Research News and Market Data on AUIAF

April 28, 2026 10:00 AM EDT | Source: Aurania Resources Ltd.

This release corrects and replaces the press release issued by Aurania Resources Ltd. on April 28, 2026 – 7:25AM EDT, correcting the anniversary timelines of exploration expenditures under the heading Summary of Terms under the Agreement.

Toronto, Ontario–(Newsfile Corp. – April 28, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) is pleased to announce that it has entered into a definitive option agreement (the “Agreement”) dated April 27, 2026 (the “Execution Date”) with St-Georges Eco-Mining Corp (CSE: SX) (“St-Georges“), a Canadian incorporated mineral exploration company and its wholly owned subsidiary Iceland Resources ehf (“IR”), an Icelandic incorporated precious metals exploration company to work collaboratively to define and execute a phased exploration program aimed at advancing the Thormodsdalur gold project (“Thor’s Valley” or the “Project”), towards initial modern resource definition. The Thor’s Valley project is held by IR and is located approximately 20 kilometres east of Reykjavík, the capital of Iceland.

Aurania’s President and CEO, Dr. Keith Barron commented, “After visiting the project area and personally reviewing the archived drill core, the Thor’s Valley project represents a compelling opportunity with strong exploration upside. By formalizing our collaboration with St-Georges, we are positioning ourselves to unlock the potential of an under-explored geological district. Thor’s Valley displays all the key signatures of a robust epithermal gold system, supported by a history of documented high-grade mineralization and a suite of compelling structural targets that remain largely untested by modern exploration methods. This Agreement allows Aurania to deploy its technical expertise toward a highly prospective gold project. We look forward to progressing this Project with discipline, technical rigour, and a strong commitment to unlocking its full potential.”

Comment from Thordis Bjork Sigurbjornsdottir, CEO of Iceland Resources: “This is an important partnership for Iceland Resources, and we are pleased to welcome Aurania Resources Ltd. as a partner on the Thormodsdalur project. Over the past several years, we have engaged in discussions with several groups with the objective of identifying a partner with the right technical experience and approach for this type of epithermal gold system. We believe Aurania brings that combination, supported by relevant experience in advancing high-grade epithermal discoveries. We look forward to working together to advance Thormodsdalur in a disciplined and value-focused manner.”

Summary of Terms under the Agreement

- Initial payment of US$150,000 in common shares of Aurania (the “Shares”) to be issued to St. Georges on the closing date of the Agreement at a deemed price per Share equal to the volume weighted average price of the Shares on each business day commencing on the Execution Date and ending on the last business day prior to the closing date of the Agreement.

- Aurania to incur exploration expenditures of US$5 million over four years to earn a 70% interest in the Project, such exploration expenditures to be incurred as follows:

- At least US$500,000 prior to the first anniversary of the Execution Date;

- At least US$1,000,000 prior to the second anniversary of the Execution Date;

- At least US$1,500,000 prior to the third anniversary of the Execution Date;

- At least US$2,000,000 prior to the fourth anniversary of the Execution Date;

- Upon completing the First Option, St-Georges will have the option to choose between maintaining a 30% interest in the Project through a joint venture or retain an up to 3% net smelter return royalty on the Project (the “Royalty”), with such Royalty to be reduced as necessary such that the aggregate royalty burden on the Project shall not exceed 3%, inclusive of any pre-existing NSR royalties; and

- If St. Georges elects to retain the Royalty, Aurania will have the right, in its sole discretion, to increase its ownership to in the Project to 100% by incurring an additional US$2,000,000 of exploration expenditures.

- A joint exploration committee will be established between Aurania and St-Georges, with Aurania being the technical operator.

The Agreement is subject to certain conditions, including the approval of the TSX Venture Exchange. The Shares will be subject to a hold period of four months and one day from the date of issuance.

Thor’s Valley is a historically known gold-bearing, low-sulphidation epithermal system that was initially discovered in 1903 when two Icelandic farm boys picked up pieces of white quartz from a stream, which proved to be gold-bearing. A number of ventures were organized from 1911 to 1924 using German or British capital. Two shafts were sunk and approximately 400 metres of lateral workings performed. As a result of this, the productive vein was estimated to be 1 metre wide and at least 1 kilometre long. Reported grades were 11 g/t to 315 g/t gold[1]. The ore was “direct shipping” and initially sent to Norway and later to Germany for treatment. There are no historic tailings on site. Perhaps significantly, the historical record indicates that the last operator, Arcturus, a German company, failed due to the Weimar hyperinflation rather than ore depletion.

In the 1990’s, several programmes of geochemical and petrographical studies were done, including a vertical geothermal well to a depth of 455 metres which encountered multiple mineralized quartz veins, including one at the bottom of the hole. In 1997, a total of 1069.21metres were diamond drilled in nine holes, however, average core recovery was only 52%. The intervals sampled graded 1.13 g/t to 46.10 g/t Au but this is not considered representative and true widths could not be calculated.

Between 2005 and 2006, the private exploration company Melmi ehf drilled 32 holes totaling 2431m, which returned results up to 415.40 g/t Au. Melmi ehf was acquired by Iceland Resources in 2020, which completed 11 additional drill holes totaling 1780m with results of up to 113 g/t Au1.

Figure 1. Sample of historic drill core from 1996. This is a typical hydrothermal breccia, as commonly seen in epithermal systems. This type of ore deposit is the same as that at Fruta del Norte in Ecuador.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2477/294569_f7885709c477d829_001full.jpg

The Thor Valley mineralization is a classic banded epithermal chalcedony-ginguro vein system with gold occurring both in free form and in association with sulphides. There are obviously a number of different vein sets here that appear controlled by regional and local structures.

The Project consists of a National Exploration Permit covering approximately 51,300 hectares in Iceland.

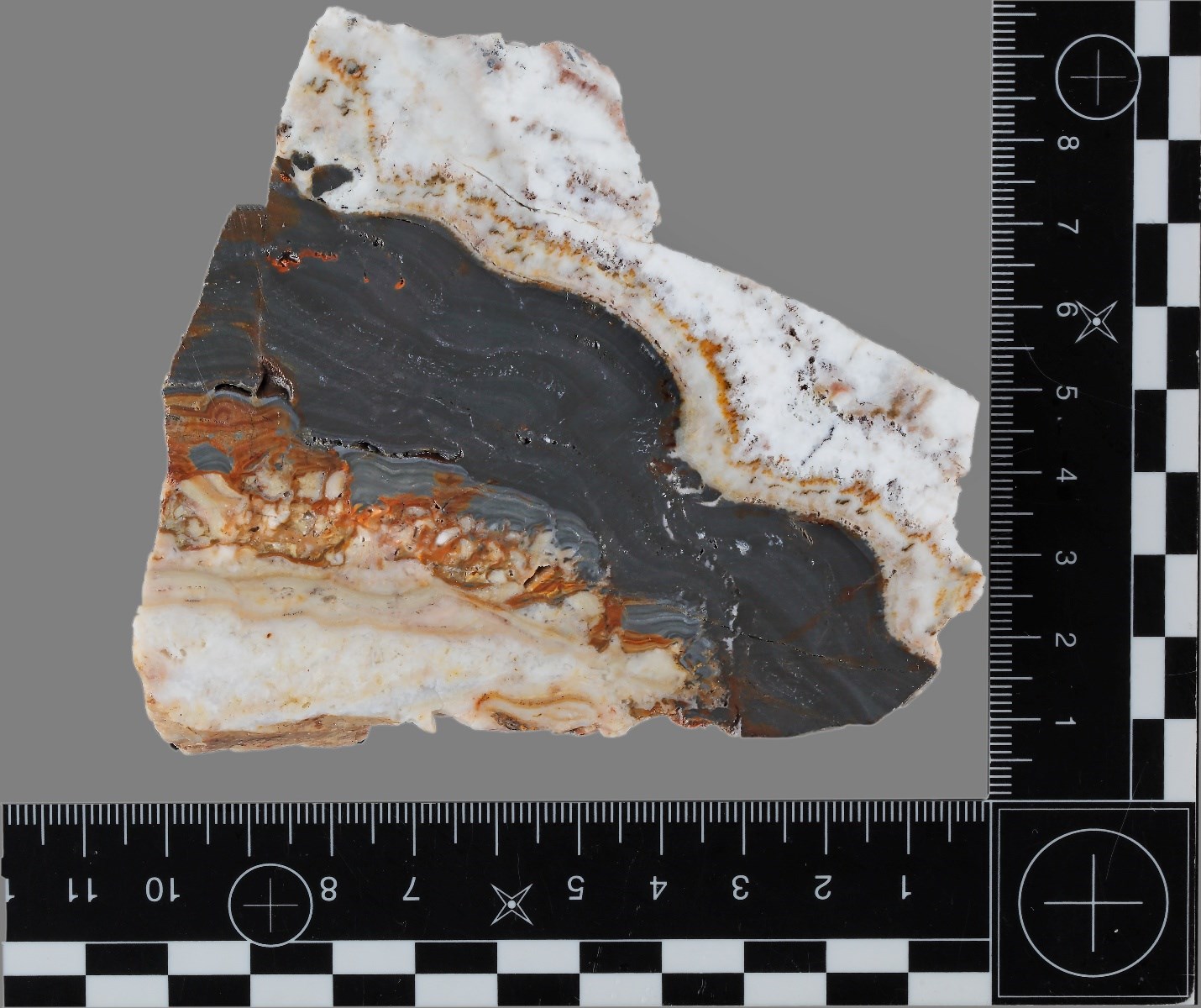

Figure 2: Hand sample of mineralization with typical rhythmic banding. The black area is composed of very fine-grained pyrite. This sample was found as float on the site and will be sent in for assay.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/2477/294569_f7885709c477d829_002full.jpg

Planned Work Program

Aurania anticipates completing an initial exploration program focused on targeted drilling and surface exploration designed to test deeper and along-strike continuity of the known mineralized zones, utilising both historical data and newly generated technical information. Several of the previous drill holes with poor recovery will be twinned.

The Company cautions the reader that the historical information referred to herein is based on data compiled by previous operators and publicly available sources and is being provided for reference purposes only. A qualified person retained by Aurania has not undertaken sufficient work to verify the historical data, and such information should not be relied upon. Further exploration work, including drilling and data verification, is required and may or may not result in the delineation of a mineral resource.

No current mineral resources or mineral reserves, as defined under National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”), have been established on the Project.

The technical and scientific information contained in this news release has been reviewed and approved by Jean-Paul Pallier, MSc., Vice-President Exploration of the Company. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About St-Georges Eco-Mining Corp.

St-Georges develops new technologies and holds a diversified portfolio of assets and patent-pending Intellectual Property within several highly prospective subsidiaries including: EVSX, a leading North American advanced battery processing and recycling initiative; St-Georges Metallurgy, with metallurgical R&D and related IP, including processing and recovering high grade lithium from spodumene; Iceland Resources, with high grade gold exploration projects including the flagship Thor Project; H2SX, developing technology to convert methane into solid carbon and turquoise hydrogen; and Quebec exploration projects including the Manicouagan and Julie nickel, Copper and PGE critical mineral projects on Quebec’s North Shore, and Notre-Dame niobium Project in Lac St Jean.

Information on St-Georges Eco-Mining Corp. can be found on the company’s website at www.stgeorgesecomining.com. For all other inquiries: [email protected].

About Iceland Resources

Iceland Resources is an Icelandic mineral exploration company focused on early-stage precious metal projects, including Thormodsdalur. The company’s exploration strategy emphasizes systematic, data-driven evaluation of prospective targets in under-explored volcanic terrains.

Information on Iceland Resources and technical reports are available at https://icelandresources.is/, as well as on Facebook at https://www.facebook.com/icelandresources, and X (formerly Twitter) at https://x.com/Iceland_Res.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Information on Aurania and technical reports are available at www.aurania.com and www.sedarplus.ca, as well as on Facebook at https://www.facebook.com/auranialtd/, X (formerly Twitter) at https://x.com/AuraniaLtd, and LinkedIn at https://www.linkedin.com/company/aurania-resources-ltd-.

For further information, please contact:

Carolyn Muir

VP Corporate Development & Investor Relations

Aurania Resources Ltd.

(416) 367-3200

[email protected]

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes: statements regarding the terms of the Agreement, earn-in requirements, anticipated exploration programs, timing of activities, the potential to advance the Project, Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the tonnage and grade of mineralization which has the potential for economic extraction and processing, the merits and effectiveness of known process and recovery methods, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things: failure to achieve the anticipated results, incorrect assumptions made in the initial evaluation of the Project, failure to identify mineral resources; failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; the inability to recover and process mineralization using known mining methods; the presence of deleterious mineralization or the inability to process mineralization in an environmentally acceptable manner; commodity prices, supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and base metals; and those risks set out in the Company’s public documents filed on SEDAR+. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

[1] Additional information regarding the Thormodsdalur project is available on Iceland Resources’ website at www.icelandresources.is/thormodsdalur.

Source: Aurania Resources Ltd.

{kind=link}

{kind=link}