CALGARY, AB, May 8, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces its financial and operating results for the three months ended March 31, 2025 and an updated 2025 capital budget following the successful completion of the strategic acquisition of Cardium light oil focused assets (the “Acquired Assets“) in the Pembina area of Alberta (the “Acquisition“) from Obsidian Energy Ltd. And certain of its affiliates (collectively “Obsidian“). InPlay’s condensed unaudited interim financial statements and notes, as well as Management’s Discussion and Analysis (“MD&A”) for the three months ended March 31, 2025 will be available at “www.sedarplus.ca” and on our website at “www.inplayoil.com“. All figures presented herein reflect the Company’s six (6) to one (1) share consolidation, which was effective April 14, 2025. An updated corporate presentation will be available on our website shortly.

First Quarter 2025 Highlights

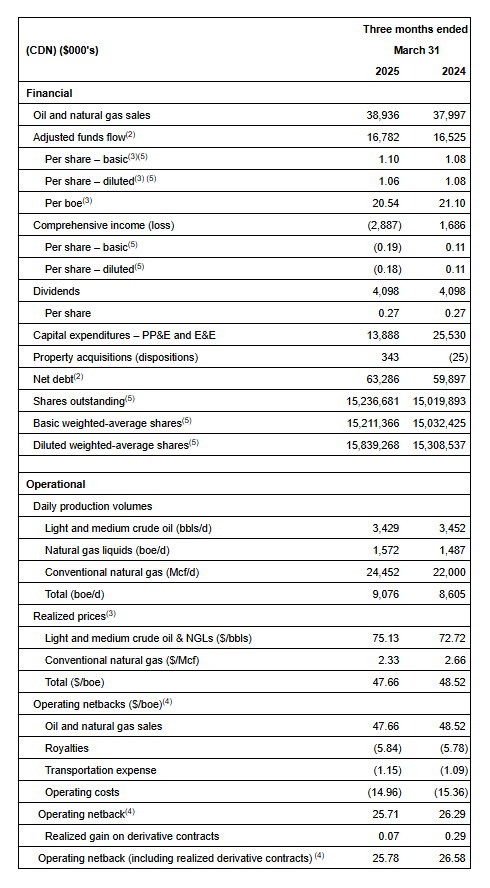

Achieved average quarterly production of 9,076 boe/d(1) (55% light crude oil and NGLs), a 5% increase over Q1 2024 and ahead of internal forecasts.

Generated strong quarterly Adjusted Funds Flow (“AFF”)(2) of $16.8 million ($1.10 per basic share(3)).

Returned $4.1 million to shareholders by way of monthly dividends, equating to a 16% yield relative to the current share price. Since November 2022 InPlay has distributed $44 million in dividends including dividends declared to date.

Maintained a strong operating income profit margin(3) of 54%.

Improved field operating netbacks(3) to $25.71/boe, an increase of 3% compared to Q4 2024.

First quarter results exceeded expectations, driven in part by the outperformance of newly drilled wells at Pembina Cardium Unit #7 (PCU#7). A two well pad delivered average initial production (“IP”) rates of 677 boe/d (75% light oil and NGLs) over the first 30 days and 492 boe/d (66% light oil and NGLs) over the first 60 days, both significantly above expectations. Over the initial two-month period, production from these wells was more than 100% above our type curve. These wells ranked in the top-ten for production rates for all Cardium wells in the basin for the month of March.

Complementing InPlay’s strong operational momentum, Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which started production mid quarter, are outperforming our internal type curve by approximately 50% with average IP rates of 304 boe/d (91% light oil and NGLs) over the first 30 days and 295 boe/d (85% light oil and NGLs) over the first 60 days. The remaining two wells, brought online in the final days of the first quarter, are performing more than 350% above our internal type curve, with average IP rates per well of 887 boe/d (88% light oil and NGLs) over their initial 30 day period.

The Company is very excited about the highly accretive Pembina Acquisition announced February 19, 2025 and had anticipated strong results from the combined assets. The exceptional results from the first quarter drilling program, combined with the outperformance of base production, have driven current field estimated production to approximately 21,500 boe/d (64% light oil and NGLs) significantly exceeding what we had initially forecasted at the announcement of the Acquisition. Given the current volatility in commodity prices, this material outperformance provides the Company with significant flexibility to scale back our capital program, providing “more for less” while maintaining our production forecasts, allowing for more aggressive debt repayment even in a lower pricing environment.

2025 Capital Budget and Associated Guidance

Following the closing of the highly accretive Acquisition on April 7, 2025, InPlay is pleased to provide initial pro forma guidance inclusive of the Acquired Assets. This guidance reflects the exceptional operational performance across the Company’s expanded asset base, while taking into account the current volatile commodity price environment. It also underscores InPlay’s continued commitment to maximizing free cash flow to support ongoing debt reduction, while positioning the Company to support its return to shareholder strategy.

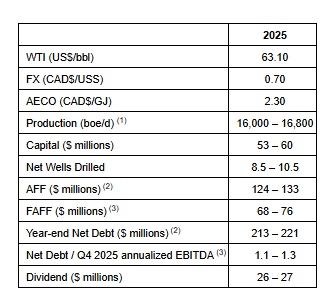

InPlay’s Board has approved an updated capital program of $53 – $60 million for 2025. InPlay plans to drill approximately 5.5 – 7.5 net Extended Reach Horizontal (“ERH”) Cardium wells over the remainder of the year. A significant portion of the remaining 2025 capital budget is expected to be directed toward the Acquired Assets, which (as outlined above) continue to materially outperform internally modelled type curves. Cost efficiencies realized through InPlay’s recent drilling program, combined with the application of InPlay’s drilling and completion techniques to the Acquired Assets, are expected to further enhance well economics. Capital will also be spent tying in certain InPlay assets into the newly acquired facilities, eliminating significant trucking costs, and marks the first step in our synergy cost savings strategy. Due to the outperformance of production across our asset base, InPlay has reduced total capital spending for the remainder of 2025 by approximately 30% (relative to initial expectations) without reducing production estimates.

Key highlights of the updated 2025 capital program include:

Production per Share Growth:

Forecasted average annual production of 16,000 – 16,800 boe/d(1) (60% – 62% light oil and NGLs), a 15% increase (based on mid-point) in production per weighted average share compared to 2024 despite 30% less capital spending than initially expected, driven by:

Lower corporate base decline rate of 24% due to the favorable decline profile of the Acquired Assets;

Improved corporate netbacks driven by the higher oil and liquids weighting of the Acquired Assets; and

Enhanced capital efficiencies from high graded drilling inventory of the pro forma assets.

FAFF Generation and Dividend Sustainability:

AFF(2) per weighted average share(4) of $5.00 – $5.35, a 13% increase (based on mid-point) compared to 2024.

Free adjusted funds flow (“FAFF”)(3) of $68 – $76 million equating to a 35% – 40% FAFF Yield(3), a 10x increase (based on mid-point) in FAFF per share compared to 2024 despite a 17% year over year reduction in forecasted WTI price.

Top Tier Returns:

Total return of 50% – 55% after combining FAFF Yield and production per share growth(4), which is expected to be at the high end of our peer group.

Debt Reduction:

Excess FAFF(3) is planned to be used to reduce debt.

Projected year-end Net Debt(2) of $213 – $221 million equating to a $31 – $39 million reduction from closing of the Acquisition.

Year-end Net Debt to Q4 2025 annualized EBITDA(3) ratio of 1.1x – 1.3x.

InPlay continues to monitor global trade and commodity dynamics, including United States tariffs on Canada. Capital spending will be weighted towards the back end of the year with drilling expected to resume again in August, providing ample time to finalize capital spending allocation depending on commodity pricing and continued asset performance. As a result of minimal capital spending in the second quarter, InPlay anticipates generating significant FAFF which will be directed to reducing debt. InPlay will remain flexible and will make decisions based on our core strategy of disciplined capital allocation, maintaining financial strength to ensure the long term sustainability of our strategy and return to shareholder program.

Updated 2025 Guidance Summary:

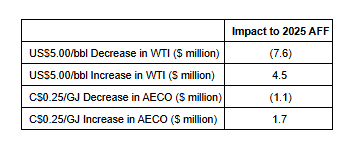

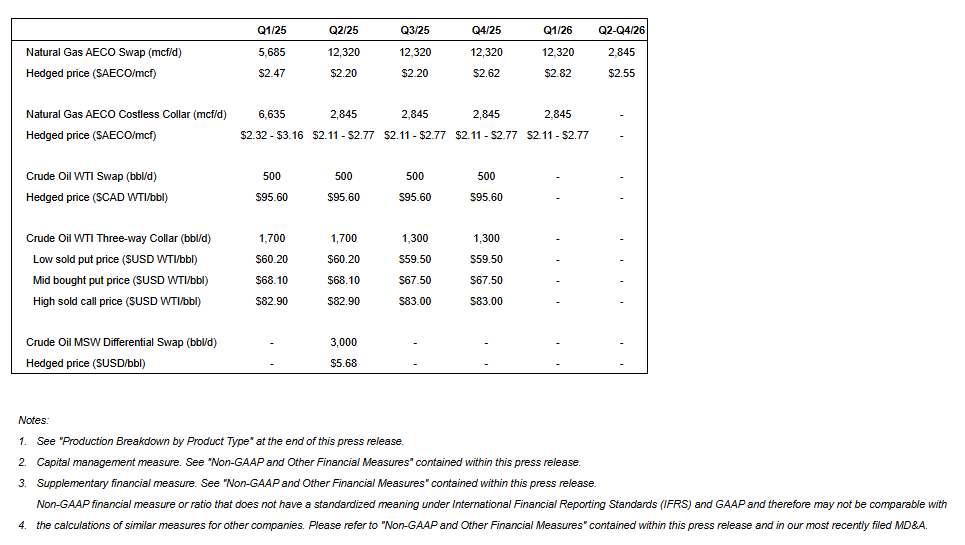

Following closing of the Acquisition, a significant hedging program was undertaken to help provide downside commodity price protection. As further detailed in the hedging summary section in this press release, InPlay has hedged approximately 75% of its net after royalty oil production and 67% of its net after royalty production on a BOE basis for the remainder of 2025. InPlay’s strong hedge book provides insulation to the current commodity price volatility which is highlighted in the sensitivity table below.

With low decline high netback assets, a flexible budget, a resilient balance sheet, and becoming a larger company, InPlay remains well positioned to sustainably navigate future commodity price cycles. Adhering to this disciplined strategy has allowed the Company to navigate previous commodity price cycles including the COVID-19 pandemic price environment.

Financial and Operating Results:

First Quarter 2025 Financial & Operations Overview:

The year has begun with strong momentum as production for the quarter exceeded internal forecasts, largely due to the outperformance of new ERH wells in PCU#7. Three (3.0 net) ERH wells were brought online at the end of February as part of a $13.9 million capital program, inclusive of $1.4 million invested in well optimization initiatives which continues to lower corporate declines. Production averaged 9,076 boe/d(1) (55% light crude oil and NGLs) in the quarter, a 5% increase from 8,605 boe/d(1) in the first quarter of 2024.

Notably, a two well pad drilled in PCU#7 exceeded expectations, delivering average IP rates of 677 boe/d (75% light oil and NGLs) and 492 boe/d (66% light oil and NGLs) per well over their first 30 and 60 days, respectively, which is over 100% above our internally modeled type curve for these wells.

Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which came on production mid quarter, are outperforming the internal type curve with IP rates averaging 304 boe/d (91% light oil and NGLs) and 295 boe/d (85% light oil and NGLs) over the first 30 and 60 days, respectively (approximately 50% above our internally modelled type curve). The last two wells were brought online in the final days of the quarter and are performing significantly above internal forecasts with IP rates averaging 887 boe/d (88% light oil and NGLs) per well over their first 30 days (more than 350% above our type curve).

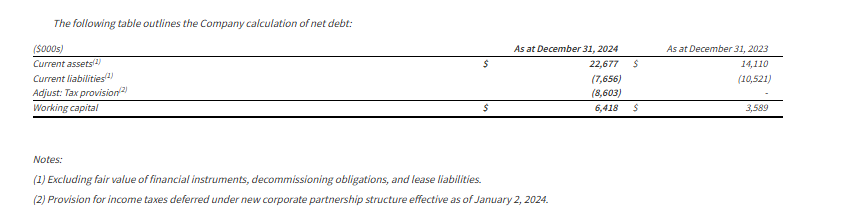

AFF for the quarter was $16.8 million. In addition, the Company returned $4.1 million ($0.09 per share) in base dividends to shareholders which equates to a yield of 16% based on the current share price. Net debt at quarter-end totaled $63 million, with a net debt to EBITDA ratio(3) of 0.8x, reflecting a healthy financial position.

On behalf of the entire InPlay team and the Board of Directors, we thank our shareholders for their continued support as we advance our strategy of disciplined growth, returns, and long-term value creation. We are excited to report our progress with respect to the strategic Acquisition.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Key Points: – Astec Industries will acquire TerraSource Holdings for $245 million in cash, expanding its scale, global reach, and aftermarket parts business. – Astec posted a 6.5% increase in net sales to $329.4 million and more than quadrupled net income to $14.3 million year-over-year. – The acquisition is expected to be earnings accretive from day one, with $10 million in expected run-rate synergies and a 5.9x adjusted EBITDA multiple.

Astec Industries (NASDAQ: ASTE) reported a robust start to the year, posting solid first-quarter earnings and announcing a definitive agreement to acquire TerraSource Holdings, LLC in a $245 million cash deal. The acquisition, expected to close in early Q3 pending regulatory approvals, will significantly expand Astec’s scale, aftermarket revenue, and presence in adjacent material processing markets.

The Tennessee-based manufacturer of infrastructure and materials processing equipment posted Q1 net sales of $329.4 million, a 6.5% increase from the same period last year. Net income surged to $14.3 million, or $0.62 per diluted share, from $3.4 million, or $0.15 per share, in the prior year. Adjusted net income came in at $20.3 million, or $0.88 per share, while adjusted EBITDA jumped 86% to $35.2 million. Free cash flow was reported at $16.6 million.

“We are pleased to report another strong quarter in line with our plans to deliver consistency, profitability, and growth,” said Astec CEO Jaco van der Merwe. “The TerraSource acquisition adds scale and accretive margins, opens access to new markets, and strengthens our aftermarket parts offering—all aligned with our disciplined growth strategy.”

TerraSource, a material processing equipment manufacturer with over $150 million in annual revenue, brings a robust aftermarket business to the table. Roughly 60% of its revenues and 80% of its gross profit are derived from aftermarket parts—a key area of focus for Astec as it looks to increase recurring revenue and margin stability.

Astec said the deal, financed through cash on hand and new committed financing, is expected to be accretive to earnings immediately. With expected run-rate synergies of $10 million within two years and tax benefits of approximately $15 million, the transaction represents an adjusted EBITDA multiple of 5.9x.

From a segment standpoint, Astec’s Infrastructure Solutions division led Q1 performance with $236 million in sales, up 16.7% year-over-year, benefiting from strong demand in road building and concrete plants. The Materials Solutions division, however, saw a 12.7% decline to $93.4 million due to softer domestic equipment sales, though dealer interest remained high.

CFO Brian Harris emphasized the financial strength behind the transaction, noting that “TerraSource enhances our financial profile with expanded margins and quality of earnings. The acquisition aligns with our strategy and positions us for long-term growth.”

Despite a 28% year-over-year drop in backlog—down to $402.6 million—Astec remains confident in its ability to convert new demand as infrastructure markets evolve and financing capacity improves across contractor and dealer channels.

The TerraSource acquisition adds meaningful scale and global reach for Astec, reinforcing its position as a top-tier provider of material and infrastructure solutions. The company is expected to maintain its adjusted EBITDA guidance of $105 million to $125 million for the full year, excluding the pending deal.

With strong financials, a growing aftermarket footprint, and a major acquisition in play, Astec is positioning itself for long-term gains amid rising global infrastructure needs. Investors responded favorably in early trading, with Astec shares ticking higher following the announcement

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Share consolidation. As of April 21, 2025, InPlay Oil shares are trading on a post-consolidation basis, with 27,939,437 common shares outstanding. The terms of the share consolidation were one post-consolidation common share per six pre-consolidation common shares. Fractional shares resulting from the consolidation were rounded down to the nearest whole number.

Updating estimates and price target. We are updating our 2025 estimates to reflect fewer shares outstanding and lower crude oil price estimates. For 2025, we are lowering our oil and gas revenue and earnings per share estimates to C$318.7 million and C$1.34, from C$333.5 million and C$1.46, both adjusted for the share consolidation. Moreover, we have lowered our adjusted funds flow (AFF) to C$149.5 million from C$161.6 million. We are maintaining our production estimate of 18,750 barrels of oil equivalent per day (boe/d) post the Pembina acquisition, which averages 15,816 boe/d for the full-year 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full-year 2024 financial results. Hemisphere Energy reported full-year net income and earnings per share of C$33.1 million and C$0.33, respectively, slightly above our estimates of C$32.3 million and C$0.32. The variance is mainly due to stronger oil pricing of $79.48, compared to our estimate of $76.31. Year-over-year, oil and natural gas revenue increased ~18% to C$79.7 million from C$67.7 million. This increase was driven by increased production and more robust pricing of 3,436 barrels of oil equivalent per day (boe/d) and $79.48, respectively, compared to 3,125 boe/d and $74.07. Likewise, adjusted funds flow (AFF) increased 16% in 2024 to C$45.8 million from C$39.4 million in 2023. We had forecast AFF of C$45.4 million.

Updating estimates. Based on lower crude oil price estimates, we are lowering our 2025 net income and earnings per share estimates to C$30.3 million and C$0.29, respectively, from C$37.2 million and C$0.37. Additionally, we are decreasing our adjusted funds flow estimate to C$42.9 million from C$50.6 million. We are maintaining our 2025 average daily production estimate of 3,900 boe/d, an increase of ~14% over 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Vancouver, British Columbia–(Newsfile Corp. – April 17, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the fourth quarter and year ended December 31, 2024.

2024 Highlights

Increased annual production by 10% to a record of 3,436 boe/d (99% heavy oil).

Generated annual revenue of $99.9 million, an 18% increase over the previous year.

Achieved a 16% increase in annual adjusted funds flow from operations (“AFF”)(1) to $45.8 million.

Invested $22 million to drill nine wells, upgrade facilities, and purchase land at Atlee Buffalo in Alberta, as well as drill five wells (three production wells and two injection wells) and build the facilities required to test a pilot polymer flood at Marsden, Saskatchewan.

Generated $23.9 million of annual free funds flow (“FFF”)(1), a 6% increase over annual FFF reported for 2023.

Achieved robust operating and transportation costs of $15.60/boe.

Distributed $9.8 million in quarterly base dividends to shareholders during the year.

Distributed $5.9 million in special dividends to shareholders during the year.

Purchased and cancelled 3.4 million shares at an average price of $1.62 per share under the Company’s normal course issuer bid (“NCIB”), returning $5.5 million to shareholders during the year.

Exited 2024 with a positive working capital(1) position of $6.4 million compared to $3.6 million at December 31, 2023.

Note: (1)Non-IFRS financial measure that is not a standardized financial measure under International Financial Reporting Standards (“IFRS”) and may not be comparable to similar financial measures disclosed by other issuers. Refer to “Non-IFRS and Other Financial Measures” section below.

Financial and Operating Summary

Selected financial and operational highlights should be read in conjunction with Hemisphere’s audited consolidated financial statements and related Management’s Discussion and Analysis for the year ended December 31, 2024. These reports, including the Company’s Annual Information Form for the year ended December 31, 2024, are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Operations Update and Outlook

2024 marked another strong year for Hemisphere, with record production levels of over 3,400 boe/d (99% heavy oil), near record AFF of $45.8 million, record shareholder returns of over $21 million ($0.21/share) through dividends and share buybacks, and an increase in its net cash position at year end to $6.4 million. The Company’s first quarter 2025 field estimated production has since grown to 3,800 boe/d (99% heavy oil) through continued success of its polymer floods, despite no new wells being drilled since the third quarter of 2024.

Given the strong financial position and performance outlook of the Company, Hemisphere recently announced a special dividend of C$0.03 per common share to be paid on April 28, 2025 to shareholders of record on April 17, 2025. In 2024, Hemisphere’s total dividend payments to shareholders of C$0.16 per common share included two special dividends of C$0.03 per common share (in each of July and November), in addition to the base annual dividend of C$0.10 per common share. These special dividends are an important part of Hemisphere’s overall shareholder return model.

As seen over the first two weeks of April, pricing outlook for the oil market is experiencing significant volatility influenced by geopolitical developments, supply-demand dynamics, and trade tensions. Hemisphere’s 2025 budget is extremely flexible with minimal capital spending planned until summer. The Company’s robust balance sheet, ultra-low decline assets, and limited sustaining capital requirements for 2025 position Hemisphere well to withstand these economic headwinds.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-Looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements that a special dividend will be paid to shareholders on April 28, 2025 to shareholders of record on April 17, 2025; Hemisphere’s intention to have minimal capital spending until summer; and the Company’s view that its robust balance sheet, ultra-low decline assets, and limited sustaining capital requirements for 2025 position Hemisphere well to withstand economic headwinds.

Forward‐Looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; current budgets; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; trade and tariff matters, including the impacts on costs and supply chains; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, changes in Hemisphere’s budget, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

This MD&A contains the terms adjusted funds flow from operations, free funds flow, operating field netback and operating netback, capital expenditures and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

a)Adjusted funds flow from operations “AFF“ (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for tax provision and decommissioning expenditures, and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculatedusing the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

b)Free funds flow (“FFF”) (Non-IFRS Financial Measures): Calculated by taking adjusted funds flow and subtracting capital expenditures, excluding acquisitions and dispositions. Management believes that free funds flow provides a useful measure to determine Hemisphere’s ability to improve returns and to manage the long-term value of the business.

c)Capital Expenditures (Non-IFRS Financial Measure): Management uses the term “capital expenditures” as a measure of capital investment in exploration and production assets, and such spending is compared to the Company’s annual budgeted capital expenditures. The most directly comparable IFRS measure for capital expenditures is cash flow used in investing activities. A summary of the reconciliation of cash flow used in investing activities to capital expenditures is set forth below:

d)Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): A benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses, and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e)Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): Calculated as the operating field netback plus the Company’s realized gain (loss) on derivative financial instruments on an absolute and per barrel of oil equivalent basis.

f)Working capital/Net debt (Non-IFRS Financial Measure): Closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding derivative financial instruments, decommissioning obligations, and lease liabilities, adjusted for tax provision and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

g)Supplementary Financial Measures and Ratios

“Adjusted Funds Flow from operations per basic share” is comprised of funds from operations divided by basic weighted average common shares. “Adjusted Funds Flow from operations per diluted share” is comprised of funds from operations divided by diluted weighted average common shares. “Annual Free Funds Flow” is comprised of free funds flow from the current three-month period multiplied by four. “Operating expense per boe” is comprised of operating expense, as determined in accordance with IFRS, divided by the Company’s total production. “Realized heavy oil price” is comprised of heavy crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. “Realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. “Realized combined price” is comprised of total commodity sales from production, as determined in accordance with IFRS, divided by the Company’s total production. “Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the Company’s total production. “Transportation costs per boe” is comprised of transportation expenses, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2024, which is available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to initial production rates (including as a result of recent water or polymer flood activities) are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

WCS

Western Canadian Select

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Mboe

thousand barrels of oil equivalent

C$

Canadian Dollar

MMboe

million barrels of oil equivalent

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transformative acquisition closed. InPlay Oil recently closed its acquisition of Cardium light oil focused assets in the Pembina area of Alberta from Obsidian Energy for net consideration of approximately $301 million. The transaction more than doubles InPlay’s total output to 18,750 barrels of oil equivalent per day (boe/d). The assets are 68% weighted in oil and natural gas liquids (NGLs) and have a low decline rate of 22%. Management expects greater production, a lower decline rate, and enhanced operational efficiency. Following the completion of the acquisition, InPlay had 167,636,627 shares issued and outstanding.

Share consolidation. Effective April 14, InPlay will implement a share consolidation based on one common share for six common shares. The consolidation was unanimously approved by the company’s board and by 96.56% of the votes cast during a special meeting of shareholders. Post-consolidation, InPlay will have approximately 27,939,438 common shares issued and outstanding. The shares are expected to begin trading on a post-consolidation basis two to three trading days following the effective date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY AB, April 7, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) is pleased to announce that it has closed the previously announced strategic acquisition of Cardium light oil focused assets in the Pembina area of Alberta (the “Acquired Assets“) from Obsidian Energy Ltd. (the “Vendor“) for net consideration of approximately $301 million (the “Acquisition“).

The highly accretive Acquisition was funded by a combination of net proceeds released to InPlay pursuant to its previously announced $32.8 million bought deal subscription receipt financing (the “Financing“), an amended $330 million credit facility with a $190 million revolving credit facility, a letter of credit facility of up to $30 million, a fully drawn $110 million two-year amortizing term loan and the issuance of 54,838,709 InPlay common shares to the Vendor at a deemed price of $85 million or $1.55 per share (the “Share Consideration“). The Share Consideration is subject to a six-month lock up period, which may be shortened in certain circumstances.

In accordance with their terms, each one (1) subscription receipt issued pursuant to the Financing was automatically exchanged for one (1) InPlay Share concurrently with the completion of the Acquisition, and the net proceeds were released to InPlay from escrow and used to fund a portion of the cash consideration payable to the Vendor under the Acquisition. Previous holders of subscription receipts of InPlay are not required to take any action to receive the underlying InPlay Shares. Trading in the subscription receipts on the Toronto Stock Exchange is expected to be halted today and the subscription receipts delisted in due course.

Immediately following completion of the Acquisition, InPlay has 167,636,627 InPlay Shares issued and outstanding, inclusive of the underlying 21,145,625 InPlay Shares issued upon conversion of subscription receipts previously issued pursuant to the Financing and the Share Consideration issued to the Vendor.

Concurrent with completion of the Acquisition, InPlay entered into an amended and restated credit agreement with a syndicate of lenders (the “Lenders“) pursuant to which the aggregate available borrowing capacity under InPlay’s Senior Credit Facility has been increased from $110 million to $330 million by way of an increased $190 million revolving credit facility with a term out date extended to June 30, 2026, a fully drawn $110 million two-year amortizing term loan (the “Term Loan“) and a letter of credit facility of up to $30 million. The Term Loan includes quarterly amortization payments of $4.1 million. The covenant and security package under the new Term Loan is substantially the same as the revolving credit facility, with the exception of an additional affirmative covenant to satisfy certain prescribed hedging requirements during the period the Term Loan remains outstanding.

In accordance with a shareholder rights agreement between InPlay and the Vendor, the Vendor nominated Stephen E. Loukas, President and Chief Executive Officer and Peter D. Scott, Senior Vice President and Chief Financial Officer, both of Obsidian Energy Ltd., for election to the InPlay Board of Directors at the Special Meeting. Both nominees were elected as directors of InPlay to serve until the next annual meeting of shareholders or until their successors are elected or appointed. The Vendor nominees have agreed to support the resolutions brought before InPlay shareholders at the 2025 annual general meeting of shareholders.

Reader Advisories

Forward-Looking Information and Statements

This document contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this document contains forward-looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives; light crude oil and NGLs weighting estimates; expectations regarding future commodity prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures; the amount and timing of capital projects; and methods of funding our capital program.

The internal projections, expectations, or beliefs underlying our Board approved 2025 capital budget and associated guidance are subject to change in light of, among other factors, changes to U.S. economic, regulatory and/or trade policies (including tariffs), the impact of world events including the Russia/Ukraine conflict and war in the Middle East, ongoing results, prevailing economic circumstances, volatile commodity prices, and changes in industry conditions and regulations. InPlay’s 2025 financial outlook and revised guidance provides shareholders with relevant information on management’s expectations for results of operations, excluding any potential acquisitions or dispositions, for such time periods based upon the key assumptions outlined herein. Readers are cautioned that events or circumstances could cause capital plans and associated results to differ materially from those predicted and InPlay’s revised guidance for 2025 may not be appropriate for other purposes. Accordingly, undue reliance should not be placed on same.

Forward-looking statements or information are based on a number of material factors, expectations or assumptions of InPlay which have been used to develop such statements and information, but which may prove to be incorrect. Although InPlay believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because InPlay can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current U.S. economic, regulatory and/or trade policies; the impact of increasing competition; the general stability of the economic and political environment in which InPlay operates; the timely receipt of any required regulatory approvals; the ability of InPlay to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which InPlay has an interest in to operate the field in a safe, efficient and effective manner; the ability of InPlay to obtain debt financing on acceptable terms; the anticipated tax treatment of the monthly base dividend; that other than the tariffs that came into effect on March 4, 2025 (some of which were subsequently paused on March 6, 2025), neither the U.S. nor Canada (i) increases the rate or scope of such tariffs (if they come into effect in the future), or imposes new tariffs, on the import of goods from one country to the other, including on oil and natural gas, and/or (ii) imposes any other form of tax, restriction or prohibition on the import or export of products from one country to the other, including on oil and natural gas; the potential scope and duration of tariffs, export taxes, export restrictions or other trade actions; magnitude and duration of potential new or increased tariffs may be imposed on goods imported from Canada into the United States, which could adversely impact InPlay’s revenues; the potential for new and increased U.S. tariffs and protectionist trade measures on Canadian oil and gas imports; changes in political and economic conditions, including risks associated with tariffs, export taxes, export restrictions or other trade actions; impacts of any tariffs imposed on Canadian exports into the United States by the Trump administration and any retaliatory steps taken by the Canadian federal government; that InPlay’s results and operations could be adversely affected by economic or geopolitical developments, including protectionist trade policies such as tariffs, or other events; conditions in international markets, including social and political conditions, civil unrest, terrorist activity, governmental changes, restrictions on the ability to transfer capital across borders, tariffs and other protectionist measures; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and the ability of InPlay to secure adequate product transportation; future commodity prices; that various conditions to a shareholder return strategy can be satisfied; the ongoing impact of the Russia/Ukraine conflict and war in the Middle East; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which InPlay operates; and the ability of InPlay to successfully market its oil and natural gas products.

Without limitation of the foregoing, readers are cautioned that the Company’s future dividend payments to shareholders of the Company, if any, and the level thereof will be subject to the discretion of the Board of Directors of InPlay. The Company’s dividend policy and funds available for the payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to pay dividends will be subject to applicable laws, including satisfaction of solvency tests under the Business Corporations Act (Alberta), and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness. Further, the actual amount, the declaration date, the record date and the payment date of any dividend are subject to the discretion of the InPlay Board of Directors. There can be no assurance that InPlay will pay dividends in the future.

The forward-looking information and statements included herein are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); the risk that the Pembina Cardium asset acquisition may not be completed on the anticipated terms or timing; risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for InPlay’s products and/or otherwise adversely affects InPlay, or lead to the termination of InPlay’s financing arrangements for the Pembina Cardium asset acquisition, including specifically that the imposition of tariffs or similar measures in excess of 10% would be an adverse tariff event for the purposes of InPlay’s new credit facilities to be entered into in connection with the transaction and that the lenders thereunder may choose not to fund the transaction; the continuing impact of the Russia/Ukraine conflict and war in the Middle East; potential changes to U.S. economic, regulatory and/or trade policies as a result of a change in government; inflation and the risk of a global recession; changes in our planned 2025 capital program; changes in our approach to shareholder returns; changes in commodity prices and other assumptions outlined herein; the risk that dividend payments may be reduced, suspended or cancelled; the potential for variation in the quality of the reservoirs in which InPlay operates; changes in the demand for or supply of InPlay’s products; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans or strategies of InPlay or by third party operators of InPlay’s properties; changes in InPlay’s credit structure, increased debt levels or debt service requirements; inaccurate estimation of InPlay’s light crude oil and natural gas reserve and resource volumes; limited, unfavorable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in InPlay’s continuous disclosure documents filed on SEDAR+ including InPlay’s Annual Information Form dated March 27, 2024 and the annual management’s discussion & analysis for the year ended December 31, 2024.

This document contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about InPlay’s financial and leverage targets and objectives, potential dividends, and beliefs underlying our Board approved 2025 capital budget and associated guidance, all of which are subject to the same assumptions, risk factors, limitations, and qualifications as set forth in the above paragraphs. The actual results of operations of InPlay and the resulting financial results will likely vary from the amounts set forth in this document and such variation may be material. InPlay and its management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s reasonable estimates and judgments. However, because this information is subjective and subject to numerous risks, it should not be relied on as necessarily indicative of future results. Except as required by applicable securities laws, InPlay undertakes no obligation to update such FOFI. FOFI contained in this document was made as of the date of this document and was provided for the purpose of providing further information about InPlay’s anticipated future business operations and strategy. Readers are cautioned that the FOFI contained in this document should not be used for purposes other than for which it is disclosed herein.

The forward-looking information and statements contained in this document speak only as of the date hereof and InPlay does not assume any obligation to publicly update or revise any of the included forward-looking statements or information, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Risk Factors to FLI

Risk factors that could materially impact successful execution and actual results of the Company’s 2025 capital program and associated guidance and estimates include:

risks related to an international trade war, including the risk that the U.S. government imposes additional tariffs on Canadian goods, including crude oil and natural gas, and that such tariffs (and/or the Canadian government’s response to such tariffs) adversely affect the demand and/or market price for the Company’s products and/or otherwise adversely affects the Company;

volatility of petroleum and natural gas prices and inherent difficulty in the accuracy of predictions related thereto;

the extent of any unfavourable impacts of wildfires in the province of Alberta.

changes in Federal and Provincial regulations;

the Company’s ability to secure financing for the Board approved 2025 capital program and longer-term capital plans sourced from AFF, bank or other debt instruments, asset sales, equity issuance, infrastructure financing or some combination thereof; and

those additional risk factors set forth in the Company’s MD&A and most recent Annual Information Form filed on SEDAR+.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President, Business Development, InPlay Oil Corp., Telephone: (587) 893-6804

Vancouver, British Columbia–(Newsfile Corp. – April 3, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to announce that its board of directors has approved the declaration of a special dividend to shareholders.

Special Dividend

Given the strong financial position and performance outlook of the Company, Hemisphere’s board of directors has approved the declaration of a special dividend of C$0.03 per common share, in accordance with its dividend policy. The special dividend will be paid on April 28, 2025, to shareholders of record on April 17, 2025, and is designated as an eligible dividend for Canadian income tax purposes. It is in addition to the Company’s quarterly base dividend of C$0.025 per common share.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood EOR methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation, or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a special dividend will be paid to shareholders on April 28, 2025, to shareholders of record on April 17, 2025.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the timing for payment of the special dividend; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in project timelines and workstreams; changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Reserve report. Hemisphere released results from its independent reserve evaluation as of December 31, 2024. Compared to the year-end 2023 reserve report, proved developed producing (PDP) reserves increased 13.1% to 9,302.2 thousand barrels of oil equivalents. The growth in PDP reserves replaced 186% of 2024 production. Hemisphere’s estimated 2024 capital expenditures of ~C$22 million funded PDP reserve growth, annual production growth of ~10%, additional infrastructure, and the testing of a new resource play in Saskatchewan with an enhanced oil recovery (EOR) polymer pilot project.

Outlook for 2025.Hemisphere expects 2025 capital expenditures of ~C$17 million which are expected to support ~15% growth in annual average production to 3,900 barrels of oil equivalent per day (boe/d) compared to 2024. Most of the capital will be allocated to drilling, optimization, and facility work, with ~10% allotted to exploration and land acquisition. The majority of the planned expenditures are scheduled for the third quarter of 2025, providing the company with the flexibility to adjust plans based on changes in commodity prices.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VIRGINIA CITY, NEVADA, March 19, 2025 – Comstock Inc. (NYSE: LODE) (“Comstock,” “our” and the “Company”), today announced its 2025 Annual Meeting of shareholders will be held online May 22, 2025 in a virtual-only format via webcast.

Comstock shareholders as of the record date of March 25, 2025, can participate in the online annual meeting, including to vote their shares electronically and/or submit questions during the meeting. The Company’s proxy statement will be sent to shareholders of record and will describe the matters to be voted upon.

Electronic entry to the meeting will begin at 8:45 a.m. PDT / 11:45 a.m. EDT and the meeting will begin promptly at 9:00 a.m. PDT / 12:00 p.m. EDT.

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies that are deployable across entire industries to contribute to energy abundance by efficiently extracting and converting under-utilized natural resources, such as waste and other forms of woody biomass into renewable fuels, and end-of-life electronics into recovered electrification metals. Comstock’s innovations group is also developing and using artificial intelligence technologies for advanced materials development and mineral discovery for sustainable mining. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: RB Milestone Group LLC Tel (203) 487-2759 ir@comstockinc.com

For media inquiries or questions: Comstock Inc., Tracy Saville Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future market conditions; future explorations or acquisitions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; business opportunities, growth rates, future working capital, needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; operational or technical difficulties in connection with exploration, metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious and other metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; challenges to, or potential inability to, achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology and efficacy, quantum computing and generative artificial intelligence supported advanced materials development, development of cellulosic technology in bio-fuels and related material production; commercialization of cellulosic technology in bio-fuels and generative artificial intelligence development services; ability to successfully identify, finance, complete and integrate acquisitions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

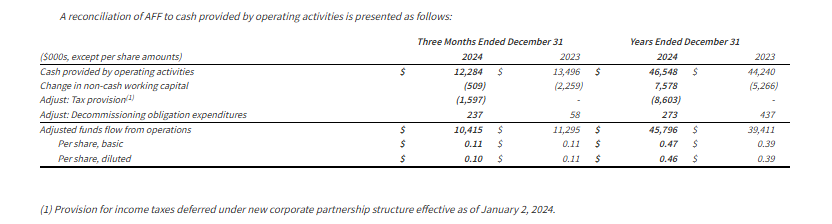

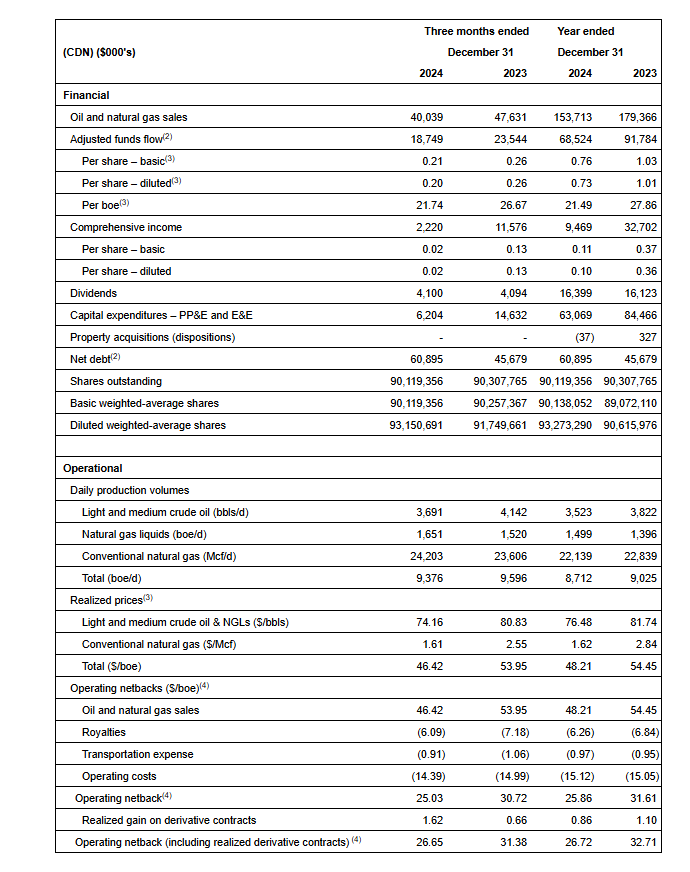

Full-year 2024 financial results. InPlay Oil reported full-year net income and earnings per share of C$9.5 million and C$0.10, respectively, below our estimates of approximately C$11.4 million and C$0.12. The variance was primarily due to lower-than-expected natural gas revenue driven by weaker AECO pricing. Production for the year averaged 8,712 barrels of oil equivalent per day (boe/d) compared to 9,025 boe/d in 2023. Consequently, revenue decreased to C$153.7 million compared to C$179.4 million in 2023. Adjusted funds flow in 2024 was C$68.5 million, down from C$91.8 million in 2023.

Updated 2025 estimates. Please note that our revised estimates assume the closing of the pending Pembina acquisition on April 15th, 2025. For 2025, our oil and gas revenue estimate is C$333.5 million compared to our prior estimate of C$159.4 million. We have raised our 2025 AFF and EPS estimates to C$161.6 million and C$0.27, respectively, from C$71.7 million and C$0.14. We forecast net income of C$40.9 million, up from our previous estimate of C$13.2 million. Our 2025 estimates are based on an average annual production of 15,879 boe/d compared to our prior forecast of 8,901 boe/d.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

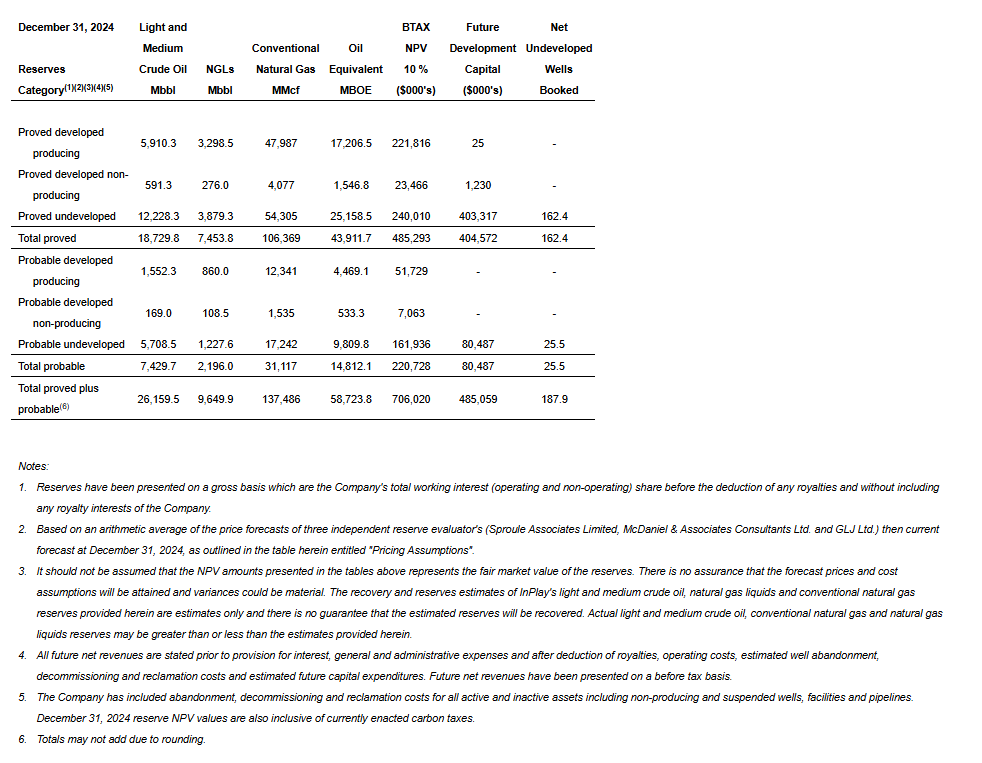

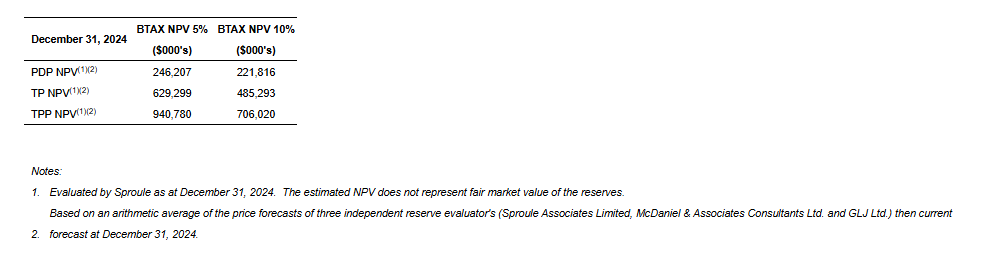

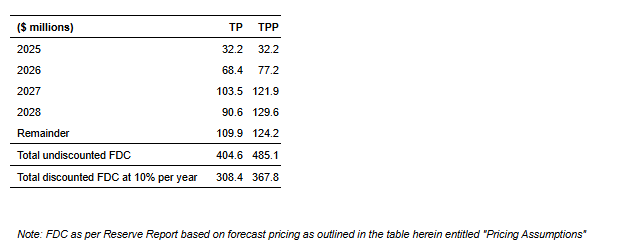

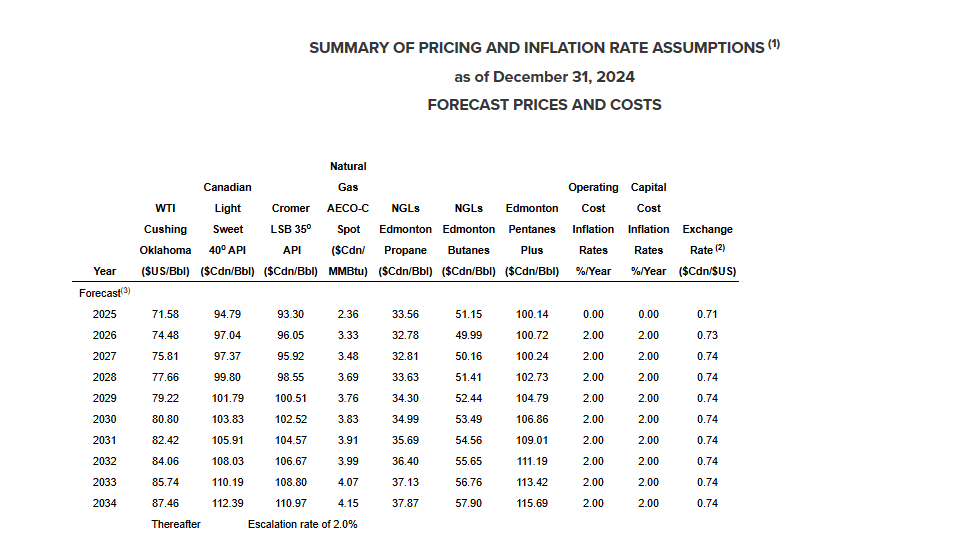

CALGARY, AB, March 14, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three and twelve months ended December 31, 2024, along with the results of its independent oil and gas reserves evaluation effective December 31, 2024 (the “Reserve Report”) prepared by Sproule Associates Limited (“Sproule”). InPlay’s audited annual financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2024 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated presentation will be available after closing of the Pembina Cardium asset acquisition which is expected in April.

Message to Shareholders:

The upcoming year is set to be a transformational year for InPlay. We believe that the highly accretive acquisition of Pembina Cardium assets from Obsidian Energy Ltd. announced on February 19, 2025 will fundamentally shift the future of the Company. The acquired assets strategically complement InPlay’s existing holdings in the Pembina Cardium, an area where the Company has proven operational expertise. The acquisition will significantly expand our operational scale, with attributes including large oil in place, a higher oil weighting, strong netbacks, low decline rates and a robust inventory of high-quality drilling locations, enhancing our overall sustainability. This is expected to strengthen free adjusted funds flow (“FAFF”)(4) generation, allowing for debt reduction while supporting our shareholder return strategy, with over three times FAFF coverage of our existing base dividend (11.3%) expected for 2025. We are excited to begin operations of these newly acquired assets acquired in this synergistic acquisition and to demonstrate our expertise and ability to unlock the intrinsic value of our share price. We will remain committed to financial discipline maintaining our strong balance sheet, to ultimately generate shareholder value through FAFF growth and return of capital to shareholders.

The resumption of development of our Pembina Cardium Unit # (“PCU7”) asset was a key highlight in 2024. This area is our most prolific asset as it offers high production rates and lower declines. As a result of significantly improved capital costs, PCU7 yields the highest returns and strongest capital efficiencies in our current asset portfolio. Our 2024 development of PCU7 exceeded internal expectations. Operational enhancements since our last PCU7 drilling program in spring of 2022 resulted in costs 25% below budget. These new techniques can be leveraged across our Cardium asset base, including those acquired as part of the Pembina Cardium asset acquisition. Three additional 100% PCU7 extended reach horizontal (“ERH”) wells were drilled in the first quarter of 2025 and recently brought on production.

During 2024, InPlay remained focused on operational execution, disciplined capital allocation and prioritizing FAFF while preserving a strong balance sheet which resulted in adjusting our operational and capital activities accordingly. InPlay’s disciplined approach allowed the Company to capitalize on the transformational Pembina Cardium asset acquisition.

Following closing of the Pembina Cardium asset acquisition, InPlay will provide updated development plans and revised full-year 2025 guidance. The acquisition is currently expected to close in April 2025.

2024 was a year of disciplined execution, operational efficiency, and delivering shareholder returns. We remain focused on financial strength, sustainable production, and value creation for our shareholders. As we move into 2025, we believe the Pembina Cardium asset acquisition positions InPlay for significant growth and long-term success. On behalf of our employees, management team and Board of Directors, we would like to thank our shareholders for their support.

2024 Financial and Operating Results:

Achieved average annual production of 8,712 boe/d(1) (58% light crude oil and NGLs) with fourth quarter production average of 9,376 boe/d(1) (57% light crude oil and NGLs).

Generated adjusted funds flow (“AFF”)(2) of $68.5 million ($0.76 per basic share(3)) despite a 44% drop in AECO natural gas prices compared to 2023.

Distributed $16.4 million in dividends, equating to a 10.4% yield relative to year-end market capitalization. Since November 2022, total dividends distributed amounted to $39.2 million ($0.435 per share, including dividends declared to date in 2025).