Gray Television is a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets in the United States. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station. We also own video program companies Raycom Sports, Tupelo Honey, PowerNation Studios and Third Rail Studios.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Misses Q3 expectations. Q3 revenue of $950.0 million was below our $1.02 billion estimate, with the largest variance due to lower than expected Political advertising and weaker core advertising. Political was $173.0 million versus our $200.0 million estimate. Q3 adj. EBITDA of $322.0 million was lower than our $396.0 million estimate. Figure #1 Q3 Results illustrate our estimates versus reported results.

Disappointing Political outlook. Management indicated that Q4 Political advertising will be in the range of $248 million to $253 million and in the range of $495 million to $500 million for the full year 2024, well below our $380 million and $652 million estimate, respectively. The shortfall appears to be due to a shift in spending for Senate and House races into more competitive markets which were outside of Gray’s footprint.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATLANTA, Nov. 08, 2024 (GLOBE NEWSWIRE) — Gray Television, Inc. (“Gray,” “Gray Media,” “we,” “us” or “our”) (NYSE: GTN) today announced a strong third quarter ended September 30, 2024. Gray also projected full-year 2024 political advertising revenue of $500 million, as well as full-year 2024 Net Debt reduction of $500 million.

SUMMARY OF THIRD QUARTER RESULTS

OPERATING HIGHLIGHTS:

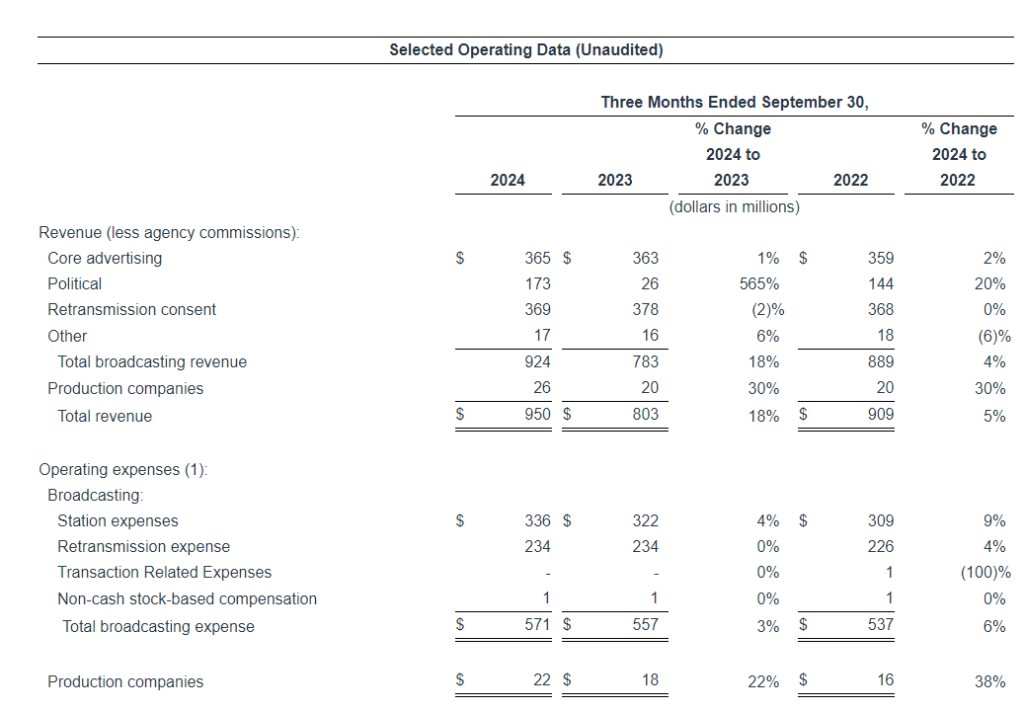

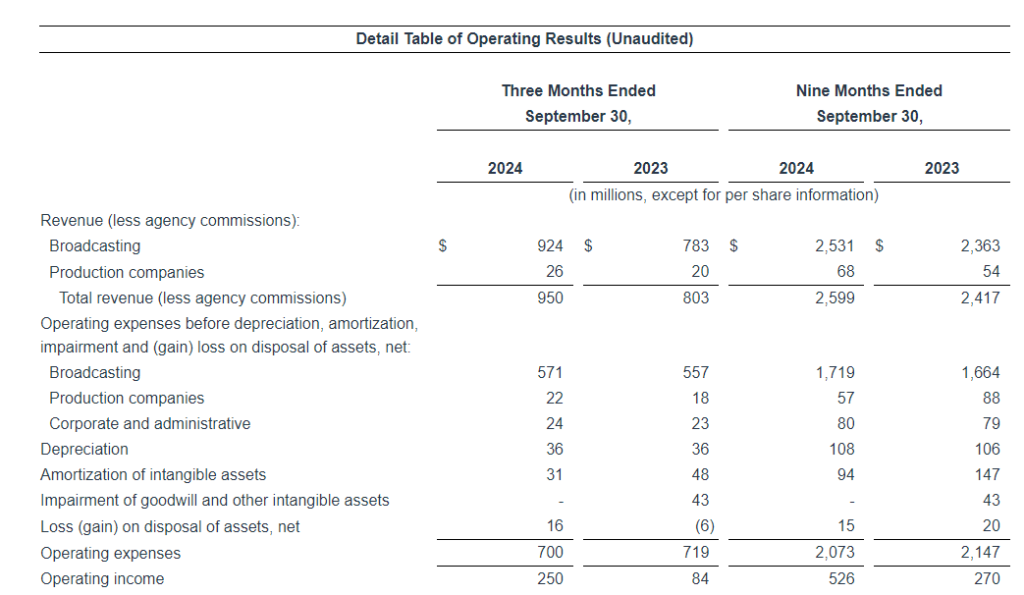

Total revenue in the third quarter of 2024 was $950 million, an increase of 18% from the third quarter of 2023.

Core advertising revenue in the third quarter of 2024 was $365 million, an increase of 1% from the third quarter of 2023.

Retransmission consent revenue in the third quarter of 2024 was $369 million, a decrease of 2% from the third quarter of 2023.

Political advertising revenue in the third quarter of 2024 was $173 million, an increase of 565% from the third quarter of 2023.

Total operating expenses (before depreciation, amortization and loss on disposal of assets) in the third quarter of 2024 was $617 million, which was 2% below the low end of our previously announced guidance for the quarter.

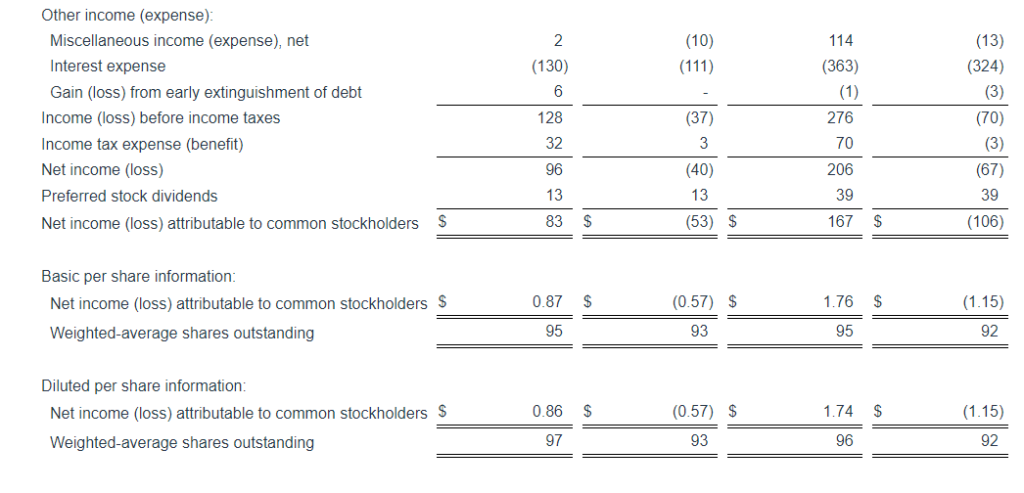

Net income attributable to common stockholders was $83 million in the third quarter of 2024, compared to a net loss attributable to common stockholders of $53 million in the third quarter of 2023.

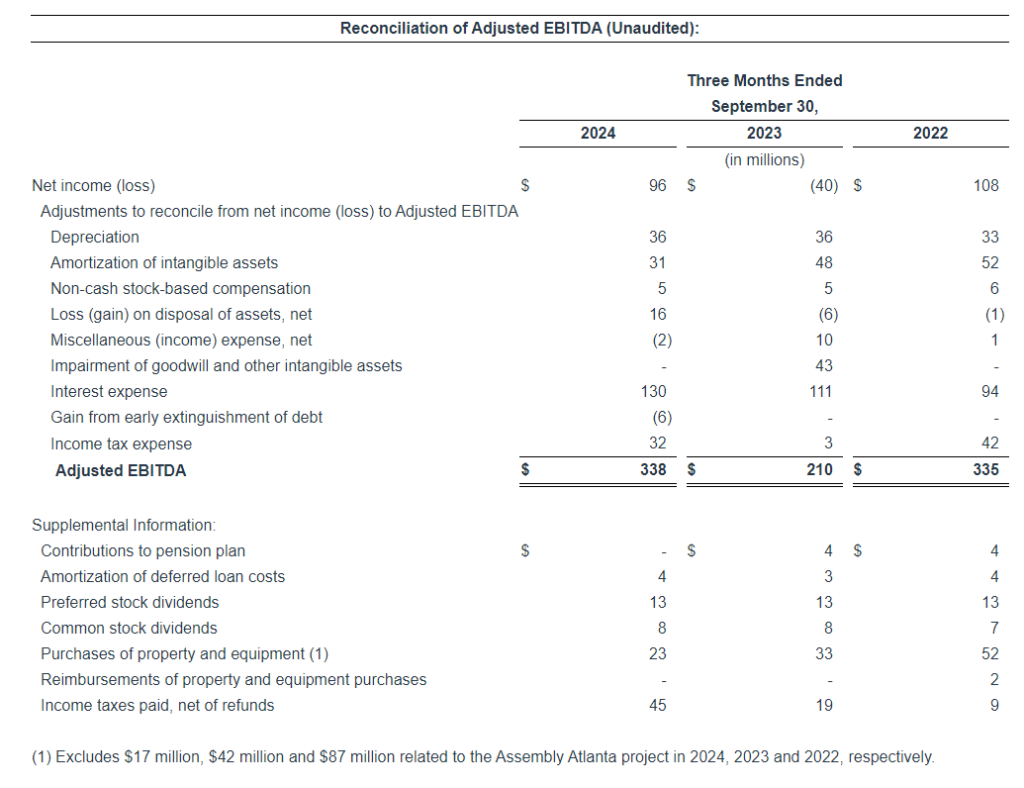

Adjusted EBITDA was $338 million in the third quarter of 2024, an increase of 61% from the third quarter of 2023, due primarily to the cyclical increase in political advertising revenue.

OTHER KEY METRICS:

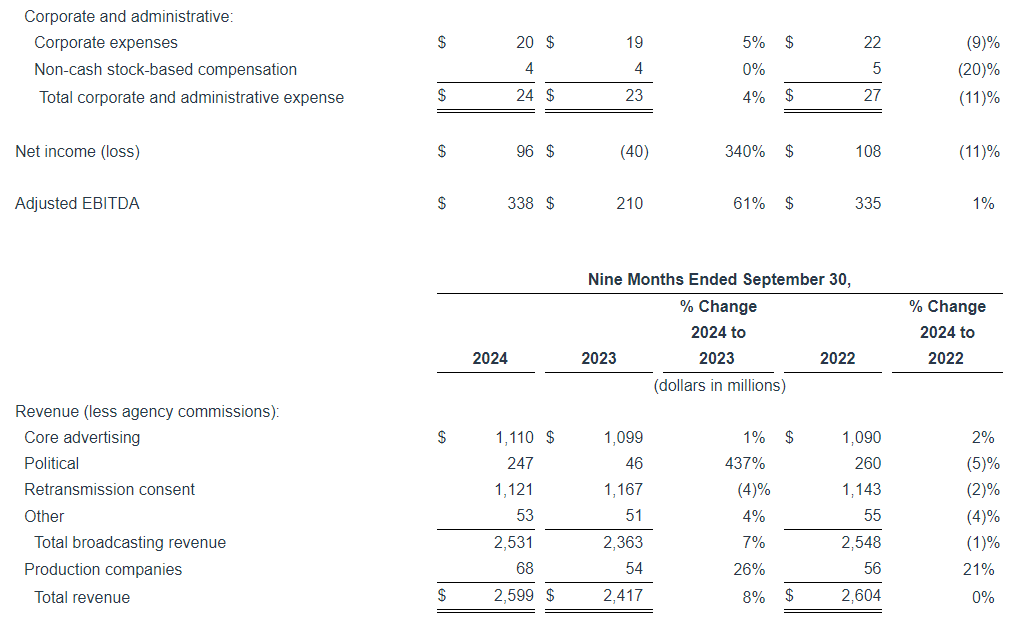

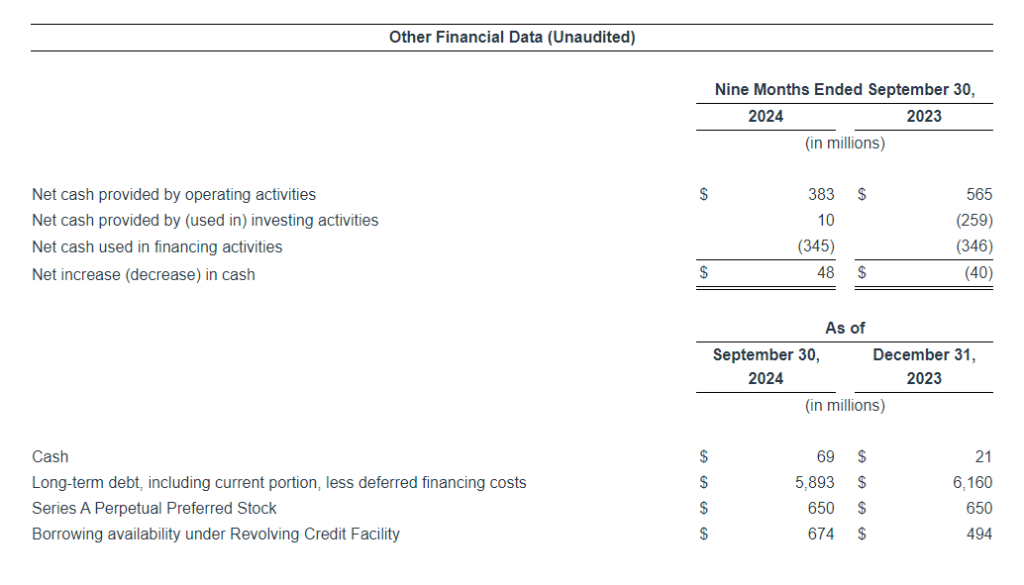

Through September 30, 2024, we reduced the principal amount of our debt by $241 million in 2024 and expect full-year 2024 Net Debt reduction of approximately $500 million.

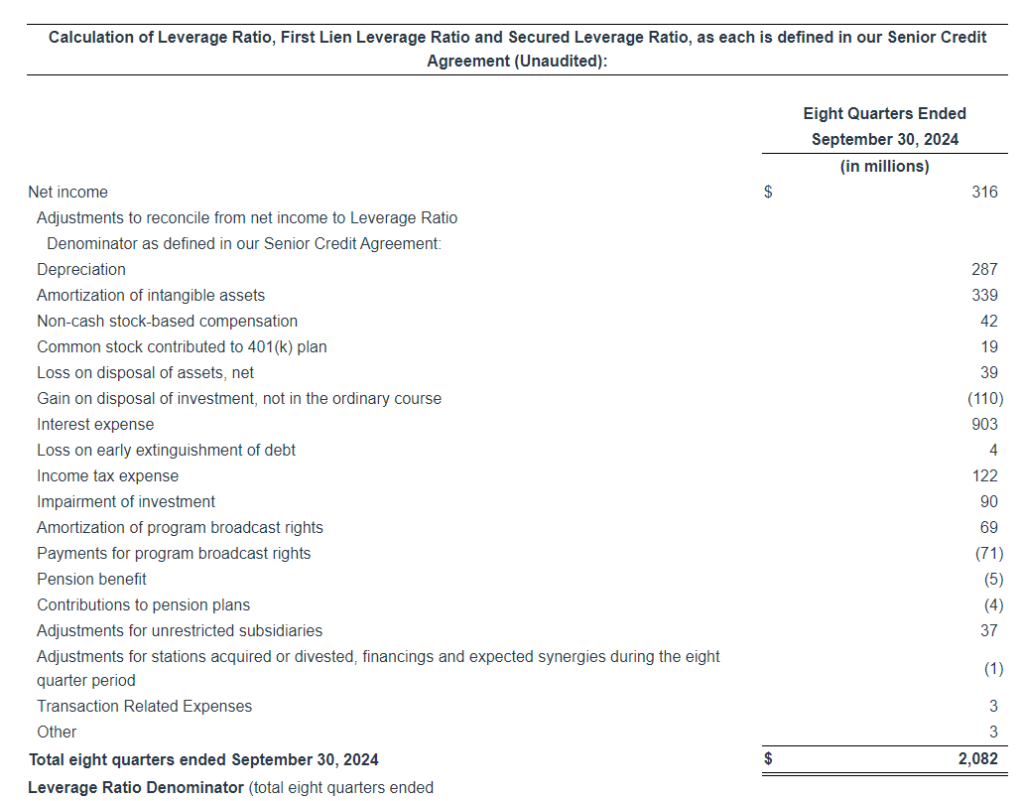

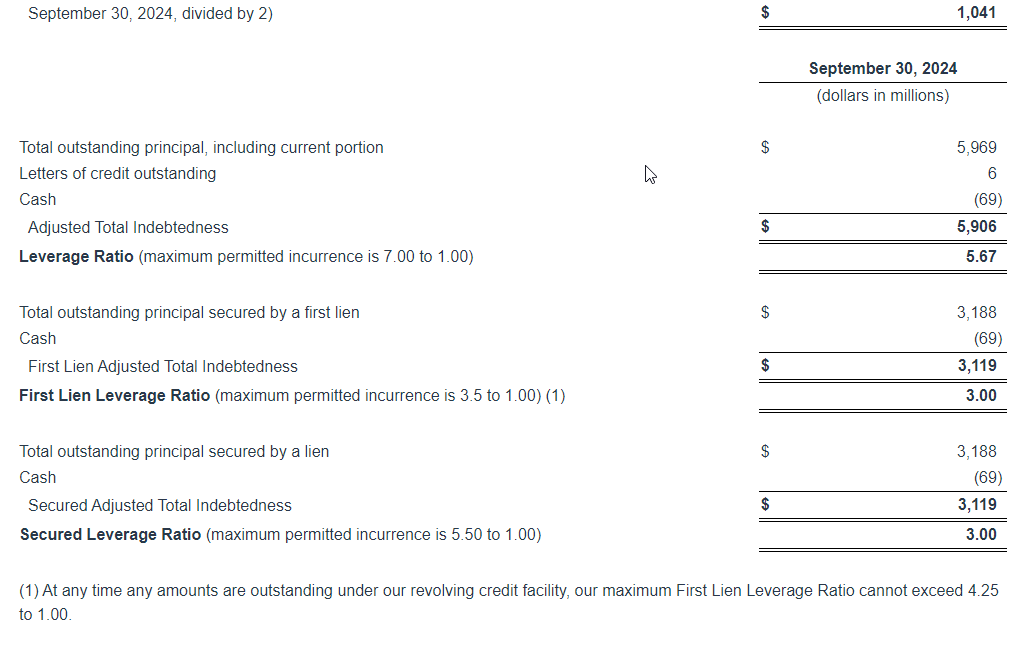

As of September 30, 2024, calculated as set forth in our Senior Credit Agreement, our First Lien Leverage Ratio and Leverage Ratio, which are net of $69 million of cash, were 3.00 to 1.00 and 5.67 to 1.00, respectively.

Currently, we have $674 million of borrowing availability under our undrawn Revolving Credit Facility.

Non-cash stock-based compensation was $5 million during each of the third quarters ended September 30, 2024 and 2023.

FINANCIAL RESULTS AND EXPECTATIONS

Our results in the third quarter were largely in line with our guidance, with the exception of political advertising revenues, which, while strong, were slightly below our expectations. Our broadcast and corporate operating expenses were much lower than expectations.

Our total revenue and our Core advertising revenue were within our guidance range at $950 million and $365 million, respectively, with Core advertising revenue up 1% compared to the third quarter of 2023. Our local television stations in several Southeastern markets experienced reductions in Core and political advertising revenues during late September, due to their extensive, often round-the-clock and commercial-free coverage of Hurricane Helene to support those affected communities in the third quarter.

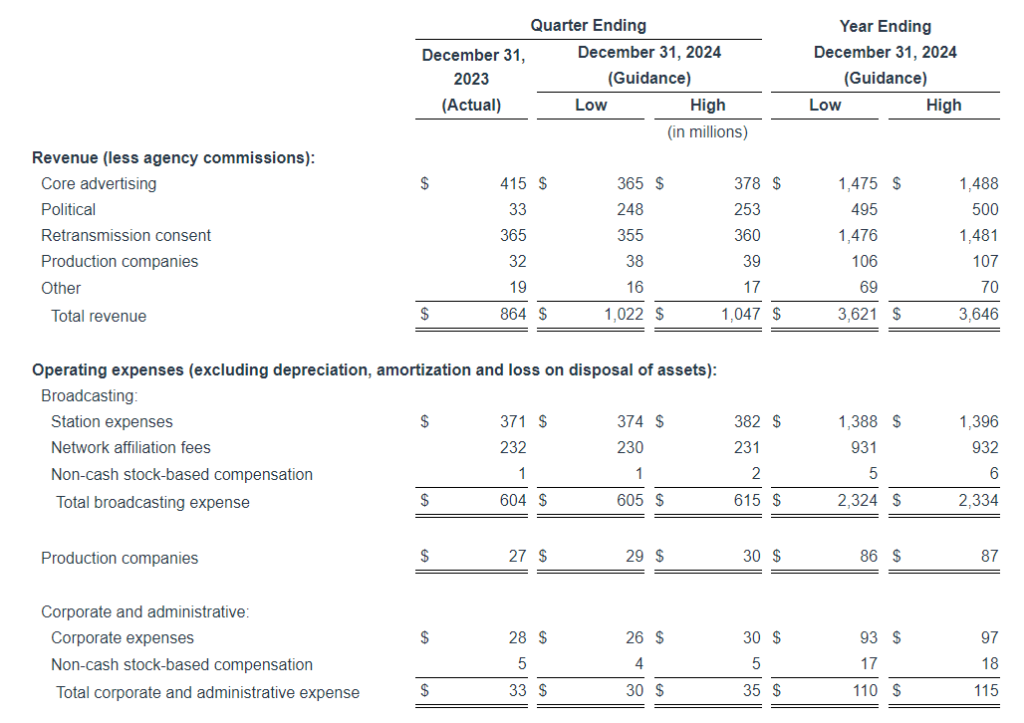

For the fourth quarter of 2024, we currently expect that Core advertising revenue will be down approximately 11% compared to the fourth quarter of 2023, due primarily to political advertising revenue displacement and the movement of SEC college football games in our Southeastern markets from the CBS Network to the ABC Network. In addition, the continuing impact of Hurricane Helene and the added impact of Hurricane Milton in the fourth quarter is expected to adversely impact Core advertising revenue in several of our Southeastern markets. We now anticipate Core advertising revenues within a range of $1.475 billion to $1.488 billion for full-year 2024, which is down approximately 3% from our earlier guidance of $1.525 billion and down approximately 2% compared to full-year 2023.

Our political advertising revenue in the third quarter of 2024 was $173 million, compared to the $190 million of political advertising revenue during the third quarter of 2020 that was recorded by our current television station portfolio. We anticipate that political advertising revenues for the fourth quarter of 2024 will be within a range of $248 million to $253 million, and for full-year 2024 within a range of $495 million to $500 million. Our political advertising revenue was impacted by fewer competitive non-presidential races in some of our markets during the second half of this year as well as the same significant factors affecting core advertising that are identified above.

Our retransmission consent revenue in the third quarter of 2024 was $369 million, which was within our guidance range. We currently expect retransmission consent revenues in the range of $355 million to $360 million for the fourth quarter of 2024 and, in a range of approximately $1.476 billion to $1.481 billion, for full-year 2024.

For the third quarter of 2024, our broadcasting operating expenses and corporate operating expenses were $14 million and $3 million below the low end of the expense guidance ranges, respectively. For full-year 2024, we currently expect broadcasting operating expenses and corporate operating expenses will be within the range of $2.324 billion to $2.334 billion, and $110 million to $115 million, respectively. These updated full-year expense estimates reflect significant decreases from the initial full-year guidance, provided in February of this year, of approximately $2.4 billion and $125 million, respectively. In addition, we currently anticipate capital expenditures for full-year 2024 of $135 million, which includes approximately $35 million, net of reimbursements, related to Assembly Atlanta. We expect additional reimbursements of approximately $18 million in the first quarter of 2025 related to 2024 capital expenditures at Assembly Atlanta.

COST CONTAINMENT INITIATIVES

Starting in August 2024, we began identifying and implementing various measures throughout the company that we expect will further reduce our operating expense run-rate by approximately $60 million on an annualized basis. As part of our routine budgeting process, we are carefully evaluating our capital expenditure needs for 2025.

We have taken several steps to reduce personnel expenses in 2025. These steps include streamlining workflows at our television stations and other business units, closing certain unfilled positions for which we were recruiting, eliminating certain positions that will not be filled following normal attrition throughout the second half of this year, and, for the first time in many years, eliminating certain positions in a handful of television stations and certain business units. Importantly, despite these staffing changes, we will continue to produce local newscasts with local journalists and local meteorologists in all of our existing local news markets, including small markets.

In terms of non-operating expenses, we anticipate a significant amount of interest savings due to lower debt balances resulting from open market debt repurchases and debt paydowns that have already occurred, and we anticipate will continue on an ongoing basis. We also anticipate that our cash income tax payments, net of refunds, for full-year 2024 will be approximately $133 million, approximately $49 million less than estimated in August of this year, due in part to interest expense deductibility in connection with Gray’s real estate assets, driven primarily by our Assembly Atlanta development.

DEBT REPURCHASES AND REPAYMENTS

We continue to focus on improving our balance sheet. From January 1, 2024 through September 30, 2024, we have reduced our principal amount of debt outstanding by $241 million. During the third quarter of 2024, we:

Repurchased and retired $29 million of our outstanding 2027 Notes on the open market at an average price of approximately 92.1% of par value, thereby reducing the remaining par value of our 2027 Notes to $671 million;

Repaid all amounts outstanding under our Revolving Credit Facility; and

Repurchased and retired approximately $16 million of our outstanding 2021 Term Loan on the open market at an average price of approximately 90.8% of par value.

In addition to the amounts above, we have previously entered into agreements to further reduce our 2021 Term Loan by an additional $39 million at an average price of approximately 92.6% of par value, which transactions will close in November 2024. We anticipate that upon completion of all of the above transactions, the remaining 2021 Term Loan principal outstanding at par value will be $1.400 billion.

We project, including actions taken to date, reduction of our Net Debt (also referred to herein as Adjusted Total Indebtedness) during full-year 2024 of $500 million during full-year 2024.

On November 7, 2024, our Board of Directors approved an increase in our debt repurchase authorization to repurchase additional debt in the open market, which replenished the previous authorization, bringing the total current authorization to $250 million. The extent of such repurchases, including the amount and timing of any repurchases, will depend on general market conditions, regulatory requirements, alternative investment opportunities and other considerations. This repurchase program supersedes any previous repurchase authorization, does not require us to repurchase a minimum amount of debt, and it may be modified, suspended or terminated at any time without prior notice.

TAXES

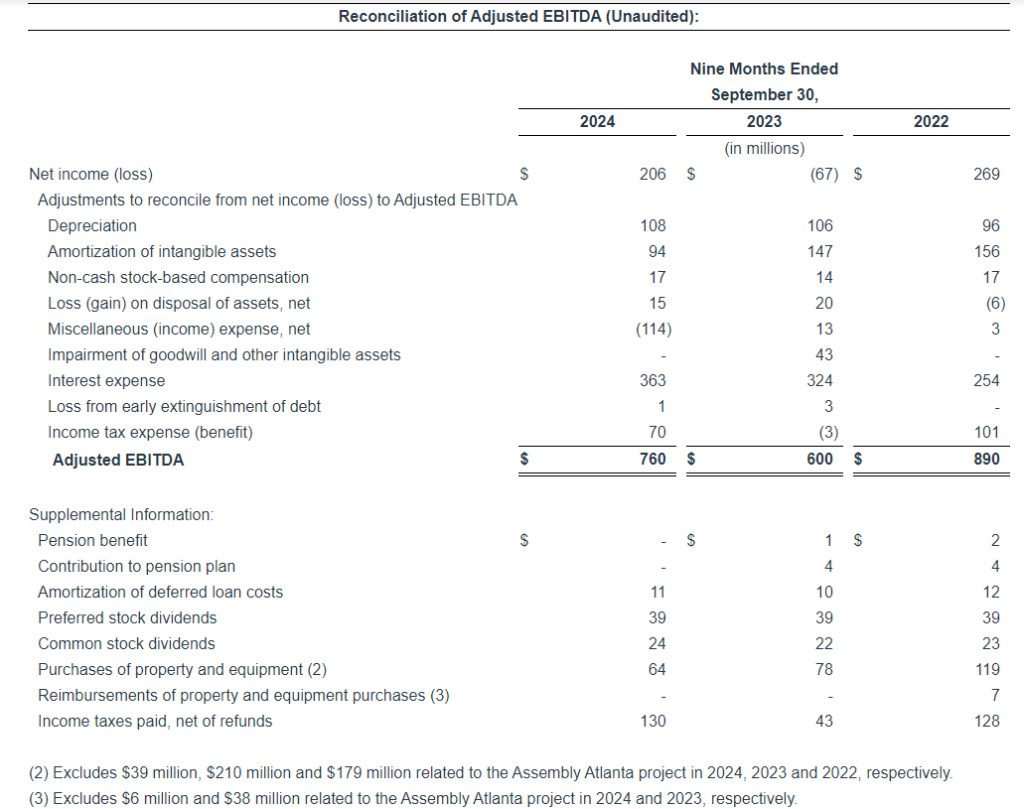

During the nine-months ended September 30, 2024 and 2023, we made income tax payments, net of refunds, of $130 million and $43 million, respectively. During the fourth quarter of 2024, based on our current forecasts, we anticipate making income tax payments, net of refunds, of approximately $3 million.

As of September 30, 2024, we have an aggregate of $282 million of various state operating loss carryforwards, of which we expect that approximately $201 million will not be utilized.

GUIDANCE FOR THE THREE MONTHS AND TWELVE MONTHS ENDING DECEMBER 31, 2024

Based on our current forecasts for the quarter ending December 31, 2024, we anticipate the following key financial results, as outlined below in approximate ranges and as compared to the quarter ended December 31, 2023, as well as certain currently anticipated full-year financial results. As always, guidance may change in the future based on several factors and therefore may not reflect actual results:

The Company

We are a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets serving 113 television markets that collectively reach approximately 36 percent of US television households. The portfolio includes 77 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station, as well as the largest Telemundo Affiliate group with 43 markets totaling nearly 1.5 million Hispanic TV households. We also own Gray Digital Media, a full-service digital agency offering national and local clients digital marketing strategies with the most advanced digital products and services. Our additional media properties include video production companies Raycom Sports, Tupelo Media Group, and PowerNation Studios, and studio production facilities Assembly Atlanta and Third Rail Studios. Gray also owns a majority interest in Swirl Films.

Cautionary Statements for Purposes of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act

This press release contains certain forward-looking statements that are based largely on our current expectations and reflect various estimates and assumptions by us. These statements are statements other than those of historical fact and may be identified by words such as “estimates,” “expect,” “anticipate,” “will,” “implied,” “assume” and similar expressions. Forward-looking statements are subject to certain risks, trends and uncertainties that could cause actual results and achievements to differ materially from those expressed in such forward-looking statements. Such risks, trends and uncertainties, which in some instances are beyond our control, include: estimates of future revenue, future expenses, future capital expenditures, future income tax payments, future workforce reductions and other future events. We are subject to additional risks and uncertainties described in our quarterly and annual reports filed with the Securities and Exchange Commission from time to time, including in the “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections contained therein, which reports are made publicly available via our website, www.graymedia.com. Any forward-looking statements in this press release should be evaluated in light of these important risk factors. This press release reflects management’s views as of the date hereof. Except to the extent required by applicable law, Gray undertakes no obligation to update or revise any information contained in this press release beyond the published date, whether as a result of new information, future events or otherwise. Information about certain potential factors that could affect our business and financial results and cause actual results to differ materially from those expressed or implied in any forward-looking statements are included under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in our Annual Report on Form 10-K for the year ended December 31, 2023, and may be contained in reports subsequently filed with the U.S. Securities and Exchange Commission and available at www.sec.gov.

Conference Call Information:

We will host a conference call to discuss our third quarter operating results on November 8, 2024. The call will begin at 11:00 AM Eastern Time. The live dial-in number is 1 (800) 285-6670. The call will be webcast live and available for replay at www.graymedia.com. The taped replay of the conference call will be available at 1 (888) 556-3470, Confirmation Code: 898476# until December 8, 2024.

Gray Contacts

Web site: www.graymedia.com

Hilton H. Howell, Jr., Executive Chairman and Chief Executive Officer, (404) 266-5513

Pat LaPlatney, President and Co-Chief Executive Officer, (334) 206-1400

Jeffrey R. Gignac, Executive Vice President and Chief Financial Officer, (404) 504-9828

Kevin P. Latek, Executive Vice President, Chief Legal and Development Officer, (404) 266-8333

Non-GAAP Terms

In addition to results prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), this earnings release discusses “Adjusted EBITDA” a non-GAAP performance measure that management uses to evaluate the performance of the business. Adjusted EBITDA is calculated as net income (loss), adjusted for income tax expense (benefit), interest expense, loss on extinguishment of debt, non-cash stock-based compensation costs, non-cash 401(k) expense, depreciation, amortization of intangible assets, impairment of goodwill and other intangible assets, impairment of investments, loss (gain) on asset disposals and certain other miscellaneous items. We consider Adjusted EBITDA to be an indicator of our operating performance.

In addition to results prepared in accordance with GAAP, “Leverage Ratio Denominator” is a metric that management uses to calculate our compliance with our financial covenants in our indebtedness agreements. This metric is calculated as specified in our Senior Credit Agreement and is a significant measure that represents the denominator of a formula used to calculate compliance with material financial covenants within the Senior Credit Agreement that govern our ability to incur indebtedness, incur liens, make investments and make restricted payments, among other limitations usual and customary for credit agreements of this type. Accordingly, management believes this metric is a very material metric to our debt and equity investors. Leverage Ratio Denominator gives effect to the revenue and broadcast expenses of all completed acquisitions and divestitures as if they had been acquired or divested, respectively, on October 1, 2022. It also gives effect to certain operating synergies expected from the acquisitions and related financings and adds back professional fees incurred in completing the acquisitions. Certain of the financial information related to the acquisitions, if applicable, has been derived from, and adjusted based on, unaudited, un-reviewed financial information prepared by other entities, which Gray cannot independently verify. We cannot assure you that such financial information would not be materially different if such information were audited or reviewed and no assurances can be provided as to the accuracy of such information, or that our actual results would not differ materially from this financial information if the acquisitions had been completed on the stated date. In addition, the presentation of Leverage Ratio Denominator as determined in the Senior Credit Agreement and the adjustments to such information, including expected synergies, if applicable, resulting from such transactions, may not comply with GAAP or the requirements for pro forma financial information under Regulation S-X under the Securities Act of 1933. Leverage Ratio Denominator, as determined in the Senior Credit Agreement, represents an average amount for the preceding eight quarters then ended.

We define Transaction Related Expenses as incremental expenses incurred specific to acquisitions and divestitures, including but not limited to legal and professional fees, severance and incentive compensation, and contract termination fees. We present certain line items from our selected operating data, net of Transaction Related Expenses, in order to present a more meaningful comparison between periods of our operating expenses and our results of operations.

Our “Adjusted Total Indebtedness” or “Net Debt”, “First Lien Adjusted Total Indebtedness” and “Secured Adjusted Total Indebtedness” in each case net of all cash, represents the amount of outstanding principal of our long-term debt, plus certain other obligations as defined in our Senior Credit Agreement for the applicable amount of indebtedness.

These non-GAAP terms are not defined in GAAP and our definitions may differ from, and therefore may not be comparable to, similarly titled measures used by other companies, thereby limiting their usefulness. Such terms are used by management in addition to, and in conjunction with, results presented in accordance with GAAP and should be considered as supplements to, and not as substitutes for, net income and cash flows reported in accordance with GAAP.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In line quarter. Total company revenues of $115.3 million was roughly flat with the year earlier period and in line with our $115.0 million estimate. Q3 adj. EBITDA was $25.5 million versus our $26.5 million estimate. Notably, the results were in line with the company’s previous guidance.

Digital revenue accelerates. Total digital revenue swung positive in the latest quarter, up 1.1%, the first time since q2 2023. The revenue improvement was led by its Ignite business (up 4.7%) and a significant moderation in the revenue decline at Townsquare Ignite (down 5.8%, much better than down 12.9% in Q2). Management indicated that Ignite’s Q4 revenue growth should triple to near 15% and Interactive should swing positive.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 results. The company reported Q3 revenue of $28.1 million and adj. EBITDA of $3.6 million, both of which were in line with our estimates of $28.7 million and $3.6 million, respectively. Notably, the company ended an unprofitable relationship with a digital services provider, which contributed to digital revenue growth slowing to 3.2% in Q3. While we anticipate this will make year-over-year digital revenue comparisons difficult in the short term, we believe the company’s digital segment offers a favorable growth outlook.

Q4 outlook. Management indicated that Q4 revenue is pacing down low to mid-single digits, highlighting a difficult advertising market that is feeling the effects of the high interest rate environment. Furthermore, operating expenses on a same station basis are guided to increase in the range of 3% – 5% over the prior year period. We anticipate this increase will largely be attributed to investments in the company’s digital growth initiatives.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Digital Represents 52% of September YTD Total Net Revenue Ignite’s Digital Advertising Revenue Growth Accelerates in Q3 Repurchased $25 Million of Debt ($36M through October) and $24 Million of Equity in September YTD Period

PURCHASE, N.Y., Nov. 07, 2024 (GLOBE NEWSWIRE) — Townsquare Media, Inc. (NYSE: TSQ) (“Townsquare”, the “Company,” “we,” “us,” or “our”) announced today its financial results for the third quarter ended September 30, 2024.

“I am pleased to share that Townsquare’s net revenue returned to year-over-year growth, driven by sequential improvement across each of our three business segments, due to our local focus and our unique and differentiated digital platform, as well as the benefit from political revenue. Third quarter net revenue increased +0.2% year-over-year and Adjusted EBITDA decreased -6.3% year-over-year, both meeting guidance and reflecting a sequential improvement from the first and second quarter. In addition, net income improved $47.8 million year-over-year, in large part due to a reduction in non-cash impairment charges,” commented Bill Wilson, Chief Executive Officer of Townsquare Media, Inc. “Our return to net revenue growth in the third quarter coincided with our return to total Digital net revenue growth, which increased by +1% year-over-year. In particular, Townsquare Interactive’s sequential revenue growth improved to +3% quarter-over-quarter, and Digital Advertising net revenue increased +5% year-over-year, an acceleration from the +1% revenue growth rates in the first six months of 2024. In total, Digital represented more than half of Townsquare’s net revenue in the first nine months of the year, a true point of differentiation from others in local media, as we have evolved from a local broadcast radio company that was founded in 2010, to a Digital First Local Media Company with a world class team and a unique and differentiated strategy, assets, platforms and solutions.”

Mr. Wilson continued, “We have executed and delivered on what we said we would do, while simultaneously building value for our shareholders through dividend payments, debt reduction and share repurchases. In the first nine months of the year, we have repurchased and retired $25 million of our bonds at a discount to par ($36 million through October), and repurchased $24 million of equity, or 2.3 million shares, including the accretive share repurchase of 1.5 million shares from Madison Square Garden. At the same time, we have maintained our high yielding dividend and a strong cash balance, which was $22 million at the end of the third quarter, and net leverage remained below 4.9x. We are gearing up for our upcoming refinancing, and we look forward to sharing that outcome with our investors when we next report.”

The Company announced today that its Board of Directors approved a quarterly cash dividend of $0.1975 per share. The dividend will be payable on February 1, 2025 to shareholders of record as of the close of business on January 21, 2025. As of yesterday’s closing price that reflects a dividend yield of approximately 8%.

Segment Reporting We have three reportable operating segments, Subscription Digital Marketing Solutions, Digital Advertising and Broadcast Advertising. The Subscription Digital Marketing Solutions segment includes our subscription digital marketing solutions business, Townsquare Interactive. The Digital Advertising segment, marketed externally as Townsquare Ignite, includes digital advertising on our owned and operated digital properties, our first party data digital management platform and our digital programmatic advertising platform. The Broadcast Advertising segment includes our local, regional, and national advertising products and solutions delivered via terrestrial radio broadcast, and other miscellaneous revenue that is associated with our broadcast advertising platform. The remainder of our business is reported in the Other category, which includes our live events business.

Third Quarter Results*

As compared to the third quarter of 2023:

Net revenue increased 0.2%, and decreased 2.5% excluding political

Net income increased $47.8 million

Adjusted EBITDA decreased 6.3%

Total Digital net revenue increased 1.1%

Subscription Digital Marketing Solutions (“Townsquare Interactive”) net revenue decreased 5.8%

Digital Advertising net revenue increased 4.7%

Total Digital Adjusted Operating Income decreased 8.9%

Subscription Digital Marketing Solutions Adjusted Operating Income decreased 11.0%

Digital Advertising Adjusted Operating Income decreased 7.9%

Broadcast Advertising net revenue increased 0.3%, and decreased 5.3% excluding political

Net Income per diluted share was $0.63 and Adjusted Net Income per diluted share was $0.35

Repurchased an aggregate $11.0 million of our 2026 Senior Secured Notes below par

Repurchased 0.1 million shares of the Company’s common stock at an average price of $11.32

Year-to-Date Highlights*

As compared to the nine months ended September 30, 2023:

Net revenue decreased 1.8%, and 3.3% excluding political

Net loss decreased $5.2 million

Adjusted EBITDA decreased 8.0%

Total Digital net revenue decreased 2.6%

Subscription Digital Marketing Solutions net revenue decreased 11.5%

Digital Advertising net revenue increased 2.4%

Total Digital Adjusted Operating Income decreased 17.0%

Subscription Digital Marketing Solutions Adjusted Operating Income decreased 10.3%

Digital Advertising Adjusted Operating Income decreased 20.2%

Broadcast Advertising net revenue decreased 0.3%, and 3.4%, excluding political

Repurchased an aggregate $24.7 million of our 2026 Senior Secured Notes below par

Repurchased 2.3 million shares of the Company’s common stock at an average price of $10.31

Repurchased and retired 3.2 million options expiring in July 2024 for a net purchase price of $3.60 per option

*See below for discussion of non-GAAP measures.

Guidance For the fourth quarter of 2024, net revenue is expected to be between $114.8 million and $118.8 million, and Adjusted EBITDA is expected to be between $30.8 million and $31.8 million.

For the full year 2024, net revenue is expected to be between $448 million and $452 million, and Adjusted EBITDA is expected to be between $100 million and $101 million, both within our original guidance ranges.

Quarter Ended September 30, 2024 Compared to the Quarter Ended September 30, 2023

Net Revenue Net revenue for the three months ended September 30, 2024 increased $0.2 million, or 0.2%, to $115.3 million as compared to $115.1 million in the same period in 2023. Digital Advertising net revenue increased $1.9 million, or 4.7%, as compared to the same period in 2023, and Broadcast Advertising net revenue increased $0.2 million, or 0.3%, as compared to the same period in 2023. These increases were partially offset by a decrease in Subscription Digital Marketing Solutions net revenue of $1.2 million, or 5.8%, and a $0.6 million, or 37.3%, decrease in Other net revenue as compared to the same period in 2023. Excluding political revenue of $3.7 million and $0.6 million for the three months ended September 30, 2024 and 2023, respectively, net revenue decreased $2.9 million, or 2.5%, to $111.6 million. Broadcast Advertising net revenue decreased $2.8 million, or 5.3%, to $50.8 million, and Digital Advertising net revenue increased $1.8 million, or 4.6%, to $40.7 million.

Net Income (Loss) For the three months ended September 30, 2024, we reported net income of $11.3 million, an increase of $47.8 million as compared to a net loss of $36.5 million in the same period last year. The increase was primarily due to a $29.0 million decrease in non-cash impairment charges, partially offset by a $2.5 million increase in direct operating expenses and a $22.6 million decrease in the income tax provision due to the valuation allowance for interest expense carryforwards and an increase in certain non-deductible compensation costs. Adjusted Net Income decreased $2.2 million as compared to the same period last year.

Adjusted EBITDA Adjusted EBITDA for the three months ended September 30, 2024 decreased $1.7 million, or 6.3%, to $25.5 million, as compared to $27.2 million in the same period last year. Adjusted EBITDA (Excluding Political) decreased $4.3 million, or 16.3%, to $22.3 million, as compared to $26.6 million in the same period last year.

Nine Months Ended September 30, 2024 Compared to the Nine Months Ended September 30, 2023

Net Revenue Net revenue for the nine months ended September 30, 2024, decreased $6.3 million, or 1.8%, to $333.2 million as compared to $339.4 million in the same period in 2023. Subscription Digital Marketing Solutions net revenue decreased $7.2 million, or 11.5%, Other net revenue decreased $1.3 million, or 15.3%, and Broadcast Advertising net revenue decreased $0.4 million, or 0.3%, as compared to the same period in 2023. These declines were partially offset by a $2.7 million, or 2.4%, increase in Digital Advertising net revenue as compared to the same period in 2023. Excluding political revenue of $6.2 million and $1.2 million for the nine months ended September 30, 2024 and 2023, respectively, net revenue decreased $11.3 million, or 3.3% to $327.0 million, Broadcast Advertising net revenue decreased $5.1 million, or 3.4%, to $147.6 million, and Digital Advertising net revenue increased $2.5 million, or 2.2%, to $116.2 million.

Net Loss For the nine months ended September 30, 2024, we reported a net loss of $36.0 million, a decrease of $5.2 million as compared to a net loss of $41.1 million in the same period last year. The decrease was due to a $29.4 million decrease in non-cash impairment charges, partially offset by increases in stock-based compensation and transaction and business realignment costs, the decrease in net revenue and a $4.5 million increase in the income tax provision was driven by the valuation allowance for interest expense carryforwards and an increase in certain non-deductible compensation costs. Adjusted Net Income decreased $9.7 million as compared to the same period last year.

Adjusted EBITDA Adjusted EBITDA for the nine months ended September 30, 2024 decreased $6.0 million, or 8.0% to $69.2 million, as compared to $75.2 million in the same period last year. Adjusted EBITDA (Excluding Political) decreased $10.3 million, or 13.8%, to $63.9 million, as compared to $74.2 million in the same period last year.

Liquidity and Capital Resources As of September 30, 2024, we had a total of $21.8 million of cash and cash equivalents and $478.9 million of outstanding indebtedness, representing 5.10x and 4.86x gross and net leverage, respectively, based on Adjusted EBITDA for the twelve months ended September 30, 2024, of $94.0 million.

The table below presents a summary, as of November 1, 2024, of our outstanding common stock (net of treasury shares).

Security

Number Outstanding

Description

Class A common stock

14,231,917

One vote per share.

Class B common stock

815,296

10 votes per share.1

Class C common stock

500,000

No votes.1

Total

15,547,213

1 Each share converts into one share of Class A common stock upon transfer or at the option of the holder, subject to certain conditions, including compliance with FCC rules.

Conference Call Townsquare Media, Inc. will host a conference call to discuss certain third quarter 2024 financial results and 2024 guidance on Thursday, November 7, 2024 at 10:00 a.m. Eastern Time. The conference call dial-in number is 1-800-717-1738 (U.S. & Canada) or 1-646-307-1865 (International) and the conference ID is “Townsquare”. A live webcast of the conference call will also be available on the investor relations page of the Company’s website at www.townsquaremedia.com.

A replay of the conference call will be available through November 14, 2024. To access the replay, please dial 1-844-512-2921 (U.S. and Canada) or 1-412-317-6671 (International) and enter confirmation code 1142541. A web-based archive of the conference call will also be available at the above website.

About Townsquare Media, Inc. Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for SMBs; a robust digital advertising division, Townsquare Ignite, a powerful combination of a) an owned and operated portfolio of more than 400 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 349 local terrestrial radio stations in 74 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com and NJ101.5.com, and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com, and Loudwire.com. For more information, please visit www.townsquaremedia.com, www.townsquareinteractive.com and www.townsquareignite.com.

Forward-Looking Statements Except for the historical information contained in this press release, the matters addressed are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements often discuss our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “aim,” “anticipate,” “estimate,” “expect,” “forecast,” “outlook,” “potential,” “project,” “projection,” “plan,” “intend,” “seek,” “believe,” “may,” “could,” “would,” “will,” “should,” “can,” “can have,” “likely,” the negatives thereof and other words and terms. Actual events or results may differ materially from the results anticipated in these forward-looking statements as a result of a variety of factors. While it is impossible to identify all such factors, factors that could cause actual results to differ materially from those estimated by us include the impact of general economic conditions in the United States, or in the specific markets in which we currently do business including supply chain disruptions, inflation, labor shortages and the effect on advertising activity, industry conditions, including existing competition and future competitive technologies, the popularity of radio as a broadcasting and advertising medium, cancellations, disruptions or postponements of advertising schedules in response to national or world events, our ability to develop and maintain digital technologies and hire and retain technical and sales talent, our dependence on key personnel, our capital expenditure requirements, our continued ability to identify suitable acquisition targets, and consummate and integrate any future acquisitions, legislative or regulatory requirements, risks and uncertainties relating to our leverage and changes in interest rates, our ability to obtain financing at times, in amounts and at rates considered appropriate by us, our ability to access the capital markets as and when needed and on terms that we consider favorable to us and other factors discussed in this section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this report and under “Risk Factors” in our 2023 Annual Report on Form 10-K, for the year ended December 31, 2023, filed with the SEC on March 15, 2024, as well as other risks discussed from time to time in our filings with the SEC. Many of these factors are beyond our ability to predict or control. In addition, as a result of these and other factors, our past financial performance should not be relied on as an indication of future performance. The cautionary statements referred to in this section also should be considered in connection with any subsequent written or oral forward-looking statements that may be issued by us or persons acting on our behalf. The forward-looking statements included in this report are made only as of the date hereof or as of the date specified herein. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Non-GAAP Financial Measures and Definitions In this press release, we refer to Adjusted Operating Income, Adjusted EBITDA, Adjusted EBITDA (Excluding Political), Adjusted Net Income and Adjusted Net Income Per Share which are financial measures that have not been prepared in accordance with generally accepted accounting principles in the United States (“GAAP”).

We define Adjusted Operating Income by Segment as operating income by segment before the deduction of depreciation and amortization, stock-based compensation, corporate expenses, transaction costs, business realignment costs, impairments and net loss (gain) on sale and retirement of assets. We define Adjusted EBITDA as net income before the deduction of income taxes, interest expense, net, gain on repurchases of debt, transaction and business realignment costs, depreciation and amortization, stock-based compensation, impairments, net loss (gain) on sale and retirement of assets and other expense (income) net. We define Adjusted EBITDA (Excluding Political) as Adjusted EBITDA less political net revenue, net of a fifteen percent deduction to account for estimated national representative firm fees, music licensing fees and sales commissions expense. Adjusted Net Income is defined as net income before the deduction of transaction and business realignment costs, impairments, gains on sale of investments, change in fair value of investment, net loss (gain) on sale and retirement of assets, gain on repurchases of debt, gain on sale of digital assets, gain on insurance recoveries and net income attributable to non-controlling interest, net of income taxes stated at the Company’s applicable statutory effective tax rate. Adjusted Net Income Per Share is defined as Adjusted Net Income divided by the weighted average shares outstanding. We define Net Leverage as our total outstanding indebtedness, net of our total cash balance as of September 30, 2024, divided by our Adjusted EBITDA for the twelve months ended September 30, 2024. These measures do not represent, and should not be considered as alternatives to or superior to, financial results and measures determined or calculated in accordance with GAAP. In addition, these non-GAAP measures are not based on any comprehensive set of accounting rules or principles. You should be aware that in the future we may incur expenses or charges that are the same as or similar to some of the adjustments in the presentation, and we do not infer that our future results will be unaffected by unusual or non-recurring items. In addition, these non-GAAP measures may not be comparable to similarly-named measures reported by other companies.

We use Adjusted Operating Income by Segment to evaluate the operating performance of our business segments. We use Adjusted EBITDA and Adjusted EBITDA (Excluding Political) to facilitate company-to-company operating performance comparisons by backing out potential differences caused by variations in capital structures (affecting interest expense), taxation and the age and book depreciation of facilities and equipment (affecting relative depreciation expense), which may vary for different companies for reasons unrelated to operating performance, and to facilitate year over year comparisons, by backing out the impact of political revenue which varies depending on the election cycle and may be unrelated to operating performance. We use Adjusted Net Income and Adjusted Net Income Per Share to assess total company operating performance on a consistent basis. We use Net Leverage to measure the Company’s ability to handle its debt burden. We believe that these measures, when considered together with our GAAP financial results, provide management and investors with a more complete understanding of our business operating results, including underlying trends, by excluding the effects of transaction costs, net loss (gain) on sale and retirement of assets, business realignment costs and certain impairments. Further, while discretionary bonuses for members of management are not determined with reference to specific targets, our board of directors may consider Adjusted Operating Income by Segment, Adjusted EBITDA, Adjusted EBITDA (Excluding Political), Adjusted Net Income, Adjusted Net Income Per Share, and Net Leverage when determining discretionary bonuses.

The E.W. Scripps Company (NASDAQ: SSP) is a diversified media company focused on creating a better-informed world. As one of the nation’s largest local TV broadcasters, Scripps serves communities with quality, objective local journalism and operates a portfolio of 61 stations in 41 markets. The Scripps Networks reach nearly every American through the national news outlets Court TV and Newsy and popular entertainment brands ION, Bounce, Defy TV, Grit, ION Mystery, Laff and TrueReal. Scripps is the nation’s largest holder of broadcast spectrum. Scripps runs an award-winning investigative reporting newsroom in Washington, D.C., and is the longtime steward of the Scripps National Spelling Bee. Founded in 1878, Scripps has held for decades to the motto, “Give light and the people will find their own way.”

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. The company reported revenue of $646.3 million and adj. EBITDA of $176.8 million, both of which were record highs. Notably, the quarter was driven by strong political revenue of $125.2 million, which exceeded expectations. Furthermore, the company was able to capitalize on the influx of high-margin political revenue and pay down $115 million of debt in the quarter.

Record political advertising. The company generated $125.2 million in political revenue for Q3, a record high, and increased its full year political revenue guidance from $270 million – $290 million to a minimum of $340 million. The company’s increased 2024 political revenue guidance reflects a roughly 30% increase over its highest political advertising year, 2020.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Off to a good start. Fiscal Q1 end Sept. results were better than expectations. Revenues were $260.2 million versus our $240.0 million estimate. Adj. EBITDA was $62.9 million versus our $59.0 million estimate. The key revenue upside driver was a solid performance in Food & Beverage, up a strong 17.3% y-o-y and beating our estimate by a solid 10.7%. Figure #1 Q1 Results highlight the quarter versus our estimates.

Raises low end of fiscal 2025 guidance. Management increased its total revenue guidance for fiscal 2025 by $10 million on the low end of its previous guidance range of $1.22 billion to $1.28 billion, now $1.23 billion to $1.28 billion. The guidance implies attractive mid-single digit to 10% plus year over year revenue growth. Adj. EBITDA margins are expected to be 32% to 34%, or adj. EBITDA between $390 million to $430 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NAPLES, Fla., Nov. 01, 2024 (GLOBE NEWSWIRE) — Beasley Broadcast Group, Inc. (Nasdaq: BBGI) (“Beasley” or the “Company”), a multi-platform media company, announced today that it will report its 2024 third quarter financial results before the market opens on Tuesday, November 5, 2024. The Company will host a conference call and webcast at 11:30 a.m. ET that morning to review the results.

To access the conference call, interested parties may dial 877-407-4018 or 201-689-8471, conference ID 13749767 (domestic and international callers). Participants can also listen to a live webcast of the call at the Company’s website at www.bbgi.com. Please allow 15 minutes to register and download and install any necessary software. Following its completion, a replay of the webcast can be accessed for five days on the Company’s website, www.bbgi.com.

Questions from analysts, institutional investors and debt holders may be e-mailed to ir@bbgi.com at any time up until 9:00 a.m. ET on November 5, 2024. Management will answer as many questions as possible during the conference call and webcast (provided the questions are not addressed in their prepared remarks).

About Beasley Broadcast Group The Company is a multi-platform media company whose primary business is operating radio stations throughout the United States. The Company offers local and national advertisers integrated marketing solutions across audio, digital and event platforms. The Company owns and operates 57 AM and FM stations in the following large- and mid-size markets in the United States: Atlanta, GA, Augusta, GA, Boston, MA, Charlotte, NC, Detroit, MI, Fayetteville, NC, Fort Myers-Naples, FL, Las Vegas, NV, Middlesex, NJ, Monmouth, NJ, Morristown, NJ, Philadelphia, PA, and Tampa-Saint Petersburg, FL. Approximately 20 million consumers listen to the Company’s radio stations weekly over-the-air, online and on smartphones and tablets, and millions regularly engage with the Company’s brands and personalities through digital platforms such as Facebook, X, text, apps and email. For more information, please visit www.bbgi.com.

For further information, or to receive future Beasley Broadcast Group news announcements via e-mail, please contact Beasley Broadcast Group, at 239-263-5000 or email@bbgi.com, or Joseph Jaffoni, JCIR, at 212-835-8500 or bbgi@jcir.com.

CONTACT:

Heidi Raphael Chief Communications Officer Beasley Broadcast Group, Inc. 239-263-5000 or email@bbgi.com

Joseph Jaffoni, Jennifer Neuman JCIR 212-835-8500 or bbgi@jcir.com

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In-line Q3 results. The company reported revenue of $203.6 million and adj. EBITDA of $24.1 million, in-line with our estimates of $203.3 million and $24.8 million, respectively. Its digital businesses, now 20% of total revenues, was the highlight of the quarter, up 7.5% from the prior year. Political advertising was a little softer than expected, $4.4 million versus our $5.5 million estimate.

National/Network remains lackluster. National advertising is over 50% of total company revenues and carries very high margins. A recovery in National/Network will be key toward improved company fundamentals. Management indicated that National advertisers appear to be hesitant to spend, possibly due to economic uncertainty and concerns over the upcoming presidential elections.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

October 30, 2024 – Limassol, Cyprus – GDEV Inc. (NASDAQ: GDEV), an international gaming and entertainment company (“GDEV” or the “Company”), announces changes to its Board of Directors and executive leadership team as part of its ongoing strategy to enhance operational efficiency and support its global growth ambitions.

Olga Loskutova, who has served as an Independent Director on GDEV’s Board since 2022, will be stepping down from her position on the Board of Directors to assume the role of Chief Operating Officer (COO) of GDEV. Olga brings with her a wealth of experience in global business and general management, positioning her to provide management, leadership, and vision to guide GDEV Inc. towards meeting both its short-term and long-term strategic goals.

Following Olga’s transition, GDEV’s Board will consist of six members, with four remaining independent directors. In addition, Olga’s seat on the Nomination and Compensation Committee, on which she previously served, has been assumed by current independent director Tal Shoham.

Anton Reinhold, the former COO of GDEV, will now fully focus on his current role as CEO of Nexters Global Ltd., GDEV’s flagship game studio. This decision will enable him to dedicate his efforts to further expanding the Hero Wars franchise and driving the development of new products within the studio.

“During 2 years as an independent board member, I’ve had the opportunity to gain invaluable insight into the company and the gaming industry as a whole,” said Olga Loskutova. “In my time on the board, I’ve come to admire what makes GDEV truly special – its values, exceptional people, and bold ambitions. I am excited to step into this role and partner with the CEO and the team to help GDEV achieve its strategic goals.”

ABOUT GDEV

GDEV is a gaming and entertainment holding company, focused on development and growth of its franchise portfolio across various genres and platforms. With a diverse range of subsidiaries including Nexters and Cubic Games, among others, GDEV strives to create games that will inspire and engage millions of players for years to come. Its franchises, such as Hero Wars, Island Hoppers, Pixel Gun 3D and others have accumulated over 550 million installs and $2.5 bln of bookings worldwide. For more information, please visit www.gdev.inc

CONTACTS:

Investor Relations

Roman Safiyulin | Chief Corporate Development Officer

Certain statements in this press release may constitute “forward-looking statements” for purposes of the federal securities laws. Such statements are based on current expectations that are subject to risks and uncertainties. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements.

The forward-looking statements contained in this press release are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that the Company has anticipated. Forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Company’s control) or other assumptions. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of the Company’s 2023 Annual Report on Form 20-F, filed by the Company on April 29, 2024, and other documents filed by the Company from time to time with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize, or should any of the Company’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 preview. We estimate the company’s upcoming Q3 revenue and adj. EBITDA to be $103.0 million and $4.9 million, respectively. There is the prospect for an upside surprise, however, particularly for adj. EBITDA. We believe that the company’s ongoing strategy for improving operational efficiency could be reflected in this quarter. The company is expected to report Q3 results in the second week in November.

Enhancing efficiency. During the company’s Q2 earnings call, management highlighted its focus on efficiency in its user acquisition strategy. We believe the company’s efficient use of marketing spend, particularly in areas that provide sufficient returns, could indicate upside surprise potential for adj. EBITDA, not only from our estimate, but also the Street consensus which is $8.5 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Marie Tedesco to Retire as CFO Following Three Decades of Service

October 24, 2024 07:00 ET

NAPLES, Fla., Oct. 24, 2024 (GLOBE NEWSWIRE) — Beasley Broadcast Group, Inc. (Nasdaq: BBGI), a multi-platform media company, today announced the appointment of Lauren Burrows Coleman as Chief Financial Officer, effective Friday, November 1, 2024. Longtime CFO Marie Tedesco will retire from Beasley after 33 years of dedicated service to the company.

Before joining Beasley, Ms. Burrows Coleman served as Global Head of Strategic Corporate and Commercial Finance at Wayfair (NYSE: W), where she led a global team of 50 across Financial Planning & Analysis, Commercial Finance, Capital Markets, Corporate Development, and Global Tax functions.

Ms. Burrows Coleman’s impressive career also includes leadership positions at WindSail Capital Group and Wind Point Partners, both private equity firms, as well as GE Capital, where she managed equity and debt investments across various industries. She began her career as an investment banker in the Communications & Media group at Lehman Brothers.

“We are absolutely thrilled to welcome Lauren into the Beasley family,” said Caroline Beasley, Chief Executive Officer of Beasley Broadcast Group, Inc. “Her extensive and diverse experience, combined with her leadership skills, are exactly what we need to drive the company forward as we evolve into the future.”

Ms. Burrows Coleman holds an MBA from Harvard Business School and an A.B. cum laude from Dartmouth College.

She will succeed Marie Tedesco, who is retiring on November 1st after more than three decades with the organization.

“Marie has been an integral part of our success and her contributions have shaped the organization into what it is today,” said Caroline Beasley. “It has been a privilege to work alongside her, and we are deeply grateful for her unwavering commitment, hard work, and leadership. We will greatly miss Marie’s wisdom and guidance, and we wish her nothing but the very best!”

About Beasley Broadcast Group: Beasley Broadcast Group, Inc. (NASDAQ: BBGI) is a multi-platform media company whose primary business is operating radio stations throughout the United States. The Company offers local and national advertisers integrated marketing solutions across audio, digital and event platforms. The Company owns and operates stations in the following markets: Atlanta, GA, Augusta, GA, Boston, MA, Charlotte, NC, Detroit, MI, Fayetteville, NC, Fort Myers-Naples, FL, Las Vegas, NV, Middlesex, NJ, Monmouth, NJ, Morristown, NJ, Philadelphia, PA, and Tampa-Saint Petersburg, FL. Approximately 20 million consumers listen to the Company’s radio stations weekly over-the-air, online and on smartphones and tablets, and millions regularly engage with the Company’s brands and personalities through digital platforms such as Facebook, Twitter, text, apps and email. For more information, please visit www.bbgi.com.

Contact

Joseph Jaffoni, Jennifer Neuman JCIR (212) 835-8500 bbgi@jcir.com

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Steady as she goes. Third quarter results were in line with our estimates, with revenue of $20.1 million (down 2.4% year over year), versus our estimate of $20.9 million. Adj. EBITDA was $4.6 million (up 19.3% year over year), better than our estimate of $3.8 million by almost 21% due to lower than expected sales & marketing expenses.

Swing toward revenue growth. Advertising revenue was down slightly to $19.7 million from $20.0 million in Q2, with membership revenue up from $1.2 million in Q2 to $1.4 million in Q3. The membership revenue increase reflected improved subscriptions with Jack’s Flight Club, which was expanded into Canada.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.