MCLEAN, Va., Feb. 14, 2024 /PRNewswire/ — V2X, Inc., (NYSE: VVX), a leading provider of global mission solutions, will report fourth quarter and full year 2023 financial results on Tuesday, March 5, 2024, before market open. Senior management will conduct a conference call at 8:00 a.m. ET that same day.

U.S.-based participants may dial in to the conference call at 877-407-3982, while international participants may dial 201-493-6780. A live webcast of the conference call as well as an accompanying slide presentation will be available at https://app.webinar.net/WrwGVYwl6dA and on the Investors section of the V2X website at https://gov2x.com/.

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 19, 2024, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 13743860.

ABOUT V2X V2X builds smart solutions designed to integrate physical and digital infrastructure – by aligning people, actions, and outputs. Formed by the merger of Vectrus and Vertex, we bring a combined 120 years of successful mission support. Our lifecycle solutions improve security, streamline logistics, and enhance readiness.

The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training, and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation to operations, to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

Contact Information

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

Media Contact Angelica Spanos Deoudes Senior Media Strategist Communications@goV2X.com 571-338-5195

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 14, 2024– The ODP Corporation (NASDAQ:ODP) (“ODP,” or the “Company”), a leading provider of business services, products and digital workplace technology solutions to businesses and consumers, will announce fourth quarter and full year 2023 financial results before the market open on Wednesday, February 28th, 2024. The ODP Corporation will webcast a call with financial analysts and investors that day at 9:00 am Eastern Time which will be accessible to the media and the general public.

To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event. A copy of the earnings press release, supplemental financial disclosures and presentation will also be available on the website.

About The ODP Corporation The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, a B2B digital procurement solution, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; Veyer, LLC; and Varis, Inc., The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Office Depot is a trademark of The Office Club, LLC. OfficeMax is a trademark of OMX, Inc. Veyer is a trademark of Veyer, LLC. Varis is a trademark of Varis, Inc. Grand&Toy is a trademark of Grand & Toy, LLC in Canada. Any other product or company names mentioned herein are the trademarks of their respective owners.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Receipt of Final Permit. Comstock Metals received conditional approval from the Nevada Division of Environmental Protection for the processing of waste solar panels and photovoltaics in its new materials recovery facility in Silver Springs, Nevada. With the receipt of all required permits, Comstock Metals may now complete the installation of the process equipment, and test, commission, and start up the material recovery facility. The facility includes proprietary technologies for efficiently crushing, conditioning, extracting, and recycling metal concentrates from photovoltaics.

Supplier Commitments. Comstock Metals is receiving waste panels for processing and has commenced commissioning activities. Comstock Metals continues to secure supplier commitments and is experiencing greater than initially expected inquiries from many different sources of waste panels. Decommissioning end-of-life solar panels is accelerating in the southwest region of the United States where solar panels were adopted early. Because Comstock Metals will receive an upfront disposal fee for handling the end-of-life solar panels, Comstock Metals could begin generating cash flow with revenue recognized once the waste is processed and recycled.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Buys attractive radio station group. Saga plans to purchase Lafayette, IN radio stations WKOA (FM), WKHY (FM), WASK (FM), WXXB (FM), WASK (AM) and W269DJ from Neuhoff Communications in a cash transaction for $5.3 million. The transaction is subject to regulatory approval and is expected to close in May. We view the transaction favorably.

Attractive market. Lafayette is in line with the company’s target acquisition markets. The stations are located in a growing community with a broad-based economy including a large university (Purdue University), biotech and healthcare services, advanced manufacturing (Caterpillar large engines and Wabash), Aerospace (GE Aviation, SAAB, & Rolls Royce), and Automotive (Subaru) which is expanding.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The mining sector has produced enormous wealth for investors who’ve managed to time the boom and bust cycles. Legendary investors like Robert Friedland, Ross Beaty, Lukas Lundin and Rick Rule have built fortunes by profiting from these fluctuations. Understanding their success stories can help guide investors looking to capitalize on the next mining upcycle.

Rick Rule – The Contrarian

Rick Rule pioneered a contrarian approach to mining investment. When others fled during downturns, Rule saw opportunity. He built expertise in natural resources first as a broker and then establishing Global Resource Investments in the 1990s.

Rule made fortunes by financing promising junior miners and explorers when markets were depressed. He helped fund their projects and acquisitions, earning stakes that paid off enormously when prices recovered. Rule exemplified patience in holding assets through slumps and rigor in evaluating companies.

For investors, Rule’s story highlights the potential of a contrarian mindset. The best values often emerge when sentiment is bleakest. Rule continues dispensing wisdom and seeking hidden gems, now as part of Sprott Inc.

Robert Friedland – The Visionary

Few capture the boom and bust nature of mining like Robert Friedland. The self-made billionaire got his start in mining by investing $50,000 to acquire an abandoned mine in Canada. He turned it into the wildly productive Voisey’s Bay nickel project that later sold for $4.3 billion.

Friedland replicated this formula across continents with Ivanhoe Mines, discovering major copper deposits in Asia and platinum reserves in South Africa. His eye for recognizing potential deposits before others has earned him the moniker of the “mining visionary.”

Ross Beaty – The Speculator

Canadian financier Ross Beaty took a more speculative approach to mining fortunes. In the 1990s, he bought cheap silver reserves in Bolivia that would become the basis for Pan American Silver, one of the world’s top producers.

When silver prices spiked in 2011, Beaty cashed out at the market peak – turning an initial $2 million investment into a $1 billion windfall. He replicated this success by speculating early on lithium miners in anticipation of surging electric vehicle demand.

Lukas Lundin – The Empire Builder

As the scion of a famous Swedish mining family, Lukas Lundin seemed destined for the industry. He helped grow the Lundin Group into a billion dollar mining empire through acquisitions and mergers.

Lundin acquired undervalued assets during slumps and consolidated them into larger firms like Lundin Mining when prices recovered. He also partnered with legendary explorers like Robert Friedland to help discover new deposits.

Positioning for the Next Supercycle

With the mining industry potentially on the cusp of a new supercycle, there are lessons to draw from these legends. Rule’s contrarian approach demonstrates the value of investing when others are fearful. Friedland’s discoveries show the vast potential still remaining. Beaty’s speculation reveals the leverage possible with junior miners. And Lundin’s empire reveals the power of diversification across the sector.

Madrid, Spain and Tel Aviv, Israel, February 14, 2024 (GLOBE NEWSWIRE) – Codere Online Luxembourg, S.A. (Nasdaq: CDRO / CDROW) (the “Company” or “Codere Online”) a leading online gaming operator in Spain and Latin America, today announced that it will release its fourth quarter and full year 2023 results prior to 8:30AM US Eastern Time on February 29, 2024.

At 8:30AM US Eastern Time on the same day, Codere Online’s management will host a conference call to discuss the results and provide a business update.

The Company’s earnings press release and related materials will be available on Codere Online’s website at www.codereonline.com. Dial-in details for the conference call as well as the audio webcast registration link are accessible on the Events & Presentations section of the same website. A recording of the webcast will be available following the conference call.

About Codere Online

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile applications. Codere currently operates in its core markets of Spain, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence.

About Codere Group Codere Group is a multinational group devoted to entertainment and leisure. It is a leading player in the private gaming industry, with four decades of experience and with presence in seven countries in Europe (Spain and Italy) and Latin America (Argentina, Colombia, Mexico, Panama, and Uruguay).

Contacts:

Investors and Media Guillermo Lancha Director, Investor Relations and Communications Guillermo.Lancha@codere.com (+34)-628-928-152

Clinical results show that Tonyma™ has broad-spectrum activity, addressing the three core fibromyalgia symptoms: pain, fatigue, and sleep disturbance

Tonmya™ has a favorable tolerability profile well-suited for chronic treatment

CHATHAM, N.J., Feb. 14, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a biopharmaceutical company with marketed products and a pipeline of development candidates, held a key opinion leader (KOL) webinar to discuss the positive Phase 3 data of Tonmya™ (also known as TNX-102 SL, cyclobenzaprine HCl sublingual tablets) for the management of fibromyalgia, and the path to file for FDA approval in the second half of 2024. The webinar was held on January 31, 2024 and hosted by Alliance Global Partners (A.G.P.).

The webinar featured two thought leaders in the field of fibromyalgia: Daniel Clauw, M.D., Professor of Anesthesiology, Medicine and Psychiatry, Director Chronic Pain & Fatigue Research Center, University of Michigan, and Lesley Arnold, M.D., Professor of Psychiatry and Behavioral Neuroscience, University of Cincinnati College of Medicine.

Tonmya™ is a centrally acting, non-opioid, non-addictive, bedtime medication. As previously announced, Tonix’s second positive Phase 3 study, RESILIENT, met its pre-specified primary endpoint, significantly reducing daily pain compared to placebo (p=0.00005) in participants with fibromyalgia. Statistically significant and clinically meaningful results (p=0.001 or better) were also seen in all key secondary endpoints related to improving sleep quality, reducing fatigue, and improving overall fibromyalgia symptoms and function.

Tonix plans to submit a New Drug Application (NDA) to the U.S. Food and Drug Administration (FDA) in the second half of 2024 for Tonmya™ for the management of fibromyalgia.

“These data offer new hope for patients with fibromyalgia,” said Dr. Arnold. “Many of my patients have required combination treatments to combat their multiple fibromyalgia-related symptoms. We haven’t seen a medication that can treat fatigue, sleep, and pain all together. Having a compound like Tonmya™ that may address all three is very exciting.”

“The fact that cyclobenzaprine was beneficial in many other key symptom domains, including sleep quality, is important to fibromyalgia patients,” said Dr. Clauw. “We’re really beginning to understand how crucial sleep is in alleviating and potentially preventing fibromyalgia symptoms.”

Dr. Arnold stated that most patients are open to new treatment options, citing lack of efficacy in some cases, tolerability issues and unwanted side effects associated with the currently approved fibromyalgia treatments. “Since patients typically need to be treated for prolonged periods of time, it is important to develop a therapeutic which is well-tolerated.”

“We believe that these positive results show that fibromyalgia can be successfully treated by Tonmya™ and may provide the opportunity for Tonix to have the first FDA-approved drug for fibromyalgia in more than a decade,” said Seth Lederman, M.D., President and Chief Executive Officer of Tonix Pharmaceuticals. “We are now an important step closer to bringing a new, first-line treatment to fibromyalgia patients that offers broad symptom relief and favorable tolerability for chronic use and adherence.”

About the Phase 3 RESILIENT Study The RESILIENT study was a double-blind, randomized, placebo-controlled trial designed to evaluate the efficacy and safety of Tonmya™ (TNX-102 SL: cyclobenzaprine HCl sublingual tablets) for the management of fibromyalgia. The two-arm trial randomized 457 participants in the U.S. across 33 sites. The first two weeks of treatment consisted of a run-in period in which participants started on TNX-102 SL 2.8 mg (1 tablet) or placebo. Thereafter, all participants increased their dose to TNX-102 SL 5.6 mg (2 x 2.8 mg tablets) or two placebo tablets for the remaining 12 weeks. The study met the pre-specified primary endpoint of daily diary pain severity score change (TNX-102 SL 5.6 mg vs. placebo) from baseline to Week 14 (using the weekly averages of the daily numerical rating scale scores), analyzed by mixed model repeated measures with multiple imputation (p=0.00005).

For more information, see ClinicalTrials.gov Identifier: NCT05273749.

About Fibromyalgia Fibromyalgia is a chronic pain disorder that is understood to result from amplified sensory and pain signaling within the central nervous system. Fibromyalgia afflicts an estimated 6 million to 12 million adults in the U.S., the majority of whom are women. Symptoms of fibromyalgia include chronic widespread pain, nonrestorative sleep, fatigue, and morning stiffness. Other associated symptoms include cognitive dysfunction and mood disturbances, including anxiety and depression. Individuals suffering from fibromyalgia struggle with their daily activities, have impaired quality of life, and frequently are disabled. Physicians and patients report common dissatisfaction with currently marketed products.

About Tonmya™ (also known as TNX-102 SL) Tonmya is a patented sublingual tablet formulation of cyclobenzaprine hydrochloride which is designed for daily administration at bedtime with a proposed mechanism of improving sleep quality in fibromyalgia. Tonmya provides rapid transmucosal absorption and reduced production of a long half-life active metabolite, norcyclobenzaprine, due to bypass of first-pass hepatic metabolism. As a multifunctional agent with potent binding and antagonist activities at the 5-HT2A-serotonergic, α1-adrenergic, H1-histaminergic, and M1-muscarinic cholinergic receptors, Tonmya is in development as a daily bedtime treatment for fibromyalgia. TNX-102 SL is also in development fibromyalgia-type Long COVID (formally known as post-acute sequelae of COVID-19 [PASC]), alcohol use disorder, and agitation in Alzheimer’s disease. The United States Patent and Trademark Office (USPTO) issued United States Patent No. 9636408 in May 2017, Patent No. 9956188 in May 2018, Patent No. 10117936 in November 2018, Patent No. 10,357,465 in July 2019, and Patent No. 10736859 in August 2020. The Protectic™ protective eutectic and Angstro-Technology™ formulation claimed in the patent are important elements of Tonix’s proprietary Tonmya composition. These patents are expected to provide Tonmya, upon NDA approval, with U.S. market exclusivity until 2034/2035. In addition, Tonix has pending but not issued U.S. patent applications directed to the transmucosal absorption of CBP-HCl, with U.S. market exclusivity expected until 2033, for treating depressive symptoms in fibromyalgia, with U.S. market exclusivity expected until 2032, and for treating pain in fibromyalgia with U.S. market exclusivity expected until 2041.

Tonix Pharmaceuticals Holding Corp.* Tonix is a biopharmaceutical company focused on commercializing, developing, discovering and licensing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s development portfolio is focused on central nervous system disorders. Tonix’s priority is to submit a New Drug Application (NDA) to the FDA for Tonmya, which has completed two positive Phase 3 studies for the management of fibromyalgia. Tonix intends to meet with the FDA in the first half of 2024 and submit an NDA for the approval of Tonmya for the management of fibromyalgia in the second half of 2024. TNX-102 SL is being developed to reduce the severity of acute stress reaction and the frequency of acute stress disorder and posttraumatic stress disorder. This trial is being sponsored by the University of North Carolina and received funding support from the U.S. Department of Defense. TNX-102 SL is also being developed to treat fibromyalgia-type Long COVID, a chronic post-acute COVID-19 condition, and topline results from a proof-of-concept study were reported in the third quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA and received funding from the National Institute on Drug Abuse (NIDA). A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2024. Tonix’s rare disease development portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome (PWS). TNX-2900 has been granted Orphan Drug designation by the FDA and an investigational new drug (IND) application has been cleared to support a Phase 2 study in PWS patients. Tonix’s immunology development portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 was initiated in the third quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases, including TNX-1800, in development as a vaccine to protect against COVID-19. During the fourth quarter of 2023, TNX-1800 was selected by the U.S. National Institutes of Health (NIH), National Institute of Allergy and Infectious Diseases (NIAID) Project NextGen for inclusion in Phase 1 clinical trials. The infectious disease development portfolio also includes TNX-3900 and TNX-4000, which are classes of broad-spectrum small molecule oral antivirals. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg under a transition services agreement with Upsher-Smith Laboratories, LLC from whom the products were acquired on June 30, 2023. Zembrace SymTouch and Tosymra are each indicated for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

This Valentine’s Day, chocolate lovers may experience some sticker shock. Cocoa prices have soared to record highs, driving up the cost of sweets. While pricier candy may cause consternation, the cocoa boom offers key investing insights around commodities and consumer stocks.

The surge in cocoa futures to all-time highs comes as adverse weather hammered crops in major producing countries like Ghana and Ivory Coast. With chocolate a staple gift for Valentine’s Day, limited cocoa supplies are creating a supply-demand mismatch. This highlights the importance of monitoring key commodity markets for indications of inflationary pressures and consumer impacts.

While candy makers will pass on higher input costs, demand for affordable treats remains strong. In fact, chocolate has historically been recession-resistant as consumers seek small indulgences during tough times. This illustrates why careful stock picking among consumer stocks can pay dividends, even amid high inflation.

Major chocolate manufacturers like Hershey and Mondelez have pricing power to maintain margins amid commodity inflation. Their brand recognition and dominance in impulse buy categories like candy help sustain volumes.

However, these companies still face risks from consumers trading down to cheaper alternatives. Investors should assess how they are adapting their product mix and packaging to maintain appeal. Companies keeping prices restrained and managing costs may fare better.

Hershey has invested in upgrading its Reese’s brand through new flavors and packaging while Mondelez has expanded its premium offerings. Their balance of classic candies and innovative products helps broaden their consumer base.

Further down the value chain, cocoa suppliers and traders like Cargill and Barry Callebaut play an outsized role in global chocolate production. They benefit from rising commodity prices but face risks if high prices reduce demand. Their processing capabilities, logistics infrastructure and long-term contracts provide resilience.

Diversified commodities giants like Cargill can hedge their chocolate exposure through other segments. But more specialized players like Callebaut are doubling down – investing over $775 million to expand cocoa processing capacity amid the supply shortages.

Ingredient suppliers like Ingredion and Archer-Daniels-Midland could see higher demand for cocoa substitutes and chocolate alternatives as manufacturers reformulate products. Companies that adapt best to the changing industry trends can capture market share.

Ingredion produces specialty starches that can replace cocoa butter to lower costs. ADM offers cocoa replacers using grains like oats. With their R&D and patented technologies, they provide options for chocolate makers facing margin pressures.

For retailers, merchandising and promotions will be key to managing chocolate inventory this Valentine’s Day. Discount retailers like Dollar Tree and Dollar General selling smaller packaging at impulse price points may have an edge. Monitoring sales volumes and margins at leading retailers around holidays offers clues on consumer health.

Dollar stores appeal to budget-conscious shoppers when prices are high while prestige retailers like Godiva attract gift givers wanting luxury chocolates. Tracking consumer bifurcation across income levels provides insights on discretionary demand.

While Americans consume $22 billion in chocolate annually, it is still a cyclical agricultural commodity. Cocoa’s meteoric rise this year reminds investors not to overextend on consumer stocks when input costs are inflated. Monitoring commodity trends provides valuable context on margins and pricing power.

Consumer staples stocks shine brightest when they judiciously pass on costs while maintaining loyal brand recognition. Keeping pulse on consumer sentiment through holidays like Valentine’s Day informs on how discretionary some categories truly are.

Finally, analyzing the full supply chain offers unique angles, whether transporters fueling commerce, packaging tying together trends, or warehouses at the nucleus of distribution. Even when commodity markets look frothy, the diversified ecosystem supporting consumer spending reveals pockets of value.

So this Valentine’s Day, both candy lovers and investors have something to take away from cocoa’s climb. While chocolate prices may be testing appetites, they represent just one ingredient in a recipe for long-term returns.

PDF Version•Up to 16 million adults in the US are living with a neurological disease, the leading cause of physical and cognitive disability, and 1.2 million new cases are diagnosed annually.•The review article summarizes data demonstrating that inflammation resulting from activation of more than one type of inflammasome contributes to development of neurological diseases and that ASC specks lead to their progression.•ZyVersa is developing IC 100, a monoclonal antibody targeting inflammasome ASC and ASC specks from multiple types of inflammasomes to block initiation and perpetuation of damaging inflammation.•IC 100 preclinical data demonstrate that it penetrates the brain, and that it has promising therapeutic potential for neurological diseases based on preclinical studies representative of multiple sclerosis, Alzheimer’s disease, traumatic brain injury, and spinal cord injury.WESTON, Fla., Feb. 14, 2024 (GLOBE NEWSWIRE) — ZyVersa Therapeutics, Inc. (Nasdaq: ZVSA or “ZyVersa”), a clinical stage specialty biopharmaceutical company developing first-in-class drugs for treatment of inflammatory and renal diseases, highlights data from a review article published in Nature Reviews Neurology. This article provides increasing evidence that activation of several types of inflammasomes and extracellular ASC specks contribute to the development and progression of multiple neurological diseases including Alzheimer’s disease (AD), Parkinson’s disease (PD), multiple sclerosis (MS), amyotrophic lateral sclerosis (ALS), epilepsy, traumatic brain injury (TBI), and stroke.In the paper titled, “Inflammasomes in neurological disorders — mechanisms and therapeutic potential,” the authors reviewed 297 published papers that included data from cell cultures, preclinical disease models, and human tissue analysis to summarize the current evidence for and understanding of inflammasome activation in various neurological diseases. Key learnings include:•Many neurological conditions involve an underlying chronic inflammasome-mediated inflammatory process that worsens the trajectory of these conditions.•Beyond NLRP3, evidence suggests that other inflammasomes, including but not restricted to NLRP1, NLRC4, and AIM2, and their downstream effectors contribute to neuropathology in AD, PD, ALS, MS, stroke, epilepsy, and TBI.•Inflammasome-induced release of ASC specks into the extracellular space seems to be important in the speed of neurodegeneration in conditions such as AD and PD.The authors concluded, “Use of inflammasome-targeted therapeutic approaches could improve existing therapeutic strategies for multiple neurological conditions.” To review the publication, Click Here.“We are thrilled to see the large number of studies summarized in the review article published in Nature Reviews Neurology that reinforce the role of multiple types of inflammasomes and extracellular ASC specks in the development and progression of numerous neurological diseases,” commented Stephen C. Glover, ZyVersa’s Co-founder, Chairman, CEO, and President. These studies, in combination with our own preclinical program, substantiate the rationale for targeting inflammasome ASC to inhibit multiple inflammasome pathways and to disrupt the function of ASC specks to control inflammation in numerous neurological diseases.” To review a white paper summarizing the mechanism of action and preclinical data for IC 100, Click Here.About Inflammasome ASC Inhibitor IC 100IC 100 is a novel humanized IgG4 monoclonal antibody that inhibits the inflammasome adaptor protein ASC. IC 100 was designed to attenuate both initiation and perpetuation of the inflammatory response. It does so by binding to a specific region of the ASC component of multiple types of inflammasomes, including NLRP1, NLRP2, NLRP3, NLRC4, AIM2, and Pyrin. Intracellularly, IC 100 binds to ASC monomers, inhibiting inflammasome formation, thereby blocking activation of IL-1β early in the inflammatory cascade. IC 100 also binds to ASC in ASC Specks, both intracellularly and extracellularly, further blocking activation of IL-1β and the perpetuation of the inflammatory response that is pathogenic in inflammatory diseases. Because active cytokines amplify adaptive immunity through various mechanisms, IC 100, by attenuating cytokine activation, also attenuates the adaptive immune response.About ZyVersa Therapeutics, Inc.ZyVersa (Nasdaq: ZVSA) is a clinical stage specialty biopharmaceutical company leveraging advanced, proprietary technologies to develop first-in-class drugs for patients with renal and inflammatory diseases who have significant unmet medical needs. The Company is currently advancing a therapeutic development pipeline with multiple programs built around its two proprietary technologies – Cholesterol Efflux Mediator™ VAR 200 for treatment of kidney diseases, and Inflammasome ASC Inhibitor IC 100, targeting damaging inflammation associated with numerous CNS and other inflammatory diseases. For more information, please visit www.zyversa.com.Cautionary Statement Regarding Forward-Looking StatementsCertain statements contained in this press release regarding matters that are not historical facts, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These include statements regarding management’s intentions, plans, beliefs, expectations, or forecasts for the future, and, therefore, you are cautioned not to place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. ZyVersa Therapeutics, Inc (“ZyVersa”) uses words such as “anticipates,” “believes,” “plans,” “expects,” “projects,” “future,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,” “guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions. Such forward-looking statements are based on ZyVersa’s expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements due to a number of factors, including ZyVersa’s plans to develop and commercialize its product candidates, the timing of initiation of ZyVersa’s planned preclinical and clinical trials; the timing of the availability of data from ZyVersa’s preclinical and clinical trials; the timing of any planned investigational new drug application or new drug application; ZyVersa’s plans to research, develop, and commercialize its current and future product candidates; the clinical utility, potential benefits and market acceptance of ZyVersa’s product candidates; ZyVersa’s commercialization, marketing and manufacturing capabilities and strategy; ZyVersa’s ability to protect its intellectual property position; and ZyVersa’s estimates regarding future revenue, expenses, capital requirements and need for additional financing.New factors emerge from time-to-time, and it is not possible for ZyVersa to predict all such factors, nor can ZyVersa assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements included in this press release are based on information available to ZyVersa as of the date of this press release. ZyVersa disclaims any obligation to update such forward-looking statements to reflect events or circumstances after the date of this press release, except as required by applicable law.This press release does not constitute an offer to sell, or the solicitation of an offer to buy, any securities.Corporate, Media, and IR Contact:Karen CashmereChief Commercial Officerkcashmere@zyversa.com786-251-9641

GAITHERSBURG, Md., Feb. 14, 2024 /PRNewswire/ — YS Biopharma Co., Ltd. (Nasdaq: YS) (“YS Biopharma” or the “Company”, and together with its subsidiaries, “YS Group”), a global biopharmaceutical company dedicated to discovering, developing, manufacturing, and delivering new generations of vaccines and therapeutic biologics for infectious diseases and cancer, today announced the appointment of six new members to its Board of Directors (the “Board”), effective February 13, 2024. The six new directors are: Dr. Yuntao Cui; Dr. Jin Wang; Mr. Henry Chen; Mr. Haitao Zhao; Mr. Pierson Yue Pan; and Ms. Brenda Chunyuan Wu.

In addition to the new appointments, the Board has elected Dr. Ajit Shetty, who had served as the Company’s Interim Chairperson of the Board since December 9, 2023, as Chairperson of the Board, effective February 13, 2024.

Dr. Yuntao Cui has over 15 years of law-related work experience, and has previously worked as a Senior Lawyer at Zhong Lun Law Firm, one of the top law firms in China, and as General Manager of Legal Affairs at Wanda Group, a top conglomerate in the real estate, finance, and hospitality industries. Dr. Cui is currently a Senior Vice President and General Counsel at Juventas Cell Therapy Ltd., a leading immune cell therapy company. Dr. Cui holds a JD from Renmin University of China.

Dr. Jin Wang is Founding Partner and CEO of Manhattan Capital Investment Consulting Group (“MCG”), and has managed the venture capital investment fund Nuokang Venture Fund since 2014. Dr. Wang has more than 27 years of experience finding, building, and strategizing for biotech companies, including his co-founding and angel investment in leading medical professional networking and service firm DXY. Dr. Wang previously worked as an analyst and Asia/Greater China Regional Director for Paramount Capital Investment, LLC, and co-founded the Sino-American Pharmaceutical Professionals Association (“SAPA”) in 1993. Dr. Wang holds a PhD in Biomedical Science from Worcester Polytechnic Institute.

Mr. Henry Chen is the CEO of Monument Pacific Development Corp., a California-based company dedicated to developing, managing, and operating residential and commercial properties in Northern and Southern California. Mr. Chen received his MBA from the University of California, Berkeley’s Hass School of Business in 2012, and a Bachelor of Laws in Business Administration and Management from the Beijing University of Chemical Technology in 2005.

Mr. Haitao Zhao has served as a Partner of the Shanxi Tie Niu law firm since 2016, where he is responsible for handling corporate law related to intellectual property protection, corporate internal governance, and financing-related legal services. Previously, Mr. Zhao worked as an Attorney for the Beijing Ding En law firm from 2012-2016. He holds an MA in International Law from Shanxi University.

Mr. Pierson Yue Pan has served as a Vice President of Monument Pacific Development Corp. since 2018. Previously, Mr. Pan worked as Vice President of Project Development at real estate developer Propriis from 2012-2018, and as General Manager of the Africa Market with the China Civil Engineering Construction Company Nigeria Limited from 2004-2011. Mr. Pan holds an MBA from the University of California, Berkeley’s Hass School of Business.

Ms. Chunyuan (Brenda) Wu currently serves as the CFO of YS Group, a position she has held since December 31, 2020. Previously, Ms. Wu served as CFO of YS Group Biopharma from 2018-2020, and as Financial Controller for the same company from 2013-2018. Ms. Wu has also previously worked as a Senior Auditor at Ernst & Young. Ms. Wu holds degrees in Accounting and Finance from Washington State University.

Dr. Ajit Shetty, Chairperson of the Board of Directors of the Company, commented, “We are pleased to welcome each of our new directors to the Board. Each of these talented individuals brings valuable expertise in various aspects of corporate governance, legal affairs, business management, and strategic decision-making. We expect that their diverse experience and commitment to success will serve our company well going forward.”

About YS Biopharma

YS Biopharma is a global biopharmaceutical company dedicated to discovering, developing, manufacturing, and commercializing new generations of vaccines and therapeutic biologics for infectious diseases and cancer. It has developed a proprietary PIKA® immunomodulating technology platform and a series of preventive and therapeutic biologics with a potential for improved Rabies, Coronavirus, Hepatitis B, Influenza, and Shingles vaccines. YS Biopharma operates in China, the United States, Singapore and the Philippines, and is led by a management team that combines rich local expertise and global experience in the bio-pharmaceutical industry. For more information, please visit investor.ysbiopharm.com.

This press release contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical or current fact included in this press release are forward-looking statements, including but not limited to statements regarding the expected growth of the Company, the development progress of all product candidates, the progress and results of all clinical trials, the Company’s ability to source and retain talent, and the cash position of the Company following the closing of the Business Combination. Forward-looking statements may be identified by the use of words such as “estimate,” “plan,” “project,” “forecast,” “intend,” “will,” “expect,” “anticipate,” “believe,” “seek,” “target” or other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These statements are based on various assumptions, whether identified in this press release, and on the current expectations of YS Biopharma’s management and are not predictions of actual performance.

These statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance, or achievements to be materially different from those expressed or implied by these forward-looking statements. Although YS Biopharma believes that it has a reasonable basis for each forward-looking statement contained in this press release, YS Biopharma cautions you that these statements are based on a combination of facts and factors currently known and projections of the future, which are inherently uncertain. In addition, there are risks and uncertainties described in the documents filed by YS Biopharma from time to time with the U.S. Securities and Exchange Commission (“SEC”). These filings may identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements.

YS Biopharma cannot assure you that the forward-looking statements in this press release will prove to be accurate. These forward-looking statements are subject to a number of risks and uncertainties, including, among others, the outcome of any potential litigation, government or regulatory proceedings, the sales performance of the marketed vaccine product and the clinical trial development results of the product candidates of YS Biopharma, and other risks and uncertainties, including those included under the heading “Risk Factors” in the post-effective amendment No. 2 to Form F-1 filed with the SEC on January 23, 2024 which became effective on January 25, 2024, and other filings with the SEC. There may be additional risks that YS Biopharma does not presently know or that YS Biopharma currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In light of the significant uncertainties in these forward-looking statements, nothing in this press release should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. The forward-looking statements in this press release represent the views of YS Biopharma as of the date of this press release. Subsequent events and developments may cause those views to change. However, while YS Biopharma may update these forward-looking statements in the future, there is no current intention to do so, except to the extent required by applicable law. You should, therefore, not rely on these forward-looking statements as representing the views of YS Biopharma as of any date subsequent to the date of this press release. Except as may be required by law, YS Biopharma does not undertake any duty to update these forward-looking statements.

IRVINE, Calif., Feb. 13, 2024 (GLOBE NEWSWIRE) — Eledon Pharmaceuticals, Inc. (“Eledon”) (NASDAQ: ELDN) today announced that the Company’s Compensation Committee granted 42,500 restricted stock units (RSUs) and stock options to purchase an aggregate of 90,000 common shares, at a per share exercise price of $1.77, the closing price of Eledon’s common stock on the grant date, to one employee. The RSUs and stock options were granted as inducements material to the new employee entering employment with Eledon in accordance with Nasdaq Listing Rule 5635(c)(4).

The RSUs vest fully on the one-year anniversary of the grant date. The stock options have a ten-year term and vest over four years, with 25% of the original number of shares vesting on the one-year anniversary of the grant date and 6.25% of the stock options vesting quarterly thereafter until fully vested on the fourth anniversary of the grant date. In each case, vesting is subject to the relevant employee’s continued service with Eledon on the applicable vesting date.

About Eledon Pharmaceuticals and tegoprubart

Eledon Pharmaceuticals, Inc. is a clinical stage biotechnology company that is developing immune-modulating therapies for the management and treatment of life-threatening conditions. The Company’s lead investigational product is tegoprubart, an anti-CD40L antibody with high affinity for CD40 Ligand, a well-validated biological target within the costimulatory CD40/CD40L cellular pathway. The central role of CD40L signaling in both adaptive and innate immune cell activation and function positions it as an attractive target for non-lymphocyte depleting, immunomodulatory therapeutic intervention. The Company is building upon a deep historical knowledge of anti-CD40 Ligand biology to conduct preclinical and clinical studies in kidney allograft transplantation, xenotransplantation, and amyotrophic lateral sclerosis (ALS). Eledon is headquartered in Irvine, California. For more information, please visit the Company’s website at www.eledon.com.

Follow Eledon Pharmaceuticals on social media: LinkedIn; Twitter

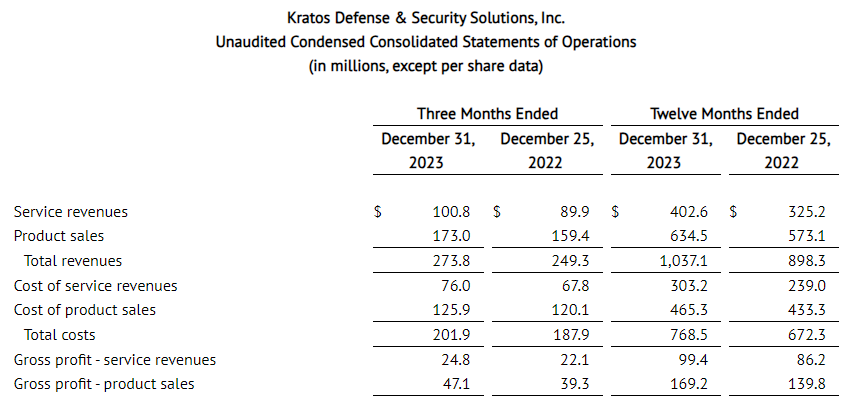

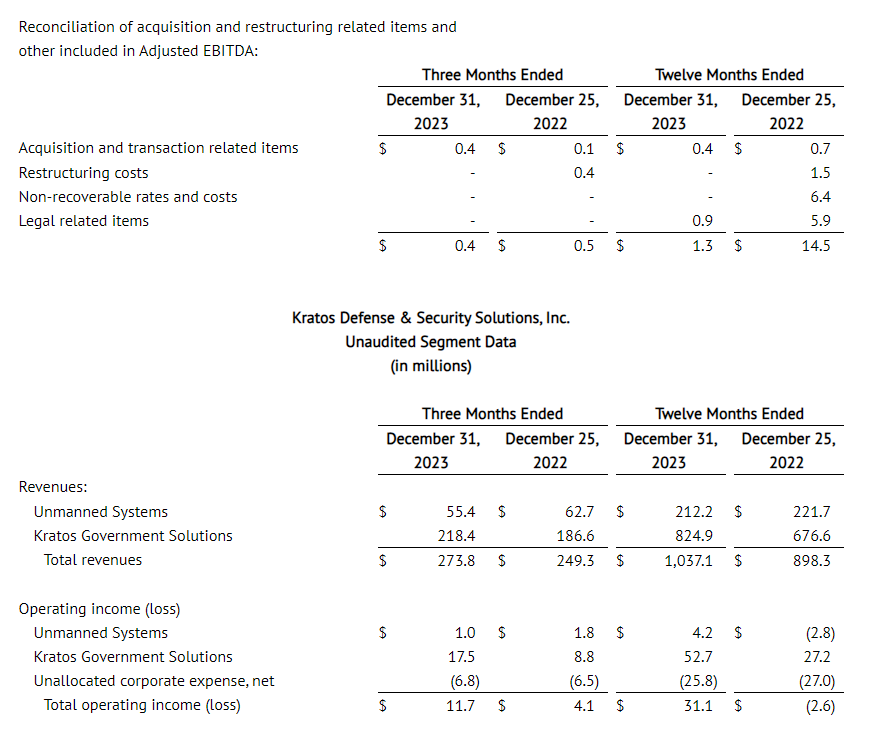

Full Year 2023 Revenues of $1.037 Billion Reflect 15.5 Percent Growth and 12.6 Percent Organic Growth, Respectively, Over Full Year 2022 Revenues of $898.3 Million

Fourth Quarter Revenues of $273.8 Million Reflect 9.8 Percent Growth and 7.3 Percent Organic Growth, Respectively, Over Fourth Quarter 2022 Revenues of $249.3 Million

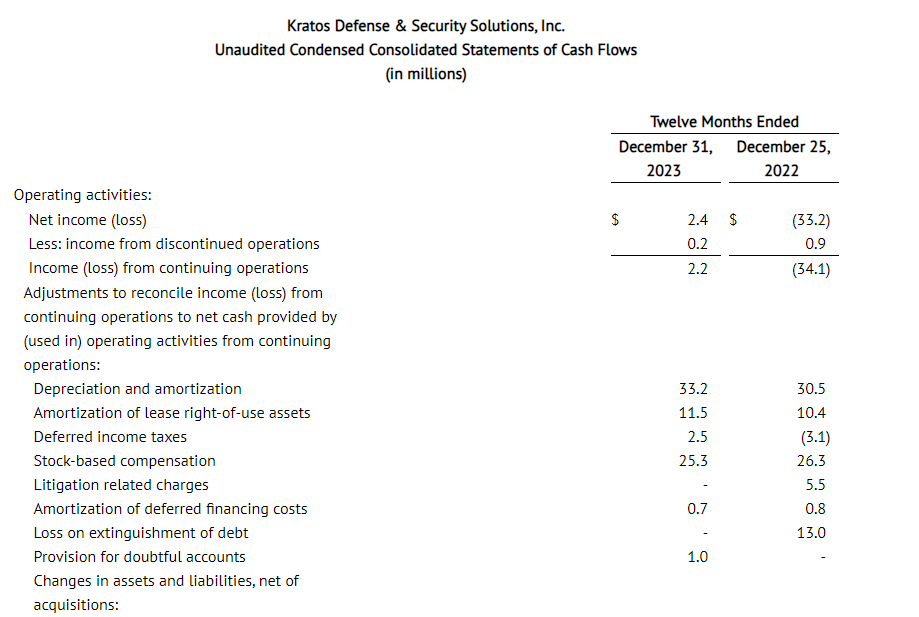

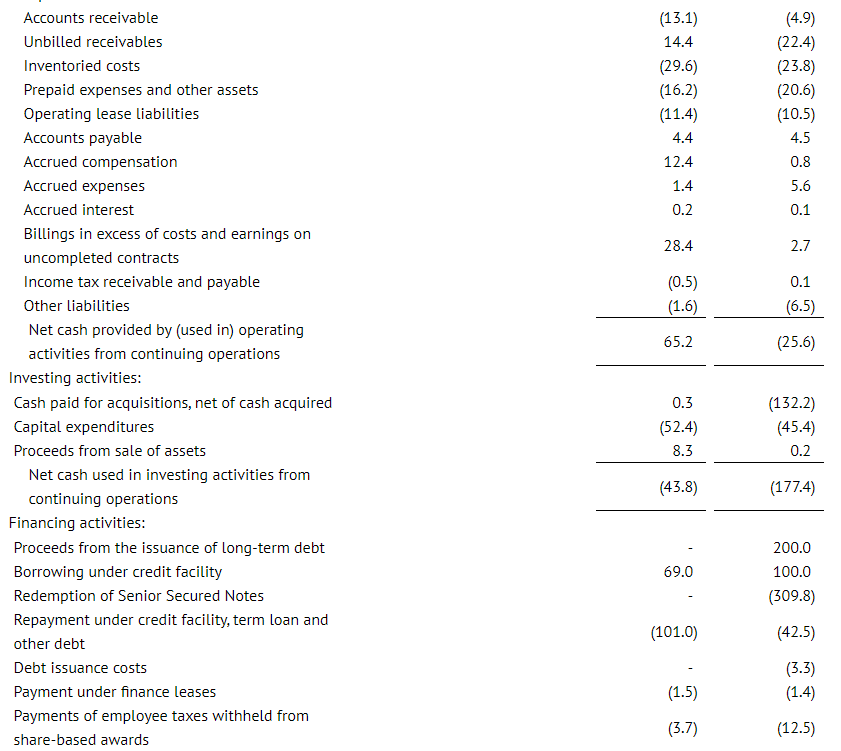

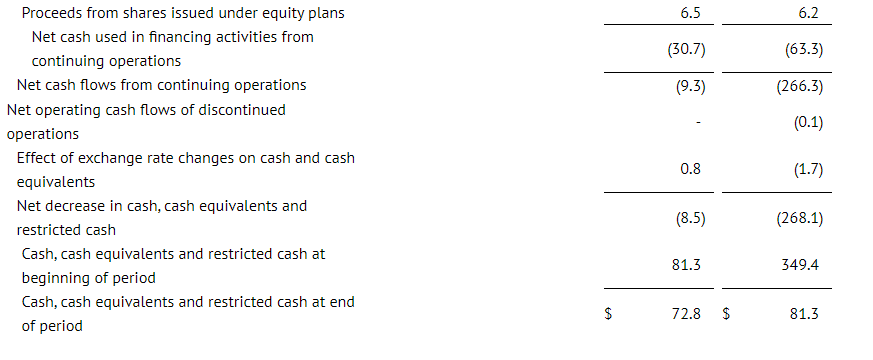

Fourth Quarter 2023 Cash Flow Generated from Operations of $67.4 Million Full Year 2023 Cash Flow Generated from Operations of $65.2 Million

Fourth Quarter 2023 Consolidated Book to Bill Ratio of 1.2 to 1 and Bookings of $330 Million

Last Twelve Months Ended December 31, 2023 Consolidated Book to Bill Ratio of 1.1 to 1 and Bookings of $1.15 Billion

2024 Financial Forecast Includes 10 Percent Organic Revenue Growth

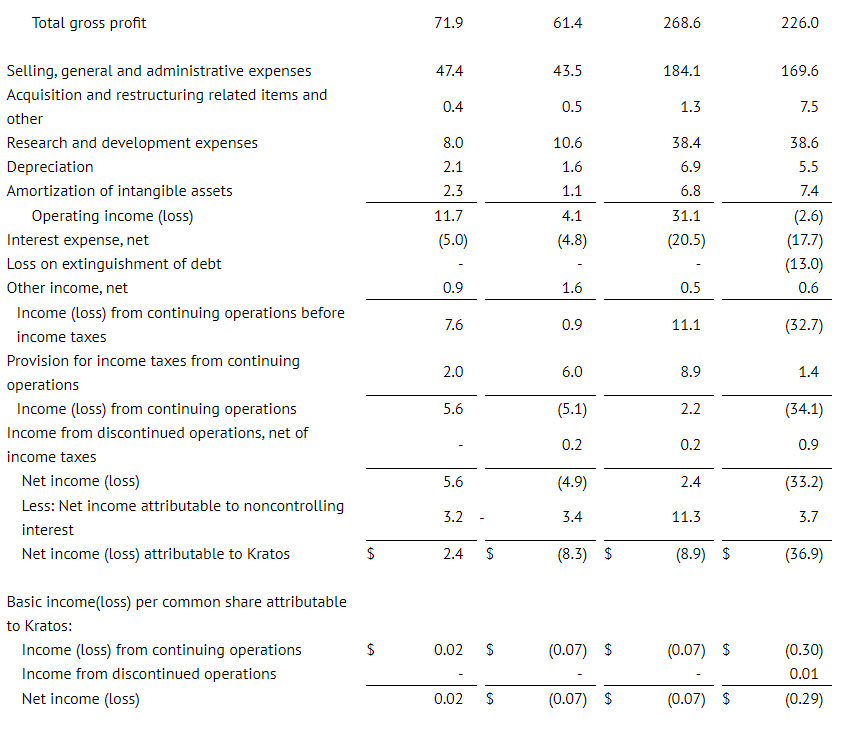

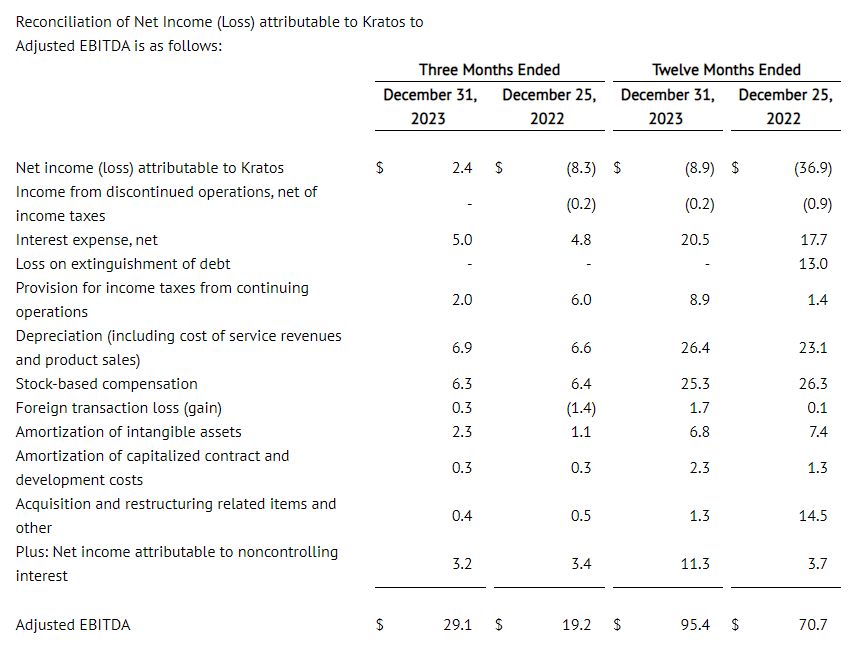

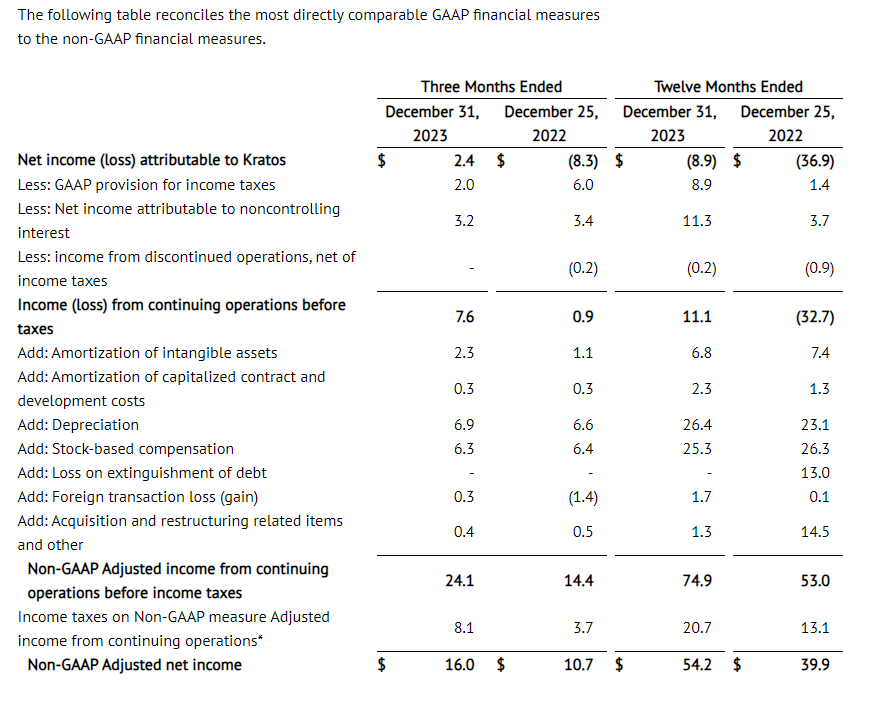

SAN DIEGO, Feb. 13, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology Company in the Defense, National Security and Global Markets, today reported its fourth quarter 2023 financial results, including Revenues of $273.8 million, Operating Income of $11.7 million, Net Income attributable to Kratos of $2.4 million, Adjusted EBITDA of $29.1 million and a consolidated book to bill ratio of 1.2 to 1.0.

Included in fourth quarter 2023 Net Income and Operating Income is non-cash stock compensation expense of $6.3 million and Company-funded Research and Development (R&D) expense of $8.0 million, which includes significant ongoing development efforts in our Space and Satellite Communications business to develop our virtual, software-based OpenSpace command & control (C2), telemetry tracking & control (TT&C) and other ground system solutions. The fourth quarter 2023 Net Income attributable to Kratos includes $3.2 million attributable to a non-controlling interest, which includes a charge of $2.7 million adjustment recorded to reflect the estimated increase in the value of the redeemable non-controlling interest to the estimated redemption amount by Kratos.

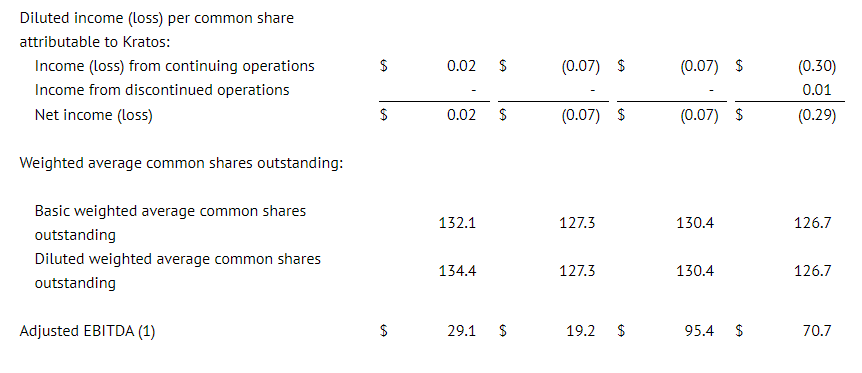

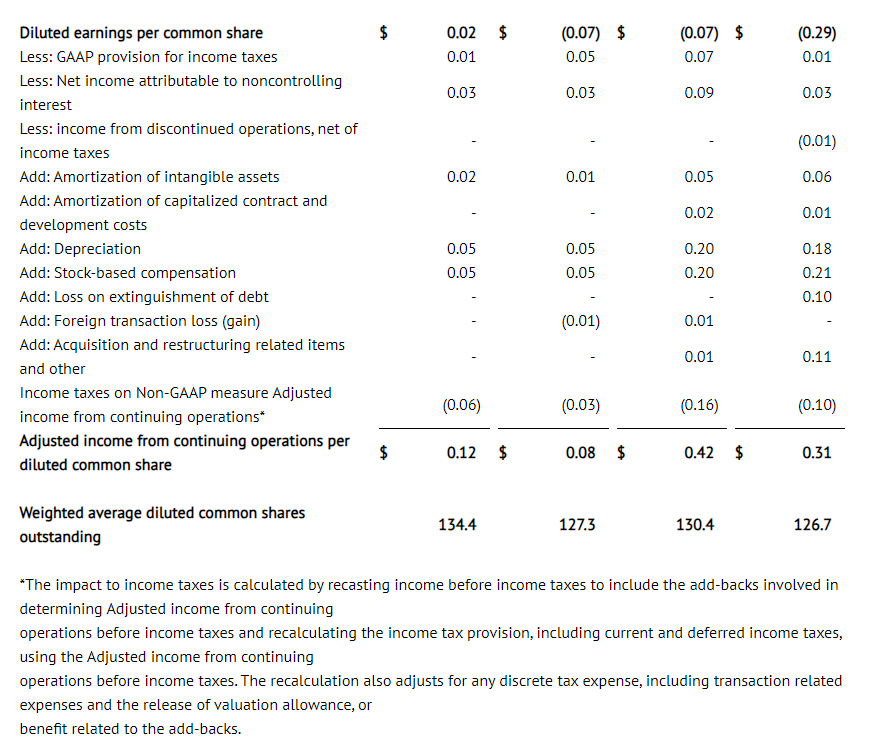

Kratos reported fourth quarter 2023 GAAP Net Income attributable to Kratos of $2.4 million and a GAAP Net Income per share of $0.02, compared to a GAAP Net Loss attributable to Kratos of $8.3 million and a GAAP Net Loss per share of $0.07 for the fourth quarter of 2022. Adjusted earnings per share (EPS) was $0.12 for the fourth quarter of 2023, compared to $0.08 for the fourth quarter of 2022.

Fourth quarter 2023 Revenues of $273.8 million increased $24.5 million, reflecting 9.8 percent and 7.3 percent organic growth, respectively, from fourth quarter 2022 Revenues of $249.3 million. Fourth quarter 2023 Cash Flow Generated from Operations was $67.4 million, primarily reflecting the receipt of accelerated favorable customer milestone payments, resulting in a Consolidated Days Sales Outstanding reduction from 117 days in the third quarter of 2023 to 109 days in the fourth quarter of 2023 and increases in deferred revenues or customer advanced payments to $101.8 million at the end of the fourth quarter of 2023, up from $79.4 million at the end of the third quarter of 2023. Free Cash Flow Generated from Operations for the Fourth Quarter of 2023 was $48.1 million after funding of $19.3 million of capital expenditures. Capital expenditures remain elevated due primarily to the manufacture of two production lots of Valkyries prior to contract award, to meet anticipated customer orders and requirements.

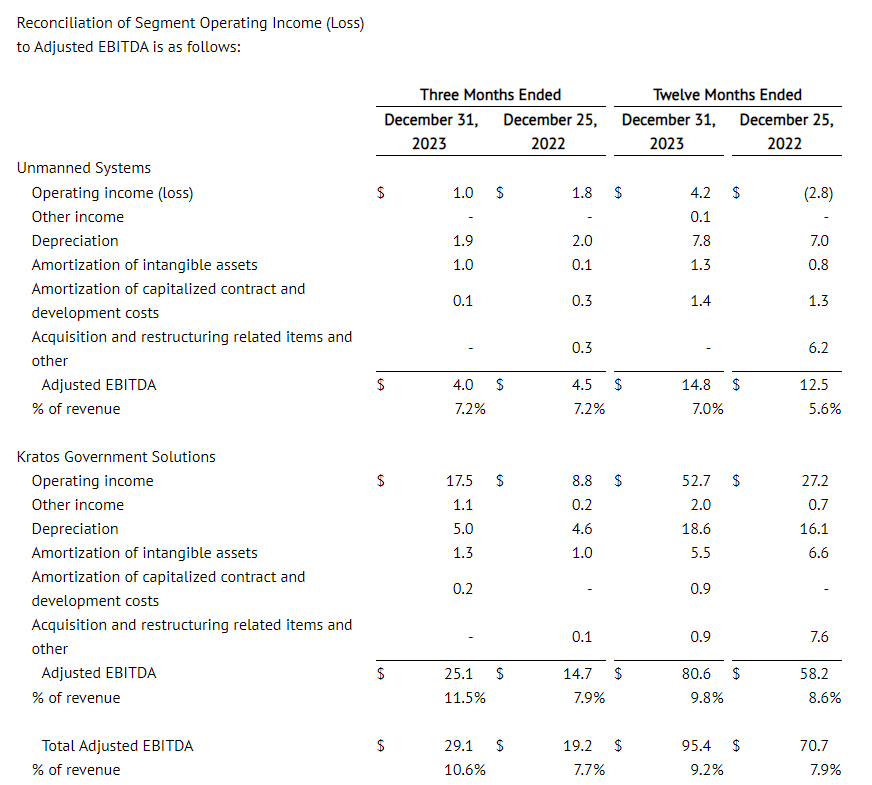

For the fourth quarter of 2023, Kratos’ Unmanned Systems (KUS) segment generated Revenues of $55.4 million, which included contribution of $6.4 million from the recent Sierra Technical Services, Inc. (STS) acquisition, as compared to $62.7 million in the fourth quarter of 2022, primarily reflecting reduced tactical drone activity. KUS’s Operating Income was $1.0 million in the fourth quarter of 2023 compared to $1.8 million in the fourth quarter of 2022. KUS’s Adjusted EBITDA for the fourth quarter of 2023 was $4.0 million, compared to fourth quarter 2022 KUS Adjusted EBITDA of $4.5 million, reflecting reduced volume.

KUS’s book-to-bill ratio for the fourth quarter of 2023 was 1.1 to 1.0 and 1.2 to 1.0 for the last twelve months ended December 31, 2023, with bookings of $61.2 million for the three months ended December 31, 2023, and bookings of $244.2 million for the last twelve months ended December 31, 2023. Total backlog for KUS at the end of the fourth quarter of 2023 was $255.8 million compared to $227.8 million at the end of the third quarter of 2023.

For the fourth quarter of 2023, Kratos’ Government Solutions (KGS) segment Revenues of $218.4 million increased from Revenues of $186.6 million in the fourth quarter of 2022, reflecting a 17.0 percent growth and organic growth rate. The increased Revenues includes organic revenue growth in our Space, Satellite, Cyber and Training Solutions, Turbine Technologies, C5ISR, and Microwave Products businesses.

KGS reported operating income of $17.5 million in the fourth quarter of 2023 compared to $8.8 million in the fourth quarter of 2022, primarily reflecting a more favorable mix and increased revenue volume. Fourth quarter 2023 KGS Adjusted EBITDA was $25.1 million, compared to fourth quarter 2022 KGS Adjusted EBITDA of $14.7 million, primarily reflecting the increased revenue and more favorable mix.

Kratos’ Space, Satellite, Cyber and Training business generated Revenues of $112.9 million in the fourth quarter of 2023 compared to $97.7 million in the fourth quarter of 2022, reflecting a 15.5 percent organic growth rate.

KGS reported a book-to-bill ratio of 1.2 to 1.0 for the fourth quarter of 2023, a book to bill ratio of 1.1 to 1.0 for the last twelve months ended December 31, 2023 and bookings of $269.2 million and $902.2 million for the three and last twelve months ended December 31, 2023, respectively. KGS includes Kratos’ Space, Satellite, Cyber and Training Solutions business, which reported a book to bill ratio of 1.2 to 1.0 for the fourth quarter and the last twelve months ended December 31, 2023. Bookings for Kratos’ Space, Satellite, Cyber and Training business for the three months and last twelve months ended December 31, 2023 were $132.2 million and $493.5 million, respectively. KGS’s total backlog at the end of the fourth quarter of 2023 was $988.0 million, as compared to $937.3 million at the end of the third quarter of 2023.

Kratos reported consolidated bookings of $330.3 million and a book-to-bill ratio of 1.2 to 1.0 for the fourth quarter of 2023, and consolidated bookings of $1.15 billion and a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended December 31, 2023. Consolidated backlog was $1.24 billion on December 31, 2023 and $1.17 billion on October 1, 2023. Kratos’ bid and proposal pipeline was $11.0 billion at December 31, 2023 and $10.3 billion at October 1, 2023. Backlog at December 31, 2023 included funded backlog of $944.6 million and unfunded backlog of $299.3 million.

Full Year 2023 Results

Kratos reported its full year 2023 financial results, including Revenues of $1.037 billion, Operating Income of $31.1 million, Net Loss attributable to Kratos of $8.9 million, Adjusted EBITDA of $95.4 million and a consolidated book to bill ratio of 1.1 to 1.0.

Included in the full year 2023 Net Loss and Operating Income is non-cash stock compensation expense of $25.3 million and Company-funded Research and Development (R&D) expense of $38.4 million, which includes significant ongoing development efforts in our Space and Satellite Communications business to develop our first to market, virtual, software-based OpenSpace command & control (C2), telemetry tracking & control (TT&C) and other ground system solutions. The full year 2023 Net Loss attributable to Kratos includes $11.3 million attributable to a non-controlling interest, which includes charges of $9.9 million of adjustments recorded to reflect the estimated increase in the value of the redeemable non-controlling interest to the estimated redemption amount by Kratos.

Kratos reported full year 2023 GAAP Net Loss attributable to Kratos of $8.9 million and a GAAP Net Loss per share of $0.07, compared to a GAAP Net Loss attributable to Kratos of $36.9 million and a GAAP Net Loss per share of $0.29 for the full year 2022. Adjusted earnings per share (EPS) was $0.42 for the full year 2023, compared to $0.31 for full year 2022.

Full year 2023 Revenues of $1.037 billion increased $138.8 million, reflecting 15.5 percent growth and 12.6 percent organic growth, respectively, from full year 2022 Revenues of $898.3 million. Full year 2023 Cash Flow Generated from Operations was $65.2 million, primarily reflecting the receipt of accelerated favorable customer milestone payments, offset partially by working capital uses including increases in inventories of approximately $29.6 million. Free Cash Flow Generated from Operations was $21.1 million after funding of $52.4 million of capital expenditures, less $8.3 million in receipt of proceeds for sale of Valkyries that were built as Kratos capital assets. Full year 2023 capital expenditures were elevated due primarily to the manufacture of the two production lots of Valkyries prior to contract award to meet anticipated customer orders and requirements.

For full year 2023, KUS generated Revenues of $212.2 million, which included contribution of $6.4 million from the recent STS acquisition, as compared to $221.7 million in the full year 2022, primarily reflecting reduced tactical drone activity. KUS’s Operating Income was $4.2 million in full year 2023 compared to an Operating Loss of $2.8 million in full year 2022. KUS’s Adjusted EBITDA for full year 2023 was $14.8 million, compared to full year 2022 KUS Adjusted EBITDA of $12.5 million, reflecting the reduced volume offset by a more favorable mix.

For full year 2023, KGS Revenues of $824.9 million increased $148.3 million, reflecting 21.9 percent growth and 18.9 percent organic growth, respectively, from Revenues of $676.6 million in full year 2022. The increased Revenues includes organic revenue growth in our Space, Satellite, Cyber and Training Solutions, Turbine Technologies, C5ISR, and Microwave Products businesses.

KGS reported operating income of $52.7 million in full year 2023 compared to $27.2 million in full year 2022, primarily reflecting a more favorable mix and increased revenue volume. Full year 2023 KGS Adjusted EBITDA was $80.6 million, compared to full year 2022 KGS Adjusted EBITDA of $58.2 million, primarily reflecting the more favorable mix and increased revenue.

Kratos’ Space, Satellite, Cyber and Training business generated Revenues of $423.0 million in full year 2023 compared to $359.0 million in full year 2022, reflecting a 17.8 percent growth and organic growth rate.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ strategy as a technology company and making internally funded investments to be first to market with affordable systems, software and products, is being successfully executed. Additionally, Kratos taking the prime or lead position on program opportunities where we believe the Kratos internal investment required is acceptable and the probability of Kratos win is high, and also Kratos teaming with a traditional system integrator partner, for a combined even greater probability of win on other opportunities is clearly working. Kratos’ low cost, innovation, rapid development and engineering up front for affordable mass production, brings significant value to our customers, our prime system integrator partners in teaming situations, and to our shareholders.”

Mr. DeMarco continued, “As we begin 2024, expected Kratos’ base case growth areas include: satellite communications; jet engines for drones, missiles, loitering munitions, supersonic and space systems; hypersonic systems; C5ISR and microwave electronics for missile, radar and CUAS systems and augmented reality training systems. We are currently producing approximately 160 high performance tactical and target jet drones annually, with a validated and executing supply chain in place, and we are making the investments necessary to triple our drone production capacity. As the only Company with a family of affordable, attritable, tactical jet drones flying today with weapons range pedigree and with additional new jet drones in development, all under customer funded contracts, we are confident that we will be successful. We are forecasting Kratos’ unmanned systems business to be one of our leading growth drivers in 2024, including target drone production and tactical drone RDT&E and S&T contracts, including a new tactical drone program award.”

Mr. DeMarco concluded, “Business challenges include our ability to obtain and retain qualified personnel, including those that are willing and able to obtain National Security clearances and the related high cost of these individuals, which is currently adversely impacting our margins. Additionally, the U.S. Federal Government budgetary situation is a challenge for the industry and for Kratos, and one that we cannot control and an extended Continuing Resolution Authorization (CRA) could adversely impact our business and financial forecast if not resolved soon.”

Financial Guidance

We are providing our initial 2024 first quarter and full year financial guidance, which includes our current forecasted business mix, and our assumptions, including as related to: employee sourcing, hiring and retention; manufacturing, production and supply chain disruptions; parts shortages and related continued potential significant cost and price increases, including for employees, materials and components that are impacting the industry and Kratos. The range of our expected first quarter and full year 2024 Revenues and Adjusted EBITDA includes assumptions of forecasted execution, including the number and estimated costs of qualified personnel expected to be obtained and retained to successfully execute on our programs and contracts, as well as expected contract awards. A U.S. Government budget was not passed by October 1, 2023, the beginning of Federal Fiscal Year 2024, and as a result, Kratos and others in our industry are operating under a Continuing Resolution Authorization (CRA), which currently expires March 8, 2024, under which no new contracts and no increases in existing contracts production or funding, among other stipulations, is permitted. Kratos’ 2024 financial forecast and guidance provided today assumes that the current CRA will be resolved and that a U.S. Federal and DoD budget which includes no unexpected budget cuts impacting our business will be in place by March 8, 2024. As a result, similar to Kratos’ 2023 quarterly financial trajectory, which fiscal year also experienced a CRA, we are forecasting Kratos’ third and fourth financial quarter’s results of 2024 to be significantly greater than the fiscal first and second quarter’s results, with the fourth quarter expected to be particularly strong in both revenue and Adjusted EBITDA. If the current CRA goes beyond the existing March 8, 2024 date, we will evaluate Kratos’ 2024 financial forecast at that time, based on the existing facts, circumstances and expectations.

Kratos’ 2024 financial forecast and guidance includes elevated investments for capital expenditures, including continued manufacture of two production lots of Valkyries prior to contract award, to meet anticipated customer orders and requirements, the expansion and build-out of the Company’s Microwave Products production facilities, and the expansion of our manufacturing and production facilities in our Rocket Systems and Hypersonic businesses.

Our first quarter and full year 2024 guidance ranges are as follows:

Current Guidance Range

$M

Q124

FY24

Revenues

$240 – $260

$1,125 – $1,150

R&D

$9 – $11

$42 – $45

Operating Income

$1 – 3

$37 – $41

Depreciation

$6 – $8

$28 – $30

Amortization

$2 – $3

$8 – $10

Stock Based Compensation

$6 – $7

$26- $28

Adjusted EBITDA

$16 – $18

$102 – $107

Operating Cash Flow

$50 – $60

Capital Expenditures

$70 – $80

Free Cash Flow Use

($10 – $30)

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice RegardingForward-LookingStatements This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its first quarter and full year 2024 revenues, organic revenue growth rates, R&D, operating income (loss), depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2024 operating cash flow, capital expenditures and other investments, and free cash flow, the Company’s future growth trajectory and ability to achieve improved revenue mix and profit in certain of its business segments and the expected timing of such improved revenue mix and profit, including the Company’s ability to achieve sustained year over year increasing revenues, profitability and cash flow, the Company’s expectation of ramp on projects and that investments in its business, including Company funded R&D expenses and ongoing development efforts, will result in an increase in the Company’s market share and total addressable market and position the Company for significant future organic growth, profitability, cash flow and an increase in shareholder value, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, planned 2024 investments, including in the tactical drone and satellite areas, and the related potential for additional growth in 2025 and beyond, ability to successfully compete and expected new customer awards, including the magnitude and timing of funding and the future opportunity associated with such awards, including in the target and tactical drone and satellite communication areas, performance of key contracts and programs, including the timing of production and demonstration related to certain of the Company’s contracts and control (TT&C) product offerings, the impact of the Company’s restructuring efforts and cost reduction measures, including its ability to improve profitability and cash flow in certain business units as a result of these actions and to achieve financial leverage on fixed administrative costs, the ability of the Company’s advanced purchases of inventory to mitigate supply chain disruptions and the timing of converting these investments to cash through the sales process, benefits to be realized from the Company’s net operating loss carry forwards, the availability and timing of government funding for the Company’s offerings, including the strength of the future funding environment, the short-term delays that may occur as a result of Continuing Resolutions or delays in U.S. Department of Defense (DoD) budget approvals, timing of LRIP and full rate production related to the Company’s unmanned aerial target system offerings, as well as the level of recurring revenues expected to be generated by these programs once they achieve full rate production, market and industry developments, and the current estimated impact of COVID-19 and employee absenteeism, supply chain disruptions, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoD may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoD Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates and risks related to the interest rate swap contract to hedge Term SOFR associated with the Company’s Term Loan A; currently unforeseen risks associated with COVID-19 and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 31, 2023, and in our other filings made with the Securities and Exchange Commission.