Revenues Increased 148.4% to $211.1 Million Benihana Same Store Sales Increased 0.7% and STK Transactions Increased 4.1%

DENVER–(BUSINESS WIRE)– The ONE Group Hospitality, Inc. (“The ONE Group” or the “Company”) (Nasdaq: STKS) today reported its financial results for the first quarter ended March 30, 2025.

Highlights for the first quarter 2025 compared to the same quarter in 2024 are as follows (the prior year quarter excludes any contribution from the acquisition of Benihana Inc. which closed in May 2024):

Total GAAP revenues increased 148.4% to $211.1 million from $85.0 million;

Consolidated comparable sales*decreased 3.2%;

Operating income increased$11.3 million to $10.7 million from an operating loss of $0.6 million;

Restaurant EBITDA**increased 162.7% to $34.0 million from $12.9 million;

GAAP net loss available to common stockholders was $6.6 million, or $0.21 net loss per share ($0.14 adjusted net income per share)***, compared to GAAP net loss available to common stockholders of $2.1 million, or $0.07 net loss per share ($0.02 adjusted net loss per share)***

Adjusted EBITDA**** attributable to The ONE Group Hospitality, Inc. increased 233% to $25.2 million from $7.6 million.

“We were pleased that revenues, comparable sales and adjusted EBITDA reached or exceeded the higher end of our guided ranges. These accomplishments were driven by another quarter of sequential improvement in our comparable sales trend, positive comparable sales at our Benihana restaurants and strong positive transaction growth of 4.1% at our flagship STK brand. Notably, adjusted EBITDA grew 233% to $25.2 million, significantly exceeding our top-line growth and demonstrating our ability to increase profitability through the execution of our initiatives, tight cost management and our growing economies of scale. We are reiterating our full year guidance for 2025 and remain on track to deliver at least $20 million in acquisition synergies by 2026,” said Emanuel “Manny” Hilario, President and CEO of The ONE Group.

“In 2025, we plan to open five to seven new venues. Over the long term, we aim to balance our significant unit growth opportunities between company-owned and asset-light development, driving shareholder returns while maintaining flexibility in our balance sheet,” Hilario concluded.

Restaurant Development

The Company plans to open five to seven new venues in 2025.

Date

Brand

Location

Type

Status

March 2025

Benihana

San Mateo, California

Owned

Open

April 2025

STK

Topanga, California

Owned

Open

May 2025

STK

Los Angeles, California

Owned

Under Construction (re-location)

Upcoming

Kona Grill

Seattle, Washington

Owned

Under Construction

Liquidity and Share Repurchase Program

As of March 30, 2025, we held $34.1 million in cash and short-term credit card receivables and had $33.6 million available under our revolving credit facility. Under the current conditions, our credit facility does not have any financial covenants.

In March 2024, our Board of Directors authorized a $5 million share repurchase program. During the first quarter ended March 30, 2025, the Company purchased 0.1 million shares for aggregate consideration of $0.3 million

2025 Targets

As of January 1, 2025, we will report financial information on a fiscal quarter basis using four 13-week quarters with the addition of a 53rd week when necessary. For 2025, our fiscal calendar begins on January 1, 2025 and ends on December 28, 2025 and our first quarter had 89 days.

Financial Results and Other Select Data US$s in millions

Q2 2025 Guidance June 29, 2025

2025 Guidance December 28, 2025

Total GAAP revenues

$205 to $210

$835 to $870

Consolidated comparable sales

-5.5% to -4%

-3% to 1%

Managed, license and franchise fee revenues

$3 to $4

$15 to $16

Total owned operating expenses as a percentage of owned restaurant net revenue

Approx. 83%

83.5% to 82.2%

Consolidated total G&A, excluding stock-based compensation

Approx. $11

Approx. $47

Consolidated Adjusted EBITDA*

$23 to $25

$95 to $115

Consolidated restaurant pre-opening expenses

$1.5 to $2

$7 to $8

Consolidated effective income tax rate

Approx. 7.5%

Consolidated total capital expenditures, net of allowances received by landlords

$45 to $50

Consolidated number of new system-wide venues

2 new venues

5-7 new venues

*We have not reconciled guidance for Consolidated Adjusted EBITDA to the corresponding GAAP financial measure because we do not provide guidance for the various reconciling items. We are unable to provide guidance for these reconciling items because we cannot determine their probable significance, as certain items are outside of our control and cannot be reasonably predicted since these items could vary significantly from period to period. Accordingly, reconciliations to the corresponding GAAP financial measure are not available without unreasonable effort.

Conference Call and Webcast

Emanuel “Manny” Hilario, President and Chief Executive Officer, and Tyler Loy, Chief Financial Officer, will host a conference call and webcast today at 4:30 PM Eastern Time.

The conference call can be accessed live over the phone by dialing 412-542-4186. A replay will be available after the call and can be accessed by dialing 412-317-6671; the passcode is 10198138. The replay will be available until Thursday, May 22, 2025.

The webcast can be accessed from the Investor Relations tab of The ONE Group’s website at www.togrp.com under “News / Events.”

About The ONE Group

The ONE Group Hospitality, Inc. (Nasdaq: STKS) is an international restaurant company that develops and operates upscale and polished casual, high-energy restaurants and lounges and provides hospitality management services for hotels, casinos and other high-end venues both in the U.S. and internationally. The ONE Group’s focus is to be the global leader in Vibe Dining, and its primary restaurant brands and operations are:

STK, a modern twist on the American steakhouse concept with restaurants in major metropolitan cities in the U.S., Europe and the Middle East, featuring premium steaks, seafood and specialty cocktails in an energetic upscale atmosphere.

Benihana, an interactive dining destination with highly skilled chefs preparing food right in front of guests and served in an energetic atmosphere alongside fresh sushi and innovative cocktails. The Company franchises Benihanas in the U.S., Caribbean, Central America, and South America.

Kona Grill, a polished casual, bar-centric grill concept with restaurants in the U.S., featuring American favorites, award-winning sushi, and specialty cocktails in an upscale casual atmosphere.

RA Sushi, a Japanese cuisine concept that offers a fun-filled, bar-forward, upbeat, and vibrant dining atmosphere with restaurants in the U.S. anchored by creative sushi, inventive drinks, and outstanding service.

Salt Water Social is your gateway to the seven seas, featuring an array of signature and unique fresh seafood items, complemented by the highest quality beef dishes and elegant, delicious cocktails.

Samurai, an interactive dining experience located in sunny Miami, FL and soon to be in Westwood, CA, provides a distinctive dining experience where skilled personal chefs masterfully perform the ancient art of teppanyaki, anywhere from two to twenty tables, right before your eyes along with a robust selection of steak offerings.

ONE Hospitality, The ONE Group’s food and beverage hospitality services business develops, manages and operates premier restaurants and turnkey food and beverage services within high-end hotels and casinos currently operating venues in the U.S. and Europe.

Additional information about The ONE Group can be found at www.togrp.com.

Non-GAAP Definitions

We have evolved our definition of non-GAAP financial measures starting in Q3 2024 and Q1 2025. We use certain non-GAAP measures in analyzing operating performance and believe that the presentation of these measures provides investors and analysts with information that is beneficial to gaining an understanding of the Company’s financial results. Non-GAAP disclosures should not be viewed as a substitute for financial results determined in accordance with GAAP.

We exclude items management does not consider in the evaluation of its ongoing core operating performance from adjusted net income, adjusted net income / (loss) per share, and Adjusted EBITDA. Starting in Q3 2024, we no longer deduct pre-opening expenses from Adjusted EBITDA. Starting in Q1 2025, we are deducting Series A Preferred Stock paid in kind dividend and accretion from adjusted net income / (loss). Reconciliations of these non-GAAP measures are included under “Reconciliation of Non-GAAP Measures” in this press release.

*Comparable sales represent total U.S. food and beverage sales at owned and managed units, a non-GAAP financial measure, opened for at least a full 24-months. This measure includes total revenue from our owned and managed locations. The Company monitors sales growth at its established restaurant base in addition to growth that results from restaurant acquisitions and new restaurant openings. Refer to the reconciliation of GAAP revenue to total food and beverage sales at owned and managed units in this press release.

**We define Restaurant EBITDA as owned restaurant net revenue minus owned restaurant cost of sales and owned restaurant operating expenses before non-cash rent. Restaurant EBITDA has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of Operating income to Restaurant EBITDA in this press release.

***We define adjusted net income / (loss) as net income / (loss) available to common stockholders before Series A Preferred Stock paid-in-kinddividend andaccretion, transaction and exit expenses, transition and integration expenses, non-cash rent during the pre-opening period, other non-recurring costs and the income tax effect of any adjustments. Adjusted net income / (loss) has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of net (loss) / income to adjusted net income / (loss) available to common stockholders in this press release.

****We define Adjusted EBITDA as net income before interest expense, provision for income taxes, depreciation and amortization, non-cash impairment loss, non-cash rent expense, non-recurring gains and losses, stock-based compensation, transaction and exit costs and transition and integration expenses. Starting in Q3 2024, pre-opening expenses are no longer deducted from Adjusted EBITDA. Adjusted EBITDA has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of Net Income to Adjusted EBITDA in this press release.

Cautionary Statement on Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including with respect to the impact of the Benihana Inc. acquisition, restaurant openings and 2025 financial targets. Forward-looking statements may be identified by the use of words such as “target,” “intend,” “anticipate,” “believe,” “expect,” “estimate,” “plan,” “outlook,” and “project” and other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. A number of factors could cause actual results or outcomes to differ materially from those indicated by such forward-looking statements, including but not limited to: (1) our ability to integrate the new or acquired restaurants into our operations without disruptions to operations; (2) our ability to capture anticipated synergies; (3) our ability to open new restaurants and food and beverage locations in current and additional markets, grow and manage growth profitably, maintain relationships with suppliers and obtain adequate supply of products and retain employees; (4 )factors beyond our control that affect the number and timing of new restaurant openings, including weather conditions and factors under the control of landlords, contractors and regulatory and/or licensing authorities; (5) our ability to successfully improve performance and cost, realize the benefits of our marketing efforts and achieve improved results as we focus on developing new management and license deals; (6) changes in applicable laws or regulations; (7) the possibility that The ONE Group may be adversely affected by other economic, business, and/or competitive factors, including economic downturns; (8) the impact of actual and potential changes in immigration policies and the imposition of tariffs, including increases in food prices and inflation and potential labor shortages and any resulting negative impacts on the macro-economic environment; and (9) other risks and uncertainties indicated from time to time in our filings with the Securities and Exchange Commission, including our Annual Report on Form 10-K filed for the year ended December 31, 2024 and Quarterly Reports on Form 10-Q.

Investors are referred to the most recent reports filed with the Securities and Exchange Commission by The ONE Group Hospitality, Inc. Investors are cautioned not to place undue reliance upon any forward-looking statements, which speak only as of the date made, and we undertake no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

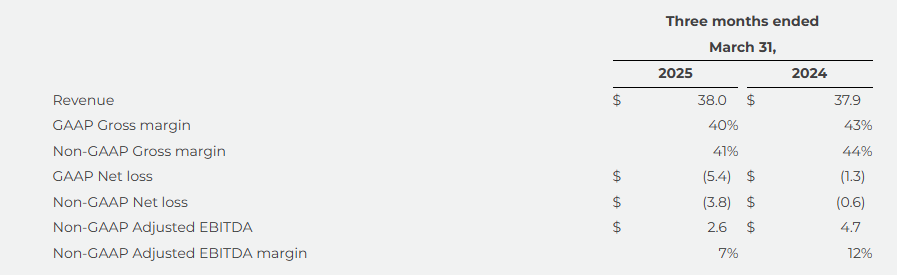

NORWOOD, Mass., May 07, 2025 (GLOBE NEWSWIRE) — MariMed Inc. (“MariMed” or the “Company”) (CSE: MRMD) (OTCQX: MRMD), a leading multi-state cannabis operator focused on improving lives every day, today announced its financial results for the first quarter ended March 31, 2025.

Management Commentary

“We are executing on our vision to build the best consumer packaged goods company in cannabis, and over the past quarter we continued to penetrate more storefronts and capture more market share for our innovative, high-quality portfolio of brands,” said Jon Levine, MariMed Chief Executive Officer. “Our Betty’s Eddies™ cannabis chews remained the top-selling edible in Massachusetts, Maryland, and Delaware, and moved up to the #5 position in Illinois after its launch there just over a year ago. Our other core brands also achieved strong market share growth as we sold our products into 70 new storefronts. Wholesale sales now account for 44 percent of our revenue mix, an upward trend that we anticipate will continue as we further leverage our brands as the primary growth engine for the Company.”

“We are pleased to report sequential revenue growth in the first quarter of 2025, driven by continued strength in wholesale performance,” said Mario Pinho, MariMed Chief Financial Officer. “Wholesale sales helped to offset the financial impact of a soft quarter at retail as well as ramp-up costs associated with our new assets in Illinois and Missouri. We remain confident in delivering enhanced shareholder value through expanded brand distribution into new storefronts; the pursuit of new revenue streams, including through M&A, brand licensing, and potential entry into the hemp space; and a continued focus on disciplined cost management, operational efficiencies, and improved execution.”

Financial Highlights1

The following table summarizes the Company’s consolidated financial highlights (in millions, except percentage amounts):

1 See the reconciliations of non-GAAP financial measures to the most directly comparable GAAP measures and additional information about non-GAAP measures in the section entitled “Discussion of Non-GAAP Financial Measures” below and in the financials information included herewith.

CONFERENCE CALL

MariMed management will host a conference call on Thursday, May 8, 2025 at 8:00 a.m. Eastern time, to discuss these results. The conference call may be accessed through MariMed’s Investor Relations website, or by clicking the following link: Q125 MRMD Earnings Call.

FIRST QUARTER 2025 OPERATIONAL HIGHLIGHTS

During the first quarter, the Company announced the following development in the implementation of its strategic growth plan:

February 28: Completed its acquisition of First State Compassion Center (“FSCC”), the leading cannabis operator in Delaware, in accordance with the terms of the previously announced Omnibus Agreement entered into with FSCC in July 2023. The acquisition integrates FSCC’s cultivation and processing facilities and two dispensaries into MariMed’s fully vertical operations, further enhancing the Company’s revenue and profitability.

OTHER DEVELOPMENTS

Subsequent to the end of the first quarter, the Company announced the following further developments:

April 1: Commenced distribution of its Nature’s Heritage™-branded cannabis flower, pre-rolls, and vapes in Illinois, marking the first time the brand’s premium products are available in the state.

April 3: Expanded the line-up of its top-selling Betty’s Eddies™-branded cannabis chews with the introduction of a new caramel chew, Betty’s Caramelt Away.

April 8: Promoted Ryan Crandall to Chief Commercial Officer to lead the Company’s commercial strategy and activities, including Sales, Marketing, Product Development, and Retail Operations. He had served as the Company’s Chief Revenue Officer since July 2022, and prior was its Chief Products Officer and SVP, Sales for four years.

DISCUSSION OF NON-GAAP FINANCIAL MEASURES

MariMed’s management uses several different financial measures, both GAAP and non-GAAP, in analyzing and assessing the overall performance of its business, making operating decisions, and planning and forecasting future periods. The Company has provided in this release several non-GAAP financial measures: Non-GAAP Adjusted EBITDA and non-GAAP Adjusted EBITDA margin, Non-GAAP Gross margin, Non-GAAP Operating expenses and Non-GAAP Net income (loss), as supplements to Revenue, Gross margin, Operating expenses, Income (loss) from operations, Net income (loss) and other financial measures prepared in accordance with GAAP.

Management believes these non-GAAP financial measures are useful in reviewing and assessing the performance of the Company, and when planning and forecasting future periods, as they provide meaningful operating results by excluding the effects of expenses that are not reflective of its operating business performance. In addition, the Company’s management uses these non-GAAP financial measures to understand and compare operating results across accounting periods and for financial and operational decision-making. The presentation of these non-GAAP measures is not intended to be considered in isolation or as a substitute for the financial information prepared in accordance with GAAP.

Management believes that investors and analysts benefit from considering non-GAAP financial measures in assessing the Company’s financial results and its ongoing business, as it allows for meaningful comparisons and analysis of trends in the business. In particular, non-GAAP adjusted EBITDA is used by many investors and analysts themselves, along with other metrics, to compare financial results across accounting periods and to those of peer companies.

As there are no standardized methods of calculating non-GAAP financial measures, the Company’s calculations may differ from those used by analysts, investors and other companies, even those within the cannabis industry, and therefore may not be directly comparable to similarly titled measures used by others.

Management defines non-GAAP Adjusted EBITDA as income (loss) from operations, determined in accordance with GAAP, excluding the following items:

depreciation and amortization of property and equipment;

amortization of acquired intangible assets;

impairment or write-downs of acquired intangible assets;

inventory revaluation;

stock-based compensation;

severance;

legal settlements; and

acquisition-related and other expenses.

For further information, please refer to the publicly available financial filings available on MariMed’s Investor Relations website, as filed with the U.S. Securities and Exchange Commission, or as filed with the Canadian securities regulatory authorities on the SEDAR website.

ABOUT MARIMED

MariMed Inc. is a leading multi-state cannabis operator, known for developing and managing state-of-the-art cultivation, production, and retail facilities. Our award-winning portfolio of cannabis brands, including Betty’s Eddies™, Bubby’s Baked™, Vibations™, InHouse™, and Nature’s Heritage™, sets us apart as an industry leader. These trusted brands, crafted with quality and innovation, are recognized and loved by consumers across the country. With a commitment to excellence, MariMed continues to drive growth and set new standards in the cannabis industry. For additional information, visit www.marimedinc.com.

IMPORTANT CAUTION REGARDING FORWARD-LOOKING STATEMENTS:

The information in this release contains “forward-looking” statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, which are subject to several risks and uncertainties. All statements other than statements of historical facts contained in this release, including without limitation statements regarding projected financial results for 2025, including anticipated openings of dispensaries and facilities, timing of regulatory approvals, plans and objectives of management for future operations, are forward-looking statements. Without limiting the foregoing, the words “anticipates”, “believes”, “estimates”, “expects”, “expectations”, “intends”, “may”, “plans”, and other similar language, whether in the negative or affirmative, are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

Forward-looking statements are based on our current beliefs and assumptions regarding our business, timing of regulatory approvals, the ability to obtain new licenses, business prospects and strategic growth plan, and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Our actual results may differ materially from those contemplated in these forward-looking statements due to various risks, uncertainties, and other important factors, including, among others, reductions in customer spending, our ability to recruit and retain key personnel, and disruptions from the integration efforts of acquired companies.

These factors are not intended to be an all-encompassing list of risks and uncertainties that may affect our business and results of operations. These statements are not a guarantee of future performance and involve risk and uncertainties that are difficult to predict, including, among other factors, changes in demand for the Company’s services and products, changes in the law and its enforcement, and changes in the economic environment. Additional information regarding these and other factors can be found in our reports filed with the U.S. Securities and Exchange Commission. In providing these forward-looking statements, the Company expressly disclaims any obligation to update these statements publicly or otherwise, whether as a result of new information, future events or otherwise, except as required by law.

All trademarks and service marks are the property of their respective owners.

For More Information Contact:

Howard Schacter, Chief Communications Officer Email: hschacter@marimedinc.com Phone: (781) 277-0007

SAN DIEGO, May 07, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, today announced it will webcast a special presentation from President and CEO Eric DeMarco as part of its 2025 Annual Meeting of Shareholders. The webcast will be open to the public and will take place on Wednesday, May 14, 2025, at 9:00 a.m. PDT.

During the webcast, Mr. DeMarco will provide a comprehensive business-wide update covering Kratos’ strategic priorities, operational highlights, technology initiatives, and market outlook across all divisions. The presentation will also highlight the company’s progress in hypersonic systems, unmanned platforms, propulsion, space-based capabilities, and dual-use technologies.

Shareholders who have logged into the meeting with their 16-digit Control Number will have the opportunity to submit questions relevant to the matters properly addressed during the meeting after the formal business of the meeting has been conducted. Instructions for submitting questions will be provided to shareholders once logged into the meeting. The Annual Meeting is open to shareholders of record as of March 17, 2025 (Record Date) and/or their designated representatives. Interested persons who were not shareholders as of the close of business on the Record Date may view, but not participate in, the Annual Meeting at www.virtualshareholdermeeting.com/KTOS2025.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Alphabet shares dropped more than 8% on Wednesday following comments from Apple’s senior vice president of services, Eddy Cue, who warned that artificial intelligence-powered tools could soon overtake traditional search engines like Google. Cue made the remarks during his testimony in a federal court in Washington, where the Department of Justice is pursuing an antitrust case against Alphabet.

According to reporting from Bloomberg, Cue said he expects that advanced AI services—such as those from OpenAI, Perplexity, and Anthropic—will eventually become key search tools and will likely be added as options in Apple’s Safari browser. The implication is clear: the long-standing dominance of Google in the search space may be approaching a turning point.

The market reaction was swift. Alphabet’s stock tumbled by 7.7%, shaving billions off its market cap, while Apple’s shares dipped by nearly 2%, signaling broader investor concern over the shifting dynamics of the search engine ecosystem.

Cue’s testimony comes at a critical moment. The Justice Department’s lawsuit centers on Google’s dominance in digital advertising and its long-running practice of paying companies—particularly Apple—billions of dollars annually to remain the default search engine on their platforms. In 2022 alone, Google is believed to have paid Apple as much as $20 billion for this privilege.

While the partnership has been lucrative for both tech giants, Cue’s comments suggest cracks are forming. He admitted he’s “lost sleep” over the possibility of Apple losing its massive revenue share from Google, yet he also acknowledged the surge in AI adoption is starting to impact user behavior. In fact, he revealed that search queries in Safari declined in April for the first time—something he attributes to users increasingly turning to generative AI platforms to answer questions and find information.

This trend could reshape the entire search business. If users shift from traditional keyword-based engines to conversational AI tools capable of synthesizing and contextualizing results, Google’s core advertising model—which relies heavily on search traffic—could face existential pressure.

The irony is that Apple, while currently a beneficiary of Google’s dominance through revenue sharing, is now signaling it may contribute to that dominance unraveling. By embracing AI competitors as viable alternatives to Google in Safari, Apple may be preparing for a future in which users prefer personalized, context-rich AI interactions over the standard search box.

The timing also adds pressure to Alphabet as it faces increased regulatory scrutiny and competition. Google has been investing in its own AI initiatives, such as Gemini, but the pace of user migration toward competitors could prove disruptive before Alphabet fully adjusts its strategy.

If Cue is right, and if Safari becomes an open platform for AI-powered search alternatives, the current Google-Apple alliance could evolve—or fracture entirely. The future of search may be less about who owns the default setting and more about who delivers the smartest, most helpful answers.

LOS ANGELES, May 07, 2025 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 13 other restaurant concepts, today announced that the Company will host a conference call to review its first quarter 2025 financial results on Thursday, May 8, 2025 at 5:30 PM ET. A press release with first quarter 2025 financial results will be issued prior to the conference call that day.

The conference call can be accessed live over the phone by dialing 1-877-704-4453 from the U.S. or 1-201-389-0920 internationally. A replay will be available after the call until Thursday, May 29, 2025, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 13752592. Hosting the call will be Andy Wiederhorn, Chairman, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call will also be webcast live from the corporate website at www.fatbrands.com, under the “Investors” section. A replay of the webcast will be available through the corporate website shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Allowed Patent Claims Cover the Synergistic Combination of Gedeptin® Therapy with Radiation As a Targeted Approach for Solid Tumors

Atlanta, GA – May 7, 2025 – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing immunotherapies and vaccines against solid tumors and infectious diseases, announced today that the U.S. Patent and Trademark Office has issued a Notice of Allowance related to U.S. patent application 17/502,101 entitled “Enhanced Therapeutic Usage of a Purine Nucleoside Phosphorylase or Nucleoside Hydrolase Prodrug”. The allowed claims further strengthen GeoVax’s intellectual property position in the oncology space.

The allowed claims describe a method for treating solid tumors—including glioblastoma, breast, prostate, head and neck, glioma, and lung cancers—through the direct intratumoral administration of an adenoviral vector encoding purine nucleoside phosphorylase (Ad/PNP), followed by local administration of the prodrug fludarabine phosphate (F-araAMP), and subsequent radiation therapy. This triple-combination strategy is designed to generate local, targeted cytotoxic activity within the tumor microenvironment while minimizing systemic toxicity.

The allowed patent joins the growing Gedeptin intellectual property portfolio, which was exclusively licensed to GeoVax through a prior agreement with PNP Therapeutics, Inc. and the University of Alabama at Birmingham (UAB)/Southern Research. Under the agreement, GeoVax has assumed all licensing rights and IP prosecution responsibilities for the Gedeptin platform.

David Dodd, Chairman and CEO of GeoVax, commented, “This allowed patent underscores the clinical and commercial promise of our Gedeptin platform and demonstrates our commitment to expanding therapeutic options for patients with difficult-to-treat cancers. While the claims do not directly mirror our ongoing clinical programs, they establish a critical foundation for future directions, including potential integration with advanced delivery systems for tumors that are challenging to access.”

Dodd continued, “The USPTO’s recognition of this therapeutic method further validates our approach and underscores the growing value of our wholly owned, co-owned, and in-licensed intellectual property estate, now standing at over 135 granted or pending patent applications spread across 23 distinct patent families”.

Having successfully completed a Phase 1/2a study, as monotherapy in advanced head and Neck cancer patients, Gedeptin is scheduled to begin a Phase 2 trial in combination with an Immune Check Inhibitor (ICI) for patients with first recurrence of head and neck cancer. The newly allowed claims provide further protection as GeoVax explores expanded applications, including novel device-based delivery approaches in potential partnership with interventional oncology companies.

About Gedeptin

Gedeptin is a viral-vectored gene therapy that employs a non-replicating adenoviral vector encoding the E. coli enzyme purine nucleoside phosphorylase (PNP). When injected directly into a tumor and followed by systemic administration of the prodrug fludarabine phosphate, PNP enzymatically converts the prodrug into a cytotoxic metabolite (fluoroadenine), resulting in selective killing of tumor cells by disrupting RNA and protein synthesis.

This tumor-targeted approach offers several key advantages:

Localized cytotoxicity with reduced systemic side effects,

Potential synergy with immune checkpoint inhibitors (ICIs),

Applicability across multiple solid tumor types, particularly those accessible for intratumoral injection.

Gedeptin will soon be evaluated in a Phase 2 clinical trial for patients with first recurrence of head and neck cancer in combination with an approved ICI. It has been granted Orphan Drug Designation by the U.S. FDA for intratumoral treatment of oral and pharyngeal cancers.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel vaccines against infectious diseases and therapies for solid tumor cancers. The Company’s lead clinical program is GEO-CM04S1, a next-generation COVID-19 vaccine currently in three Phase 2 clinical trials, being evaluated as (1) a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, (2) a booster vaccine in patients with chronic lymphocytic leukemia (CLL) and (3) a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. In oncology the lead clinical program is evaluating a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, having recently completed a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. The Company is also developing GEO-MVA, a vaccine targeting Mpox and smallpox. GeoVax has a strong IP portfolio in support of its technologies and product candidates, holding worldwide rights for its technologies and products. For more information about the current status of our clinical trials and other updates, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

FLORHAM PARK, NJ, May 7, 2025 – Conduent Incorporated (Nasdaq: CNDT), a global technology-led business process solutions and services company, today announced its first quarter 2025 financial results.

Cliff Skelton, Conduent President and Chief Executive Officer stated, “Conduent had a good start to 2025, especially amidst the broad uncertainty in the macro-economic landscape. Our results are in line with internal expectations and consistent with our 2025 outlook with respect to Adjusted Revenue, and

Adjusted EBITDA margins exceeded expectations. New business signings and our Net ARR Activity Metric, both signals of future growth, improved on a year-over-year basis. Operating cash flow comparison was negatively influenced by several one-time events in 2024 which when normalized, was better versus Q1 2024. Fortunately, while macro-economic and geopolitical environments affect everyone, most of our business segments are somewhat insulated from trade and government efficiency challenges, and in some cases, may benefit from opportunities. Our portfolio rationalization efforts are being reinvigorated with additional opportunities and are on track toward achieving more than $1B in deployable capital. Finally, we remain confident in achieving our previously stated 2025 exit rate targets we outlined two years ago.”

Key Financial Q1 2025 Results

($ in millions, except margin and per share data)

Q1 2025

Q1 2024

CurrentQuarterY/Y B/(W)

Revenue

$751

$921

(18.5)%

Adjusted Revenue(1)

$751

$821

(8.5)%

GAAP Net Income (Loss)

$(51)

$99

n/m

Adjusted EBITDA(1)

$37

$36

2.8%

Adjusted EBITDA Margin (1)

4.9%

4.4%

50 bps

GAAP Income (Loss) Before Income Tax

$(56)

$127

n/m

GAAP Diluted EPS

$(0.33)

$0.46

n/m

Adjusted Diluted EPS(1)

$(0.13)

$(0.09)

(44.4)%

Cash Flow from Operating Activities

$(58)

$(37)

(56.8)%

Adjusted Free Cash Flow(1)

$(74)

$(60)

(23.3)%

Performance Commentary

Conduent’s liquidity position at the end of the quarter remained strong with $293 million of cash and our $550 million revolving credit facility largely undrawn.

Pre-tax income (loss) for the first quarter of 2025 was $(56) million versus $127 million in the prior year period. This decrease is primarily driven by the gain on the transfer of the BenefitWallet portfolio in the prior year period.

Q1 2025 Adjusted EBITDA of $37 million and Adjusted EBITDA Margin of 4.9% both increased versus the prior year period and were ahead of our expectations.

Cash Flow from Operating Activities and Adjusted Free Cash Flow, while down year-over-year, are significantly better in Q1 2025 versus Q1 2024 when adjusting for the positive impacts of the tax refund and contributions from divested assets in the prior year period.

Additional Q1 2025 Performance Highlights

Conduent achieved several milestones in technology-led solutions, operational excellence and helping organizations achieve operating efficiencies:

As part of its efficiency and cost reduction initiatives, selected by a leading global logistics company to expand its digital customer experience based on proven outcomes, building on a trusted relationship spanning more than three decades;

Played an integral role in implementing a Congestion Relief Zone in New York City, the first of its kind in the United States, by facilitating the toll transactions and payment processing, helping to reduce traffic and improve air quality for the New York Metropolitan Area;

Launched fraud prevention tool that leverages traditional rules-based AI combined with GenAI to help prevent account take-over fraud in government benefits, initially being used in production for our payment card solutions to prevent fraud;

Awarded a contract by NJ TRANSIT to install state-of-the-art 3D fare gates at two New Jersey stations to modernize and enhance its fare collections and infrastructure;

Launched Conni, an innovative GenAI virtual assistant, designed to strengthen quality of inquiry results and improve customer experience across Conduent platforms for companies and government agencies;

Announced the selections by the Oklahoma State Department of Health and the Republic of Ireland’s Health Service Executive to deploy the company’s Maven system;

Announced a $92 million contract by the Alaska Department of Health, Division of Health Care Services to operate, manage and modernize the state’s MMIS;

For the fourth time, a leading healthcare provider recognized the Company’s for quality, ensuring efficient and effective call handling and delivering top performance through the use of analytics and insights; and

Secured a contract with the Urban Transport Authority for Lima and Callao (ATU) to implement a new transit fare collection system that enables interoperability across all transit options in the city of Lima and allows for new forms of payments including EMV and digital wallets.

FY 2025 Outlook(3)

FY 2024 Actuals

FY 2025 Outlook(3)

Adj. Revenue(1)

$3,176M

$3,100M – $3,250M

Adj. EBITDA(1) / Adj. EBITDA Margin(1)

$124M / 3.9%

4.5% – 5.5%

(1) Refer to Appendix for definition and complete non-GAAP reconciliations of Adjusted Revenue, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Diluted EPS and Adjusted Free Cash Flow. (2) Refer to Appendix for definition. (3) Refer to Appendix for additional information regarding non-GAAP outlook.

Conference Call

Management will present the results during a conference call and webcast on May 7, 2025 at 9:00 a.m. ET.

The call will be available by live audio webcast along with the news release and online presentation slides at https://investor.conduent.com/.

The conference call will also be available by calling 877-407-4019 toll-free. If requested, the conference ID for this call is 13752430.

The international dial-in is 1-201-689-8337. The international conference ID is also 13752430.

A recording of the conference call will be available by calling 1-877-660-6853 three hours after the conference call concludes. The replay ID is 13752430.

The telephone recording will be available until May 20, 2025.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 53,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling approximately 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 13 million tolling transactions every day. Learn more at www.conduent.com.

Non-GAAP Financial Measures

We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures. We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, our reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions. Providing such nonGAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures. Refer to the “Non-GAAP Financial Measures” section attached to this release for a discussion of these non-GAAP measures and their reconciliation to the reported U.S. GAAP measures.

Forward-Looking Statements

This press release, any exhibits or attachments to this release, and other public statements we make may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “estimate,” “expect,” “expectations,” “in front of us,” “plan,” “intend,” “will,” “aim,” “should,” “could,” “forecast,” “target,” “may,” “continue to,” “looking to continue,” “endeavor,” “if,” “growing,”

“projected,” “potential,” “likely,” “see,” “ahead,” “further,” “going forward,” “on the horizon,” “as we progress,” “going to,” “path from here forward,” “think,” “path to deliver,” “from here,” “on track,” “remain” and similar expressions (including the negative and plural forms of such words and phrases), as they relate to us, are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. All statements other than statements of historical fact included in this press release or any attachment to this press release are forward-looking statements, including, but not limited to, statements regarding our financial results, condition and outlook; changes in our operating results; general market and economic conditions; and our projected financial performance, including all statements made under the section captioned “FY 2025 Outlook” within this release. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions, many of which are outside of our control, that could cause actual results to differ materially from those expected or implied by such forward-looking statements contained in this press release, any exhibits to this press release and other public statements we make.

Important factors and uncertainties that could cause our actual results to differ materially from those in our forward-looking statements include, but are not limited to: government appropriations and termination rights contained in our government contracts, the competitiveness of the markets in which we operate and our ability to renew commercial and government contracts, including contracts awarded through competitive bidding processes; our ability to recover capital and other investments in connection with our contracts; our reliance on third-party providers; risk and impact of geopolitical events and increasing geopolitical tensions (such as the war in the Ukraine and conflict in the Middle East), macroeconomic conditions, natural disasters and other factors in a particular country or region on our workforce, customers and vendors; our ability to deliver on our contractual obligations properly and on time; changes in interest in outsourced business process services; claims of infringement of third-party intellectual property rights; our ability to estimate the scope of work or the costs of performance in our contracts; the loss of key senior management and our ability to attract and retain necessary technical personnel and qualified subcontractors; our failure to develop new service offerings and protect our intellectual property rights; our ability to modernize our information technology infrastructure and consolidate data centers; expectations relating to environmental, social and governance considerations; utilization of our stock repurchase program; risks related to our use of artificial intelligence; the failure to comply with laws relating to individually identifiable information and personal health information; the failure to comply with laws relating to processing certain financial transactions, including payment card transactions and debit or credit card transactions; breaches of our information systems or security systems or any service interruptions; risks related to hacking or other cybersecurity threats to our data systems, information systems and network infrastructure and other service interruptions, including relating to the cyber event that took place in January 2025, including Conduent’s investigation of such incident and mitigation and remediation efforts, the nature and extent of such incident, the potential disruption to our business or operations, the potential impact on Conduent’s reputation, and Conduent’s assessments of the likely financial and operational impacts of such incident; our ability to comply with data security standards; developments in various contingent liabilities that are not reflected on our balance sheet, including those arising as a result of being involved in a variety of claims, lawsuits, investigations and proceedings; risks related to recently completed divestitures including (i) the transfer of the Company’s BenefitWallet’s health savings account, medical savings account and flexible spending account portfolio, (ii) the sale of the Company’s Curbside Management and Public Safety Solutions businesses and (iii) the sale of the Company’s Casualty Claims Solutions business, including but not limited to the Company’s ability to realize the benefits anticipated from such transactions, unexpected costs, liabilities or delays in connection with such transactions, and the significant transaction costs associated with such transactions; risk and impact of potential goodwill and other asset impairments; our significant indebtedness and the terms of such indebtedness; our failure to obtain or maintain a satisfactory credit rating and financial performance; our ability to obtain adequate pricing for our services and to improve our cost structure; our ability to collect our receivables, including those for unbilled services; a decline in revenues from, or a loss of, or a reduction in business from or failure of significant clients; fluctuations in our non-recurring revenue; increases in the cost of voice and data services or significant interruptions in such services; our ability to receive dividends or other payments from our subsidiaries; and other factors that are set forth in the “Risk Factors” section, the “Legal Proceedings” section, the “Management’s Discussion and Analysis of

Financial Condition and Results of Operations” section and other sections in our 2024 Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with or furnished to the Securities and Exchange Commission. Any forward-looking statements made by us in this release speak only as of the date on which they are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements, whether because of new information, subsequent events or otherwise, except as required by law.

First Quarter Revenue of $1.7 Billion with GAAP EPS of $(0.97); Adjusted EPS of $1.06

GAAP Operating Loss of $32 Million; Net Loss of $29 Million; Operating Cash Flow of $57 Million

Adjusted EBITDA of $76 Million; Adjusted Free Cash Flow of $45 Million

Announced Key Supplier Partnerships in Hospitality Industry Enhancing Foundation for Growth

Announced New B2B Customers During Quarter

BOCA RATON, Fla.–(BUSINESS WIRE)–May 7, 2025– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the first quarter ended March 29, 2025.

Consolidated (in millions, except per share amounts)

1Q25

1Q24

Selected GAAP and Non-GAAP measures:

Sales

$1,699

$1,869

Sales change from prior year period

(9)%

Operating income (loss)

$(32)

$41

Adjusted operating income (1)

$54

$66

Net income (loss) from continuing operations

$(29)

$31

Diluted earnings (loss) per share from continuing operations

$(0.97)

$0.83

Adjusted net income from continuing operations (1)

$32

$50

Adjusted earnings per share from continuing operations (fully diluted) (1)

$1.06

$1.31

Adjusted EBITDA (1)

$76

$91

Operating Cash Flow from continuing operations

$57

$44

Free Cash Flow (2)

$36

$13

Adjusted Free Cash Flow (3)

$45

$17

First Quarter 2025 Summary(1)(3)

Total reported sales of $1.7 billion, down 9% versus the prior year period on a reported basis. The decrease in reported sales is largely related to lower sales in its Office Depot Division, primarily due to 46 fewer retail locations in service compared to the previous year and reduced retail and online consumer traffic, as well as lower sales in its ODP Business Solutions Division

GAAP operating loss of $32 million and net loss from continuing operations of $29 million, or $(0.97) per diluted share, versus GAAP operating income of $41 million and net income from continuing operations of $31 million, or $0.83 per diluted share, in the prior year period. GAAP operating results in the first quarter of 2025 included $86 million of charges of which $48 million is related to the Company’s Optimize for Growth restructuring plan

Adjusted operating income of $54 million, compared to $66 million in the first quarter of 2024; adjusted EBITDA of $76 million, compared to $91 million in the first quarter of 2024

Adjusted net income from continuing operations of $32 million, or adjusted diluted earnings per share from continuing operations of $1.06, versus $50 million or $1.31, respectively, in the prior year period

Operating cash flow from continuing operations of $57 million and adjusted free cash flow of $45 million, versus $44 million and $17 million, respectively, in the prior year period

$653 million of total available liquidity including $185 million in cash and cash equivalents at quarter end

“We are off to a better start to the year, with our overall performance reflecting positive momentum and improving trends in the first quarter,” said Gerry Smith, Chief Executive Officer of The ODP Corporation. “We delivered solid operational results as we continued to maintain laser focus on the core business, resulting in EBITDA improving sequentially and free cash flow increasing meaningfully over last year. Our consumer division was a key contributor, driving stronger top-line trends, achieving sequential margin improvements, and continuing to deliver solid cash flow.”

“In our B2B distribution business, while the market remained soft, we’re making significant strides beneath the surface. We’ve recently secured some of the most meaningful new business contracts in our history, including our recently announced agreement with CoreTrust, and the pace of customer onboarding is beginning to accelerate, positioning us to drive stronger monthly performance trends.”

“Additionally, we’re making significant underlying progress on our efforts to serve the hospitality industry, including forging key supplier relationships, preparing our inventory and sales force, and actively engaging with potential new customers. Through our recently announced partnership with a leading hospitality management company, we’re laying the foundation to serve the over 15,000 members within this buying group, and we are having positive discussions with other major industry participants. We believe our progress has us on track to begin driving more meaningful results in the hospitality segment beginning in the second half of this year.”

“In our supply chain business, Veyer continued to deliver exceptional results, achieving over 85% revenue growth from third-party customers and adding significant new accounts to its portfolio.”

“Overall, while there is still substantial work ahead, we are encouraged by the progress we’re making,” added Smith. “We’re also closely monitoring the tariff environment, and while we are not immune to shifts in policy, we have taken actions to help mitigate potential impacts. As we move forward, we remain focused on executing the foundational strategies required to drive success and are confident in our ability to capitalize on the opportunities before us, positioning ODP for sustained, profitable growth in the future. And considering our strong balance sheet, valuable asset base, supply chain and distribution capabilities, and cash flow profile, we believe ODP offers a unique and compelling value proposition for shareholders.”

Consolidated Results

Reported (GAAP) Results Total reported sales for the first quarter of 2025 were $1.7 billion, a decrease of 9% compared with the same period last year, driven primarily by lower sales in both its consumer and business-to-business (“B2B”) divisions. Lower sales in its consumer division, Office Depot, was primarily due to lower retail and online consumer traffic as well as 46 fewer stores in service compared to last year related to planned store closures. Sales at ODP Business Solutions Division were lower compared to last year, largely due to lower demand related to reduced spending, macroeconomic conditions, fewer customers, and severe weather challenges. Meanwhile, Veyer continued to provide strong logistics support for the ODP Business Solutions and Office Depot Divisions on lower internal sales volume, and continued to execute across its growth strategy, delivering supply chain and procurement solutions to third-party customers and driving increases in external revenue.

The Company reported GAAP operating loss of $32 million in the first quarter of 2025, down compared to GAAP operating income of $41 million in the prior year period. Operating results in the first quarter of 2025 included $86 million of charges primarily related to $48 million in restructuring expenses associated with the Optimize for Growth restructuring plan, and $28 million in non-cash asset impairments of operating lease right-of-use (“ROU”) assets associated with the Company’s retail store locations. Additionally, the Company incurred $2 million related to the impairment of operating lease ROU assets associated with the Company’s supply chain facilities, $5 million related to impairment of software, and $3 million related to the impairment of fixed assets. Net loss from continuing operations was $29 million, or $(0.97) per diluted share in the first quarter of 2025, down compared to net income from continuing operations of $31 million, or $0.83 per diluted share in the first quarter of 2024.

Adjusted (non-GAAP) Results(1) Adjusted results for the first quarter of 2025 exclude charges and credits totaling $86 million as described above and the associated tax impacts.

First quarter 2025 adjusted EBITDA was $76 million compared to $91 million in the prior year period. This included adjusted depreciation and amortization of $25 million in both the first quarter of 2025 and 2024

First quarter 2025 adjusted operating income was $54 million, down compared to $66 million in the first quarter of 2024

First quarter 2025 adjusted net income from continuing operations was $32 million, or $1.06 per diluted share, compared to $50 million, or $1.31 per diluted share, in the first quarter of 2024, a decrease of 19% on a per share basis

Division Results

ODP Business Solutions Division Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue of $3.5 billion.

Reported sales were $852 million in the first quarter of 2025, down 8% compared to the same period last year. The decrease in sales was related primarily to weaker macroeconomic conditions causing a more cautious business spending environment, lower demand, fewer customers, and severe weather impacts. Severe weather impacts are estimated to account for 80 basis points of the decline in sales

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 44% of total ODP Business Solutions’ sales

Executed initiatives to convert strong pipeline of potential new business in traditional office supply segments and implemented several initiatives to regain top-line traction, including progress on initiating service for one of the largest contracts in Company history, and winning key new business including its agreement with CoreTrust — a 3,500+ business member purchasing collective serving major industries in manufacturing, retail, hospitality and finance

Made significant progress on establishing presence in new industry segments. Since becoming a key supplier and distribution partner for one of the leading hospitality management companies that includes over 15,000 addressable members, ODP Business Solutions signed agreements with major suppliers in the hospitality industry, including Sobel Westex for premium linens and towels, and Hunter Amenities for a wide range of hotel and guest amenities including liquid beauty products, soaps, dry goods and more. The Company is also engaging in discussions with other major market participants and is making significant progress on its service launch in the $16 billion hospitality industry and expects these efforts to begin to contribute more meaningfully beginning in the second half of the year

Made progress on customer onboarding efforts and expect revenue generation from recent new business wins to ramp up in future quarters

Operating income was $21 million in the first quarter of 2025, down compared to $31 million in the same period last year on a reported basis. EBITDA was $27 million, or 3% on a percentage of sales basis

Office Depot Division Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and eCommerce presence.

Reported sales were $838 million in the first quarter of 2025, down 11% compared to the prior year reflecting an improvement over recent prior quarterly trends, as targeted profitable sales strategies gained traction. Overall sales were impacted by 46 fewer retail locations in service associated with planned store closures, as well as lower demand relative to last year in the majority of our product categories, and lower online sales, partially offset by higher average order volumes and the impact of targeted sales promotions. The Company closed 12 retail stores in the quarter and had 857 stores at quarter end. Sales were down 5% on a comparable store basis, representing a meaningful improvement over the 10% decrease in the prior year period

Store and online traffic were lower year over year due to macroeconomic factors causing continued weak consumer activity. Targeted sales promotions resulted in higher average order volumes and sales per shopper, strengthening top-line results and margins

Operating income was $45 million in the first quarter of 2025, compared to operating income of $50 million during the same period last year on a reported basis, driven primarily by the flow through impact from lower sales. On a percentage of sales, operating income remained flat compared to the same period last year

Veyer Division Nationwide supply chain, distribution, procurement and global sourcing operation supporting Office Depot and ODP Business Solutions, as well as third-party customers. Veyer’s assets and capabilities include 8 million square feet of infrastructure through a network of distribution centers, cross-docks, and other facilities throughout the United States; a global sourcing presence in Asia; a large private fleet of vehicles; and business next-day delivery capabilities to 98.5% of U.S. population.

In the first quarter of 2025, Veyer provided support for its internal customers, ODP Business Solutions and Office Depot, as well as its third-party customers, generating reported sales of $1.2 billion

Reported operating income was $8 million in the first quarter of 2025, compared to operating income of $9 million in the prior year period driven by the flow through impact of lower sales to internal customers, partially offset by services to third-party customers

Executed supply chain services for one of the world’s largest social media-focused e-commerce companies to deliver warehousing and fulfillment services for their online sales. Focused on converting strong pipeline of new business and adding key new customers to its portfolio

In the first quarter of 2025, sales generated from third-party customers increased by 89% compared to the same period last year, resulting in sales of $17 million. EBITDA generated from third-party customers was $3 million in the quarter, flat with the prior year period

Balance Sheet and Cash Flow

As of March 29, 2025, ODP had total available liquidity of $653 million, consisting of $185 million in cash and cash equivalents and $468 million of available credit under the Fourth Amended Credit Agreement. Total debt was $262 million.

For the first quarter of 2025, cash provided by operating activities of continuing operations increased to $57 million, which included $10 million in restructuring spend, compared to cash provided by operating activities of continuing operations of $44 million in the first quarter of the prior year, which included $4 million in restructuring spend. The year-over-year increase in operating cash flow is primarily related to operational discipline including strong cash conversion, as well as prudent working capital management helping to offset the impact of lower sales.

Capital expenditures were $21 million in the first quarter of 2025 versus $31 million in the prior year period, as the Company continued to prioritize capital investments towards B2B growth opportunities supporting its supply chain operations, distribution network, and digital capabilities. Adjusted Free Cash Flow(3) was $45 million in the first quarter of 2025, up compared to $17 million in the prior year period.

“Our team’s unwavering commitment to operational discipline drove a significant improvement in cash conversion, resulting in $45 million in adjusted free cash flow for the quarter—a 165% increase compared to the same period last year,” said Adam Haggard, co-CFO of The ODP Corporation. “Looking ahead, we remain focused on prioritizing capital allocation to strategically invest in our core business. This approach positions us to capture opportunities in both our traditional business segments and emerging higher-growth industries, such as hospitality, positioning ODP to pursue sustainable growth and long-term value creation.”

Hospitality Industry Progress

In the first quarter of 2025, ODP Business Solutions announced a strategic partnership with one of the world’s largest hotel management organizations, becoming a preferred provider for Operating Supplies & Equipment (“OS&E”). This agreement positions ODP as a reliable distribution partner, supporting the recurring in-room hotel supply needs of its over 15,000 members. By ensuring seamless operations, efficient room resets, and exceptional guest experiences, this partnership underscores ODP’s evolution beyond office supplies and highlights its ability to deliver tailored solutions to businesses in the hospitality, healthcare, and adjacent sectors.

Building on this momentum, ODP Business Solutions has established key agreements with leading suppliers in the hospitality industry, including Sobel Westex and Hunter Amenities, providing access to high quality products to allow ODP to better serve the hospitality industry. Sobel Westex, a global leader in hospitality and retail textiles, will provide to ODP premium products such as pillows, plush terry towels, high-quality linens, blankets, pool towels, and spa-like robes—creating a luxurious and inviting atmosphere for guests. Similarly, Hunter Amenities, a pioneer in personal care and hospitality manufacturing for over four decades, will offer to ODP its portfolio of high-end personal care products, elevating guest experiences.

“We are making significant progress in expanding our presence in the hospitality industry,” said Gerry Smith, CEO of The ODP Corporation. “By building critical relationships with top-tier suppliers, procuring in-demand inventory, and engaging with additional key market participants, we are laying the foundation for meaningful growth in the future. We are excited about the opportunities ahead and expect these efforts to begin contributing more meaningfully to our results starting in the second half of 2025.”

“Optimize for Growth” B2B Revenue Acceleration Plan

The Company made progress on its “Optimize for Growth” restructuring plan. This initiative focuses on capitalizing on ODP’s core strengths — including its supply chain and procurement expertise, robust distribution network, and strong B2B customer base — to accelerate growth in the B2B distribution and third-party logistics (3PL) market segments, while reducing retail exposure and associated liabilities. The plan strategically realigns the Company’s organizational structure, product offerings, and go-to-market strategies to target high-growth opportunities in the B2B market, while also expanding into new enterprise segments, including hospitality, healthcare, and adjacent sectors.

As part of the plan, ODP is prioritizing investments in resources and infrastructure critical to its growth in the B2B sector, while reducing fixed costs associated with retail operations, including store and distribution center leases. Concurrently, the Company has suspended growth investments in its consumer business as it continues to optimize its retail store footprint. Despite reduced retail growth investments, ODP remains firmly committed to supporting and providing an exceptional service experience at its active retail locations, ensuring that customers continue to receive the top-tier care they expect.

In connection with this plan in the first quarter of 2025, the Company recognized $48 million of restructuring expense primarily related to severance costs and the closure of 9 retail stores. In total for multi-year life of the plan, the Company expects to incur costs in the range of $185 million to $230 million, which we anticipate will generate approximately $380 million in EBITDA improvement and generate over $1.3 billion in total value over the multi-year life of the plan.

The ODP Corporation will webcast a call with financial analysts and investors on May 7, 2025, at 9:00 am Eastern Time, which will be accessible to the media and the general public. To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event.

(1)

As presented throughout this release, adjusted results represent non-GAAP financial measures and exclude charges or credits not indicative of core operations and the tax effect of these items, which may include but not be limited to merger integration, restructuring, acquisition costs, and asset impairments. Reconciliations from GAAP to non-GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(2)

As used in this release, Free Cash Flow is defined as cash flows from operating activities less capital expenditures and changes in restricted cash. Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(3)

As used in this release, Adjusted Free Cash Flow is defined as Free Cash Flow excluding cash charges associated with the Company’s restructuring programs, and related expenses. Adjusted Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services and technology solutions through an integrated business-to-business (B2B) distribution platform and omni-channel presence, which includes supply chain and distribution operations, dedicated sales professionals, online presence, and a network of Office Depot and OfficeMax retail stores. Through its operating companies ODP Business Solutions, LLC; Office Depot, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.