Rising Unemployment: Economists Sometimes Say it’s Good for the Economy, But Are They Right?

interest rates are up, which means that projections for growth are down. Put simply, the proverbial something is close to hitting the fan.

Business closures and job losses are likely to become another hurdle for the global economy – and that points to rising unemployment. Yet, while most people would think of rising unemployment as a bad thing, some economists don’t entirely agree.

Economists have long pointed to a counterintuitive positive relationship between unemployment and entrepreneurship, born of the fact that people who lose their job often start businesses. This is often referred to within economic literature as necessity-based or push-factor entrepreneurship.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts ofDaragh O’Leary, PhD Researcher in Economics, University College Cork

Where it Gets Tricky

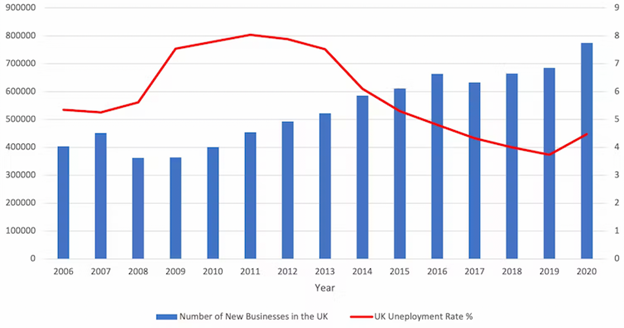

There is certainly good evidence for the existence of this contradictory relationship. The graph below shows the rates of UK business creation in blue and unemployment in red. As you can see, unemployment started to increase during the global financial crisis of 2007-09 and business creation followed not long after.

UK new business creation and unemployment, 2006-2020

This relationship between business creation and unemployment has previously been used by some as a justification for cold social policies towards the unemployed on the rationale that “the market fixes itself” in the long run. They see business closures and job losses not as human miseries that require government help, but necessary evils that are needed to reallocate the money, people and other resources back into the economy in more efficient ways .

But my latest research has found that rising unemployment is not quite the silver bullet for reigniting the economic engine that it’s cracked up to be. I looked at 148 regions across Europe from 2008 to 2017. Although I did find evidence that unemployment can stimulate business creation over time, this only seems to happen in higher performing regions within higher performing economies such as the Netherlands, Finland and Austria.

In lower performing regions within lower performing economies such as Bulgaria, Romania and Hungary, the relationship between unemployment and business creation actually appears to be negative. In other words, rather than inducing business creation, unemployment simply seems to lead to more unemployment.

The reason why higher performing regions in wealthier areas have a positive relationship between job losses and business creation is that they enjoy what are known as “urbanisation economies”. These are positive benefits derived from the scale and density of economic activity occurring within that area, including wider arrays of services, greater pools of customers and greater numbers of transactions relative to other areas of the economy.

For example, a firm located in a capital city like London will benefit from more abundant access to consumers, suppliers and lenders as well as larger labour pools. The higher population density in these areas also makes it more likely that firms and workers will learn faster as they observe the activities of their many neighbours. In more peripheral areas with fewer of these characteristics, the opposite is true. This is why unemployment affects different places differently.

What it Means

One consequence is that economists need to stop explaining how economies perform differently based solely on national factors. And it’s not just unemployment where this becomes apparent. For example, Ireland’s longstanding low rate of corporation tax (12.5%) has been cited as a reason for its high foreign direct investment, which accounts for roughly 20% of private sector employment.

Yet while just over 43% of all Irish enterprises in 2020 were located in either Dublin or Cork, counties like Leitrim in the north accounted for fewer than 1% of enterprises. So while national measures can help induce entrepreneurship and increase the overall size of the pie, the pie is shared very unequally. Just as rising unemployment can benefit some areas while hindering others, the same is true of government interventions.

Rural areas like County Leitrim have benefited far less from Ireland’s low corporation tax than more urbanised regions further south. Julia Gavin/Alamy

We therefore need to stop viewing the free market and government intervention as either wrong or right. In some contexts one is going to be more helpful, while in other contexts it will be the opposite. Recognizing this reality would improve on much of the polarized debate in politics and economics, in which those on the right can come across as cold and ignorant, while those on the left can seem self-righteous and sanctimonious, viewing capitalism and markets as dirty words.

How does this apply to today’s gathering downturn? It would make sense for governments to prioritize supporting businesses in more peripheral regions, while leaving those in wealthier urban areas to fend for themselves.

The famous economist John Kenneth Galbraith gave what I believe to be one of the best pieces of commentary on this topic, saying:

Where the market works, I’m for that. Where government is necessary, I’m for that … I’m in favor of whatever works in the particular case.

If we are to survive this upcoming recession and get things going again, we are going to need to acknowledge that centralized “one-size-fits-all” policies won’t be useful everywhere. The solutions to economic recovery are in some cases government intervention and in others the free market, but not always one or the other.

The Old Congress May Rush to Push Through a Debt Ceiling Agreement

Will there be a government shutdown as Congress grapples with debt ceiling issues?

Only Congress can spend money, so it is the job of Congress to set the upper limit if the nation may decide to go into debt. It is tricky most years, as the process often threatens the government shutdown of non-essential workers. Emergency spending measures often are used before an agreement is passed, before doing any further damage. The most damaging would be to the global faith in the U.S. Government to make do on its debts. Most U.S. Treasury securities are refinanced by reissuing new debt issues. If new debt issues can not be increased to cover today’s higher interest rates, or other increased levels of budgeted spending, the nation faces severe economic trouble.

Treasury Secretary Janet Yellen warned this weekend that lawmakers’ failure to raise the statutory limit on U.S. debt posed a “huge threat” to America’s credit rating and the functioning of U.S. financial markets.

Yellen said that cooperation is still possible between the two major political parties on other financial priorities, but lifting the debt ceiling is a non-negotiable item on the list.

Both parties always jockey for position to get funding for their projects as the country and government workers reel from the negotiation process each year. Currently, U.S. public debt stands at $31.2 trillion. Without an increase, it’s expected that there will be a default crisis by the third quarter of 2023.

Republicans tend to pay more lip service to making spending cuts. In 2010, a Republican lead Congress tried to hold the line on raising the budget risking a possible default on U.S. Government backed securities. The uncertainty over whether the U.S. could fund maturing U.S. Treasuries prompted a first-ever ratings cut on Treasury debt by Standard and Poor’s.

Yellen was asked whether Democrats, who will be in a weakened state after the new Congressional leaders take office in January, should pass legislation in the post-election session, while they still hold a majority. “I think it’s irresponsible not to raise the debt ceiling. It’s always been raised,” Yellen said. “It would be a huge threat to the country not to do it, and completely irresponsible to threaten the credit rating of America and the functioning of the single most important financial market.”

One of the higher priorities that Republicans would want to chop from the budget is the $87 billion in new funds the President wants for the IRS.

Yellen reminded that some Republicans backed last year’s infrastructure act and this year’s investments in semiconductors and research, she suggested the administration would look for measures that could draw further bipartisan support.

Take Away

Each year the U.S. Congress grapples with spending and financing the spending. The financed part, involves Congress providing enough money for the budgeted items. As interest rates rise, they become one more expense to be budgeted for and generally financed.

Janet Yellen, speaking at a G20 meeting in Indonesia warned of the need to lift the debt ceiling, as not doing so would have devastating economic impacts.

There is Potential for a Change in Sentiment Spurred by this Week’s Wholesale Inflation Report

One economic number doesn’t make a trend. The members of the Federal Open Market Committee know this, and certainly, the Chair, Jay Powell, understands. As it relates to last week’s CPI report, he may wish that one lower-than-expected inflation data point could prevent him from needing to do more, but it simply isn’t enough info from which the Fed can glean any actionable information.

As we head into the first trading session of a new week, it’s uncertain what the reaction of interest rates will be. They dropped substantially in response to last Thursday’s inflation data coming in better than expected. However, there was no chance of follow-through or reversal as Friday’s Veteran’s Day holiday left the bond markets closed.

With this, inflation numbers continue to be the most significant for both stock and bond investors. On this coming Tuesday, November 15, wholesale prices will be reported as the Producer Price Index (PPI). This release could have more weight in trade action than usual.

Thursday is another big day on the calendar as the markets will be grappling with a larger-than-normal volume of economic releases.

Monday 11/14

11:00 AM ET, The NY Federal Reserve Bank’s one and five-year inflation forecast. This is not an event that is usually paid much attention to by market participants. However, considering there are many parties interested in what members of the Federal Reserve System are now thinking, a dramatic shift from the previous forecast could inspire the financial markets to adjust accordingly.

Previously the one-year inflation expectation was 5.7%. The five-year inflation forecast was 2.2%.

Tuesday 10/15

8:30 AM ET, The Producer Price Index (PPI) from the Bureau of Labor Statistics (BLS) is an inflation gauge that measures the average change over time in the prices received by U.S. producers of goods and services. The prices are typically considered input costs for final products and can impact CPI, it may also impact company costs of production and, therefore, profits. The trend has been lower, YOY PPI has been running at 8.5%, and last month, it rose 0.4%, the expectation is for another 0.4% increase.

Michael Burry, and Warren Buffet’s holdings. The SEC requires investment funds to file a 13-f disclosing their publicly traded security positions. It is required every 45 days, making all of the information a minimum of 45 days old. Looking at a successful investor’s 13F filings can be revealing, especially when looking at industries they’ve been hot on or comparing one holding period to another.

Wednesday 10/16

11:00 AM ET, The Mortgage Bankers Association (MBA) creates a statistic from several mortgage loan indexes. The Mortgage Applications index measures applications at mortgage lenders. It’s considered a leading indicator and is especially important for single-family home sales and housing construction. Both are considered foundational in a strong economy. Last week the Purchase Index was 162.6.

11:00 AM ET, The Mortgage Bankers Association (MBA) also provides an average 30-year mortgage level which is consistently calculated so that it is an oranges-to-oranges comparison from previous periods. Last period the rate was 7.14%.

12:30 PM ET, Export Prices (MoM), this data set reflects changes in prices of goods and services that are produced in and exported from the United States in the given month compared to the previous one. Last reading, this came in at a negative 0.8%.

12:30 PM ET, Import Prices (MoM) The import price index m/m measures the price changes of the respective month compared to the previous month. Last month they fell 1.2% (not adjusted for fx), this month, expectations are for a decline of 0.5%.

12:30 PM ET, U.S. Retail Sales have been flat, neither rising nor falling. As we head toward Thanksgiving and Black Friday sales levels, the market will be taking more and more interest in how strong the consumer is. Expectations for October are for a rise of 0.8 percent overall, an increase from 0.0 percent. When excluding vehicles, the projection is for an increase of 0.4%, up from 0.1%. and up 0.4 when also excluding gasoline.

1:15 PM ET, Capacity Utilization is expected to remain unchanged at an 80.3% use of available manufacturing capacity. Reading well above, this may be considered inflationary as production could be using less efficient means.

1:15 PM ET, Industrial Production is expected to have been weaker at a 0.2% increase compared to a 0.4% increase.

2:00 PM ET, NAHB Housing Market Index this is expected to continue weakening, the October number was 38.

2:00 PM ET, Business inventories are expressed in dollar value held by manufacturers, wholesalers, and retailers. The level of inventories in relation to sales is an important indicator of the near-term direction of production activity. Rising inventories can be an indication of business optimism that sales will be growing in the coming months. However, if unintended inventory accumulation occurs, then production will probably have to slow while those inventories are worked off. Last month’s inventories increased by 0.8%.

Thursday 10/17

12:30 PM ET, Housing Starts, last month housing starts had declined for the seventh consecutive month by 8.7%.

Friday 10/18

2:00 PM ET, Leading Economic Indicators are expected to show a decline of 0.3% vs. a decline of 0.4% the prior month.

What Else

The focus on signs of economic weakness or receding inflation will be high, and reactions may be extra sensitive. The following week is shortened in terms of trading. The focus will be on how strong the consumer shows they will be for the holidays.

Established New R&D Facility and Expanded Existing cGMP Manufacturing Facility

Received Notice of Allowance for Patent Applications Covering Directed Differentiation Methods for Retinal Pigmented Epithelium and Oligodendrocyte Progenitor Cells

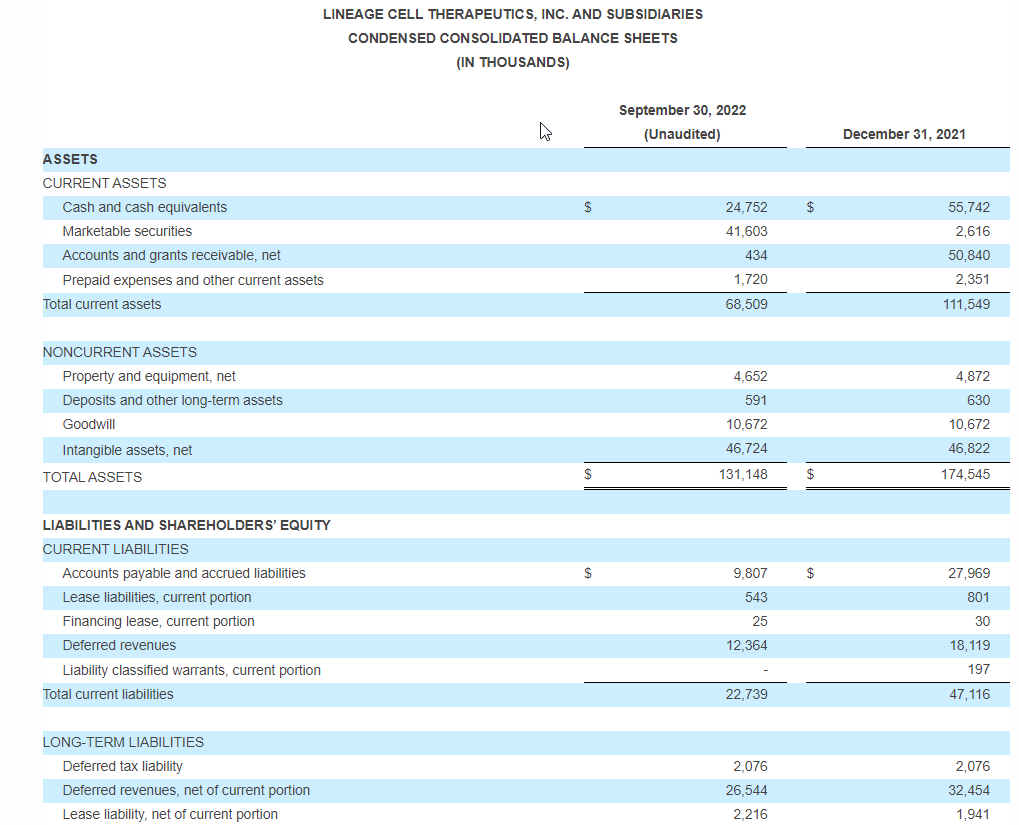

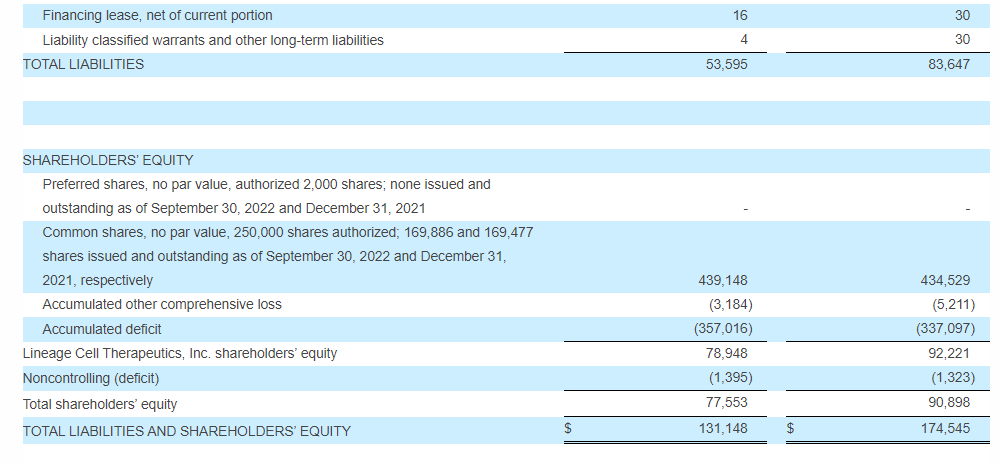

Cash, Cash Equivalents, and Marketable Securities of $66.4 Million as of September 30, 2022 Expected to Provide Capital Into Q3 2024

CARLSBAD, Calif.–(BUSINESS WIRE)–Nov. 10, 2022– Lineage Cell Therapeutics, Inc. (NYSE American and TASE: LCTX), a clinical-stage biotechnology company developing allogeneic cell therapies for unmet medical needs, today reported financial and operating results for the third quarter of 2022. Lineage management will host a conference call and webcast today at 4:30 p.m. Eastern Time/1:30 p.m. Pacific Time to discuss its third quarter 2022 financial and operating results and to provide a business update.

“A single administration of RG6501 (OpRegen®), a proprietary retinal pigment epithelial cell transplant, across an area of atrophy in advanced AMD patients has shown the potential to slow, stop, or reverse the progression of GA in our phase 1/2a clinical trial. To our knowledge, this is the first intervention that has reported anatomical changes of this magnitude in the field of GA, so we are pleased with the continued progress on RG6501 and the efforts which have been made to initiate its next clinical trial,” stated Brian M. Culley, Lineage CEO. “Looking ahead, our focus turns increasingly to planned regulatory interactions for OPC1 and VAC2, from which we expect to inform and enable their next phases of clinical development in spinal cord injury and oncology, respectively. In parallel, we are advancing our newly launched cell transplant programs in photoreceptors for vision disorders and auditory neurons for hearing loss, with initial preclinical studies from our photoreceptor program currently ongoing and the start of preclinical testing of our auditory neuron program anticipated prior to year-end. We believe that completing these efforts while maintaining our commitment to disciplined spending will help Lineage create shareholder value in the coming year.”

Recent milestones and activities included:

– Announced appointment of Jill Howe as Chief Financial Officer effective November 14, 2022

Ms. Howe brings more than 20 years of significant strategic, financial, and operational experience to Lineage, with an emphasis on capital strategy, corporate finance, treasury management, global infrastructure, and operational excellence. Ms. Howe has successfully built biotechnology organizations and implemented operational infrastructures alongside the execution of over $1.66 billion of capital raising transactions and will bring extensive strategic experience to the role.

– Established new U.S. R&D facility and expanded current GMP manufacturing facility in Israel

New Carlsbad facility will allow us to broaden R&D capabilities in the U.S. and facilitate the advancement of current and future allogeneic cell transplant programs and partnerships; the expansion of the Israel-based facility is expected to increase infrastructure, including development and optimization of larger-scale clinical manufacturing processes, and continued execution under the ongoing collaboration with Roche and Genentech for RG6501 (OpRegen).

Company announced notice of allowance of two patents covering processes for manufacturing allogeneic oligodendrocyte progenitor and retinal pigmented epithelium cells.

– OPC1

Completed verification and validation and preclinical testing activities for the novel parenchymal spinal delivery (PSD) system to support an upcoming regulatory submission.

– VAC2

Pre-Investigational New Drug (IND) application briefing package submitted to the U.S. Food and Drug Administration (FDA) to support U.S. clinical development for immuno-oncology.

– ANP1 & PNC1

Continued process development and activities in support of ongoing and planned preclinical testing.

Some of the key upcoming milestones and activities anticipated by Lineage include:

– Planned Regenerative Medicine Advanced Therapy (RMAT) submission to FDA before year-end regarding an OPC1 IND amendment to enable clinical testing of a novel spinal cord delivery system.

– Response to a pre-IND regulatory submission which should provide clarity on a VAC2 CMC, nonclinical, and clinical information package to inform future U.S. clinical development, expected around year-end.

– Completion of an R&D manufacturing process sufficient to support initiation of preclinical testing and the initiation of such testing with ANP1 for the treatment of hearing loss, anticipated prior to year-end.

– An additional OPC1 manuscript from a Phase 1/2a clinical study in subacute cervical spinal cord injury.

– Submission of a grant application to California Institute for Regenerative Medicine (CIRM) for the continued support of the clinical development of OPC1.

– Clinical data update from the ongoing VAC2 Phase 1 non-small cell lung cancer (NSCLC) study, pending release from Cancer Research UK (CRUK).

– Evaluation of new partnership opportunities and/or expansion of existing collaborations.

– Continued participation in investor and partnering meetings and medical and industry conferences to broaden awareness of our mission, programs, and accomplishments.

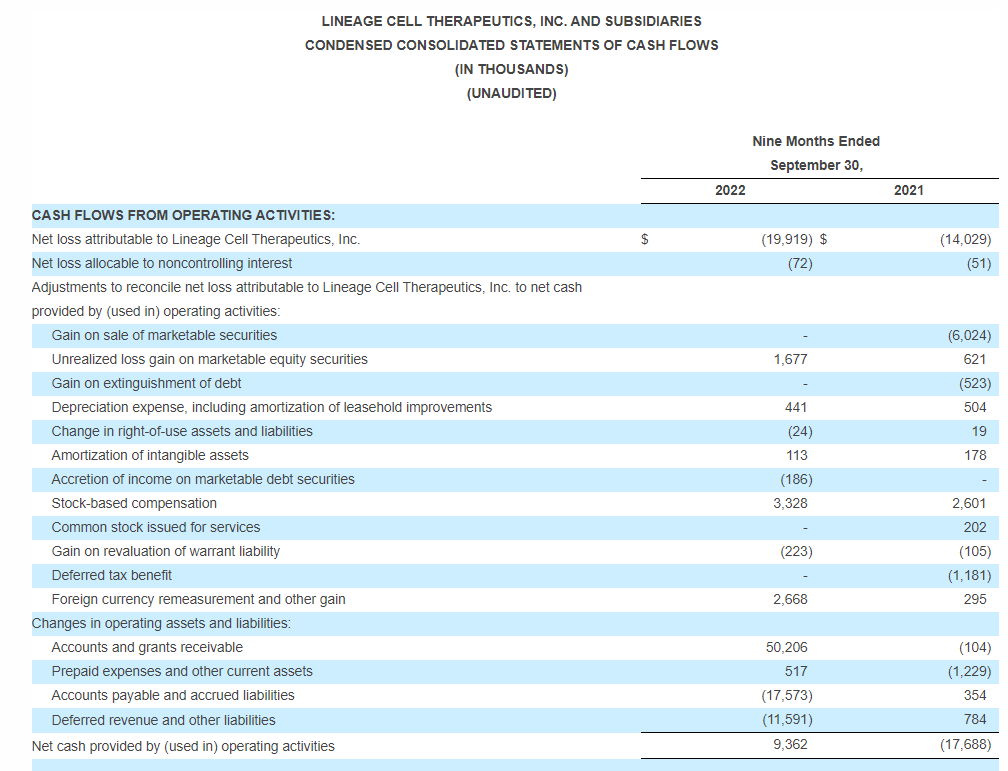

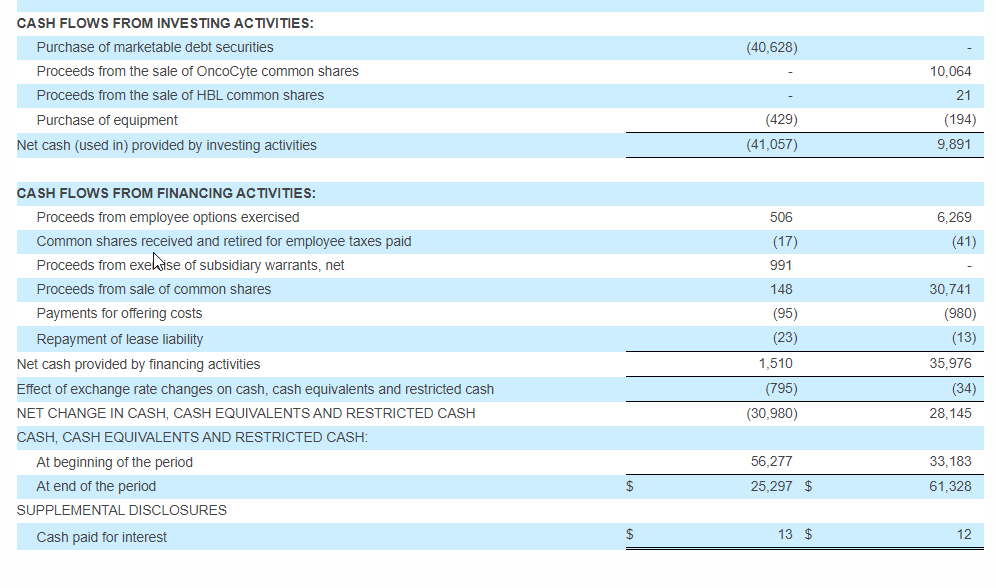

Balance Sheet Highlights

Cash, cash equivalents, and marketable securities totaled $66.4 million as of September 30, 2022, which is expected to support planned operations into Q3 2024.

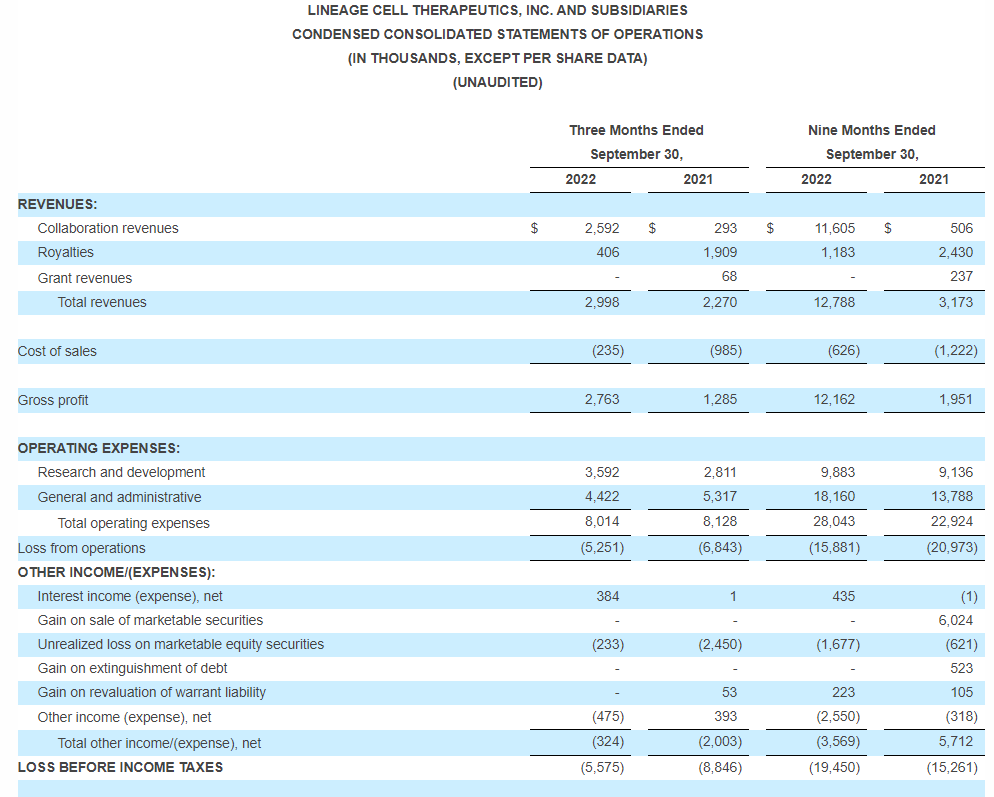

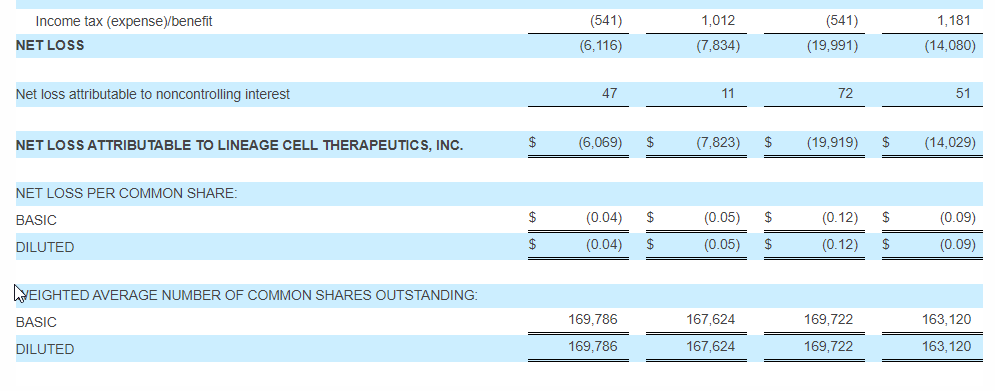

Third Quarter Operating Results

Revenues: Lineage’s revenue is generated primarily from licensing fees, royalties, collaboration revenues, and research grants. Total revenues for the three months ended September 30, 2022 were approximately $3.0 million, a net increase of $0.7 million as compared to $2.3 million for the same period in 2021. The increase was driven by collaboration and licensing revenue recognized from deferred revenues from the Roche Agreement, partially offset by less royalty revenues.

Operating Expenses: Operating expenses are comprised of research and development (“R&D”) expenses and general and administrative (“G&A”) expenses. Total operating expenses for the three months ended September 30, 2022 were $8.0 million, a decrease of $0.1 million as compared to $8.1 million for the same period in 2021.

R&D Expenses: R&D expenses for the three months ended September 30, 2022 were $3.6 million, a net increase of $0.8 million as compared to $2.8 million for the same period in 2021. The net increase was primarily driven by higher OpRegen related expenses to support the Roche collaboration.

G&A Expenses: G&A expenses for the three months ended September 30, 2022 were $4.4 million, a net decrease of approximately $0.9 million as compared to $5.3 million for the same period in 2021. The decrease was primarily driven by $1.1 million in lower litigation and legal expenses and $0.3 million in lower investor relations expense, partially offset by a $0.5 million increase in payroll and related benefits expense.

Loss from Operations: Loss from operations for the three months ended September 30, 2022 was $5.2 million, a decrease of $1.6 million as compared to $6.8 million for the same period in 2021.

Other Expenses, Net: Other expenses, net for the three months ended September 30, 2022 reflected other expense, net of $0.3 million, compared to other expense, net of $2.0 million for the same period in 2021. The net change was primarily driven by a decrease in the value of marketable equity securities and exchange rate fluctuations related to Lineage’s international subsidiaries.

Net Loss Attributable to Lineage: The net loss attributable to Lineage for the three months ended September 30, 2022 was $6.1 million, or $0.04 per share (basic and diluted), compared to a net loss attributable to Lineage of $7.8 million, or $0.05 per share (basic and diluted), for the same period in 2021.

Conference Call and Webcast

Interested parties may access today’s conference call by dialing (800) 715-9871 from the U.S. and Canada and should request the “Lineage Cell Therapeutics Call” or provide conference ID number 5262180. A live webcast of the conference call will be available online in the Investors section of Lineage’s website. A replay of the webcast will be available on Lineage’s website for 30 days and a telephone replay will be available through November 17, 2022, by dialing (800) 770-2030 from the U.S. and Canada and entering conference ID number 5262180.

About Lineage Cell Therapeutics, Inc.

Lineage Cell Therapeutics is a clinical-stage biotechnology company developing novel cell therapies for unmet medical needs. Lineage’s programs are based on its robust proprietary cell-based therapy platform and associated in-house development and manufacturing capabilities. With this platform Lineage develops and manufactures specialized, terminally differentiated human cells from its pluripotent and progenitor cell starting materials. These differentiated cells are developed to either replace or support cells that are dysfunctional or absent due to degenerative disease or traumatic injury or administered as a means of helping the body mount an effective immune response to cancer. Lineage’s clinical and preclinical programs are in markets with billion dollar opportunities and include five allogeneic (“off-the-shelf”) product candidates: (i) OpRegen, a retinal pigment epithelial cell therapy in development for the treatment of geographic atrophy secondary to age-related macular degeneration, is being developed under a worldwide collaboration with Roche and Genentech, a member of the Roche Group; (ii) OPC1, an oligodendrocyte progenitor cell therapy in Phase 1/2a development for the treatment of acute spinal cord injuries; (iii) VAC2, a dendritic cell therapy produced from Lineage’s VAC technology platform for immuno-oncology and infectious disease, currently in Phase 1 clinical development for the treatment of non-small cell lung cancer; (iv) ANP1, an auditory neuronal progenitor cell therapy for the potential treatment of auditory neuropathy; and (v) PNC1, a photoreceptor neural cell therapy for the potential treatment of vision loss due to photoreceptor dysfunction or damage. For more information, please visit www.lineagecell.com or follow the company on Twitter @LineageCell.

Forward-Looking Statements

Lineage cautions you that all statements, other than statements of historical facts, contained in this press release, are forward-looking statements. Forward-looking statements, in some cases, can be identified by terms such as “believe,” “aim,” “may,” “will,” “estimate,” “continue,” “anticipate,” “design,” “intend,” “expect,” “could,” “can,” “plan,” “potential,” “predict,” “seek,” “should,” “would,” “contemplate,” “project,” “target,” “tend to,” or the negative version of these words and similar expressions. Such statements include, but are not limited to, statements relating to: our ability to support our planned operations into the third quarter of 2024 with our existing cash, cash equivalents and marketable securities; Ms. Howe’s employment with Lineage and the anticipated or implied benefits thereof to Lineage and Lineage’s continued growth and ability to exhibit greater productivity in the future; plans and expectations regarding our products in development and our ability to advance our product candidates into their next phases of clinical or preclinical testing; our ability to create shareholder value in the future; the potential benefits to us and our operations of our new and expanded facilities, including the broadening of our R&D capabilities, advancing our programs and partnerships, and increasing our infrastructure; our ability to support multiple years of progress and achieve important milestones; our collaboration and license agreement with Roche and Genentech and the potential to receive milestone and other consideration thereunder; the potential benefits of treatment with OpRegen; the potential future achievements of our clinical and preclinical programs; the timing of anticipated FDA interactions, preclinical activities, clinical trials, and clinical data updates related to our programs, and the submission of a grant application to the CIRM; plans and expectations regarding publications relating to our programs; plans and expectations regarding potential new partnership opportunities and existing collaborations; and our ability to broaden awareness of our mission and accomplishments. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause Lineage’s actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by the forward-looking statements in this press release, including, but not limited to, the following risks: that we may need to allocate our cash to unexpected events and expenses causing us to use our cash more quickly than expected; that potential benefits of the new and expanded facilities to the Company and its operations may not be realized as quickly as expected or at all; that potential benefits of newly developed intellectual property to the Company may not be realized as quickly as expected or at all; that positive findings in early clinical and/or nonclinical studies of a product candidate may not be predictive of success in subsequent clinical and/or nonclinical studies of that candidate; that competing alternative therapies may adversely impact the commercial potential of OpRegen; that Roche and Genentech may not successfully advance OpRegen or be successful in completing further clinical trials for OpRegen and/or obtaining regulatory approval for OpRegen in any particular jurisdiction; that we may not establish new partnerships or expand existing collaborations; that we do not successfully broaden awareness of our mission or accomplishments; that we may not be able to manufacture sufficient clinical quantities of its product candidates in accordance with current good manufacturing practice; and those risks and uncertainties inherent in Lineage’s business and other risks discussed in Lineage’s filings with the Securities and Exchange Commission (SEC). Lineage’s forward-looking statements are based upon its current expectations and involve assumptions that may never materialize or may prove to be incorrect. All forward-looking statements are expressly qualified in their entirety by these cautionary statements. Further information regarding these and other risks is included under the heading “Risk Factors” in Lineage’s periodic reports with the SEC, including Lineage’s most recent Annual Report on Form 10-K and Quarterly Report on Form 10-Q filed with the SEC and its other reports, which are available from the SEC’s website. You are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they were made. Lineage undertakes no obligation to update such statements to reflect events that occur or circumstances that exist after the date on which they were made, except as required by law.

How Cancer Cells can Become Immortal – New Research Finds a Mutated Gene that Helps Melanoma Defeat the Normal Limits on Repeated Replication

A defining characteristic of cancer cells is their immortality. Usually, normal cells are limited in the number of times they can divide before they stop growing. Cancer cells, however, can overcome this limitation to form tumors and bypass “mortality” by continuing to replicate.

Telomeres play an essential role in determining how many times a cell can divide. These repetitive sequences of DNA are located at the ends of chromosomes, structures that contain genetic information. In normal cells, continued rounds of replication shorten telomeres until they become so short that they eventually trigger the cell to stop replicating. In contrast, tumor cells can maintain the lengths of their telomeres by activating an enzyme called telomerase that rebuilds telomeres during each replication.

Telomeres are protective caps at the ends of chromosomes

Telomerase is encoded by a gene called TERT, one of the most frequently mutated genes in cancer. TERT mutations cause cells to make a little too much telomerase and are thought to help cancer cells keep their telomeres long even though they replicate at high rates. Melanoma, an aggressive form of skin cancer, is highly dependent on telomerase to grow, and three-quarters of all melanomas acquire mutations in telomerase. These same TERT mutations also occur across other cancer types.

Unexpectedly, researchers found that TERT mutations could only partially explain the longevity of telomeres in melanoma. While TERT mutations did indeed extend the life span of cells, they did not make them immortal. That meant there must be something else that helps telomerase allow cells to grow uncontrollably. But what that “second hit” might be has been unclear.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Pattra Chun-OnPh.D. Candidate in Environmental and Occupational Health, University of Pittsburgh Health Sciences and Jonathan AlderAssistant Professor of Medicine, University of Pittsburgh Health Sciences.

We are researchers who study the role telomeres play in human health and diseases like cancer in the Alder Lab at the University of Pittsburgh. While investigating the ways that tumors maintain their telomeres, we and our colleagues found another piece to the puzzle: another telomere-associated gene in melanoma.

Cell Immortality Gets a Boost

Our team focused on melanoma because this type of cancer is linked to people with long telomeres. We examined DNA sequencing data from hundreds of melanomas, looking for mutations in genes related to telomere length.

We identified a cluster of mutations in a gene called TPP1. This gene codes for one of the six proteins that form a molecular complex called shelterin that coats and protects telomeres. Even more interesting is the fact that TPP1 is known to activate telomerase. Identifying the TPP1 gene’s connection to cancer telomeres was, in a way, obvious. After all, it was more than a decade ago that researchers showed that TPP1 would increase telomerase activity.

We tested whether having an excess of TPP1 could make cells immortal. When we introduced just TPP1 proteins into cells, there was no change in cell mortality or telomere length. But when we introduced TERT and TPP1 proteins at the same time, we found that they worked synergistically to cause significant telomere lengthening.

To confirm our hypothesis, we then inserted TPP1 mutations into melanoma cells using CRISPR-Cas9 genome editing. We saw an increase in the amount of TPP1 protein the cells made, and a subsequent increase in telomerase activity. Finally, we returned to the DNA sequencing data and found that 5% of all melanomas have a mutation in both TERT and TPP1. While this is still a significant proportion of melanomas, there are likely other factors that contribute to telomere maintenance in this cancer.

Our findings imply that TPP1 is likely one of the missing puzzle pieces that boost telomerase’s capacity to maintain telomeres and support tumor growth and immortality.

Making Cancer Mortal

Knowing that cancer use these genes in their replication and growth means that researchers could also block them and potentially stop telomeres from lengthening and make cancer cells mortal. This discovery not only gives scientists another potential avenue for cancer treatment but also draws attention to an underappreciated class of mutations outside the traditional boundaries of genes that can play a role in cancer diagnostics.

QuoteMedia is a leading software developer and cloud-based syndicator of financial market information and streaming financial data solutions to media, corporations, online brokerages, and financial services companies. The Company licenses interactive stock research tools such as streaming real-time quotes, market research, news, charting, option chains, filings, corporate financials, insider reports, market indices, portfolio management systems, and data feeds. QuoteMedia provides industry leading market data solutions and financial services for companies such as the Nasdaq Stock Exchange, TMX Group (TSX Stock Exchange), Canadian Securities Exchange (CSE), London Stock Exchange Group, FIS, U.S. Bank, Broadridge Financial Systems, JPMorgan Chase, CI Financial, Canaccord Genuity Corp., Hilltop Securities, HD Vest, Stockhouse, Zacks Investment Research, General Electric, Boeing, Bombardier, Telus International, Business Wire, PR Newswire, FolioFN, Regal Securities, ChoiceTrade, Cetera Financial Group, Dynamic Trend, Inc., Qtrade Financial, CNW Group, IA Private Wealth, Ally Invest, Inc., Suncor, Virtual Brokers, Leede Jones Gable, Firstrade Securities, Charles Schwab, First Financial, Cirano, Equisolve, Stock-Trak, Mergent, Cision, Day Trade Dash and others. Quotestream®, QModTM and Quotestream ConnectTM are trademarks of QuoteMedia. For more information, please visit www.quotemedia.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mixed Q3 results. The company reported revenue of $4.39 million, missing our estimate of $4.76 million by 7.7%. Revenues were partially impacted by currency exchange. Adj. EBITDA of $670,000 was in line with our estimate of $680,000. While revenue was below our estimate the company still grew revenue by 15% and is on pace for historic high revenue.

Currency rate impact. Over the latest quarter, the Canadian dollar (CAD) depreciated against the U.S dollar (USD). Depreciation of CAD negatively affected company revenues, as the company receives roughly 33% of its revenue in CAD. Management noted that on a constant currency basis Q3 revenue growth would have been approximately 18% to 19%, considerably closer to company guidance of 20% revenue growth.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers. Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony, and IBM among others. Headquartered in Chelmsford, Massachusetts , Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific .

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q3 results. The company reported strong results despite a challenging macroeconomic environment. Third quarter revenue was $53.9 million, beating our estimate of $50.25 million by 7.2%. Adj. EBITDA of $5.3 million was a hair below our estimate of $5.5 million, largely due to the mix in lower margin revenue from its fulfillment & logistics segment.

Counter cyclical segments. The company has a unique revenue mix that carries counter cyclical qualities in its fulfillment & logistics and customer care segments. Fulfillment & logistics beat our revenue estimate of $19 million by 23.7%, and is expected to continue its strong performance through 2023.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q3 results. The company reported another strong quarter, beating our estimates on both revenue and adj. EBITDA. Revenue of $26.0 million was 41% better than our forecast of $18.4 million and adj. EBITDA of $2.4 million beat our forecast of $1.8 million by 34%.

Sell-side revenue jumps. Sell-side revenue from Colossus SSP continues to drive the company’s impressive growth. The SSP generated $18.9 million in the quarter, 64% better than our forecast of $11.5 million.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex announced it has received approval to uplist to the NYSE. Shares are expected to begin trading on November 15 under the symbol OILS (warrants will trade under OILSW). The uplisting follows a October 31st announcement that Permex would consolidate outstanding shares on the basis of a one for every sixty pre-consolidation shares. We indicated at the time that we believed management was doing a reverse stock split as a prerequisite to uplisting on the NYSE. We believe listing on the NYSE will greatly enhance the company’s ability to attract investor attention and unlock Permex’s hidden value.

Permex has filed an offering registration. On November 4th, Permex file a S-1 Registration Statement with the SEC to offer 2 million common shares (post reverse stock split currently trading under the symbol OIL on the Toronto exchange and on the OTC under the symbol OILCD.) On November 9th, the company filed an addendum increasing the share offering to 3.6 million shares which now include a warrant to purchase shares at a 125% premium to the offering price. The offering is being done in conjunction with the uplisting implying it will be completed by November 15th.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

One Stop Systems, Inc. (OSS) designs and manufactures innovative AI Transportable edge computing modules and systems, including ruggedized servers, compute accelerators, expansion systems, flash storage arrays, and Ion Accelerator™ SAN, NAS, and data recording software for AI workflows. These products are used for AI data set capture, training, and large-scale inference in the defense, oil and gas, mining, autonomous vehicles, and rugged entertainment applications. OSS utilizes the power of PCI Express, the latest GPU accelerators and NVMe storage to build award-winning systems, including many industry firsts, for industrial OEMs and government customers. The company enables AI on the Fly® by bringing AI datacenter performance to ‘the edge,’ especially on mobile platforms, and by addressing the entire AI workflow, from high-speed data acquisition to deep learning, training, and inference. OSS products are available directly or through global distributors. For more information, go to www.onestopsystems.com.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Results. Record quarterly revenue of $18.8 million, up 17.7% y-o-y. Consensus was $18.5 million and we also had forecast $18.5 million. OSS reported GAAP net income of $132,533, or $0.01 per share, compared to $980,696, or $0.05 per share last year. Adjusted EPS was $0.03 in 3Q22, compared to $0.08 per share in 3Q21. We were at $0.02 and $0.04, respectively. Consensus was at $0.04 per share.

AI Transportable Business a Contributor. The AI Transportable business posted solid growth in the quarter, with two AI Transportable clients now in the top 10 of OSS’s clients. The Company won six major programs during the quarter, five of which are in the AI Transportables space. At quarter’s end, OSS had 30 pending awards, 18 of which are in the AI Transportables space.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Genco Shipping & Trading Limited, incorporated on September 27, 2004, transports iron ore, coal, grain, steel products and other drybulk cargoes along shipping routes through the ownership and operation of drybulk carrier vessels. The Company is engaged in the ocean transportation of drybulk cargoes around the world through the ownership and operation of drybulk carrier vessels. As of December 31, 2016, its fleet consisted of 61 drybulk carriers, including 13 Capesize, six Panamax, four Ultramax, 21 Supramax, two Handymax and 15 Handysize drybulk carriers, with an aggregate carrying capacity of approximately 4,735,000 deadweight tons (dwt). Of the vessels in its fleet, 15 are on spot market-related time charters, and 27 are on fixed-rate time charter contracts. As of December 31, 2016, additionally, 19 of the vessels in its fleet were operating in vessel pools.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Locking in shipping rates when prices were high is paying off. Genco reported revenues of $136 million for the 2022-3Q. While revenues were below 2021-3Q levels of $155 million, they were close to 2022-2Q levels and our expectations. TCE rates were $23,624 down slightly from the previous quarter due to lower spot rates, but reflective of management’s strategy of locking in rates for roughly 75% of shipping days. With spot rates now having fallen below $15,000, such a strategy is proving to have paid off.

Costs are rising but shipping rates are still well above Genco’s break-even point. Genco, like most of the industry, is facing higher costs as labor, steel, and fuel costs rise. That said, shipping rates (even lower spot rates) are well above Genco’s break-even point of roughly $9,000/shipping day. The company continues to generate large significant free cash flow which it has used to reduce debt ($261 million since 2021) and pay a dividend ($2.74 per share in the last four quarters). Free cash flow will most likely decline in future quarters, but should be ample enough to continue to reduce debt and pay a dividend.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

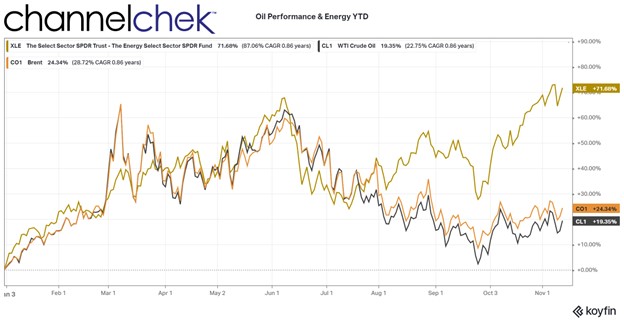

Factors Still Point to Higher Oil Prices and Sizeable Bets on Crude

There are many factors impacting why traditional energy prices and producers may have a hurricane-force tailwind heading into the holidays and next year.

A boost in demand for oil is expected as China just announced that it is lowering its quarantine requirements for visitors from outside the country. But Chinese Covid policies aren’t the only impetus pushing up oil demand – around the globe, there are supply challenges that are playing out. Oil hasn’t risen above $100 a barrel since early Summer, some traders are speculating it will rise above $200 in the coming months. Here’s why.

China

In addition to the announcement that the CPR was cutting the required quarantine period for the country (to five days from seven, with three days of home isolation), the required PCR test hurdle is being lowered as well. And airlines no longer run the risk of being suspended if the travelers they bring in that test positive is five or more.

Europe

The European Union has agreed to stop all oil imports from Russia on Dec. 5. The plan is to cap the prices at which EU nations would buy oil from Russia, that price is expected to be near $60 per barrel. Russia has reacted by increasing exports to Asia, but the price cap is expected to reduce its exports and lower total supply by up to one million barrels per day.

United States

Back in May, the U.S. took the drastic step of increasing available supply by selling oil from the U.S. Strategic Petroleum Reserve at a rate of nearly one million barrels per day starting in May. The increased supply has kept oil prices down. But the sales are unsustainable and expected to be reduced. Congress has allowed another sale of 26 million barrels that are expected to carry through to October 2023. This is a much slower pace of oil releases from the reserves. Plus, the reserves will need to be replenished.

After the Congressionally approved release, the reserve will be down to 348 million barrels, this is half the quantity compared to January of this year —the lowest since 1983. Congress has said that the reserve must stay above 252.4 million barrels, and the incoming Congress is expected to be more conservative when it comes to using these strategic assets to control prices.

Production growth overall in the U.S. has stalled after having increased through most of the year. Government data show that U.S. production dropped to 11.9 million barrels per day last week, this is tied for the lowest level in several months. Supplies of products such as diesel and heating oil in the U.S. are at multiyear lows. So there is not abundant supply should a weather-related or some other fuel-demanding crisis surface.

Oil is now trading between $92 and $93 a barrel. It had reached a high above $130 in March, shortly after the war began, and hasn’t seen the $100 a barrel level since late June.

Trading this week showed significant flows into an options contract that speculates that $200 per barrel may be in store. The most actively traded Brent crude options contract on Thursday was an option to buy Brent at $200 in March 2023. This was the most active oil contract of the day.

How significant is this bullish activity surrounding oil prices? The ratio of bullish to bearish bets in the options market is wider than at any time in recorded history, according to Bloomberg. Oil options traders are positioned more aggressively than ever before.

Take Away

Oil demand could rise soon in China as travel restrictions are lessened. Elsewhere in the world, oil demand is expected to increase as supplies remain the same or decrease. Demand remained elevated globally despite slower economies.

With supply likely to drop and demand ramping up, $200 by the third week in March is one price expectation for a record number of trades transacted at recently. More than doubling in a few months sounds unthinkable, but the massive trades were transacted by experienced institutional traders.

MIAMI, Nov. 10, 2022 (GLOBE NEWSWIRE) — As previously announced, Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”) confirmed today that the 1-for-10 reverse stock split of the Company’s Class A and Class B common stock became effective as of 12:01 a.m. EST on November 10, 2022 (the “Effective Time”).

Motorsport Games effected the reverse stock split by filing a charter amendment with the Delaware Secretary of State. The reverse stock split was previously approved by the Company’s Board of Directors and stockholders pursuant to Sections 228 and 242 of the Delaware General Corporation Law.

The Company’s Class A common stock began trading on the NASDAQ on a split-adjusted basis when the market opened today, November 10, 2022, under a new CUSIP number, 62011B 201.

As a result of the reverse stock split, each 10 shares of the Company’s Class A and Class B common stock issued and outstanding immediately prior to the Effective Time were automatically combined into 1 share of Class A common stock and Class B common stock, respectively, subject to the elimination of fractional shares, as described below.

The same 1-for-10 reverse stock split ratio was used to effect the reverse stock split of both Motorsport Games Class A and Class B common stock, and accordingly, all stockholders were affected proportionately. The reverse stock split reduced the Company’s issued and outstanding shares of common stock from approximately 11,673,587 shares of Class A common stock and 7,000,000 shares of Class B common stock to approximately 1,167,358 and 700,000 shares, respectively.

The number of shares of Class A common stock subject to the Company’s outstanding employee and director stock options, as well as the relevant exercise price per share, will be proportionately adjusted to reflect the reverse stock split. Accordingly, the approximately 821,962 outstanding stock options will be reduced to approximately 82,196 outstanding stock options. The number of shares authorized for issuance under the Company’s stock plan will also be reduced from 1,000,000 shares of Class A common stock to 100,000 shares of Class A common stock using the same 1-for-10 split ratio.

The Company has notified NASDAQ that the Company is not in compliance with the Nasdaq Listing Rules requiring minimum of 500,000 publicly held shares.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

FORWARD-LOOKING STATEMENTS

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, unexpected developments with respect to the reverse stock split, including, without limitation, future decreases in the price of the Company’s Class A common stock whether due to, among other things, the announcement of the reverse stock split, the Company’s inability to make its Class A common stock more attractive to a broader range of institutional or other investors. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

Websites

Social Media

motorsportgames.com

Twitter: @msportgames & @traxiongg

traxion.gg

Instagram: msportgames & traxiongg

motorsport.com

Facebook: Motorsport Games & traxiongg

LinkedIn: Motorsport Games

Twitch: traxiongg

Reddit: traxiongg

The contents of these websites and social media channels are not part of, nor will they be incorporated by reference into, this press release.