The White House, on Monday, June 26, launched an effort to refresh and even rebrand the administration’s economic policies. “Bidenomics” is the latest name given to the White House initiatives to invest in the country’s future. The unveiling of the latest spending plans includes $42.5 billion that will be spread to benefit all 50 states.

While the largest details of what Bidenomics is expected to entail will be presented in Chicago on Wednesday, some of the plans were unveiled on Monday. Spokespeople, including President Biden and Vice President Harris, laid out an “internet for all” plan in a public address.

The plan is to spend, on average, $750 million in each state in a bidding process for high-speed internet projects where there is none.

The overall thinking is that internet availability is viewed as a utility, much like the electrification of all communities.

President Biden indicated Made in America would be integral to the plan. Pointing out thousands of miles of fiber optic cable will be built and laid as part of the project.

Other investment areas that may see added demand is commodities such as copper. The metal is a key element in cables, routers, and switches. As a result, the demand for copper could be expected increase as more and more people connect to the internet.

Fiber optic cables were specifically mentioned in the announcement; manufacturers of not just the cable, but connections, and companies that install the cable could potentially benefit from the $42.5 billion being spread, for coast-to-coast high-speed internet.

While the project is to be completed over the next six years, for each new household or business that gains internet access along the way, a potential new customer for many types of businesses goes online. Beneficiaries could include telecommunications, media, education, online retail, and of course big tech. As the internet has more steady users, these industries will all see increased demand for their services.

Take Away

Investing in companies that benefit from changes in government policies or spending is a common strategy that has helped many portfolios.

A big announcement on what to expect from the new Bidenomics was made on June 26; the country is promised an even greater announcement on June 28. Investors should note, the government does not build out these projects themselves; it engages private companies. At times the US government quickly becomes a large customer of these companies’, adding stability of revenue and significant profit to bottom lines. The President promised a Made in America approach to the contract process.

This Week’s Economic Focus Will be on PCE Inflation

It’s the last trading week of the month, quarter, and first half of 2023. The Fed Chair is scheduled to speak on Wednesday at the ECB Forum on Central Bank Policy, and the Fed’s favored inflation gauge will be released on Friday. As we approach the 2023 halfway point, the S&P 500 is up 13.25% YTD. Historically, whenever the S&P 500 is up at least 10% YTD at the end of June, the index ends the year up on the year 82% of the time. However, it gained 7.7% on average for those years, which suggests some gains were given back in the average year.

Monday 6/26

• The ECB Forum on Central Banking 2023 is a three day event beginning Monday. The US Federal Reserve Chairman will take part in a panel discussion Wednesday.

Tuesday 6/27

• 8:30 PM ET, Durable Goods orders are forecasted to have fallen 1.0 percent in May after April’s 1.1 percent rise. Ex-transportation orders are seen unchanged with core capital goods orders, after jumping 1.3 percent in April, rising a further 0.6 percent.

• 10:00 AM ET, Consumer Confidence is expected to rebound slightly in June to 103.7 versus May’s 102.3 which was better than expected but still down 1.4 points from April. The index has sat at depressed levels for the past year.

• 1:00 PM ET, Money Supply, including the closely watched M2 will be released. M2 had stood at $20,673.1 Billion as of the last reporting. The act of the Fed tightening credit conditions, is typically orchestrated by reducing money in the system which can be expected to reduce money supply by its two most watched measures, M1 and M2.

Wednesday 6/28

• 9:30 AM ET, at 2:30 PM in Portugal a panel discussion on policy will be modersated by CNBCs Sara Eisen. The four member panel will include J. Powell, US Federal Reserve, A. Bailey, Bank of England, C. Lagarde, ECB, and K. Ueda, Bank of Japan.

• 10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products.

Thursday 6/29

• 8:30 AM ET, First quarter GDP third estimate is expected to show 1.4% growth. While this is not e a strong pace, it indicates the US is not currently in a recession.

• 8:30 AM ET, Jobless Claims for the week ending June 24 are expected to be 270,000 versus a second straight and elevated 264,000 in the two prior weeks and 262,000 the week before.

• 4:30 PM ET, Factors Affecting Reserve Balances, otherwise known as The Fed’s Balance Sheet or the H.4.1 report is a weekly report of a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report.

Friday 6/30

• 8:30 AM ET, Personal Income and Outlays, including PCE Inflation, will be released as part of a data set. Income is expected to rise 0.4 percent in May, with consumption expenditures expected to increase by 0.2 percent. These would compare with April’s 0.4 percent gain for income and 0.8 percent jump for consumption. PCE Inflation readings for May are expected at monthly increases of 0.1 percent overall and 0.4 percent for the core (versus April’s respective increases of 0.4 percent for both) for annual rates of 3.8 and 4.7 percent (versus April’s 4.4 and 4.7 percent).

• 10:00 AM ET, Consumer Sentiment is expected to end the first half of 2023 at 63.9 for June, this would be up nearly 4 points from May.

What Else

The summer doldrums is a Wall Street term for reduced trading activity between Memorial Day and Labor Day. Many professional investors take time off from work during the summer; this means portfolios are in the hands of the second-string portfolio managers that are there to monitor and maintain but not take big positions or make big decisions. Volume is often reduced, which could cause exaggerated swings in prices.

Lifeway Foods, Inc. (LWAY), which has been recognized as one of Forbes’ Best Small Companies, is America’s leading supplier of the probiotic fermented beverages. Wherever you are on Monday, you can attend the virtual roadshow and better understand directly from management the many intricacies of the probiotic food business as it relates to Lifeway. Should you have a question for management, there will be an ample Q&A period for participants to get their questions answered.

Adopts Limited Duration Shareholder Rights Plan to Protect the Best Interest of Shareholders

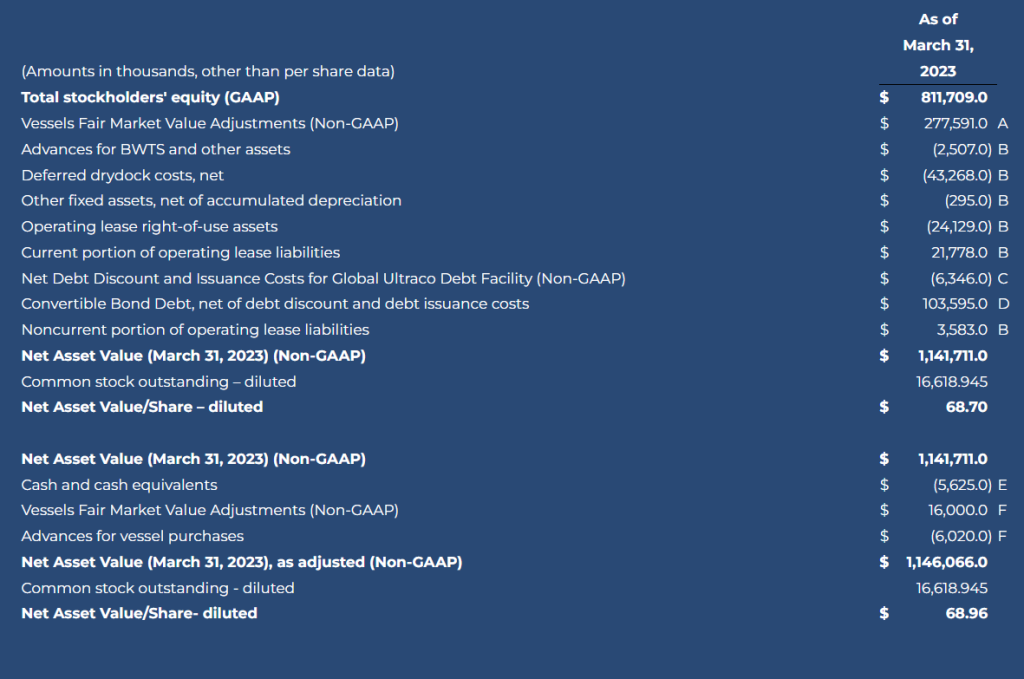

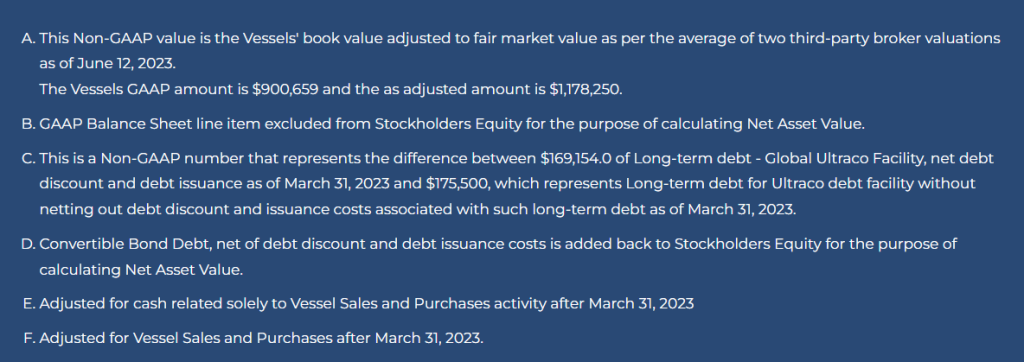

STAMFORD, Conn., June 22, 2023 (GLOBE NEWSWIRE) — Eagle Bulk Shipping Inc. (NYSE: EGLE) (“Eagle Bulk”, “Eagle”, or the “Company”), one of the world’s largest owner-operators within the midsize drybulk vessel segment, today announced that its Board of Directors has approved an agreement with Oaktree Capital Management (“Oaktree”) and certain of its affiliates pursuant to which Eagle has repurchased approximately 3.8 million shares of Eagle common stock, representing Oaktree’s entire stock ownership of approximately 28% in the Company, for an aggregate purchase price of approximately $219.3 million. The purchase price of $58.00 per share represents a discount of approximately $11.00 per share or approximately 16% to Net Asset Value, as adjusted (“NAV”) per share-diluted based on March 31, 2023 financials and current fleet valuations.1

The Board unanimously arrived at its determination after careful consideration, including consultation with outside legal and financial advisors.

Eagle’s Chairman Paul Leand, Jr. commented, “Today’s transaction is in the best interest of our shareholders, both financially and strategically. It ensures that shareholders maintain the opportunity to realize the value of their investment in Eagle Bulk and eliminates any potential disruption resulting from the sale of a very significant interest in the Company.”

Eagle’s CEO Gary Vogel added, “We believe the transaction will be significantly accretive to NAV per share and EPS in future periods based on historically strong supply-side fundamentals. Looking ahead, we will continue to execute on our growth and renewal strategy, including building upon our 33 previous ship acquisitions, and remain committed to acting opportunistically to create value for all of our shareholders.”

Eagle’s balance sheet remains strong, with total liquidity of approximately $188 million based on March 31, 2023 financials, as adjusted for this transaction, previously communicated financing, and vessel sale and purchase activity. The Company noted that it remains committed to its balanced capital allocation strategy, including maintaining its current dividend policy of 30% of net income, which we believe will be positively impacted by this transaction, and continued repayment of term debt.

As a result of this transaction, the Company’s outstanding common stock will be reduced to approximately 9.3 million shares. The transaction will be financed by cash-on-hand and drawings under the Company’s credit facility.

Eagle Bulk provided supplemental slides in connection with this announcement under the “Investors” section of the Company’s website https://ir.eagleships.com/.

Oaktree became a shareholder in Eagle Bulk in October 2014.

Shareholder Rights Plan

Additionally, the Company announced that its Board of Directors has unanimously adopted a limited duration shareholder rights plan (the “Rights Plan”). The Rights Plan is effective immediately and has a one year duration expiring on June 22, 2024 unless extended by shareholders. The Rights Plan will reduce the likelihood that any person or group gains control of the Company through open market accumulation, or other abusive tactics potentially disadvantaging the interests of all shareholders, without paying all shareholders an appropriate control premium or providing the Company’s Board of Directors sufficient time to make informed decisions in the best interest of all shareholders. The Rights Plan is not intended to interfere with any transaction that the Board of Directors determines to be in the best interests of shareholders, nor does the Rights Plan prevent the Board of Directors from considering any proposal.

Pursuant to the Rights Plan, the Company will distribute one right for each share of common stock outstanding as of the close of business on July 3, 2023. While the Rights Plan is effective immediately, the rights generally would become exercisable only if a person or group (including a group of persons that are acting in concert with each other) acquires beneficial ownership, as defined in the Rights Plan, of 15% or more of the Company’s common stock in a transaction not approved by the Company’s Board of Directors. In that situation, each holder of a right (other than the acquiring person or group) will have the right to purchase, upon payment of the then-current exercise price, a number of shares of Company common stock having a market value of twice the exercise price of the right. In addition, at any time after a person or group acquires 15% or more of the Company’s common stock, the Company’s Board of Directors may exchange one share of the Company’s common stock for each outstanding right (other than rights owned by such person or group, which would have become void).

The Rights Plan will expire on the close of business on the first anniversary of the date of entry into the Rights Plan unless extended for two more years by shareholders. It could also expire earlier if prior to such date, the rights are redeemed or exchanged. The Company’s Board of Directors may consider an earlier termination of the Rights Plan if market and other conditions warrant.

Further details regarding the Oaktree transaction and Rights Plan will be contained in a Current Report on Form 8-K that the Company will be filing with the U.S. Securities and Exchange Commission (“SEC”). These filings will be available on the SEC’s web site at www.sec.gov.

Akin Gump Strauss Hauer & Feld LLP is serving as legal advisor to the Company. Hogan Lovells US LLP is serving as legal advisor and Houlihan Lokey is serving as financial advisor to the Company’s Board of Directors.

About Eagle Bulk Shipping Inc.

Eagle Bulk Shipping Inc. (“Eagle” or the “Company”) is a US-based, fully integrated shipowner-operator providing global transportation solutions to a diverse group of customers including miners, producers, traders, and end users. Headquartered in Stamford, Connecticut, with offices in Singapore and Copenhagen, Eagle focuses exclusively on the versatile midsize drybulk vessel segment and owns one of the largest fleets of Supramax / Ultramax vessels in the world. The Company performs all management services in-house (including strategic, commercial, operational, technical, and administrative) and employs an active-management approach to fleet trading with the objective of optimizing revenue performance and maximizing earnings on a risk-managed basis. For further information, please visit our website: www.eagleships.com.

Supplemental Information – Non-GAAP Financial Measures

This release includes Net Asset Value per share-diluted, a non-GAAP financial measure as defined under the rules of the SEC. We believe non-GAAP measures provide important supplemental information to investors regarding the information discussed in this release. However, you should not rely on any non-GAAP financial measure alone as a measure of our performance. We believe that non-GAAP financial measures reflect an additional way of viewing our business that, when taken together with GAAP results and the reconciliations to corresponding GAAP financial measures that we also provide, give a more complete understanding of factors and trends affecting our business. We strongly encourage you to review all of our financial statements and publicly-filed reports in their entirety and to not solely rely on any single non-GAAP financial measure. Because non-GAAP financial measures are not standardized, it may not be possible to compare these financial measures with other companies’ non-GAAP financial measures, even if they have similar names.

Forward-Looking Statements Matters discussed in this release may constitute forward-looking statements that may be deemed to be “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and are intended to be covered by the safe harbor provided for under these sections. These statements may include words such as “believe,” “estimate,” “project,” “intend,” “expect,” “plan,” “anticipate,” and similar expressions in connection with any discussion of the timing or nature of future operating or financial performance or other events. Forward-looking statements in this release reflect management’s current expectations and observations with respect to future events and financial performance. Where we express an expectation or belief as to future events or results, including future plans with respect to financial performance, the payment of dividends and/or repurchase of shares, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, our forward-looking statements are subject to risks, uncertainties, and other factors, which could cause actual results to differ materially from future results expressed, projected, or implied by those forward-looking statements.

Where we express an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, our forward-looking statements are subject to risks, uncertainties, and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by those forward-looking statements. The principal factors that affect our financial position, results of operations and cash flows include market freight rates, which fluctuate based on various economic and market conditions, periods of charter hire, vessel operating expenses and voyage costs, which are incurred primarily in U.S. dollars, depreciation expenses, which are a function of the purchase price of our vessels and our vessels’ estimated useful lives and scrap value, general and administrative expenses, and financing costs related to our indebtedness. The accuracy of the Company’s assumptions, expectations, beliefs and projections depends on events or conditions that change over time and are thus susceptible to change based on actual experience, new developments and known and unknown risks. The Company gives no assurance that the forward-looking statements will prove to be correct and does not undertake any duty to update them. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of certain factors which could include the following: (i) volatility of freight rates driven by changes in demand for seaborne transportation of drybulk commodities and in supply of drybulk shipping capacity; (ii) changes in drybulk carrier capacity driven by levels of newbuilding orders, scrapping rates or fleet utilization; (iii) changes in rules and regulations applicable to the drybulk industry, including, without limitation, regulations of the International Maritime Organization and the European Union (the “EU”), requirements of the Environmental Protection Agency and other governmental and quasi-governmental agencies; (iv) changes in U.S. and EU economic sanctions and trade embargo laws and regulations as well as equivalent economic sanctions laws of other relevant jurisdictions; (v) actions taken by regulatory authorities including, without limitation, the U.S. Treasury Department’s Office of Foreign Assets Control (“OFAC”); (vi) changes in the typical seasonal variations in drybulk freight rates; (vii) changes in national and international economic and political conditions including, without limitation, the current conflict between Russia and Ukraine, the current economic and political environment in China and the environment in historically high-risk geographic areas such as the South China Sea, the Indian Ocean, the Gulf of Guinea and the Gulf of Aden; (viii) changes in the condition of the Company’s vessels or applicable maintenance or regulatory standards (which may affect, among other things, our anticipated drydocking costs); (ix) the duration and impact of the novel coronavirus (“COVID-19”) pandemic and measures implemented by governments of various countries in response to the COVID-19 pandemic; (xi) volatility of the cost of fuel; (xii) volatility of costs of labor and materials needed to operate our business due to inflation; (xiii) any legal proceedings which we may be involved from time to time; and (xiv) other factors listed from time to time in our filings with the SEC.

We have based these statements on assumptions and analyses formed by applying our experience and perception of historical trends, current conditions, expected future developments and other factors we believe are appropriate in the circumstances. The Company’s future results may be impacted by adverse economic conditions, such as inflation, deflation, or lack of liquidity in the capital markets, that may negatively affect it or parties with whom it does business. Should one or more of the foregoing risks or uncertainties materialize in a way that negatively impacts the Company, or should the Company’s underlying assumptions prove incorrect, the Company’s actual results may vary materially from those anticipated in its forward-looking statements, and its business, financial condition and results of operations could be materially and adversely affected.

Risks and uncertainties are further described in reports filed by Eagle Bulk Shipping Inc. with the SEC.

1 This is a non-GAAP financial measure. A reconciliation of GAAP to this non-GAAP financial measure has been provided in the financial table included in this press release.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Busy Week. Kratos had two announcements this week, including the Company’s successful static test of its new Zeus 1 rocket motor at Aerojet Rocketdyne’s Camden, Arkansas facility and an expansion of the Company’s Space Domain Awareness (SDA) network locations into India.

Zeus 1 Motor. Kratos’ Zeus 1 motor is an affordable commercial solid rocket motor (SRM) in development, with the SRM being able to operate as launch vehicle stages for Kratos’ research, hypersonic, ballistic missile target, and “other” vehicles. The preliminary hardware and data inspection of the test showed the robustness of the motor design and its applicability for multiple customer applications. The Zeus 1 is one of two solid rocket motors being developed and funded, with the larger Zeus 2 motor scheduled for static test later this year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Takeaways from the Reuters Global Energy Transition Event

All videos now live on demand!

The Takeaway Series is available exclusively to Channelchek members. It’s totally free to join the community, just click the join button at the top of the page, or the Register button below.For best results, log in to your Channelchek account above before viewing the videos.

Noble Capital Markets Senior Research Analyst Michael Heim provides his takeaways from the event, plus all the fireside chats with c-suite energy executives. All in one click.

Almost No One Uses Bitcoin as Currency, New Data Proves. It’s Actually More Like Gambling

In recent weeks the asset status of Bitcoin has gained additional legitimacy as an asset but has done little to bolster any claim that it is a medium of exchange for goods and services. Does this matter? A Senior Lecturer on Economics and Society shares his thoughts on the present and future of Bitcoin and how that compares with its promise. – Paul Hoffman, Managing Editor, Channelchek

Bitcoin boosters like to claim Bitcoin, and other cryptocurrencies, are becoming mainstream. There’s a good reason to want people to believe this.

The only way the average punter will profit from crypto is to sell it for more than they bought it. So it’s important to talk up the prospects to build a “fear of missing out”.

There are loose claims that a large proportion of the population – generally in the range of 10% to 20% – now hold crypto. Sometimes these numbers are based on counting crypto wallets, or on surveying wealthy people.

But the hard data on Bitcoin use shows it is rarely bought for the purpose it ostensibly exists: to buy things.

Little Use for Payments

The whole point of Bitcoin, as its creator “Satoshi Nakamoto” stated in the opening sentence of the 2008 white paper outlining the concept, was that:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.

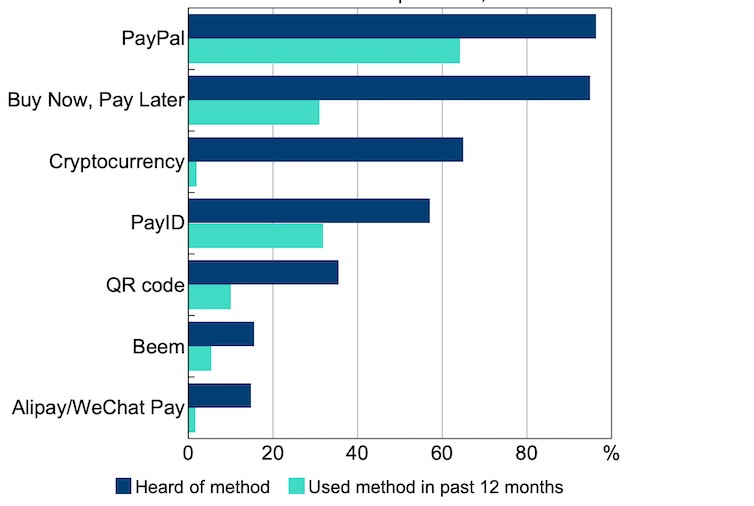

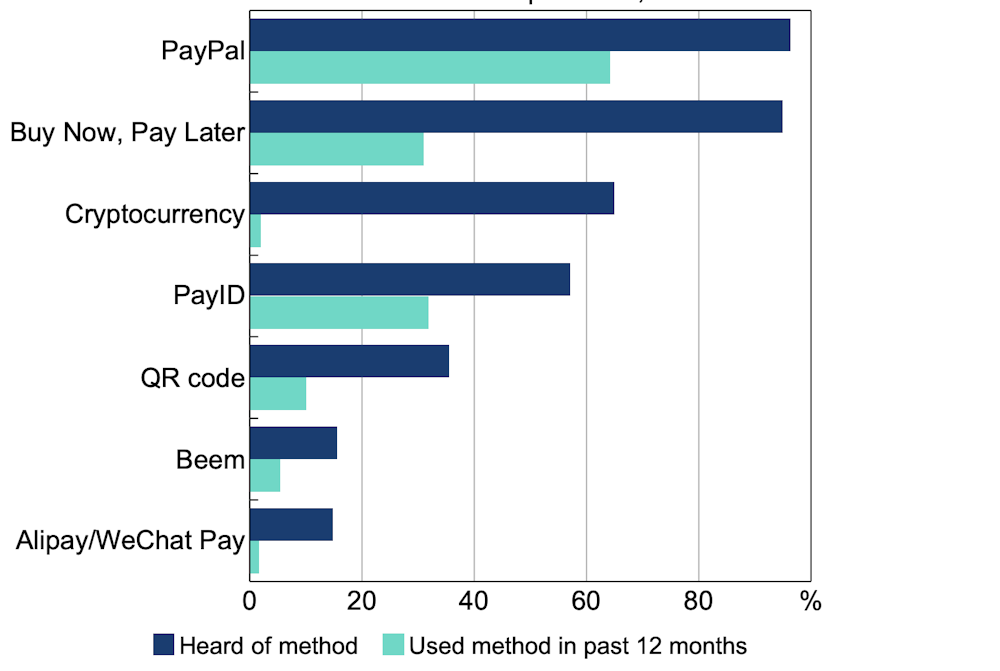

The latest data demolishing this idea comes from Australia’s central bank.

Every three years the Reserve Bank of Australia surveys a representative sample of 1,000 adults about how they pay for things. As the following graph shows, cryptocurrency is making almost no impression as a payments instrument, being used by no more than 2% of adults.

Payment Methods Being Used by Australians

Reserve Bank calculations of Australians’ awareness vs use of different payment methods, based on Ipsos data.

By contrast more recent innovations, such as “buy now, pay later” services and PayID, are being used by around a third of consumers.

These findings confirm 2022 data from the US Federal Reserve, showing just 2% of the adult US population made a payment using a cryptocurrrency, and Sweden’s Riksbank, showing less than 1% of Swedes made payments using crypto.

The Problem of Price Volatility

One reason for this, and why prices for goods and services are virtually never expressed in crypto, is that most fluctuate wildly in value. A shop or cafe with price labels or a blackboard list of their prices set in Bitcoin could be having to change them every hour.

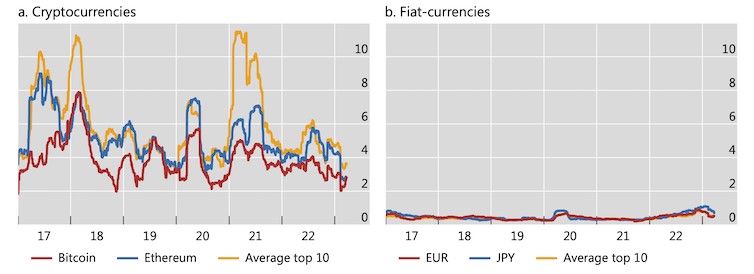

The following graph from the Bank of International Settlements shows changes in the exchange rate of ten major cryptocurrencies against the US dollar, compared with the Euro and Japan’s Yen, over the past five years. Such volatility negates cryptocurrency’s value as a currency.

There have been attempts to solve this problem with so-called “stablecoins”. These promise to maintain steady value (usually against the US dollar).

But the spectacular collapse of one of these ventures, Terra, once one of the largest cryptocurrencies, showed the vulnerability of their mechanisms. Even a company with the enormous resources of Facebook owner Meta has given up on its stablecoin venture, Libra/Diem.

This helps explain the failed experiments with making Bitcoin legal tender in the two countries that have tried it: El Salvador and the Central African Republic. The Central African Republic has already revoked Bitcoin’s status. In El Salvador only a fifth of firms accept Bitcoin, despite the law saying they must, and only 5% of sales are paid in it.

Storing Value, Hedging Against Inflation

If Bitcoin’s isn’t used for payments, what use does it have?

The major attraction – one endorsed by mainstream financial publications – is as a store of value, particularly in times of inflation, because Bitcoin has a hard cap on the number of coins that will ever be “mined”.

In terms of quantity, there are only 21 million Bitcoins released as specified by the ASCII computer file. Therefore, because of an increase in demand, the value will rise which might keep up with the market and prevent inflation in the long run.

The only problem with this argument is recent history. Over the course of 2022 the purchasing power of major currencies (US, the euro and the pound) dropped by about 7-10%. The purchasing power of a Bitcoin dropped by about 65%.

Speculation or Gambling?

Bitcoin’s price has always been volatile, and always will be. If its price were to stabilize somehow, those holding it as a speculative punt would soon sell it, which would drive down the price.

But most people buying Bitcoin essentially as a speculative token, hoping its price will go up, are likely to be disappointed. A BIS study has found the majority of Bitcoin buyers globally between August 2015 and December 2022 have made losses.

The “market value” of all cryptocurrencies peaked at US$3 trillion in November 2021. It is now about US$1 trillion.

Bitcoins’s highest price in 2021 was about US$60,000; in 2022 US$40,000 and so far in 2023 only US$30,000. Google searches show that public interest in Bitcoin also peaked in 2021. In the US, the proportion of adults with internet access holding cryptocurrencies fell from 11% in 2021 to 8% in 2022.

UK government research published in 2022 found that 52% of British crypto holders owned it as a “fun investment”, which sounds like a euphemism for gambling. Another 8% explicitly said it was for gambling.

The UK parliament’s Treasury Committee, a group of MPs who examine economics and financial issues, has strongly recommended regulating cryptocurrency as form of gambling rather than as a financial product. They argue that continuing to treat “unbacked crypto assets as a financial service will create a ‘halo’ effect that leads consumers to believe that this activity is safer than it is, or protected when it is not”.

Whatever the merits of this proposal, the UK committtee’s underlying point is solid. Buying crypto does have more in common with gambling than investing. Proceed at your own risk, and and don’t “invest” what you can’t afford to lose.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society, University of Canberra.

Different investment timelines call for different investments.

Have you ever looked at a chart of a company you were interested in, let’s say year-to-date, and thought, wow, this company has just dipped to where it could be expected to start to bring in buyers and go up? Then you look at a five-year chart, and the same stock has been trending down for years, and is actually close to where, from a longer-term perspective, a technical analyst would view it as more likely to weaken. Based on time perspective, both expectations can coincide with each other. This is why it is important to understand your own investment time frame before pulling the trigger on a stock.

The big question that needs to be answered first is, are you expecting the trade to work out in minutes, weeks, or years? Often this is based on any future needs of your invested capital.

If a trader is trying to make incremental income, they may use a five-minute chart. An investor looking to gain by holding weeks or months may use a one or three-year chart. Longer-term investors, those that are looking to put to bed what they hope will be the next Apple or Tesla in terms of performance, may look at charts using 20 years, or the “Max” time period.

Those that are longer-term investors can be less cautious about the exact timing on most investments, or less concerned about deciding if this is the ideal timing. This is especially relevant today in light of recession talk, rate increases, global risk, and other possible disruptions.

In fact, last year’s downward market direction was a wake up call for a lot of less seasoned investors, coming off so many so many positive years before. And this years retracement back up, is a good reminder that over time, markets have always broken new highs.

As mentioned above, when times are less certain, the investor that is looking to hold for an extended period, is the investor less likely to question their decision; many actually average into a position based on calendar buys, not price targets.

Having the long view, or deciding uncertain markets has dictated a longer view, would likely steer the investor to include smaller companies. Smaller companies have had the best long-term performance. It’s a category that may be more volatile but over time, has served investors better.

Over the past few years, small cap stocks have participated far less in the upward trend. That is less than larger companies (on average) and far less than they have versus their own historical average relative to large caps.

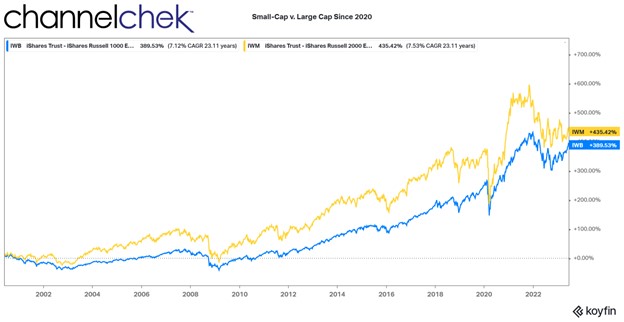

The chart above compares performance since the beginning of the decade of the Russell 2000 Large Cap performance (blue) to the Russell 2000 Small Cap index (gold). One thing that is evident immediately is the small cap stocks outperformed large caps long term by a large margin over time. The second is the trend is up. If you’d like, add a third which is there has been a significant dip in value (last year’s bear market).

“From our perspective, the uncertain present offers a highly opportune time to invest in small caps for the long run.” —Francis Gannon, Co-CIO Gannon Investment Partners (June 13. 2023)

Long term investors looking at this scenario could easily make a case for getting involved knowing that small caps historically overperform large caps. So if an investor is looking to maximize return, large caps may not have the highest probabilities. The above graph makes both points clear.

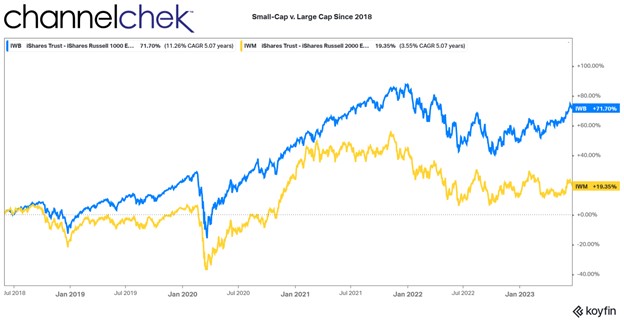

This second chart begins only five year ago. If one was to look at it by itself, the trendline over the years is upward, with gains in both large cap and small cap . But the large caps have a steeper upward pace. On the other hand, small caps are noticeably flat since the beginning of 2022.

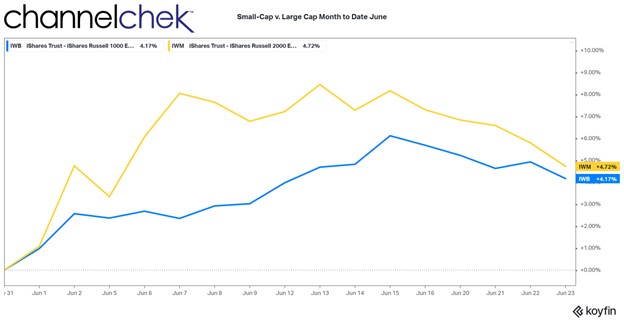

The last chart is just since the beginning of this month. Small cap stocks seem to finally have caught their tailwind, going up by more on most up days, and coming down by less on down days. Time will tell if this is a trend that will continue.

The small cap stock index won’t catch the large caps over night. If it happens, it will be months or years before investors that have been in small caps catch and pass those that have been in large cap stocks. Those investing now will outperform those that got in earlier. Of course, long-term investors are cautioned to also be diversified across many industries and of even market cap sectors.

Perhaps rebalancing the allocation after so many periods of small cap underperformance is a strategy that fits all the basic tenets that have been true of long-term investing.

They are:

Over time the stock market goes up and breaks new records.

Diversified portfolios spread risk and are less volatile.

Rebalance so allocations in sectors that have done well are not now undermining your asset mix.

Take Away

One can look at the same stock, over different time periods and see completely different trends. Those investing longer term, providing the company or industry isn’t in a decades long tailspin, reduce the risk of loss by letting time iron out the ups and downs.

Small cap stocks over time have outperformed larger companies. Assuming this hasn’t changed, when the volatility is “ironed out” small caps have a lot of catching up to do before they pass. This argues that they will return even greater comparative performance than if they were already ahead in recent years.

How Will AI Affect Workers? Tech Waves of the Past Show How Unpredictable the Path Can Be

The explosion of interest in artificial intelligence has drawn attention not only to the astonishing capacity of algorithms to mimic humans but to the reality that these algorithms could displace many humans in their jobs. The economic and societal consequences could be nothing short of dramatic.

The route to this economic transformation is through the workplace. A widely circulated Goldman Sachs study anticipates that about two-thirds of current occupations over the next decade could be affected and a quarter to a half of the work people do now could be taken over by an algorithm. Up to 300 million jobs worldwide could be affected. The consulting firm McKinsey released its own study predicting an AI-powered boost of US$4.4 trillion to the global economy every year.

The implications of such gigantic numbers are sobering, but how reliable are these predictions?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Bhaskar Chakravorti, Dean of Global Business, The Fletcher School, Tufts University.

I lead a research program called Digital Planet that studies the impact of digital technologies on lives and livelihoods around the world and how this impact changes over time. A look at how previous waves of such digital technologies as personal computers and the internet affected workers offers some insight into AI’s potential impact in the years to come. But if the history of the future of work is any guide, we should be prepared for some surprises.

The IT Revolution and the Productivity Paradox

A key metric for tracking the consequences of technology on the economy is growth in worker productivity – defined as how much output of work an employee can generate per hour. This seemingly dry statistic matters to every working individual, because it ties directly to how much a worker can expect to earn for every hour of work. Said another way, higher productivity is expected to lead to higher wages.

Generative AI products are capable of producing written, graphic and audio content or software programs with minimal human involvement. Professions such as advertising, entertainment and creative and analytical work could be among the first to feel the effects. Individuals in those fields may worry that companies will use generative AI to do jobs they once did, but economists see great potential to boost productivity of the workforce as a whole.

The Goldman Sachs study predicts productivity will grow by 1.5% per year because of the adoption of generative AI alone, which would be nearly double the rate from 2010 and 2018. McKinsey is even more aggressive, saying this technology and other forms of automation will usher in the “next productivity frontier,” pushing it as high as 3.3% a year by 2040.That sort of productivity boost, which would approach rates of previous years, would be welcomed by both economists and, in theory, workers as well.

If we were to trace the 20th-century history of productivity growth in the U.S., it galloped along at about 3% annually from 1920 to 1970, lifting real wages and living standards. Interestingly, productivity growth slowed in the 1970s and 1980s, coinciding with the introduction of computers and early digital technologies. This “productivity paradox” was famously captured in a comment from MIT economist Bob Solow: You can see the computer age everywhere but in the productivity statistics.

Digital technology skeptics blamed “unproductive” time spent on social media or shopping and argued that earlier transformations, such as the introductions of electricity or the internal combustion engine, had a bigger role in fundamentally altering the nature of work. Techno-optimists disagreed; they argued that new digital technologies needed time to translate into productivity growth, because other complementary changes would need to evolve in parallel. Yet others worried that productivity measures were not adequate in capturing the value of computers.

For a while, it seemed that the optimists would be vindicated. In the second half of the 1990s, around the time the World Wide Web emerged, productivity growth in the U.S. doubled, from 1.5% per year in the first half of that decade to 3% in the second. Again, there were disagreements about what was really going on, further muddying the waters as to whether the paradox had been resolved. Some argued that, indeed, the investments in digital technologies were finally paying off, while an alternative view was that managerial and technological innovations in a few key industries were the main drivers.

Regardless of the explanation, just as mysteriously as it began, that late 1990s surge was short-lived. So despite massive corporate investment in computers and the internet – changes that transformed the workplace – how much the economy and workers’ wages benefited from technology remained uncertain.

Early 2000s: New Slump, New Hype, New Hopes

While the start of the 21st century coincided with the bursting of the so-called dot-com bubble, the year 2007 was marked by the arrival of another technology revolution: the Apple iPhone, which consumers bought by the millions and which companies deployed in countless ways. Yet labor productivity growth started stalling again in the mid-2000s, ticking up briefly in 2009 during the Great Recession, only to return to a slump from 2010 to 2019.

Smartphones have led to millions of apps and consumer services but have also kept many workers more closely tethered to their workplaces. (Credit: Campaigns of the World)

Throughout this new slump, techno-optimists were anticipating new winds of change. AI and automation were becoming all the rage and were expected to transform work and worker productivity. Beyond traditional industrial automation, drones and advanced robots, capital and talent were pouring into many would-be game-changing technologies, including autonomous vehicles, automated checkouts in grocery stores and even pizza-making robots. AI and automation were projected to push productivity growth above 2% annually in a decade, up from the 2010-2014 lows of 0.4%.But before we could get there and gauge how these new technologies would ripple through the workplace, a new surprise hit: the COVID-19 pandemic.

The Pandemic Productivity Push – then Bust

Devastating as the pandemic was, worker productivity surged after it began in 2020; output per hour worked globally hit 4.9%, the highest recorded since data has been available.

Much of this steep rise was facilitated by technology: larger knowledge-intensive companies – inherently the more productive ones – switched to remote work, maintaining continuity through digital technologies such as videoconferencing and communications technologies such as Slack, and saving on commuting time and focusing on well-being.

While it was clear digital technologies helped boost productivity of knowledge workers, there was an accelerated shift to greater automation in many other sectors, as workers had to remain home for their own safety and comply with lockdowns. Companies in industries ranging from meat processing to operations in restaurants, retail and hospitality invested in automation, such as robots and automated order-processing and customer service, which helped boost their productivity.

But then there was yet another turn in the journey along the technology landscape.

The 2020-2021 surge in investments in the tech sector collapsed, as did the hype about autonomous vehicles and pizza-making robots. Other frothy promises, such as the metaverse’s revolutionizing remote work or training, also seemed to fade into the background.

In parallel, with little warning, “generative AI” burst onto the scene, with an even more direct potential to enhance productivity while affecting jobs – at massive scale. The hype cycle around new technology restarted.

Looking Ahead: Social Factors on Technology’s Arc

Given the number of plot twists thus far, what might we expect from here on out? Here are four issues for consideration.

First, the future of work is about more than just raw numbers of workers, the technical tools they use or the work they do; one should consider how AI affects factors such as workplace diversity and social inequities, which in turn have a profound impact on economic opportunity and workplace culture.

For example, while the broad shift toward remote work could help promote diversity with more flexible hiring, I see the increasing use of AI as likely to have the opposite effect. Black and Hispanic workers are overrepresented in the 30 occupations with the highest exposure to automation and underrepresented in the 30 occupations with the lowest exposure. While AI might help workers get more done in less time, and this increased productivity could increase wages of those employed, it could lead to a severe loss of wages for those whose jobs are displaced. A 2021 paper found that wage inequality tended to increase the most in countries in which companies already relied a lot on robots and that were quick to adopt the latest robotic technologies.

Second, as the post-COVID-19 workplace seeks a balance between in-person and remote working, the effects on productivity – and opinions on the subject – will remain uncertain and fluid. A 2022 study showed improved efficiencies for remote work as companies and employees grew more comfortable with work-from-home arrangements, but according to a separate 2023 study, managers and employees disagree about the impact: The former believe that remote working reduces productivity, while employees believe the opposite.

Third, society’s reaction to the spread of generative AI could greatly affect its course and ultimate impact. Analyses suggest that generative AI can boost worker productivity on specific jobs – for example, one 2023 study found the staggered introduction of a generative AI-based conversational assistant increased productivity of customer service personnel by 14%. Yet there are already growing calls to consider generative AI’s most severe risks and to take them seriously. On top of that, recognition of the astronomical computing and environmental costs of generative AI could limit its development and use.

Finally, given how wrong economists and other experts have been in the past, it is safe to say that many of today’s predictions about AI technology’s impact on work and worker productivity will prove to be wrong as well. Numbers such as 300 million jobs affected or $4.4 trillion annual boosts to the global economy are eye-catching, yet I think people tend to give them greater credibility than warranted.

Also, “jobs affected” does not mean jobs lost; it could mean jobs augmented or even a transition to new jobs. It is best to use the analyses, such as Goldman’s or McKinsey’s, to spark our imaginations about the plausible scenarios about the future of work and of workers. It’s better, in my view, to then proactively brainstorm the many factors that could affect which one actually comes to pass, look for early warning signs and prepare accordingly.

The history of the future of work has been full of surprises; don’t be shocked if tomorrow’s technologies are equally confounding.

Iconic Burger Franchise Opens New Location in Riverview, FL

LOS ANGELES, June 22, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger and 16 other restaurant concepts, announces Fatburger’s return to the Tampa area. Located in Riverview, FL, the new restaurant marks the first location in the state in approximately 20 years. The opening is just the start of a new wave of locations arriving in Florida for the all-American burger brand -three more locations will be opening in Tampa in the next five years, in addition to 10 locations in Orlando within the next seven years.

“We are heavily invested in growing the Fatburger brand in Florida,” said Jake Berchtold, COO of FAT Brands’ Fast Casual Division. “Making our return to the state after two decades is incredibly rewarding, especially with a committed, experienced partner like Whole Factor Inc., who will be opening 13 more units in Florida. Fans have been eagerly waiting for us and the time has finally come for them to grab their favorite burgers, fries, and milkshakes!”

Ever since the first Fatburger opened in Los Angeles 70 years ago, the chain has been known for its delicious, grilled-to-perfection and cooked to order burgers. Founder Lovie Yancey believed that a big burger with everything on it is a meal in itself; at Fatburger “everything” is not just the usual roster of toppings. Burgers can be customized with everything from bacon and eggs to chili and onion rings. In addition to its famous burgers, the Fatburger menu also includes Fat and Skinny Fries, sweet potato fries, scratch-made onion rings, Impossible™ Burgers, turkeyburgers, hand-breaded crispy chicken sandwiches, and hand-scooped milkshakes made from 100% real ice cream.

To celebrate the new restaurant, the Riverview location will be hosting a grand opening celebration on June 24, with the first 100 customers receiving a free Original Fatburger. Additionally, fans can score a free drink with any purchase throughout the day.

The new Fatburger Riverview restaurant is located at 9950 Upper Alafia Court, Riverview, FL33578. The location is open Sunday through Wednesday, 10 a.m. to 11 p.m., and Thursday through Saturday, 10 a.m. to 2 a.m.

For more information or to find a Fatburger near you, please visit www.fatburger.com.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

AboutFatburger

An all-American, Hollywood favorite, Fatburger is a fast-casual restaurant serving big, juicy, tasty burgers, crafted specifically to each customer’s liking. With a legacy spanning 70 years, Fatburger’s extraordinary quality and taste inspire fierce loyalty amongst its fan base, which includes a number of A-list celebrities and athletes. Featuring a contemporary design and ambiance, Fatburger offers an unparalleled dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1952 – The Last Great Hamburger Stand™. For more information, visit www.fatburger.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings. Forward-looking statements reflect expectations of FAT Brands Inc. (“we”, “our” or the “Company”) concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies, including but not limited to uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

SAN DIEGO, June 22, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced an expansion of its Space Domain Awareness (SDA) network locations into India. Kratos’ SDA network monitors the behavior of space-based radio frequency (RF) signals to identify critical information about satellites in orbit, such as their position, maneuvering, health, proximity to other satellites and more. It is the world’s largest global RF sensor network providing commercially available SDA services in all segments: orbital, link and terrestrial.

Recent strategic installations within the Asia Pacific region including the new India-based facility have increased Kratos’ global satellite tracking coverage by over 30 percent. The sensor network can offer SDA services in real-time for the full 360-degree GEO belt. Growth in the network supports a variety of services for international defense, civilian government and commercial customers, including development efforts from the U.S. Department of Commerce’s NOAA Office of Space Commerce to provide basic space situational awareness safety information and services through the Traffic Coordination System for Space. Kratos was the recipient of one of five commercial data contracts NOAA awarded for GEO space object tracking data last year.

Kratos’ SDA network includes over twenty worldwide sites hosting more than 140 fixed and steerable RF sensors and antennas. It can track and detect space vehicles in the GEO belt with great accuracy (closer than 100m) and in real-time as satellites maneuver frequently. Real-time detection gives the ability to adequately react to spacecraft anomalies or threats to nearby satellites.

Frank Backes, Senior VP of Kratos Federal Space said, “There are over 500 operational satellites in GEO. Many governments and commercial organizations rely on Kratos to enhance and augment their awareness of activity in the space domain. Our new India installation is important to expanding regional coverage.”

The Kratos SDA network supplies intelligence across all areas of the SDA mission through a variety of available services, among them signal characterization, interference mitigation, transmitter geolocation and more. Kratos’ satellite communications experts manage the 24/7 network operations center with coverage of L, S, C, X, and Ku bands.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology company that develops and fields transformative, affordable systems, products, and solutions for United States National Security, our allies, and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems, and technologies rather than slide decks or renderings. Through proven commercial and venture capital-backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions well in advance of the competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR, and Virtual and Augmented Reality Training Systems.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations, and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events, or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

August. Information Services Group announced yesterday that the Company’s Executive Vice President and CFO Bert Alfonso will be retiring in August to devote more time to family matters. Michael A. Sherrick will be succeeding him effective August 7th. Mr. Sherrick will report to chairman and CEO Michael Connors and join the ISG Executive Board.

Michael Sherrick’s Background. Mr. Sherrick provides ISG with over 25 years of financial and operating experience, as his most recent position was from Cognizant Software & Platform Engineering as senior vice president and chief operating officer. Cognizant Technology Solutions Corporation is a global provider of information technology, consulting and business process services, similar to ISG.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

There is Record Government Funding for Energy, According to a New Report

Governments around the globe spent a lot of money on energy research and development last year, according to data presented in the newly released World Energy Investment 2023 report. As presented, government investment in newer technology hit record highs in 2022. The report lays out how unevenly the money is distributed. It’s no surprise that ever-increasing amounts have been allocated to clean energy technologies. Understanding these allocations can be helpful to both the public and private investors involved or seeking to be involved in an industry that is considered a necessity for life.

The report also shows that investment in energy innovation increased. But cautions that a weaker economy may lead to a reduced ability to fund newer ideas, especially those that rely on private capital. This could possibly create a period where the fast pace of innovation, improvement, and efficiency tapers.

In addition to possible increased economic weakness as a risk, countries are turning their focus closer to home. Many are investing in their own clean energy industries. This also risks decelerating the “clean energy” pace – cooperation between countries helps lubricate development, and poorer countries, potentially with a larger carbon footprint per capita, benefit from the assistance of the global community. The report shows an expectation that sharing of information and technology decreased in 2022, but the G7 and G20 are starting to address the barriers to energy R&D investment and the disparities between countries.

The report also shows that investment in clean energy technologies is significantly outpacing spending on fossil fuels, as affordability and security concerns triggered by the global energy crisis strengthen the momentum behind more sustainable options.

Public spending on all energy research and development is estimated to have grown by $US 44 billion or 10% in 2022, with 80% estimated to have been spent to benefit “clean energy.” As far as non-government investments, listed companies in energy-related sectors, demonstrated a similar rise in R&D budgets in 2022, while early-stage venture capital investment into clean energy start-ups reached a new high of $US 6.7 billion. These solid outcomes came despite higher costs of capital and pervading economic uncertainty.

Early-stage equity funding for energy start-ups had its biggest year ever in 2022, with increases in most clean energy technology areas. Funding for start-ups in CO2 capture, energy efficiency, nuclear and renewables nearly doubled or more than doubled from 2021, which was already much higher than the average of the preceding decade. This type of funding supports technology testing and design and plays a critical role in honing good ideas and adapting them to market opportunities.

Growth-stage funding, which requires more capital but funds less risky innovation, rose by only 1% in 2022 and was very weak in Q1 2023, indicating that the value of growth-stage deals for energy start-ups could fall by nearly 60% in 2023. Prevailing macroeconomic conditions have slowed the amount of capital available and raised the cost of scaling up businesses.

The report indicates that early-stage equity funding for energy start-ups is booming, led by clean mobility and renewables, but later-stage funding is eroding.

Take Away

Overall, the World Energy Investment 2023 report shows that there is an increase of 10% in investment in energy innovation. This increase is both in government-related funding and public/private sector investment. The pace has helped many companies blossom and brought ideas to light, but there are some risks that this may have peaked.

Outside of newer energy solutions, fossil fuels represent about 20% of the capital allocated to energy.

Sherrick brings significant tech industry, operational and financial expertise to role

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced that Humberto “Bert” Alfonso, executive vice president and chief financial officer, will retire in August to devote more time to family matters and that Michael A. Sherrick has been named to succeed him, effective August 7.

“I want to express my deepest gratitude to Bert for his valued service to ISG,” said Michael P. Connors, chairman and CEO. “I have known Bert for many years and will miss his wise counsel and contributions to the firm. Everyone here at ISG extends our best wishes to Bert and his family.”

Sherrick joins ISG from Cognizant Technology Solutions Corporation, a $19 billion global provider of information technology, consulting and business process services. He currently serves as senior vice president and chief operating officer of Cognizant Software & Platform Engineering.

At ISG, Sherrick will have global responsibility for finance, investor relations, legal, and mergers and acquisitions. He will report to Connors and join the internal ISG Executive Board.

“I am delighted Michael is joining ISG,” said Connors. “With his unique combination of technology industry knowledge, experience in operations, strategy and finance, and background in investment banking and financial services, Michael will quickly become a key contributor in advancing our ISG NEXT operating model and helping us drive growth and value in the years ahead.”

Sherrick brings more than 25 years of financial and operating experience to ISG. He joined Cognizant in 2016 where he was appointed to a series of roles, including COO of Cognizant Digital Systems and Technology and COO of Cognizant Americas, before assuming his current position.

Prior to joining Cognizant, in 2013 Sherrick co-founded Scoria Capital Partners, where, as a portfolio manager, he managed the firm’s investments in the technology, business services and consumer sectors. Earlier in his career, he held positions with S.A.C. Capital, Morgan Stanley and PwC, among others. Sherrick holds a B.A. degree in economics from Bucknell University and is both a licensed certified public accountant (CPA) and a chartered financial analyst (CFA).

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

{kind=link}