Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Turn the Page. With the appointment of Ken Peterman as CEO and President, Comtech is entering a new chapter, in our view. With a track record of building and creating sustainable, profitable growth, we believe Mr. Peterman will be able to capitalize on the high-growth opportunity set in front of Comtech.

Convergence. A key theme from Mr. Peterman is the belief of a coming “convergence” between the satellite and space communications and terrestrial and wireless communications, or Comtech’s two core markets. With an unsurpassed skill set across both of these areas, we believe Comtech is uniquely positioned to capitalize on this coming convergence.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FQ2 2023 reported for period ending July 31, 2022. As a clinical stage company, ChitogenX reported no revenues in the quarter. Expenses, both G&A and R&D, were lower than our quarter expectations, offset by higher share-based compensation expense. R&D expenses were reduced by a $500,000 (all figures in C$) grant received in May 2022 to advance the meniscus repair indication. The result was a net loss of $1.363 million vs. expected $1.59 million. Loss per share was $0.03 vs. expected loss of $0.03.

ChitogenX is pushing well beyond orthopedics. The rebranding recently instituted was more than a simple name change. The Company is leveraging its chitosan biopolymer technology expertise to attack a much larger global regenerative medicine market, including areas like oncology, neurology, and cardiology. Regenerative medicines have an inherent inability to stick to repair sites and ChitogenX seeks to resolve the problem with their ChitogenX Biopolymer. We expect the Company to establish partnerships, license the technology, or seek grants in these additional markets.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

PDS Biotech Announces FDA Meeting Results. PDS Biotech announced the outcome of an End-of-Phase 2 meeting with the FDA to determine the clinical development pathway for PDS0101. In the meeting, data from the interim analysis of the VERSATILE-002 trial testing PDS0101 in HPV-positive head-and-neck cancer was evaluated and regulatory guidance provided. Although the trial is still ongoing, the efficacy and safety data will allow moving into a Phase 3 pivotal study ahead of schedule during 2023.

VERSATILE-002 Showed Strong Response Rates. The VERSATILE-002 Phase 2 trial was designed to test PDS0101 in HPV-positive cancer of the head and neck in combination with the checkpoint inhibitor pembrolizumab (Keytruda, from Merck). As discussed in our Research Note reviewing the data at the ASCO conference last May 31, the tumor response rate (shrinkage of 30% or more) was 41.2% (7 out of 17 patients). This compares with published data showing 19% response rate for checkpoint inhibitors alone. Progression-free survival (PFS) at nine months was 55.2% and overall survival (OS) was 87.2%.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Energy stocks, as measured by the XLE Energy Index, were essentially flat during the third quarter rising 0.1%. The performance was impressive given overall market weakness. The S&P Composite Index declined 5.0% during the quarter. What makes the performance even more impressive is the fact that spot oil prices declined 25% during the quarter. We believe energy stocks remain an attractive investment and are an important part of a diversified investment portfolio.

WTI prices peaked at $120 per barrel in the first week of June. Since then, prices have declined in response to signs of a global economic slowdown. Near month oil future contracts are now below $80 per barrel. We believe recent weakness largely reflects demand concerns and foreign currency changes but is not a condition of oversupply. The domestic rig count remains at less than half peak levels. What’s more, rig count has leveled off in recent months in response to the decline in oil prices.

Production has risen to 90% of peak, but it has been done by harvesting the low-hanging fruit. When oil prices began falling early in 2020, there was an increase in Drilled Uncompleted (DUC) wells. When prices rose, drillers focused on completing DUCs. With the number of DUCs having fallen in half, future supply increases will be more difficult. If demand does not decrease in reaction to a slowing economy, domestic production may be hard pressed to meet demand. If worries about a recession are overblown and demand increases, there’s a good chance oil prices will be back at a price of $120 or even higher.

Energy industry fundamentals remain strong. The recent drop in oil prices does not concern us as long-term prices are still above the levels assumed in our financial and valuation models. Energy company cash flow generation is high, and companies are facing the envious position of trying to decide what to do with the cash. Debt levels have been pared down and managements are reluctant to initiate/raise dividends in case the industry goes into a down cycle forcing them to reverse course. Share repurchase remains a viable option especially if energy stocks continue to be weak alongside the overall market.

Energy Stocks

Energy stocks, as measured by the XLE Energy Index, were essentially flat during the third quarter rising 0.1%. The performance was impressive given overall market weakness. The S&P Composite Index declined 5.0% during the quarter. What makes the performance even more impressive is the fact that spot oil prices declined 25% during the quarter. We believe energy stocks remain an attractive investment and are an important part of a diversified investment portfolio.

Oil Prices

Oil prices rose steadily over a two-year period beginning the spring of 2020. WTI prices peaked at $120 per barrel in the first week of June. Since then, prices have declined in response to signs of a global economic slowdown as governments raise interest rates to fight inflation. Near month oil future contracts are now below $80 per barrel.

Figure #1

We believe recent weakness largely reflects demand concerns and foreign currency changes but is not a condition of oversupply. Historically, oil prices are lower when the dollar is stronger. This is because most oil suppliers, including international suppliers, demand payments in dollars.

The domestic rig count remains at less than half peak levels. According to Baker Hughes, there were 764 active rigs as of September 23, 2022, as compared to 1600 in 2015. What’s more, rig count has leveled off in recent months in response to the decline in oil prices.

Figure #2

Rig count is one way to forecast future supply. While only half the peak number of rigs are active, that does not mean that production is half of peak levels. In fact, as the chart below shows, domestic daily production surpassed 2015 peak rig production levels in 2018. Production declined sharply when oil prices fell in 2020 but have recovered to a point where production has reached 90% of peak production. The increased production demonstrates an improved productivity per well as drillers better tailor drilling techniques to individual formations.

Figure #3

But before we chalk up increased production to improved technology, let’s look at one more chart. The chart below shows the number of drilled but uncompleted (DUC) wells against active rigs. The chart shows that the number of uncompleted wells has declined sharply the last two years as the active rig count has grown. When oil prices began falling early in 2020, drillers continued drilling but often did not complete the wells. This led to a large increase in the number of DUC wells. When prices started rising in the summer of 2020, drilling returned. However, drilling was largely focused on completing or reworking wells.

Figure #4

The implication of a declining DUC count is that the industry is running out of low hanging fruit. Future drilling will need to focus on wells that are likely to have a lower production rate per rig than what we have witnessed recently. Declining production could exasperate already low inventory levels (see chart below). Thus, if demand does not decrease in reaction to a slowing economy, domestic production may be hard pressed to meet demand. If worries about a recession are overblown and demand increases, there’s a good chance oil prices will be back at a price of $120 or even higher.

Figure #5

Natural Gas Prices

Natural gas prices tend to track oil prices but with a few distinctions. Natural gas demand and supply is less global than oil. Imports (and now exports) of liquefied natural gas represent a small portion of domestic supply and demand. Secondly, natural gas is used primarily for space heating. That means demand is more seasonal. It also means demand can be affected by weather conditions. On the other hand, natural gas demand is less affected by general economic conditions than oil. As the chart below shows, natural gas prices do not seem to be affected by recession concerns as compared to oil prices.—-

Figure #6

Source: Natural Gas Intelligence

Summer is usually a quiet time for natural gas prices. Wells are producing more gas than is demanded, and gas is put in inventory. As is the case with oil, inventory levels are running below historical averages as we approach the point of withdrawing from inventory. This bodes well for natural gas prices remaining at current historical high levels and perhaps even rising higher.———- page break ———-

Figure #7

Outlook

Energy industry fundamentals remain strong. The recent drop in oil prices does not concern us as long-term prices are still above the levels assumed in our financial and valuation models. Energy company cash flow generation is high, and companies are facing the envious position of trying to decide what to do with the cash. Debt levels have been pared down and managements are reluctant to initiate/raise dividends in case the industry goes into a down cycle forcing them to reverse course. Share repurchase remains a viable option especially if energy stocks continue to be weak alongside the overall market.

We also believe the case for smaller cap energy stocks is strong. Major oil companies are facing increasing pressure to focus on renewable energy. While the majors are increasing drilling, they are doing so in a controlled manner as they also invest in green energy. Smaller cap energy companies are less tethered and often able to acquire and exploit properties being ignored by the majors. If our belief that a world-wide recession is already factored into energy prices is correct, small cap energy companies will be in the best position to take advantage of any price increase.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lowering 4Q Projections. We are taking a more conservative view of the fourth quarter given the impact of Ian on Florida. Orion has a number of projects in the area and we expect to see a push back given the need for more humanitarian efforts. We are now forecasting revenue of $165 million for the quarter, down from a prior $168 million estimate, adjusted EBITDA of $8.55 million, down from $10.55 million, and breakeven EPS, down from a prior $0.03 EPS estimate. For the full year, we are now at revenue of $709.5 million and adjusted EBITDA of $28.1 million.

But More Future Work? The devastation wrought by Ian is undeniable, not just in Florida but also in the Carolinas. This unfortunate event, however, could create substantial future work for Orion. While it is way too early yet to determine, typically such storms end up being a net positive in terms of new work.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FFO, NFFO, and AFFO Projections. We modestly adjusted our projections for Funds From Operations, Normalized Funds From Operations, and Adjusted Funds From Operations. Our prior estimates reflected a larger estimate for depreciation and amortization and other than we are now using. We are now projecting third quarter FFO at $0.31 per share, versus a prior $0.36, NFFO of $0.31 versus $0.37, and AFFO of $0.31 versus a prior $0.32.

No Change in Business Outlook. We are not currently expecting any major change in the business environment and our projections for revenue and EPS remain unchanged. ICE ADP has risen from below 20,000 in the spring to nearly 26,000 in September, while Southwest Border encounters exceeded 200,000/mth since March and likely will be up over 32% from the full fiscal year 2021.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Fundamental Reasons the Strength in Precious Metals May Continue

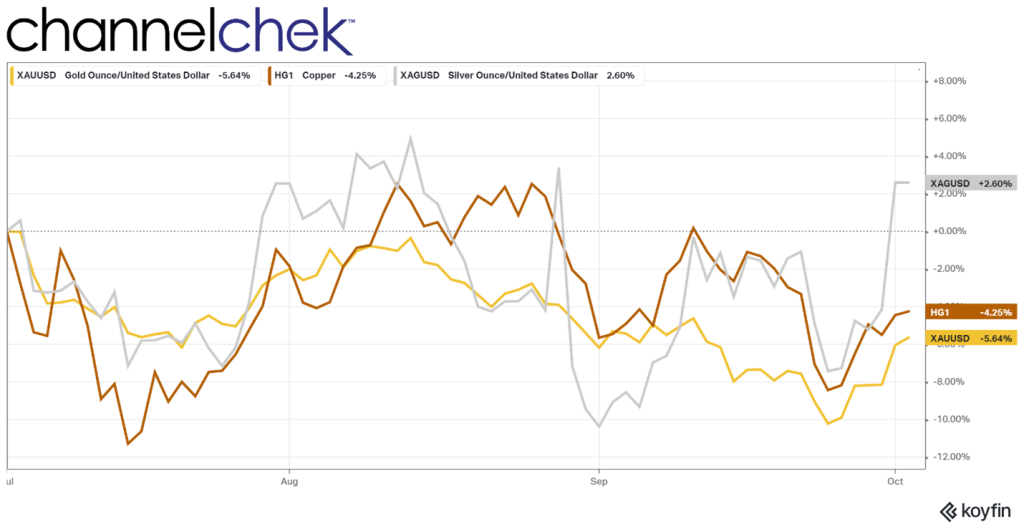

What’s happening with precious metals? Silver has been outshining gold the past few days as the rally in both precious metals (PM) has grabbed the attention of investors and perhaps caught those that were short silver off guard. Why are the metals rising, can the strength last, and what is the longer-term outlook for PM?

Silver reached a six-week high in the first week of October, and gold is at its highest level in three weeks. As financial markets are becoming more uncertain, the two metals are showing they never really lost their safe-haven status. The concerns have just not been high enough for many to rotate out of the investments they were in. The move to what has always been viewed as the highest level of safe, gold and silver. This rotation follows months of movement to $ U.S. dollar-denominated securities. The heightened level of safety was inspired by the media being focused on a potential financial crisis in Europe and discussions of Russia unleashing a nuclear weapon in Putin’s attempt to annex Ukraine.

Silver, Gold and Copper performance since September 1. Source: Koyfin

As if the words “nuclear bomb” aren’t enough to send some investors taking a larger allocation in safe-haven assets, there are rumors circulating that the global investment bank Credit Suisse may be in serious financial trouble. For many market participants, the rumblings about an investment bank having problems are reminiscent of 2007, the rumors of Bear Stearns, and the market troubles that followed. Revisiting the activity of the precious metals market that followed in 2008, silver outperformed copper, which outperformed gold.

As silver and gold rise, many speculators that were comfortable with short positions are finding themselves forced with the decision to decide to purchase to close out their short positions. Active hedge funds and other money managers will often play precious metals against the U.S. dollar. With the dollar at a 20-year high, the sentiment around metals was negative. If this is the beginning of a longer rotation into PM, the rotation could build into a strong short squeeze. Short covering serves to strengthen prices.

Other Fundamentals

Prior to Monday’s 7% increase in the price of silver and the 3% increase in gold, both with strong follow-up on Tuesday, some analysts were becoming more positive on the metals and miners category. In his quarterly Metals & Mining Review and Outlook, released on Channelchek pre-market Monday, Mark Reichmann, Sr. Research Analyst, wrote, “While higher rates and a strong U.S. dollar pose significant headwinds for gold, an inflection point may be reached as investors seek to preserve value amid deteriorating economic conditions, increasing geopolitical uncertainty, and market volatility.”

Reichmann seems to be long-term positive on metals, thinking gold and silver may turn first; he wrote, “Precious metals prices may strengthen in advance of industrial metals. Therefore, investors may desire to lean into precious metals mining names to benefit from a positive shift in investor sentiment.” He continued, “While it may take longer for industrial metals to recover, an eventual return to economic growth could result in strong prices due to potential supply and demand imbalances.”

For a complete list and the most current research reports of producers of precious and industrial metals companies covered by Mark Reichmann, visit his analyst webpage here.

Take Away

The move earlier this year toward U.S. dollar denominated assets, to capture higher yields and low sovereign risk has been an ongoing investment trend since at least March. With the newly recognized potential of additional turmoil entering the market psyche, including Russia and whether they would use the bomb, and whether the recent about-face for England’s monetary policy indicates deep trouble beneath the financial world’s surface has created further allocations to precious metals.

The suddenness of the move may have caught some large investors who have been bearish on silver and gold to make unexpected decisions on short positions they had been carrying. This short-squeeze is likely contributing to the strength of both gold and silver as it plays out.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

More Awards. In the last week of the Federal government’s fiscal year, Great Lakes was the recipient of additional work. The Department of Defense contract awards reports four additional significant wins totaling a cumulative $109.8 million of potential new business.

Sole Awards. The Company received a $26.6 million award for dredging with work to be performed in Savannah, Georgia; Brunswick, Georgia; Wilmington, North Carolina; Morehead City, North Carolina; and Charleston, South Carolina; a $12.195 million contract for dredging with work to be performed in Irvington, Alabama; and a $21.531 million award for beach re-nourishment in Cape May, New Jersey.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Mining companies outperform broader market. During the third quarter, mining companies (as measured by the XME) declined 2.1% compared to a loss of 5.3% for the S&P 500 index. The VanEck Vectors Gold Miners (GDX) and Junior Gold Miners (GDXJ) ETFs were down 11.9% and 7.9%, respectively. Gold, silver, copper, zinc, and lead futures prices fell 6.8%, 6.2%, 8.5%, 8.8%, and 0.4%, respectively. The commodity price declines reflect expected impacts of Federal Reserve monetary policy on interest rates, U.S. dollar strength, and the economic environment.

Outlook for precious metals. The U.S. Dollar Index rose 7.1% during the third quarter, while the yield on a 10-year treasury note increased from 3.0% to 3.8% as of September 30. While higher rates and a strong U.S. dollar pose significant headwinds for gold, an inflection point may be reached as investors seek to preserve value amid deteriorating economic conditions, increasing geopolitical uncertainty, and market volatility. While down 7.9% year-to-date through September 30, the price of gold has remained relatively resilient this year despite challenging headwinds. Not being able to benefit from strengthening gold prices, investors have focused more on silver’s industrial applications which make it more sensitive to economic expectations.

Industrial metals demand expected to remain challenged. The decline in industrial metals prices reflect concerns about economic growth in the U.S. and abroad. While the long-term investment case for owning industrial metals mining companies remains favorable, industrial metals prices may remain challenged into 2023.

Putting it all together. Precious metals prices may strengthen in advance of industrial metals. Therefore, investors may desire to lean into precious metals mining names to benefit from a positive shift in investor sentiment. While it may take longer for industrial metals to recover, an eventual return to economic growth could result in strong prices due to potential supply and demand imbalances.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Bassett Furniture Industries, Incorporated manufactures, markets, and retails home furnishings in the United States. The company operates in three segments: Wholesale, Retail, and Logistical Services. It is involved in the design, manufacture, sourcing, sale, and distribution of furniture products to a network of company-owned and licensee-owned Bassett Home Furnishings (BHF) retail stores, as well as independent furniture retailers; and wood and upholstery operations. As of September 16, 2017, the company operated a network of 91 company-and licensee-owned stores. It also provides shipping, delivery, and warehousing services to customers in the furniture industry. In addition, the company owns and leases retail store properties. It also distributes its products through other multi-line furniture stores, Bassett galleries or design centers, specialty stores, and mass merchants. Bassett Furniture Industries was founded in 1902 and is based in Bassett, Virginia.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Results. Revenue for the fiscal third quarter ended August 27, 2022 was $118 million, up 12.5% over the prior year period. Wholesale revenue rose 8.3% to $79 million, while Retail revenue rose 21.0% to $70.9 million. Excluding a $4.6 million one-time gain, operating income was $6.1 million, up 22.1%. Bassett reported net income from continuing operations of $7.8 million, or $0.84 per share, compared to net income from continuing operations of $3.4 million, or $0.35 per share, in the prior year. We had forecast revenue of $120 million and EPS from continuing operations of $0.65.

Retail the Star. Once again, Bassett’s retail network was the quarter’s star performer, with “best ever” third quarter deliveries of $70.9 million and $4.5 million of operating profit. Segment operating profits in the first nine months exceed any full year performance to date.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Axcella is a clinical-stage biotechnology company pioneering a new approach to treat complex diseases using compositions of endogenous metabolic modulators (EMMs). The company’s product candidates are comprised of EMMs and derivatives that are engineered in distinct combinations and ratios to restore cellular homeostasis in multiple key biological pathways and improve cellular energetic efficiency. Axcella’s pipeline includes lead therapeutic candidates in Phase 2 development for the treatment of Long COVID and non-alcoholic steatohepatitis (NASH), and the reduction in risk of overt hepatic encephalopathy (OHE) recurrence. The company’s unique model allows for the evaluation of its EMM compositions through non-IND clinical studies or IND clinical trials. For more information, please visit www.axcellatx.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Axcella Announced Positive Interim NASH Results. An interim analysis from the Phase 2b EMMPACT Study of AXA1125 in non-alcoholic steatohepatitis (NASH) showed improvements in measures of liver fibrosis and liver fat. The data presented was from patients who had been treated for 12 and 24 weeks of the 48-week treatment period. The study is continuing as planned, and we believe the interim data raise the probability of success for the trial.

Study Design and Analysis. The EMMPACT study was designed to test two doses of AXA1125 against placebo. Patients receive either placebo, low dose (45.2g/day), or high dose (67.8g/day) twice daily for 48 weeks. It has a target enrollment of 270 patients with biopsy-confirmed Stage 2 or Stage 3 NASH, divided into three arms with 90 patients each. The interim analysis used non-invasive tests to evaluate reduction in liver fibrosis and inflammation.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Nobel Prizes, Election Outcomes and Sports Championships – Prediction Markets Try to Foresee the Future

Who will win Nobel Prizes in 2022? Wikipedia posits a handful of contenders for Physiology or Medicine, about 20 different possible winners for the Peace Prize and several dozen potential winners of the Literature Prize. But since the Swedish Academy never announces nominees in advance, there are few insights indicating who will win, or even if the eventual winner is on a given list.

Are there ways to predict the future winners?

The Delphi approach, named after the oracle in ancient Greece, gathers multiple rounds of opinions from a group of experts to generate a prediction. Gambling firms provide betting odds on the likelihood that specific competitors will win. Crowdsourced competitions, such as the Yahoo Soccer World Cup “Pick-Em,” have participants predict individual contest winners and then aggregate the results.

Another approach is a prediction market that provides insight into what people expect will happen in the future by creating a stock market-like environment to capture the “wisdom of the crowd.” Groups and crowds often are collectively smarter than individuals when many independent opinions are combined.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Daniel O’Leary, Professor of Accounting and Information Systems, University of Southern California.

As an accounting and information systems professor at the University of Southern California, I investigate issues related to the crowd both in my research and in my teaching. Here’s how prediction markets harness what the crowd thinks to forecast the future.

The Wisdom of the Market

In prediction markets, participants buy and sell stocks. Each stock’s price is tied to a different event happening in the future. Information about the future is captured in the stock prices.

For instance, in a prediction market focused on the Nobel Peace Prize, maybe Greta Thunberg is trading at $0.10 while Pope Francis is trading at $0.15, and the stocks for the entire group of candidates add up to sum to $1. The prices reflect the traders’ aggregated beliefs about the probability of their winning – a higher price means a higher perceived likelihood of winning.

Examples of Prediction Markets

Anyone can get in on the prediction game by trading on one of these markets or even just checking out which stocks are up or down.

Prediction markets have various ways of setting stock prices. The Iowa Electronic Markets took following approach during the 2020 U.S. presidential election:

Stock DEM2020 pays off $1 if the Democratic candidate wins, and $0 otherwise,

Stock REP2020 pays off $1 if the Republican candidate wins, and $0 otherwise.

The stock prices capture the probabilities of each candidate winning, in two mutually exclusive events. If the price of DEM2020 is $0.52, then that is treated as the probability of that event occurring – a 52% chance. If DEM2020 is $0.52, then REP2020 is $0.48.

Prediction markets may use real money, or they can use play money. Google’s market used what it called “Goobles,” while the Hollywood Stock Exchange uses Hollywood Dollars. The Iowa Electronic Markets and PredictIt, both sponsored by universities, use real money. Researchers have found that there are no differences in the performance of markets using real money versus those using play money.

Although using play money makes it possible for many people to participate, one potential challenge for prediction markets that don’t use real money is gaining and maintaining interested participants. Despite using different devices to keep up engagement, such as leader boards indicating who has accumulated the biggest portfolio, there is literally no money on the table to keep participants interested in the market.

Market participants who know more about the game might better predict winners. Image Credit: Marco verch (Flickr)

Participants Bring Their Knowledge to the Market

Prediction markets and crowdsourcing do not function in a vacuum.

Researchers have found that information about events finds its way into the prediction processes from various sources. For example, when I analyzed the relationship between the betting odds and the Yahoo Pick-Em crowd’s guesses for the 2014 FIFA World Cup, I found that there was no statistical difference between the proportion of correct guesses in each. My conclusion is that either the crowd’s guesses incorporated the betting odds information or the crowd’s guesses added up to the same result by some other means.

Generally, prediction markets use play money or are run by non-profit universities to study markets, elections and human decision making. Although gambling houses can take bets for many activities, external prediction markets are more restricted in the activities they can be used to investigate, and are typically limited to elections. However, internal prediction markets – run within a corporation, for instance – can explore almost any topic of interest.

Typically, prediction markets function better with informed participants. Although using so-called inside information is illegal in some markets, including the New York Stock Exchange, there generally are no such limitations in prediction markets, or other crowdsourcing approaches. If those with inside information were to participate in a prediction market, it would likely lead to more accurate stock prices, as insiders make trades informed by their knowledge. However, if others find out that a participant has inside information, then they may very well try to gain access to that info, follow the insider’s actions or even decide to leave the unfair market.

The accuracy of prediction markets depends on many factors, including who is in the market, what their biases are and how heterogeneous the participants are. Accuracy can also depend on how many people are in the market – more is generally better – and the extent to which they are informed about the events of interest.

Researchers have found that prediction markets have outperformed polls in presidential elections roughly 75% of the time. But accurate results are not guaranteed. For example, prediction markets did not correctly predict that Donald Trump would win the U.S. presidency in 2016.

Who Will be in Stockholm for the Ceremony?

In 2011, Harvard University economics faculty had a real-money prediction market site, referred to as “the world’s most accurate prediction market.” The site had been used for predicting the Nobel Prize in Economics, but Harvard advised the site to shut down.

I couldn’t find any current public prediction markets active for the 2022 Nobel Prizes.

For the moment, perhaps the closest to participating in a Nobel prediction market would be to place a bet at one of the gambling houses that takes bets on the Nobel Prizes. Or find a Nobel Prize Pick-Em site, propose such an event to an existing prediction market or build your own prediction market using some of the available software.

Inflation Still Surprisingly Strong and Economy Weak

Two important numbers were released on the last day of September. One was based on old news but significant in its finality; it’s the final revision to GDP for the second quarter. The next is viewed as the Fed’s preferred inflation gauge, the PCE deflator. The final GDP number will make it more difficult for public officials or pundits to suggest we can avoid a recession in 2022, and the second did not give any hope that the Fed will have any reason to change course on tightening.

A Recession By Any Other Name

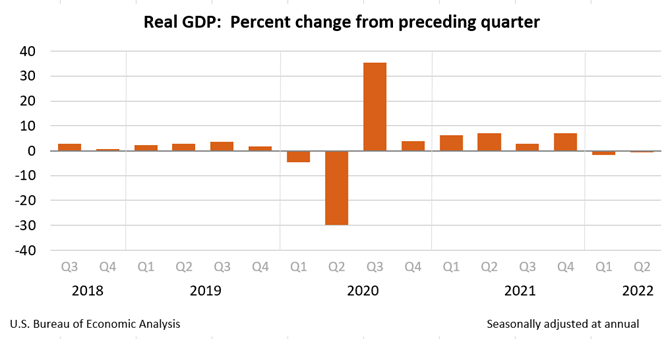

Gross domestic product (GDP) is the indicator that reflects the amount of output produced quarterly in a country. In the U.S., the Bureau of Economic Analysis (BEA) releases two estimates of quarterly GDP, known as the advance and preliminary estimates, in the two months before the release of the final number. So until the final number prints, the number GDP measure is subject to revision.

On September 30, 2022, the Final GDP report for the second quarter was released by the BEA. The report shows that GDP decreased at an annual rate of 0.6 percent in the second quarter of 2022 (table 1). This decline in economic output follows a decline of 1.6% in the first quarter of 2022.

Do two-quarters of a receding economy, based on GDP, indicate the U.S. is in the recessionary part of the business cycle? Most textbooks would agree with that definition. However, there is a Business Cycle Dating Committee within the National Bureau of Economic Research (NBER) that determines and labels where the nation is within the economic cycles; they have not made any declaration.

So far, in 2022, the economy has not experienced any economic growth. If the six months of contraction is eventually deemed an official recession, it will thus far have been a shallow one, characterized by strong employment.

Price Increases Higher than Expected

Inflation is still on many investor’s radar. The Fed is targeting reducing inflation to its 2% target. The inflation measure they use for this target is the PCE Deflator. That measure was released this morning, and it validates the aggressive actions being taken by the Federal Reserve. And suggests the Fed has a lot more work to do.

The personal consumption expenditures price index (PCE), which the Fed targets at 2%, rose 6.2% in August from a year earlier, the Commerce Department reported. Underlying inflation, as measured by a core reading that excludes food and energy prices, rose 4.9% from 4.7% previously.

These numbers are well in excess of the Fed’s target and seemingly trending upward. Expectations are the Fed will provide up to another 150 bp increase (1.50%) over the coming months. This would cause the Fed Funds rate to trade near 5%. There is nothing in today’s release that would likely cause expectations to change.

Stagflation?

High inflation and negative growth have many repeating the word “stagflation”. Stagflation has one more element missing, which is high unemployment. The current economic conditions in the U.S. include high demand for workers, this shortage actually helps feed into the inflation the Fed is trying to tame.

Take Away

The economy contracted slightly in the second quarter of 2022. The decline in production was smaller than measured during the first quarter. Federal Reserve policymakers saw one more reason to keep applying the economic brake pedal by taking money out of the economy, increasing upward rate pressures. The Fed caused rates to rise from 40-year lows faster than any time since the 1980s.

Stock market participants are factored into the Fed’s policy only to the extent that market moves may impact inflation or employment. The markets (stocks, bonds, real estate, gold) are negative on the year. There are some who suggest the Fed will use this as a signal to alter policy, if the Fed bowed to any of the markets listed here, the sign of weakness might actually cause a market collapse in stocks and bonds.