Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Mining companies trail the broader market. During the second quarter, mining companies (as measured by the XME) declined 4.4% compared to a gain of 8.3% for the S&P 500 index. The VanEck Vectors Gold Miners (GDX) and Junior Gold Miners (GDXJ) ETFs were down 6.9% and 9.7%, respectively. Gold, silver, copper, and zinc futures prices fell 2.0%, 5.6%, 8.2%, and 15.6%, respectively, while lead increased 1.2%. Year-to-date through June 30, gold futures prices were up 5.7%, while silver was down 5.1%. Copper, lead, and zinc prices declined 1.40%, 3.1%, and 19.9%, respectively.

Precious metals headwinds. While gold prices crossed $2,000 an ounce during the second quarter on the back of turmoil in the banking sector, concerns moderated, and the resiliency of the U.S. economy seemed to favor risk-on assets. Additionally, rising short-term interest rates have provided investors with an alternative haven for their funds. During the January, March, and May Federal Open Market Committee (FOMC) meetings, the Federal Reserve served up three 25 basis point rate increases and paused in June keeping the target federal funds rate in the range of 5.00% to 5.25%. Expectations are for additional increases in 2023. Precious metals may be challenged as real yields rise, along with the potential for a stronger U.S. dollar. While we expect precious metals prices to remain at levels that are economic for producers, we expect some weakness in pricing during the second half of 2023.

Outlook for industrial metals. While the long-term investment case for owning industrial metals mining companies remains favorable, it is still too early to offer a bullish call due to near-term concerns about economic growth in the U.S. and abroad. Longer-term secular trends, including electrification, remain supportive of supply and demand fundamentals for copper.

Putting it all together. While well-diversified portfolios should have exposure to precious metals, mining equities may offer a stronger current alternative to bullion. In our opinion, junior companies remain attractive based on valuation, and we expect industry consolidation to increase as senior producers seek to replenish reserves and resources. Longer-term, global central banks could increase gold reserves as they seek to move away from their reliance on the U.S. dollar as a reserve currency which could be supportive of gold prices. While the near-term outlook for industrial metals could be negatively impacted by near-term macroeconomic factors, an eventual return to economic growth could result in strong prices due to potential supply and demand imbalances.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Takeaways from the Reuters Global Energy Transition Event

All videos now live on demand!

The Takeaway Series is available exclusively to Channelchek members. It’s totally free to join the community, just click the join button at the top of the page, or the Register button below.For best results, log in to your Channelchek account above before viewing the videos.

Noble Capital Markets Senior Research Analyst Michael Heim provides his takeaways from the event, plus all the fireside chats with c-suite energy executives. All in one click.

On the heels of the announcement that NobleCon19, Noble Capital Markets 19th Annual Emerging Growth Equity Conference, will be held at FAU, and the achievement of the Owls basketball team making it to the Final Four, Florida Atlantic University College of Business’ Executive Education program earned a prestigious global endorsement in the 2023 Financial Times rankings for open enrollment professional education programs.

FAU ranked No. 2 in the United States and was the only university in Florida and one of only seven in the U.S. to be honored. The rankings are considered the gold standard for executive education coursework across the globe.

“It’s clear that we are making a difference in the professional advancement of all our students,” said Daniel Gropper, Ph.D., dean of FAU’s College of Business. “I am very proud of our students, faculty and staff for making this possible.”

FAU also ranked No. 1 in the U.S. and No. 4 in the world for female participation and No. 17 globally for overall satisfaction. Financial Times establishes the rankings using student feedback, course design, faculty, teaching methods and facilities.

FAU’s high-quality offerings include the most diversified selection of more than 60 national and international certification and professional development programs, said Vegar Wiik, executive director of FAU Executive Education. He added that a new state-of-the-art building, the Schmidt Family Complex for Academic and Athletic Excellence, is equipped with the latest technology that allows FAU to offer top-notch programs and corporate training. “We are thrilled that this December the facility will transform into NobleCon19, with 100+ public company executive teams and the large audience expected to learn more about them,” Wiik said. “And with the early announcement that the 43rd President of the United States, George W. Bush will headline, the excitement continues to build.”

In addition to hosting NobleCon19, FAU’s Edu-Vantage Partner Program, which works with businesses, corporations and organizations to provide a high-quality educational strategy for fulfilling their employee education packages, established partnerships with JM Family Enterprises and NextEra Energy, parent company of Florida Power & Light, to offer full-time associates full tuition for both undergraduate and graduate degrees and certifications.

NobleCon19 is scheduled for December 3-5, 2023, at FAU College of Business, Executive Education in Boca Raton, Florida. Although institutional investors, licensed brokers and accredited investors will be in attendance, NobleCon19 is open to all individuals and organizations interested in learning more about these companies.

To receive NobleCon agenda updates and registration opportunities, join Channelchek.com, Companies with market capitalization of $3 billion or less wishing to learn more about presenting at NobleCon19 can Inquire Here.

About Noble Capital Markets

Noble Capital Markets, Inc. was incorporated in 1984 as a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed emerging growth companies through investment banking, wealth management, trading & execution, and equity research activities. Over the past 39 years, Noble has raised billions of dollars for companies and published more than 45,000 equity research reports. For more information, visit www.noblecapitalmarkets.com or email contact@noblecapitalmarkets.com.

About Florida Atlantic University Florida Atlantic University, established in 1961, officially opened its doors in 1964 as the fifth public university in Florida. Today, the University serves more than 30,000 undergraduate and graduate students across six campuses located along the southeast Florida coast. In recent years, the University has doubled its research expenditures and outpaced its peers in student achievement rates. Through the coexistence of access and excellence, FAU embodies an innovative model where traditional achievement gaps vanish. FAU is designated a Hispanic-serving institution, ranked as a top public university by U.S. News & World Report and a High Research Activity institution by the Carnegie Foundation for the Advancement of Teaching. For more information, visit www.fau.edu.

And President Bush is only one of the events at your Alma Mater! NobleCon19 will feature 100+ executive team presentations and breakouts, provocative panels and keynotes, world-class networking events, and the exclusive conversation with President George W. Bush, moderated by Noble’s Director of Research. By registering below, we will keep you updated on all the happenings at and around Noble Capital Markets’ 19th Annual Emerging Growth Equity Conference – NobleCon19… for the first time hosted by Florida Atlantic University.

The objective of NobleCon19 is to build awareness for lesser-known companies that may shape the future of technology, medicine, manufacturing, retail, transportation, distribution, and natural resources. Most of the companies presenting will be public, thereby offering investment opportunities. Although institutional investors, licensed brokers and accredited investors will be in attendance, NobleCon19 is open to all individuals and organizations interested in learning more about these companies. And that, of course, includes you as an FAU Alumni!

Space is limited and demand is high. Noble is offering a special consideration for FAU Alumni to attend the entire conference and/or an exclusive invitation to attend the President George W. Bush fireside chat at little or no cost. To be considered for this extremely rare opportunity, and to receive NobleCon19 agenda updates, register below. All the companies that will attend NobleCon19 are featured on this site as well as thousands of other small-cap companies. Attendance is prioritized by the date you register. BTW Channelchek is an open-access secure site with no cost to join, and no pitches to purchase anything, ever.

Noble Capital Markets (“Noble”) announced today that the 43rd President of the United States and Founder of the George W. Bush Presidential Center will be featured at NobleCon19, Noble’s 19th Annual Emerging Growth Conference to be held at Florida Atlantic University, College of Business, Executive Education, December 3-5, 2023, in Boca Raton, Florida. Noble’s Director of Research, Michael Kupinski will moderate the hour-long fireside chat with President Bush.

George W. Bush served as 43rd President of the United States of America from 2001 to 2009. As Commander in Chief, President Bush worked to expand freedom, opportunity, and security at home and abroad. His Administration reformed America’s education system, restored robust private-sector economic growth and job creation, protected our environment, and pursued a comprehensive strategy to keep America safe after the terrorist attacks on September 11, 2001.

In this more casual and personable format, President Bush will discuss his time in the Oval Office and the challenges facing our nation today.

In addition to admittance to the President Bush fireside chat, attendees of NobleCon19 will be exposed to 100+ executive teams from all across North America, through formal presentations, Q&A sessions, organized breakouts and selected one-on-one meeting. Topical panel presentations, to-be-announced keynotes and networking events, and “The After” first-day evening event featuring world-class entertainment rounds out the agenda.

The objective of NobleCon19 is to build awareness for emerging growth companies that may shape the future of technology, media, telecom, medicine, manufacturing, retail, transportation and distribution, and natural resources. Most of the companies presenting will be public, thereby offering investment opportunities. Although institutional investors, licensed brokers and accredited investors will be in attendance, NobleCon19 is open to all individuals and organizations interested in learning more about these companies.

To receive NobleCon agenda updates and registration opportunities, join Channelchek.com, Noble’s online investment community, listing more than 6,000 public emerging growth companies. This is an open-access site with no cost (ever) to join. Companies with market capitalization of $3 billion or less wishing to learn more about presenting at NobleCon19 can Inquire Here.

Please note: Some sessions of this conference are closed to the media with no personal recording, photography, or note-taking permitted.

About Noble Capital Markets

Noble Capital Markets, Inc. was incorporated in 1984 as a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed emerging growth companies through investment banking, wealth management, trading & execution, and equity research activities. Over the past 39 years, Noble has raised billions of dollars for companies and published more than 45,000 equity research reports. www.noblecapitalmarkets.comcontact@noblecapitalmarkets.com

About Florida Atlantic University

Florida Atlantic University, established in 1961, officially opened its doors in 1964 as the fifth public university in Florida. Today, the University serves more than 30,000 undergraduate and graduate students across six campuses located along the southeast Florida coast. In recent years, the University has doubled its research expenditures and outpaced its peers in student achievement rates. Through the coexistence of access and excellence, FAU embodies an innovative model where traditional achievement gaps vanish. FAU is designated a Hispanic-serving institution, ranked as a top public university by U.S. News & World Report and a High Research Activity institution by the Carnegie Foundation for the Advancement of Teaching. For more information, visit www.fau.edu.

Hundreds of public company executive guest speakers. Headliners like three of the most recognizable celebrity investors on the planet. AI-Focused keynote panel featuring Zack Kass. One-on-one meetings. The After Hangar Party. NobleCon20. The premier in-person multi-sector emerging growth equity conference of the year. – December 3-4, Boca Raton, Florida

Registered Channelchek Members enjoy $250 off Attendee Registration. Use code CCMEMBERDISC. Not a member? Click the button below to join the community. It’s absolutely free to join.

December 3-4, 2024 @ Florida Atlantic University, College of Business Executive Education, Boca Raton, FL

Featured Event – a 95 minute fireside chat and pitch competition (featuring hopeful entrepreneurs selected by Noble from the Florida Atlantic student and alumni communities) featuring 3 of the original Sharks from ABC’s Shark Tank

Artificial Intelligence keynote panel featuring Zack Kass, former Head of Go-to-Market OpenAI / ChatGPT

Hundreds of emerging growth public company senior executives

Topical panel presentations

Expanded one-on-one meeting schedule

Disco-themed edition of ‘The After” – held in conjunction with Money Channel NYC / Moneyball Networking and Goliath Resources – at the Privaira Private Aviation Hangar, Boca Raton Airport

Takeaways from the National Association of Broadcasters’ NAB Show

All videos now live on demand!

The Takeaway Series is available exclusively to Channelchek members. It’s totally free to join the community, just click the join button at the top of the page, or the Register button below.For best results, log in to your Channelchek account above before viewing the videos.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Key takeaways from the NAB. Media investors are unpacking the information from the National Association of Broadcaster’s (NAB) convention. While there are promising new technologies that are sure to create shiny new objects to catch investor’s attention, particularly AI, the chatter is about the current advertising environment. Looking for the key takeaways? Sign up here for the virtual conference on April 27th.

Digital Media & Technology:Head fake? Every one of Noble’s Internet and Digital Media Indices not only finished the quarter up, but significantly outperformed the S&P 500. The best performing index was Noble’s Social Media Index, which increased by 70% in the first quarter of 2023, followed by Noble’s Ad Tech Index (+31%), MarTech Index (+30%), and Digital Media Index (+18%).

Television Broadcasting: Weak current revenue trends.While auto advertising appears to be faring better, the weight of the economic challenges appear to be causing further moderation in advertising. Will auto and, potentially Political, carry the second half 2023 revenue performance?

Radio Broadcasting: All out of love.The industry is reeling from a Wall Street research downgrade to an underperform on iHeart Media, which sent all radio stocks tumbling. Some stocks performed better than others. What’s behind the downgrade and which stocks performed better?

Publishing:Advertising takes a hit. After a period of moderating revenue trends, Publishers reported a weakened advertising environment. The downturn was due to Print advertising which took a nose dive. As a result, publishing companies implemented another round of expense cuts to bolster cash flow. There is a bright spot as Digital continues to perform strongly.

Overview

The NAB Show Stopper

Media investors are unpacking all of the information from last week’s National Association of Broadcaster’s (NAB) convention. There is a lot to digest given that there were over 1,400 exhibits, 140 new exhibitors this year. Because of the overwhelming number of exhibitors, many that go to Vegas for this annual convention do not go to the convention floor. It is a shame. There was a lot to see and learn. As Noble’s Media & Entertainment Analyst I walked the convention floor, which covers 4.6 million square feet of exhibit halls and meeting rooms. I stopped by booths and taped presentations to explain the new technologies, the plan for implementation of new services, and the prospect for revenue monetization. One important demonstration focused on the new broadcast standard, ATSC 3.0, the hope for a bright future for the television industry. This new standard should allow the industry to become more contemporary in terms of how its audience consumes video and information. In addition, it offers the ability for the industry to participate in new revenue streams, including Datacasting, which may become bigger than Retransmission revenue in the future.

In addition to touring the floor, I attended NAB panel discussions and hosted meetings with media management teams in a fireside chat format to discuss current business trends, the new technologies (including Artificial Intelligence (AI) and the new broadcast standard). In addition, these C-suite management teams provided their key takeaways from the NAB convention and offered why they participated in the conference this year. These discussions are available to you for free on Channelchek.com on April 27th in a virtual conference. In this upcoming Channelchek Takeaway Series on the NAB Show, I offer my key takeaways, including the current advertising outlook, my take on the monetization of the new technologies and what media investors should do now given the current economic and advertising environment. Your free registration to this informative event is available here.

This report highlights the performance of the media sectors over the past 12 months and past quarter. Overall, media stocks struggled in the past year, but there has been some improved quarterly performance, particularly in Digital Media and Broadcast Television, discussed later. All media stocks are struggling to offset losses over the course of the past year with trailing 12 months stocks down in the range of 5% on the low end to down 68% on the high end. The best performing sector in the past 12 months were Social Media stocks, down 5% versus the general market decline of 9% over the comparable period.

In the first quarter, stock performance was mixed. The best performers in the traditional media sectors were Broadcast Television stocks, up nearly 10% versus the general market which increased 7% in the comparable period. But, the individual TV stock performance reflected a different story, explained later in this report. The worse performer for the quarter were the radio stocks, driven by a Wall Street downgrade of one of the leading radio broadcasters. The Digital Media stocks had another good performance. We believe that stock performance will be a roller coaster for at least another quarter or two as the weight of the Fed rate increases begin to adversely affect the economy.

While National advertising has remained weak, we believe that Local advertising is now beginning to moderate as well. The Local advertising weakness appears to be in the smaller markets as well as the larger markets. This is somewhat different than the most recent economic cycles whereby the smaller markets were somewhat resilient. It seems that the smaller markets are feeling the adverse affects from inflation, rising employment costs and tightening bank credit. In our view, the disappointing advertising outlook likely will cause second quarter revenue estimates to come down, creating a difficult environment for media stocks. As such, we encourage investors to be opportunistic and take an accumulation approach to building positions for the prospective economic and advertising improvement. Our favorites have digital media exposure, given that we expect Digital Advertising (while softening as well) will be more resilient than traditional advertising mediums. Our favorites include Travelzoo (TZOO), Townsquare Media (TSQ), Harte Hanks (HHS), E.W. Scripps (SSP), and Direct Digital (DRCT).

Digital Media

Head fake?

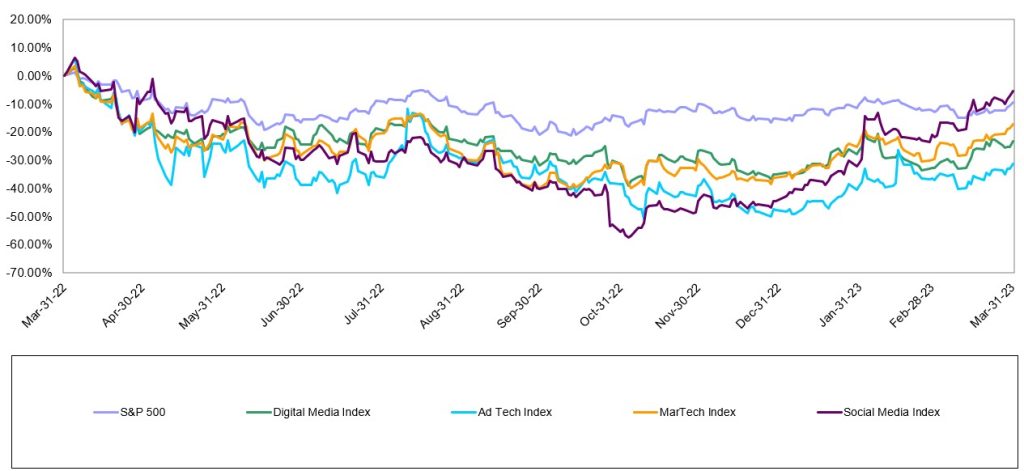

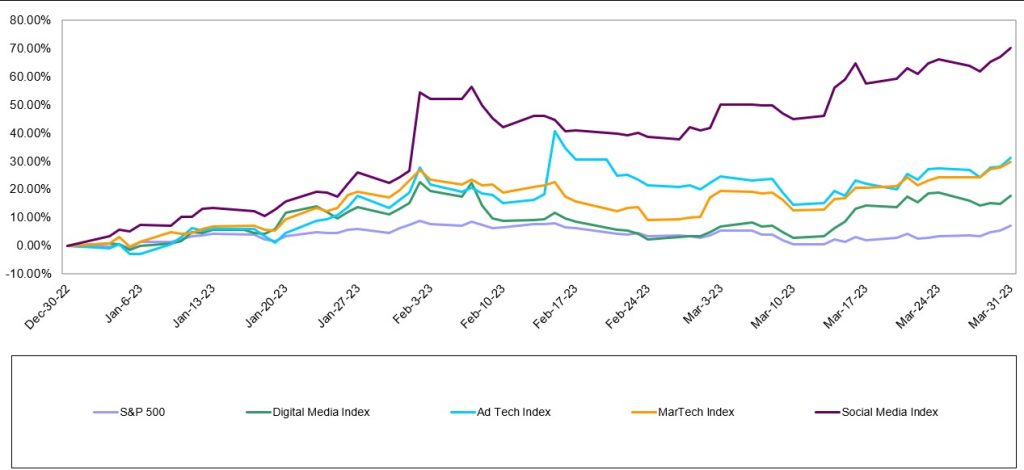

Last quarter we wrote that the S&P 500 increased for the first time since the fourth quarter of 2021 and that we were beginning to see signs of life in Noble’s Internet and Digital Media Indices as well. Those signs of life continued to bear fruit throughout the first quarter, as every one of Noble’s Internet and Digital Media Indices not only finished the quarter up, but significantly outperformed the S&P 500. Figure #1 LTM Digital Media Performance highlights that many of the Digital Media sectors are now approaching year earlier levels given the most recent favorable performance. The best performing index was Noble’s Social Media Index, which increased by 70% in the first quarter of 2023, followed by Noble’s Ad Tech Index (+31%), MarTech Index (+30%), and Digital Media Index (+18%).

Figure #1 LTM Digital Media Performance

Source: Capital IQ

Noble’s Indices are market cap weighted, and we attribute the strength of the Social Media Index to its largest constituent, Meta Platforms (META; a.k.a. Facebook) whose shares increased by 76% in the first quarter. Figure #2 Q1 Digital Media Performancehighlights the first quarter performance for the digital stocks.Meta’s management stirred interest in the shares from its 4Q 2022 earnings call when they spent most of their time talking about “efficiency”, which investors interpreted to mean that Meta was newly focused on profitability. After a relatively disastrous 3Q 2022 earnings call, after which shares fell by 25%, the company demonstrated on its 4Q 2022 earnings call that it clearly had gotten the message: investors were not enamored about the company’s plans in October 2022 to spend billions of dollars to develop its Metaverse initiatives. Rather, on its fourth quarter call, management focused on driving its short form video initiative, Reels (i.e., becoming more TikTok like), reducing its headcount by reducing layers of management, lowering its operating expenses and reducing its capital expenditures. Investors applauded this newfound focus on profitability and shares rebounded from a low of $88.90 per share in early November to $211.94 at the March quarter-end.

The next best performing index was Noble’s Ad Tech Index which increased by 31% during 1Q 2023. Fourteen of the 23 stocks in the index were up in the first quarter. Standouts during the quarter were Integral Ad Science (IAS; +62%) and Perion Networks (PERI; +56%). Integral Ad Science exceeded expectations in its fourth quarter results and guided to better-than-expected results in 1Q 2023. The company continues to expand its product suite, scale its social media offerings (i.e., for TikTok) and is well positioned to continue to benefit from the shift from linear TV to connected TV (CTV). Perion shares continued their winning: Perion was the only ad tech stock whose shares were up in 2022. Perion’s 56% increase in 1Q 2023 reflected beat on both revenues (by 2%) and EBITDA (by 10%) as well as improved guidance for 1Q 2023. Perion’s profitability increased significantly in 2022, with EBITDA nearly doubling (+90%) from 2021 ($70M) to 2022 ($132M).

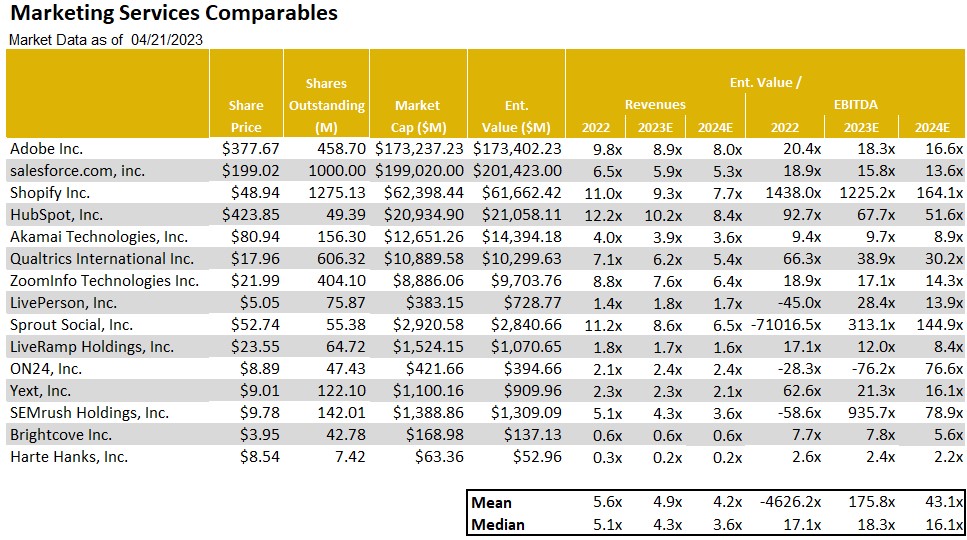

Noble’s MarTech Index increased by 30% with 14 of the 22 stocks in the index posting increases in 1Q 2023. The best performing stocks were Qualtrics (XM; +70%) Sprinklr (CXM; +59%), Salesforce (CRM; +51%), Hubspot (HUBS; +48%) and Yext (YEXT; +47%). Qualtrics agreed to be acquired for $12.5 billion by Silver Lake and the Canadian Pension Plan Investment Board, which came at a 73% premium to its 30-day volume weighted stock price. Sprinklr beat revenue expectations and significantly beat EBITDA expectations (doubling the Street expectations) and guided to a current year forecast that focuses more on efficiency and profitability.

MarTech stocks have been victims of their own success. Two years ago at this time the sector was trading at 11.3x forward revenue estimates, and a year ago the group was trading at 6.5x forward revenues. Today the group trades at 4x forward revenues and investors appear to be wading back into the sector. Figure #3 Marketing Tech Comparables highlights the compelling stock valuations.One of the laggards in the sector has been Harte Hanks (HHS), which declined 20% in the first quarter. We believe that the shares have not gained traction following the successful rebound toward profitability in 2022. The shares advanced a powerful 136% in 2022 from lows in May to highs achieved in August 2022. Since that time, investors appear to be taking chips off the table. In our view, the HHS shares appear to be oversold. Its business appears to be resilient. Given the recent weakness in the shares, the shares appear to be undervalued and offer a favorable risk reward relationship. As such, the HHS shares are among our favorites in the sector.

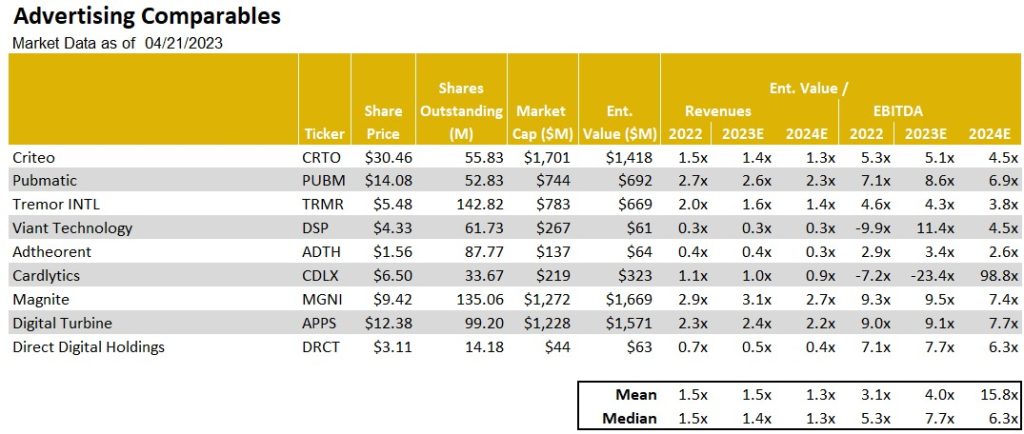

Another one of our current favorites is Direct Digital Holdings (DRCT). As Figure #4 Advertising Tech Comparables illustrates, the DRCT shares trade in line with the averages for the group at roughly 5.4 times 2024 adj. EBITDA. Notably, the company recently restated upward its 2022 full year revenue and adj. EBITDA results. Given the favorable operating momentum, we raised our full year 2023 and 2024 revenue and adj. EBITDA estimates, keeping our previous growth estimates. With the higher 2024 adj. EBITDA, we tweaked upward our price target from $5.50 to $6.00. Given a favorable fundamental outlook and compelling stock valuation, we view the shares as among our favorites.

Finally, Noble’s Digital Media Index, while lagging that of its digital peers at an 18% increase, significantly outperformed the S&P 500 (+7%), with a broad based recovery in which 9 of the sector’s 11 stocks increased during 1Q 2023. The best performing stock was Spotify (SPOT; +69%), whose revenues fell short of expectations by less than 1%, significantly beat consensus Street EBITDA expectations by $58M and more importantly pivoted towards demonstrating operating leverage. Spotify, which posted an EBITDA loss of nearly $500 billion in 2022, is expected to generate $650 billion in EBITDA in 2024, according to Street estimates. A deteriorating ad market in 2022 combined with higher interest rates likely prompted the company to shift its priorities to running a profitable company and doing it more quickly and with some urgency. The second best performing stock was Travelzoo (TZOO; +36%), as the company’s 4Q 2022 revenues and EBITDA increased by 31% and 328%, respectively. Notably, Travelzoo’s EBITDA came in 58% higher than Street consensus. The company appears to be benefiting from pent up travel demand for travel and management highlighted the opportunity for margin expansion in the coming quarters. Given the favorable outlook, we raised our price target to $10. Near current levels, the TZOO shares appear to offer above average returns and we reiterate our Outperform rating.

Figure #2 Q1 Digital Media Performance

Source: Capital IQ

Figure #3 Marketing Tech Comparables

Source: Eikon, Company filings & Noble estimates

Figure #4 Advertising Tech Comparables

Source: Eikon, Company filings & Noble estimates

Traditional Media

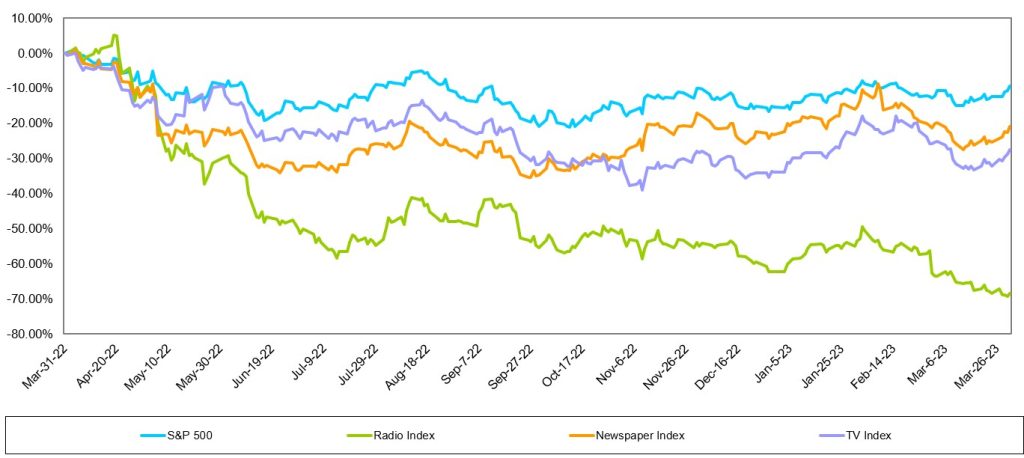

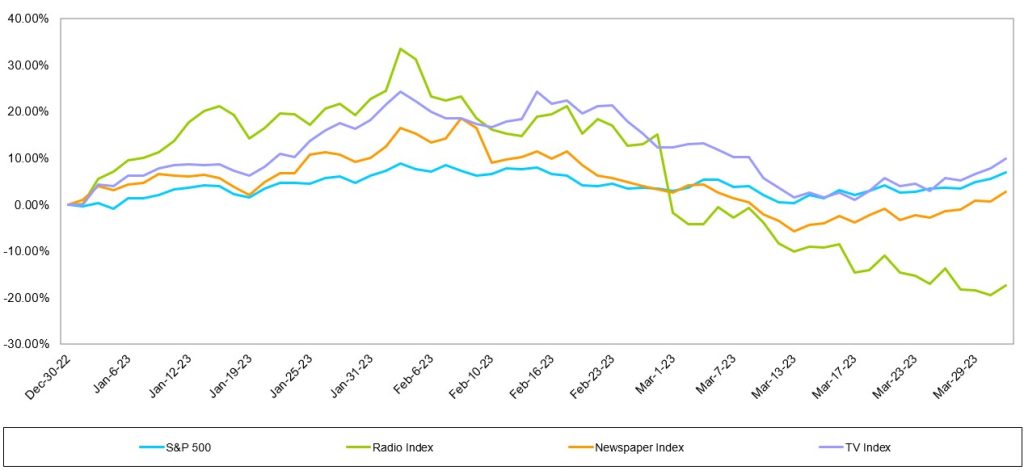

As Figure #5 LTM Traditional Media Performance illustrates, these stocks have struggled to gain sea legs, trending lower over the course of the past year. All traditional media sectors have underperformed over the past year, with Radio the poorest performing group. As Figure #6 Q1 Traditional Media Performance illustrates, only the TV Broadcast stocks edged out the general market performance in the latest quarter.

Figure #5 LTM Traditional Media Performance

Source: Capital IQ

Figure #6 Q1 Traditional Media Performance

Source: Capital IQ

Television Broadcast

Weak current revenue trends

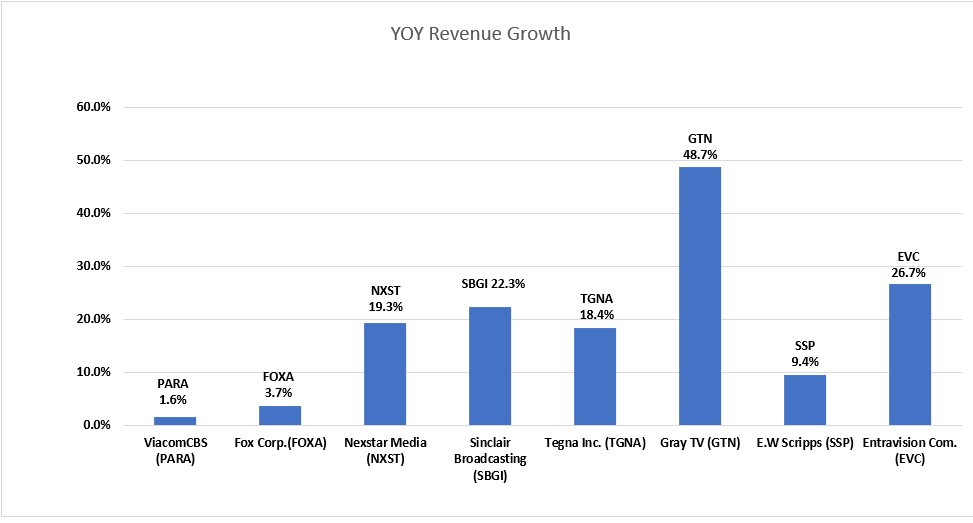

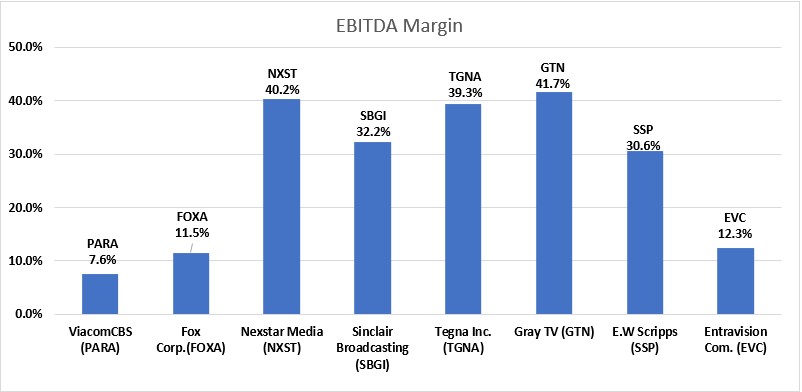

As illustrated in the previous chart, the TV stocks outperformed the general market in the first quarter. This market cap weighted index masked the performance of many poor performing stocks in the quarter. Sinclair Broadcasting (SBGI; up 10%), Entravision (EVC; up a strong 26%), and Fox (FOX; up 12%) were among the best performing stocks and favorably influenced the TV index in the quarter. But, there were many poor performing stocks including E.W. Scripps (SSP; down 29%), Gray Television (GTN; down 22%) and Tegna (TGNA; down 20%). We believe that there was heightened interest in Entravision given its favorable Q1 results which was fueled by its fast growing Digital business. Figure #7 TV Q4 YoY Revenue Growth illustrates the Entravision’s Q4 revenue performance was among the best in the industry. While Entravision was among the best revenue performers, its margins are below that of its peer group as illustrated in Figure #8 TV Q4 EBITDA Margins. This is due to the accounting treatment of its Digital revenues given that it is an agency business. Given that Digital represents roughly 80% of the company’s total company revenue, we plan to put the EVC shares into the Digital Media sector to more accurately reflect its business. The poorer performing stocks are among the higher debt levered in the industry. As such, we believe the underperformance reflects concern of a slowing economy and investors flight to quality in the sector.

We do not believe that we are out of the woods with the TV stocks and the market is expected to be volatile. The advertising environment appears to be deteriorating given weakening economic conditions. There are bright spots which include some improvement in the Auto category. Dealerships appear to be stepping up advertising given higher inventory levels. In addition, broadcasters appear optimistic about Political advertising, which could begin in the third quarter 2023. There is a planned Republican presidential candidate debate scheduled in August. As such, there is some promise that candidates will advertise in advance of that debate and into the fourth quarter given the early primary season. We do not believe that Political and Auto will be enough to offset the weakness in National and in the weakening Local category. In our view, Q2 and full year 2023 estimates are likely to come down. Furthermore, we believe that broadcasters will be shy about predicting Political advertising even into 2024 given the past disappointments in management forecasts in the last Political cycle.

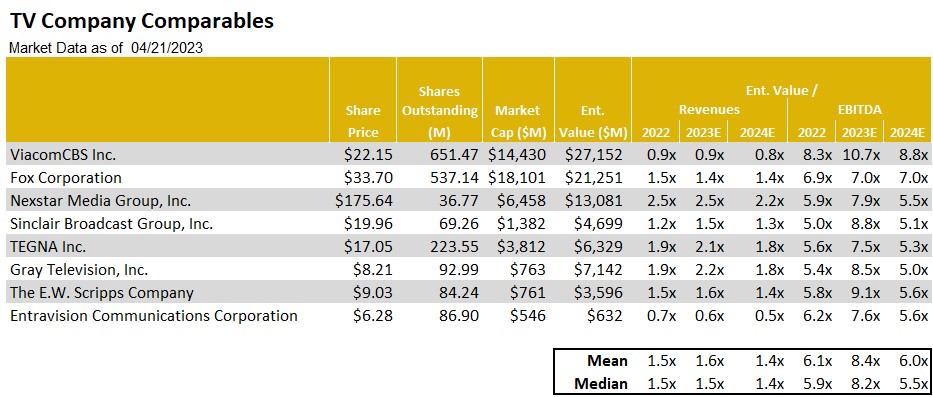

We encourage investors to take an accumulation approach to the sector. Notably, as Figure #9 TV Comparables highlights, nearly all of the stocks are trading near each other, with the exception of the larger media stocks. In our view, the valuations are near recession type valuations and appear to have limited downside risk. Our current favorite is E.W. Scripps (SSP). While the company is not immune to the current weak advertising environment, we believe that there is a favorable Retransmission revenue opportunity as 75% of its subscribers are due in the next 12 months. In addition, we believe that Retransmission margins will improve. Given the relatively small float for the shares, the SSP shares tend to underperform when the industry is out of favor, but then outperform when the industry is back in favor. In our view, the SSP shares offer a favorable risk/reward relationship and top our favorites in the sector.

Figure #7 TV Q4 YoY Revenue Growth

Source: Eikon & Company filings

Figure #8 TV Q4 EBITDA Margins

Source: Eikon & Company filings

Figure #9 TV Comparables

Source: Noble Estimates & Eikon

Radio Broadcasting

All out of love

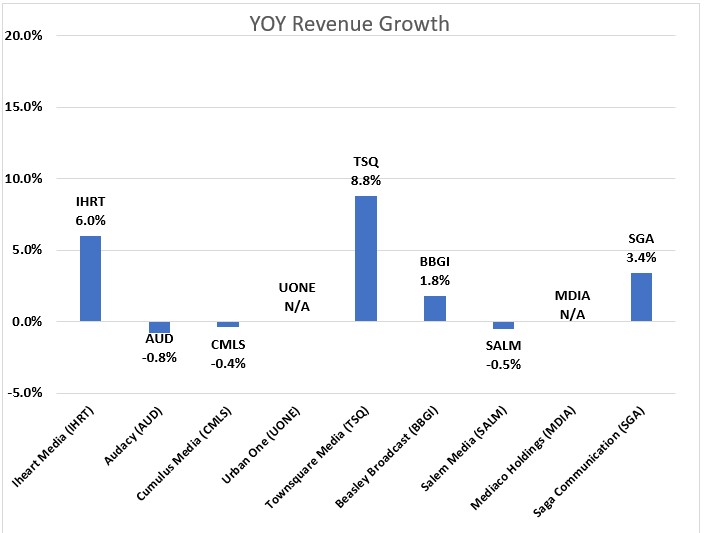

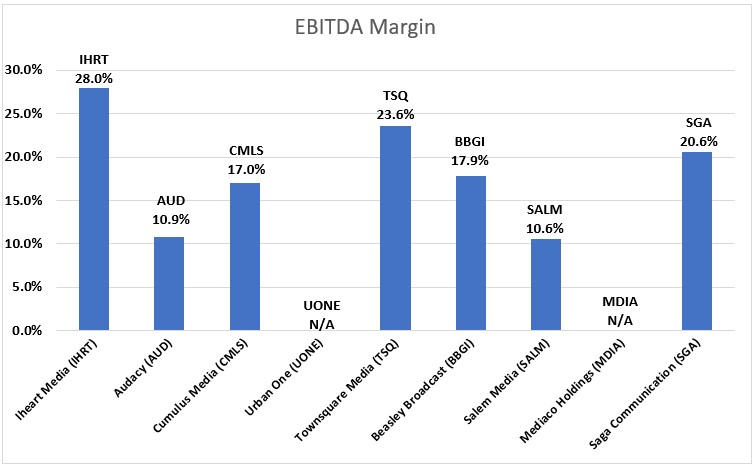

The Radio stocks had another tough quarter, down 17% versus a 7% gain for the general market. Notably, there was a wide variance in the individual stock performance, with the largest stocks in the group having the worst performance in the quarter, including Audacy (AUD; down 40%), Cumulus Media (CMLS; down 41%) and iHeart Media (IHRT; down 36%). The first quarter stock performance did not appear to reflect the fourth quarter results. As Figure #10 Radio Industry Q4 YoY Revenue Growth illustrates, revenues were relatively okay, with some exceptions. Some of the larger Radio companies which have a large percentage of National advertising, underperformed relative to the more diversified Radio companies, especially those with a strong Digital segment presence. Figure #11 Radio Industry Q4 YoY EBITDA Margins illustrate that the margins for the industry remain relatively healthy.

The weakness in the Radio stocks was fueled in the quarter from a downgrade to under perform on the shares of iHeart by a Wall Street firm. Many radio stocks were down in sympathy. The analyst attributed the downgrade to the current macro environment and its heavy floating rate debt burden. The company is not expected to generate enough free cash flow to de-lever its balance sheet. We believe the downgrade as well as the excessive debt profile of Audacy, another industry leader which likely will need to restructure, sent all radio stocks tumbling. Some stocks performed better than others. While Cumulus Media’s debt profile is not as levered as iHeart or Audacy, the shares were caught in the net of a weak advertising outlook. Cumulus is among the most sensitive to National advertising, which currently continues to be weak.

Some of our favorite stocks which are diversified and have developing digital businesses performed better. Those stocks included Townsquare Media (TSQ; up 10%), and Salem Media (SALM; up 4%). Notably, while the shares of Beasley Broadcasting (BBGI) were down 10%, the shares performed better than the 17% decline for the industry in the quarter. Importantly, Beasley recently provided favorable updated Q1 guidance for the first quarter. Q1 revenues are expected to increase 1% to 2.5% and EBITDA growth is expected to be in the range of 40% to 50%, significantly better than our estimates. Furthermore, management provided a sanguine outlook for 2023 and 2024. Digital revenue is expected to reach 20% to 30% of total revenue with a goal of reaching 40% in 2024. By comparison, Digital revenue was 17% of total revenue in the fourth quarter 2022. Furthermore, the company is sitting on roughly $35 million in cash. It has opportunistically repurchased $10 million of its bonds at a significant discount. We believe that it is likely to maintain a strong cash position given the economic uncertainty.

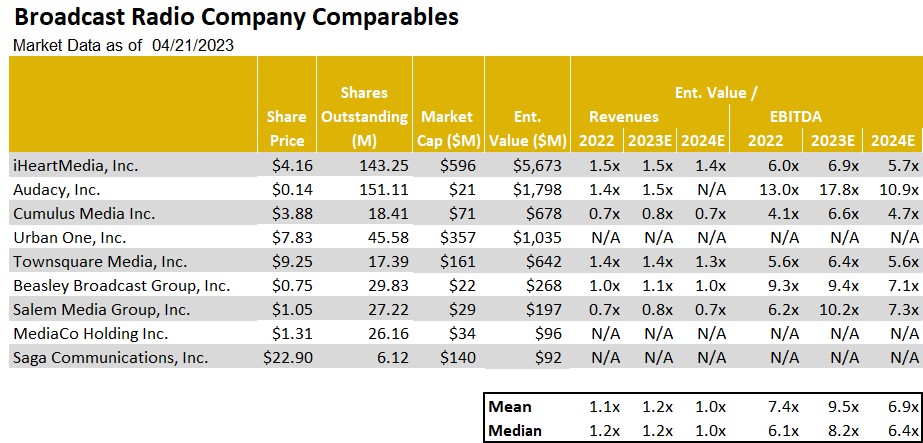

We view Townsquare Media (TSQ), Salem Media (SALM) and Beasley Broadcast (BBGI) as among our favorites in the industry given the diverse revenue streams. While these companies are not immune to the economic headwinds, we believe that its Digital businesses should offer some ballast to its more sensitive Radio business. In the case of Salem, 30% of its revenues are relatively stable with block programming. As Figure #12 Broadcast Radio Comparables illustrates, the shares of Townsquare are among the cheapest in the industry, trading below peer group averages. Notably, the company instituted a hefty dividend. As a result, investors get paid while we await a favorable upturn in fundamentals. As such, the shares of TSQ tops our list of favorites.

Figure #10 Radio Industry Q4 YoY Revenue Growth

Source: Eikon & Company filings

Figure #11 Radio Industry Q4 YoY EBITDA Margins

Source: Eikon & Company filings

Figure #12 Broadcast Radio Comparables

Source: Noble estimates & Eikon

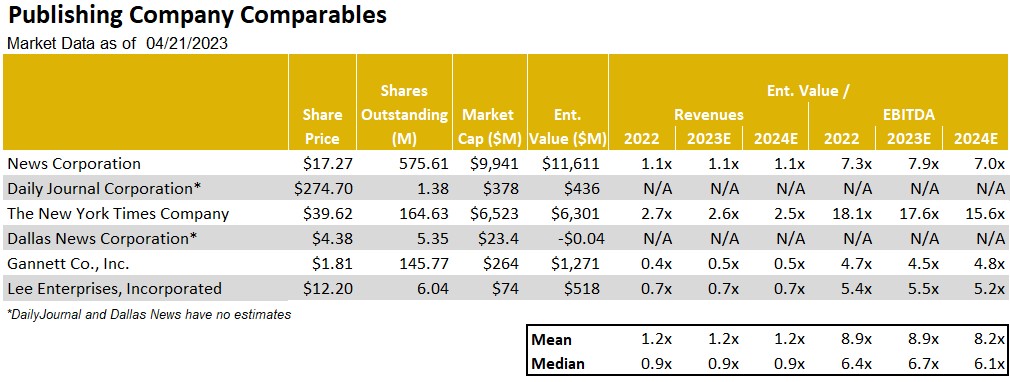

Publishing

Advertising takes a hit

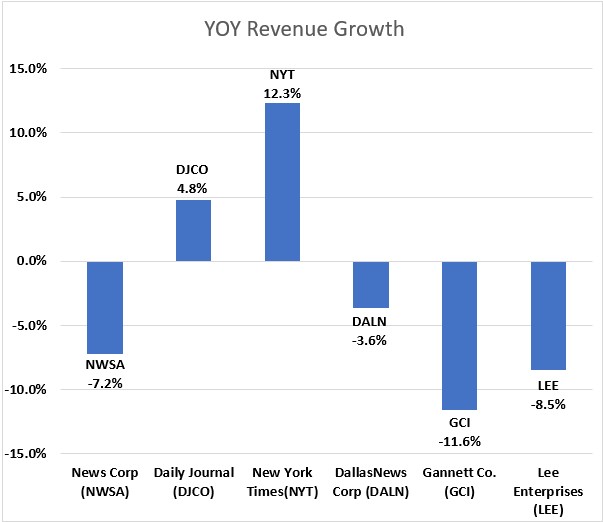

After a period of moderating revenue trends, Publishers reported a weakened advertising environment. As illustrated in Figure #13 Publishing Industry YOY Revenue Growth, illustrates that revenue trends deteriorated with Print advertising taking a nose dive. This trend was illustrative in the results from Lee Enterprises, one of our current favorites in the sector. After a fiscal fourth quarter flat revenue performance, the company reported a 8.5% decline in its fiscal first quarter. The Q1 revenue performance reflected an 18.5% decrease in Print advertising, an acceleration in the rate of the 11% decline in the previous quarter.

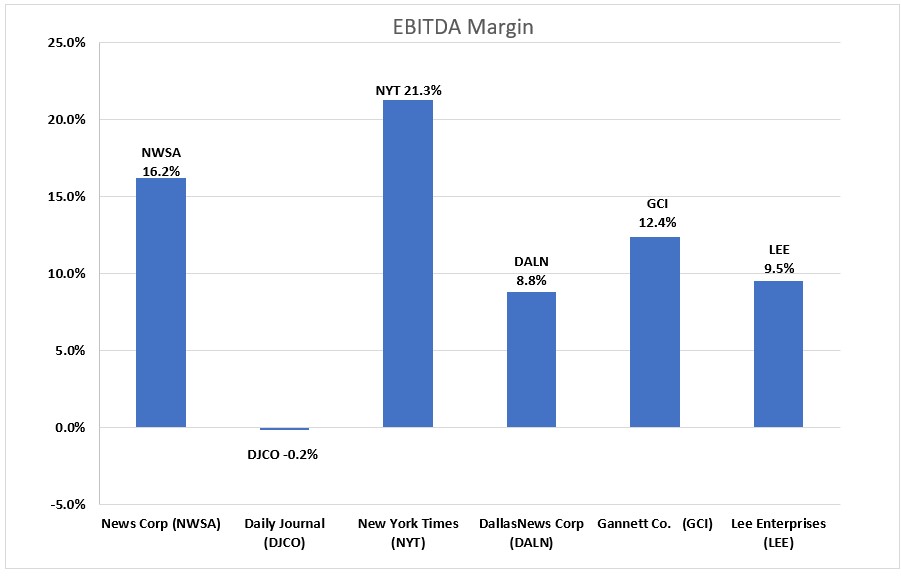

The surprisingly weak quarter hit the company’s adj. EBITDA margins. Traditionally, Lee maintained some of the best margins in the industry. As Figure #14 Q4 Publishing Industry EBITDA Margins illustrates, the company fell in ranking to among the lowest in the sector. Importantly, in spite of the revenue weakness, the company maintains its previous adj. EBITDA guidance of $94 million to $100 million. To achieve its cash flow target in light of the soft revenue outlook, Lee implemented a round of expense cuts to bolster cash flow. Cost reductions are expected to result in $40 million of savings in FY23, and $60 million in annualized savings going forward. While we are disappointed that the company’s Print business is not moderating as previously expected, the company’s Digital businesses remain favorably robust. In addition, its Digital business is turning toward contributing margins. As such, we remain sanguine about the company’s digital transition.

As Figure #15 Publishing Comparables highlights, there is a wide gap between the valuation of the New York Times (NYT) and the rest of the industry, including Lee. While the highly debt levered shares of Gannett appear cheaper, we believe that Lee has a more favorable debt profile with a fixed 9% annual rate, no fixed principal payments, no performance covenants and a 25 year maturity. With the shares trading at 5.3 times our 2024 adj. EBITDA estimate compared with 15.4 times at the New York Times, we believe that there is limited downside risk in the LEE shares. Furthermore, we believe that the company is well positioned as economic and advertising prospects improve. Given the company’s favorable outlook for its Digital transition, we believe that the shares should close the gap in valuations with the leadership stock in the group. Consequently, the shares of LEE are among our favorite play for an improving economic outlook.

Figure #13 Publishing Industry YoY Revenue Growth

Source: Eikon & Company filings

Figure #14 Q4 Publishing Industry EBITDA Margins

Source: Eikon & Company filings

Figure #15 Publishing Comparables

Source: Noble estimates & Eikon

For more information on companies mentioned in this report click on the following:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Mark Reichman, Managing Director, Natural Resources Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Big Vein strike length extended to 722 meters. Labrador Gold released results from five drill holes at the Big Vein target within the company’s 100%-owned Kingsway project. Step out drilling to the northeast and southwest continue to intersect gold mineralization at Big Vein which has now been extended to 722 meters in strike length and remains open in both directions. Hole K-23-216 intersected 3.69 grams of gold per tonne over 2.97 meters from 389.41 meters including 12.05 grams of gold per tonne over 0.59 meters, while Hole K-23-218 returned 1.95 grams of gold per tonne over 9 meters including 8.97 grams of gold per tonne over 1.6 meters. Hole K-23-225, a 100-meter step-out to the northeast intersected 1 gram of gold per tonne over 10.1 meters from 46.9 meters, that included an interval of 2.28 grams of gold per tonne over 2.26 meters containing visible gold.

Discovery of a new mineralized zone. Hole K-22-214B returned 5.22 grams of gold per tonne over 2.80 meters from 418.6 meters that included 22.02 grams of gold per tonne over 0.4 meters, along with 8.62 grams of gold per tonne over 0.7 meters from 496 meters. Both it and Hole K-22-214 are associated with a new mineralized zone, the Greenmantle Zone, that lies below the HTC Zone at a vertical depth of 415 meters. The discovery of the Greenmantle zone demonstrates the potential for continued mineralization at depth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Energy & Transportation Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results demonstrate strong production growth and a sharp increase in cash flow and earnings. Production rates (preannounced) increased 55%. Increased production was partially offset by a drop in energy prices. Lower-than-expected prices were partially offset by a decrease in royalty rates. Production costs (excluding transportation costs) remain somewhat elevated as they were in the September quarter. We look for production costs per barrel to decrease modestly as new production comes on line in 2023.

As netbacks rose, so did the company’s Adjusted Fund Flow (AFF). The margin between prices and costs is high. Operating netbacks (realized prices less royalties and operating costs) is leading to strong cash flow which management is turning their focus toward returning to shareholders now that debt is virtually eliminated and drilling programs have been accelerated.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CULVER CITY, Calif., April 13, 2023 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, is pleased to announce that that Noble Capital Markets has initiated company-sponsored equity research coverage on the Company. The full report by Noble Capital Markets Senior Research Analyst Michael Kupinski, as well as news and advanced market data on Snail, Inc. is available on Channelchek.

About Snail, Inc.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

About Noble Capital Markets

Noble Capital Markets, Inc. was incorporated in 1984 as a full-service SEC / FINRA registered broker-dealer, dedicated exclusively to serving underfollowed small / microcap companies through investment banking, wealth management, trading & execution, and equity research activities. Over the past 37 years, Noble has raised billions of dollars for these companies and published more than 45,000 equity research reports. www.noblecapitalmarkets.com email: contact@noblecapitalmarkets.com

About Channelchek

Channelchek (.com) is a comprehensive investor-centric portal – featuring more than 6,000 emerging growth companies – that provides advanced market data, independent research, balanced news, video webcasts, exclusive c-suite interviews, and access to virtual road shows. The site is available to the public at every level without cost or obligation. Research on Channelchek is provided by Noble Capital Markets, Inc., an SEC / FINRA registered broker-dealer since 1984. www.channelchek.com email: contact@channelchek.com

Favorable safety and tolerability profile related to OCU400 investigational product candidate

Initial clinical data from low and medium dose cohorts indicates positive trend in Multi-luminance mobility testing and Best-Corrected Visual Acuity scores for OCU400 treated eyes

71.4% (5/7) of OCU400 treated eyes in low and medium dose cohorts experienced at least 1 Lux luminance level improvement in mobility test from baseline

66.7% (2/3) of OCU400 treated eyes in low dose cohorts at 9-month follow-up experienced at least 2 Lux luminance level improvement in mobility test from baseline

Ocugen believes these preliminary data supports potential of modifier gene therapy platform in gene-agnostic treatment of complex and heterogenous inherited genetic diseases

MALVERN, Pa., April 14, 2023 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced positive preliminary data among retinitis pigmentosa (RP) participants treated in the first two cohorts of the Phase 1/2 trial to assess the safety and efficacy of OCU400 for RP associated with NR2E3 and Rhodopsin (RHO) mutations and Leber Congenital Amaurosis (LCA) with mutation(s) in the CEP290 gene. These preliminary results provide support that OCU400, Ocugen’s first-in-class therapeutic approach utilizing a proprietary modifier gene therapy platform, has the potential to be a gene-agnostic therapeutic for RP and LCA patients with inherited retinal degeneration.

“It is very gratifying to see these positive preliminary results from our novel modifier gene therapy approach,” said Dr. Shankar Musunuri, Chairman, Chief Executive Officer, and Co-Founder of Ocugen. “This is the first clinical validation of the platform where patient responses across various genetic mutations support that OCU400 has the potential to transform the lives of many patients who are struggling with debilitating blindness diseases.”

This Phase 1/2 trial is a multicenter, open-label, dose ranging study. A total of 18 RP subjects have been enrolled in this study—10 subjects in the dose escalation and 8 subjects in the expansion phase, respectively. The age of subjects enrolled to date ranges from 18-77 years across RHO and NR2E3 gene mutations. We further expanded this Phase1/2 trial to enroll LCA patients with CEP290 gene mutation and pediatric patients with NR2E3, RHO and CEP290 mutations.

In Cohort 1 and 2 of the clinical trial, 7 participants with severe vision impairment due to RP associated with RHO and NR2E3 gene mutations received a unilateral subretinal injection of either a low dose (1.66 x 1010 vg/mL) or medium dose (3.33 x 1010 vg/mL) OCU400, respectively. In the preliminary data analysis, 9-month follow-up data for 3 subjects [Cohort 1], and 6-month follow-up data for 4 subjects [N=1 from Cohort 1 and N=3 from Cohort 2] were evaluated.

Results showed a favorable safety profile and visual improvements after treatment with OCU400 as measured by multi-luminance mobility testing (MLMT) and best corrected visual acuity assessment (BCVA).

Key efficacy outcomes from 7 subjects demonstrated:

100% of treated eyes showed a stable or improved MLMT score trend;

5 of 7 (71.4%) OCU400 treated eyes demonstrated a 1 or more Lux level improvement in MLMT score compared to 28.6 % of untreated eyes;

66.7% (2 of 3) of OCU400 treated eyes in Cohort 1 with 9-month follow-up demonstrated a 2 or more Lux level improvement in MLMT score compared to none of the untreated eyes; and

3 of 7 (42.9%) OCU400 treated eyes demonstrated 8-11 letters of improvement in BCVA score compared to none of the untreated eyes.

“I was not expecting such substantial improvements in visual function among the trial participants I have been working with because of the advanced stage of their retinal disease,” said David Birch, PhD, Scientific Director, Retina Foundation of the Southwest, principal investigator of the study. “I am very pleased by the outcomes I have seen in my own clinic and am hopeful that OCU400 could provide a therapeutic solution for RP patients who are not only facing loss of vision, but also challenged with the psychological burden of losing their independence.”

“The early results from patients treated in the Phase 1/2 clinical trial are encouraging and support the paradigm-changing potential of modifier gene therapy technology to address unmet medical needs for patients with RP and LCA,” said Arun Upadhyay, PhD, Chief Scientific Officer and Head of Research, Development and Medical at Ocugen. “With this favorable safety profile and positive trend in efficacy signals, we are very eager to see longer-term data, and to potentially initiate Phase 3 trials in the U.S. and EU.”

Ocugen will continue to monitor long-term safety and efficacy data from the treated patients, and advance development of OCU400 to bring a potential treatment option to RP and LCA patients.

CanSinoBIO, Ocugen’s strategic partner, provided all CMC development and clinical supplies for the Phase 1/2 trial of OCU400.

A webcast and conference call will take place today at 8 a.m. ET: Dial-in Numbers: (800) 715-9871 for U.S. callers and (646) 307-1963 for international callers Conference ID: 4898155 Webcast: Available on the events section of the Ocugen investor site

About Modifier Gene Therapy Modifier gene therapy is designed to fulfill unmet medical needs related to retinal diseases, including IRDs, such as RP, LCA, and Stargardt disease, as well as dry AMD. Our modifier gene therapy platform is based on the use of NHRs, master gene regulators, which have the potential to restore homeostasis — the basic biological processes in the retina. Unlike single-gene replacement therapies, which only target one genetic mutation, we believe that our modifier gene therapy platform, through its use of NHRs, represents a novel approach that has the potential to address multiple retinal diseases caused by mutations in multiple genes with one product, and to address complex diseases that are potentially caused by imbalances in multiple gene networks. Currently Ocugen has three modifier gene therapy programs OCU400 (RP, LCA), OCU410 (dry AMD), OCU410ST (Stargardt disease).

About OCU400 OCU400 is the Company’s gene-agnostic modifier gene therapy product based on NHR gene, NR2E3. NR2E3 regulates diverse physiological functions within the retina—such as photoreceptor development and maintenance, metabolism, phototransduction, inflammation and cell survival networks. Through its drive functionality, OCU400 resets altered/affected cellular gene-networks and establishes homeostasis—a state of balance, which has potential to improve retinal health and function in patients with inherited retinal diseases.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patients’ lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties, including, but not limited to, statements regarding the development of OCU400 and the interpretation of preliminary clinical trial results. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including, but not limited to, the risk that preliminary clinical data may not be indicative of final clinical data or data in later stage clinical trials. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.Contact: Tiffany Hamilton Head of Communications IR@ocugen.com

Toronto, Ontario, April 13, 2023 – Aurania Resources Ltd. (TSXV: ARU; OTCQB: AUIAF; Frankfurt: 20Q) (“Aurania” or the “Company”) is pleased to announce its proposed 2023 exploration activities.

As the concessions for its mineral properties in Ecuador are fully renewed and in good standing for another year after payment of all concession fees in March, the Company is able to develop the 2023 exploration programs.

Aurania attended the Prospector’s and Developer’s Association of Canada meeting (PDAC) in Toronto the first week of March, and we were delighted by the interest shown by several Major companies in our Ecuador asset. As a result of follow-up meetings there are now several companies in our data room. The primary interest has been in our porphyry copper and sediment-hosted copper-silver prospects.

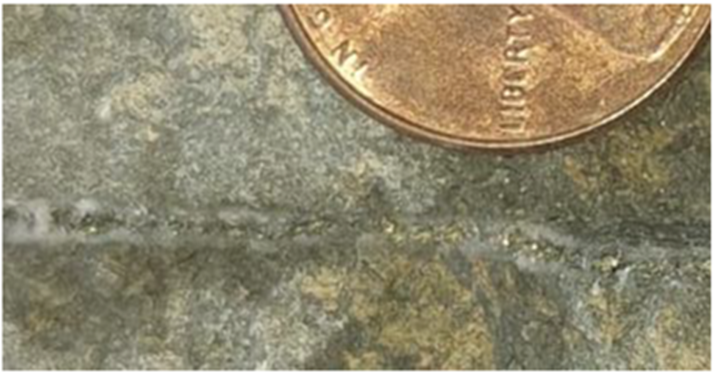

To date, approximately 45% of the Awacha Porphyry Target has been covered by “Anaconda-style Mapping”. This is an intensive mapping technique that was originally developed by the famous Anaconda Copper Company, and has been taught to the Aurania geological staff by consultant Dr. Steve Garwin. This target is approximately 11 km x 5 km in size and was discovered by stream sediment sampling which showed elevated copper and molybdenum in the vicinity of two strong airborne magnetic anomalies. This size is significantly larger than any copper porphyry known and so our working hypothesis is that it is a cluster of porphyries, and similar to the Warintza cluster to the south of our concessions. Intrusive rock types from gabbro to diorite to monzonite and syenite have been mapped. Many of these intrusives show secondary biotite (potassic) alteration and fine quartz veins containing molybdenite or a centre line of chalcopyrite. These so called distinctive “B veins” are classic evidence of mineralized porphyry systems. An independent explanation of B veins can be found at: https://www.youtube.com/watch?v=gL0WzJ70z3s

Figure 1: Quartz vein with centre line of chalcopyrite, covellite and pyrite. US cent for scale.

Most of the Awacha area is covered by a unit of black shale which obscures the geology except where streams have cut down through the sediments and exposed the porphyry. The area is also covered by thick jungle. Nevertheless, Terraspec Mineral Spectrometer analysis of soils in the southern half of the anomaly indicates chlorite, kaolinite, white micas, dickite and pyrophyllite which are compatible with porphyry-style alteration. The last two minerals are typically found in the upper part of porphyry systems.

Copper soil anomalies are patchy, which is in keeping with soil results seen near outcropping sediment hosted copper elsewhere on the property. It would seem that copper is easily flushed away from surface soils by the significant rainfall in the area. Molybdenum however, which is essentially insoluble and immobile presents a much more coherent group of anomalies. Half of the Awacha target is still to be sampled for soils.

The reinterpretation of the surficial geology and structure in the areas of outcropping sediment-hosted copper-silver and zinc-lead-silver has generated a large number of compelling drill targets (see press release dated October 17, 2022). This copper-silver-zinc system across the concessions is 38 kilometres in lngth and is open to the north over an additional 15 kilometres. We believe this is perhaps one of the best areas of the property to find an economic ore deposit, considering the numerous high assays already yielded to date. A few areas are highlighted for follow-up, but we concede that a comprehensive programme here is more appropriate for a Major mining company partner.

The Tatasham epithermal gold/porphyry copper target is compelling due to the presence of what are believed to be pipe breccias. The area is, however, in steep terrain and the geology is mostly covered by post-mineral sedimentary cover and does not outcrop. Soil samples along the ridgeline above the previous porphyry drilling campaign yielded anomalous antimony, which is a pathfinder element in gold systems. An additional soil survey is required at Tatasham to extend the antimony anomaly that is still open to the north. Intensive mapping and prospecting are required. The discovery of the epithermal system at Tatasham was unexpected, in our pursuit of a copper porphyry target indicated by geophysics. That porphyry target is still valid, but it may lie at considerable depth, or it may lie laterally.

Over the next six months it is intended to finish the Anaconda mapping on Awacha, and bring it to drill readiness. At the same time, Tatasham will be re-examined in the belief that the antimony anomaly in soils may be due to a subcropping mineralized system. The Fruta del Norte gold deposit was discovered by drilling a geochemical anomaly of antimony, arsenic and mercury which had virtually no gold on surface. Aurania is currently investigating the feasibility of conducting an Induced Polarization (IP) geophysical survey at Tatasham and Awacha.

The proposed exploration programmes are dependent on raising further funding. The proceeds of the current private placement (as announced on March 13, 2023 and March 23, 2023) to date, have been applied to concession fees and general and administrative expenses.

Qualified Person

The geological information contained in this news release has been verified and approved by Aurania’s VP Exploration, Mr. Jean-Paul Pallier, MSc. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Information on Aurania and technical reports are available at www.aurania.com and www.sedar.com, as well as on Facebook at https://www.facebook.com/auranialtd/, Twitter at https://twitter.com/auranialtd, and LinkedIn at https://www.linkedin.com/company/aurania-resources-ltd-.

For further information, please contact:

Carolyn Muir

VP Corporate Development & Investor Relations Aurania Resources Ltd.

(416) 367-3200

carolyn.muir@aurania.com

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the Company’s teams being on track ahead of any drill program, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that, there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things, the ability to anticipate and counteract the effects of COVID-19 pandemic on the business of the Company, including without limitation the effects of COVID-19 on the capital markets, commodity prices supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and copper; and. those risks set out in the Company’s public documents filed on SEDAR. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.