MIAMI, Feb. 01, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”), today announced that it has entered into a definitive agreement for the issuance and sale of an aggregate of 183,020 shares of the Company’s Class A common stock at a purchase price of $21.40 per share in a registered direct offering priced at-the-market under Nasdaq rules. The closing of the offering is expected to occur on or about February 3, 2023, subject to the satisfaction of customary closing conditions.

H.C. Wainwright & Co. is acting as the exclusive placement agent for the offering.

The gross proceeds to Motorsport Games from the offering are expected to be approximately $3.9 million, before deducting the placement agent’s fees and other offering expenses payable by the Company. Motorsport Games currently intends to use the net proceeds from the private placement for development of multiple games, working capital and general corporate purposes.

The shares of Class A common stock described above are being offered and sold by the Company pursuant to a “shelf” registration statement on Form S-3 (Registration No. 333-262462), including a base prospectus, previously filed with the Securities and Exchange Commission (SEC) on February 1, 2022 and declared effective by the SEC on February 10, 2022. The offering of the shares of Class A common stock are being made only by means of a prospectus supplement that forms a part of the registration statement. A final prospectus supplement and an accompanying base prospectus relating to the offering will be filed with the SEC and will be available on the SEC’s website located at http://www.sec.gov. Electronic copies of the final prospectus supplement and accompanying base prospectus may also be obtained by contacting H.C. Wainwright & Co., LLC at 430 Park Avenue, 3rd Floor, New York, NY 10022, by phone at (212) 856-5711 or e-mail at [email protected].

This press release shall not constitute an offer to sell or a solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or jurisdiction.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, market and other conditions, statements regarding the completion of the registered direct offering, the satisfaction of customary closing conditions related to the registered direct offering and the anticipated use of proceeds therefrom. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Motorsport Games, a Motorsport Network company, combines innovative and engaging video games with exciting esports competitions and content for racing fans and gamers around the globe. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”). Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Debt for equity swap. The company announced that it entered into an agreement with its majority shareholder, Motorsport Network, to repay $1 million in debt for 338,983 MSGM shares. The move significantly improves the company’s liquidity and reduces its interest expense. Notably, the move adds confidence that Motorsport Network has confidence in Motorsport Games.

Regains compliance with listing rules. Following the move, the company received notice from Nasdaq that Motorsport regained full compliance with the Nasdaq Listing Rules.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MIAMI, Jan. 31, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or “Company”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, announced today that it has received notice from the Nasdaq Stock Market LLC (Nasdaq) on January 30, 2023 informing Motorsport Games that it has regained full compliance with the Nasdaq Listing Rules.

Motorsport Games previously notified Nasdaq on November 11, 2022 that it was no longer in compliance with Nasdaq Listing Rule 5550(a)(4) requiring minimum of 500,000 publicly held shares, as defined in the Nasdaq Listing Rules, and (ii) Nasdaq Listing Rule 5605(b)(1), which requires a majority of the Company’s board of directors (the “Board”) to be comprised of independent directors as defined in Rule 5605(a)(2), and Nasdaq Listing Rule 5605(c)(2), which requires the audit committee of the Board to consist of at least 3 independent directors meeting the heightened independence standards for audit committee members.

As previously disclosed by the Company, as a result of the issuances by the Company to Alumni Capital LP of the Company’s Class A common stock pursuant to the previously reported purchase agreement with Alumni Capital LP, the Company’s publicly held shares exceeded 500,000 shares. Dmitry Kozko, Chief Executive Officer of Motorsport Games, commented, “With the addition of Nav Sunner in January and Andrew Jacobson in December, joining John Delta as independent directors, the board of directors is reconstituted adding significant talent and resources to our collective experience.”

Bios:

Nav Sunner is a highly experienced lawyer and business development expert immersed in the video games industry. After qualifying as a lawyer with Pinsent Masons, he spent several years as Head of Legal at Codemasters as well as General Counsel at Mastertronic Group. Following a further period practicing law as Co-Head of Interactive Entertainment for Osborne Clarke and, subsequently, as Head of Computer Games for Wiggin, Nav worked with Japanese games company GREE. Nav then spent time as Commercial Director for a games studio at Microsoft as well as being on the Board of esports company EGL. Currently, in addition to his video game consultancy “Navatron,” he is a Director at MMO games company Vavel. Nav’s long career in the video games industry has included extensively being involved with legal and business issues relating to racing games.

Andrew Jacobson is a digital media sales and marketing executive with over two decades of leadership experience in the online publishing, ad tech and automotive industries. During his career he has guided teams and companies – both large and startups – to record sales and revenue growth. In his current position, he leads Epsilon’s automotive programmatic digital media client team, and acts as a consultant to publishers and startups on strategy, product development, CRM, programmatic monetization, organization structure and compensation planning. In 2015, as Global Head of Sales, Andrew was part of the leadership team that grew and sold digital media company VerticalScope Holdings for more than $300 million. He has been a top-rated speaker, moderator and panelist at many industry conferences including J.D. Power Automotive Marketing Roundtable, SEMA, Programmatic I/O, Digital Dealer, Automotive Attribution Summit and others. Andrew holds a B.A. from Pomona College and an M.B.A. from the Kellogg School of Management, Northwestern University.

John Delta is an experienced operating and financial executive and entrepreneur with experience in enterprises from $2 million to $500 million. He is currently a Partner at TechCXO, which provides outsourced on demand C-Suite executives to institutionally-backed companies. He was formerly a consultant at McKinsey & Co. and Deloitte & Touche and was Vice President of Interactive Services at the NASDAQ Stock Market. He has extensive experience with both portfolio companies of Private Equity firms and US and international publicly traded companies. His main areas of focus are mid-stage software, SaaS and consumer-facing firms in need of assistance with CFO duties, transaction execution and scaling their finance/operations. John has broad consulting, operations and finance experience, and holds both a BA and MBA from the University of Virginia.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, whether provided the Company will be able to maintain its compliance with the Nasdaq Listing Rules. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”) today announced that the Company has entered into a debt-for-equity exchange agreement (the “Agreement”) with its majority stockholder, Motorsport Network, LLC (“Motorsport Network”), to repay $1,000,000 in debt (including principal and accrued and not yet paid interest) of the Company under its $12 million line of credit with Motorsport Network.

Under the Agreement, for a period of 60 days from the closing of the transactions contemplated under the Agreement, the Company agreed to file a registration statement with the Securities and Exchange Commission (“SEC”) upon Motorsport Network’s demand in order to register the resale of the shares acquired by Motorsport Network under the Agreement, subject to the terms and conditions of the Agreement. The Agreement also granted certain piggyback registration rights to Motorsport Network.

“This debt exchange benefits our balance sheet, allows us to pay less interest expense and will help Motorsport Games to pursue product development and growth opportunities,” said Dmitry Kozko, CEO and Executive Chairman of Motorsport Games. “This debt exchange also signals the ongoing confidence that our majority shareholder, Motorsport Network, has in Motorsport Games.”

The foregoing summary of the Agreement is incomplete, and further details relating to the Agreement, including additional terms and conditions, and this transaction will be contained in the Current Report on Form 8-K the Company intends to file with the SEC later today.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward Looking Statements:

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, issuance of shares of Class A common stock under the Agreement impacting the value of the Company’s Class A common stock and less than expected benefits, such as the ability to develop product and achieve growth, from any transaction under the Agreement. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Adam Breeden, the pioneer of competitive socialising in the UK and entrepreneurial force behind some of the sector’s most successful concepts, has officially opened his most ambitious and exciting project. F1® Arcade, the world’s first official premium F1 experiential venue, opened on December 12, 2022 in London at One New Change, St Pauls.

The immersive state of the art F1 racing simulation experience comes with 60 motion F1 simulators, powered by the rFactor 2 racing simulation software provided by Motorsport Games, combined with exclusive F1® content, enabling guests to live the thrill of racing, complemented by a best-in-class food and beverage offering created by an executive chef and expert mixologists.

“With a mission of making the thrill of motorsports available to everyone, we graciously appreciate the selection of rFactor 2 to provide the virtual racing experience and real world handling and competition to F1® Arcade and their customers!” said Dmitry Kozko, CEO, at Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world.

Dom Duhan, Executive Producer at Studio 397 added, “It was a pleasure for our expert simulation development team at Studio 397 to collaborate on developing the racing elements, and we expect that customers will be blown away by the experience.”

“Since opening F1® Arcade in December, the take up has been absolutely phenomenal. Our ambition was to introduce a truly innovative experience that makes sim racing accessible for all in a fun and premium competitive socialising environment. To deliver on this, we needed a partner that could fully tailor the game experience, which is why we selected rFactor 2 and Motorsport Games to work with us on this project. The reaction from customers in our first month has been fantastic and we look forward to welcoming many more at our first London venue and future venues as we expand,” said Adam Breeden, Founder and Chief Executive of Kindred Concepts.

Future plans for F1® Arcade include a Birmingham, UK site in 2023 with further locations powered by rFactor 2 set to be announced. For all F1® Arcade news, be sure to follow @F1Arcade on social media platforms.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements include, but are not limited to, statements concerning expectations and benefits of the rFactor 2 simulation platform in powering F1® Arcade, as well as expectations that future F1® Arcade locations will be powered by the rFactor 2 simulation platform. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to: difficulties, delays in or unanticipated events that may impact the timing and expected benefits of the rFactor 2 simulation platform, such as rFactor 2 updates and/or related products and features. Factors other than those referred to above could also cause Motorsport Games’ results to differ materially from expected results. Additional examples of such risks and uncertainties include, but are not limited to: (i) delays and higher than anticipated expenses related to the ongoing and prolonged COVID-19 pandemic, any resurgence of COVID-19 and the Russia invasion of Ukraine; (ii) Motorsport Games’ ability (or inability) to maintain existing, and to secure additional, licenses and other agreements with various racing series; (iii) Motorsport Games’ ability to successfully manage and integrate any joint ventures, acquisitions of businesses, solutions or technologies; (iv) unanticipated operating costs, transaction costs and actual or contingent liabilities; (v) the ability to attract and retain qualified employees and key personnel; (vi) adverse effects of increased competition; (vii) changes in consumer behavior, including as a result of general economic factors, such as increased inflation, higher energy prices and higher interest rates; (viii) Motorsport Games’ inability to protect its intellectual property; and/or (ix) local, industry and general business and economic conditions. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Tough comps ahead. The conventional investment scenario is to expect a weak first half of 2023 and a stronger second half. However, we believe the absence of high margin political advertising and the dissolution of the WynnBet partnership calls for a more conservative outlook for 2023. In our view, there are troubling near term signs for the company that have led us to take a more sober outlook for 2023.

Economic headwinds and National advertising. Weakness in National advertising continues to be prevalent as macroeconomic headwinds persist. Additionally, we believe Local advertising is starting to show weakness.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers. Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony, and IBM among others. Headquartered in Chelmsford, Massachusetts , Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific .

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 Preview. Fundamentals at the company appear favorable and Q4 revenue and adj. EBITDA estimates appear to be on target. We are adjusting our EPS estimate to reflect the repurchase of its convertible preferred shares with Wipro. The agreement was for liquidation value at $9.9 million, plus 100,000 HHS shares. Due to an accounting treatment, the company is expected to report a non cash $1.6 million loss on the repurchase. We are adjusting our Q4 EPS from $0.34 to $0.12 to reflect this charge.

Q1 Outlook. The company’s first quarter revenue mix is expected to skew toward lower margin revenue business, plus the company is expected to spend more heavily on technology investments and for the integration of a recent acquisition, InsideOut. Q1 revenues are expected to increase year over year, but Adj. EBITDA is expected to be lower.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, NY / ACCESSWIRE / January 19, 2023 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME)(TSXV:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced the Company has received notice from The Nasdaq Stock Market (“NASDAQ”) on January 19, 2023 informing Engine that it has regained compliance with the minimum bid price requirement under NASDAQ Listing Rule 5550(a)(2) for continued listing on The Nasdaq Capital Market. Consequently, Engine is now in compliance with all applicable listing standards and its common stock will continue to be listed on The Nasdaq Capital Market.

Engine was previously notified by NASDAQ on June 23, 2022 that it was not in compliance with the minimum bid price rule because its common stock failed to meet the closing bid price of $1.00 or more for 30 consecutive business days. In order to regain compliance with the Rule, the Company was required to maintain a minimum closing bid price of $1.00 or more for at least 10 consecutive trading days. This requirement was met on January 18, 2023, the tenth consecutive trading day when the closing bid price of the Company’s common stock was over $1.00.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME)(TSXV:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine Gaming generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Cautionary Statement on Forward-Looking Information

This news release contains forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Engine to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. In respect of the forward-looking information contained herein, Engine has provided such statements and information in reliance on certain assumptions that management believed to be reasonable at the time. Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements stated herein to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Actual results could differ materially from those currently anticipated due to a number of factors and risks. Accordingly, readers should not place undue reliance on forward-looking information contained in this news release.

The forward-looking statements contained in this news release are made as of the date of this release and, accordingly, are subject to change after such date. Engine does not assume any obligation to update or revise any forward-looking statements, whether written or oral, that may be made from time to time by us or on our behalf, except as required by applicable law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Company Contact:

Lou Schwartz 647-725-7765

Investor Relations Contact:

Shannon Devine MZ North America Main: 203-741-8811 [email protected]

Engine Gaming and Media, Inc. (NASDAQ:GAME) (TSX-V:GAME) provides premium social sports and esports gaming experiences, as well as unparalleled data analytics, marketing, advertising, and intellectual property to support its owned and operated direct-to-consumer properties, while also providing these services to enable its clients and partners. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; WinView Games, a social predictive play-along gaming platform for viewers to play while watching live events; and Frankly Media, a digital publishing platform used to create, distribute and monetize content across all digital channels. Engine Media generates revenue through a combination of direct-to-consumer fees, streaming technology and data SaaS-based offerings, and programmatic advertising. For more information, please visit www.enginegaming.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results. The company reported revenue of $10.3 million, which beat our estimate of $9.8 million by 5%. Revenue was better than expected despite a decrease in advertising revenue due to changes in the algorithms that drive audience traffic. Adj. EBITDA for the quarter was a loss of $2.7 million, in line with our estimate.

Favorable influencer analytics trends. Management noted that there is heightened demand for influencer marketing. Notably. influencer and gaming analytics software as a service (SaaS) revenue grew by 34.6% on a year over year basis, helping to offset a decline in advertising revenues.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, NY / ACCESSWIRE / January 17, 2023 / Engine Gaming and Media, Inc. (“Engine” or the “Company”) (NASDAQ:GAME)(TSXV:GAME), a data-driven, gaming, media and influencer marketing platform company, today announced results for its fiscal first quarter 2023 ended November 30, 2022. All amounts are stated in U.S. dollars unless otherwise indicated.

Financial Highlights:

The Company announced the successful completion of its strategic process resulting in the signed merger agreement with GameSquare Esports, Inc

For the fiscal first quarter 2023 net loss improved significantly to $5.4 million, compared to $15.2 million in the fiscal fourth quarter 2022, an improvement of 65%

Significant improvement in Adjusted EBITDA of 32% to $(2.7) million in the first fiscal quarter 2023 sequentially compared to an Adjusted EBITDA of $(4.0) million in the fiscal fourth quarter 2022

The Company’s Influencer and Data Technology SaaS revenues increased 35% during the first fiscal quarter of 2023 compared to the first fiscal quarter of 2022

Management Commentary

“We are proud of the continued improvement we have made towards our near-term goal of achieving cash-flow breakeven. This quarter is highlighted by a 65% improvement in net loss of nearly $10 million and a 32% improvement in Adjusted EBITDA on a sequential basis to $(2.7) million, despite the restructuring charges related to discontinued operations said Lou Schwartz, Chief Executive Officer of Engine. “Despite some expected short-term headwinds in the advertising market, driven by Google algorithm changes, we continue to see heightened demand for our influencer and data technology SaaS services by our gaming and brand clients, which grew 35% YoY. We see this as a welcoming trend heading into our merger with GameSquare.”

Tom Rogers, Executive Chairman of the Company, commented on the recently announced merger with GameSquare, adding, “Our strengths speak to the heart of the thesis behind the GameSquare transaction. GameSquare brings content development, a publisher advertising network, and a gaming influencer network, which is complementary to our gaming content analytics technology, our programmatic advertising technology, and our influencer marketing and management technology. When the two companies’ assets are combined, these elements create an end-to-end solution for brands to reach their target audience. Moreover, the combined companies offering provides a highly scaled answer to reach younger demographics at a level sought by brands, which traditional media can no longer perform. In addition, digital advertising continues to be constrained by new privacy protection steps of the major tech players, which has inhibited efficient targeting of certain audiences particularly gaming audiences. Traditional media’s failings and digital advertising limitations create the setting for why the combined company provides a solution to both problems that is both differentiated and scalable.”

Fiscal First Quarter 2023 Financial Results

Total revenue in the fiscal first quarter of 2023 was $10.3 million, compared to revenue of $11.5 million in the fiscal fourth quarter of 2022. Overall Software-as-a-Service (SaaS) revenues were relatively flat due to the declines in legacy content management related SaaS revenues. However, gaming and influencer data and analytics SaaS revenues grew 34.6% YoY. The decrease in advertising revenues was primarily due to changes in Google discovery and algorithms which impacted audience traffic that is expected to gradually improve throughout the fiscal second quarter and fiscal third quarter of 2023.

Expenses in the fiscal first quarter were $15.8 million, an improvement of approximately $6.0 million, when compared to $21.8 million on a sequential basis.

Net Loss in the fiscal first quarter improved 64.7% to $5.4 million, compared to a net loss of $15.2 million in the fiscal fourth quarter of 2022 inclusive of the restructuring charges related to discontinued operations.

Adjusted EBITDA was $(2.7) million for the fiscal first quarter, an improvement of 32.5% when compared to $(4.0) million in the fiscal fourth quarter of 2022, and when compared to the same year-ago quarter Adjusted EBITDA improved 17.5%.

At November 30, 2022, the Company had cash of $6.9 million.

Recent Operational Highlights:

Successful completion of Strategic Process resulting in signed merger with GameSquare.

Stream Hatchet new and expanded client highlights for the quarter include XSET, Benefit Cosmetics, a16z, Immortal, Tencent and Epic.

Sideqik new and expanded client highlights for the quarter include PDP Gaming, AverMedia, Misfits Gaming and ASUS.

Frankly new and expanded client highlights for the quarter include Citadel Communications, Krol Communications, Beyond TV, Sports News Highlights, Palmetto Network, and BmovieNation.

FY Q1 2023 Earnings Conference Call

Management will host an investor conference call at 8:45 a.m. EDT (5:45 a.m. PDT) today, Tuesday, January 17, 2023, to discuss Engine Gaming and Media, Inc.’s fiscal first quarter 2023 financial results, provide a corporate update, and conclude with a Q&A from participants. To participate, please use the following information:

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

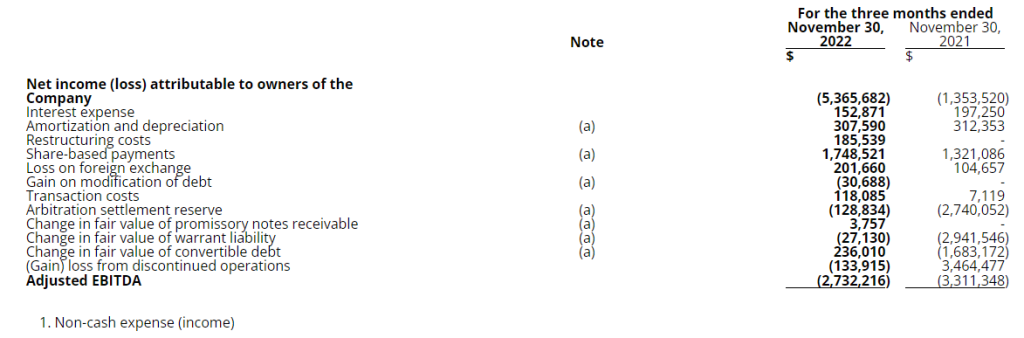

Non-IFRS Measures

The Company reports earnings before interest, taxes, depreciation and amortization (“EBITDA”) and Adjusted EBITDA, which are not financial measures calculated and presented in accordance with International Financial Reporting Standards (“IFRS”) and therefore may not be comparable to similar measures presented by other issuers. EBITDA and Adjusted EBITDA should not be considered in isolation or as a substitute to net income (loss) or any other financial measures of performance or liquidity calculated and presented in accordance with IFRS. The Company defines Adjusted EBITDA as EBITDA, adjusted to exclude certain non-cash charges and other items that we do not believe are reflective of our ongoing operating results. The Company utilizes Adjusted EBITDA internally for purposes of forecasting, determining compensation, and assessing the performance of our business, therefore, we believe this measure provides useful supplemental information that may assist investors in assessing an investment in the Company.

The following unaudited table presents the reconciliation of net loss to Adjusted EBITDA for the three months ended November 30, 2022, and 2021, respectively.

About Engine Gaming and Media, Inc.

Engine Gaming and Media, Inc. (NASDAQ:GAME)(TSXV:GAME) provides unparalleled live streaming data and social analytics, influencer relationship management and monetization, and programmatic advertising to support the world’s largest video gaming companies, brand marketers, ecommerce companies, media publishers and agencies to drive new streams of revenue. The company’s subsidiaries include Stream Hatchet, the global leader in gaming video distribution analytics; Sideqik, a social influencer marketing discovery, analytics, and activation platform; and Frankly Media, a digital publishing platform used to create, distribute, and monetize content across all digital channels. Engine generates revenue through a combination of software-as-a-service subscription fees, managed services, and programmatic advertising. For more information, please visit www.enginegaming.com.

Cautionary Statement on Forward-Looking Information

This news release contains forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Engine to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. In respect of the forward-looking information contained herein, Engine has provided such statements and information in reliance on certain assumptions that management believed to be reasonable at the time. Forward-looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements stated herein to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Actual results could differ materially from those currently anticipated due to a number of factors and risks. Accordingly, readers should not place undue reliance on forward-looking information contained in this news release.

The forward-looking statements contained in this news release are made as of the date of this release and, accordingly, are subject to change after such date. Engine does not assume any obligation to update or revise any forward-looking statements, whether written or oral, that may be made from time to time by us or on our behalf, except as required by applicable law.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview:Will It Be A Happy New Year? The full impact of the recent increase in interest rates likely have not been fully reflected in the economy. But, many media stocks seem to anticipate that the industry is in a downturn now. Notably, some stocks have recently performed better and the current fundamentals are not falling off of a cliff.

Digital Media: Coming Off Of Its Sugar High?While Google now plans to phase out cookies in the second half of 2024, it is likely that the plan will affect 2023 as marketers and publishers prepare for the deprecation of cookies.

Television Broadcasting: A Watershed Year For Streaming. Streaming has now eclipsed both broadcast TV and cable TV in terms of viewing based on Nielsen data. Recently, Netflix launched a new pricing plan on November 3 which offers a basic tier, with advertising, at a low price point of $6.99. What does this mean for the TV industry?

Radio Broadcasting:Digital Is Bolstering Performance. It has been a bloodbath for Radio stocks, but the fundamentals appear better than the stock performance might suggest. Radio broadcasters with significant digital businesses are anticipated to report favorable pacings in Q1.

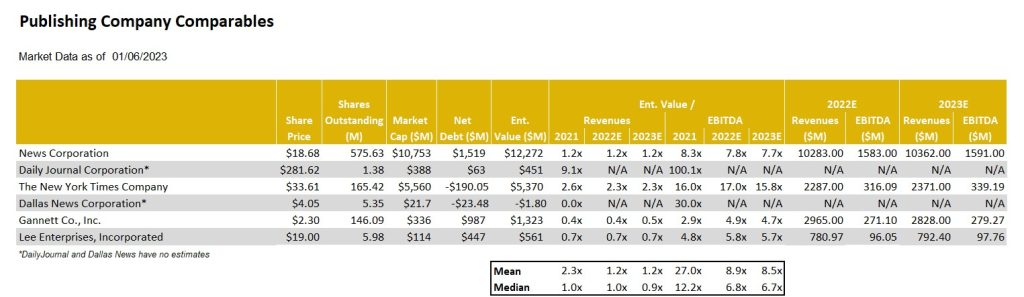

Publishing: You Are Golden If You Have Digital. The trouble with the largest newspaper company, Gannett, has created a pall over the group as it struggles to cut expenses. But, companies with substantial digital operations have performed well. We highlight one of our current favorites Lee Enterprises (LEE).

Overview

Will It Be A Happy New Year?

2022 was one of the worse for media stock performance in recent memory, with stocks across traditional and digital media sectors down over 40% or more. Media stocks underperformed the general market, as measured by the S&P 500 Index, which was down a more moderate 19.4% on a comparable basis for the full year 2022. It is typical for media stocks to underperform in a late-stage economic cycle or in the midst of an economic downturn. But, the significant stock declines are stunning. Macro-economic issues including inflation, rising interest rates, and the prospect of a looming economic downturn, all contributed to the poor performance.

The question is “will 2023 be better?” We believe so. There has been recent signs of life. The S&P 500 increased by 7% during the fourth quarter of 2022, marking the first time the Index had increased since fourth quarter of 2021. Notably, the Noble Publishing and Noble MarTech Indices outperformed the general market in the latest quarter. But, the full impact of the recent interest rate increase likely have not been reflected in the economy. Many media stocks seem to anticipate an economic downturn, but current fundamentals do not appear to be in a freefall and may be better than expected. If the economy further deteriorates from the recent or future rate hikes, it appears now that it may adversely affect the second half of 2023. Advertising pacings appear to be holding up well so far in the first half 2023. Notably, media stocks may begin to anticipate an improving economic outlook and overlook the weak fundamental environment in the second half.

Conventional thought anticipates that increasing concerns over an economic recession may prompt mortgage rates to trend lower in 2023. Furthermore, it is possible that the Fed may lower interest rates if inflation moderates, although the Fed is not currently anticipating rate decreases in 2023. Nonetheless, this paints a favorable picture for media stocks in 2023. Traditionally, the best time to buy media stocks is in the midst of an economic downturn. In addition, these consumer cyclical stocks tend to be among the first movers in an early-stage economic cycle and tend to perform well in a moderating interest rate environment. As mentioned earlier, the stocks may currently be oversold given the prospect that the current fundamental

environment is better anticipated.

What is the risk to this favorable outlook? We believe that the resurging Chinese economy may be disruptive. Within the last month, the China’s economy has been reopened from Covid lockdowns, which may put pressure on global energy prices. Such a prospect may make our fight on inflation more stubborn to combat, potentially throwing off our favorable outlook for moderating interest rates. In our view, we are closer to the light at the end of the tunnel than we were last year. Given the prospect that these stocks tend to outperform the market in an early stage economic recovery, we believe it is time for investors to accumulate positions in the media sectors. In this quarterly, we highlight some of our favorite plays in the Digital, Media & Technology space.

Digital Media & Technology

A Year To Forget

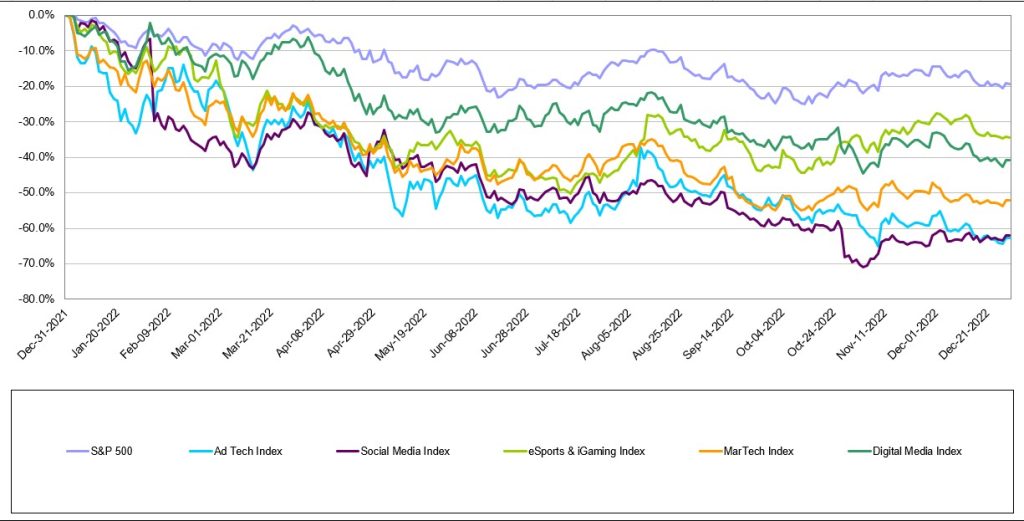

While there were signs of life in the fourth quarter of 2022 for the Internet and Digital Media sectors, 2022 was a year most investors in these sectors would like to forget. As Figure #1 LTM Internet & Digital Technology Performance illustrates, every one of these sectors substantially underperformed the S&P 500 last year. The S&P 500 Index finished the year down 19% which was substantially better than Noble’s Digital Media Index (-41%), MarTech Index (-52%), Social Media Index (-63%), and Ad Tech Index (-63%). Rather than focus on the stocks that significantly underperformed their respective Indices (and there are many), we would rather focus on the three stocks that finished 2022 up for the year.

The shares of one of our favorites, Harte Hanks (HHS)increased by 53% in 2022. The company continued its multi-year turnaround from a highly levered and unprofitable business (in 2019), to a double digit EBITDA margin business with a debt-free balance sheet. Furthermore, we believe that many of the company’s business lines have recession resilient qualities. The other stocks that performed well are Tencent (TME), whichincreased by 21%in 2022. Shares declined earlier in the year as China’s economy slowed as it maintained its Zero Covid-19 lockdowns, but surged in the fourth quarter as it appeared that the company would enjoy an increase in demand as China begins easing Covid restrictions. Finally, the shares of Perion Networks (PERI) increased by 5% in 2022 as Perion consistently beat expectation and raised its guidance throughout 2022. In the first week of 2023, the company once again pre-announced better than expected results for the fourth quarter, and shares are already up 14% since the start of the new year.

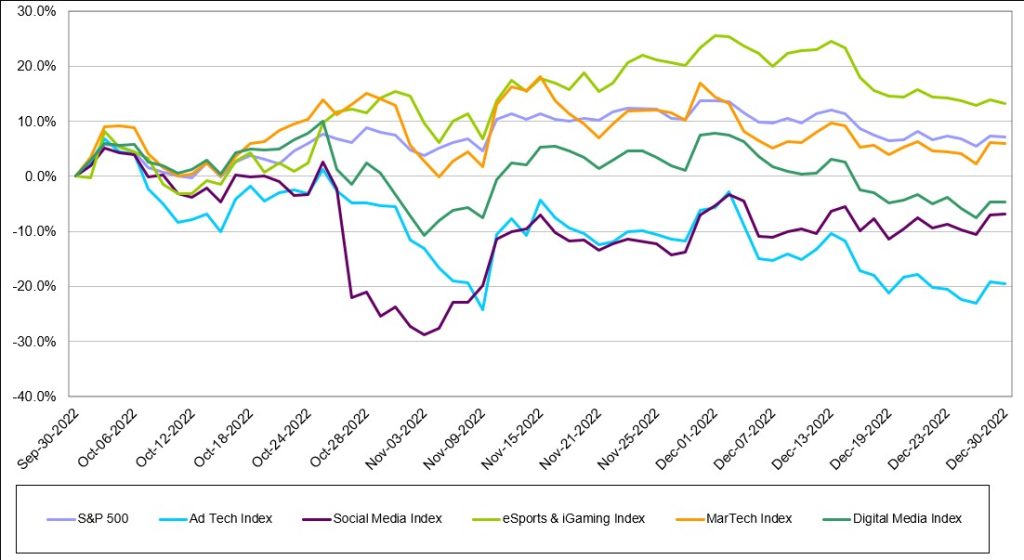

As Figure #2 Q4 Internet & Digital Technology Performancehighlights, there has been signs of life in Noble’s MarTech Index which increased 6%, roughly in-line with the market. In Noble’s MarTech Index, 11 of the 22 stocks in the index posted gains, led by Yext (YEXT; +46%), Shopify (SHOP; +29%), LiveRamp (RAMP; +29%) and Adobe (ADBE; +22%). This marks significant improvement from last quarter when only 4 of the sectors’ stocks finished the quarter in positive territory. MarTech stocks have suffered from a market reset to revenue multiples that began when the Fed began raising rates. MarTech share price declines in the first, second and third quarters of 2022 were mostly driven by multiple compression as investors rotated out of high-flying tech sectors where companies had chased growth at all costs (at the expense of profitability). Only 7 of the MarTech companies in the Index posted positive EBITDA in the latest quarter. Laggards during the fourth quarter were Noble’s Digital Media Index (-5%), Social Media Index (-7%) and Ad Tech Index (-20%).

Coming Off Of A Sugar High?

One of the largest issues affecting the Digital Media industry in 2023 will be the phase out of the use of third-party cookies. Cookies were used to track a user visits on internet sites and that data was used to model behavior. The industry has moved away from the use of cookies as governments and consumers have raised concerns over privacy issues and as consumers wanted more control over how their data is used. Governments have taken a more active role in protecting consumer privacy. California, Colorado, Connecticut, Utah, and Virginia have passed privacy laws. It is likely that there will be a federal privacy law at some point.

How will this affect the industry? We believe that there has been plenty of time to “work around” this issue. The implementation of the phase out of cookies has been delayed several times, originally announced by Google in 2020. Google now plans to phased out cookies in the second half of 2024, if it is not delayed again. As marketers and publishers prepare for the deprecation of cookies, digital advertising likely will be begin to affect 2023.

Digital Advertising Outlook for 2023

Last October eMarketer revised lower its 2023 U.S. digital advertising forecast by $5.5 billion, from $284.1 billion to $278.6 billion. While this sounds like a substantial drop in percentage terms, the 2023 guidance was lowered from 14% growth to 12% growth. Most of the global ad agencies expect digital to continue to grow by double digits driven with dollars migrating to such digital ad channels as retail media and connected TV. Both sectors continue to demonstrate impressive growth.

Retail Media – A retail media network is a retailer-owned advertising service that allows marketers to purchase advertising space across all digital assets owned by a retail business, using the retailer’s first-party data to connect with shoppers throughout the buying journey. eMarketer forecasts that retail media ad spending grew by 31% last year to $41 billion and will grow to $61 billion over the next two years, by which time it will equate to 20% of digital advertising. The leaders in retail media are Amazon, Walmart and Instacart.

Through a retail media network, partners (advertisers) get direct access to a retailer’s customers. The benefit to the partners/advertisers is that they get access to first party data. Retailers own and store this data and allow advertisers to access them through their retail media programs. The first party data is valuable because it is collected at the point of sale allowing brands to get better insights into purchase behavior. Traditional retailers are beginning to follow suit. Traditional retailers with the largest digital audiences (per comScore) are Walmart, Target, Home Depot, Lowes, CVS, Walgreens, Costco and Kohls.

On January 10th, Microsoft announced that it intended to create the industry’s most complete omnichannel retail media technology stack supported by its Promote IQ platform, a company Microsoft acquired in 2019. We expect companies that serve the retail media sector from an Ad Tech or Mar Tech standpoint are poised to benefit from secular trends in this sector.

Connected TV (CTV) – Last July, Nielsen announced that for the first time U.S. streaming TV viewership was larger than cable TV viewing. In July 2022, eMarketer forecast that CTV advertising would reach $18.9 billion in 2022. However, in October 2022, eMarketer raised its forecast for CTV advertising by $2.3 billion to $21.2 billion in 2022. In October, the forecaster also raised its 2023 CTV advertising forecast by $3 billion to $26.9 billion, up from $23.9 billion in the July 2022 forecast. The big increase is due primarily to Netflix and Disney+ announcing they were launching ad supported tiers to their streaming offerings. Ad Tech or Mar Tech companies that serve this market are also poised to benefit from secular viewing trends and the advertising dollars that are migrating to these platforms, discussed later in this report.

The ability to target specific audiences and measure specific outcomes tied to the ads that viewers watched, has made CTV a force to be reckoned with, particularly for those advertisers that are never quite sure which advertising mediums provide the highest returns. Historically, TV was a mass medium used by large brands that wanted massive reach. CTV has opened the door to a wider variety of advertisers that are looking to reach more targeted, even niche, audiences. According to MNTN, a connected TV performance marketing platform, many CTV advertisers are first-time TV advertisers. With new FAST (Free Ad-Supported Streaming TV) channels coming online every month, there is no shortage of supply coming to market. This is just one reason why eMarketer predicts CTV advertising to grow by $10+ billion over the next two years and reach nearly $32 billion in advertising revenue in 2024.

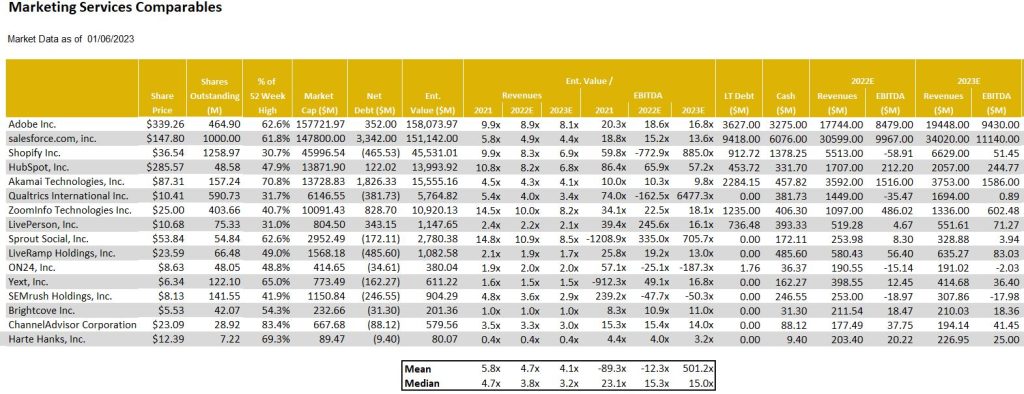

As we look toward 2023, our current favorites include Harte Hanks (HHS) and Direct Digital (DRCT). In terms of Harte Hanks, we believe that the company has recession resilient qualities and that the company’s balance sheet is in a sound position. Furthermore, given the recent rising interest rate environment, the company’s unfunded pension liabilities have dramatically improved. The company may have the opportunity to further mitigate its pension liabilities in 2023. Figure #3 Marketing Tech Comparables highlights, the shares of HHS are trading well below its peers. We believe that there is meaningful upside potential in the shares as it closes the valuation gap with its peers.

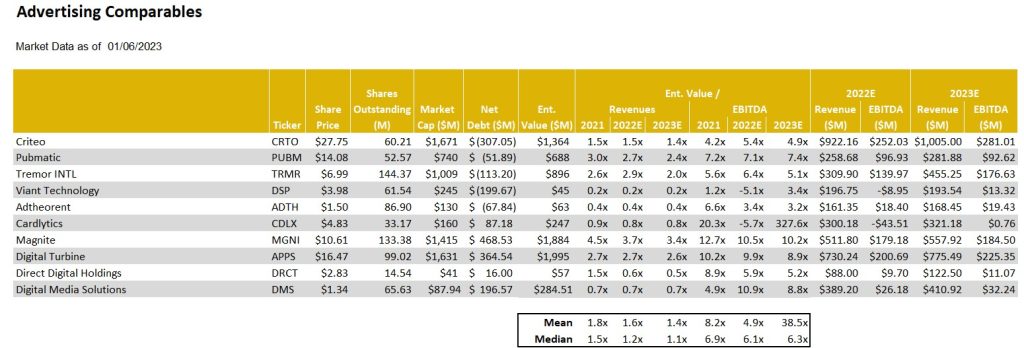

While the deprecation of cookies has created a pall over the sector, we believe that Direct Digital has worked with its Publishers to mitigate this issue. In addition, the company is a relatively small player in a very large marketplace. As such, we believe that the company has the ability to attractively grow in 2023. In our view, the shares appear to be oversold given the continuation of favorable advertising trends. Figure #4 Advertising Tech Comparables illustrates that the DRCT shares trade below the average valuation in its Advertising Marketing peer set. In our view, the valuation should be higher than the averages given that the company has leading industry revenue growth. Closing this valuation gap offers compelling stock appreciation potential.

Figure #1 LTM Internet & Digital Technology Performance

Source: Capital IQ

Figure #2 Q4 Internet & Digital Technology Performance

Source: Capital IQ

Marketing Technology

Figure #3 Marketing Tech Comparables

Source: Eikon, Company filings and Noble estimates

Figure #4 Advertising Tech Comparables

Source: Eikon, Company filings and Noble estimates

Traditional Media

Another Quarter Of Moderating Stock Performance

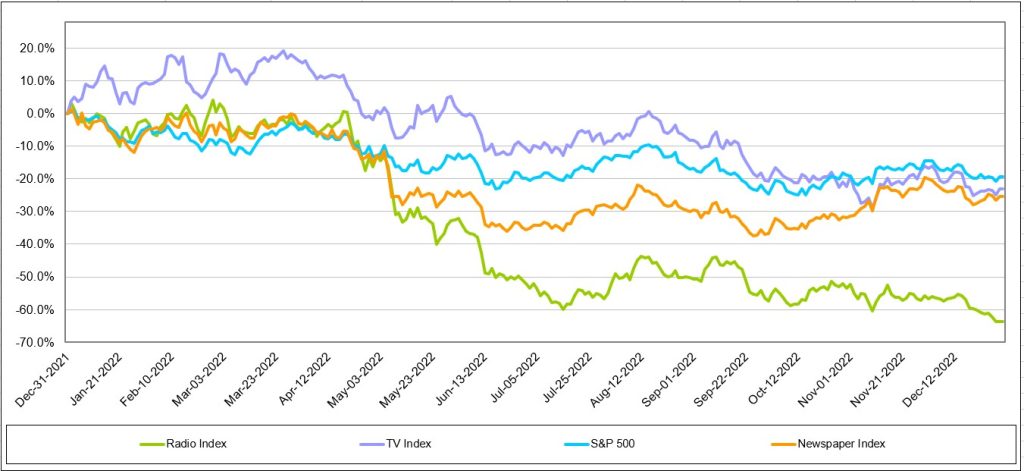

Traditional media stocks underperformed the general market in 2022, with the Radio sector the hardest hit. As Figure #5 LTM Traditional Media Performance Chart illustrates, the Noble Radio Index declined 63.8% versus 19.4% for the general market, as measured by the S&P 500, in a comparable time period. Television and Publishing stocks were down 23.2% and 25.4%, respectively, more in line with the general market returns. But, there were notable company stock performance disparities within each sector, highlighted later in this report. Larger market capitalized companies performed better, which skewed the market cap weighted Indices.

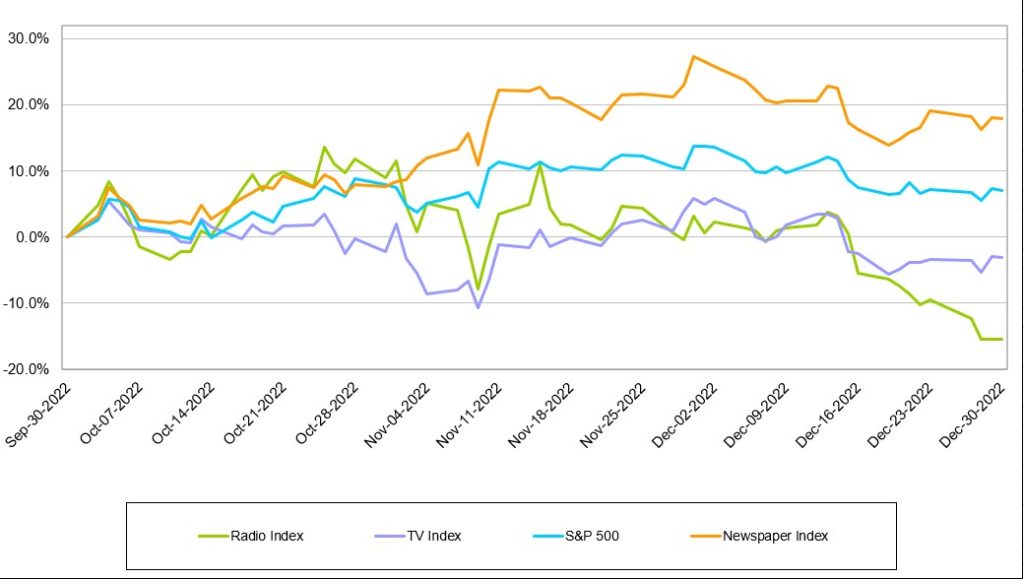

The traditional media stocks seemed to have stabilized from the rapid declines earlier in the year. Possible signs of life in the traditional media sector as well? As Figure #6 Q4 Traditional Media Performance highlights, the Publishing sector once again outperformed the general market in the quarter. The Noble Television Index declined 3.2%, but this decline moderated from the 10.1% decline in the third quarter. The Radio industry still has not yet stabilized, with the Noble Radio Index down 15.4% in the latest quarter.

Figure #5 LTM Traditional Media Performance

Source: Capital IQ

Figure #6 Q4 Traditional Media Performance

Source: Capital IQ

Television Broadcast

Will Netflix suck the air out of the room?

Netflix launched a new pricing plan on November 3 which offers a basic tier, with advertising, at a low price point of $6.99. This compares with its previous tiers of $9.99 and $19.99 for advertising free streaming. While reports indicate that the advertising platform is off to a slow start, we believe that the Netflix move could be disruptive to the Broadcast Television Network business as its lower price basic service gains traction. It is likely that there will be some cannibalization from its higher pricing tier, but we believe that the move will broaden its subscriber base. While Netflix has not considered offering live sports on its streaming platform given the cost of sports rights, we believe that the potential success of its subscription/advertising tier may provide a platform to upend that decision. There is a strong tailwind for viewership trends on streaming platforms, which now exceed that of broadcast television viewing. A decision to enter sports will be a big deal and disruptive to Network broadcasting.

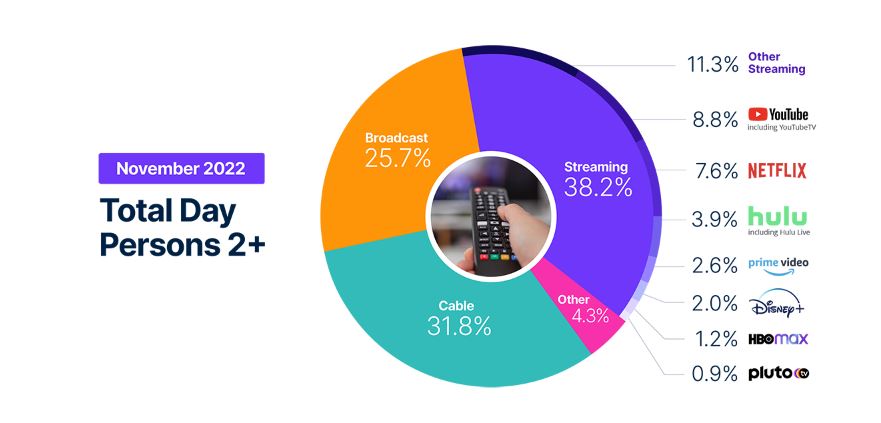

Streaming viewership not only eclipsed television viewing in July 2022, but also that of cable viewing, 34.8% versus 34.4%. In addition, based on the latest Nielsen data from November 2022, streaming now accounts for 38.2% of total viewing with Broadcast at 25.7% and cable at 31.8%. Figure #7 Viewership illustrates the November viewership data. While TV viewership increased 7.8% in November, largely due to sports content, streaming usage year over year was up more than 41%.

Figure #7 Viewership

Source: Nielsen Media Insights

Scripps Plans To Expand Sports

The declining cable subscriptions and cable viewership, especially on regional sports networks, led E.W. Scripps to launch a new Scripps Sports division. This division plans to seek broadcast rights from teams and leagues and bring that programming to broadcast television. The company plans to obtain rights either in local TV markets where it can partner with the the teams or on a national basis, utilizing its distribution on its Ion Network. It is important to note that ION is unique from other networks. Ion’s distribution is nearly 100% of the US television market given that it has local licenses and local towers in every market, it is fully distributed on cable and satellite, and is offered over the air. As such, we believe that Scripps offers a unique proposition to sports teams interested in building its audiences.

Will ATSC 3.0 Stream The Tide?

Furthermore, the broadcast industry appears to be more aggressively ramping its own streaming capabilities with the rollout of its new broadcast standard, ATSC 3.0. ATSC 3.0 is built on the same Internet Protocol as other streaming platforms, and, as such, broadcast programming and internet content can be accessible in the car, on mobile devices, as well as in the home. Importantly, the new standard can handle signal shifting, like if you were moving in a car, and the signal is more robust so you may be able to pick up more stations in a local market. While there are many opportunities for the new standard, services and offerings are still being developed. But, it offers promising opportunities for broadcasters to compete with streaming services in the future. We expect that the industry will make more announcements about this promising technology at future events, including the upcoming NAB Show, April 16-19 in Las Vegas, NV.

Are We In A Recession?

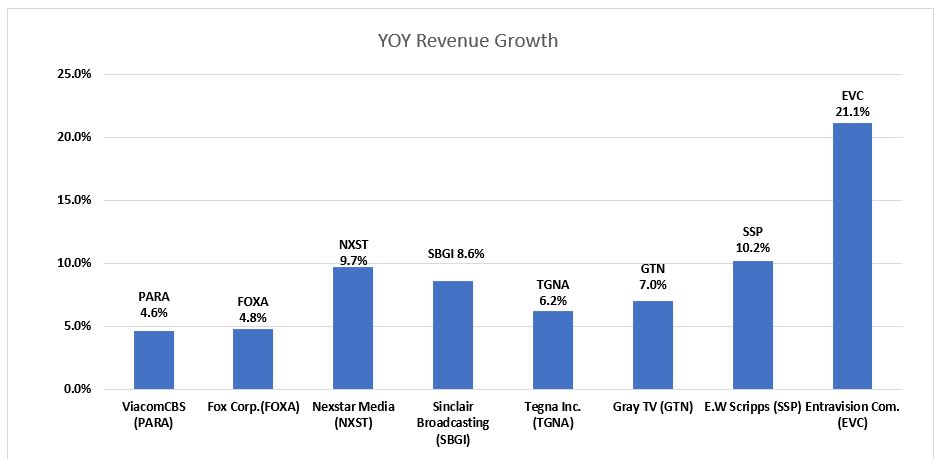

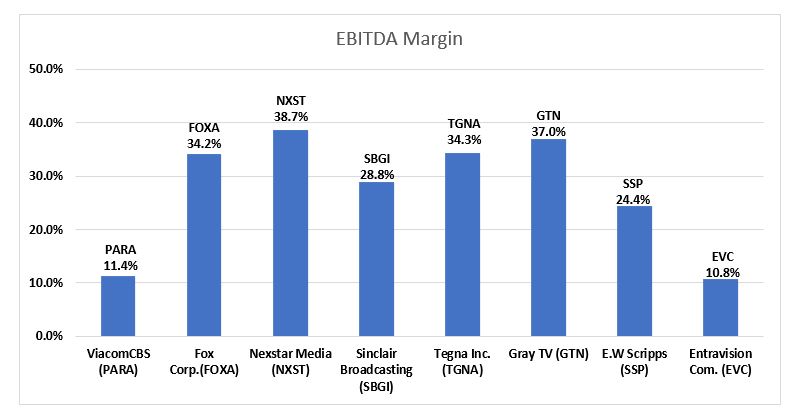

In our view, the current fundamentals may be better than the stocks project. Advertising seems to be holding up, post political advertising. As Figure #8 TV Q3 YoY Revenue Growth highlights, most companies in the industry reported strong Q3 revenue growth, influenced by a large influx of Political advertising. Figure #9 TV Q3 EBITDA Margins illustrates that the largest broadcasters, particularly Nexstar, has the largest EBITDA margins. Notably, the two stocks with the highest revenue growth in the quarter, Entravision and E.W. Scripps, performed the best in the fourth quarter, discussed later.

Notably, Local advertising appears to be fairing better than National advertising. Based on our estimates, core local advertising is expected to be down in the range of 5% to 8%, with core National down as much as the double digits. We believe that some large advertising categories like Auto, Retail and Home Improvement will show improving trends. The first quarter 2023 appears to be consistent with the fourth quarter. Smaller market TV likely will perform at the lower end of the range, while larger market TV will be at the higher end (greater core revenue decline). Broadcast Network is another story, which we believe is weak. Network has potential heightened competition. Figure #8 TV Q3 YoY Revenue Growth

Source: Eikon and Company filings

Figure #9 TV Q3 EBITDA Margins

Source: Eikon and Company filings

As mentioned earlier, the Noble Television Broadcast Index declined 3.2% in the latest quarter, underperforming the general market’s 7.2% advance. Importantly, the 3.2% decline in valuations was a moderation from the 10.1% decline in the third quarter. There were variances in the performance and some notable performers including two of our favorites: E.W. Scripps, which increased 5.8% and Entravision, which increase 5.3%. Both of these companies were among the strongest revenue performers in the third quarter. Among the poor performers was Gray Television, down a significant 33.7% and Sinclair Broadcasting, down 24.0%. With the TV stocks down a significant 23.2% for the year, have the stocks already assumed that the industry is in an economic downturn? We believe that the stock may be oversold based on the prospect that advertising is currently holding up in the first quarter.

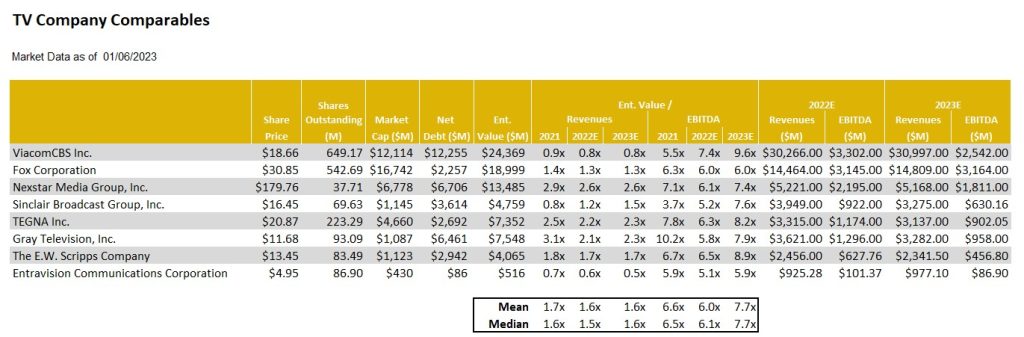

Is There Room For Upside?

As Figure # 10 TV Industry Comparables highlight, most TV stocks are trading in a tight range of each other. The biggest variance in stock valuations is our current favorite Entravision, trading at 5.9 times EV to our 2023 EBITDA estimate, well below that of its industry peers which trade on average at 7.7 times. We believe that Entravision, which has migrated to become a leading Digital Media company which contributes roughly 80% of its total company revenues, should trade at a premium to its broadcast peers, rather than at a discount. Investors appear to be somewhat confused by the company’s relatively low EBITDA margins, which is a function of how revenues are accounted for in its Digital Media Division. We would also note that its financial profile is among the best in the industry, with a large cash position and modest net debt position of $86 million. As such, EVC leads our favorites in this sector.

Figure #10 TV Industry Comparables

Source: Eikon, Company filings and Nobles estimates

Radio Broadcast

Digital Is Bolstering Performance

The radio industry index was the worst performing index in the traditional media segment, declining 15.4% in the quarter and 63.8% for the year. The radio industry is feeling the pressure that recessionary concerns place on the demand for advertising. In addition to increased competition for audiences from digital music providers and shifting advertising dollars from radio to a more targeted advertising medium, digital media.

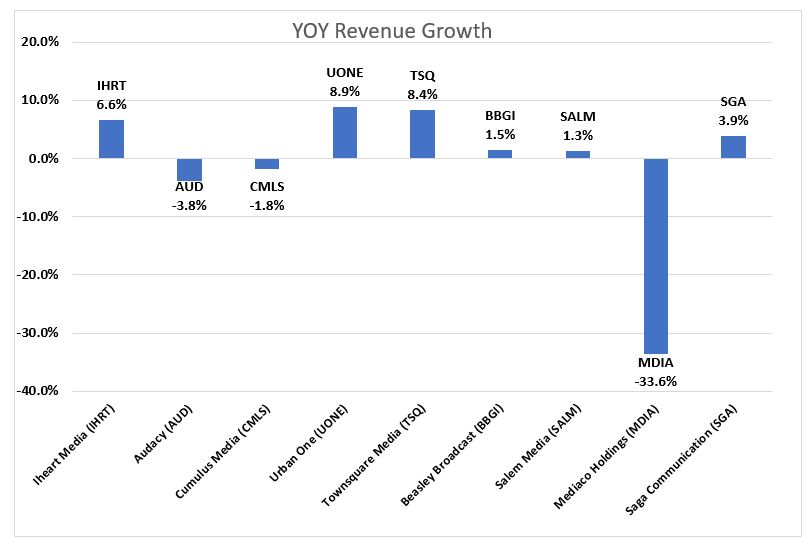

Figure #11 Radio Industry Q3 YoY Revenue Growth chart illustrates the year over year change in revenue for the third quarter. Urban One and Townsquare Media top their peers with revenue growth of 8.9% and 8.4%, respectively. A common theme with companies at the top of the list are diversified revenue streams. Salem Media and Beasley Broadcast Group are in the middle of the pack and are both taking steps to further diversify revenue. Salem has diversified into content creation and digital media and Beasley is continuing to pursue digital agency model. The median Q3 revenue growth rate was 1.5%, and the average revenue growth was -1%. The Average growth rate of -1% is skewed due to the poor performance of Medico holdings. In previous quarters Medico benefited from Covid-19 vaccine advertising campaigns and ticket sales for an annual outdoor live event that took place in Q3 of 2021. Without Covid vaccine advertising and Medico’s concert being held in Q2 2022 instead of Q3 resulted in revenue declining 33.6% on a year over year basis.

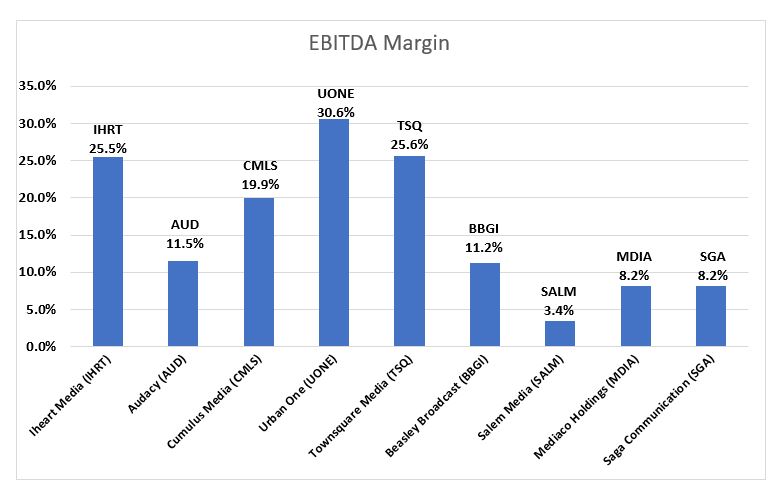

Industry adj. EBITDA margins were healthy, as Figure #12 Radio Industry Q3 EBITDA margins illustrates, Urban one, Townsquare Media and Iheart Media top the list with adj. EBITDA margins of 30.6%, 25.6% and 25.5%, respectively.

After the 2022 calendar year ended, Moody’s downgraded Cumulus Media’s Corporate Family Rating to B3 from B2. Moody’s believes Cumulus Media will face a further decline in advertising demand as the economy weakens. Moody’s could upgrade its rating if leverage decreases to 5x as a result of positive performance and could downgrade its rating if leverage ratio increases to 7x as a result of poor performance. It should be noted that Cumulus has a large cash position of $118 million and could access an additional $100 million through an asset backed loan.