Why the Fed Needs to Gain Trust, Gain Momentum, and Gain More Yards

Monetary policy and its implementation is as much sport as science. Economics is actually a social science, so it relies on human behavior to mimic past behaviors as its prediction guide. But as in sports, victory is difficult if there is distrust in the coach that’s calling the shots (in this case Powell), or if there are people on your side that have reason to work against you, (an example would be Yellen). Consistency in blocking and tackling (doing the right thing) and not giving up, over time, wins games. Knowing what to expect from the opposing team (consumers) wins a healthy economy.

One repeated trait in monetary policy is that there is a lag between implementation (easing or tightening) and a change in economic conditions. It isn’t a short lag, and the impact varies. Since it could take more than a year for a policy change to begin to impact the economy, the Fed usually moves at a slow and measured pace in order to not overdo it.

The slow pace allows policymakers to observe the impact of their moves and change tactics (positions on the playing field) mid-game.

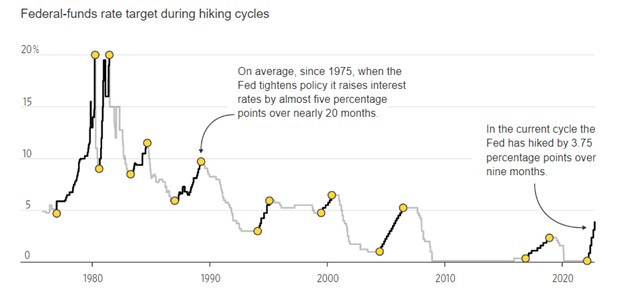

Federal-Funds Rate During Tightening Cycles

Note: From December 2008, midpoint of target range. December 2015 hike excluded from 2016-18 cycle

Source: Federal Reserve

Over the past nine months, we have been in a tightening cycle. During this period, the Fed has raised rates by 3.75%. On average (since 1975), when the Fed has tightened rates, they are notched up by 5.00% over 20 months.

The Fed’s current pace is faster than average. This is because inflation took them by surprise, and rose rapidly. Putting up a strong defense against inflation that has been rampant is necessary to not be shut out and allow the Fed to gain control over the outcome.

Because one has to be able to reflect back more than 40 years to have experienced the Fed raising rates this fast. Many have lost confidence in its ability, and are in their own way working against a winning outcome.

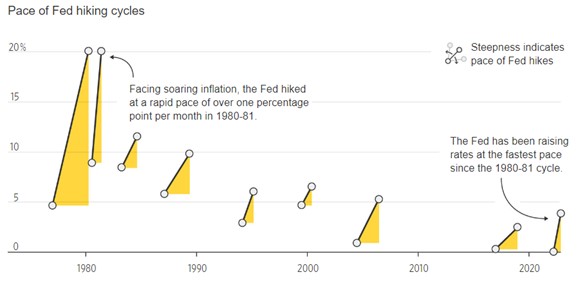

Pace of Fed Hiking Cycles

Note: From December 2008, the midpoint of target range

Source: Federal Reserve

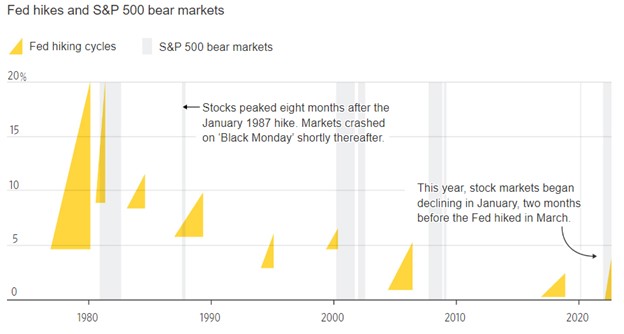

The stock and bond markets move in group anticipation of expected policy moves by the Fed. This has been more pronounced in recent years as the Fed has basically shared its expectations after each meeting, setting up for the next. Higher rates make bonds and bank deposits more attractive. Higher rates also weaken the economy and corporate profits, and that induces investors to move away from stocks and even real estate.

Bonds now offer the highest yields since 2007. The stock market may have anticipated what was to come as it peaked in early January of this year, more than two months before the Fed began hiking in March.

Fed Hikes and S&P 500 Bear Markets

Sources: Federal Reserve; Dow Jones Market Data

Sources: Federal Reserve; Dow Jones Market Data

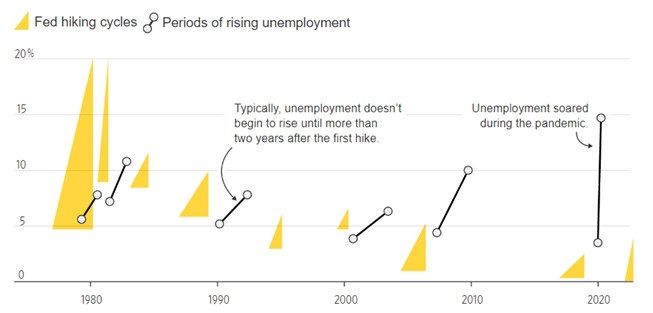

Employment

The Fed is concerned with a wage-price spiral feeding on itself. It likely won’t be satisfied that its tightening has been sufficient until it can be confident that it has avoided a wage-price storm on the economy.

Ideally, this would happen without unemployment rising. Soft landings took place in 1983-84 and 1994-95. But when inflation starts out too high, as it is now, unemployment usually rises notably, and a recession occurs.

Historically, this doesn’t happen until several years after the first increase. This time it is hoped it will be different, since the Fed is playing more aggressively.

Periods of Fed Hiking and Rising Unemployment

Note: The unemployment rate rose to 3.7% in October, up from the pandemic low of 3.5% a month earlier. Sources: Federal Reserve; Labor Department

Inflation

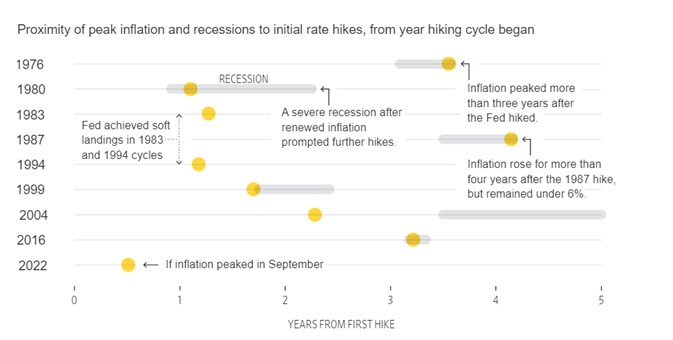

Historically, inflation has only fallen to acceptable levels after unemployment has increased, and long after the first rate increase – the exact timing has varied. If the fall in core inflation (which excludes the volatile food and energy components) between September and October continues, and September proves to be the peak, the time between the first Fed increase and the high point of inflation will be one of the shortest of any Fed hiking cycle.

Often, the break in inflation has been accompanied by a recession. The economy receded in each of the first two quarters and then grew in the third. The changes in the inflation component in Gross Domestic Product may have borrowed from one quarter and have been additive to the next. The fourth quarter reading should help level the growth averages out to see if we were indeed in a shallow recession.

Proximity of Peak Inflation and Recessions to Initial Rate Hikes, from Year Hiking Cycle Began

Note: Inflation refers to core CPI.

Sources: Federal Reserve; Labor Department

Take Away

As in many team sports, once one side gets momentum, they are difficult to stop . The Fed needs to gain the trust of the individual players in the economy in order to be successful. Saying one thing, then doing another, would undermine this trust. So far, despite the Fed originally being wrong about inflation, the Fed has done what it has said it would do. Stock and bond markets, which are a considerable part of the economy, have been slow to understand the Fed’s resolve.

It has been implementing the balance sheet run-off plan and raising rates toward a level it believes would equate to a future 2% inflation rate. Like so many other things in the social sciences, widely held expectations of the future become self-fulfilling.

CHATHAM, N.J., Nov. 22, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals, will deliver an oral presentation at the World Vaccine and Immunotherapy Congress 2022, which will be held in San Diego, Calif., November 28 – December 1, 2022. A copy of the Company’s presentation will be available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com following the conference. Additional meeting information can be found on the World Vaccine and Immunotherapy Congress website here.

Oral Presentation Details

Title:

Showcase 1: Early Development of Smallpox & Monkey Pox Vaccines

Location:

Loews Coronado Bay Resort, San Diego, Calif.

Date:

December 1, 2022

Time:

10:40 a.m. PT (1:40 p.m. ET)

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Railroad Unions and Their Employers at an Impasse: Freight-Halting Strikes are Rare, and this Would be the First in 3 Decades

The prospect of a potentially devastating rail workers strike is looming again.

Fears of a strike in September 2022 prompted the Biden administration to pull out all the stops to get a deal between railroads and the largest unions representing their employees.

That deal hinged on ratification by a majority of members at all 12 of those unions. So far, eight have voted in favor, but four have rejected the terms. If even one continues to reject the deal after further negotiations, it could mean a full-scale freight strike will start as soon as midnight on Dec. 5, 2022. Any work stoppage by conductors and engineers would surely interfere with the delivery of gifts and other items Americans will want to receive in time for the holiday season, along with coal, lumber and other key commodities.

Strikes that obstruct transportation rarely occur in the United States, and the last one involving rail workers happened three decades ago. But when these workers do walk off the job, it can thrash the economy, inconveniencing millions of people and creating a large-scale crisis.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Erik Loomis, Professor of History, University of Rhode Island.

I’m a labor historian who has studied the history of American strikes. I believe that with the U.S. teetering toward at least a mild recession and some of the supply chain disruptions that arose at the outset of the COVID-19 pandemic still wreaking havoc, I don’t think the administration would accept a rail strike for long.

19th Century Rail Strikes

Few, if any, workers have more power over the economy than transportation workers. Their ability to shut down the entire economy has often led to heavy retaliation from the government when they have tried to exercise that power.

In 1877, a small strike against a West Virginia railroad that had cut wages spread. It grew into what became known as the Great Railroad Strike, a general rebellion against railroads that brought thousands of unemployed workers into the streets.

Seventeen years later, in 1894, the American Railway Union went on strike in solidarity with the Pullman Sleeping Car company workers who had gone on strike due to their boss lowering wages while maintaining rents on their company housing.

In both cases, the threat of a railroad strike led the federal government to call out the military to crush the labor actions. Dozens of workers died.

Once those dramatic clashes ended, for more than a century rail unions have played a generally quiet role, preferring to focus on the needs of their members and avoiding most broader social and political questions. Fearful of more rail strikes, the government passed the Railway Labor Act of 1926, which gives Congress the power to intervene before a rail strike starts.

Breaking the Air Traffic Controllers Union

With travel by road and air growing in importance in the 20th century, other transportation workers also engaged in actions that could shut down the economy.

The Professional Air Traffic Controllers Association walked off the job in 1981 after a decade of increased militancy over the stress and conditions of their job. The union had engaged in a series of slowdowns through the 1970s, delaying airplanes and frustrating passengers.

When it went on strike in 1981, the union broke the law, as federal workers do not have the right to strike. That’s when President Ronald Reagan became the first modern U.S. leader to retaliate against striking transportation workers. Two days after warning the striking workers that they would lose their jobs unless they returned to work, Reagan fired more than 11,000 of them. He also banned them from ever being rehired.

In the aftermath of Reagan’s actions, the number of strikes by U.S. workers plummeted. Rail unions engaged in brief strikes in both 1991 and 1992, but Congress used the Railway Labor Act to halt them, ordering workers back on the job and imposing a contract upon the workers.

In 1992, Congress passed another measure that forced a system of arbitration upon railroad workers before a strike – that took power away from workers to strike.

New Era of Labor Militancy

Following decades of decline in the late 20th century, U.S. labor organizing has surged in recent years.

Most notably, unionization attempts at Starbucks and Amazon have led to surprising successes against some of the biggest corporations in the country. Teachers’ unions around the nation have also held a series of successful strikes everywhere from Los Angeles to West Virginia.

United Parcel Service workers, who held the nation’s last major transportation strike, in 1997, may head back to the picket lines after their contract expires in June 2023. UPS workers, members of the Teamsters union, are angry over a two-tiered system that pays newer workers lower wages, and they are also demanding greater overtime protections.

But rail workers, angered by their employers’ refusal to offer sick leave and other concerns, may go on strike first.

Rail companies have greatly reduced the number of people they employ on freight trains as part of their efforts to maximize profits and take advantage of technological progress. They generally keep the size of crews limited to only two per train.

Many companies want to pare back their workforce further, saying that it can be safe to have crews consisting of a single crew member on freight trains. The unions reject this arrangement, saying that lacking a second set of eyes would be a recipe for mistakes, accidents and disasters.

The deal the Biden administration brokered in September would raise annual pay by 24% over several years, raising the average pay for rail workers to $110,000 by 2024. But strikes are often about much more than wages. The companies have also long refused to provide paid sick leave or to stop demanding that their workers have inflexible and unpredictable schedules.

The Biden administration had to cajole the rail companies into offering a single personal day, while workers demanded 15 days of sick leave. Companies had offered zero. The agreement did remove penalties from workers who took unpaid sick or family leave, but this would still leave a group of well-paid workers whose daily lives are filled with stress and fear.

What Lies Ahead

Seeing highly paid workers threaten to take action that would surely compound strains on supply chains at a time when inflation is at a four-decade high may not win rail unions much public support.

A coalition representing hundreds of business groups has called for government intervention to make sure freight trains keep moving, and it’s highly likely that Congress will again impose a decision on workers under the Railway Labor Act. The Biden administration, which has shown significant sympathy to unions, has resisted supporting such a step so far.

No one should expect the military to intervene like it did in the 19th century. But labor law remains tilted toward companies, and I believe that if the government were to compel striking rail workers back on the job, the move might find a receptive audience.

A team of scientists at the Whitehead Institute for Biomedical Research and the Broad Institute of MIT and Harvard has systematically evaluated the functions of over 5,000 essential human genes using a novel, pooled, imaged-based screening method. Their analysis harnesses CRISPR-Cas9 to knock out gene activity and forms a first-of-its-kind resource for understanding and visualizing gene function in a wide range of cellular processes with both spatial and temporal resolution. The team’s findings span over 31 million individual cells and include quantitative data on hundreds of different parameters that enable predictions about how genes work and operate together. The new study appears in the Nov. 7 online issue of the journal Cell.

“For my entire career, I’ve wanted to see what happens in cells when the function of an essential gene is eliminated,” says MIT Professor Iain Cheeseman, who is a senior author of the study and a member of Whitehead Institute. “Now, we can do that, not just for one gene but for every single gene that matters for a human cell dividing in a dish, and it’s enormously powerful. The resource we’ve created will benefit not just our own lab, but labs around the world.”

Systematically disrupting the function of essential genes is not a new concept, but conventional methods have been limited by various factors, including cost, feasibility, and the ability to fully eliminate the activity of essential genes. Cheeseman, who is the Herman and Margaret Sokol Professor of Biology at MIT, and his colleagues collaborated with MIT Associate Professor Paul Blainey and his team at the Broad Institute to define and realize this ambitious joint goal. The Broad Institute researchers have pioneered a new genetic screening technology that marries two approaches — large-scale, pooled, genetic screens using CRISPR-Cas9 and imaging of cells to reveal both quantitative and qualitative differences. Moreover, the method is inexpensive compared to other methods and is practiced using commercially available equipment.

“We are proud to show the incredible resolution of cellular processes that are accessible with low-cost imaging assays in partnership with Iain’s lab at the Whitehead Institute,” says Blainey, a senior author of the study, an associate professor in the Department of Biological Engineering at MIT, a member of the Koch Institute for Integrative Cancer Research at MIT, and a core institute member at the Broad Institute. “And it’s clear that this is just the tip of the iceberg for our approach. The ability to relate genetic perturbations based on even more detailed phenotypic readouts is imperative, and now accessible, for many areas of research going forward.”

Cheeseman adds, “The ability to do pooled cell biological screening just fundamentally changes the game. You have two cells sitting next to each other and so your ability to make statistically significant calculations about whether they are the same or not is just so much higher, and you can discern very small differences.”

Cheeseman, Blainey, lead authors Luke Funk and Kuan-Chung Su, and their colleagues evaluated the functions of 5,072 essential genes in a human cell line. They analyzed four markers across the cells in their screen — DNA; the DNA damage response, a key cellular pathway that detects and responds to damaged DNA; and two important structural proteins, actin and tubulin. In addition to their primary screen, the scientists also conducted a smaller, follow-up screen focused on some 200 genes involved in cell division (also called “mitosis”). The genes were identified in their initial screen as playing a clear role in mitosis but had not been previously associated with the process. These data, which are made available via a companion website, provide a resource for other scientists to investigate the functions of genes they are interested in.

“There’s a huge amount of information that we collected on these cells. For example, for the cells’ nucleus, it is not just how brightly stained it is, but how large is it, how round is it, are the edges smooth or bumpy?” says Cheeseman. “A computer really can extract a wealth of spatial information.”

Flowing from this rich, multi-dimensional data, the scientists’ work provides a kind of cell biological “fingerprint” for each gene analyzed in the screen. Using sophisticated computational clustering strategies, the researchers can compare these fingerprints to each other and construct potential regulatory relationships among genes. Because the team’s data confirms multiple relationships that are already known, it can be used to confidently make predictions about genes whose functions and/or interactions with other genes are unknown.

There are a multitude of notable discoveries to emerge from the researchers’ screening data, including a surprising one related to ion channels. Two genes, AQP7 and ATP1A1, were identified for their roles in mitosis, specifically the proper segregation of chromosomes. These genes encode membrane-bound proteins that transport ions into and out of the cell. “In all the years I’ve been working on mitosis, I never imagined ion channels were involved,” says Cheeseman.

He adds, “We’re really just scratching the surface of what can be unearthed from our data. We hope many others will not only benefit from — but also build upon — this resource.”

This work was supported by grants from the U.S. National Institutes of Health as well as support from the Gordon and Betty Moore Foundation, a National Defense Science and Engineering Graduate Fellowship, and a Natural Sciences and Engineering Research Council Fellowship.

A team of scientists at the Whitehead Institute for Biomedical Research and the Broad Institute of MIT and Harvard has systematically evaluated the functions of over 5,000 essential human genes using a novel, pooled, imaged-based screening method. Their analysis harnesses CRISPR-Cas9 to knock out gene activity and forms a first-of-its-kind resource for understanding and visualizing gene function in a wide range of cellular processes with both spatial and temporal resolution. The team’s findings span over 31 million individual cells and include quantitative data on hundreds of different parameters that enable predictions about how genes work and operate together. The new study appears in the Nov. 7 online issue of the journal Cell.

“For my entire career, I’ve wanted to see what happens in cells when the function of an essential gene is eliminated,” says MIT Professor Iain Cheeseman, who is a senior author of the study and a member of Whitehead Institute. “Now, we can do that, not just for one gene but for every single gene that matters for a human cell dividing in a dish, and it’s enormously powerful. The resource we’ve created will benefit not just our own lab, but labs around the world.”

Systematically disrupting the function of essential genes is not a new concept, but conventional methods have been limited by various factors, including cost, feasibility, and the ability to fully eliminate the activity of essential genes. Cheeseman, who is the Herman and Margaret Sokol Professor of Biology at MIT, and his colleagues collaborated with MIT Associate Professor Paul Blainey and his team at the Broad Institute to define and realize this ambitious joint goal. The Broad Institute researchers have pioneered a new genetic screening technology that marries two approaches — large-scale, pooled, genetic screens using CRISPR-Cas9 and imaging of cells to reveal both quantitative and qualitative differences. Moreover, the method is inexpensive compared to other methods and is practiced using commercially available equipment.

“We are proud to show the incredible resolution of cellular processes that are accessible with low-cost imaging assays in partnership with Iain’s lab at the Whitehead Institute,” says Blainey, a senior author of the study, an associate professor in the Department of Biological Engineering at MIT, a member of the Koch Institute for Integrative Cancer Research at MIT, and a core institute member at the Broad Institute. “And it’s clear that this is just the tip of the iceberg for our approach. The ability to relate genetic perturbations based on even more detailed phenotypic readouts is imperative, and now accessible, for many areas of research going forward.”

Cheeseman adds, “The ability to do pooled cell biological screening just fundamentally changes the game. You have two cells sitting next to each other and so your ability to make statistically significant calculations about whether they are the same or not is just so much higher, and you can discern very small differences.”

Cheeseman, Blainey, lead authors Luke Funk and Kuan-Chung Su, and their colleagues evaluated the functions of 5,072 essential genes in a human cell line. They analyzed four markers across the cells in their screen — DNA; the DNA damage response, a key cellular pathway that detects and responds to damaged DNA; and two important structural proteins, actin and tubulin. In addition to their primary screen, the scientists also conducted a smaller, follow-up screen focused on some 200 genes involved in cell division (also called “mitosis”). The genes were identified in their initial screen as playing a clear role in mitosis but had not been previously associated with the process. These data, which are made available via a companion website, provide a resource for other scientists to investigate the functions of genes they are interested in.

“There’s a huge amount of information that we collected on these cells. For example, for the cells’ nucleus, it is not just how brightly stained it is, but how large is it, how round is it, are the edges smooth or bumpy?” says Cheeseman. “A computer really can extract a wealth of spatial information.”

Flowing from this rich, multi-dimensional data, the scientists’ work provides a kind of cell biological “fingerprint” for each gene analyzed in the screen. Using sophisticated computational clustering strategies, the researchers can compare these fingerprints to each other and construct potential regulatory relationships among genes. Because the team’s data confirms multiple relationships that are already known, it can be used to confidently make predictions about genes whose functions and/or interactions with other genes are unknown.

There are a multitude of notable discoveries to emerge from the researchers’ screening data, including a surprising one related to ion channels. Two genes, AQP7 and ATP1A1, were identified for their roles in mitosis, specifically the proper segregation of chromosomes. These genes encode membrane-bound proteins that transport ions into and out of the cell. “In all the years I’ve been working on mitosis, I never imagined ion channels were involved,” says Cheeseman.

He adds, “We’re really just scratching the surface of what can be unearthed from our data. We hope many others will not only benefit from — but also build upon — this resource.”

This work was supported by grants from the U.S. National Institutes of Health as well as support from the Gordon and Betty Moore Foundation, a National Defense Science and Engineering Graduate Fellowship, and a Natural Sciences and Engineering Research Council Fellowship.

Will Global Rate Hikes Set Off a Global Debt Bomb?

The higher levels of risky corporate debt issuance over the past few year will need to be refinanced between 2023 and 2025, In numbers terms, there will be over $10 trillion of the riskiest debt at much higher interest rates and with less liquidity. In addition to domestic high yield issuance, the majority of the major European economies have issued negative-yielding debt over the past three years and must now refinance at significantly higher rates. In 2020–21. the annual increase in the US money supply (M2) was 27 percent, more than 2.5 times higher than the quantitative easing peak of 2009 and the highest level since 1960. Negative yielding bonds, an economic anomaly that should have set off alarm bells as an example of a bubble worse than the “subprime” bubble, amounted to over $12 trillion. Even if refinancing occurs smoothly but at higher costs, the impact on new credit and innovation will be enormous, and the crowding out effect of government debt absorbing the majority of liquidity and the zombification of the already indebted will result in weaker growth and decreased productivity in the future.

Raising interest rates is a necessary but insufficient measure to combat inflation. To reduce inflation to 2 percent, central banks must significantly reduce their balance sheets, which has not yet occurred in local currency, and governments must reduce spending, which is highly unlikely.

The most challenging obstacle is also the accumulation of debt.

The so-called expansionary policies have not been an instrument for reducing debt, but rather for increasing it. In the second quarter of 2022, according to the Institute of International Finance (IIF), the global debt-to-GDP ratio will approach 350 percent of GDP. IIF anticipates that the global debt-to-GDP ratio will reach 352 percent by the end of 2022.

Global issuances of high-yield debt have slowed but remain elevated. According to the IMF, the total issuance of European and American high-yield bonds reached a record high of $1,6 trillion in 2021, as businesses and investors capitalized on still low interest rates and high liquidity. According to the IMF, high-yield bond issuances in the United States and Europe will reach $700 billion in 2022, similar to 2008 levels. All of the risky debt accumulated over the past few years will need to be refinanced between 2023 and 2025, requiring the refinancing of over $10 trillion of the riskiest debt at much higher interest rates and with less liquidity.

Moody’s estimates that United States corporate debt maturities will total $785 billion in 2023 and $800 billion in 2024. This increases the maturities of the Federal government. The United States has $31 trillion in outstanding debt with a five-year average maturity, resulting in $5 trillion in refinancing needs during fiscal 2023 and a $2 trillion budget deficit. Knowing that the federal debt of the United States will be refinanced increases the risk of crowding out and liquidity stress on the debt market.

According to The Economist, the cumulative interest bill for the United States between 2023 and 2027 should be less than 3 percent of GDP, which appears manageable. However, as a result of the current path of rate hikes, this number has increased, which exacerbates an already unsustainable fiscal problem.

If you think the problem in the United States is significant, the situation in the eurozone is even worse. Governments in the euro area are accustomed to negative nominal and real interest rates. The majority of the major European economies have issued negative-yielding debt over the past three years and must now refinance at significantly higher rates. France and Italy have longer average debt maturities than the United States, but their debt and growing structural deficits are also greater. Morgan Stanley estimates that, over the next two years, the major economies of the eurozone will require a total of $3 trillion in refinancing.

Although at higher rates, governments will refinance their debt. What will become of businesses and families? If quantitative tightening is added to the liquidity gap, a credit crunch is likely to ensue. However, the issue is not rate hikes but excessive debt accumulation complacency.

Explaining to citizens that negative real interest rates are an anomaly that should never have been implemented is challenging. Families may be concerned about the possibility of a higher mortgage payment, but they are oblivious to the fact that house prices have skyrocketed due to risk accumulation caused by excessively low interest rates.

The magnitude of the monetary insanity since 2008 is enormous, but the glut of 2020 was unprecedented. Between 2009 and 2018, we were repeatedly informed that there was no inflation, despite the massive asset inflation and the unjustified rise in financial sector valuations. This is inflation, massive inflation. It was not only an overvaluation of financial assets, but also a price increase for irreplaceable goods and services. The FAO food index reached record highs in 2018, as did the housing, health, education, and insurance indices. Those who argued that printing money without control did not cause inflation, however, continued to believe that nothing was wrong until 2020, when they broke every rule.

In 2020–21, the annual increase in the US money supply (M2) was 27 percent, more than 2.5 times higher than the quantitative easing peak of 2009 and the highest level since 1960. Negative yielding bonds, an economic anomaly that should have set off alarm bells as an example of a bubble worse than the “subprime” bubble, amounted to over $12 trillion. But statism was pleased because government bonds experienced a bubble. Statism always warns of bubbles in everything except that which causes the government’s size to expand.

In the eurozone, the increase in the money supply was the greatest in its history, nearly three times the Draghi-era peak. Today, the annualized rate is greater than 6 percent, remaining above Draghi’s “bazooka.” All of this unprecedented monetary excess during an economic shutdown was used to stimulate public spending, which continued after the economy reopened … And inflation skyrocketed. However, according to Lagarde, inflation appeared “out of nowhere.”

No, inflation is not caused by commodities, war, or “disruptions in the supply chain.” Wars are deflationary if the money supply remains constant. Several times between 2008 and 2018, the value of commodities rose sharply, but they do not cause all prices to rise simultaneously. If the amount of currency issued remains unchanged, supply chain issues do not affect all prices. If the money supply remains the same, core inflation does not rise to levels not seen in thirty years.

All of the excess of unproductive debt issued during a period of complacency will exacerbate the problem in 2023 and 2024. Even if refinancing occurs smoothly but at higher costs, the impact on new credit and innovation will be enormous, and the crowding out effect of government debt absorbing the majority of liquidity and the zombification of the already indebted will result in weaker growth and decreased productivity in the future.

Europe May Be Saved from the December Planned Oil Embargo in a Nick of Time

On December 5, the European Union plans to cap oil prices at levels where EU nations would then be permitted to buy oil from Russia. This would significantly reduce the petroleum supply of the region going into winter. The day before this goes into effect, (December 4), OPEC+ will meet to set output levels. Saudi Arabia and other OPEC producers are expected to discuss an output increase, according to emissaries from the group. The 11th hour move could keep much needed petroleum flowing into the region at a time that weather-related demand would naturally grow, holiday driving would be expected to increase, and war-related strategies would have reduced oil coming out of Russia. While western news has verified their sources as actual delegates of OPEC+, the Saudi’s are now saying that their plans are always secret.

About the New Expectations

A production increase of up to 500,000 barrels a day is now expected to be the discussion at OPEC+’s December 4 meeting, delegates said. Any output increase would mark a partial reversal of a controversial decision last month to cut production by 2 million barrels a day. This was agreed upon at the most recent meeting of the Organization of the Petroleum Exporting Countries and their Russia-led allies, a group known collectively as OPEC+.

The White House had said the production cut undermined global efforts to negatively impact Russia’s war in Ukraine. Saudi-U.S. relations have hit a low point over oil-production disagreements this year; if the December 4 OPEC+ meeting leads to increased oil, this may warm the cooled Saudi-U.S. relations.

About the EU December 5th Plan

The European Union has agreed to stop all oil imports from Russia on December 5. The plan is to cap the prices at which EU nations would buy oil from Russia, that price is expected to be near $60 per barrel. Russia has reacted by increasing exports to Asia, but the price cap is expected to reduce its exports and lower total supply by up to one million barrels per day.

About the OPEC+ December 4th Expectations

A production increase of up to 500,000 barrels a day is now under discussion for OPEC+’s December 4 meeting, emissaries said.

Any increase in OPEC+ output will partially undo the decision made at OPEC+’s its last monthly meeting. In October the cartel voted to cut production by 2 million barrels per day. The decision by the Organization of the Petroleum Exporting Countries and their Russia-led allies, (OPEC+) was a disappointment to the White House and NATO nations that saw reduced production as strengthening Russia’s ability to fund its war with higher priced exports.

Under normal production discussions by OPEC+ production increases, with oil prices falling more than 10% since the first week of November, one might not expect an increase. Brent crude traded at about $87 a barrel on Monday, while WTI, the U.S. benchmark, fell below $80 a barrel for the first time since September. Production increases could cause prices to fall further.

Emissaries say, a production increase would be to respond to expectations that oil consumption will rise in the winter. Oil demand is expected to increase by 1.69 million barrels a day to 101.3 million barrels a day in the first quarter next year, compared with the average level in 2022.

OPEC and its allies say they have been carefully studying the G-7 plans to impose a price cap on Russian oil, conceding privately that they see any such move by crude consumers to control the market as a threat. Russia has said it wouldn’t sell oil to any country participating in the price cap, potentially resulting in another effective production cut from Moscow—one of the world’s top three oil producers.

Raising oil production ahead of the December 5 EU embargo would give the Saudis another argument that they are acting in their own interests, and not is support of Russia’s.

Talk of the production increase emerged after the Biden administration told a federal court judge that Saudi Crown Prince Mohammed bin Salman should have sovereign immunity from a U.S. federal lawsuit related to the killing of Saudi journalist Jamal Khashoggi. The immunity decision is seen by some as a concession to Prince Mohammed, and heighten his standing as the kingdom’s de facto ruler. The move comes after the Biden administration tried for months to isolate him.

Another factor that helps account for the timing of OPEC+’s discussion to raise output is the two large OPEC members, Iraq and the United Arab Emirates that want to pump more oil. Both countries are pushing the oil-producing nations to allow them a higher daily-production ceiling, which would lead to more oil produced globally.

Saudi officials late Monday denied reports the kingdom is reversing course and helping the West with added production.

Chief Medical Officer, Dr. Lauren V. Wood, to present on the development of targeted immunotherapies for solid tumors based on the Versamune® platform

Dr. Siva Gandhapudi, Director of Immunology Product Development, to present on development of a universal flu vaccine based on the Infectimune™ platform

FLORHAM PARK, N.J., Nov. 21, 2022 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced two executives will be giving presentations at the World Vaccine & Immunotherapy Congress, which will take place from November 28 through December 1, 2022, in San Diego.

PDS Biotech speakers at the conference include:

Speaker

Time

Subject

Dr. Lauren V. Wood, Chief Medical Officer

Tuesday, Nov. 29, 4:50 p.m. Pacific Time

Development of targeted immunotherapies for solid tumors based on the Versamune® platform

Dr. Siva Gandhapudi, Director of Immunology Product Development

Wednesday, Nov. 30, 2:30 p.m. Pacific Time

Development of a universal flu vaccine based on the InfectimuneTM platform

More than 800 attendees are expected to attend the World Vaccine & Immunotherapy Congress to examine challenges around scientific, commercial, public health and policy issues in manufacturing, clinical trials, regulation, immune profiling, biomarkers, platform technologies, and additional topics.

“We welcome the opportunity to highlight the Versamune® and Infectimune™ platforms and their potential to address significant unmet medical needs to the biotechnology and scientific community,” said Dr. Frank Bedu-Addo, PDS Biotech President and CEO. “We are looking forward to advancing our product development in both oncology and infectious disease, ultimately to improve patient care.”

About Versamune®

Current immunotherapies have demonstrated an ability to treat certain cancers, but limitations with their effectiveness persist. Versamune® is a novel investigational T cell activating platform designed to stimulate a precise immune system response to cancer-specific proteins. PDS Biotech is advancing multiple Versamune® based clinical and pre-clinical programs with its lead clinical candidate – PDS0101 – targeting HPV-positive cancers.

About InfectimuneTM

Infectimune™ is a novel proprietary investigational T cell immune activating platform technology designed to train the immune system to better protect against disease. The Infectimune™ platform stimulates the immune system to recognize the pathogen and induce potent killer T cell and memory T cell response for long-term protection safely with no clinically relevant toxicities.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune® and Infectimune™ T cell-activating technology platforms. We believe our targeted Versamune® based candidates have the potential to overcome the limitations of current immunotherapy by inducing large quantities of high-quality, potent polyfunctional tumor specific CD4+ helper and CD8+ killer T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the potential to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV-positive cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0202 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0202 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control, including unforeseen circumstances or other disruptions to normal business operations arising from or related to COVID-19. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology.

CHATHAM, N.J., Nov. 21, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals, will deliver an oral presentation at the World Antiviral Congress 2022, which will be held in San Diego, Calif., November 28 – December 1, 2022. A copy of the presentation will be available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com following the conference. Additional meeting information can be found on the World Antiviral Congress website here.

Oral Presentation Details

Title:

Development of fully human monoclonal antibodies against SARS-CoV2 using peripheral B-cells from COVID-19 survivors

Location:

Loews Coronado Bay Resort, San Diego, Calif.

Date:

November 30, 2022

Time:

12:40 p.m. PT (3:40 p.m. ET)

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter financial results. Sierra Metals reported an adjusted net loss of $10.7 million or $(0.07) per share, compared to an adjusted net loss of $3.1 million or $(0.02) per share during the prior year period. Third quarter revenue from metals payable declined 36% to $38.8 million due to a decrease in metal sales and a decline in average realized prices for all metals. Adjusted EBITDA declined to $(3.9) million compared to $17.4 million during the third quarter of 2021 due mainly to lower sales and commodity prices. Third quarter production was negatively impacted, among other things, by a mudslide at the Yauricocha mine and flooding at the Bolivar mine.

Updating estimates. We have lowered our full year 2022 EPS and EBITDA estimates to $(0.13) and $18.0 million from $(0.08) and $29.9 million, respectively. Additionally, we have reduced our 2023 EPS and EBITDA estimates to $0.07 and $63.2 million from $0.12 and $76.1 million. Our estimates reflect lower production levels for both Yauricocha and Bolivar.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 results. The company reported revenue of $1.2 million and an adj. EBITDA loss of $6.4 million in the quarter, missing our estimates by 57% and 19%, respectively. Management attributed the lower-than-expected revenue to weakness in retail, digital and mobile game sales. Figure #1 Q3 Variance illustrates how the quarter compared with our estimates.

Financial position. As of October 31, the company had $1.8 million in cash, with a monthly burn rate of approximately $1.5 million. Management noted that cash burn for November would be higher, in the range of $1.5 million to $2.0 million, due to the production of game cards for the recent release of NASCAR Rivals.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Dramatic Collapse of the Cryptocurrency Exchange FTX Contains Lessons for Investors but Won’t Affect Most People

In the fast-paced world of cryptocurrency, vast sums of money can be made or lost in the blink of an eye. In early November 2022, the second-largest cryptocurrency exchange, FTX, was valued at more than US$30 billion. By Nov. 14, FTX was in bankruptcy proceedings along with more than 100 companies connected to it. D. Brian Blank and Brandy Hadley are professors who study finance, investing and fintech. They explain how and why this incredible collapse happened, what effect it might have on the traditional financial sector and whether you need to care if you don’t own any cryptocurrency.

What Happened?

In 2019, Sam Bankman-Fried founded FTX, a company that ran one of the largest cryptocurrency exchanges.

FTX is where many crypto investors trade and hold their cryptocurrency, similar to the New York Stock Exchange for stocks. Bankman-Fried is also the founder of Alameda Research, a hedge fund that trades and invests in cryptocurrencies and crypto companies.

Sam Bankman-Fried founded both FTX and the investment firm Alameda Research. News sources have reported some less-than-responsible financial dealings between the two companies. Image via The Conversation.

Within the traditional financial sector, these two companies would be separate firms entirely or at least have divisions and firewalls in place between them. But in early November 2022, news outlets reported that a significant proportion of Alameda’s assets were a type of cryptocurrency released by FTX itself.

A few days later, news broke that FTX had allegedly been loaning customer assets to Alameda for risky trades without the consent of the customers and also issuing its own FTX cryptocurrency for Alameda to use as collateral. As a result, criminal and regulatory investigators began scrutinizing FTX for potentially violating securities law.

These two pieces of news basically led to a bank run on FTX.

Large crypto investors, like FTX’s competitor Binance, as well as individuals, began to sell off cryptocurrency held on FTX’s exchange. FTX quickly lost its ability to meet customer withdrawals and halted trading. On Nov. 14, FTX was also hit by an apparent insider hack and lost $600 million worth of cryptocurrency.

That same day, FTX, Alameda Research and 130 other affiliated companies founded by Bankman-Fried filed for bankruptcy. This action may leave more than a million suppliers, employees and investors who bought cryptocurrencies through the exchange or invested in these companies with no way to get their money back.

Among the groups and individuals who held currency on the FTX platform were many of the normal players in the crypto world, but a number of more traditional investment firms also held assets within FTX. Sequoia Capital, a venture capital firm, as well as the Ontario Teacher’s Pension, are estimated to have held millions of dollars of their investment portfolios in ownership stake of FTX. They have both already written off these investments with FTX as lost.

In traditional markets, corporations generally limit the risk they expose themselves to by maintaining liquidity and solvency. Liquidity is the ability of a firm to sell assets quickly without those assets losing much value. Solvency is the idea that a company’s assets are worth more than what that company owes to debtors and customers.

But the crypto world has generally operated with much less caution than the traditional financial sector, and FTX is no exception. About two-thirds of the money that FTX owed to the people who held cryptocurrency on its exchange – roughly $11.3 billion of $16 billion owed – was backed by illiquid coins created by FTX. FTX was taking its customers’ money, giving it to Alameda to make risky investments and then creating its own currency, known as FTT, as a replacement – cryptocurrency that it was unable to sell at a high enough price when it needed to.

In addition, nearly 40% of Alameda’s assets were in FTX’s own cryptocurrency – and remember, both companies were founded by the same person.

This all came to a head when investors decided to sell their coins on the exchange. FTX did not have enough liquid assets to meet those demands. This, in turn, drove the value of FTT from over $26 a coin at the beginning of November to under $2 by Nov. 13. By this point, FTX owed more money to its customers than it was worth.

In regulated exchanges, investing with customer funds is illegal. Additionally, auditors validate financial statements, and firms must publish the amount of money they hold in reserve that is available to fund customer withdrawals. And even if things go wrong, the Securities Investor Protection Corporation – or SIPC – protects depositors against the loss of investments from an exchange failure or financially troubled brokerage firm. None of these guardrails are in place within the crypto world.

Why is this a Big Deal in Crypto?

As a result of this meltdown, the company Binance is now considering creating an industry recovery fund – akin to a private version of SIPC insurance – to avoid future failures of crypto exchanges.

But while the collapse of FTX and Alameda – valued at more than $30 billion and now essentially worth nothing – is dramatic, the bigger implication is simply the potential lost trust in crypto. Bank runs are rare in traditional financial institutions, but they are increasingly common in the crypto space. Given that Bankman-Fried and FTX were seen as some of the biggest, most trusted figures in crypto, these events may lead more investors to think twice about putting money in crypto.

If I Don’t Own Crypto, Should I Care?

Though investment in cryptocurrencies has grown rapidly, the entire crypto market – valued at over $3 trillion at its peak – is much smaller than the $120 trillion traditional stock market.

While investors and regulators are still evaluating the consequences of this fall, the impact on any person who doesn’t personally own crypto will be minuscule. It is true that many larger investment funds, like BlackRock and the Ontario Teachers Pension, held investments in FTX, but the estimated $95 million the Ontario Teachers Pension lost through the collapse of FTX is just 0.05% of the entire fund’s investments.

The takeaway for most individuals is not to invest in unregulated markets without understanding the risks. In high-risk environments like crypto, it’s possible to lose everything – a lesson investors in FTX are learning the hard way.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of D. Brian Blank, Assistant Professor of Finance, Mississippi State University and Brandy Hadley, Associate Professor of Finance and the David A. Thompson Professor in Applied Investments, Appalachian State University

Will the Fed Minutes on Wednesday Suggest the Fed Will Finally Back Off?

Fed Chair Jerome Powell said in a press conference after the last FOMC meeting that the committee has “some ways to go” on easing surging prices. Investors wondered what “some ways to go” equate to in terms of basis points. The markets will get more insight this week as minutes from that meeting will be released. This may be the most market-moving highlight of the week, but the stock and bond markets are closed on Thursday, November 24, and stock markets close at 2 PM EST on Friday, shortening this week’s cumulative trading sessions more than any other week during the year.

What’s on Tap for investors:

Monday 11/21

8:30 AM EST, Chicago Fed National Activity Index. The index is expected to be .10% with a three-month average of .17%. vs .10% last period. CFNAI is a monthly index that tracks overall economic activity and inflationary pressures. It’s a weighted average of 85 existing monthly indicators of national economic activity. Its benchmark average, by creation, is designed to be 0.00% and a standard deviation of one. Since economic activity tends toward trend growth over time, a positive index reading corresponds to growth above trend and a negative index reading corresponds to growth below trend.

Tuesday 11/22

10:00 AM EST, Richmond Fed’s Manufacturing Index had been trending lower with a reading of negative 10 last month. The consensus this week is for negative 1, which would be less negative than it has been.

11:00 AM EST, Loretta Mester, President Cleveland Fed, will speak. Last week she showed her continued hawkish stance saying the Fed is “just beginning to move into restrictive territory.” This suggests that it is Mester’s position that rates will have to be led much higher.

1:00 PM EST, Money Supply is expected to have shrunk $128 billion.

Wednesday 11/23

7:00 AM EST, Mortgage Applications. The purchase applications index measures applications at mortgage lenders. This is a leading indicator for single-family home sales and housing construction.

8:30 AM EST, Durable Goods Orders are seen as rising 0.3 percent in October following a 0.4 percent rise in September. Ex-transportation orders are seen inching 0.1 percent higher with core capital goods orders, which fell back in September by 0.4 percent, rising 0.2 percent.

8:30 AM EST, Jobless Claims for the prior week are expected to come in at 225,000 versus a steady 222,000 two weeks ago.

10 AM EST, New Home Sales have declined the last three months in a row. It is expected to come in at a 574,000 annualized rate in October versus 603,000 in September.

10 AM EST, Consumer Sentiment is expected to show a deeply depressed 55.0 versus 54.7 at mid-November. Consumer spending accounts for more than two-thirds of the economy, more during the holiday weeks. So the markets wantt to have a finger on their overall mood.

10:30 AM EST, EIA Petroleum Status Report. The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products, this has been a big focus for investors because of its implications for prices.

12:00 PM EST, EIA Natural Gas Report. The Energy Information Administration (EIA) provides weekly information on natural gas inventories in the U.S., whether produced here or abroad.

2:00 PM EST, FOMC Minutes for November meeting. With just two more hours to trade before the Thanksgiving break, the FOMC minutes will be digested and reacted on quickly. It is not unusual to get a whipsaw market with such important releases in such a compressed time period.

Thursday 11/24

Image Credit: Marco Verch (Flickr)

Friday 11/25

The day after Thanksgiving is Black Friday in the U.S. It is named this because it is the day most retailers are consireded to have broken through to turn a profit. Market watchers view this day of intense shopping as a bellwether for the retail sector and overall consumer confidence. Recent retail earnings reports have been more mixed than usual with Target disappointing last week.

What Else

The last full week of November leads us to the last full month of 2022. There is still a strong push and pull between bulls and bear’s as the year comes to a close. The overall market is much cheaper than it began the year. At times like this, it is important to realize that there are always individual companies attaining above-average, positive performance. Channelchek is an excellent resource to explore and discover companies in the small and microcap space that are less reported on than other stocks that are more likely to follow market direction. Learn more.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex Petroleum decided to postpone its listing on the NYSE American due to market conditions. The company also indicated that a registration statement with the SEC has not yet become effective. The shares of Permex (now trading as OILCD) have fallen approximately 50% following the announcement of a 2 million (later raised to 3.6 million) common share offering. The offering was to be completed in conjunction with the move to the NYSE. Prior to the uplisting and registration announcement, Permex completed a 1-60 reverse stock split.

We are adjusting our estimates and price target to reflect a lower share count associated with the reverse stock split. Our new price target is now $40 per share versus our pre-stock split price target of $4 per share. We have increased our price target by less than a 60-1 multiple due to the following reasons. We have increased the discount rate we are using for the company to reflect what we view as increased financing risk. In addition, we have slowed the assumed pace of new well drilling to one every other quarter instead of one per quarter. We also believe the company will focus primarily on less expensive, but less productive, vertical wells until it starts generating cash flow to fund drilling.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.