U.S. equities slid sharply Thursday as geopolitical tensions in the Middle East reignited volatility across global markets. A renewed surge in crude oil prices, combined with uncertainty surrounding the expanding conflict involving Iran, pushed investors toward risk-off positioning and weighed heavily on major indices.

The Dow Jones Industrial Average fell more than 800 points, dropping roughly 1.8% in afternoon trading. The S&P 500 declined about 0.8%, while the Nasdaq Composite slipped approximately 0.6%, reflecting broad selling pressure across sectors as investors reassessed geopolitical and inflation risks.

At the center of the market’s concern is the escalating confrontation between the U.S.-Israel coalition and Iran. The conflict has now entered its sixth day, with reports indicating continued military strikes across the region. U.S. officials said more than 2,000 targets have been hit, while the White House indicated American forces are moving toward what it described as “complete and total control of Iranian airspace.”

For markets, the immediate concern is energy supply.

Iran is the fourth-largest producer in OPEC, and disruptions to its production capacity or shipping routes through the Strait of Hormuz could ripple through global oil markets. Even the perception of supply disruption has been enough to drive crude prices higher.

West Texas Intermediate crude futures rose toward $79 per barrel, while Brent crude climbed above $84, marking a renewed rally in energy prices after a brief pullback earlier this week.

Higher oil prices often feed directly into inflation expectations — a dynamic that has quickly caught the attention of investors already watching the Federal Reserve’s next policy moves. Rising energy costs can push transportation, manufacturing, and consumer prices higher, potentially complicating the Fed’s interest rate outlook if inflation proves sticky.

The ripple effects were visible across other asset classes Thursday.

Despite its reputation as a safe-haven asset, gold fell more than 1%, pressured by a stronger U.S. dollar. When the dollar strengthens, commodities priced in dollars become more expensive for international buyers, often weighing on prices.

Other precious metals followed suit. Silver, platinum, and palladium also declined, reflecting a broader commodities pullback outside of oil.

Meanwhile, Treasury markets also saw movement, with 10-year yields rising as bond prices fell. Higher yields can add another layer of pressure to equities by increasing borrowing costs and reducing the relative attractiveness of stocks compared with fixed income.

Energy costs are already filtering into the real economy.

According to AAA data, the national average gasoline price climbed to $3.25 per gallon, up $0.27 from a week ago. Diesel prices have risen even more sharply, jumping $0.41 to $4.16 per gallon, their highest level since 2023. Diesel plays a critical role in shipping, trucking, and industrial activity, meaning sustained increases could amplify inflation across supply chains.

Looking ahead, markets may remain sensitive to both geopolitical headlines and incoming economic data.

Friday’s U.S. monthly jobs report is expected to provide the next major signal about the health of the labor market and whether economic momentum remains strong despite mounting global uncertainty.

Investors will also watch corporate earnings releases after the closing bell Thursday from Costco and Marvell Technology, which could provide additional insight into consumer demand and technology spending trends.

For now, however, the primary driver of market sentiment remains geopolitical risk — and the unpredictable path of oil prices that often accompanies it.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Canadian government steps up with financial support. First Phosphate received conditional approval for up to C$16.7 million in non-repayable funding through Natural Resources Canada under the Global Partnerships Initiative. The contribution will fund the assessment of technical and engineering parameters, including processing circuits and equipment, needed to validate the company’s ability to produce battery-grade phosphate concentrate aligned with its definitive offtake agreement. The funding supports study activities through 2028. First Phosphate received US$523,017 under a long-term phosphate concentrate offtake agreement, reinforcing commercial validation and establishing initial cash flow tied to downstream demand.

Phosphate added to Canada’s critical minerals list. The Canadian federal government amended the 2025 budget to include phosphate as a critical mineral essential for clean technology. This designation makes First Phosphate eligible for the 30% Critical Mineral Exploration Tax Credit (CMETC) and the 30% Clean Technology Manufacturing Investment Tax Credit (CTM). The CMETC enhances the company’s ability to raise exploration capital, while the CTM offers the potential to materially reduce downstream capital intensity for the planned phosphoric acid and LFP cathode active material facilities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

USA Rare Earth (NASDAQ: USAR) announced a definitive agreement to acquire Texas Mineral Resources Corp. (OTCQB: TMRC) in an all-stock transaction valued at approximately $73 million, a deal that would consolidate ownership of one of the most significant rare earth deposits in the United States. The transaction centers on the Round Top Heavy Rare Earth and Critical Minerals Project in West Texas, a large domestic resource that has drawn increasing attention amid global efforts to secure critical mineral supply chains.

Texas Mineral Resources currently holds an approximately 19% minority interest in the Round Top project, while USA Rare Earth operates the development through a joint venture structure. By acquiring Texas Mineral Resources, USA Rare Earth would effectively gain full ownership of the project, simplifying governance and aligning development strategy under a single operator. The companies said the transaction will be completed through the issuance of roughly 3.8 million shares of USA Rare Earth common stock to TMRC shareholders, with closing expected by the third quarter of 2026, subject to shareholder approval and customary closing conditions.

The Round Top deposit, located in Hudspeth County, Texas, roughly 85 miles southeast of El Paso, is considered one of the largest known deposits of heavy rare earth elements in North America. Heavy rare earths such as dysprosium and terbium are essential inputs for high-performance permanent magnets used in electric vehicles, defense technologies, robotics, and advanced electronics. As global demand for these materials continues to grow, governments and manufacturers have increasingly focused on developing domestic supply chains to reduce dependence on overseas processing and mining capacity.

USA Rare Earth has positioned Round Top as the cornerstone of its broader “mine-to-magnet” strategy, which aims to vertically integrate rare earth mining, processing, metal production, and magnet manufacturing within the United States. The company is advancing development of the deposit under an accelerated mining plan and has previously indicated that commercial production could begin later in the decade. At full scale, the operation is expected to process tens of thousands of metric tons of mineral feedstock per day by 2030, supporting the growing demand for critical materials used across high-technology and clean-energy industries.

The Round Top project also carries broader economic and strategic implications. Rare earth elements are widely considered critical to national security and advanced manufacturing, and the United States has prioritized domestic production after decades of reliance on foreign suppliers. China currently dominates global rare earth refining capacity, creating supply chain vulnerabilities that policymakers have increasingly sought to address through investment, policy initiatives, and support for domestic mining projects.

The consolidation of Round Top under a single owner may streamline project financing, engineering development, and permitting processes as the project moves toward the construction phase. USA Rare Earth has previously engaged engineering and infrastructure partners to support feasibility work and project planning tied to the future development of the mine and associated processing facilities.

For investors watching the rare earth and critical minerals sector, the acquisition underscores a broader trend of consolidation and vertical integration as companies seek to control strategic resources and build domestic supply chains. As demand for rare earth elements continues to expand across electric vehicles, renewable energy systems, and advanced electronics, projects like Round Top remain central to the evolving landscape of U.S. critical mineral development.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)—a high–grade Copper–PGE, Nickel, gold and silver system—toward Canada’s next polymetallic mine. On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~212.86 km² and roughly 50 km of prospective basin margins. Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs. Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025. It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s JabalSaid Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Expansion of Lion mineralization. Recent drilling at Lion East and Lion West resulted in a newly identified shallow eastward plunging structural trend that controls high grade copper mineralization and extends the Lion system beyond its previously defined limits. Step-out drilling expanded mineralization both east and west, and the emerging structural model may vector toward a larger nickel copper source at depth, enhancing the project’s long-term potential.

Encouraging results at Lion West. Drilling intersected massive nickel-bearing sulphide within the UM zone, indicating the presence of a deeper nickel-palladium-copper system much like mineralization observed at Tiger. Follow-up drilling is underway to better define the geometry and relationship to the Lion geological stratigraphy.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

TORONTO, March 3, 2026 /CNW/ – Power Metallic Mines Inc. (the “Company” or “Power Metallic”) (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt: IVV1) is pleased to provide an exploration update of recent drilling and results of regional exploration from its fall drill program

Lion East and Lion West Target Areas

Figure 1 Lion long section with Lion East and Lion West holes illustrated (drill hole intersections in Lion Zone not shown for clarity). (CNW Group/Power Metallic Mines Inc.)Figure 2 Mineralization intersected in PML-26-054 east of the Lion deposit along a shallow east plunging high grade trend (CNW Group/Power Metallic Mines Inc.)Figure 3 Mineralization intersected in PML-26-067 west of the Lion deposit along shallow east plunging high grade trend (CNW Group/Power Metallic Mines Inc.)Figure 4 – Location of PMX exploration holes with areas of interest tested in the summer-fall of 2025. (CNW Group/Power Metallic Mines Inc.)

Structural analysis of mineralization orientation from Lion Zone drill core, while confirming the dominant steep westerly plunge of the Lion Zone, also identified a shallow easterly plunge that appears to control the highest-grade zones within the Lion Zone (Figure 1). Currently four (4) easterly trending structures have been identified.

Recent drilling targeted the shallowest of these trends to determine if this mineralization trend had validity and would extend beyond the known boundaries of the Lion Zone. The first hole in this program, PML-26-054 has intersected 5m of Lion style mineralization with visible copper in narrow massive lenses (Figure 2) and disseminated and stringer style chalcopyrite.

With the confirmation of the easterly plunging trend extending high grade mineralization to the east, hole PML-26-067 was drilled on the western edge of Lion along the same structural trend in an area previously believed to be low grade, and at a vertical depth of approximately 50m this hole intersected 1m of massive copper sulphides (Figure 3) and 3.3 meters of disseminated copper mineralization. Follow-up holes are currently being drilled to establish the size of these two extensions to Lion.

Of significance, the easterly trending structure currently being tested has a trend that aligns with mineralization intersected 350 meters east of Lion in hole PML-25-021 (see news release November 4, 2025), adding further support to the structural trend. This opens the potential of hundreds of meters of strike along the trend plunge direction of this shallowest trend line.

Finally, a three additional easterly plunging trends below the shallowest one currently being tested have yet to be tested by any drilling and all have the potential to add additional zones of mineralization in both the Lion East and the Lion West areas. “The verification of this plunge trend, while expanding the Lion target area, also is acting as a vector direction towards a potential large Ni-Cu deposit that is the source for the mobilized copper mineralization, giving the geologists a new focus for this long-term exploration target”, states Joe Campbell, VP of Exploration for Power Metallic.

The Lion West target area also is actively being drilled following the magnetic high that defines the UM zone between Lion and Nisk. The first hole drilled on this target (PML-25-040) collared in the UM, so was in front of the Lion Zone stratigraphy. This established that there is an offset from the edge of the Lion Zone shifting geology to the north. Despite missing the Lion stratigraphy, below the UM the hole hit mineralization over 0.31m consisting of massive nickeliferous sulphides (2.42% Ni, 1.83 g/t Pd, 0.11% Cu) within a tonalite dyke. This mineralization is like the ‘rafted’ rip-up blocks seen at the Tiger deposit and indicate that a Ni-Pd-Cu deposit exists somewhere below the rafted block. Power Metallic has subsequently moved the drill collar further north to intersect the Lion stratigraphy structurally above the UM, and that hole is currently being drilled.

Summer-Fall Regional Drilling (PMX holes) – New Gold Zone in Hinge Area

The summer-fall 2025 regional exploration program targeted EM anomalies identified in the summer airborne survey, supplemented by surface mapping to identify favourable rock types for Ni-Cu mineralization. The EM survey produced more than 100 conductors. The initial drilling tested a variety of target areas to ascertain their prospectivity for Nisk and Lion style mineralization.

The Power Metallic properties now cover over 330 km2, and to date only 16 holes have been drilled within an area approximately 40km x 10 km in size. Each area drilled is separated by several kilometers, and individual holes are generally hundreds of meters apart, so this initial program should be treated as a first reconnaissance of the regional property.

Five target areas were tested based on EM anomalies, structural complexity, and proximity to potential ultra-mafic source rocks for Ni-Cu mineralization (Figure 4). All holes intersected sufficient semi-massive to massive sulphides to explain the EM conductors. In summary:

Zone 1 – Hinge/Hydro Lands – PMX-25-001, 002, 015, 016

This area produced the best indications of potential Ni-Cu mineralization, and possible mobilized polymetallic (Lion Style). Mineralization is dominantly pyrrhotite within or proximal to high magnesium basalts (komatiitic) and gabbros, with local pyroxenite. Of significance, all holes intersected highly anomalous arsenic and tungsten in, or proximal to, the high magnesium rocks. Both these minerals are considered pathfinders to mineralization in the Sudbury camp. Local indications of polymetallic mineralization include Pd (up to 0.10 g/t), Pt (0.11 g/t) in hole PMX-25-015, and Au (0.36 g/t) in hole PMX-25-001 in the high Mg rocks.

The four holes test an area of more than 2 km of strike along the prospective EM targets, and drill holes are hundreds of meters apart. The consistency of the alteration (As, W) and the rock types is encouraging, but the spacing of the holes is too large to provide any detailed modelling. Currently this area is being tested with follow-up drilling.

Also, of significance in this area hole PMX-25-016, the last hole in the regional program intersected a broadly anomalous gold zone in a recognizable felsic-intermediate volcanic unit (33 meters of low anomalous gold), and contained within this zone is a high-grade intersection of 34.6 g/t Au over 1.50m from 273.5m to 275.0m. This intersection contains a foliation parallel stringer of visible gold. This unit has been identified in surface mapping over several kilometers and was also intersected in hole PMX-25-15 approximately 500m to the east of PMX-25-16. Relogging and resampling of this unit in both holes was incomplete and is being carried out now. Finally, the deep hole (PML-25-021X) targeting the Elephant BHEM plate also intersected this unit approximately 600m below PMX-25-016 with possible indications of mineralization. Assays are pending from this hole.

Zone 2 – Nisk Far West – PMX-25-003

This target was an isolated EM conductor located approximately 10km west of the Nisk deposit. It failed to intersect prospective rock types or anomalous mineralization.

Zone 3 – South Basin Margin West – PMX-25-004, 005, 006, 007, 008, 010

This target tested EM anomalies with complex structures and surface mapping support for hosting UM intrusions along the southern margin of the sedimentary-volcanic basin. The 6 holes were broadly scattered across approximately 5km of strike. All holes hit significant zones of sulphides. The anomalous mineralization consisted largely of Zn, Ag, Pd, Cu, indicative of a VMS deposit style signature. Although this is not Power Metallic’s primary target type, the mineralization observed will require follow-up. There were UM rocks intersected (11m in hole PMX-25-008 as example) but they contained no significant Ni-Cu-PGE anomalism.

Zone 4 – Center Basin Tonalite – PMX-25-009, 011

Like Zone 3, the sulphide mineralization in these two holes appears to support a VMS style mineralization. There were no significant zones of UM rocks in these two holes.

Zone 5 – South Basin Margin East – PMX-25-012, 013, 014

Like Zone 3 these three holes covered approximately 5km of strike along the southern boundary of the basin. Indications from the sulphides intersected suggest a VMS style with anomalous Zn, Cu, Ag.

Elephant and Tiger Deep BHEM Targets

Drilling of the Elephant BHEM target (extension of hole PML-25-021) intersected pyrrhotite mineralization that did not appear to be Ni-Cu affinity. Follow-up BHEM has not established a strong off-hole conductor. The contact zone stratigraphy associated with the Lion deposit and the UM intrusion has been identified, but this contact did not contain UM. BHEM is currently being reassessed to develop new target vectors, and assay results on the contact zone are pending.

The first hole at Tiger Deep was collared to drill between two BHEM generated conductor plates to refine the target area. While no visual mineralization was intercepted, the geology was encouraging, and follow-up drilling is now targeting a refined BHEM plate. Assay results on the initial hole are pending.

Qualified Person

Joseph Campbell, P. Geo, VP Exploration at Power Metallic, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Metallic Mines Inc.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)–a high–grade Copper–PGE, Nickel, gold and silver system–toward Canada’s next polymetallic mine.

On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). In June 2025 the Company purchased 313 adjoining claims (~167 km²) from Li–FT Power. As of Dec 31 2025, the Company has added additional land vis its staking efforts and the Company now controls ~330 km² and roughly 50 km of prospective basin margins.

Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs.

Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025.

It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s Jabal Said Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

For further information, readers are encouraged to contact: Power Metallic Mines Inc. The Canadian Venture Building 82 Richmond St East, Suite 202 Toronto, ON

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

QAQC and Sampling

GeoVector Management Inc (“GeoVector”) is the Consulting company retained to perform the actual drilling program, which includes core logging and sampling of the drill core.

All core in this news release is NQ sized core. Drill core is re-fitted and measured. Geotech on core includes photographs (wet & dry), rock quality index, magnetic susceptibility, conductivity, and recovery estimates. Core is logged for lithology, mineralogy, and structural features, and sample intervals are delineated and tagged.

Sampled core is mechanically sawn, and half-core is retained for future reference. GeoVector’s QAQC program includes regular insertion of CRM standards, duplicates, and blanks into the sample stream with a stringent review of all results. QAQC and data validation was performed, and no material errors were observed.

All samples were submitted to and analyzed at Activation Laboratories Ltd (“Actlabs”), a commercial laboratory independent of Power Metallic with no interest in the Project. Actlabs is an ISO 9001 and 17025 certified and accredited laboratories. Samples submitted through Actlabs are run through standard preparation methods and analysed using RX-1 (Dry, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 μm) preparation methods, and using 1F2 (ICP-OES) and 1C-OES – 4-Acid near total digestion + Gold-Platinum-Palladium analysis and 8-Peroxide ICP-OES, for regular and over detection limit analysis. Pegmatite samples are analyzed using UT7 – Li up to 5%, Rb up to 2% method. Actlabs also undertake their own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibration.

This message contains certain statements that may be deemed “forward-looking statements” concerning the Company within the meaning of applicable securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential,” “indicates,” “opportunity,” “possible” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, are subject to risks and uncertainties, and actual results or realities may differ materially from those in the forward-looking statements. Such material risks and uncertainties include, but are not limited to, among others; the timing for various drilling plans; the ability to raise sufficient capital to fund its obligations under its property agreements going forward and conduct drilling and exploration; to maintain its mineral tenures and concessions in good standing; to explore and develop its projects; changes in economic conditions or financial markets; the inherent hazards associates with mineral exploration and mining operations; future prices of nickel and other metals; changes in general economic conditions; accuracy of mineral resource and reserve estimates; the potential for new discoveries; the ability of the Company to obtain the necessary permits and consents required to explore, drill and develop the projects and if accepted, to obtain such licenses and approvals in a timely fashion relative to the Company’s plans and business objectives for the applicable project; the general ability of the Company to monetize its mineral resources; and changes in environmental and other laws or regulations that could have an impact on the Company’s operations, compliance with environmental laws and regulations, dependence on key management personnel and general competition in the mining industry.

SOURCE Power Metallic Mines Inc.

For further information on Power Metallic Mines Inc., please contact: Duncan Roy, VP Investor Relations, 416-580-3862, duncan@powermetallic.com

Oil markets have swung sharply higher since the outbreak of war between the United States and Iran, with traders rapidly repricing geopolitical risk into crude benchmarks. U.S. crude rose more than 5% Monday after surging as much as 12% intraday, while Brent climbed above $77 per barrel before easing from session highs. The moves reflect mounting concern that the conflict could trigger sustained supply disruptions in one of the world’s most strategically vital energy corridors.

At the center of the market’s anxiety is the Strait of Hormuz, the narrow waterway linking the Persian Gulf to global markets. Shipping analysts report that tanker traffic through the Strait has effectively stalled as operators reassess security risks. In 2025, more than 14 million barrels per day—roughly one-third of the world’s seaborne crude exports—passed through this chokepoint. A prolonged disruption would have immediate consequences for refiners and importers across Asia, Europe, and North America.

Iran itself produces approximately 3.3 million barrels per day, ranking as OPEC’s fourth-largest oil producer. Beyond its own output, however, its geographic position gives it indirect leverage over exports from Saudi Arabia, Iraq, Kuwait, and the United Arab Emirates. The conflict introduces overlapping supply risks: potential declines in Iranian production due to instability or infrastructure damage, and constraints on maritime transit that could temporarily restrict exports from multiple Gulf producers. Even the perception of restricted flows has been enough to trigger aggressive buying in crude futures and energy-linked equities.

Major banks have begun outlining upside price scenarios if the disruption persists. Some analysts suggest Brent could approach $100 per barrel under an extended supply squeeze, while more severe regional escalation could drive prices materially higher. For now, markets are oscillating between risk premium expansion and cautious optimism that diplomatic channels could reopen. President Donald Trump stated that U.S. combat operations will continue until objectives are met, while also indicating openness to talks. Iranian officials have publicly rejected negotiations, adding to uncertainty over the conflict’s trajectory.

The implications extend well beyond the energy sector. A sustained rally in crude would complicate global inflation dynamics at a time when central banks have been attempting to stabilize price pressures. Higher oil prices feed directly into transportation, manufacturing, and consumer goods costs, potentially delaying interest rate normalization. Equity markets, particularly rate-sensitive and consumer-facing sectors, could experience renewed volatility if energy-driven inflation reaccelerates.

For small- and mid-cap companies, the effects are uneven. Domestic exploration and production firms may benefit from improved pricing and stronger cash flow if elevated crude levels persist. Oilfield services providers could also see renewed capital spending from producers seeking to capitalize on higher margins. Conversely, airlines, logistics operators, chemicals manufacturers, and other fuel-intensive businesses face margin compression if input costs rise faster than pricing power allows. Emerging market equities in energy-importing nations may also encounter currency and trade balance pressures.

The broader theme resurfacing in 2026 is the fragility embedded in global supply chains. While U.S. shale growth and diversified sourcing have added resilience over the past decade, the Strait of Hormuz remains irreplaceable in the near term. Even with strategic petroleum reserves and spare capacity assumptions, a chokepoint freeze underscores how quickly geopolitical flashpoints can ripple through commodity markets and financial assets.

Oil is once again functioning as a real-time geopolitical barometer. Until tanker traffic resumes at scale or a clearer diplomatic path emerges, volatility is likely to remain elevated. Investors across asset classes will be watching crude not only as an energy benchmark, but as a signal of broader macroeconomic risk.

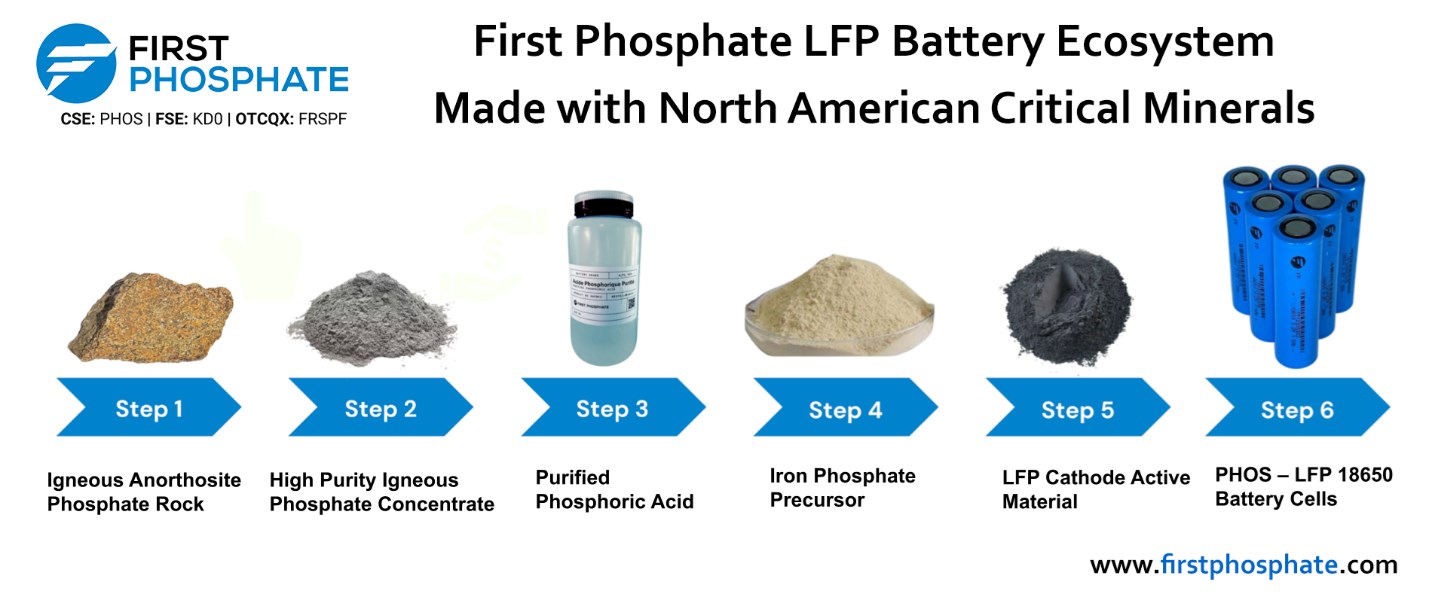

Saguenay, Québec–(Newsfile Corp. – March 2, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) has been conditionally approved for a non-repayable contribution agreement for up to C$16.7 million with the Government of Canada through Natural Resources Canada (“NRCan”) under the Global Partnerships Initiative (“GPI”).

This contribution funded by the Government of Canada will be deployed to assess the technical and engineering parameters – including processing circuits and equipment – needed to validate the ability to produce a phosphate concentrate that meets the quality requirements of the lithium iron phosphate (“LFP”) battery market. The work will be conducted based on the parameters established under the contract between First Phosphate and its definitive offtaker.

“Canada and our partners are putting real capital behind the secure and resilient critical mineral supply chains that our economies and defence industries rely on,” said The Honourable Tim Hodgson, Minister of Energy and Natural Resources. “By supporting companies like First Phosphate, we are helping deliver the minerals the world needs and the prosperity and security Canadians deserve.”

“This financial support of the Government of Canada represents an important lever for the continuation of our development work,” stated Armand MacKenzie, President of First Phosphate. “This contribution enables us to carry out detailed work aimed at validating LFP application requirements and the expectations of our offtakers and international partners.”

The development work will help strengthen Canada’s strategic positioning within the LFP battery value chain through the development of domestic capacity to process apatite (phosphate concentrate) into high-purity phosphoric acid (“PPA”) for battery applications.

The project will develop a scalable Canadian process for the production of battery-grade phosphate concentrate, reducing dependence on foreign supply chains.

The activities will contribute to significant economic benefits, including the creation of skilled jobs and the potential establishment of a Canadian phosphoric acid facility supported by local commercial production of phosphate concentrate.

The financial contribution is granted for the completion of a study of the Company’s integrated phosphate concentrate project in Saguenay-Lac-Saint-Jean and covers eligible activities planned through 2028, in accordance with the terms of the agreement. It forms part of an initiative to support industrial collaboration and the integration of Canadian projects into international supply chains for battery materials.

The scientific and technical disclosure for First Phosphate included in this news release has been reviewed and approved by Gilles Laverdière, P.Geo. Mr. Laverdière is Chief Geologist of First Phosphate and a Qualified Person under National Instrument 43-101 – Standards of Disclosure of Mineral Projects (“NI 43-101”).

About Natural Resources Canada

Natural Resources Canada (“NRCan”) is the federal department responsible for developing policies and programs to ensure the sustainable and responsible development of Canada’s natural resources. Through its initiatives and funding programs, including the International Partnerships Program, NRCan supports projects that contribute to strengthening supply chains, industrial innovation, and Canada’s competitiveness in the critical and strategic minerals sectors.

About First Phosphate Corp

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay-Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

Forward-Looking Information and Cautionary Statements

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, this press release contains forward-looking information relating to, among other things: the execution and final terms of a written contribution agreement to be entered into among the parties and the Company’s compliance with the terms thereof; the funding amount, anticipated benefits, timing, and potential outcomes of the GPI funding award under the contribution agreement with NRCan and the project funded thereby including, but not limited to, the strengthening of Canada’s strategic positioning within the LFP battery value chain, the development of domestic capacity to process apatite into high-purity PPA for battery applications, the development of a scalable Canadian process for the production of battery-grade phosphate concentrate, the reduction of dependence on foreign supply chains, and the contribution to significant economic benefits, including the creation of skilled jobs and the potential establishment of a Canadian phosphoric acid facility; and the Company’s plans for building and onshoring a vertically integrated mine-to-market LFP battery supply chain for North America. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things, assumptions regarding general business and economic conditions; there being no significant disruptions affecting the activities of the Company or inability to access required project inputs; permitting and development of the projects being consistent with the Company’s expectations; the accuracy of the current mineral resource estimates for the Company and results of metallurgical testing; certain price assumptions for P2O5 and Fe2O3; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the Company’s relationship with First Nations and other Indigenous parties remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

Saguenay, Quebec–(Newsfile Corp. – February 27, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) applauds the amendment to the 2025 Canadian federal budget which passed yesterday to include phosphate on the list of critical minerals essential for clean technology.

Phosphate exploration and downstream processing facilities will now benefit from numerous Canadian federal programs dedicated to key critical minerals including these two essential tax credit programs:

The Critical Mineral Exploration Tax Credit (“CMETC”), a 30% Canadian refundable tax credit for Canadian investors in junior mining companies in respect of targeted exploration expenses.

The Clean Technology Manufacturing Investment Tax Credit (“CTM”), a 30% refundable tax credit for Canadian corporations investing in new machinery and equipment for manufacturing clean technologies or processing critical minerals.

The CMETC will assist First Phosphate in raising funds geared towards further exploring and developing its mineral properties in Saguenay-Lac-St-Jean, Quebec and to continue to develop the region’s district-level phosphate zone.

The CTM will be beneficial to First Phosphate in building out infrastructure associated with the operating and mining of its advanced phosphate properties as well as its future downstream processing facilities such as the planned phosphoric acid plant and the planned lithium iron phosphate (“LFP”) cathode active material plant.

First Phosphate wishes to thank members of the Standing Committee on Finance, Canada and members of the Standing Committee on Natural Resources, Canada for recognizing that phosphate is no longer just about fertilizer but also about high technology. An overwhelming majority of batteries produced on the planet are now based on LFP chemistry of which the majority of the cathode is comprised of high-purity phosphate such as the type found on First Phosphate properties in Saguenay-Lac-St-Jean, Quebec.

The high-purity phosphoric acid for these LFP 18650 battery cells was produced using rare igneous anorthosite rock extracted from the Company’s Bégin-Lamarche property in Saguenay-Lac-Saint-Jean, Quebec.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration, development and cleantech company dedicated to examining and ultimately building and onshoring a vertically integrated mine-to-market lithium iron phosphate (LFP) battery supply chain for North America. Target markets include energy storage, data centers, robotics, mobility and national security.

First Phosphate’s flagship Bégin-Lamarche Property in Saguenay-Lac-Saint-Jean, Quebec, Canada is a North American rare igneous phosphate resource yielding high-purity phosphate with minimal impurities.

Forward-Looking Information and Cautionary Statements

This release includes certain statements that may be deemed “forwarding information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, this press release contains forward-looking information relating to, among other things: the assistance the CMETC will provide First Phosphate in raising funds geared towards exploring and developing its mineral properties in Saguenay-Lac-St-Jean, Quebec and to continue to develop the region’s district-level phosphate zone; the benefit the CTM will provide First Phosphate in building out infrastructure associated with the operating and mining of its advanced phosphate properties as well as its future downstream processing facilities such as the planned phosphoric acid purification plant and the planned LFP cathode active material plant; the Company’s planned exploration and production activities and the results thereof; the properties and composition of any extracted phosphate; the Company’s plans relating to the design, build, operation and maintenance of operations and mining at its Bégin-Lamarche property or elsewhere (and the possibility of eventual economic extraction of minerals from therefrom); the achievement and completion of all required steps to build and operate facilities to process phosphate concentrate, and phosphoric acid, including, without limitation, access to financing, and regulatory and environmental approvals; and the Company’s plans for building and onshoring a vertically integrated mine-to-market LFP battery supply chain for North America. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things, assumptions regarding general business and economic conditions; there being no significant disruptions affecting the activities of the Company or inability to access required project inputs; permitting and development of the projects being consistent with the Company’s expectations; the accuracy of the current mineral resource estimates for the Company and results of metallurgical testing; certain price assumptions for P2O5 and Fe2O3; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the Company’s relationship with First Nations and other Indigenous parties remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Operational momentum continues. Nicola reported a significant increase in throughput of high-grade gold and silver mill feed from its partnership with Blue Lagoon Resources at the Dome Mountain Gold Project. Processing at the Merritt Mill has shifted from a gravity-and-flotation circuit to a flotation-only flowsheet, better aligning with the sulphide-hosted mineralization and enhancing recoveries, concentrate grades, and payable metal output. Ongoing plant upgrades are expected to improve efficiency and throughput. Underground development at Dome Mountain is progressing, with additional mining faces being prepared to support sustainable increases in mill feed tonnage.

Advancing the next phase of gold production at Dominion Creek. Dominion represents an additional driver of growth, targeting high-grade gold mineralization. Nicola is procuring needed mobile equipment and personnel ahead of the planned extraction in July 2026 under a bulk sample permit. The bulk sample program is intended to validate grade continuity, metallurgical performance, and mining selectivity, while also contributing incremental cash flow.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent assay results confirm strong nickel-cobalt grades. Aurania reported results from 28 new samples at the Balangero Nickel-Cobalt Project in northern Italy, returning nickel values between 1,560 and 2,015 parts per million (ppm) and averaging 1,763 ppm, along with 81.5 to 108 ppm cobalt and 16.2 to 146 ppm copper. These results align with more than 200 historical samples and validate the presence of awaruite, a nickel-iron alloy suitable to be used as a direct source of furnace feed for stainless steel production or processed downstream EV battery-grade nickel sulphate production. Notably, samples from development rock piles were confirmed to be asbestos-free, potentially expanding the resource base beyond tailings.

A differentiated alternative to greenfield peers. Unlike comparable awaruite-focused projects, which require full mine development, Balangero’s potential resource consists primarily of dry-stacked, pre-crushed tailings and surface rock already extracted from the ground. This eliminates the need for drilling, blasting, and underground haulage. The project benefits from electric power, rail access, highway connectivity, and an available skilled workforce, positioning it as a potentially accelerated development opportunity with significant cost advantages.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Toronto, Ontario–(Newsfile Corp. – February 26, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) reports that results have been delivered from 28 samples taken across the Balangero Ni-Co Project (the “Project”) in northern Italy. The samples were assayed at Laboratoire GeoRessources – École Nationale Supérieure de Géologie, Université de Lorraine. The samples yielded between 1560 and 2015 ppm nickel (average 1763 ppm), 81.5 to 108 ppm cobalt, and 16.2 to 146 ppm copper. These new results are in line with the more than 200 historical samples taken from the site.

Aurania’s President and CEO, Dr. Keith Barron, commented, “There is a lot of historic data from Balangero, and this confirmed what was already suspected. In 1942, the Italian Government created SANI (Societá Anonima Nichelio Italiana) specifically to look for sources of nickel within Italy. At Balangero, the magnetic sand-sized fraction of the waste from asbestos beneficiation was actually recovered and used to make hardened steel for some months in 1943 for the war effort. This information has remained buried in the Archive of the City of Turin. For a variety of reasons, nickel supply has once again become critically important in Europe, and we believe Balangero offers the most readily and easily accessible source of the metal today.”

The Balangero Mine (also called San Vittorio), 30 kilometres from the city of Turin in northern Italy, produced asbestos between 1918 and 1990 and was the largest open pit asbestos mine in Europe. During 1966, the waste from the mine was thoroughly investigated as a potential by-product source of nickel and cobalt. Aurania staff became acquainted with the project while doing a literature search on their Northern Corsica Ni-Co project. The Balangero site, like Corsica, contains an abundance of the mineral awaruite, a rather rare nickel-iron natural alloy that does not contain sulphur, and can be used as a direct source of furnace feed for stainless steel production, or processed downstream for EV Battery Grade nickel sulphate. As a potential source of “Green” nickel, it certainly aligns with the stated goals of the European Union (EU) for the extraction and production of Clean Critical Metals.

Several companies are looking at the small number of awaruite occurrences as potential sources of Green Nickel and Cobalt. Among them are FPX Nickel Corp, with a market capitalization of circa $183 million CAD, and First Atlantic Nickel Corp, with a market capitalization of $27 million CAD. FPX’s project is in northern British Columbia, and First Atlantic, in Central Newfoundland. Both are greenfields projects which will require the development of open pit mines. Both have limited site infrastructure, other than a few bush roads. Aurania’s Balangero Project is essentially identical in nickel grade to FPX and First Atlantic, but with the obvious difference in projects is that the potential resource at Balangero consists of dry-stacked tailings that have already been crushed to <4 centimetres. This material has already been extracted from the ground, negating any need for drilling, blasting, tunneling and haulage from the subsurface. Moreover, there is existing electric power to the site, a railhead less than a kilometre away, a paved highway to the mine gate, and an abundant source of skilled labour nearby.

A Preliminary Economic Assessment (PEA) for the Balangero Project, in progress by SRK International Consultants, will provide an estimation of Aurania’s proposed project capex, but obviously there is no need for expensive installation of infrastructure, overburden stripping, and mining of the rock, resulting in tremendous cost savings. The Company is discussing whether to carry out a Pre-feasibility Study (PFS) before the end of 2026. Recently, a legal opinion determined that Aurania could perform Sonic Drill Sampling and Bulk Sampling on the Project under the existing permits of our MOU partner, RSA, rather than submitting lengthy environmental impact studies. This would substantially accelerate the project timetable. The Company believes the Project could be fast-tracked under the European Union’s Critical Raw Materials Act. Nickel, cobalt and copper are all considered “Strategic Raw Materials” (SRM). The 17 SRM are a subset within the designated 34 Critical Raw Materials and are mandated to be domestically sourced in the EU.

Aurania has also had confirmation from Dr. Chiara Boschi at the Institute of Geosciences and Earth Resources (IGG-CNR, Pisa, Italy) that a number of the 28 collected samples from across the Balangero Project do not contain asbestos, but all contain awaruite. These samples which were asbestos-free were taken from old development rock piles. This suggests that the potential nickel resource at Balangero will ultimately consist of both crushed tailings and broken and excavated development rock at the surface. There is no historical measurement of the volume of these rock piles, though this will be assessed in future. We expect inclusion of these development rock piles to be accretive to the Project.

Comminution tests of the Balangero tailings are still in progress at STEVAL in Nancy, France. To date, the material appears amenable to easy extraction of the awaruite and magnetite, and there have been no “red flags”. A sonic drilling programme to confirm the grades and thicknesses in the main tailings pile is being contemplated for April 2026.

Qualified Persons: The geological information contained in this news release has been verified and approved by Aurania’s VP Exploration, Mr. Jean-Paul Pallier, MSc. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About Aurania Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes: that if results of the MOU prove favourable, a commercial agreement is expected to be entered into with respect to the extraction of minerals from the waste piles, the assumption that the waste pile may have the potential to contain circa 229,500 tonnes of nickel, that this represents a valuable resource which has already been extracted, crushed and dry-stacked, the expectation that the evaluation of 450 kg of material will provide mineralogical characterization and other expected information about such material, the timing to produce a Scoping Level Review on the Mineral Assets of the Balangero tailings retreatment project, Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the tonnage and grade of mineralization which has the potential for economic extraction and processing, the merits and effectiveness of known process and recovery methods, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that, there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things: failure to achieve the anticipated results, incorrect assumptions made in the initial evaluation of the project, failure to identify mineral resources; failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; the inability to recover and process mineralization using known mining methods; the presence of deleterious mineralization or the inability to process mineralization in an environmentally acceptable manner; commodity prices, supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and base metals; and those risks set out in the Company’s public documents filed on SEDAR+. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

Saguenay, Quebec–(Newsfile Corp. – February 25, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the launch of its sponsored Level 1 American Depositary Receipt (“ADR“) program to increase exposure to American and international investors wishing direct access to Quebec igneous phosphate and the downstream lithium iron phosphate (“LFP“) battery supply chain.

The First Phosphate ADR is now available for trading in the United States on the OTCQX market under the symbol “FPHOY” (CUSIP: 33611D301; ISIN: US33611D3017).

The First Phosphate ADR is the first Canadian Level 1 company-sponsored ADR to trade on OTC Markets. The ADR ratio is set to ten (10) First Phosphate common shares for each (1) First Phosphate ADR.

Participants may issue ADRs at no cost during the first 6 months after the effectiveness date of the program (February 12, 2026) through The Bank of New York Mellon (“BNY“) which has been appointed as depositary bank for the First Phosphate ADR program.

The new First Phosphate ADR is complimentary to all other Company listings on all other stock exchanges and does not affect the Company’s current OTCQX listed common shares under symbol “FRSPF“.

BNY facilitates the issuance and cancellation of First Phosphate ADRs in accordance with instructions received from market participants. The First Phosphate ADR program operates in accordance with a deposit agreement, filed with the United States Securities and Exchange Commission (“SEC“) and available through https://www.sec.gov/Archives/edgar/data/2108542/000101915526000028/0001019155-26-000028-index.htm. The First Phosphate common shares underlying the First Phosphate ADRs are held in custody by BNY.

The establishment of the First Phosphate ADR program is not a new offering of securities and, therefore, no additional shares are being issued nor is any capital being raised in connection with the launch of the First Phosphate ADR program. Moreover, nothing herein shall be deemed to constitute an offer to sell or a solicitation of an offer to buy securities.

An ADR is a separate security denominated in US dollars that allows US investors to invest in shares of non-US companies without the need for cross-border or cross-currency transactions.

Initial Payment Received Under Long-term Offtake Agreement

The Company has now received the initial payment of USD $523,017.59 in respect of the existing, long-term phosphate concentrate offtake agreement with its existing offtake partner as announced on January 6, 2026 (https://firstphosphate.com/offtakepayment).

Options Exercise & RSU Grants

Z Six Financial Corporation, an entity controlled by Laurence W. Zeifman, Chaiman of the Board of First Phosphate, has exercised 300,000 options originally issued on September 14, 2022 and exercisable at $0.25 and 300,000 options originally issued on December 22, 2022 and exercisable at $0.35 per option.

Pursuant to an exemption granted by the Canadian Securities Exchange to Policy 6.5(7), the Company has issued 781,395 Restricted Share Units (“RSUs“) to ExpoWorld Ltd. (“ExpoWorld“), an entity controlled by John Passalacqua, CEO of First Phosphate, as consideration for the termination of 1,200,000 options held by ExpoWorld including 600,000 options originally issued on September 14, 2022 and exercisable at $0.25 per option, and 600,000 options originally issued on December 22, 2022 and exercisable at $0.35 per option (the “Options“). These vested RSUs represent the in-the-money value of the Options being terminated (calculated based on the closing price of First Phosphate shares on February 10, 2026) and serve to facilitate the cashless exercise of options while minimizing the impact that the transaction would have on the open market.

The Company also informs that Mr. Passalacqua, through ExpoWorld, made an open market purchase of 119,500 shares in the open market on January 30, 2026.

As a show of commitment to the business and alignment with shareholders, the Board and management will receive approximately 50% of their total compensation in the form of RSUs. As such, the Board has approved the grant of 1,975,000 RSUs to eligible directors, officers, consultants and employees of the Company for services to be provided for the 12-month period commencing March 1, 2026. One-half of these new RSUs will vest on August 31, 2026 and February 28, 2027, respectively. All of the common shares issuable on vesting of the RSUs will be subject to a hold period of four months plus one day from the date of vesting. The RSUs will be granted in accordance with and subject to the Company’s Omnibus Equity Incentive Plan.

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration, development and cleantech company dedicated to examining and ultimately building and onshoring a vertically integrated mine-to-market lithium iron phosphate (LFP) battery supply chain for North America. Target markets include energy storage, data centers, robotics, mobility and national security.

First Phosphate’s flagship Bégin-Lamarche Property in Saguenay–Lac-Saint-Jean, Quebec, Canada is a North American rare igneous phosphate resource yielding high-purity phosphate with minimal impurities.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2026 guidance. InPlay approved a C$66 to C$74 million capital program targeting average production of 18,600 to 19,200 boe/d (~61% light oil and NGLs), representing approximately 11% growth over the estimated 2025 production of ~17,000 boe/d. Management forecasts adjusted funds flow (AFF) of C$122 to C$129 million and free adjusted funds flow (FAFF) of C$48 to C$63 million, implying an 11% to 15% FAFF yield. Year-end net debt is guided to C$199 to C$206 million, reflecting continued deleveraging.

Estimate revisions. We have adjusted our 2026 estimates to average production of 18,900 boe/d, revenue of C$338.3 million, and AFF of C$125.2 million, or C$4.45 per share. For Q1 2026, we have assumed production of 18,605 boe/d, revenue of C$79.0 million, and AFF of C$26.6 million, or C$0.95 per share. The first quarter carries heavier drilling activity, with five wells drilled and completed, most coming onstream late in the period, marking Q1 as the lightest production quarter of the year. We forecast 2026 capital expenditures of C$70 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")

. (CNW Group/Power Metallic Mines Inc.)")

")

")

")

{kind=link}

{kind=link}