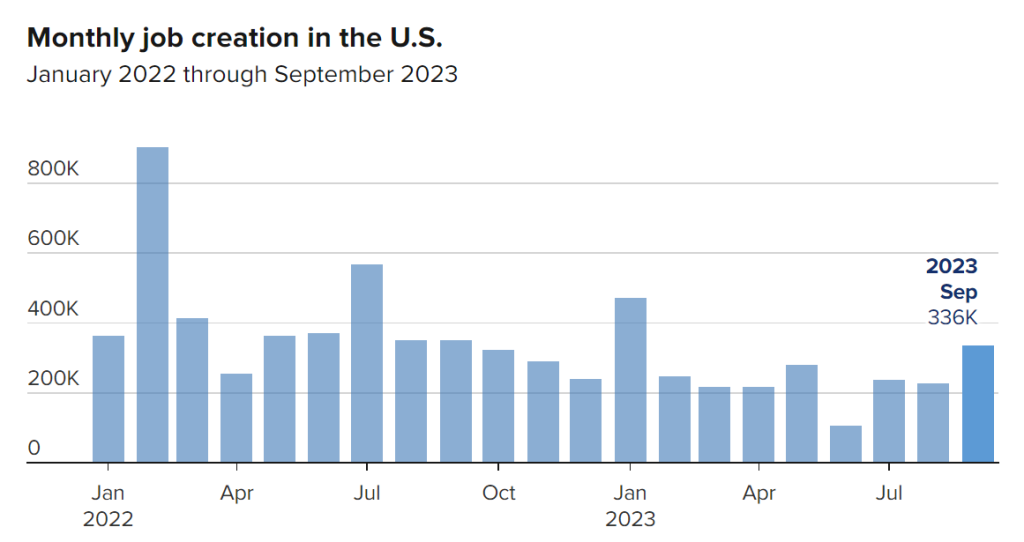

The red-hot U.S. labor market showed no signs of cooling in March, with employers adding a whopping 303,000 new jobs last month while the unemployment rate fell to 3.8%. The much stronger-than-expected employment gains provide further evidence of the economy’s resilience even in the face of the Federal Reserve’s aggressive interest rate hikes over the past year.

The blockbuster jobs number reported by the Bureau of Labor Statistics on Friday handily exceeded economists’ consensus estimate of 214,000. It marked a sizeable acceleration from February’s solid 207,000 job additions and landed squarely above the 203,000 average over the past year.

Details within the report were equally impressive. The labor force participation rate ticked up to 62.7% as more Americans entered the workforce, while average hourly earnings rose a healthy 0.3% over the previous month. On an annualized basis, wage growth cooled slightly to 4.1% but remains elevated compared to pre-pandemic norms.

Investors closely watch employment costs for signs that stubbornly high inflation may be becoming entrenched. If wage pressures remain too hot, it could force the Fed to keep interest rates restrictive for longer as inflation proves difficult to tame.

“The March employment report definitively shows inflation remains a threat, and the Fed’s work is not done yet,” said EconomicGrizzly chief economist Jeremy Hill. “Cooler wage gains are a step in the right direction, but the central bank remains well behind the curve when it comes to getting inflation under control.”

From a markets perspective, the report prompted traders to dial back expectations for an imminent Fed rate cut. Prior to the data, traders were pricing in around a 60% chance of the first rate reduction coming as soon as June. However, those odds fell to 55% following the jobs numbers, signaling many now see cuts being pushed back to late 2024.

Fed chair Jerome Powell sounded relatively hawkish in comments earlier this week, referring to the labor market as “strong but rebalancing” and indicating more progress is needed on inflation before contemplating rate cuts. While the central bank welcomes a gradual softening of labor conditions, an outright collapse is viewed as unnecessarily painful for the economy.

If job gains stay heated but wage growth continues moderating, the Fed may feel emboldened to start cutting rates in the second half of 2024. A resilient labor market accompanied by cooler inflation pressures is the so-called “soft landing” scenario policymakers are aiming for as they attempt to tame inflation without tipping the economy into recession.

Sector details showed broad-based strength in March’s employment figures. Healthcare led the way by adding 72,000 positions, followed by 71,000 new government jobs. The construction industry saw an encouraging 39,000 hires, double its average monthly pace over the past year. Leisure & hospitality and retail also posted healthy employment increases.

The labor market’s persistent strength comes even as overall economic growth appears to be downshifting. GDP rose just 0.9% on an annualized basis in the final quarter of 2023 after expanding 2.6% in Q3, indicating deceleration amid the Fed’s rate hiking campaign.

While consumers have remained largely resilient thanks to a robust labor market, business investment has taken a hit from higher borrowing costs. This divergence could ultimately lead to payroll reductions in corporate America should profits come under further pressure.

For now, however, the U.S. labor force is flexing its muscles even as economic storm clouds gather. How long employment can defy the Fed’s rate hikes remains to be seen, but March’s outsized jobs report should keep policymakers on a hawkish path over the next few months.