high historically, the retreat back below 7% could draw more prospective homebuyers back into the market.

The dip in rates comes as the housing market is showing early signs of a potential turnaround after a dismal 2023. Home sales plunged nearly 18% last year as surging mortgage rates and stubbornly high prices made purchases unaffordable for many.

But January has seen some positive signals emerge. More homes are coming up for sale as sellers who waited out 2023 finally list their properties. Real estate brokerage Redfin reported a 9% annual increase in inventory in January, the first year-over-year gain since 2019.

At the same time, buyer demand is also perking back up with the improvement in affordability. Mortgage applications jumped 10% last week compared to the prior week according to the Mortgage Bankers Association. While purchase apps remain below year-ago levels, the turnaround suggests buyers are returning.

“If rates continue to ease, MBA is cautiously optimistic that home purchases will pick up in the coming months,” said Joel Kan, MBA’s Vice President of economic and industry forecasting.

The increase in supply and demand has some experts predicting the market may be primed for a rebound in the spring home shopping season. But whether the inventory can satisfy purchaser interest remains uncertain.

“As purchase demand continues to thaw, it will put more pressure on already depleted inventory for sale,” noted Freddie Mac Chief Economist Sam Khater.

Homebuilders have pulled back sharply on new construction as sales slowed over the past year. And many current owners are still hesitant to sell with mortgage rates on their existing homes likely much lower than what they could get today. That leaves the total number of homes available for sale still historically lean.

Nonetheless, agents are reporting more bidding wars again for the limited inventory available in some markets. While not at the frenzied pace of 2022, competition for the right homes is heating up. Experts say interested buyers may want to start making offers now before the selection gets picked over.

“I’m advising house hunters to start making offers now because the market feels pretty balanced,” said Heather Mahmood-Corley, a Redfin agent. “With activity picking up, I think prices will rise and bidding wars will become more common.”

The driver of the downturn in rates since late last year has been an overall cooling of inflation pressures. The Federal Reserve pushed the 30-year fixed mortgage above 7% for the first time in over 20 years with its aggressive interest rate hikes aimed at taming inflation.

But evidence is mounting that the Fed’s policy actions are having the desired effect. Consumer price increases have steadily moderated from 40-year highs last summer. The slower inflation has allowed the central bank to reduce the size of its rate hikes.

Markets now expect the Fed to lift its benchmark rate 0.25 percentage points at its next meeting, a smaller move compared to the 0.50 and 0.75 point hikes seen last year. The slower pace of increases has taken pressure off mortgage rates.

However, the Fed reiterated it plans to keep rates elevated for some time to ensure inflation continues easing. Most experts do not foresee the central bank cutting interest rates until 2024 at the earliest. That means mortgage rates likely won’t fall back to the ultra-low levels seen during the pandemic for years.

But for homebuyers who can manage the higher rates, the recent pullback provides some savings on monthly payments. On a $300,000 loan, the current average 30-year rate would mean about $140 less in the monthly mortgage bill versus the fall peak above 8%.

While housing affordability remains strained by historical standards, some buyers are jumping in now before rates potentially move higher again. People relocating or needing more space are finding ways to cope with the increased costs.

With some forecasts calling for home prices to edge lower in 2024, this year could provide an opportunity for buyers to get in after sitting out 2023’s rate surge. It may be a narrow window however. If demand accelerates faster than supply, the competition and price gains could return quickly.

The U.S. job market continues to show resilience despite the Federal Reserve’s efforts to cool economic growth, according to new data released Thursday. Initial jobless claims for the week ending January 13 fell to 187,000, the lowest level since September of last year.

The decline in claims offers the latest evidence that employers remain reluctant to lay off workers even as the Fed raises interest rates to curb demand. The total marked a 16,000 drop from the previous week and came in well below economist forecasts of 208,000.

“Employers may be adding fewer workers monthly, but they are holding onto the ones they have and paying higher wages given the competitive labor market,” said Robert Frick, corporate economist at Navy Federal Credit Union.

The surprising strength comes even as the Fed has lifted its benchmark interest rate seven times in 2023 from near zero to a range of 4.25% to 4.50%. The goal is to dampen demand across the economy, particularly the red-hot job market, in order to bring down uncomfortably high inflation.

In addition to the drop in claims, continuing jobless claims for the week ending January 6 also declined by 26,000 to 1.806 million. That figure runs a week behind the headline number and likewise came in below economist estimates.

The resilience in the labor market comes even as broader economic activity shows signs of cooling. In its latest Beige Book report, the Fed noted that the economy has seen “little or no change” since late November.

Housing markets are a key area feeling the pinch from higher borrowing costs. The Fed summary showed residential real estate activity constrained by rising mortgage rates. Still, there were some green shoots in Thursday’s housing starts data.

Building permits, a leading indicator of future home construction, rose 1.9% in December to 1.495 million. That exceeded economist forecasts of 1.48 million permits. Actual housing starts declined 4.3% to 1.46 million, but still topped estimates calling for 1.43 million.

“The prospects of future easing from the Fed were raising hopes that the pace could accelerate,” the original article noted about housing.

Outside of housing, manufacturing activity in the Philadelphia region contracted again in January, though at a slightly slower pace. The Philly Fed’s index rose to -10.6 this month from -12.8 in December. Readings below zero indicate shrinking activity.

The survey’s gauge of employment at factories in the region also remained negative, though it improved to -1.8 from -7.4 in December. Overall, the Philly Fed report showed declining orders, longer delivery times, and falling inventories.

On inflation, the prices paid index within the survey fell to 43.4 from 51.8 last month. That indicates some easing of cost pressures for manufacturers in the region. The prices received or charged index also ticked lower.

The inflation figures align with the Fed’s latest nationwide look at the economy. The central bank’s Beige Book noted signs of slowing wage growth and easing price pressures. That could give the Fed cover to dial back the pace of interest rate hikes at upcoming meetings this year.

But policymakers also reiterated they plan to keep rates elevated for some time to ensure inflation continues cooling toward the 2% target. Markets still expect the Fed to lift rates again at both its February and March gatherings, albeit by smaller increments of 25 basis points.

With inflation showing increasing signs of moderating from four-decade highs, the focus turns to how much the Fed’s actions will slow economic growth. Thursday’s report on jobless claims hints the labor market remains on solid ground for now.

Employers added over 200,000 jobs per month on average in 2023, well above the pace needed to keep up with population growth. And the unemployment rate ended the year at 3.5%, matching a 50-year low first hit in September.

While job gains are expected to downshift in 2024, the claims report suggests employers are not rushing to cut staff yet. How long the resilience lasts as interest rates remain elevated and growth slows remains to be seen.

For the Fed, it will be a delicate balance between cooling the economy just enough to rein in inflation, without causing substantial job losses or triggering a recession. How well they thread that needle will be closely watched in 2024.

U.S. stocks slumped on Wednesday as Treasury yields climbed following better-than-expected December retail sales. The data signals ongoing economic strength, prompting investors to temper hopes for an imminent Fed rate cut.

The S&P 500 dropped 0.47% to an over one-week low of 4,743, while the Dow shed 0.01% to hit a near one-month low of 37,357. The tech-heavy Nasdaq fared worst, sinking 0.79% to 14,826, its lowest level in a week.

Driving the declines was a surge in the 10-year Treasury yield, which topped 4.1% today – its highest point so far in 2024. The benchmark yield has been rising steadily this year as the Fed maintains its hawkish tone. Higher yields particularly pressured rate-sensitive sectors like real estate, which fell 1.8% for its worst day in a month.

The catalyst behind rising yields was stronger-than-forecast December retail sales. Despite lingering inflation, sales rose 1.4% versus estimates of just 0.1%, buoyed by holiday discounts and robust auto demand. The robust spending highlights the continued resilience of the U.S. economy amidst Fed tightening.

This data substantially dampened investor hopes of the Fed cutting rates as soon as March. Before the report, markets were pricing in a 55% chance of a 25 basis point cut next month. But expectations sank to just 40% after the upbeat sales print.

Traders have been betting aggressively on rate cuts starting in Q2 2024, while the Fed has consistently pushed back on an imminent policy pivot. Chair Jerome Powell stated bluntly last week that “the time for moderating rate hikes may come as soon as the next meeting or meetings.”

“The market is recalibrating its expectations for rate cuts, but I don’t think that adjustment is completely over,” said Annex Wealth Management’s Brian Jacobsen. “A tug-of-war is playing out between what the Fed intends and what markets want.”

Further weighing on sentiment, the CBOE Volatility Index spiked to its highest level in over two months, reflecting anxiety around the Fed’s path. More Fedspeak is due this week from several officials and the release of the Beige Book economic snapshot. These could reinforce the Fed’s resolute inflation fight and keep downward pressure on stocks.

In company news, Tesla shares dropped 2.8% after the electric vehicle leader slashed Model Y prices in Germany by roughly 15%. This follows discounts in China last week as signs of softening demand grow. The price cuts hit Tesla’s stock as profit margins may come under pressure.

Major banks also dragged on markets after Morgan Stanley plunged 2% following earnings. The investment bank flagged weak trading activity and deal-making. Peer banks like Citi, Bank of America and Wells Fargo slid as a result.

On the upside, Boeing notched a 1.4% gain as it cleared a key milestone regarding 737 MAX inspections. This allows the aircraft to reenter service soon, providing a boost to the embattled plane maker.

But market breadth overall skewed firmly negative, with decliners swamping advancers by a 3-to-1 ratio on the NYSE. All 11 S&P 500 sectors finished in the red, underscoring the broad risk-off sentiment.

With the Fed hitting the brakes on easy money, 2024 is shaping up to be a far cry from the bull market of 2021-2022. Bouts of volatility are likely as policy settles into a restrictive posture. For investors, focusing on quality companies with pricing power and adjusting rate hike expectations continue to be prudent moves this year.

Shares of low-cost carrier Spirit Airlines plunged a staggering 47% on Tuesday after a federal judge ruled to block the proposed $3.8 billion acquisition by JetBlue Airways. The decision reignited antitrust concerns surrounding consolidation in the airline industry and delivered a major setback to the merger partners.

Judge Leo Sorokin of the U.S. District Court in Massachusetts sided with the Justice Department, which sued earlier this year to halt the deal between the two discount airlines. Regulators argued the merger would lead to higher fares, fewer choices, and reduced competition – particularly impacting budget-conscious leisure travelers.

In his ruling, Sorokin agreed the combination of JetBlue and Spirit would substantially reduce competition in major metropolitan areas and lead to dominant market power on hundreds of routes. Evidence also suggested the merger was likely to raise base fares above pre-merger levels, contradicting the airlines’ claims that the deal would actually lower costs for consumers.

The Justice Department applauded the decision, stating it protected the interests of millions of air travelers against the threat of increased prices and reduced options. The Biden administration has taken a tougher stance on antitrust issues across industries like tech and healthcare. Blocking this airline deal marked the first time in over 20 years regulators successfully halted a major U.S. carrier merger.

JetBlue and Spirit responded with disappointment, saying they disagree with the judge’s rationale and are evaluating their legal options. Previously, the carriers contended combining forces would fuel competition with larger legacy airlines and drive down airfares. But regulators argued JetBlue’s Northeast Alliance with American Airlines already gave the company substantial market power.

For Spirit, the failed acquisition is a crushing blow after months in limbo. The ultra-low cost airline initially agreed to merge with fellow discounter Frontier Airlines before JetBlue stepped in with a higher bid. Now, Spirit finds itself alone again after the about-face regulators delivered.

The collapsed deal and renewed antitrust scrutiny sent Spirit’s stock price into a nosedive. Shares cratered from Friday’s close of $19.66 to around $10.40 on Tuesday after the ruling. The 47% single-day wipeout vaporized over $1.4 billion in market value. Investors are surely questioning what’s next for the budget carrier without an imminent buyer or partner.

The blocked merger also casts uncertainty over ongoing consolidation in the travel and tourism sector. Many investors had bet on further airline combinations to drive efficiency and shareholder returns. With regulators now throwing up roadblocks, the appetite for large-scale airline deals could diminish. That may leave some carriers struggling to gain scale and keep pace with leading players like Delta and American.

Broader travel stocks also felt the tremor of the scuttled Spirit-JetBlue tie-up. Shares of Hawaiian Holdings, involved in a proposed merger with Alaska Air, fell nearly 2% Tuesday afternoon amid the uncertain regulatory environment. Cruise operators like Norwegian and Royal Caribbean slid as much as 5%, potentially signaling dampened outlooks for leisure sector combinations.

Potentially compounding Spirit’s challenges, competitor Frontier Airlines could come back to the table with a renewed merger proposal now that JetBlue is sidelined. Spirit already expended time and resources negotiating with Frontier last year. More uncertainty around consolidation could further destabilize the airline at a precarious moment.

Looking ahead, Spirit and JetBlue still have avenues to continue the legal fight. They could appeal the decision or take their arguments directly to regulators for another look. But after the Justice Department’s strong stance earlier in the case, the odds of overturning the ruling remain long.

For now, the blocked acquisition marks a setback in the wave of consolidation that has swept the U.S. airline industry over the past two decades. Major carriers will be wary of attempting large mergers and risking similar antitrust opposition. While the Biden administration succeeded in halting this particular deal, ongoing fragmentation may not solve the lack of competition in air travel markets across America.

In one of the largest tech industry mergers of recent years, Synopsys has announced it will acquire engineering simulation software maker Ansys in an all-cash deal valued at approximately $35 billion. The deal combines two leading players in software tools for semiconductor and electronic product design, expanding Synopsys’ total addressable market as it aims to create an integrated platform for chip design and beyond.

The merger agreement will see Synopsys pay around $390 per share for Ansys – $197 per share in cash plus about one-third of a Synopsys share for each Ansys share. This represents a premium of roughly 20% over Ansys’ recent share price. Ansys shareholders will own 16.5% of the combined company once the acquisition is finalized, expected in the first half of 2025 pending regulatory approvals.

Synopsys plans to fund the cash component of the deal through a combination of $16 billion in new debt financing and $3 billion cash on hand. The company had $1.4 billion in cash reserves as of October 2022. Synopsys CEO Sassine Ghazi has acknowledged the deal will not be accretive to earnings for at least 12 months post-closing due to financing and integration costs.

Expanding Synopsys’ Platform from Silicon to System

For Synopsys, a leading vendor of electronic design automation (EDA) software used by semiconductor companies, the deal strategically expands its platform. Ansys provides physics-based simulation software that helps engineers virtually test product design, performance and safety across industries like automotive, aerospace, consumer electronics and medical devices.

Synopsys aims to combine its strengths in chip design with Ansys’ expertise in simulating mechanical, thermal and electromagnetic effects at the full system level. This can help Synopsys address the entire electronic system lifecycle – from silicon to software to system integration.

The merger can also unlock new integrated workflows between the companies’ complementary technologies. For instance, connecting Ansys’ simulation tools to Synopsys’ ARC processor IP and DSO.ai AI-driven debugging solution. Such integration can speed up testing and validation for customers building advanced chips, electronics and embedded software.

Leveraging Ansys’ Footprint Across Industries

Another driver for Synopsys is leveraging Ansys’ customer footprint across major industries developing smart, connected products. As a leader in physics simulation, Ansys serves over 11,000 organizations globally. Its customer base includes manufacturers in automotive, aerospace, 5G telecom and medical technology.

The merger can open cross-selling opportunities for Synopsys to provide its EDA tools – from IP libraries to verification software – to Ansys’ customers working on chip-centric system designs. It also gives Synopsys greater exposure to growing demand for simulations, modelling and digital twins driven by trends like metaverse platforms, autonomous vehicles and the Internet of Things.

According to Synopsys, the combined company will have a total addressable market exceeding $50 billion by 2025 – significantly broadening its market beyond EDA software. In addition, Ansys’ recurring revenue base can provide Synopsys more stability to weather downturns in the historically cyclical semiconductor market.

Executing a Complex Tech Industry Merger

Despite the strategic benefits, executing a merger of this scale will be complex. Ansys has over 3,700 employees worldwide. Integrating its engineering teams and R&D roadmap with Synopsys’ will take time and care. Synopsys also has work ahead to achieve the full vision of a integrated “silicon-to-software” platform based on the combined portfolios.

Most importantly, the companies need to preserve Ansys’ neutrality and multi-vendor interoperability as it moves under Synopsys’ ownership. Any perception that Ansys will favor Synopsys’ own tools following the merger could drive customers to exploring alternatives. Maintaining Ansys as an “open platform” will be key.

Nonetheless, the deal provides Synopsys – already on a strong growth trajectory – a significant opportunity to expand its enterprise software footprint. If successful, it could cement Synopsys as the premier player in next-generation chip design workflows and empower even smarter, connected, electronics-driven experiences. But realizing Ansys’ full value will require skillful integration by Synopsys at a scale it has never attempted before.

British telecommunications giant Vodafone has announced a 10-year, $1.5 billion strategic partnership with Microsoft to bring next-generation artificial intelligence (AI), cloud, and Internet of Things (IoT) capabilities to Vodafone’s markets across Europe and Africa.

The deal reflects both companies’ ambitions to be at the forefront of AI and digital transformation. By combining forces, they aim to enhance Vodafone’s customer experience, network operations, and business offerings for the 300 million consumer and enterprise customers it serves.

Transforming Customer Service with AI

A major focus of the partnership will be transforming Vodafone’s customer service using AI and natural language processing. Microsoft will provide access to its Azure OpenAI platform, including technologies like GPT-3.5 for generating conversational text.

Vodafone plans to invest heavily in building customized AI models using Microsoft’s tools. This includes enhancing TOBi, Vodafone’s digital assistant chatbot, to deliver more personalized and intelligent customer interactions across text, voice, and video channels.

More consistent and contextualized responses from TOBi could improve customer satisfaction and loyalty while reducing operational costs for Vodafone. The two companies will also collaborate on conversational AI and digital twin capabilities to optimize Vodafone’s network operations.

Transitioning to the Cloud

Another key element of the deal is transitioning Vodafone away from reliance on its own data centers. It will adopt Microsoft Azure as its preferred cloud platform, migrating workloads and infrastructure to Azure’s global footprint.

This should provide Vodafone with more flexibility, scalability, and cost efficiency. Azure’s extensive compliance and security controls will also help Vodafone meet strict regulatory requirements for its markets.

Vodafone plans to train and certify hundreds of employees as Azure experts to enable the shift. The cloud transition can allow Vodafone to retire legacy systems, consolidate data platforms, and leverage new technologies like AI more quickly.

Microsoft’s Equity Investment in Vodafone’s IoT Business

To deepen integration between the two companies, Microsoft will also become an equity investor in Vodafone’s IoT division when it spins out as a separate business in 2024.

Vodafone’s IoT platform connects over 120 million devices globally across areas like asset tracking, smart metering, and automotive. Microsoft’s investment reflects the strategic value it sees in Vodafone’s IoT leadership.

Together, they aim to scale Vodafone’s IoT solutions on Azure’s global infrastructure and combine them with Microsoft’s own IoT cloud services. This can drive faster time-to-market for new solutions. Microsoft also wants to leverage Vodafone’s IoT data and networks in sustainability and digital twin projects across multiple industries.

Empowering Mobile Finance in Africa

In Africa, the partnership has a strong focus on expanding access to mobile financial services. Vodafone operates the popular M-Pesa platform which pioneered mobile money across Eastern Africa.

Microsoft will provide AI capabilities to enhance functions like credit assessment for M-Pesa users. The goal is to drive financial inclusion and provide intelligent financial tools to the unbanked population in Vodafone’s African footprint.

Microsoft and Vodafone will also cooperate to improve digital skills and literacy for small businesses by providing bundled connectivity, devices, and software through the new partnership. This aligns with both companies’ commitments to empower digital transformation and economic opportunity in the region.

An Ambitious Partnership for the AI and Cloud Era

The scale of the newly announced partnership reflects Vodafone and Microsoft’s shared ambition to shape the future of technology and connectivity. By combining Vodafone’s reach across emerging markets with Microsoft’s leading cloud and AI enterprise offerings, they want to enable inclusive digital experiences for consumers and businesses worldwide.

The deal demonstrates the transformational power of AI and cloud to reinvent customer service, improve operational efficiency, and develop innovative business models. As 5G networks expand globally over the next decade, the partnership lays the groundwork for Vodafone to transition itself into a future-ready technology leader.

Internet & Digital Media Stocks – Investors Rewarded with Exceptional Returns in 2023

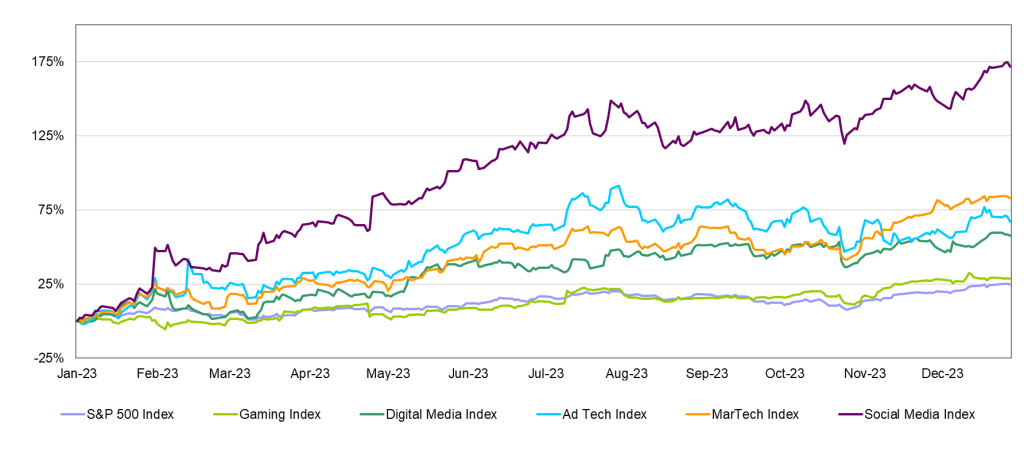

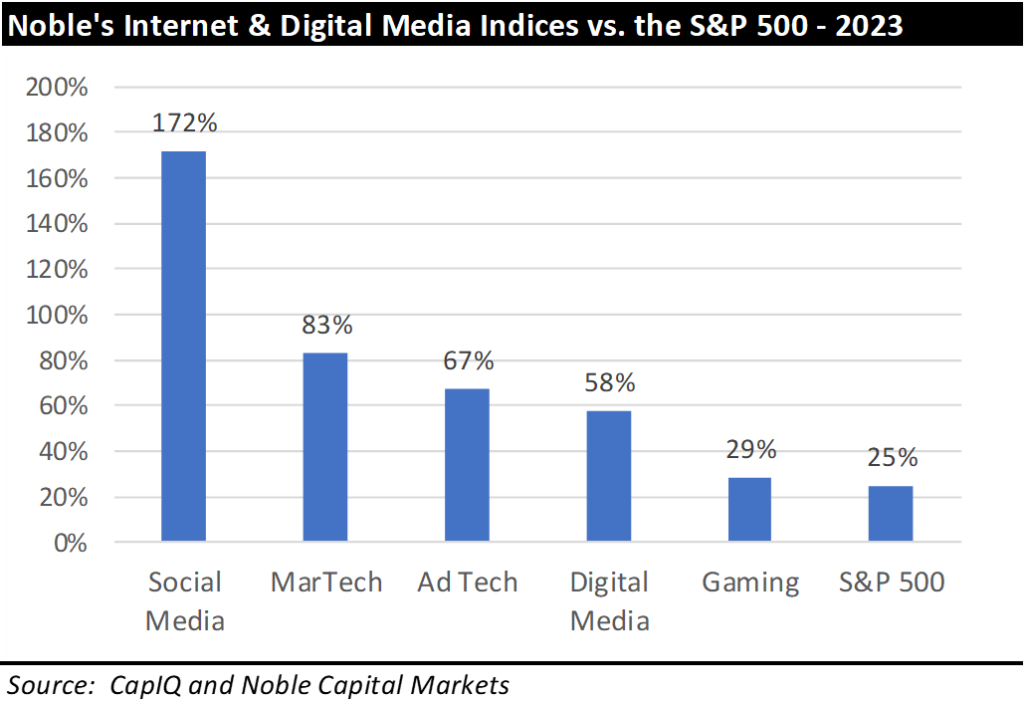

A year ago, we wrote that we were seeing signs of life in the Internet and Digital Media sectors and saw the possibility of a better year ahead. Not only was it a good year, but it was a great year for investors in these sectors. The S&P 500 was up 25% in 2023, a healthy return but one that pales in comparison to the performance of each of Noble’s Internet and Digital Media Indices. Noble’s Social Media Index finished the year up 172%, followed by Noble’s MarTech (+83%), AdTech (+67%), Digital Media (+58%) and Video Gaming (+29%) indices.

Noble’s indices are market cap driven, and last quarter we noted that while each sector performed well, it was primarily due to the largest cap stocks in each of them. In 4Q 2023, we saw that strength broaden and deepen, with mid- and small-cap stocks also joining the “party”.

STOCK MARKET PERFORMANCE: INTERNET AND DIGITAL MEDIA

Interestingly, this increase in performance from mid- and smaller cap stocks did not result in a material outperformance relative to the S&P 500 in the fourth quarter. The S&P 500 increased by 11% in 4Q 2023, but only two of these indices outperformed the broader market during this period: Noble’s MarTech Index (+24%) and Social Media Index (+19%). Noble’s Video Gaming Index (+11%) was up in-line with the S&P 500, while Noble’s Digital Media (+9%) and Ad Tech (+0%) indices underperformed. In short, while the mega cap stocks continued to outperform, this outperformance was matched or exceeded by mid- and small-cap stocks in the fourth quarter.

Meta, Snap, and Grindr All Lead the Social Media Index Higher

Noble Indices are market cap weighted, and we attribute the relative strength of the Social Media Indexto its largest constituent, Meta(META, +194%). Meta shares were up 194% for the year, including 18% in the fourth quarter. As noted before in this newsletter, Meta shares bottomed in November 2022 at $89 per share and began to recover when management decided to no longer invest as heavily in the metaverse and instead ordered a major cost-cutting initiative that included thousands of layoffs and re-focused the company’s resources toward new social media products (i.e., Threads) and generative AI (artificial intelligence).

Other social media stocks such as Snap (SNAP, +89%) and Grindr (GRND, also +89%) significantly outperformed. Snap shares increased as the company’s revenue returned to growth in the third quarter after declines in the first and second quarter of the year. Grindr went public via SPAC in 4Q 2022 and its shares stumbled out of the gate but performed exceptionally well, especially in 4Q 2023 (+53%) as the company continued to post 40%+ revenue growth and 50%+ EBITDA growth. There is no better recipe for share price appreciation than beating Street estimates and raising guidance.

MarTech Stocks Recover Strongly After Challenging 2022

Investors in the marketing technology sector were also rewarded in 2023. Noble’s MarTech Index increased by 83%, led by Shopify (SHOP, +124%), Hubspot (HUBS, +111%), Salesforce (CRM, +99%) and Adobe (+77%). MarTech stocks suffered in 2022 from a market reset in revenue multiples that began when the Fed began raising rates.

Another reason Noble’s MarTech Index was down 52% in 2022 was that most every company in this sector did not have operating profits or positive EBITDA, as companies in this sector, like most SaaS-based businesses were being operated to maximize revenues, not profitability. MarTech companies appear to have gotten the message in 2023 and made great strides in terms of operating profits. On average, operating margins significantly improved from low double-digit negative margins in 2022, to low single digit negative margins in 2023.

AdTech Stocks Rebounded Strongly in 2023

Noble’s Ad Tech Index increased by 67% in 2023, and returns were relatively widespread with more than half the stocks in the index posting double digit returns, led by Direct Digital Holdings (DRCT, +514%), AppLovin (APP, +278%), Inuvo (+92%), Double Verify (DSP, +68%), Interactive Ad Science (IAS, +64%) and The Trade Desk (+61%). Shares of Direct Digital Holdings increased by 481% in the fourth quarter alone, as the company reported significantly stronger than expected revenue and EBITDA and guided to significantly higher than expected 4Q 2023 revenue and EBITDA as well. Companies such as Double Verify, and Interactive Ad Science likely benefited as their ad platforms are designed to verify inventory and reduce fraud and waste. The Trade Desk has also developed initiatives to address “cookie deprecation” (in which Google will end support for third-party cookies, or tracking tags). It would appear that investors in the second half of 2024, investors sought out Ad Tech companies that are well positioned for this change.

A Widespread Recovery in the Digital Media Sector

Noble’s Digital Media Index increased by 58% in 2023 with 8 of the 12 stocks in the index posting double digit stock price returns, led by Spotify (SPOT, +138%), Travelzoo (TZOO, +114%), Fubo (FUBO, +83%), and Netflix (NFLX, +65%). Spotify posted double digit revenue growth while keeping expenses in check which resulted in a solid operating profit in 2023. The company is making progress on converting its growing user base to a healthy profit. Consensus Street estimates have Spotify’s EBITDA improving from a loss of nearly $250 million in 2022 to a gain of $650 million in 2024. Meanwhile, Travelzoo appears to be firing on all cylinders with revenue increasing by double digits in each of their U.S., European and Jack’s Fight Club businesses. Travelzoo appears to be in the sweet spot of the economic cycle in which demand for travel is strong, but not so strong that the company’s clients (airlines, hotels, cruise lines, car rental companies, etc.) don’t need to advertise to drive incremental demand.

We attribute much of the strong performance in 2023 in the Internet and Digital Media sectors to a change in investor sentiment most likely based upon the view that rather than go into recession, the U.S. economy may be more likely to incur a soft landing. How this plays out in 2023 is likely to be the key to the performance of these industries in 2024.

2023 M&A – Deal Activity Flat while Deal Values Decline by Nearly 80%

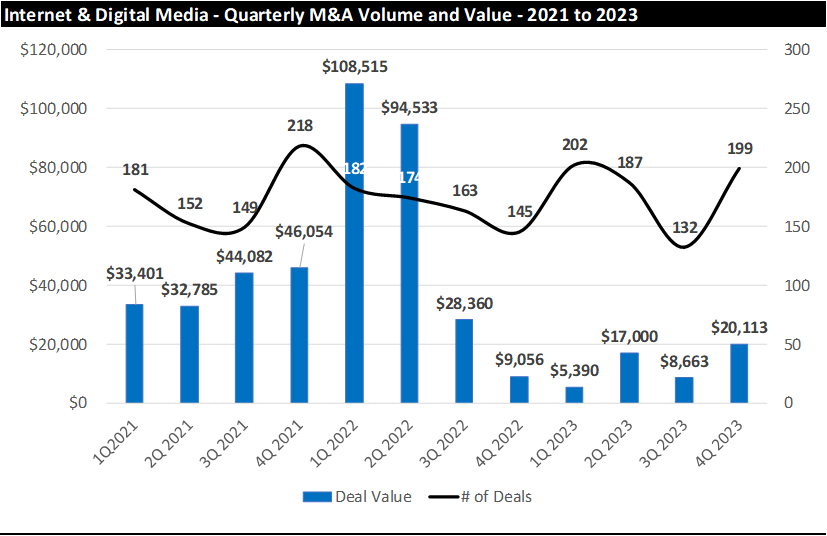

It should not surprise anyone that M&A in the Internet and Digital Media sectors was down in 2023. For starters, 2022 was a very strong year for M&A, with deal values up 71% over 2021 levels. On top of this difficult comparison, the M&A market in 2023 had to contend with numerous headwinds, including geopolitical tensions, inflation, rising interest rates, increased regulatory scrutiny and an uncertain economic outlook. In light of all of these obstacles, it is surprising then, that the number of deals we monitored in the Internet and Digital Media sectors in 2023 was flat compared to 2022 (685 deals announced in 2023 vs. 683 deals announced in 2022). This result would appear to be heroic were it not for the fact that total M&A deal values were down 79% in 2023 ($51 billion in announced deal values in 2023 vs. $243 billion in announced deal values in 2022). Given the aforementioned headwinds, perhaps it is not surprising that the animal spirits to conduct large transactions waned in 2023.

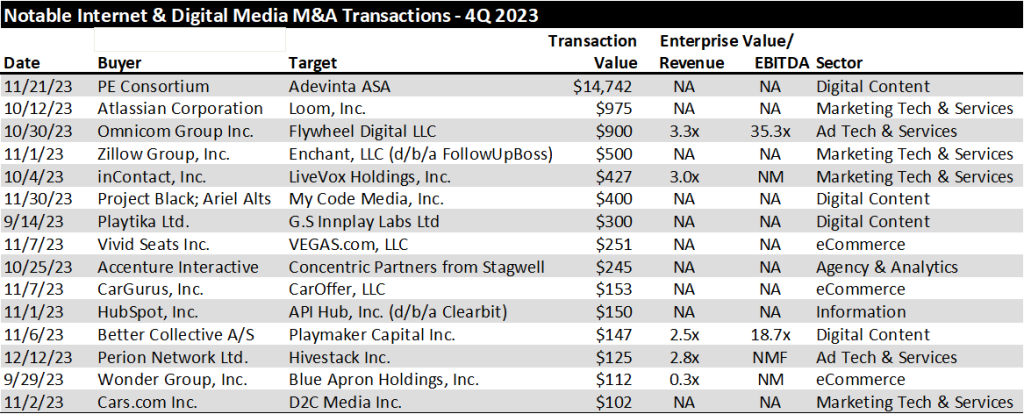

The biggest difference in the announced deal values was the number of “scaled transactions” in 2022 vs. 2023. A year ago we called 2022 the Year of the Mega Deal. For example, the were 6 announced deals in the Internet and Digital Media sectors with deal values exceeding $10 billion in 2022 vs. only one deal in 2023. In 2022, Microsoft announced its $69 billion acquisition of Activision Blizzard and Elon Musk announced his $46 billion acquisition of Twitter. In 2023, the only “scaled transaction” in the Internet and Digital Media sectors was the $14.6 billion acquisition of online classifieds company Adevinta ASA from a consortium of U.S. based private equity firms (General Atlantic, Permira and Blackstone).

4Q 2023 M&A: Greenshoots?

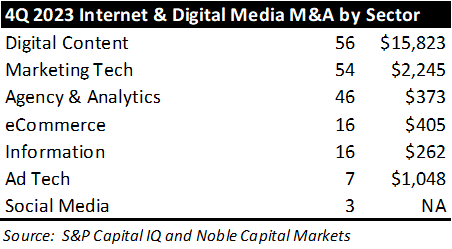

Fortunately, there was a silver lining in the fourth quarter of 2023. Deal activity picked up substantially on a sequential basis. We monitored 199 announced transactions in 4Q 2023, up 50% over the 132 announced deals 3Q 2023. Deal values in the fourth quarter of 2023 were also encouraging. We monitored $20.1 billion in announced deal values last quarter, up 132% from the $8.7 billion in announced deals in 3Q 2023, as shown in the chart below.

From a deal activity perspective, the most active sectors we tracked were Digital Content (56 deals), Marketing Tech (54 deals), Agency & Analytics (46 deals), followed by eCommerce (16 deals) and Information (16 deals). From a deal value perspective, the Digital Content sector had the largest dollar value of transactions ($15.8 billion, driven by the Adevinta deal), followed by MarTech ($2.2 billion), and AdTech ($1 billion).

The largest deals by dollar value in the fourth quarter of 2023 are shown below.

With stock prices recovering and the prospects for a soft landing improving, we believe the stage is being set for an improvement in the M&A environment in 2024. A key to this outlook will be how soon and how fast the Federal Reserve begins to lower interest rates. If inflation remains stubborn and rates remain higher for longer, then the recovery in M&A deal values is likely to take longer. However, if rates begin to ease, it will remove a key impediment to closing transactions in 2024.

TRADITIONAL MEDIA COMMENTARY

The following is an excerpt from a recent note by Noble’s Media Equity Research Analyst Michael Kupinski

Overview – Optimism for a Good 2024

The fortunes of advertising-based companies are driven by the economy and the health of the consumer. As such, we start this report with our take on the economy in 2024. On December 4th, at Florida Atlantic University (FAU) in Boca Raton, Florida, Noblecon19 hosted an economic panel to discuss the business environment outlook for 2024. The economic panel consisted of a diverse group of industry professionals with a wide range of expertise and experience. In our economic outlook for 2024, we take into consideration the perspective of Jose Torres, Senior Economist at Interactive Brokers.

Mr. Torres highlighted 2023 as a resilient year for consumer spending, which was driven by excess pandemic savings accumulated in 2020 and 2021. Mr. Torres anticipates a slowdown in consumer spending and a strong labor market in 2024. Notably, he believes a resilient labor market will keep consumers spending and will keep the country from falling into a recession. Additionally, Mr. Torres highlighted that Personal Consumption Expenditures (PCE) annualized inflation over the last six months is running near 2.5%, which is very close to the Fed’s goal of 2.0%. With moderating inflation pressures, Mr. Torres highlighted that the Fed is likely to cut rates in March of 2024, which would be beneficial for small and mid-cap companies. While Mr. Torres largely has a positive outlook for 2024 and beyond, a point of concern was the federal government’s growing interest expense on debt, he noted that the government will eventually have to reduce spending or accept 3% – 3.5% inflation over the long-term.

The general U.S. economy is expected to soften in 2024, particularly in the first half, with a prospect that the economy could slip into recession. Our economic scenario for 2024 anticipates the economy will soften in the first half of the year and rebound in the second half of the year due to the prospect of a lower interest rate environment and resilient labor market.

The video of the Economic Perspectives panel may be viewed here.

STOCK MARKET PERFORMANCE: TRADITIONAL MEDIA

Small Cap Cycle?

Small cap investors have gone through a rough period. For the past several years, investors have anticipated an economic downturn. With these concerns, investors turned toward “safe haven” large cap stocks, which by and large can weather economic downturns and have significant trading volume should investors need to sell the stock. Notably, there is a sizable valuation disparity between the two classes, large cap and small cap, one of the largest since 1999. Some of the small cap stocks we follow trade at a modest 2.5 times Enterprise Value to EBITDA, compared with large cap valuations as high as 15 times. We believe the disparity is due to higher risk in the small cap stocks, given that some companies may not be cash flow positive, have capital needs, or have limited share float.

However, investors seem to have overlooked small cap stocks with favorable fundamentals. While small cap stocks are more speculative than large caps, many are growing revenues and cash flow, have capable balance sheets, and/or are cash flow positive. In our view, the valuation gap should resolve itself over time for attractive emerging growth stocks. Some market strategists suggest that small cap stocks trade at the most undervalued in the market.

Dan Thelen, Managing Director of small cap equity at Ancora Advisors, highlighted the valuation gap between small cap and large cap stocks during the economic panel at Noblecon 19. Mr. Thelen noted that investors haven’t recognized the risk mitigation efforts small cap companies have undertaken in the high interest rate environment. He believes that changes small cap companies have implemented are not reflected in stock prices and should be a tailwind moving forward.

2024 Advertising Outlook

In our advertising outlook for 2024, we take into consideration the perspective of Lisa Knutson, Chief Operating Officer (COO) of E.W Scripps. Ms. Knutson is on the frontline of the economy as one of the largest TV broadcasters in the country. As a speaker on the Noblecon 19 economic panel, she depicted the local and national advertising markets as a tale of two cities. Notably, Ms. Knutson highlighted resilience in local advertising and sequential improvement over the past few quarters in the auto advertising category. Additionally, she highlighted green shoots in local advertising, particularly in the services, home improvement and retail advertising categories. Importantly, political ad spend for the 2024 election cycle is expected to be approximately $10 billion, which is roughly a 13% increase from 2020. About half of the high margin political advertising dollars are expected to be spent with television broadcasters.

Digital Advertising – Decelerating Revenue Growth, But Faster Than Other Advertising Categories

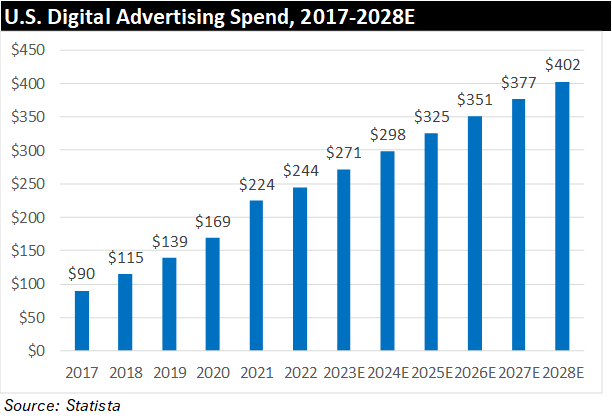

Digital advertising has been growing rapidly over the past several years, bolstered by chord-cutting trends and generally, by an increasingly digital world. Digital Advertising includes various categories of advertising, such as audio, video, influencer, search, banner, and others. According to Statista, U.S. Digital Advertising spending is expected to grow at 15% Compound Annual Growth Rate (CAGR), from 2017-2028, from $90.1 billion to $402.1 billion. The chart below illustrates U.S. Digital Advertising Spend from 2017 to 2028, which is inclusive of the various different sub-categories of digital advertising.

Specifically in 2024, U.S. digital advertising is expected to grow a healthy 10% above 2023 levels, according to Statista. There are some categories of digital advertising that are expected to grow especially fast in 2024, such as Connected TV (CTV) advertising, programmatic advertising, and influencer advertising. All three categorizations of digital advertising are estimated to have above-average growth in 2024. According to Statista, influencer advertising in the U.S. will grow at 14% in 2024, while, according to eMarketer, U.S. programmatic and CTV advertising will grow at 13% and 17%, respectively.

In our view, there are several key factors strengthening these verticals. For example, influencer advertising allows brands to reach younger demographics through personalities those demographics trust. Moreover, during a time when there is uncertainty around the future of cookies and other forms of User IDs for targeted advertising, influencer advertising offers an alternative vehicle for audience targeting. Google has indicated plans to no longer use cookies to deliver advertising in 2024, although the implementation of this plan has been delayed before. Additionally, we believe chord cutting is major factor in the growth of connected TV. We believe this could be a strong growth vertical for programmatic digital advertising.

Traditional Media

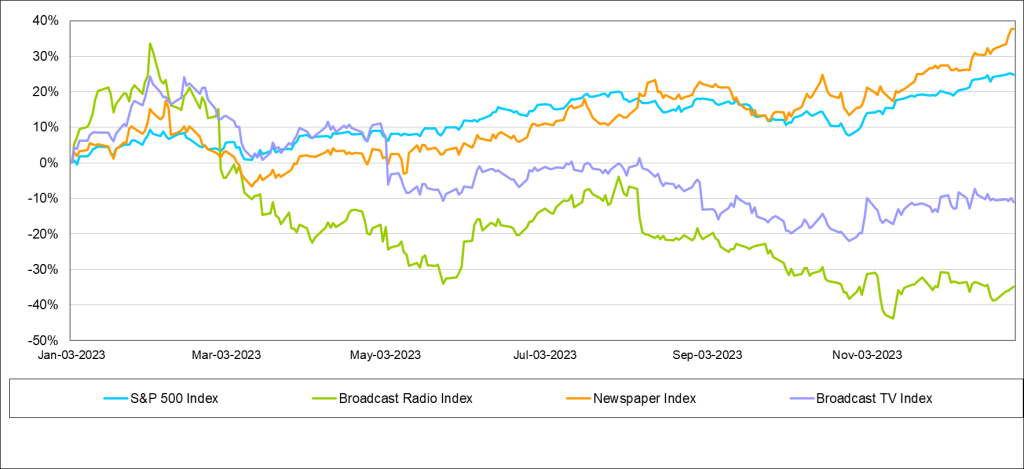

The Newspaper Index was the only traditional media sector that outperformed the general market in the past quarter and trailing 12 months. In the latest quarter, Newspaper stocks outperformed the general market, up 20% versus down 11% for the general market as measured by the S&P 500 Index. Notably, our index performances are market cap weighted, meaning larger cap stocks have a greater impact on index return than small cap stocks. In Q4, only two stocks in the Newspaper index, NYT and NWSA, posted positive returns. These are the largest cap stocks in the index. In Q4, NWSA and NYT were up 22% and 19%, respectively. For full-year 2023, four out of the five companies in the Newspaper index posted positive returns, with the strongest performers being NYT and NWSA, up 51% and 35%, respectively. The Broadcast TV Index was up a modest 5% for the fourth quarter and down 11% over the past year. The worst performing index over the last quarter was the Radio Broadcast index, down on 11% in the fourth quarter. Additionally, the Radio Index was the worst performing group over the last year as well, down 35%. While the Radio Broadcast Index and Broadcast TV Index had a tough year in 2023, we believe both indices should improve in 2024.

Broadcast Television

The Television industry had a tough year with soft core advertising and the absence of the year earlier political advertising. Television revenues are estimated to have declined as much as 20% in 2023 inclusive of the absence of year earlier political advertising. Total core television advertising is expected to have declined 3% in 2023, which excludes Political advertising, reflecting disproportionately weak national advertising and resilient local advertising. Importantly, television advertising accounts for less than 50% of total television revenue, with retransmission revenue largely accounting for the balance. With growth in retransmission revenue, we estimate that total television revenue declined roughly 10% in 2023.

We believe that revenue trends will improve in 2024 for the TV industry, supported by an influx of political advertising and moderating trends in core national advertising. Nonetheless, given the exceptional political advertising year that is expected, core advertising is expected to decline in 2024, with some advertising being displaced by the large volume of political. We anticipate that core advertising will decline roughly 2.3% in 2024, with total TV advertising up nearly 30% (including the influx of Political). Total television revenue, which includes retransmission revenues, are expected to increase roughly 20%.

We believe that the TV industry has some long-term fundamental headwinds, which include continued weak audience trends, cord cutting (which adversely affects retransmission revenue growth opportunities) and shifts in national advertising toward digital advertising. Offsetting these trends are Connected TV and prospects for new revenue opportunities offered by the new broadcast standard, ATSC 3.0. Importantly, the very high margin political advertising every even year allows the industry to reduce debt and/or return capital to shareholders.

Broadcast Radio

Based on our estimates and our closely followed companies, radio advertising is expected to have decreased 5.5% for the full year 2023 as illustrated in the chart below. This decline reflected the adverse impact of rising interest rates and significant inflation, which hurt many consumer-oriented advertising categories, as well as financials. In addition, we believe that radio struggled with some headwinds from declines in listenership, as many consumers continue to work remotely post Covid pandemic. Local advertising was more resilient than national advertising, which tends to be more economically sensitive.

We estimate that local advertising was down 6%, while national was down 19%. The results are expected to reflect the absence of political advertising from the year earlier biennial elections. Broadcast digital advertising was a bright spot, increasing 6%, largely offsetting the decline in national revenue.

Looking forward toward 2024, we expect radio advertising trends to improve throughout the year, with the expectation that December 2023 may have been the trough for this economic cycle. Both local and national advertisers should begin to anticipate improved economic conditions with the expectation that the Fed will lower interest rates late in the first quarter. Even though the economy is anticipated to continue to weaken in the first half 2024, advertisers may advertise to drive customer traffic in anticipation of improved economic conditions. We anticipate that the year will start off weak, with the first quarter 2024 revenue expected to be down, but at a more moderate decrease of between 3% to 4%. Notably, the industry does not receive a significant amount of political advertising in the first quarter.

In 2024, we expect consumer spending to soften, which will have an adverse effect on consumer-oriented advertising, particularly retail. Auto advertising is expected to buck that trend. In our view, auto manufacturers and dealers will likely increase advertising and promotions to lure consumers. Assuming lowered interest rates, we expect that the financial category should improve in the second half of the year as well. Revenues are expected to be second half weighted, with improving core advertising trends and the benefit of the influx of political advertising.

Radio does not typically receive a significant amount of political advertising, but it accounts for a meaningful 3% of total core advertising for the year. Political advertising largely falls in the third and fourth quarter. In addition, national advertising trends should improve in the second half as economic prospects improve. Digital advertising is expected to grow but more moderately than 2023, which is expected to be up 6%. We believe that Digital will increase near 5%, but some companies that have less developed digital businesses, should report faster growth.

In total, based on our closely followed companies, we anticipate Radio revenue growth of 5.6% in 2024. Our estimate is inclusive of our political advertising outlook.

This newsletter was prepared and provided by Noble Capital Markets, Inc. For any questions and/or requests regarding this news letter, please contact Chris Ensley

DISCLAIMER

All statements or opinions contained herein that include the words “ we”,“ or “ are solely the responsibility of NOBLE Capital Markets, Inc and do not necessarily reflect statements or opinions expressed by any person or party affiliated with companies mentioned in this report Any opinions expressed herein are subject to change without notice All information provided herein is based on public and non public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on their own appraisal of the implications and risks of such decision This publication is intended for information purposes only and shall not constitute an offer to buy/ sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice Past performance is not indicative of future results.

Please refer to the above PDF for a complete list of disclaimers pertaining to this newsletter.

JPMorgan Chase, the nation’s largest bank, reported a 15% decline in fourth quarter 2023 earnings on Friday, weighed down by a massive $2.9 billion fee related to the government takeover of failed regional banks last year.

The bank posted profits of $9.31 billion, or $3.04 per share, for the final three months of 2023. This compared to earnings of $10.9 billion, or $3.33 per share, in the same period a year earlier. Excluding the regional banking crisis fee and other one-time items, JPMorgan said it earned $3.97 per share in the fourth quarter.

Total revenue for the quarter rose 12% to $39.94 billion, slightly above analyst forecasts. The jump was driven by the bank’s acquisition of First Republic Bank in late 2023, higher net interest income, and increased investment banking fees.

“The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing,” said JPMorgan CEO Jamie Dimon in a statement. “These significant and somewhat unprecedented forces cause us to remain cautious.”

Dimon cited high inflation, rising interest rates, out-of-control government spending, supply chain disruptions, the war in Ukraine, and tensions in the Middle East as potential threats to the economic outlook.

For the full year 2023, JPMorgan posted record profits of nearly $50 billion, including $4.1 billion from its acquisition of First Republic. The deal instantly gave JPMorgan a leading position in serving wealthy clients in California and other coastal markets.

Smaller Competitors Squeezed

While JPMorgan has deftly navigated the rising rate environment, smaller regional banks have struggled as the Federal Reserve hiked rates aggressively to combat inflation. Many were caught holding lower-yielding assets funded by higher-cost deposits. This squeezed net interest margins.

The regional banking crisis came to a head in early 2023 as a wave of defaults and bank seizures overwhelmed the FDIC insurance fund. JPMorgan and other large banks were handed the bill, with the FDIC levying $18 billion in special fees on the industry to recapitalize the fund.

Specifically, JPMorgan paid a $2.9 billion fee in the fourth quarter related to the FDIC assessments. This was a major factor in the bank’s profit decline compared to a year ago.

JPMorgan Cautious Despite Solid Year

Despite posting record full-year earnings, Dimon and JPMorgan management struck a cautious tone in their earnings release. While U.S. consumers remain resilient for now, risks are mounting.

Inflation could prove stickier than anticipated, forcing the Fed to keep rates higher for longer. The war in Ukraine shows no signs of resolution. Middle East conflicts continue to elevate oil prices. And the U.S. government is racking up huge deficits, with no political will to cut spending.

For banks, this backdrop could pressure lending activity, loan performance, and capital levels. Mortgage rates are already above 7%, denting the housing market. Credit card delinquencies are edging higher. Corporate debt looks vulnerable as businesses face slower growth and input cost pressures.

All of this warrants a cautious stance until more clarity emerges later this year.

With JPMorgan having reported solid results for 2023, investors are now focused on the bank’s outlook for 2024 amid an expected shift in the interest rate environment.

On Friday’s earnings call, analysts will be listening closely to hear JPMorgan’s projections and commentary around key items that could impact performance this year:

Net interest income guidance for 2024. As the Fed cuts rates, net interest margins may compress. But higher loan volumes could offset this.

Expectations for credit costs and loan losses. While credit metrics are healthy now, a weaker economy could strain consumers and corporate borrowers.

Thoughts on impending hikes to capital requirements. Banks are hoping to reduce the impact of new rules on capital buffers.

M&A landscape. Does JPMorgan see opportunities for deals amid lower valuations?

Plans for excess capital deployment. Investors want to hear about potential increases in buybacks, dividends, and other uses.

JPMorgan entered 2024 with strong capital levels, putting it in position to boost shareholder returns even with new regulations. Investors will be listening to hear how management plans to leverage JPMorgan’s financial strength in the year ahead.

The bank’s 2024 outlook will be critical in determining whether its stock can build on last year’s big gains. JPMorgan was the top performing Dow stock in 2023, and investors are betting it can continue to drive profits in a more subdued rate environment.

In a move that could shape its future, BlackRock is making a huge bet on infrastructure investing with its $12.5 billion acquisition of specialist firm Global Infrastructure Partners (GIP).

The deal, announced Friday, includes $3 billion in cash and 12 million BlackRock shares to bring GIP’s $100+ billion infrastructure portfolio under its umbrella. With infrastructure booming globally, it plants BlackRock’s flag in an alternative asset class that offers stability and strong cash flows.

For Larry Fink, BlackRock’s founder and CEO, the deal provides a growth engine and caps a storied career. At 71 years old, Fink has not yet named his successor. This acquisition generates buzz around President Rob Kapito and COO Rob Goldstein as potential heirs apparent.

It also brings infrastructure investing veterans from GIP into BlackRock’s senior ranks. GIP Chairman Bayo Ogunlesi will join BlackRock’s board, while co-founders like ex-World Bank President Jim Yong Kim provide invaluable experience.

Why Infrastructure, Why Now?

Infrastructure has become increasingly attractive to institutional investors, particularly those with long-term liabilities to fund. The assets provide inflation protection, and the regulated nature of many infrastructure projects leads to predictable cash flows even during economic downturns.

Swelling demand for infrastructure also powers opportunity and growth. E-commerce and supply chain modernization require massive investment in logistics and transportation assets like airports, seaports, rail, and warehouses. The global energy transition is expected to necessitate trillions in spending on renewable power, battery storage, transmission lines, and more. And booming data usage makes digital infrastructure such as cell towers and data centers a near-certainty for major funding.

BlackRock saw the writing on the wall. With interest rates still relatively low by historical standards, it pulled the trigger on a transformative infrastructure deal rather than waiting for valuations to potentially rise further. GIP’s assets also provide diversification and inflation mitigation to complement BlackRock’s vast holdings of stocks and bonds.

For forward-thinking infrastructure investors, BlackRock’s whopper of a deal validates the long-term potential of the sector. And it positions the asset management titan to capitalize on infrastructure demand in both developed and emerging markets for decades to come.

Rejuvenating Revenues

The move into infrastructure also helps reinvigorate BlackRock’s revenues. With rock-bottom interest rates in recent years limiting fee income, BlackRock has searched for ways to accelerate growth. The company manages over $10 trillion in assets but has seen minimal increase in revenue since 2018.

Alternative investments like infrastructure represent a potential answer. They generally command higher management fees while also offering incentive fees based on investment performance. That combination bodes well for BlackRock’s results.

BlackRock has dipped its toe into alternatives over the past decade via real estate, hedge funds, private equity, and other strategies. But the GIP deal vaults infrastructure to the forefront of BlackRock’s alternatives platform. Expect heightened focus and more resources dedicated to infrastructure deals in the future.

With the Fed lifting rates this year, BlackRock also has a short-term revenue boost at its back. Higher interest rates allow BlackRock to charge more for managing cash and fixed income, its largest assets. BlackRock’s 8% increase in fourth quarter earnings served as an appetizer. The GIP acquisition is the main course in its long-term growth agenda.

Fink Caps Career with Legacy Deal

Larry Fink has run BlackRock since its inception in 1988, guiding it to become the world’s preeminent money manager. But the end of his tenure looms. While no retirement plans have been announced, Fink is 71 years old.

The GIP deal thus shapes up as a culminating move to put his stamp on BlackRock’s future. Shortly after the acquisition was announced, Fink said, “This is one of the most exciting transactions we’ve ever completed.”

What excites Fink and BlackRock is GIP’s expertise, global reach, and the long runway for infrastructure investing. Fink pulled the trigger on a legacy deal that can steer BlackRock’s course beyond when he ultimately steps down.

The acquisition also stirs up increased speculation on who could succeed the respected CEO. As BlackRock makes infrastructure integral to its future, the deal elevates infrastructure veterans like GIP Chairman Bayo Ogunlesi. COO Rob Kapito and President Rob Goldstein also see their standing boosted.

While the stock dipped slightly on Friday’s news, the deal primes BlackRock for sustainable growth. Shareholders will be monitoring the integration, but early reviews applaud Fink and BlackRock for their foresight and ability to execute.

Inflation picked up more than anticipated in December, dimming hopes that the Federal Reserve can soon pause its interest rate hiking campaign.

The Consumer Price Index (CPI) rose 0.3% in December compared to the prior month, according to Labor Department data released Thursday. Economists surveyed by Bloomberg had projected a 0.2% monthly gain.

On an annual basis, inflation hit 3.4% in December, accelerating from November’s 3.1% pace and surpassing expectations for 3.2% growth.

The uptick keeps the heat on the Fed to maintain its aggressive monetary tightening push to wrestle inflation back towards its 2% target. Investors were optimistic the central bank could stop hiking rates and even start cutting them in early 2023. But with inflation proving sticky, the Fed now looks poised to keep benchmark rates elevated for longer.

“This print is aligned with our view that disinflation ahead will be gradual with sticky services inflation,” said Ellen Zentner, chief U.S. economist at Morgan Stanley, in a note.

Core Contributes to Inflation’s Persistence

Stripping out volatile food and energy costs, the core CPI increased 0.3% in December, matching November’s rise. Core inflation rose 3.9% on an annual basis, up slightly from November’s 4.0% pace.

The core reading came in above estimates for a 0.2% monthly gain and 3.8% annual increase. The higher-than-expected core inflation indicates that even excluding food and gas, costs remain stubbornly high across many categories of goods and services.

Shelter costs are a major culprit, with rent indexes continuing to climb. The indexes for rent of shelter and owners’ equivalent rent both advanced 0.5% in December, equaling November’s rise.

Owners’ equivalent rent attempts to estimate how much homeowners would pay if they rented their properties. This category accounts for nearly one-third of the overall CPI index and over 40% of core CPI.

With shelter carrying so much weighting, persistent gains here will hinder inflation’s descent. Supply-demand imbalances in the housing market are delaying a moderation in rents.

Used Cars See Relief; Insurance Soars

Gently easing price pressures showed up in the used vehicle market. Used car and truck prices edged up just 0.1% in December following several months of declines. In November, used auto prices fell 0.2%.

New vehicle prices also cooled again, dipping 0.1% versus November’s 0.2% decrease. The reprieve comes after a long bout of supply shortages weighed on auto affordability.

But motor vehicle insurance blindsided with its largest annual increase since 1976, vaulting 20.3% higher over the last 12 months. In November, the insurance index had risen 8.7% year-over-year.

Food Index Fluctuates

Food prices have been especially volatile, reacting to supply chain disruptions and geopolitical developments like the war in Ukraine. The food index rose 0.1% in December, down from November’s 0.5% increase.

The index for food at home slid 0.1% last month, reversing course after four straight monthly gains. Egg prices spiked 8.9% higher in December, building on November’s 2.2% surge. The egg index has skyrocketed 60% year-over-year.

But not all grocery aisles saw rising costs. Fruits and vegetables turned cheaper, with the index dropping 0.6% as supply conditions improved.

Bigger Picture View

The faster-than-expected inflation in December keeps the Fed on course to drive rates higher for longer to manage price pressures. Markets are still betting officials will engineer a soft landing and start cutting interest rates by March.

But economists warn more patience is needed before declaring victory over inflation. “Overall, the December CPI report reminds us that inflation will decline on a bumpy road, not a smooth one,” said Jeffrey Roach, chief economist at LPL Financial.

Until clear, convincing signs of disinflation emerge, the Fed looks unlikely to pivot from its aggressive inflation-fighting stance. The CPI report illustrates the complexity of the inflation picture, with some components moderating while others heat up.

With shelter costs up over 6% annually and services inflation staying elevated, the Fed has reasons for caution. Moderately higher inflation won’t necessarily prompt more supersized rate hikes, but it may prolong the current restrictive policy.

Investors longing for a Fed “pivot” may need to wait a bit longer. But the war against inflation rages on, even with the December CPI report threatening to squash hopes of an imminent policy easing.

The long-awaited arrival of SEC-approved bitcoin exchange-traded funds (ETFs) promises to open the floodgates for mainstream investor exposure to the world’s largest cryptocurrency. After years of rejections and delays, the SEC appears ready to finally allow spot bitcoin ETFs that hold the digital asset directly.

This stamp of regulatory approval positions bitcoin to go fully mainstream in 2024. Financial advisors can now more easily allocate client assets into bitcoin through the familiar ETF wrapper. Major financial institutions and retirement accounts like 401(k)s will likely broaden access as well.

For crypto-curious investors, a spot bitcoin ETF offers a simpler way to gain exposure without dealing with digital wallets and exchanges. But navigating this new ETF landscape won’t be easy. Here’s what investors need to know:

Shop Around for Fees

Dozens of issuers have spot bitcoin ETF filings awaiting SEC approval. With so much competition, expense ratios are plunging. Several issuers like ARK Invest and Bitwise have waived fees completely for six months. Others range from 0.25% to over 1%. Pay close attention to fee structures, which will vary greatly between issuers.

Monitor Premiums and Discounts

While bitcoin itself is highly liquid, new ETFs may deviate from their net asset value or trading price. Factors like redemption policies and authorized participant rules could cause ETF shares to trade at small premiums initially. Keep an eye on premium/discount behavior, favoring ETFs that demonstrate efficient trading and tight spreads.

Consider Futures-Based ETFs Too

Spot bitcoin ETFs remove the futures curve drama, but don’t ignore futures-based funds. The ProShares Bitcoin Strategy ETF (BITO) has built a solid track record since launching in October 2021. Futures-based strategies could still make sense for tactical traders and institutional investors, despite added complexity.

Temper Short-Term Expectations

Bitcoin ETFs are unlikely to immediately trigger massive inflows from retail and institutional investors. Assets may reach $10 billion this year, but that’s tiny compared to bitcoin’s $900 billion market cap. Widespread adoption will take time as investors wait and see how these new products function.

Beware the Crypto Bubble

While bitcoin has rebounded from its 2022 lows, speculative excess still persists. Hundreds of altcoins with no utility or differentiators have billion dollar valuations. Cryptocurrency markets remain prone to volatility and hype cycles. ETFs offer exposure, but be wary of parabolic rallies.

Think Long-Term Store of Value

The bitcoin blockchain and protocol aren’t going away. Only 21 million BTC can ever be mined. Consider using ETFs as part of a diversified portfolio focused on bitcoin’s potential as a long-term store of value, similar to gold. But also be prepared for 50%+ drawdowns during times of market stress.

Look Beyond Bitcoin

Bitcoin ETFs are just the beginning. The SEC has yet to approve ETFs holding other major cryptocurrencies like ether and solana. If these are eventually permitted, diversified crypto ETFs could become an enticing one-stop shop. Institutional investors are already trading cryptocurrency index funds tracking a basket of assets.

Understand the Tax Implications

Cryptocurrency remains subject to complex U.S. tax rules that classify it as property. Investors must pay capital gains taxes whenever selling at a profit, including cashing out of ETFs at a higher bitcoin price. Long-term tax rates are more favorable. Financial advisors can help craft tax-smart crypto strategies.

See How Institutions Respond

Large asset managers and financial institutions will need time to evaluate these new products before allowing clients access. Their embrace could drive billions in inflows. But if major players bar access or remain cautious, retail adoption may lag. Pay attention to their stance.

Approval of spot bitcoin ETFs removes a huge roadblock to mainstream crypto investment. But it’s still early days. As investors navigate this rapidly evolving landscape, following prudent portfolio strategies and avoiding FOMO will be key to capitalizing on this milestone.