CERRITOS, Calif., Feb. 26, 2026 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (“TOI”) (NASDAQ: TOI) a pioneer in value-based community oncology care, today announced that the company will release its fourth quarter and full year 2025 financial results on Thursday, March 12, 2026, to be followed by a conference call the same day at 5:00 p.m. (Eastern Time).

The conference call can be accessed live over the phone by dialing 1-877-407-0789 or for international callers, 1-201-689-8562. A replay will be available two hours after the call and can be accessed by dialing 1-844-512-2921, or for international callers, 1-412-317-6671. The passcode for the live call and the replay is 13758646. The replay will be available until Thursday March 19, 2026.

Interested investors and other parties may also listen to a simultaneous webcast of the conference call by logging onto the Investor Relations section of the Company’s website at https://investors.theoncologyinstitute.com/.

About The Oncology Institute

Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better.

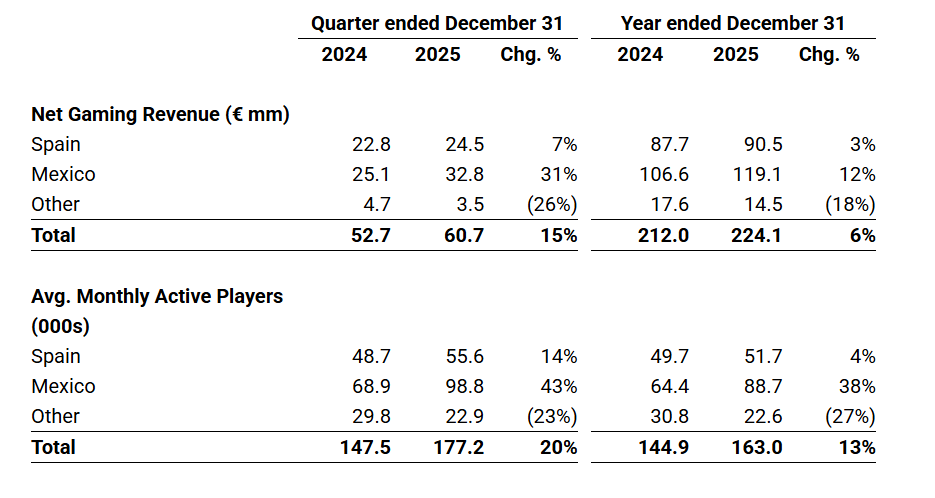

The Company delivered a strong set of results, with record net gaming revenueof €224.1 million and Adj. EBITDA of €13.8 million for FY 2025

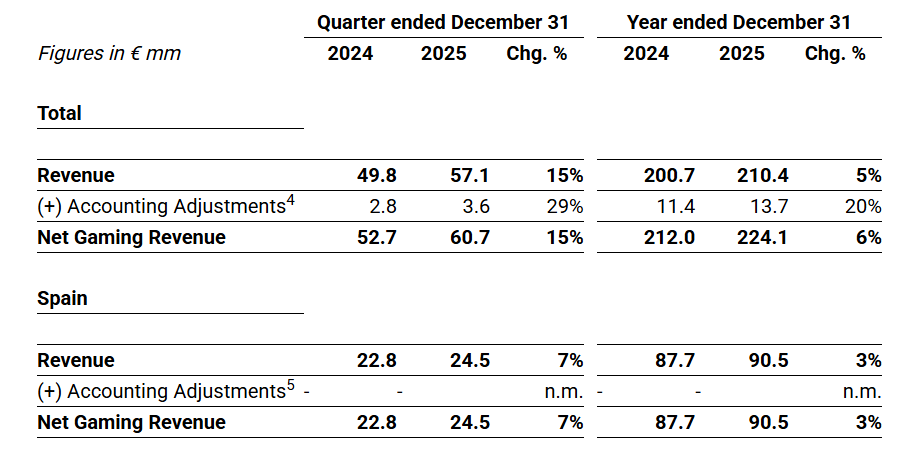

Total revenue was €57.1 mm in Q4 2025, while net gaming revenue1 was €60.7 mm, 15% above Q4 2024.

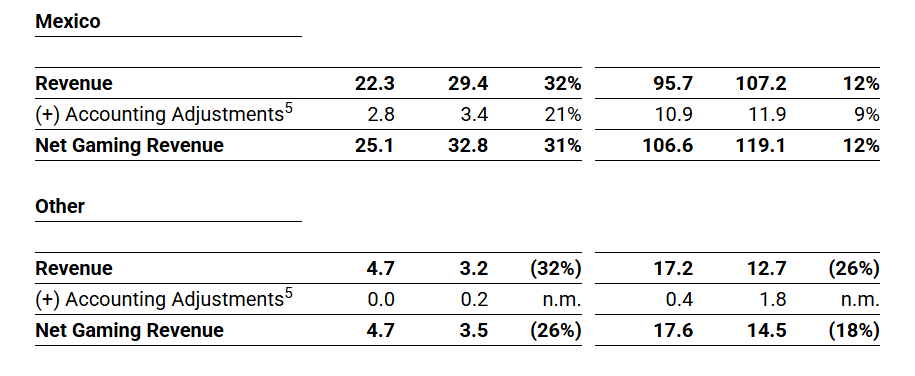

Mexico revenue was €29.4 mm in Q4 2025, while net gaming revenue was €32.8 mm, 31% above Q4 2024.

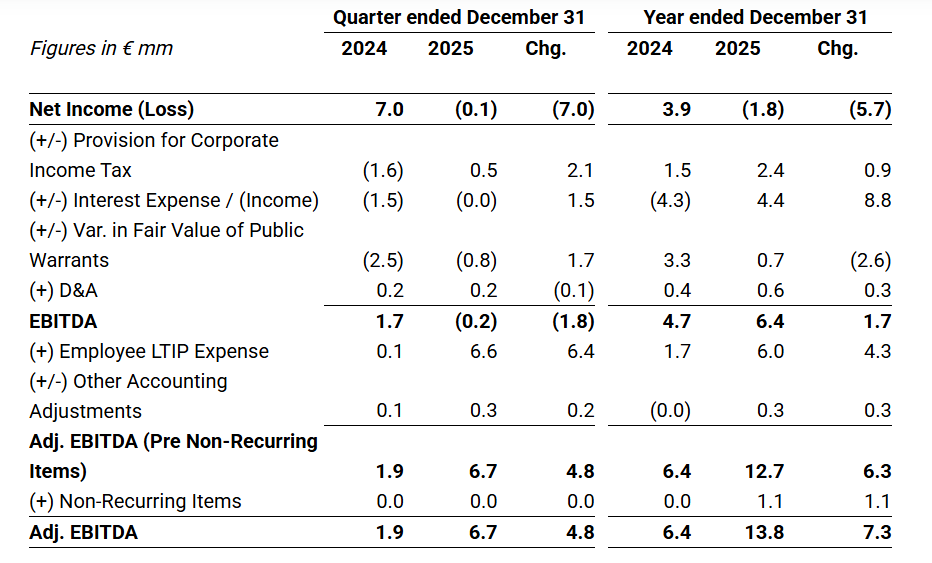

Adj. EBITDA reached €6.7 mm in Q4 2025, €4.8 mm above Q4 2024.

Net loss was €1.8 mm in 2025 versus a net income of €3.9 mm in 2024.

Total cash position of €50.0 mm and no financial debt as of December 31, 2025.

Outlook for FY 2026: Net gaming revenue of €235-245 mm and Adj. EBITDA2 of €15-20 mm.

391 thousand repurchased shares for an aggregate amount of $2.7 mm under the Company’s share buyback plan through February 25, 2026.

Madrid, Spain and Tel Aviv, Israel, February 26, 2025 – (GLOBE NEWSWIRE) Codere Online (Nasdaq: CDRO / CDROW, the “Company”), a leading online gaming operator in Spain and Latin America, has released its preliminary unaudited3 financial results for the quarter and year ended December 31, 2025.

Below are the main financial and operating metrics of the period.

Aviv Sher, Chief Executive Officer of Codere Online, commented, “In the fourth quarter of 2025, our net gaming revenue reached €60.7 million, marking the highest quarterly figure in the Company’s history.” This increase was mostly driven by Mexico, where our net gaming revenue grew 31% on the back of a 43% increase in our portfolio of active customers in the country. In December, we hit a record of 100,000 active players in the country, positioning us well for the upcoming World Cup this summer”.

Marcus Arildsson, CFO of Codere Online, commented, “Beyond the strong top line performance in the fourth quarter, we also had a significant uplift in Adj. EBITDA to €6.7 mm in the period, allowing us to meet the upper part of the 2025 outlook range we provided last year.”

Mr. Arildsson further stated, “As we look out to 2026, we are encouraged by the strong trends in both Mexico and Spain and expect our net gaming revenue for the year to be in the €235-245 million range and Adj. EBITDA between €15 and 20 million.”

Recent Events

Board Appointments

On December 1, 2025, Mr. Oscar Iglesias, who previously served as the Company’s Chief Financial Officer, was appointed as member of the Company’s board of directors (the “Board”).

On December 9, 2025, Mr. Gaëtan Dumont was appointed as member of the Board.

Colombia License Renewal

On November 13, 2025, the Company renewed its online gaming license in Colombia for a period of 5 years.

The current license will expire in November 2030.

Changes in Gaming Taxes

Effective January 1, 2026, the statutory excise tax rate applicable to gaming in Mexico (“IEPS”) was increased from 30 to 50%.

The value added (i.e. indirect) tax of 19% on all online deposits introduced through executive decree in Colombia in February 2025 expired on December 31, 2025.

Repurchases Under the Share Buyback Plan

The Company has repurchased 391 thousand shares for an aggregate amount of $2.7 million under its authorized share buyback plan through February 25, 2026.

The plan has an authorized total investment of $7.5 million or up to 1 million shares and expires on December 31, 2026.

Conference Call Information

Codere Online’s management will host a conference call to discuss the results and provide a business update at 8:30 am US Eastern Time today, February 26, 2026. Access links to the audio webcast and presentation will be accessible on Codere Online’s website at www.codereonline.com. A recording of the webcast will also be available following the conference call.

Reconciliation of Revenue (IFRS) to Net Gaming Revenue (non-IFRS)

Reconciliation of Net Income (IFRS) to Adj. EBITDA (non-IFRS)5

About Codere Online

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online, launched in 2014 as part of the renowned casino operator Codere Group, offers online sports betting and online casino through its state-of-the art website and mobile applications. Codere Online currently operates in its core markets of Spain, Mexico, Colombia, Panama and Argentina; this online business is complemented by Codere Group’s physical presence in Spain and throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence.

About Codere Group Codere Group is a multinational group dedicated to entertainment and leisure. It is a leading player in the private gaming industry, with four decades of experience and with presence in seven countries in Europe (Spain and Italy) and Latin America (Argentina, Colombia, Mexico, Panama, and Uruguay).

Note on Rounding. Due to decimal rounding, numbers presented throughout this report may not add up precisely to the totals and subtotals provided, and percentages may not precisely reflect the absolute figures.

Forward-Looking Statements Certain statements in this document may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements regarding Codere Online Luxembourg, S.A. and its subsidiaries (collectively, “Codere Online”) or Codere Online’s or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this document may include, for example, statements about Codere Online’s financial performance and, in particular, the potential evolution and distribution of its net gaming revenue; any prospective and illustrative financial information; and changes in Codere Online’s strategy, future operations and target addressable market, financial position, estimated revenues and losses, projected costs, prospects and plans.

These forward-looking statements are based on information available as of the date of this document and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Codere Online’s or its management team’s views as of any subsequent date, and Codere Online does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, Codere Online’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. There may be additional risks that Codere Online does not presently know or that Codere Online currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Some factors that could cause actual results to differ include (i) changes in applicable laws or regulations, including online gaming, privacy, data use and data protection rules and regulations as well as consumers’ heightened expectations regarding proper safeguarding of their personal information, (ii) the impacts and ongoing uncertainties created by regulatory restrictions, changes in perceptions of the gaming industry, changes in policies and increased competition, and geopolitical events such as war, (iii) the ability to implement business plans, forecasts, and other expectations and identify and realize additional opportunities, (iv) the risk of downturns and the possibility of rapid change in the highly competitive industry in which Codere Online operates, (v) the risk that Codere Online and its current and future collaborators are unable to successfully develop and commercialize Codere Online’s services, or experience significant delays in doing so, (vi) the risk that Codere Online may never achieve or sustain profitability, (vii) the risk that Codere Online will need to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all, (viii) the risk that Codere Online experiences difficulties in managing its growth and expanding operations, (ix) the risk that third-party providers, including the Codere Group, are not able to fully and timely meet their obligations, (x) the risk that the online gaming operations will not provide the expected benefits due to, among other things, the inability to obtain or maintain online gaming licenses in the anticipated time frame or at all, (xi) the risk that Codere Online is unable to secure or protect its intellectual property, (xii) the risk that Codere Online’s securities may be delisted from Nasdaq and (xiii) the possibility that Codere Online may be adversely affected by other political, economic, business, and/or competitive factors. Additional information concerning certain of these and other risk factors is contained in Codere Online’s filings with the U.S. Securities and Exchange Commission (the “SEC”). All subsequent written and oral forward-looking statements concerning Codere Online or other matters and attributable to Codere Online or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements above.

Financial Information and Non-GAAP Financial Measures Codere Online’s financial statements are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), which can differ in certain significant respects from generally accepted accounting principles in the United States of America (“U.S. GAAP”).

This document includes certain financial measures not presented in accordance with U.S. GAAP or IFRS (“non-GAAP”), such as, without limitation, net gaming revenue, Adjusted EBITDA and constant currency information. These non-GAAP financial measures are not measures of financial performance in accordance with U.S. GAAP or IFRS and may exclude items that are significant in understanding and assessing Codere Online’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to revenue, net income, cash flows from operations or other measures of profitability, liquidity or performance under U.S. GAAP or IFRS. You should be aware that Codere Online’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. In addition, the audit of Codere Online’s financial statements in accordance with PCAOB standards, may impact how Codere Online currently calculates its non-GAAP financial measures, and we cannot assure you that there would not be differences, and such differences could be material.

Codere Online believes that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in comparing Codere Online’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Reconciliations of non-GAAP financial measures to their most directly comparable measure under IFRS are included herein.

This document may include certain projections of non-GAAP financial measures. Codere Online is unable to quantify certain amounts that would be required to be included in the most directly comparable U.S. GAAP or IFRS financial measures without unreasonable effort, due to the inherent difficulty and variability of accurately forecasting the occurrence and financial impact of the various adjusting items necessary for such comparable measures or such reconciliation that have not yet occurred, are out of our control, or cannot be reasonably predicted, ascertained or assessed, which could have a material impact on its future IFRS financial results. Consequently, no disclosure of estimated comparable U.S. GAAP or IFRS measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included.

Use of Projections This document contains financial forecasts with respect to Codere Online’s business and projected financial results, including net gaming revenue and adjusted EBITDA. Codere Online’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this document, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this document. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Codere Online or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this document should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

For further information on the limitations and assumptions underlying these projections, please refer to Codere Online’s filings with the SEC.

Preliminary Information This document contains figures, financial metrics, statistics and other information that is preliminary and subject to change (the “Preliminary Information”). The Preliminary Information has not been audited, reviewed, or compiled by any independent registered public accounting firm. This Preliminary Information is subject to ongoing review including, where applicable, by Codere Online’s independent auditors. Accordingly, no independent registered public accounting firm has expressed an opinion or any other form of assurance with respect to the Preliminary Information. During the course of finalizing such Preliminary Information, adjustments to such Preliminary Information presented herein may be identified, which may be material. Codere Online undertakes no obligation to update or revise the Preliminary Information set forth in this document as a result of new information, future events or otherwise, except as otherwise required by law. The Preliminary Information may differ from actual results. Therefore, you should not place undue reliance upon this Preliminary Information. The Preliminary Information is not a comprehensive statement of financial results, and should not be viewed as a substitute for full financial statements prepared in accordance with IFRS. In addition, the Preliminary Information is not necessarily indicative of the results to be achieved in any future period.

No Offer or Solicitation This document does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor will there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended, or an exemption therefrom.

Industry and Market Data In this document, Codere Online relies on and refers to certain information and statistics obtained from publicly available information and third-party sources, which it believes to be reliable. Codere Online has not independently verified the accuracy or completeness of any such publicly-available and third-party information, does not make any representation as to the accuracy or completeness of such data and does not undertake any obligation to update such data after the date of this document. You are cautioned not to give undue weight to such industry and market data.

Contacts:

Investors and Media Guillermo Lancha Director, Investor Relations and Communications Guillermo.Lancha@codereonline.com (+34) 628.928.152

1 Net Gaming Revenue is a non-IFRS measure; please see reconciliation of Net Gaming Revenue to Revenue at the end of the report.

2 Adjusted EBITDA is a non-IFRS measure; please see reconciliation of Adjusted EBITDA to Net Income at the end of the report. Net gaming revenue and Adjusted EBITDA outlooks are forward-looking non-IFRS measures; please see important disclaimers at the end of the report. 3 See “Preliminary Information” below.

4 Figures primarily reflect differences in recognition of revenue related to certain partner and affiliate agreements in place in Colombia, VAT impact from entry fees in Mexico and the impact from the application of inflation accounting (IAS 29) in Argentina. 5 Please refer to page 25 of our Q4 2025 Earnings Presentation for further details regarding this reconciliation.

Toronto, Ontario–(Newsfile Corp. – February 26, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) reports that results have been delivered from 28 samples taken across the Balangero Ni-Co Project (the “Project”) in northern Italy. The samples were assayed at Laboratoire GeoRessources – École Nationale Supérieure de Géologie, Université de Lorraine. The samples yielded between 1560 and 2015 ppm nickel (average 1763 ppm), 81.5 to 108 ppm cobalt, and 16.2 to 146 ppm copper. These new results are in line with the more than 200 historical samples taken from the site.

Aurania’s President and CEO, Dr. Keith Barron, commented, “There is a lot of historic data from Balangero, and this confirmed what was already suspected. In 1942, the Italian Government created SANI (Societá Anonima Nichelio Italiana) specifically to look for sources of nickel within Italy. At Balangero, the magnetic sand-sized fraction of the waste from asbestos beneficiation was actually recovered and used to make hardened steel for some months in 1943 for the war effort. This information has remained buried in the Archive of the City of Turin. For a variety of reasons, nickel supply has once again become critically important in Europe, and we believe Balangero offers the most readily and easily accessible source of the metal today.”

The Balangero Mine (also called San Vittorio), 30 kilometres from the city of Turin in northern Italy, produced asbestos between 1918 and 1990 and was the largest open pit asbestos mine in Europe. During 1966, the waste from the mine was thoroughly investigated as a potential by-product source of nickel and cobalt. Aurania staff became acquainted with the project while doing a literature search on their Northern Corsica Ni-Co project. The Balangero site, like Corsica, contains an abundance of the mineral awaruite, a rather rare nickel-iron natural alloy that does not contain sulphur, and can be used as a direct source of furnace feed for stainless steel production, or processed downstream for EV Battery Grade nickel sulphate. As a potential source of “Green” nickel, it certainly aligns with the stated goals of the European Union (EU) for the extraction and production of Clean Critical Metals.

Several companies are looking at the small number of awaruite occurrences as potential sources of Green Nickel and Cobalt. Among them are FPX Nickel Corp, with a market capitalization of circa $183 million CAD, and First Atlantic Nickel Corp, with a market capitalization of $27 million CAD. FPX’s project is in northern British Columbia, and First Atlantic, in Central Newfoundland. Both are greenfields projects which will require the development of open pit mines. Both have limited site infrastructure, other than a few bush roads. Aurania’s Balangero Project is essentially identical in nickel grade to FPX and First Atlantic, but with the obvious difference in projects is that the potential resource at Balangero consists of dry-stacked tailings that have already been crushed to <4 centimetres. This material has already been extracted from the ground, negating any need for drilling, blasting, tunneling and haulage from the subsurface. Moreover, there is existing electric power to the site, a railhead less than a kilometre away, a paved highway to the mine gate, and an abundant source of skilled labour nearby.

A Preliminary Economic Assessment (PEA) for the Balangero Project, in progress by SRK International Consultants, will provide an estimation of Aurania’s proposed project capex, but obviously there is no need for expensive installation of infrastructure, overburden stripping, and mining of the rock, resulting in tremendous cost savings. The Company is discussing whether to carry out a Pre-feasibility Study (PFS) before the end of 2026. Recently, a legal opinion determined that Aurania could perform Sonic Drill Sampling and Bulk Sampling on the Project under the existing permits of our MOU partner, RSA, rather than submitting lengthy environmental impact studies. This would substantially accelerate the project timetable. The Company believes the Project could be fast-tracked under the European Union’s Critical Raw Materials Act. Nickel, cobalt and copper are all considered “Strategic Raw Materials” (SRM). The 17 SRM are a subset within the designated 34 Critical Raw Materials and are mandated to be domestically sourced in the EU.

Aurania has also had confirmation from Dr. Chiara Boschi at the Institute of Geosciences and Earth Resources (IGG-CNR, Pisa, Italy) that a number of the 28 collected samples from across the Balangero Project do not contain asbestos, but all contain awaruite. These samples which were asbestos-free were taken from old development rock piles. This suggests that the potential nickel resource at Balangero will ultimately consist of both crushed tailings and broken and excavated development rock at the surface. There is no historical measurement of the volume of these rock piles, though this will be assessed in future. We expect inclusion of these development rock piles to be accretive to the Project.

Comminution tests of the Balangero tailings are still in progress at STEVAL in Nancy, France. To date, the material appears amenable to easy extraction of the awaruite and magnetite, and there have been no “red flags”. A sonic drilling programme to confirm the grades and thicknesses in the main tailings pile is being contemplated for April 2026.

Qualified Persons: The geological information contained in this news release has been verified and approved by Aurania’s VP Exploration, Mr. Jean-Paul Pallier, MSc. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About Aurania Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes: that if results of the MOU prove favourable, a commercial agreement is expected to be entered into with respect to the extraction of minerals from the waste piles, the assumption that the waste pile may have the potential to contain circa 229,500 tonnes of nickel, that this represents a valuable resource which has already been extracted, crushed and dry-stacked, the expectation that the evaluation of 450 kg of material will provide mineralogical characterization and other expected information about such material, the timing to produce a Scoping Level Review on the Mineral Assets of the Balangero tailings retreatment project, Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the tonnage and grade of mineralization which has the potential for economic extraction and processing, the merits and effectiveness of known process and recovery methods, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that, there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things: failure to achieve the anticipated results, incorrect assumptions made in the initial evaluation of the project, failure to identify mineral resources; failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; the inability to recover and process mineralization using known mining methods; the presence of deleterious mineralization or the inability to process mineralization in an environmentally acceptable manner; commodity prices, supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and base metals; and those risks set out in the Company’s public documents filed on SEDAR+. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

WEST CHICAGO, Ill., Feb. 26, 2026 /PRNewswire/ — Titan International, Inc. (NYSE: TWI) (“Titan” or the “Company”), a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products, today reported financial results for the fourth quarter and year ended December 31, 2025. The full earnings release including a reconciliation of GAAP to Non-GAAP figures can be found in the investor relations section of the Company’s website at https://ir.titan-intl.com/news-and-events/news-releases/default.aspx.

Q4 2025 Key Figures

Revenues grew 7% to $410 million

Gross margin improved to 10.9%

Adjusted EBITDA increased 18% to $11 million

Paul Reitz, President and Chief Executive Officer, commented, “We wrapped-up 2025 with another positive quarter as our Q4 2025 results exceeded Q4 2024 in terms of revenue, gross margin and Adjusted EBITDA. Our EMC segment was a standout performer, with revenue growth of 21% and gross margin expansion of 3.4 percentage points. Importantly, we anticipate continued growth in this segment in 2026. Our Ag segment recorded a top-line increase of 2.6% in the fourth quarter, roughly flat excluding FX. Going into 2026 in Ag we expect demand for smaller equipment to outpace high-horsepower units as farmers continue to contend with elevated input costs and weaker commodity prices. In our Consumer segment, fourth quarter sales were up slightly within our Specialty division, while down modestly overall. Focusing on 2026, OEMs and their dealer networks look to have generally reached the end of their finished goods destocking and we expect to see some benefit from that as a result. A resumption in demand would therefore flow through to demand for tires, wheels and other components. It also bears repeating that our Consumer segment enjoys a high proportion of aftermarket sales and therefore is less susceptible to the OEM cycles.”

Mr. Reitz concluded, “Over the past couple years visibility across our end markets has been constrained — and that added complexity creates an advantage for Titan with our One Stop Shop strategy. Our diversified supply chain offers global manufacturing, strategic sourcing and JVs and this gives us flexibility to adapt quickly to the frequent changes we continue to see in trade policy and ultimately allows us to serve our customers better than anyone else. By keeping our customers at the forefront of everything we do, we continue to cement our market leadership position. We remain well positioned for an Ag market rebound and as always, we will continue to prioritize our customers and in doing so, we expect 2026 will be a good year for Titan.”

First Quarter and Fiscal Year 2026 Outlook

Tony Eheli, Chief Financial Officer, stated, “We ended the year with a strong balance sheet and maintained a disciplined expense profile that drove improvements in margin and profitability, while allowing us to continue to invest in our product, people, and processes. We expect to start 2026 with a seasonal uptick in activity with Q1 sales between $490 million and $510 million and Adjusted EBITDA between $28 million and $33 million. For the full year we are expecting revenue in the $1.85 to $1.95 billion range with Adjusted EBITDA between $105 million and $115 million.”

About Titan

Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the Company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

Safe Harbor Statement

This press release contains forward-looking statements. These forward-looking statements are covered by the safe harbor for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. The words “believe,” “expect,” “anticipate,” “plan,” “would,” “could,” “potential,” “may,” “will,” and other similar expressions are intended to identify forward-looking statements, which are generally not historical in nature. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effect on us. Although we believe the assumptions upon which these forward-looking statements are based are reasonable, these assumptions are subject to significant risks and uncertainties, and are subject to change based on various factors, some of which are beyond Titan International, Inc.’s control. As a result, any of these assumptions could prove to be inaccurate and the forward-looking statements based on these assumptions could be incorrect. The matters discussed in these forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results and trends to differ materially from those made, projected, or implied in or by the forward-looking statements depending on a variety of uncertainties or other factors including, but not limited to, the effect of geopolitical instability; the effect of a recession on the Company and its customers and suppliers; changes in the Company’s end-user markets into which the Company sells its products as a result of domestic and world economic or regulatory influences or otherwise; changes in the marketplace, including new products and pricing changes by the Company’s competitors; the Company’s ability to maintain satisfactory labor relations; unfavorable outcomes of legal proceedings; the Company’s ability to comply with current or future regulations applicable to the Company’s business and the industry in which it competes or any actions taken or orders issued by regulatory authorities; availability and price of raw materials; levels of operating efficiencies; the effects of the Company’s indebtedness and its compliance with the terms thereof; changes in the interest rate environment and their effects on the Company’s outstanding indebtedness; unfavorable product liability and warranty claims; actions of domestic and foreign governments, including the imposition of additional tariffs; geopolitical and economic uncertainties relating to the countries in which the Company operates or does business; risks associated with acquisitions, including difficulty in integrating operations and personnel, disruption of ongoing business, and increased expenses; results of investments; the realization of projected synergies; the effects of potential processes to explore various strategic transactions, including potential dispositions; fluctuations in currency translations; risks associated with environmental laws and regulations; risks relating to our manufacturing facilities, including that any of our material facilities may become inoperable; risks relating to financial reporting, internal controls, tax accounting, and information systems; and the other risks and factors detailed in the Company’s periodic reports filed with the Securities and Exchange Commission, including the disclosures under “Risk Factors” in those reports. These forward-looking statements are made only as of the date hereof. The Company cautions that any forward-looking statements included in this press release are subject to a number of risks and uncertainties, and the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, changed circumstances or future events, or for any other reason, except as required by law.

Nvidia delivered another quarter of eye-catching growth. Investors still found reasons to sell. Shares of the AI chip leader fell as much as 5.6% Thursday after its fiscal first-quarter revenue forecast, while ahead of average Wall Street estimates, failed to ease mounting concerns about how long the artificial intelligence spending boom can last. The decline marked the stock’s sharpest intraday drop in three months.

On paper, the results were hard to fault. Nvidia projected fiscal first-quarter revenue of about $78 billion, topping the average analyst estimate of $72.8 billion, though some forecasts had climbed closer to $80 billion in recent weeks. For the fiscal fourth quarter, revenue surged 73% to $68.1 billion, beating expectations. Adjusted earnings of $1.62 per share and gross margins of 75.2% also edged past consensus estimates.

The company’s data center division — which includes its AI accelerators and networking products — generated $62.3 billion in quarterly revenue, above projections. That business has become the centerpiece of Nvidia’s growth story as hyperscale cloud providers and enterprises race to build AI infrastructure.

Other segments were softer. Gaming revenue of $3.73 billion and automotive revenue of $604 million both trailed analyst expectations. Ongoing memory supply constraints have weighed on certain product lines, highlighting that even Nvidia is not immune to broader semiconductor supply dynamics.

The market reaction underscores a key shift: Expectations are now extraordinarily high. After explosive gains over the past two years tied to generative AI demand, investors are increasingly focused on sustainability rather than acceleration.

CEO Jensen Huang pushed back against fears of an AI bubble during the earnings call, arguing that customers are already generating returns from their AI investments. According to Huang, expanding compute capacity directly supports revenue growth for Nvidia’s clients, reinforcing the case for continued infrastructure buildouts.

Still, questions remain. Nvidia disclosed $95.2 billion in purchase obligations, up sharply from $16.1 billion a year earlier. While those commitments reflect efforts to secure supply and meet anticipated demand — with shipments extending into calendar 2027 — they also raise the stakes if capital spending slows.

Geopolitical uncertainty adds another layer. The company has received limited U.S. government licenses to ship certain processors to China, but data center revenue from the country remains excluded from guidance. Tariffs and inspection requirements create additional friction in an already complex global supply chain.

At the same time, Nvidia and its competitors are announcing large, long-term agreements with major customers to lock in computing capacity. Nvidia recently disclosed that Meta Platforms plans to deploy “millions” of its processors in the coming years, while Advanced Micro Devices announced its own multibillion-dollar AI infrastructure deal. These agreements are designed to demonstrate durable demand, though some observers caution that increasingly intertwined supplier-customer relationships can complicate traditional demand signals.

For investors, Nvidia’s quarter reflects a broader capital markets dynamic heading into 2026. Growth is still robust, but markets are scrutinizing visibility, balance sheet commitments, and the durability of capital expenditures more closely.

The AI buildout remains one of the most significant investment cycles in technology history. Nvidia’s latest results suggest momentum is intact. The stock’s reaction shows that confidence in how long it lasts is now the real debate.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updates it corporate presentation. Management recently updated its corporate presentation to provide more detail around the company’s four pillar initiative to transform it toward a more profitable, scalable, growth oriented company. The four key pillars: achieving cost savings and operational efficiency, strengthening customer focus, expanding reach beyond e-commerce, and enhancing talent alignment and accountability.

Omnichannel Expansion. The company is expanding distribution channels beyond its owned e-commerce platforms. The Company is meeting customers where they already shop by leveraging leading third-party marketplaces to lower acquisition friction and expand reach. These marketplace channels are intended to complement owned platforms, while selective physical retail testing will occur under strict ROI thresholds.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The E.W. Scripps Company (NASDAQ: SSP) is a diversified media company focused on creating a better-informed world. As one of the nation’s largest local TV broadcasters, Scripps serves communities with quality, objective local journalism and operates a portfolio of 61 stations in 41 markets. The Scripps Networks reach nearly every American through the national news outlets Court TV and Newsy and popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, Laff and TrueReal. Scripps is the nation’s largest holder of broadcast spectrum. Scripps runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. Founded in 1878, Scripps has held for decades to the motto, “Give light and the people will find their own way.”

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Better than expected Q4. Total Q4 revenues of $560.3 million was better than our $550.9 million estimate, due to better than expected Core Local advertising and better Scripps Networks revenue. Adj. EBITDA of $86.4 million beat our $75.6 million estimate on lower segment expenses, particularly in its Networks segment.

Core advertising stronger than expected. Core Advertising revenue increased a strong 12.2% to $165.4 million, better than our estimate of $162.0 million. It is not surprising given the record amount of year earlier Political advertising that there would be a large level of Core Advertising displacement. But, we are pleased that Core Advertising reflected a strong rebound in the quarter, even better than what we were looking for.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Kratos finished 2025 exceeding management’s financial objectives for the fourth quarter, generating approximately 20% year- over-year organic revenue growth, generating a 1.3 to 1.0 book-to-bill ratio on top of the organic growth, having a record backlog of $1.573 billion, and a record opportunity pipeline of $13.7 billion.

4Q25 Results. Fourth quarter revenue of $345.1 million reflected 20% y-o-y organic growth and exceeded our $320 million estimate. Unmanned Systems’ organic revenue growth was 12.1%, while Government Solutions saw 22.2% organic growth. Kratos recorded adjusted EBITDA of $34.1 million, up from $25.2 million a year ago and our $31 million estimate. Adjusted EPS came in at $0.18 versus $0.13 last year and our $0.14 estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 and FY2025 financial results. Fourth quarter net revenue increased 7.7% to $57.4 million compared to $53.3 million during the prior year period. Adjusted EBITDA and EPS were $40.7 million and $4.48, respectively, compared to $32.8 million and $3.33 during the prior year quarter. During the fourth quarter, the average time charter equivalent rate amounted to $30,268 per day compared to $26,479 during the prior year period. The company reported FY2025 adjusted EBITDA and EPS of $155.9 million and $16.74, respectively, compared to $135.8 million and $14.87 in 2024.

Revenue and earnings visibility. For 2026, Euroseas has secured 86.6% of available voyage days at an average rate of ~$30,700 per day and 71.1% of 2027 available voyage days at an average rate of $31,890 per day. For 2028, 40.8% of available voyage days are covered at ~$32,400 per day. This robust charter coverage not only underpins earnings but also provides a strong buffer against rate volatility, positioning the company to benefit from sustained high utilization in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FY2026 Reported With Onvansertib Review. Cardiff reported a FY2025 loss of $45.8 million or $(0.69) per share and reviewed the clinical data for onvansertib, its drug for RAS-mutated metastatic colorectal cancer (mCRC). Updated plans for Phase 3 are expected after discussions with the FDA during 1H26. On December 31, 2025, Cardiff ended the year with $58.3 million in cash and equivalents, which it believes can fund operations through 1Q27.

Phase 2 CRDF-004 Trial Design. The CDRF-004 Phase 2 trial was designed to test two doses of onvansertib in combination with two standard-of-care (SOC) regimens against each standard of care regimen alone. It enrolled 110 patients with RAS-mutated mCRC. The primary endpoint was objective response rate (ORR).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Google is doubling down on generative AI with the launch of Nano Banana 2, the latest version of its viral AI image generator. The update, announced Thursday, is designed to make the tool faster, more precise and better at rendering text — a key improvement for use cases such as marketing mockups, greeting cards and branded visuals. The rollout underscores how aggressively large technology platforms are iterating in the increasingly competitive AI image and video market.

Shares of Alphabet traded lower alongside the broader tech market, but the Nano Banana refresh highlights the company’s continued push to integrate generative AI deeper into its Gemini ecosystem.

Nano Banana first launched in August and quickly gained traction online as users shared AI-generated images across social platforms. Google followed with Nano Banana Pro in November, built on Gemini 3 Pro, targeting higher-fidelity and more accuracy-sensitive use cases.

Nano Banana 2 is now positioned as the speed-optimized successor.

According to Google, the new model incorporates “advanced world knowledge,” pulling real-time information from Gemini to produce more accurate visual renderings. The company emphasized three primary upgrades: faster generation, improved instruction-following and more precise text rendering inside images — an area where AI image models have historically struggled.

While Nano Banana Pro will remain available for high-fidelity tasks requiring maximum factual precision, Nano Banana 2 is being positioned for rapid creation and integrated image-search grounding. The new version will replace its predecessor across Gemini’s Fast, Thinking and Pro tiers.

The move comes as AI image and video tools are becoming mainstream consumer products. Users can now generate increasingly sophisticated visuals from simple text prompts, blurring the line between professional and consumer-grade creative tools.

Competition in the space is intensifying.

OpenAI launched its video-generation model Sora in 2024, drawing massive demand. Adobe has continued expanding Firefly, integrating generative AI across its creative software suite. ByteDance has also introduced its Seedance video-generation tool, though it has faced legal scrutiny from major studios over alleged intellectual property violations.

The rapid adoption of AI creative tools has also fueled debate around copyright, training data and the protection of original content. Media and entertainment companies have raised concerns that generative models may infringe on protected works, increasing regulatory and legal uncertainty across the sector.

For investors, Google’s Nano Banana 2 rollout highlights a broader capital allocation theme in 2026: speed of iteration is becoming a competitive advantage in AI.

Large platforms are not only investing heavily in infrastructure — such as GPUs and data centers — but are also racing to deliver user-facing AI products that drive engagement, subscription upgrades and enterprise adoption.

The generative AI market is still in its early innings. However, with major players rolling out new versions in rapid succession, product cycles are shortening, and differentiation is increasingly tied to performance, reliability and integration with broader ecosystems.

Nano Banana 2 may be an incremental upgrade. But in today’s AI arms race, incremental improvements — delivered quickly — can shape market leadership.

Clinical development is inherently capital intensive. As programs move from early-stage studies into Phase 2 and Phase 3 trials, costs typically rise due to expanded enrollment, multi-site coordination, manufacturing scale-up, and regulatory preparation.

Companies such as Eledon Pharmaceuticals, which is advancing immune-modulating therapies, and Cardiff Oncology, focused on targeted oncology treatments including onvansertib, illustrate the type of clinical-stage businesses navigating these funding dynamics. As programs mature, capital planning becomes increasingly tied to milestone timing.

Similarly, Ocugen, with gene therapy and ophthalmology-focused programs, and Cocrystal Pharma, which develops antiviral therapeutics, operate in segments where development timelines and regulatory pathways can require sustained financial flexibility.

Even companies earlier in commercialization strategy development, such as Nutriband, which is advancing transdermal pharmaceutical technologies, must balance product advancement with capital market realities.

These examples reflect a broader sector pattern: advancing innovation requires consistent access to funding.

The Importance of the Catalyst Calendar

Biotech financing windows often open around meaningful clinical or regulatory catalysts. Positive data can strengthen negotiating leverage. But waiting until after results are announced can introduce risk — particularly if broader market conditions shift.

With 2026 shaping up to include a number of anticipated data readouts across the industry, companies are evaluating whether to raise capital ahead of milestones, opportunistically during periods of sector strength, or in response to results.

Preparation matters.

Management teams that establish investor visibility and maintain consistent communication before catalysts emerge may find themselves better positioned if and when market windows open.

M&A Activity Is a Tailwind — Not a Strategy

Large pharmaceutical companies continue to evaluate external pipelines to supplement internal research efforts. Periodic acquisition activity can improve sentiment across small-cap biotech and help reset valuation benchmarks.

However, M&A remains selective and unpredictable. Most clinical-stage companies must plan under the assumption that equity or structured financing will remain the primary funding path.

For investors, that distinction is important.

Why Capital Strategy Matters for Shareholders

In small-cap biotech, capital access influences more than just cash runway. It can affect development pace, trial continuity, partnership leverage, and dilution levels.

A company that secures funding under stable market conditions may retain greater operational flexibility. One that is forced to raise under pressure may encounter less favorable terms.

As 2026 approaches, the differentiator may not simply be who generates data — but who manages capital strategy effectively alongside clinical execution.

Biotech remains data-driven and inherently volatile. Yet improving sector sentiment and a growing milestone calendar suggest that capital formation decisions could play a defining role in shaping outcomes over the next 12–18 months.

For small-cap investors, understanding both the science and the financing strategy may be equally important in the year ahead.

EL SEGUNDO, Calif.–(BUSINESS WIRE)– The Beachbody Company, Inc. (NASDAQ: BODI) (“BODi” or the “Company”), a leading fitness and nutrition company, will release its fourth quarter 2025 results on Tuesday, March 10, 2026, after the U.S. stock market closes. The Company will host a conference call at 5:00 p.m. (Eastern Time) that day to discuss the results.

For those unable to participate in the conference call, a replay will be available after the conclusion of the call on March 10, 2026, through March 17, 2026. The toll-free replay dial-in number is (866) 813-9403 (U.S & Canada). The replay passcode is 989620.

About BODi and The Beachbody Company, Inc.

BODi, formerly known as Beachbody, has been a pioneer in structured, step-by-step home fitness and nutrition programs for nearly three decades, with iconic products such as P90X, INSANITY, 21 Day Fix and the original premium superfood nutrition supplement, Shakeology. Since its inception, BODi has helped more than 30 million people reach life-changing results. Today, BODi continues to evolve with a simple mission: help people achieve their goals and lead healthier, more fulfilling lives, especially busy, time-strapped people who want to fit healthy habits into everyday life with proven solutions. The BODi community empowers millions to stay motivated and accountable, supporting healthy weight management, improved metabolic function, increased mental and physical well-being, better sleep, as well as evidence-based habits that enhance healthspan and longevity.