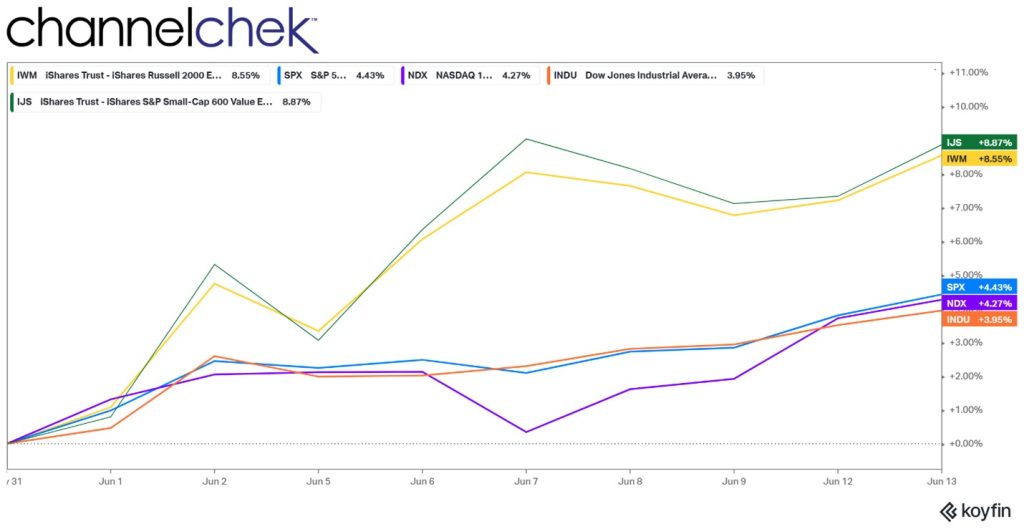

Why Interest Rates Impact Large and Small Company Profits Differently

Small-cap stocks are less sensitive to interest rate changes than large-cap stocks. Generally, when interest rates rise, it can create a bigger drag on larger companies for a number of reasons. Meanwhile, companies with small market caps are unaffected or less affected on average. While there are many factors that impact stock prices, interest rates are certainly on the list – depending on company size, rates will impact them differently.

Interest rates have moved quite a bit over the past 18 months, and they aren’t expected to stabilize now. Here are some of the stock market dynamics at play.

Revenues and Costs

Small-cap companies typically have less debt than large-cap companies. This means that they are less sensitive to changes in interest rates, as the cost of borrowing does not affect them as much as big borrowers when rates rise.

The main reason for lower debt levels is they typically have less ability to borrow through the capital markets. Smaller or less established companies in general find the cost of issuing a public market note as being behigher than the benefits. And since rising interest rates, increase the cost of borrowing, small-cap companies are not rolling large amounts of debt at the new interest rate levels. Whereas debt is often a much larger part of big company’s overall strategy and cost of capital.

It also helps that small market-cap companies are often in industries that are less sensitive to the overall economy. If rates are rising, fears of a recession often creep into investor’s mindsets. For example, smaller technology and life sciences companies are, by comparison, less sensitive to economic cycles than cyclical industries such as large manufacturing and big oil. Put another way, many smaller companies are more focused on discovery, innovation and growth, these are not as dependent on economic conditions.

However, small-cap investors should be aware that small-caps are often more volatile than large-caps. So the investor can experience larger swings in price, both up and down. This can make this investment sector more attractive to investors who are looking for growth potential, but it can also make them more risky. If they have lower trade volume, there are fewer buyers and sellers, making it more likely for prices to move up or down.

Larger companies tend to be international in their business dealings, compared to domestic small-cap companies which more commonly transact within their home-base country. For the US, an increase in interest rates relative to other nations, is likely to lead to a stronger $US dollar. A stronger US dollar makes the cost of goods sold overseas more expensive to buyers. This could lower sales expectations as overseas buyers find other suppliers. Small companies operating domestically do not have to worry about foreign exchange rates and how they are impacted by interest rate movements.

It is important to note that interest rate changes can impact all stocks, regardless of their size. The impact of interest rate changes on a particular stock will depend on a number of factors, including the company’s debt load, its industry, and its overall financial health. Overall, small-cap stocks are less sensitive to interest rate changes than large-cap stocks, but investors can expect more volatility.

Market-cap Sector Rotation

Sector rotation is the process of money moving from one stock market sector to another, based on expectations of which sectors will perform better in the future. This could be industry, types of securities (ie: bonds, real estate), or market cap.

As it relates to market cap, an investor might sell large-cap stocks and buy small-cap stocks if they believe that small-cap stocks are undervalued and are poised to outperform large-cap stocks in the future.

It can help you to stay ahead of the market. By monitoring sector performance and making changes to your portfolio accordingly, you can stay ahead of the market and make sure that your money is invested in the sectors that are most likely to perform well.

Take Away

There are many different groupings of stocks (market-cap, industry, international, region, etc.) and factors that can impact the group. One factor that has historically played a part in price discovery of small versus large-cap stocks is interest rate movements. Interest rates impact the cost of doing business and also sales. Investors add this into the myriad of other factors they try to be aware of when selecting stocks.

Managing Editor, Channelchek