Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Listing requirements not met. The company initially received a notification that it was not in compliance with the Nasdaq’s minimum stockholder equity requirement in October 2024. The company subsequently submitted a plan to regain compliance in February 2025 and was granted an extension until April 16, 2025. However, on April 16, the company had not regained compliance and received a letter of determination from Nasdaq on April 17.

Letter of determination. The letter of determination stated the company did not meet the terms of its extension, due to a noncomplete capital raise that was laid out in its plan to regain compliance, and ultimately did not meet the stockholders’ equity requirement. We believe that the company is working on capital raising initiatives, which should put the company back in compliance. The Class A Common stock is scheduled to be suspended from trading at market open on April 28. The company has filed for a hearing which should delay the delisting process for at least 35 days.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Stocks and the U.S. dollar dropped as markets reacted to Trump’s threat to remove Fed Chair Jerome Powell. – Concerns over Fed independence sparked a flight from U.S. assets into gold and foreign bonds. – Investors fear increased volatility, weakening confidence in the dollar and U.S. monetary policy.

On Monday, April 21, 2025, U.S. financial markets experienced significant volatility following President Donald Trump’s renewed criticism of Federal Reserve Chair Jerome Powell. Trump’s public suggestion that he may attempt to remove Powell has heightened concerns about political interference in monetary policy — a cornerstone of market confidence. The S&P 500 dropped over 1%, while the Bloomberg Dollar Index fell to a 15-month low. Treasury yields jumped, pushing the 10-year above 4.4%, reflecting the market’s unease with rising inflation risk and a potentially less independent Fed.

At the same time, investors poured into safe-haven assets. Gold surged to a record above $3,400 an ounce, while the Swiss franc and Japanese yen rallied. The sharp movements signal not just a knee-jerk reaction to headlines, but deeper anxiety over the future of monetary policy. Analysts have warned that undermining the Fed’s credibility could cause long-term damage to the dollar’s global reserve status and complicate the central bank’s ability to steer the economy during periods of stress.

Markets are now on edge over the prospect of a politicized Federal Reserve. National Economic Council Director Kevin Hassett confirmed that Trump is reviewing the legality of removing Powell — a move seen by many as extreme and historically unprecedented. While legal scholars argue the president lacks the authority to fire the Fed Chair without cause, the noise alone has proven enough to shake investor confidence. Fed officials have maintained a measured tone, but Chicago Fed President Austan Goolsbee warned over the weekend that undermining central bank independence is a dangerous path.

For small and micro-cap investors, the ripple effects are particularly pronounced. These companies typically have tighter margins, higher debt costs, and fewer international buffers than large-cap peers. In a rising rate or inflationary environment — or worse, one with erratic policy signals — smaller firms can see financing dry up and market multiples compress rapidly. Investors focused on this space should be watching both policy headlines and macroeconomic indicators closely, as volatility may linger longer than anticipated.

Adding to market pressure, geopolitical tensions have grown. Reports that Chinese investors are reducing U.S. Treasury holdings in favor of European and Japanese debt point to an early-stage shift in global capital allocation. If trust in U.S. governance continues to erode, further capital outflows could strain markets even more. At the same time, the White House’s ongoing tariff disputes are reshaping trade routes and disrupting sectors from tech to commodities. All of this contributes to an environment where capital seeks safety — and where policymaker credibility is paramount.

This shifting market sentiment could have meaningful implications for small-cap stocks, particularly those tracked by the Russell 2000. As investors rotate away from large-cap tech and U.S. dollar-denominated assets, the Russell’s reconstitution later this year may spotlight high-quality domestic companies with strong fundamentals and less exposure to geopolitical volatility. For savvy investors, this uncertainty could ultimately shine a light on overlooked small-cap opportunities poised to benefit from changing capital flows and renewed interest in U.S.-focused growth stories.

The small-cap sector has taken it on the chin in recent months, with widespread fear and macro uncertainty fueling a broad selloff that’s left many fundamentally solid companies trading at multi-year lows. While this environment has caused plenty of investors to retreat to the safety of larger, more liquid names, it’s also creating potential opportunities for those with a longer-term mindset.

The Russell 2000, which tracks small-cap performance, has declined steeply this year—reflecting the risk-off tone in the market. But with this pullback comes the chance to scoop up high-quality businesses at a steep discount to their intrinsic value. Historically, moments of panic often set the stage for future gains, especially in the small-cap space where sentiment tends to swing more dramatically. Right now, the indiscriminate nature of the selling has created an environment where price and value have diverged, opening the door for patient investors to build positions in companies that have been unfairly punished.

One such example is NN, Inc. (NNBR), a precision manufacturing company that operates in sectors like automotive and medical, offering highly engineered solutions. Back in December, the stock was trading around $4, but it has since dropped to roughly $1.73. While that kind of decline might suggest something is seriously broken, the business itself continues to pursue operational improvements and efficiency gains. The company has made progress in reducing debt and focusing its portfolio, and though headwinds remain, the market appears to be pricing in a worst-case scenario. For investors who believe in industrial recovery and the power of long-term restructuring, NNBR may represent deep value.

Another name that’s been dragged down in the recent slide is 1-800-Flowers.com (FLWS). In December, this online retailer was trading near $9 per share. Fast forward to today, and it’s sitting around $5.20. Despite the decline, the underlying business remains healthy. The company continues to benefit from strong seasonal demand, and its ability to cross-sell across its various gifting platforms—ranging from floral to gourmet foods—gives it a unique edge in the e-commerce space. As consumer habits shift further toward online shopping and direct-to-door services, 1-800-Flowers stands to be a long-term winner. The current pullback may have more to do with general retail fatigue and market fear than any material weakness in the business itself.

Conduent (CNDT) rounds out the list, trading at just $2 after closing last year around $4.39. Specializing in business process outsourcing and digital workflow solutions for both government and commercial clients, Conduent has a significant contract base and recurring revenue streams that provide a level of stability often overlooked in smaller tech-enabled firms. While the company has faced its share of execution challenges, it continues to win contracts and drive efficiency through restructuring efforts. If management continues to make progress and market sentiment shifts even slightly, CNDT could see meaningful upside from these levels.

In volatile times like these, it’s easy to let fear cloud judgment. But for investors who can see past short-term noise, the current small-cap selloff may offer a rare opportunity to buy good companies on sale.

The current market sentiment is one of extreme fear, with widespread selling across many small-cap stocks, especially those in the Russell 2000 index. A variety of factors, including tariffs and broader market uncertainty, have led to this wholesale selling, and as a result, many fundamentally strong small companies are being punished. However, for those willing to take a closer look, this fear-induced market drop may present some excellent investment opportunities.

On Friday, the Russell 2000 was down 27%, a sharp decline that reflects how smaller companies, particularly those in this index, are feeling the brunt of the market’s volatility. The Russell 2000 is made up of small-cap companies, which are inherently more volatile and have less liquidity than larger companies. As a result, they tend to experience more extreme price swings in response to broader market movements. This has created a situation where many small-cap stocks are now trading at huge discounts.

Take, for example, FreightCar America (RAIL). Just last December, this stock was trading at around $14. Now, it’s hovering around $4.50. Despite the severe decline, this is a stock that is fundamentally sound. The company is exempt from tariffs, has improved its financials with a successful refinancing deal in December, and has a solid business model. Yet, the stock continues to trade lower because of the broader market selloff affecting the Russell 2000 ETF. This creates a disconnect between the company’s true value and its current price.

Similarly, Graham (GHM), a defense manufacturer, was trading at $52 just a few months ago. Today, it’s at $27, representing a 50% discount on a fundamentally strong company. The Trump administration’s push to build more ships should actually work in Graham’s favor, making this steep decline even more perplexing. The fear in the market has led to excessive selling, but for long-term investors, this represents a buying opportunity.

And then there’s Eledon Pharmaceuticals (ELDN), a biopharmaceutical company whose stock has dropped from $5.50 to $2.80. This is a company with improving fundamentals, particularly positive patient data, yet the stock price has fallen sharply. This disconnect between price and performance highlights how the selloff has been more about broader market panic than about the company’s intrinsic value.

The bottom line is that there are real bargains out there in small-cap stocks for individual investors who are willing to look past the short-term fear. The Russell 2000 index has been hit harder than other indexes due to the smaller size and lower liquidity of the companies involved. As a result, the impact of impulsive, panic-driven selling is more pronounced in this index than in the larger ones.

For investors with staying power, particularly those with a 2-3 year horizon, the current market turmoil presents a significant opportunity. Many of these companies, which are being unfairly dragged down by the broader market, have strong fundamentals and the potential to rebound once market sentiment stabilizes. As the market continues to digest these challenges, patient investors may see significant returns as these companies recover and grow.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Industry dynamics. The QVC Group recently announced that it is laying off 900 employees as part of its effort to become a live social shopping company. Notably, while we don’t anticipate QVC will stop live selling on traditional TV, the increased focus on social commerce is illustrative of changing consumer viewing habits. In our view, XCEL Brands is well positioned to benefit from shift in viewing habits toward streaming alternatives.

Valuable expertise. XCEL Brands is a veteran in the live selling space and has extensive experience working with celebrities to help bring their products to market and help them sell. In our view, the company is well positioned to provide celebrities with expertise both in traditional TV and social commerce selling, or live streaming.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – IQSTEL signs MOU to acquire a 51% stake in fintech company GlobeTopper, strengthening its Fintech division. – The deal accelerates IQSTEL’s revenue growth, pushing it closer to its $1 billion target by 2027. – GlobeTopper’s integration with IQSTEL’s telecom network enhances cross-selling opportunities and market expansion.

IQSTEL Inc. (OTCQX: IQST), a rapidly expanding provider of Telecom, Fintech, Cybersecurity, and AI-driven services, has signed a Memorandum of Understanding (MOU) to acquire a 51% equity stake in GlobeTopper, LLC. This move bolsters IQSTEL’s fintech division and lays the groundwork for long-term revenue expansion.

Following its record $283 million revenue in 2024, IQSTEL projects $340 million in revenue for 2025, largely driven by its telecom division. The acquisition of GlobeTopper, a leader in B2B Top-Up solutions, is set to accelerate IQSTEL’s fintech growth, adding an estimated $60 million in revenue in 2025 and $85 million in 2026. The company aims to reach $1 billion in revenue by 2027, and this acquisition plays a critical role in achieving that milestone.

GlobeTopper’s preliminary 2024 financials show $39.4 million in revenue and $190,000 in EBITDA. IQSTEL will invest $1.2 million over 24 months to fuel further expansion, ensuring sustained growth in fintech services.

A major advantage of this acquisition is IQSTEL’s ability to integrate GlobeTopper’s fintech solutions within its extensive telecom network, spanning 21 countries and four continents. This cross-industry synergy will enable IQSTEL to unlock new high-margin revenue streams and provide added value to existing customers.

Additionally, GlobeTopper’s strong relationships with top-tier retail firms create new opportunities for IQSTEL to expand its service offerings. This partnership aligns with IQSTEL’s broader strategy of leveraging technology to diversify and enhance its business portfolio.

GlobeTopper’s CEO, Craig Span, will continue leading the company post-acquisition, ensuring stability and executing the company’s aggressive growth plans. IQSTEL’s President and CEO, Leandro Iglesias, emphasized the acquisition’s role in achieving IQSTEL’s ambitious revenue targets, stating that GlobeTopper’s fintech innovation and IQSTEL’s global telecom presence create a strong foundation for sustained expansion.

IQSTEL will acquire its 51% equity stake in GlobeTopper for $700,000, with a combination of cash payments and IQSTEL common shares. Additionally, the company will provide structured growth capital of up to $1.2 million over 24 months, contingent upon GlobeTopper achieving financial milestones.

This acquisition is a crucial step for IQSTEL in solidifying its fintech leadership while enhancing its overall business strength. As the company continues its aggressive expansion, shareholders can expect further developments in both the fintech and telecom sectors.

Key Points: – PepsiCo has acquired prebiotic soda brand Poppi for $1.95 billion, strengthening its presence in the functional beverage market. – The deal aligns with growing consumer demand for drinks that support gut health and overall well-being. – The brand, which gained traction after a successful pitch on Shark Tank, will leverage PepsiCo’s resources to expand distribution and innovation.

PepsiCo has announced its acquisition of prebiotic soda brand Poppi for $1.95 billion, marking a significant move into the growing functional beverage category. The transaction includes $300 million in anticipated cash benefits, effectively bringing the net purchase price to $1.65 billion. This deal reinforces PepsiCo’s commitment to diversifying its beverage portfolio to align with shifting consumer preferences toward health-conscious options.

“More than ever, consumers are looking for convenient and great-tasting options that fit their lifestyles and respond to their growing interest in health and wellness,” said PepsiCo Chairman and CEO Ramon Laguarta. The acquisition reflects PepsiCo’s strategy of investing in emerging brands that tap into wellness trends while complementing its existing product lineup.

Poppi, based in Austin, Texas, was founded by Allison Ellsworth, who originally developed the beverage in her kitchen in 2015. Seeking a healthier alternative to traditional sodas, Ellsworth combined fruit juices with apple cider vinegar, sparkling water, and prebiotics to create a gut-friendly drink. After selling Poppi at farmers’ markets, Ellsworth and her husband gained national attention in 2018 by pitching the brand—then called Mother Beverage—on Shark Tank. Investor Rohan Oza saw potential in the product, took a stake in the company, and led its rebranding into Poppi, with its now-iconic bright, fruit-themed packaging.

Ellsworth expressed excitement about the partnership, stating, “We can’t wait to begin this next chapter with PepsiCo to bring our soda to more people – and I know they will honor what makes Poppi so special while supporting our next phase of growth and innovation.” With PepsiCo’s extensive distribution network and marketing resources, Poppi is expected to expand its reach beyond its current stronghold in health-focused consumer markets.

Oza, co-founder of CAVU Consumer Partners—which has invested in beverage brands like Oatly and Bai—echoed this enthusiasm. “We’re beyond thrilled to be partnering with PepsiCo so that even more consumers across America, and the world, can enjoy Poppi.”

The functional beverage market has seen rapid growth as consumers prioritize health benefits in their drink choices. Poppi, with its focus on gut health through prebiotics, has positioned itself at the forefront of this trend. However, the brand has not been without challenges. In 2023, Poppi faced a class-action lawsuit from a consumer alleging that its products do not deliver on their advertised gut health benefits. While the lawsuit remains unresolved, the acquisition by PepsiCo signals confidence in the brand’s long-term potential.

For PepsiCo, this move follows a pattern of acquiring fast-growing health-oriented beverage brands, including Kevita and SodaStream. As competition in the functional drink space intensifies, integrating Poppi into its portfolio will allow PepsiCo to capture a larger share of the evolving market while reinforcing its commitment to innovation in health-conscious beverages.

Key Points: – Initial unemployment claims jumped 22,000 to 242,000, exceeding economists’ forecast of 221,000 – Federal worker layoffs from Trump’s DOGE initiative haven’t yet appeared in federal unemployment data – Consumer confidence in job availability declining despite historically low overall layoff rates

The number of Americans filing new applications for unemployment benefits jumped more than anticipated last week, according to the latest data released by the Labor Department. Initial claims for state unemployment benefits increased by 22,000 to a seasonally adjusted 242,000 for the week ended February 22, significantly exceeding economists’ projections of 221,000 claims.

Despite this unexpected rise, experts caution that the increase may not indicate a fundamental shift in labor market conditions. The Labor Department noted that seasonal adjustment factors—the models used to strip out normal fluctuations from the data—tend to artificially inflate claims figures around this time of year.

The report comes amid growing concerns about potential economic impacts from the Trump administration’s recent policies, particularly the mass layoffs of probationary federal government workers. Many of these employees were terminated around February 14 by the Department of Government Efficiency (DOGE), an entity created by President Trump and led by billionaire Elon Musk.

“These firings likely add up to the biggest layoff in the history of the United States,” said Michele Evermore, a Senior Fellow at the National Academy of Social Insurance and former deputy director for policy in the Labor Department’s Office of Unemployment Insurance Modernization. Evermore warned that “economic pain is contagious” and that federal layoffs could trigger broader economic hardship.

Interestingly, the report showed no immediate impact from these federal workforce reductions in the separate unemployment compensation for federal employees program, which is reported with a one-week lag. However, economists warn that the reduction in money flowing through the economy from lost paychecks and spending cuts could eventually lead to private-sector job losses.

The so-called continuing claims—representing people receiving benefits after an initial week of aid—actually fell by 5,000 to a seasonally adjusted 1.862 million during the week ending February 15. This figure is used when surveying households for February’s unemployment rate, which stood at 4.0% in January.

Despite the overall resilience of the labor market, there are signs that households are growing more anxious about their job prospects. A Conference Board survey published Tuesday revealed that the share of consumers who viewed jobs as “plentiful” dropped to a five-month low in February, while the proportion describing jobs as “hard to get” reached its highest level since October.

For the Federal Reserve, these labor market signals provide critical input as policymakers monitor the economic impacts of the administration’s fiscal, trade, and immigration policies—many of which economists view as potentially inflationary. Minutes from the Fed’s January meeting showed policymakers expressing concern about higher inflation resulting from Trump’s initial policy proposals.

The central bank has maintained its benchmark overnight interest rate in the 4.25%-4.50% range after reducing it by 100 basis points since September 2024. This followed an aggressive tightening cycle that raised rates by 5.25 percentage points in 2022 and 2023 to combat inflation.

For now, historically low layoffs continue to support economic expansion, though upcoming reports will be closely watched for any signs that the federal workforce reductions are beginning to impact broader employment trends.

Full Year 2024 Revenues of $1.136 Billion Reflect 9.6 Percent Growth and 9.1 Percent Organic Growth, Respectively, Over Full Year 2023 Revenues of $1.037 Billion

Full Year 2024 Unmanned Systems Revenues of $270.5 Million Reflect 27.5 Percent Growth and 25.1 Percent Organic Growth Over Full Year 2023 Revenues of $212.2 Million

Full Year 2024 KGS Revenues of $865.8 Million Reflect 5.0 Percent Organic Growth of $40.9 Million Over Full Year 2023 Revenues of $824.9 Million

Full Year 2024 Net Income of $16.3 Million and GAAP EPS of $0.11 Per Share

Fourth Quarter 2024 Revenues of $283.1 Million Reflect 3.4 Percent Growth Over Fourth Quarter 2023 Revenues of $273.8 Million

Fourth Quarter 2024 Cash Flow Generated from Operations and Free Cash Flow of $45.6 million and $32.0 million, Respectively

Fourth Quarter 2024 Consolidated Book to Bill Ratio of 1.5 to 1 and Bookings of $434.2 Million

Last Twelve Months Ended December 29, 2024 Consolidated Book to Bill Ratio of 1.2 to 1 and Bookings of $1.354 Billion

2025 Financial Forecast Includes 10 Percent Organic Revenue Growth and 2026 Initial Revenue Growth Forecast of 13 to 15 Percent over 2025 Forecast Based on Recent Program Awards

SAN DIEGO, Feb. 26, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology Company in the Defense, National Security and Commercial Markets, today reported its fourth quarter 2024 financial results, including Revenues of $283.1 million, Operating Income of $3.0 million, Net Income attributable to Kratos of $3.9 million, Adjusted EBITDA of $25.2 million and a consolidated book to bill ratio of 1.5 to 1.0.

Fourth quarter 2024 Net Income and Operating Income includes non-cash stock compensation expense of $6.8 million, Company-funded Research and Development (R&D) expense of $10.6 million, including efforts in our Space, Satellite, Unmanned Systems and Microwave Electronic businesses, and expense to accrue $3.2 million related to an employee benefit plan assumed by the Company in an acquisition completed in 2011.

Kratos reported fourth quarter 2024 GAAP Net Income attributable to Kratos of $3.9 million and GAAP Net Income per share of $0.03, compared to GAAP Net Income attributable to Kratos of $2.4 million and GAAP Net Income per share of $0.02, for the fourth quarter of 2023. Adjusted earnings per share (EPS) was $0.13 for the fourth quarter of 2024, compared to $0.12 for the fourth quarter of 2023.

Fourth quarter 2024 Revenues of $283.1 million increased $9.3 million, reflecting 3.4 percent organic growth from fourth quarter 2023 Revenues of $273.8 million. Organic revenue growth was reported in both our Unmanned Systems and KGS segments, with KGS growth including increased revenues in Kratos Turbine Technologies, Defense Rocket Systems, Microwave Products, and C5ISR, offset by the previously reported and expected decline of approximately $16.1 million in the Space and Satellite business, including the industry related impact from OEM delays in the manufacture and delivery of software defined satellites.

Fourth quarter 2024 Cash Flow Generated from Operations was $45.6 million, primarily reflecting the receipt of accelerated favorable customer milestone payments, and increases in deferred revenues or customer advanced payments to $76.3 million at the end of the fourth quarter of 2024, up from $61.9 million at the end of the third quarter of 2024. Free Cash Flow Generated from Operations for the Fourth Quarter of 2024 was $32.0 million after funding of $13.6 million of capital expenditures.

For the fourth quarter of 2024, Kratos’ Unmanned Systems (KUS) segment generated Revenues of $61.1 million and organic revenue growth of 10.3 percent, as compared to $55.4 million in the fourth quarter of 2023, primarily reflecting increased target drone sales. KUS’s Operating Loss was $0.7 million in the fourth quarter of 2024, compared to Operating Income of $1.0 million in the fourth quarter of 2023. KUS’s Adjusted EBITDA for the fourth quarter of 2024 was $2.6 million, compared to $4.0 million for the fourth quarter 2023, reflecting revenue mix, the impact of increased material and subcontractor costs on multi-year fixed price contracts and increased R&D costs.

KUS’s book-to-bill ratio for the fourth quarter of 2024 was 1.3 to 1.0 and 1.2 to 1.0 for the twelve months ended December 29, 2024, with bookings of $82.4 million for the three months ended December 29, 2024, and bookings of $326.8 million for the twelve months ended December 29, 2024. Total backlog for KUS at the end of the fourth quarter of 2024 was $295.2 million compared to $273.9 million at the end of the third quarter of 2024 and $239.0 million at the end of the fourth quarter of 2023.

For the fourth quarter of 2024, Kratos’ Government Solutions (KGS) segment Revenues of $222.0 million increased from Revenues of $218.4 million in the fourth quarter of 2023, reflecting a 1.6 percent growth and organic growth rate. The increased Revenues includes organic revenue growth in our Turbine Technologies, C5ISR, Defense Rocket Support and Microwave Products businesses of $19.7 million, offset by the previously reported and expected decline of approximately $16.1 million in the Space and Satellite business.

KGS reported Operating Income of $11.0 million in the fourth quarter of 2024 compared to $17.5 million in the fourth quarter of 2023, primarily reflecting the mix in revenues and resources as well as the expense to accrue $3.2 million in the fourth quarter of 2024 related to a benefit plan assumed by the Company in a previous acquisition. Fourth quarter 2024 KGS Adjusted EBITDA was $22.6 million, compared to fourth quarter 2023 KGS Adjusted EBITDA of $25.1 million, primarily reflecting the mix in revenues and resources.

KGS reported a book-to-bill ratio of 1.6 to 1.0 for the fourth quarter of 2024, a book to bill ratio of 1.2 to 1.0 for the last twelve months ended December 29, 2024 and bookings of $351.8 million and $1.028 billion for the three and last twelve months ended December 29, 2024, respectively. KGS’s total backlog at the end of the fourth quarter of 2024 was $1.150 billion, as compared to $1.020 billion at the end of the third quarter of 2024, and $988.0 million at the end of the fourth quarter of 2023.

Kratos reported consolidated bookings of $434.2 million and a book-to-bill ratio of 1.5 to 1.0 for the fourth quarter of 2024, and consolidated bookings of $1.354 billion and a book-to-bill ratio of 1.2 to 1.0 for the last twelve months ended December 29, 2024. Consolidated backlog was $1.445 billion on December 29, 2024, as compared to $1.294 billion at September 29, 2024 and $1.227 billion on December 31, 2023. Kratos’ bid and proposal pipeline was $12.4 billion at December 29, 2024, as compared to $11.0 billion at December 31, 2023. Backlog at December 29, 2024 included funded backlog of $1.090 billion and unfunded backlog of $355.0 million.

Full Year 2024 Results

Kratos reported its full year 2024 financial results, including Revenues of $1.136 billion, Operating Income of $29.0 million, Net Income attributable to Kratos of $16.3 million, Adjusted EBITDA of $105.7 million and a consolidated book to bill ratio of 1.2 to 1.0.

Included in the full year 2024 Net Income and Operating Income is non-cash stock compensation expense of $29.8 million, Company-funded Research and Development (R&D) expense of $40.3 million, including ongoing development efforts in our Space and Satellite Communications business to develop our first to market, virtual, software-based OpenSpace command & control (C2), telemetry tracking & control (TT&C) and other ground system solutions and ongoing development efforts in our Unmanned Systems and Microwave Products businesses, and an expense to accrue $3.2 million related to an employee benefit plan assumed by the Company in an acquisition completed in 2011.

Kratos reported full year 2024 GAAP Net Income of $16.3 million and GAAP Net Income per share of $0.11, compared to a GAAP Net Loss attributable to Kratos of $8.9 million and a GAAP Net Loss per share of $0.07, for the full year 2023. Adjusted earnings per share (EPS) was $0.49 for the full year 2024, compared to $0.42 for the full year 2023.

Full year 2024 Revenues of $1.136 billion increased $99.2 million, reflecting 9.6 percent growth and 9.1 percent organic growth, including the impact of the Sierra Technical Services, Inc. (STS) acquisition on a pro forma basis as if acquired at the beginning of 2023, respectively, from full year 2023 Revenues of $1.037 billion. Full year 2024 Cash Flow Generated from Operations was $49.7 million, including the receipt of accelerated favorable customer milestone payments, offset partially by working capital uses including increases in inventories, prepaid assets and investments in other assets and reduction of deferred revenues or advanced customer payments. Free Cash Flow Used in Operations was $8.5 million after funding of $58.2 million of capital expenditures. Full year 2024 capital expenditures were elevated due primarily to the manufacture of the two production lots of Valkyries prior to contract award to meet anticipated customer orders and requirements and due to investments related to the expansion and addition of production facilities.

For full year 2024, KUS generated Revenues of $270.5 million, as compared to $212.2 million in the full year 2023, reflecting 27.5 percent growth and 25.1 percent organic growth, including the impact of the STS acquisition on a pro forma basis as if acquired at the beginning of 2023, primarily reflecting increased domestic and international drone activity. KUS’s Operating Income was $2.9 million in full year 2024 compared to $4.2 million in full year 2023. KUS’s Adjusted EBITDA for full year 2024 was $16.3 million, compared to full year 2023 Adjusted EBITDA of $14.8 million, reflecting the increased volume partially offset by increased material and subcontractor costs on multi-year fixed price contracts and increased R&D costs.

For full year 2024, KGS Revenues of $865.8 million increased $40.9 million, reflecting 5.0 percent organic growth from Revenues of $824.9 million in full year 2023. The increased Revenues includes organic revenue growth in our Turbine Technologies, C5ISR, Microwave Products, Defense Rocket Support and Training Solutions businesses aggregating $88.7 million, offset by a reduction of $47.8 million in offset by the Space and Satellite business described previously.

KGS reported operating income of $56.6 million in full year 2024 compared to $52.7 million in full year 2023, primarily reflecting the increased revenue volume. Full year 2024 KGS Adjusted EBITDA was $89.4 million, compared to full year 2023 KGS Adjusted EBITDA of $80.6 million, primarily reflecting the increased revenue.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ full year 2024 and fourth quarter demonstrated once again that we can significantly organically grow the business, and make sizable internally funded investments, positioning the Company for accelerating future growth, while also generating significant, positive operating cash flow. We have recently received several large new program and contract awards, including in the hypersonic, target drone, jet engine, rocket, and satellite system areas, enabling us to increase our expected revenue growth rate for 2026 to a range of 13 percent to 15 percent above our current 2025 financial forecast that we provided today, which includes 10 percent growth over 2024. Kratos’ fourth quarter 1.5 to 1.0 book to bill ratio and our $12.4 Billion opportunity pipeline also provides confidence in our expected accelerating future growth trajectory, with increased margins.”

Mr. DeMarco continued, “The Trump Administration has increased emphasis on reducing cost, rapidly fielding new technology and systems and getting more for less, all which are and have been pillars of Kratos’ Mission. At Kratos, “Affordability is a Technology” and “Better is the Enemy of Good Enough Ready to Field Today”, as represented in our Erinyes, Dark Fury and other hypersonic vehicles, our Zeus, Oriole and other rocket systems, and our jet drones, jet engines and propulsion systems. We believe Kratos’ alignment with the new Administration’s objectives will be recognized in increased bookings, increased expected future growth rates and increased future profitability, including as based on recent meetings and discussions with certain of our customers.”

Mr. DeMarco concluded, “After decades of focus on fighting terrorism and asymmetric warfare, the United States has begun a generational rebuild of its industrial base and the ability to deter and defeat Nation State adversaries. The Axis of Resistance and the threat to the U.S. and its Allies is real, and Kratos is a key element of the proven Peace through Overwhelming Strength approach to Global Security and stability. As a result, we expect a future, multiyear, up and to the right organic growth trajectory with increased margins and profitability, and Kratos making the necessary investments in, among other things, property, plant, and equipment, to successfully execute for our customers and country.”

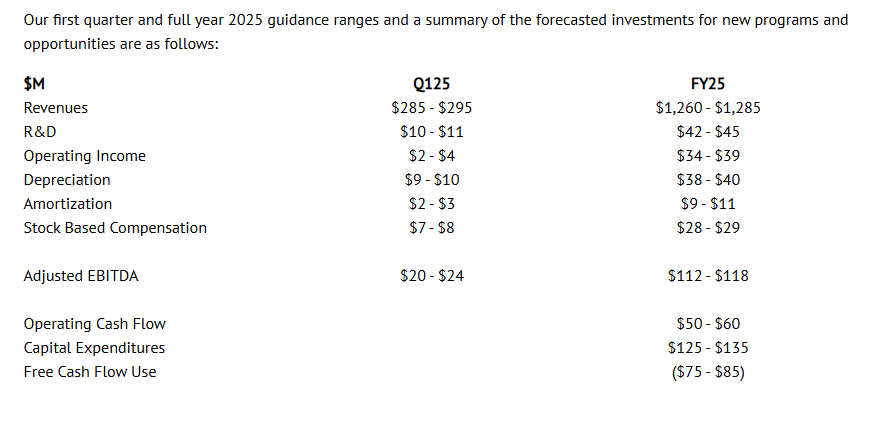

Financial Guidance

We are providing our initial 2025 first quarter and full year 2025 financial guidance range, which includes our assumptions, including as related to: current forecasted business mix, employee sourcing, hiring and retention; manufacturing, production and supply chain disruptions; parts shortages and related continued significant cost and price increases in each of these areas, that are impacting the industry and Kratos. Additionally, a U.S. Government budget was not passed by October 1, 2024, the beginning of Federal Fiscal Year 2025, and as a result, Kratos and others in our industry are operating under a Continuing Resolution Authorization (CRA), which currently expires March 14, 2025, under which no new contracts and no increases in existing contracts production or funding, among other stipulations, is permitted. If the current CRA is not resolved by March 14, 2025, the industry and Kratos will have operated under CRAs, without a DoD Budget, for approximately 12 of the previous 18 months. Kratos has a number of new and existing programs and contracts which are directly being impacted by the current CRA. Kratos’ 2025 financial forecast and guidance provided today assumes that the current CRA will be resolved by March 14, 2025, and that a U.S. Federal and DoD budget which includes no unexpected funding cuts impacting our business occurs. If the current CRA goes substantially beyond the existing March 14, 2025 date, or if there are significant reductions or changes to programs, contracts or initiatives that Kratos is or expects to be involved with, we will evaluate Kratos’ 2025 and future financial forecasts at that time, based on the existing facts, circumstances and expectations and make any adjustments required.

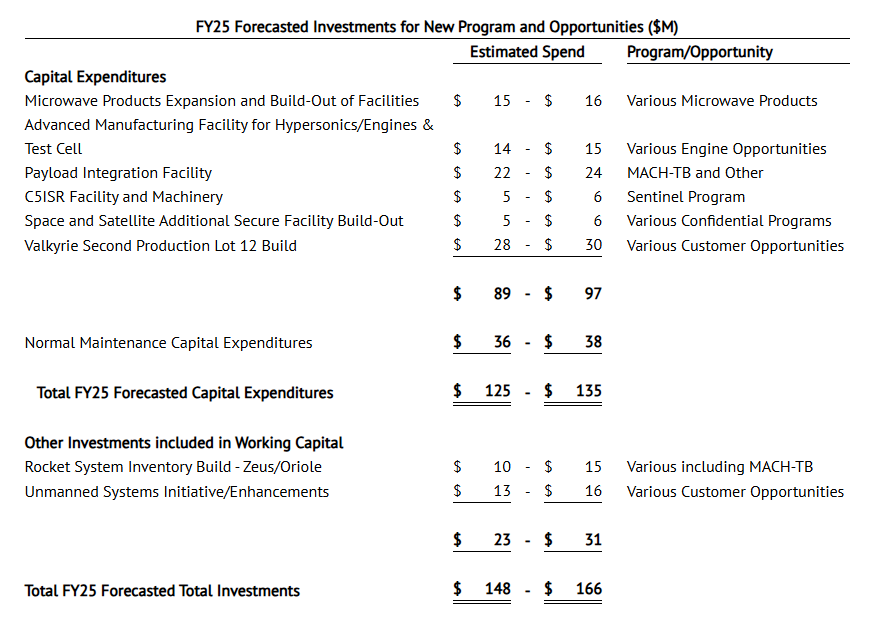

Kratos’ 2025 financial forecast and guidance includes elevated investments for capital expenditures for property, plant and equipment, including the expansion of our manufacturing and production facilities and related inventory builds in our Rocket Systems and Hypersonic businesses, primarily related to the recent MACH-TB 2.0 contract award, the continued manufacture of two production lots of Valkyries prior to contract award, to meet anticipated customer orders and requirements, the expansion and build-out of the Company’s Microwave Products production facilities, the expansion and build-out of our small jet engine production and test cell facilities, and the build-out of additional secure facilities for our federal secured space communications business, in accordance with contract and customer requirements. Kratos’ operating cash flow guidance also assumes certain investments in our rocket systems and unmanned systems businesses.

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice RegardingForward–LookingStatements This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its first quarter and full year 2025 revenues, 2026 revenue growth rates and expected contributors to 2026 projected revenue growth, organic revenue growth rates, R&D, operating income (loss), depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2025 operating cash flow, capital expenditures and other investments, and free cash flow, the Company’s future growth trajectory and ability to achieve improved revenue mix and profit in certain of its business segments and the expected timing of such improved revenue mix and profit, including the Company’s ability to achieve sustained year over year increasing revenues, profitability and cash flow, the Company’s expectation of ramp on projects and that investments in its business, including Company funded R&D expenses and ongoing development efforts, will result in an increase in the Company’s market share and total addressable market and position the Company for significant future organic growth, profitability, cash flow and an increase in shareholder value, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, planned 2025 investments, including in the tactical drone and satellite areas, and the related potential for additional growth in 2025 and beyond, ability to successfully compete and expected new customer awards, including the magnitude and timing of funding and the future opportunity associated with such awards, including in the target and tactical drone and satellite communication areas, performance of key contracts and programs, including the timing of production and demonstration related to certain of the Company’s contracts and control (TT&C) product offerings, the impact of the Company’s restructuring efforts and cost reduction measures, including its ability to improve profitability and cash flow in certain business units as a result of these actions and to achieve financial leverage on fixed administrative costs, the ability of the Company’s advanced purchases of inventory to mitigate supply chain disruptions and the timing of converting these investments to cash through the sales process, benefits to be realized from the Company’s net operating loss carry forwards, the availability and timing of government funding for the Company’s offerings, including the strength of the future funding environment, the short-term delays that may occur as a result of Continuing Resolutions or delays in U.S. Department of Defense (DoD) budget approvals, timing of LRIP and full rate production related to the Company’s unmanned aerial target system offerings, as well as the level of recurring revenues expected to be generated by these programs once they achieve full rate production, market and industry developments, and any unforeseen risks associated with any public health crisis, supply chain disruptions, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoD may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoD Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates and risks related to the interest rate swap contract to hedge Term SOFR associated with the Company’s Term Loan A; currently unforeseen risks associated with any public health crisis, and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 29, 2024, and in our other filings made with the Securities and Exchange Commission.

Note Regarding Use of Non-GAAP Financial Measures and Other Performance Metrics This news release contains non-GAAP financial measures, including organic revenue growth rates, Adjusted EPS (computed using income from continuing operations before income taxes, excluding income (loss) from discontinued operations, excluding income (loss) attributable to non-controlling interest, excluding depreciation, amortization of intangible assets, amortization of capitalized contract and development costs, stock-based compensation expense, acquisition and restructuring related items and other, which includes, but is not limited to, legal related items, non-recoverable rates and costs, and foreign transaction gains and losses, less the estimated impact to income taxes) and Adjusted EBITDA (which includes net income (loss) attributable to noncontrolling interest and excludes, among other things, losses and gains from discontinued operations, acquisition and restructuring related items, stock compensation expense, foreign transaction gains and losses, and the associated margin rates). Additional non-GAAP financial measures include Free Cash Flow from Operations computed as Cash Flow from Operations less Capital Expenditures plus proceeds from sale of assets and Adjusted EBITDA related to our KUS and KGS businesses. Kratos believes this information is useful to investors because it provides a basis for measuring the Company’s available capital resources, the actual and forecasted operating performance of the Company’s business and the Company’s cash flow, excluding non-recurring items and non-cash items that would normally be included in the most directly comparable measures calculated and presented in accordance with GAAP. The Company’s management uses these non-GAAP financial measures, along with the most directly comparable GAAP financial measures, in evaluating the Company’s actual and forecasted operating performance, capital resources and cash flow. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and investors should carefully evaluate the Company’s financial results calculated in accordance with GAAP and reconciliations to those financial results. In addition, non-GAAP financial measures as reported by the Company may not be comparable to similarly titled amounts reported by other companies. As appropriate, the most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to the Company’s financial results prepared in accordance with GAAP are included in this news release.

Another Performance Metric the Company believes is a key performance indicator in our industry is our Book to Bill Ratio as it provides investors with a measure of the amount of bookings or contract awards as compared to the amount of revenues that have been recorded during the period and provides an indicator of how much of the Company’s backlog is being burned or utilized in a certain period. The Book to Bill Ratio is computed as the number of bookings or contract awards in the period divided by the revenues recorded for the same period. The Company believes that the rolling or last twelve months’ Book to Bill Ratio is meaningful since the timing of quarter-to-quarter bookings can vary.

Key Points: – The Dow fell 805 points, with a two-day loss exceeding 1,200 points, while the S&P 500 and Nasdaq also declined. – Economic data signaled weaker consumer sentiment, a slowing housing market, and increased inflation concerns. – Investors moved toward safer assets, boosting bonds and defensive stocks, while major indexes fell below key technical levels.

Stocks sold off on Friday as new U.S. economic data raised investor concerns over slowing growth and persistent inflation. The Dow Jones Industrial Average tumbled 805 points, or 1.8%, bringing its two-day losses to more than 1,200 points. The S&P 500 fell 1.6%, while the Nasdaq Composite dropped over 2% as investors moved away from equities in search of safer assets.

United Health led the Dow’s decline, plunging 7% following a Wall Street Journal report that the insurer is under investigation by the Justice Department. The stock was on track for its worst day since March 2020. Meanwhile, broader economic indicators pointed to growing uncertainty. The University of Michigan consumer sentiment index fell to 64.7 in January, a sharper decline than expected, reflecting rising inflation concerns. Additionally, the 5-year inflation outlook in the survey hit 3.5%, its highest level since 1995.

Housing market data also contributed to the negative sentiment, with existing home sales dropping more than anticipated to 4.08 million units. The U.S. services purchasing managers index (PMI) also showed signs of weakness, slipping into contraction territory for February. These factors compounded fears that economic conditions may not be as strong as previously believed.

Investors sought refuge in traditionally defensive assets. The benchmark 10-year Treasury note yield declined by 8 basis points to 4.418%, boosting bond prices. The Japanese yen also strengthened against the U.S. dollar. Defensive stocks, including Procter & Gamble, General Mills, Kraft Heinz, and Mondelez, posted gains as investors shifted toward more stable sectors.

Market weakness extended across the week, with the S&P 500 down about 1%, the Dow shedding 2%, and the Nasdaq losing 1.6%. Several factors weighed on stocks, including Walmart’s weaker-than-expected earnings guidance, which sent its stock down 3% on Friday and more than 9% for the week. Inflation concerns and losses in Palantir further pressured the market.

Technical indicators added to the cautious outlook. The Dow and Nasdaq both fell below their 50-day moving averages in afternoon trading. The Dow, down 1.8%, slipped under its 50-day average of 43,695.91 for the first time since Jan. 21, while the Nasdaq, down 2%, dropped below 19,686.10, marking its first break of that level since Feb. 12.

As investors brace for more potential volatility, the focus remains on upcoming economic data and policy developments. With inflationary pressures persisting and uncertainty surrounding future policy decisions, the market’s direction remains uncertain heading into next week.

Key Points: – Treasury yields declined slightly as investors analyzed economic data and Trump’s proposed tariffs. – Jobless claims came in higher than expected, signaling a potential softening in the labor market. – Fed officials emphasized the need for further inflation progress before considering rate cuts.

U.S. Treasury yields edged lower on Thursday as investors assessed fresh economic data and the potential impact of U.S. President Donald Trump’s proposed tariffs. The 10-year Treasury yield declined more than 2 basis points to 4.507%, while the 2-year Treasury yield dropped 2.3 basis points to 4.253%. Yields move inversely to bond prices, meaning demand for Treasuries increased slightly as investors sought stability amid economic uncertainty.

One of the key economic reports influencing the bond market was the latest weekly initial jobless claims data, which showed 219,000 new claims for unemployment benefits in the week ending Feb. 15. This was slightly above the 215,000 claims economists had expected, signaling a modest cooling in the labor market. Investors also awaited the release of the Philadelphia Fed Manufacturing Index, an important measure of regional economic activity that could provide further insight into the strength of the U.S. economy.

At the same time, Federal Reserve officials were scheduled to speak throughout the day, offering additional perspectives on monetary policy. Among them, Fed Bank of Chicago President Austan Goolsbee and Fed Governor Adriana Kugler were expected to discuss economic conditions and the outlook for inflation. The market remained focused on any indications of future interest rate changes, particularly given the Federal Reserve’s cautious stance on inflation.

Another factor weighing on investor sentiment was Trump’s latest tariff proposal, which called for a 25% duty on key imports, including automobiles, pharmaceuticals, and semiconductors. The former president stated that these tariffs could increase significantly over time and potentially take effect as early as April 2. Investors closely monitored these developments, as trade policies can have broad economic implications, affecting corporate profitability, inflationary pressures, and overall market stability.

Meanwhile, the Federal Reserve’s recently released meeting minutes suggested that policymakers remain concerned about inflation risks. Officials emphasized that they would need to see sustained progress on inflation before considering additional interest rate cuts. They also noted that potential shifts in trade and immigration policies could create further economic uncertainty.

Bond markets reacted cautiously to these developments, with Treasury yields experiencing a slight decline as investors weighed the implications for future monetary policy. Lower yields often indicate increased investor demand for safe-haven assets, particularly when concerns about economic growth or inflation emerge.

As the economic landscape continues to evolve, market participants will closely watch upcoming data releases and Federal Reserve commentary for further indications of policy direction. The trajectory of interest rates remains a key focus, with investors balancing optimism about economic resilience against concerns over inflation and potential trade disruptions.

Key Points: – Proposed 25% tariffs target automotive, pharmaceutical, and semiconductor imports – Implementation could begin as early as April 2, following March steel and aluminum tariffs – Multiple sectors face supply chain disruption and potential cost increase

Global markets are adjusting to President Trump’s unexpected announcement of 25% tariffs on imported automobiles, pharmaceuticals, and semiconductors, with futures markets showing increased volatility. The proposal, announced Tuesday from Mar-a-Lago, represents a significant expansion of the administration’s trade policies and could reshape multiple industry sectors.

The automotive sector, which accounts for approximately 3% of U.S. GDP, faces potentially substantial restructuring. Major automakers with significant foreign manufacturing operations saw their stocks decline in after-hours trading. Companies like Toyota (TM) fell 3.2%, while General Motors (GM) and Ford (F) showed mixed reactions as investors weighed potential domestic manufacturing advantages against supply chain disruptions.

The pharmaceutical sector, already dealing with pricing pressures and supply chain challenges, could see significant market adjustments. Major pharmaceutical ETFs declined following the announcement, with the iShares U.S. Pharmaceuticals ETF (IHE) dropping 2.1%. Indian pharmaceutical ADRs were particularly affected, with Dr. Reddy’s Laboratories (RDY) and Sun Pharmaceutical Industries experiencing notable declines.

Semiconductor stocks faced immediate pressure, with the Philadelphia Semiconductor Index (SOX) declining 2.8%. Taiwan Semiconductor Manufacturing Company (TSM), a crucial supplier to U.S. tech giants, saw its ADRs fall 4.1%. The potential tariffs add another layer of complexity to an industry already managing global chip shortages and supply chain constraints.

Market data suggests significant sector rotation as investors reassess positions. Defense stocks and domestic manufacturers showed strength, while companies heavily dependent on global supply chains experienced selling pressure. The CBOE Volatility Index (VIX) jumped 15%, reflecting increased market uncertainty.

From an investment perspective, the proposed tariffs create both opportunities and risks. Domestic manufacturers could benefit from reduced competition and increased demand, while companies reliant on global supply chains may face margin pressure. The financial sector is also monitoring the situation, as trade policy shifts could impact currency markets and international banking operations.

Bond markets reflected the uncertainty, with Treasury yields declining as investors sought safe-haven assets. The 10-year Treasury yield fell 7 basis points, while gold futures rose 1.2%, indicating defensive positioning among institutional investors.

The implementation timeline, potentially beginning April 2, gives markets limited adjustment time. This compressed schedule could lead to increased volatility as companies rush to adapt supply chains and adjust pricing strategies. The speed of implementation may also affect Q2 earnings forecasts across multiple sectors.

Looking ahead, investors are focusing on several key metrics: changes in manufacturing capacity utilization, supplier cost indices, and consumer price impacts. These indicators could provide early signals of the tariffs’ economic effects and guide investment strategies in affected sectors.

The market response suggests a period of adjustment ahead as companies and investors navigate this significant shift in trade policy. With implementation potentially weeks away, sector rotation and volatility may continue as markets price in the full implications of these sweeping trade measures.

Completed Phase 2 enrollment with randomization of 51 subjects into treatment and control arms

Phase 1/2 study (N=60) demonstrated favorable safety and tolerability profile with no serious adverse events related to OCU410, including no cases of ischemic optic neuropathy, vasculitis, intraocular inflammation, endophthalmitis or choroidal neovascularization

Subjects showed considerably slower lesion growth (44%) from baseline in treated eyes versus untreated fellow eyes at 9 months in follow-up data from the Phase 1 study

Clinically meaningful 2-line (10-letter) improvement in visual function (LLVA) in treated eyes compared to untreated eyes was noted in the Phase 1 portion of the trial

Preservation of retinal tissue at 9 months around GA lesions of treated eyes with a single injection of OCU410 in Phase 1 compared favorably to published data on a leading FDA-approved complement inhibitor given monthly or every other month at the same time points

MALVERN, Pa., Feb. 12, 2025 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced that dosing is complete, ahead of schedule in the Phase 2 portion of the Phase 1/2 ArMaDa clinical trial for OCU410—a novel multifunctional modifier gene therapy candidate being developed for geographic atrophy (GA), an advanced stage of dry age-related macular degeneration (dAMD). Age-related macular degeneration (AMD) affects 1 in 8 people 60 years and older. The global prevalence of dAMD is 266 million worldwide and by 2050 more than 5 million Americans may suffer from this incurable condition. Today, GA – the later stage of dAMD – affects approximately 2-3 million people in the United States (U.S.) and Europe.

There are limited options for patients with dAMD in the U.S. and current therapies involve frequent (monthly or every other month) injections and have unwanted side effects that can affect vision. These therapies are not approved in Europe, leaving approximately 2 million patients with no therapeutic option.

“Dosing completion is a major accomplishment for our OCU410 program,” said Dr. Shankar Musunuri, Chairman, CEO, and Co-founder of Ocugen. “Based on the multifunctional effect of our modifier gene therapy, the profound unmet medical need, limited treatment options, and the fact that it is designed as a one and done treatment, we believe OCU410 can be a potential blockbuster therapy and the gold standard for treating GA worldwide. The data from this trial will help us design a future pivotal Phase 3 study planned for 2026 and enable our commercial strategy for Biologics License Application (BLA) and Marketing Authorization Application (MAA) filings as soon as 2028.”

“The preliminary efficacy and safety data from the Phase 1/2 study are highly encouraging, demonstrating the potential of OCU410 to improve both structural and functional outcomes,” said Lejla Vajzovic, MD, FASRS, Director of the Duke Surgical Vitreoretinal Fellowship Program and Professor of Ophthalmology, Pediatrics and Biomedical Engineering with Tenure at Duke University Eye Center. “I look forward to the Phase 2 results and believe a one-time gene therapy could reshape the treatment landscape, offering a transformative option for patients.”

GA is a multifactorial disease with a complex etiology that involves genetic and environmental factors. The current treatment options for GA in the U.S. are limited to those targeting a single mechanism—the complement pathway—requiring frequent intravitreal injections, either monthly or every other month. By contrast, OCU410 is a multifunctional modifier gene therapy, which targets multiple pathways associated with GA.

“Given the safety concerns associated with currently approved GA treatments, the encouraging safety and tolerability profile of OCU410 offers a promising treatment option,” said Dr. Huma Qamar, Chief Medical Officer of Ocugen. “With Phase 2 enrollment now complete, OCU410 has the potential to be a one-time treatment, reducing the burden of frequent injections, improving patient compliance, and ultimately enhancing quality of life.”

In the Phase 2 study, the safety and efficacy of OCU410 in patients with GA secondary to dAMD will be assessed. Fifty-one (51) patients were randomized 1:1:1 into either of two treatment groups (medium or high dose) or a control group. In the treatment groups, subjects received a single subretinal 200-µL administration of 5 x 1010 vector genomes (vg)/mL (medium dose) or 1.5 x 1011 vg/mL (high dose), while the control group remained untreated.

The ArMaDa clinical trial for OCU410 is being performed at 14 leading retinal surgery centers across the U.S.

About the Phase 1/2 ArMaDa clinical trial The ArMaDa Phase 1/2 clinical trial will assess the safety of unilateral subretinal administration of OCU410 in subjects with GA and will be conducted in two phases. Phase 1 is a multicenter, open label, dose-escalation study consisting of three dose levels [low dose (2.5×1010 vg/mL), medium dose (5×1010 vg/mL), and high dose (1.5 ×1011 vg/mL)]. Phase 2 is a randomized, outcome assessor-blinded, dose-expansion study in which subjects were randomized in a 1:1:1 ratio to either the medium dose or high dose OCU410 treatment groups or to an untreated control group.

AboutdAMD and GA dAMD affects approximately 10 million Americans and more than 266 million people worldwide. It is characterized by the thinning of the macula, the portion of the retina responsible for clear vision in one’s direct line of sight. dAMD involves the slow deterioration of the retina with submacular drusen (small white or yellow dots on the retina), atrophy, loss of macular function, and central vision impairment. dAMD accounts for 85-90% of all AMD cases.

AboutOCU410 OCU410 utilizes an adeno-associated virus (AAV) platform for the retinal delivery of the RORA (ROR Related Orphan Receptor A) gene. The RORA protein plays an important role in lipid metabolism, reducing lipofuscin deposits and oxidative stress, and demonstrates an anti-inflammatory role as well as inhibiting the complement system in both in vitro and in vivo (animal model) studies. These results demonstrate the ability of OCU410 to target multiple pathways linked with dAMD pathophysiology. Ocugen is developing AAV-RORA as a one-time gene therapy for the treatment of GA.

AboutOcugen,Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patients’ lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements Thispressreleasecontainsforward-lookingstatementswithinthemeaningofThePrivateSecuritiesLitigationReformActof1995,including,butnot limited to, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines,whicharesubjecttorisksanduncertainties.Wemay,insomecases,usetermssuchas “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including,butnotlimitedto,therisksthatpreliminary,interimandtop-lineclinicaltrialresultsmaynotbeindicativeof,andmaydifferfrom,finalclinical data;the ability of OCU410 to perform in humans in a manner consistent with nonclinical, preclinical or previous clinical study data;thatunfavorablenewclinicaltrialdatamayemergeinongoingclinicaltrialsorthroughfurtheranalysesofexistingclinicaltrialdata;thatearlier non-clinicalandclinicaldataandtestingofmaynotbepredictiveoftheresultsorsuccessoflaterclinicaltrials;andthatthatclinicaltrialdataare subject to differing interpretations and assessments, including by regulatory authorities.Theseandotherrisksanduncertaintiesaremorefully describedinourperiodicfilingswiththeSecuritiesandExchangeCommission(SEC),includingtheriskfactorsdescribedinthesectionentitled“Risk Factors”inthequarterlyandannualreportsthatwefilewiththeSEC.Anyforward-lookingstatementsthatwemakeinthispressreleasespeakonlyas ofthedateofthispressrelease.Exceptasrequiredbylaw,weassumenoobligationtoupdateforward-lookingstatementscontainedinthispress release whether as a result of new information, future events, or otherwise, after the date of this press release.