Key Points: – Olipop raised $50 million in a Series C funding round, valuing the prebiotic soda brand at $1.85 billion as it competes with rivals such as Poppi. – Olipop is now the top nonalcoholic beverage brand in the U.S., both by dollar sales and unit growth, according to data from Circana/SPINS. – The company is now profitable, with annual sales surpassing $400 million last year.

Prebiotic soda brand Olipop announced Wednesday that it had secured a $50 million investment in its latest Series C funding round, bringing its valuation to an impressive $1.85 billion. The funding marks a significant milestone for the brand, which has been rapidly growing in the competitive functional beverage market.

Founded in 2018, Olipop has played a pivotal role in popularizing prebiotic sodas, offering consumers a gut-health-focused alternative to traditional soft drinks. Alongside competitor Poppi, Olipop has successfully tapped into the wellness trend sweeping the beverage industry, positioning itself as a healthier alternative to mainstream sodas.

The latest investment round was led by J.P. Morgan Private Capital’s Growth Equity Partners, reflecting strong investor confidence in the brand’s future. Olipop intends to use the fresh capital to expand its product lineup, increase marketing efforts, and enhance distribution channels, ensuring wider availability of its sodas across the U.S. and beyond.

A Market Leader in Functional Beverages

Olipop has swiftly risen to dominance, becoming the top nonalcoholic beverage brand in the U.S. based on both dollar sales and unit growth, according to Circana/SPINS data. The company reports that approximately half of its growth stems from consumers switching from traditional soda brands, while the other half comes from new entrants into the carbonated beverage market. Notably, one in four Gen Z consumers has tried Olipop, highlighting its appeal among younger demographics.

A key factor in Olipop’s success has been its strategic branding and marketing, which emphasize its natural ingredients and gut-health benefits. The brand’s product formulations incorporate prebiotic fibers, botanicals, and plant-based ingredients, catering to health-conscious consumers seeking flavorful yet functional beverages.

Financial Growth and Profitability

Olipop reached profitability in early 2024, a significant achievement for a relatively young brand. Annual sales exceeded $400 million last year, doubling from the previous year. This rapid financial growth has attracted attention from major players in the beverage industry, with Olipop’s founder and CEO Ben Goodwin revealing that soda giants PepsiCo and Coca-Cola have already expressed interest in potential acquisition deals.

Competition and Industry Trends

Despite Olipop’s success, competition in the prebiotic soda space remains fierce. Poppi, a direct rival founded a decade ago, has also seen substantial growth. The company had raised $39.3 million as of 2023 at an undisclosed valuation, and its annual sales reportedly surpassed $100 million last year. Poppi gained widespread recognition with its Super Bowl advertisements in consecutive years, solidifying its presence in the category.

However, Poppi has faced challenges, including legal scrutiny over its health claims. The company is currently negotiating a settlement in a lawsuit alleging that its marketing misrepresented the true health benefits of its beverages.

As the functional beverage market continues to expand, Olipop’s latest funding round positions it strongly for future growth, allowing it to scale operations and maintain its leadership in the rapidly evolving industry.

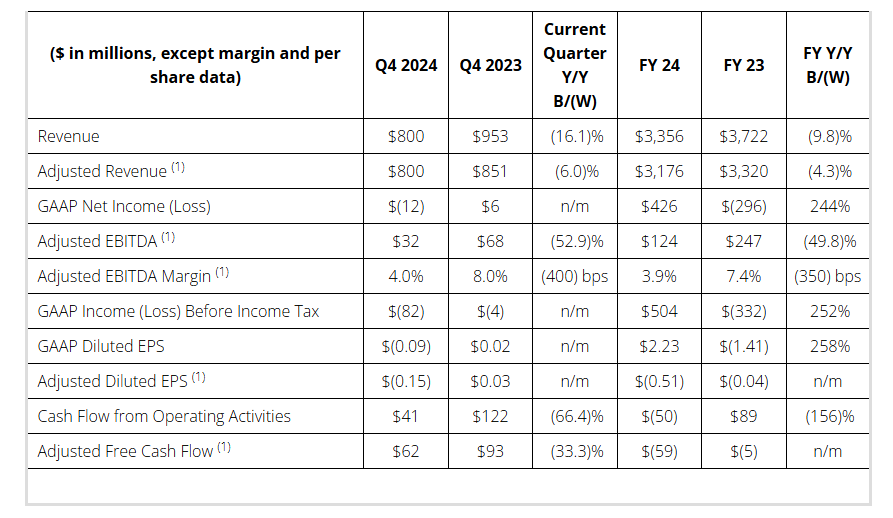

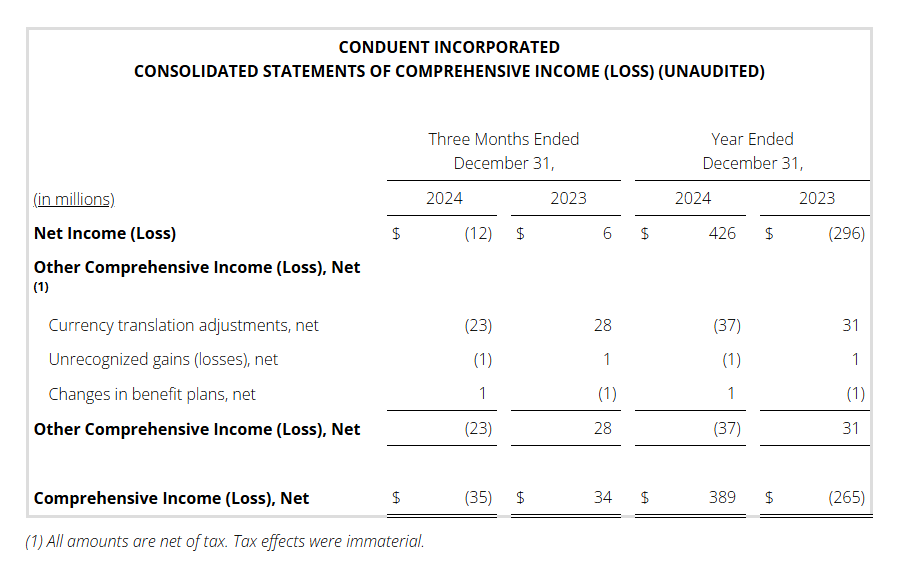

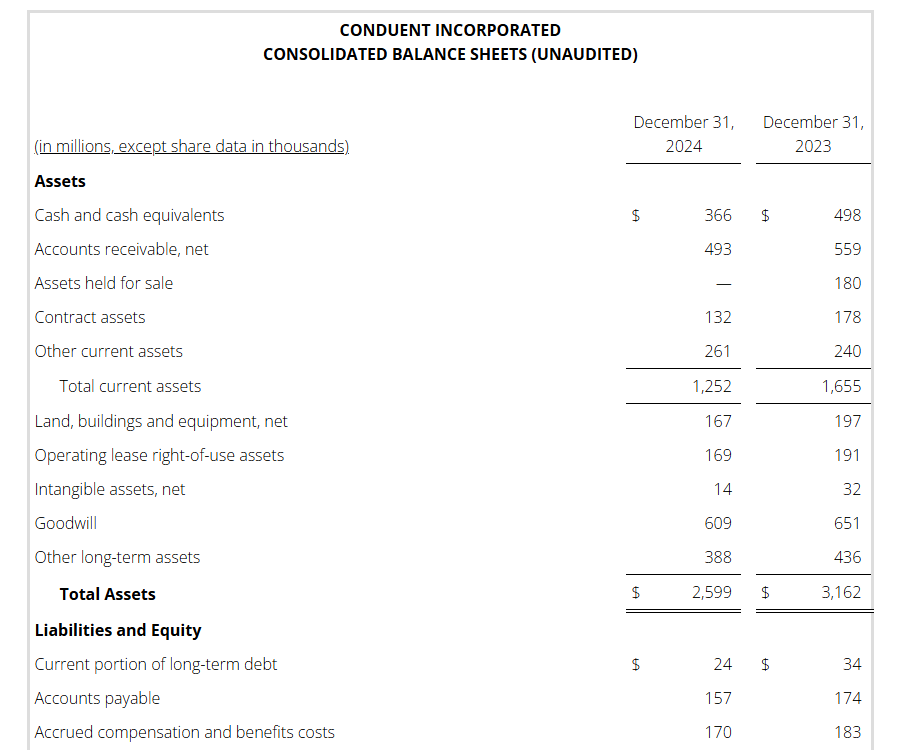

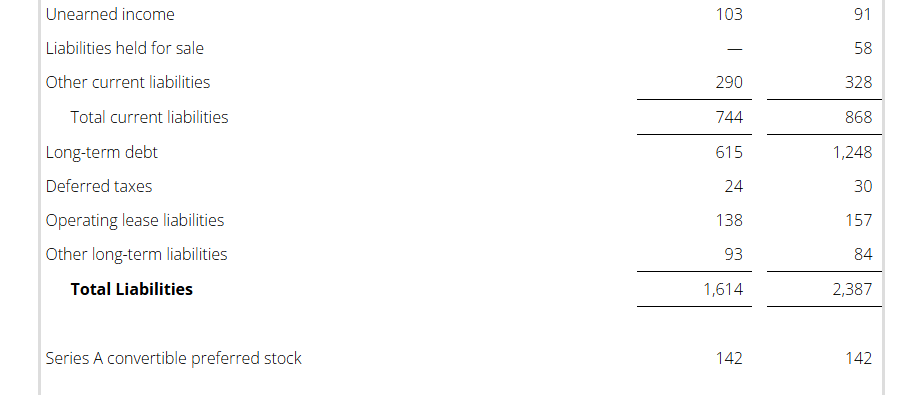

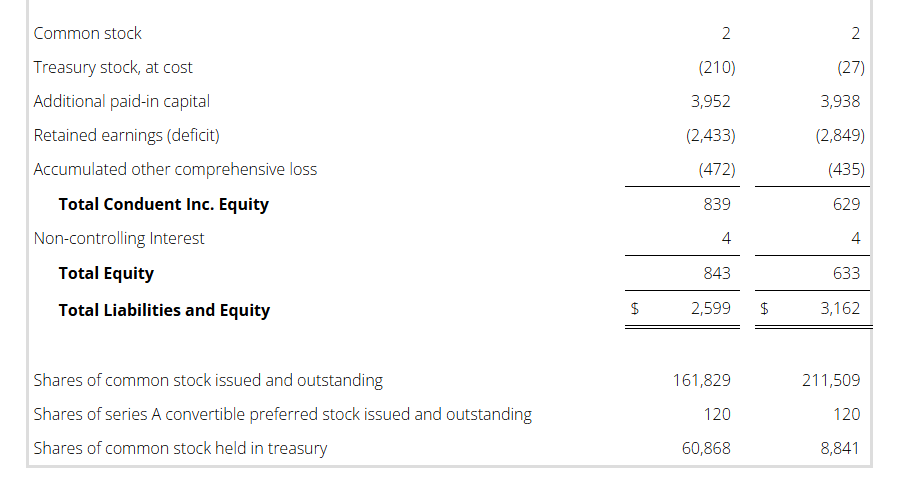

New Business Signings ACV (2) : Q4 $137M / FY $485M

Net ARR Activity Metric (2) (TTM): $92M

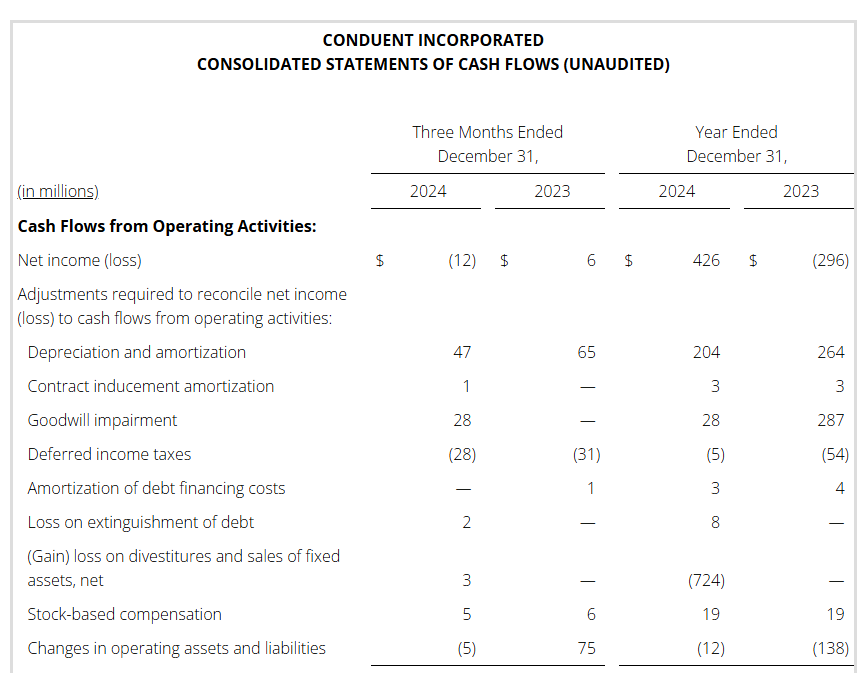

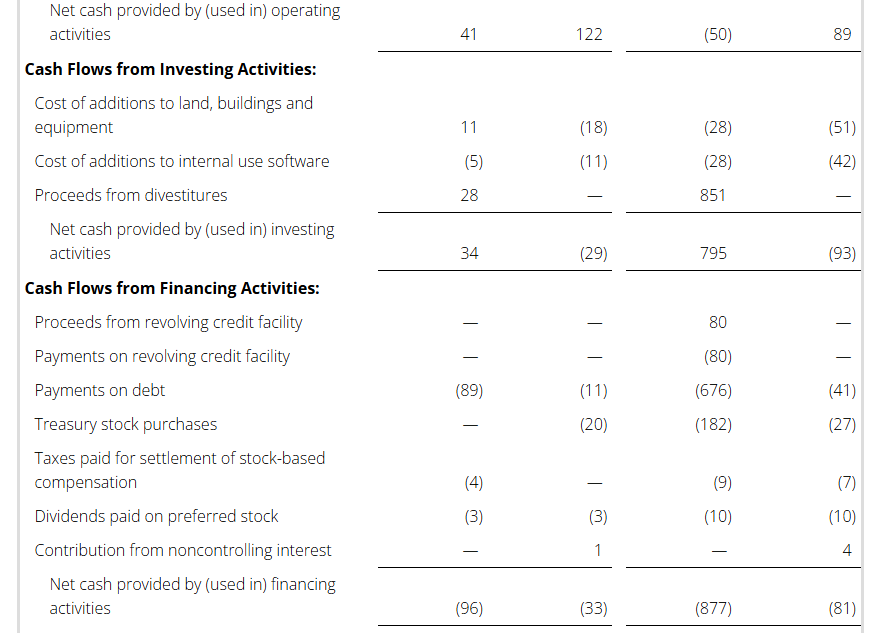

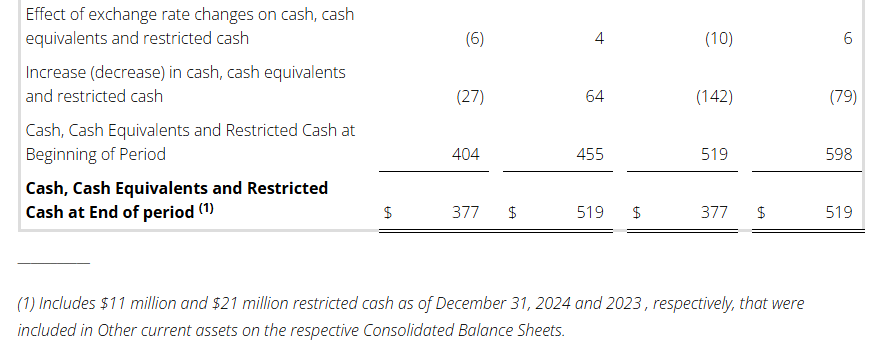

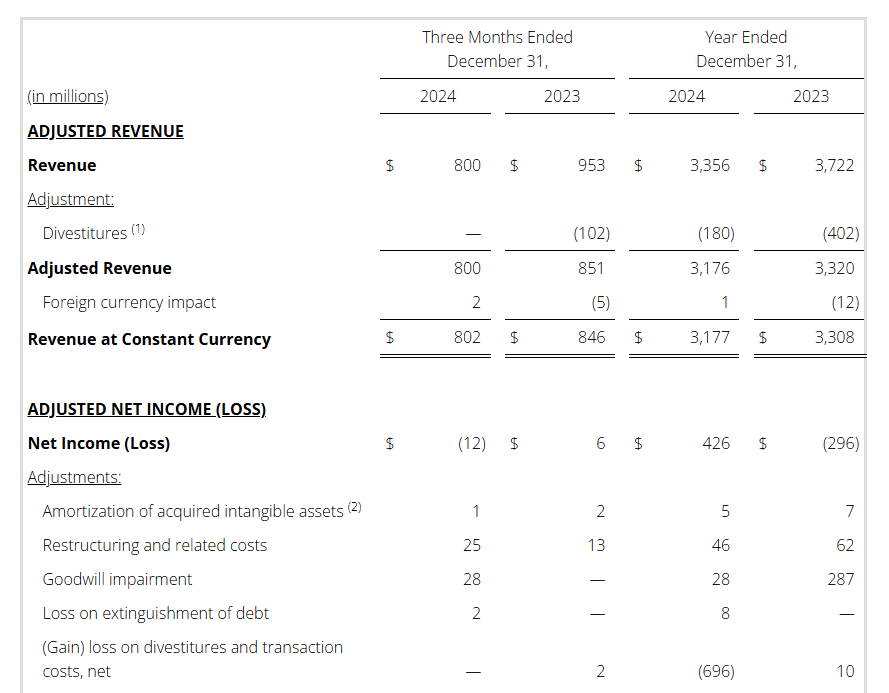

FLORHAM PARK, N.J., Feb. 12, 2025 — Conduent Incorporated (Nasdaq: CNDT), a global technology-led business process solutions and services company, today announced its fourth quarter and full year 2024 financial results.

Cliff Skelton, Conduent President and Chief Executive Officer stated, “2024 proved to be broadly in line with what we planned for. It was a year we said would be characterized by a continued shift to growth, with a focus on new leadership, a rationalized portfolio, improved industry recognition, and improved client retention. It was all of that and more, enhanced by divestitures with solid multiples and a 50% reduction in debt compared to year-end 2023.”

“From a numbers perspective, while timing drove a slightly weaker top line finish to the year, it was offset by an EBITDA margin on the high end of expectations. Quarterly Adjusted Revenue improved sequentially for the past three quarters and Adjusted EBITDA also increased over the past three quarters.”

“We remain bullish on achieving expectations in 2025. We continue to see opportunities for a further rationalized portfolio and remain focused on delivering outstanding service to our valued client base.”

Key Financial Q4 & Full Year 2024 Results

Performance Commentary During 2024, the Company completed three divestitures as part of its portfolio rationalization strategy. The transfer of the BenefitWallet portfolio was completed during the second quarter of 2024 for a total purchase price of $425 million. During the second quarter of 2024, the company also completed the sale of the Curbside Management and Public Safety businesses with a purchase price of $230 million, $50 million of which is deferred to the first half of 2025. During the third quarter of 2024, the company completed the sale of the Casualty Claims Solutions Business and received $224 million of cash consideration.

Also, during 2024, the Company used a portion of the proceeds from the divested businesses to voluntarily prepay all of the principal of the Term Loan B and $137 million of the Term Loan A.

Conduent’s liquidity position remains strong with long-dated debt maturities and a modest net leverage ratio.

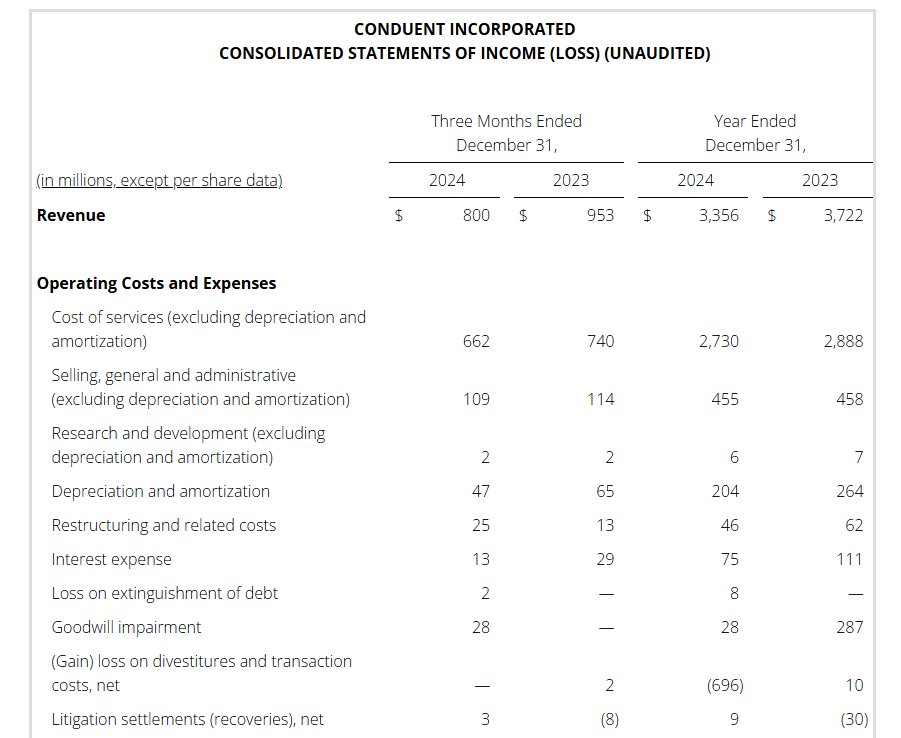

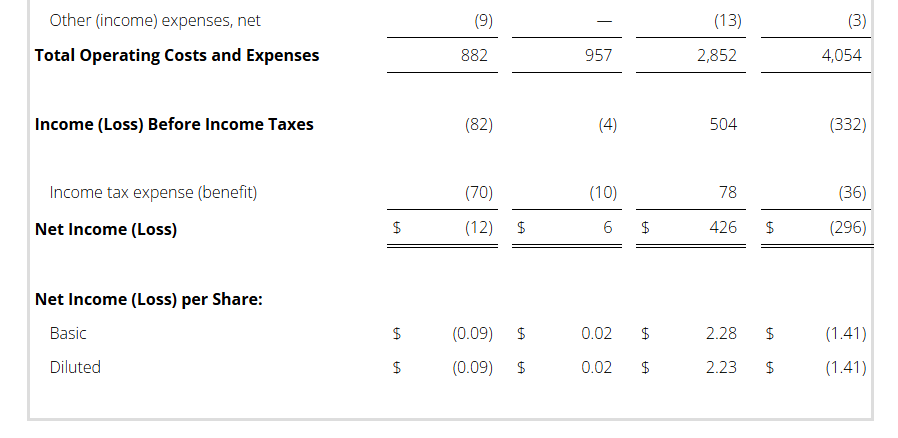

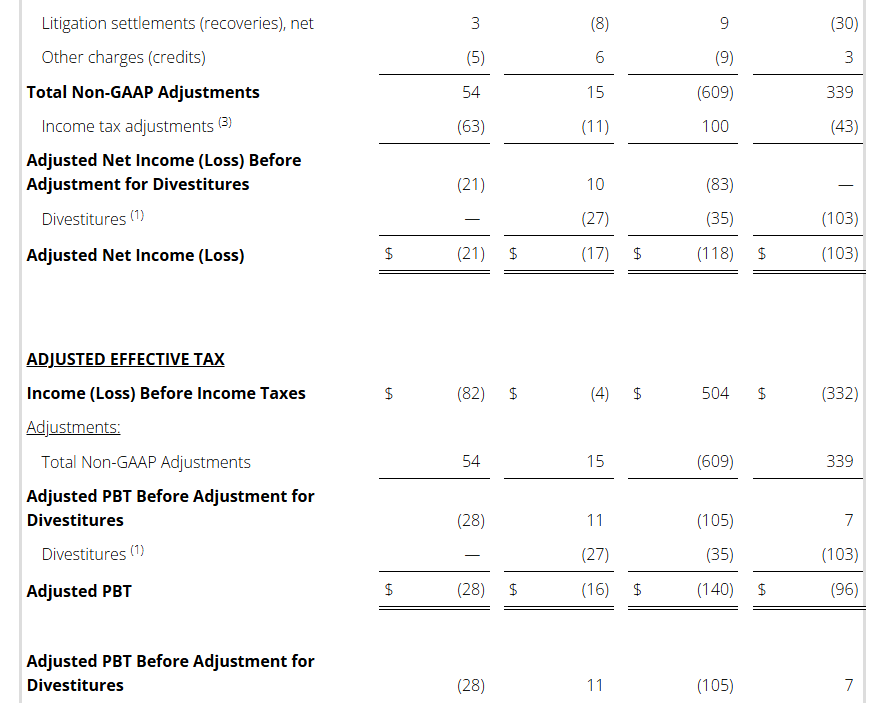

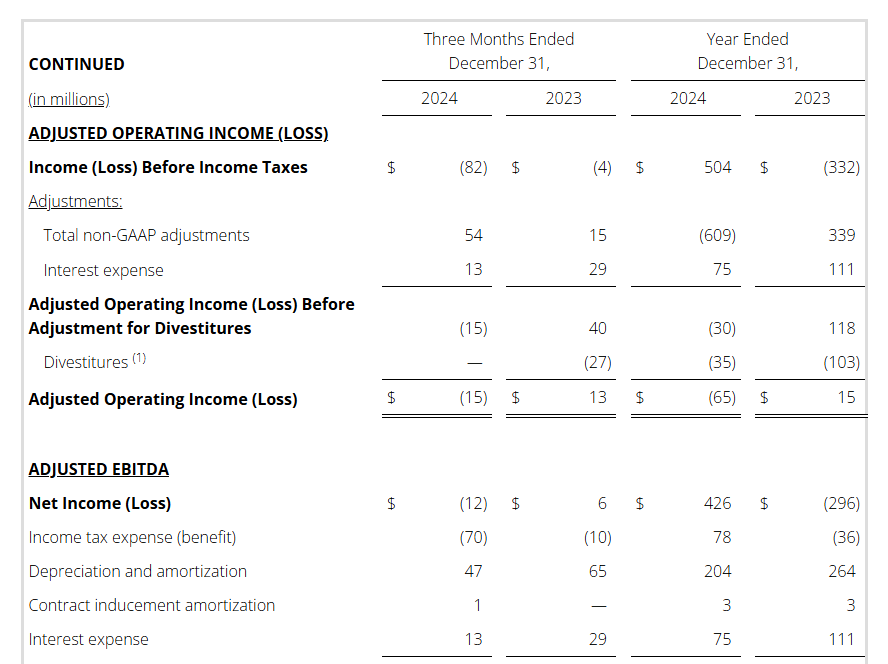

Full year 2024 pre-tax income (loss) was $504 million versus $(332) million in the prior year. This increase is primarily driven by the gain on the sale of the three divested businesses noted above, as well as a goodwill impairment in the prior year.

During 2024 the Company completed its previously approved $75 million share repurchase program and bought back a total of 52 million shares of common stock, including approximately 38 million shares purchased from Carl Icahn and affiliates.

Additional Q4 & Full Year 2024 Performance Highlights

Conduent achieved several milestones in technology-led solutions, operational excellence and culture, including:

Announced several implementations and advanced solutions in Transportation including expanded 3D fare gates, open payment digital wallet fare collection and all-electronic express lane tolling for clients in the US and Europe;

Implemented several digital payment solutions for several states that combat fraud and disburse payments to those in need;

Integrated AI-driven solutions by TALON and Jellyvision’s ALEX with Conduent’s Life@Work Connect Experience Platform to enhance employee benefits decisions;

Collaborated with Microsoft on an initiative across the Conduent portfolio to drive innovation using Microsoft Azure OpenAI Services;

Earned Leader Recognition from:

Information Services Group (ISG) as a U.S. and Europe “Leader” in its 2024 Contact Center – Customer Experience Services Provider Lens™ report; and

NelsonHall’s NEAT Report for Healthcare Payer Operational Transformation; CX Services Transformation – Cost Optimization Focus; and Multi-Process HR Transformation Services for Large Enterprises.

Earned Recognition for Industry Leadership and Culture:

“GovTech Top 100 Company” for the third consecutive year;

Newsweek Top 100 Most Loved Workplaces for third consecutive year;

“Best Place to Work for Disability Inclusion” (Disability Equality Index); and

Forbes’ list of America’s Best Employers for Diversity for the fourth consecutive year.

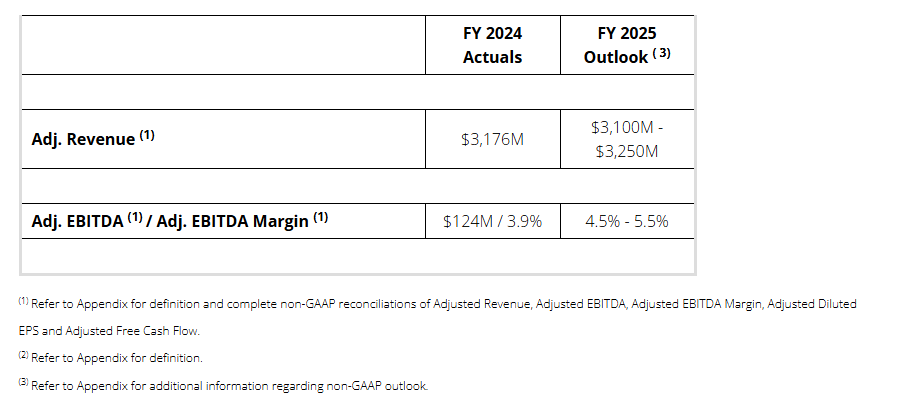

FY 2025 Outlook

Conference Call Management will present the results during a conference call and webcast on February 12, 2025 at 9:00 a.m. ET.

The call will be available by live audio webcast along with the news release and online presentation slides at https://investor.conduent.com/.

The conference call will also be available by calling 877-407-4019 toll-free. If requested, the conference ID for this call is 13750544.

The international dial-in is 1-201-689-8337. The international conference ID is also 13750544.

A recording of the conference call will be available by calling 1-877-660-6853 three hours after the conference call concludes. The replay ID is 13750544.

The telephone recording will be available until February 26, 2025.

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 56,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling approximately 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 13 million tolling transactions every day. Learn more at www.conduent.com.

Non-GAAP Financial Measures We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures. We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, our reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions. Providing such non-GAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures. Refer to the “Non-GAAP Financial Measures” section attached to this release for a discussion of these non-GAAP measures and their reconciliation to the reported U.S. GAAP measures.

Forward-Looking Statements

This press release, any exhibits or attachments to this release, and other public statements we make may contain “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “estimate,” “expect,” “expectations,” “in front of us,” “plan,” “intend,” “will,” “aim,” “should,” “could,” “forecast,” “target,” “may,” “continue to,” “looking to continue,” “endeavor,” “if,” “growing,” “projected,” “potential,” “likely,” “see,” “ahead,” “further,” “going forward,” “on the horizon,” “as we progress,” “going to,” “path from here forward,” “think,” “path to deliver,” “from here,” and similar expressions (including the negative and plural forms of such words and phrases), as they relate to us, are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. All statements other than statements of historical fact included in this press release or any attachment to this press release are forward-looking statements, including, but not limited to, statements regarding our financial results, condition and outlook; changes in our operating results; general market and economic conditions; and our projected financial performance, including all statements made under the section captioned “FY 2025 Outlook” within this release. These statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions, many of which are outside of our control, that could cause actual results to differ materially from those expected or implied by such forward-looking statements contained in this press release, any exhibits to this press release and other public statements we make.

Important factors and uncertainties that could cause our actual results to differ materially from those in our forward-looking statements include, but are not limited to: government appropriations and termination rights contained in our government contracts, the competitiveness of the markets in which we operate and our ability to renew commercial and government contracts, including contracts awarded through competitive bidding processes; our ability to recover capital and other investments in connection with our contracts; our reliance on third-party providers; risk and impact of geopolitical events and increasing geopolitical tensions (such as the war in the Ukraine and conflict in the Middle East), macroeconomic conditions, natural disasters and other factors in a particular country or region on our workforce, customers and vendors; our ability to deliver on our contractual obligations properly and on time; changes in interest in outsourced business process services; claims of infringement of third-party intellectual property rights; our ability to estimate the scope of work or the costs of performance in our contracts; the loss of key senior management and our ability to attract and retain necessary technical personnel and qualified subcontractors; our failure to develop new service offerings and protect our intellectual property rights; our ability to modernize our information technology infrastructure and consolidate data centers; expectations relating to environmental, social and governance considerations; utilization of our stock repurchase program; risks related to our use of artificial intelligence; the failure to comply with laws relating to individually identifiable information and personal health information; the failure to comply with laws relating to processing certain financial transactions, including payment card transactions and debit or credit card transactions; breaches of our information systems or security systems or any service interruptions; our ability to comply with data security standards; developments in various contingent liabilities that are not reflected on our balance sheet, including those arising as a result of being involved in a variety of claims, lawsuits, investigations and proceedings; risks related to recently completed divestitures including the (i) transfer of the Company’s BenefitWallet’s health savings account, medical savings account and flexible spending account portfolio, (ii) the sale of the Company’s Curbside Management and Public Safety Solutions businesses and (iii) the sale of the Company’s Casualty Claims Solutions business, including but not limited to the Company’s ability to realize the benefits anticipated from such transactions, unexpected costs, liabilities or delays in connection with such transactions, and the significant transaction costs associated with such transactions; risk and impact of potential goodwill and other asset impairments; our significant indebtedness and the terms of such indebtedness; our failure to obtain or maintain a satisfactory credit rating and financial performance; our ability to obtain adequate pricing for our services and to improve our cost structure; our ability to collect our receivables, including those for unbilled services; a decline in revenues from, or a loss of, or a reduction in business from or failure of significant clients; fluctuations in our non-recurring revenue; increases in the cost of voice and data services or significant interruptions in such services; our ability to receive dividends or other payments from our subsidiaries; and other factors that are set forth in the “Risk Factors” section, the “Legal Proceedings” section, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section and other sections in our 2024 Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with or furnished to the Securities and Exchange Commission. Any forward-looking statements made by us in this release speak only as of the date on which they are made. We are under no obligation to, and expressly disclaim any obligation to, update or alter our forward-looking statements, whether because of new information, subsequent events or otherwise, except as required by law.

###

Appendix

Definitions

Net ARR Activity Metric (TTM)

Projected Annual Recurring Revenue (ARR) for contracts signed in the prior 12 months, less the annualized impact of any client losses, contractual volume and price changes, and other known impacts for which the company was notified in that same time period, which could positively or negatively impact results. The metric annualizes the net impact to revenue. Timing of revenue impact varies and may not be realized within the forward 12-month timeframe. The metric is for indicative purposes only. This metric excludes non-recurring revenue signings. This metric is not indicative of any specific 12 month timeframe.

New Business Annual Contract Value (ACV): (New Business TCV / contract term) multiplied by 12.

New Business Total Contract Value (TCV): Estimated total future revenues from contracts signed during the period related to new logo, new service line or expansion with existing customers.

TTM: Trailing twelve months.

PBT: Profit before tax.

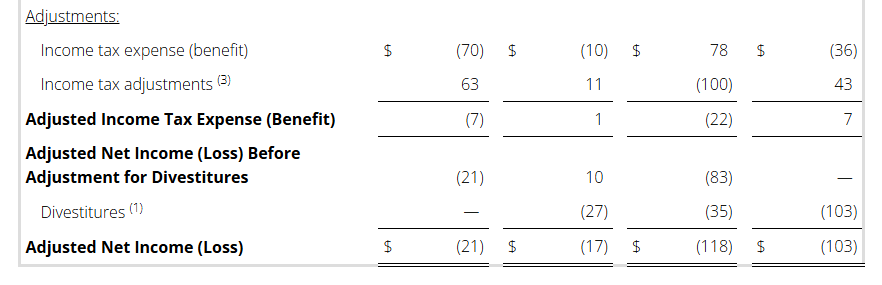

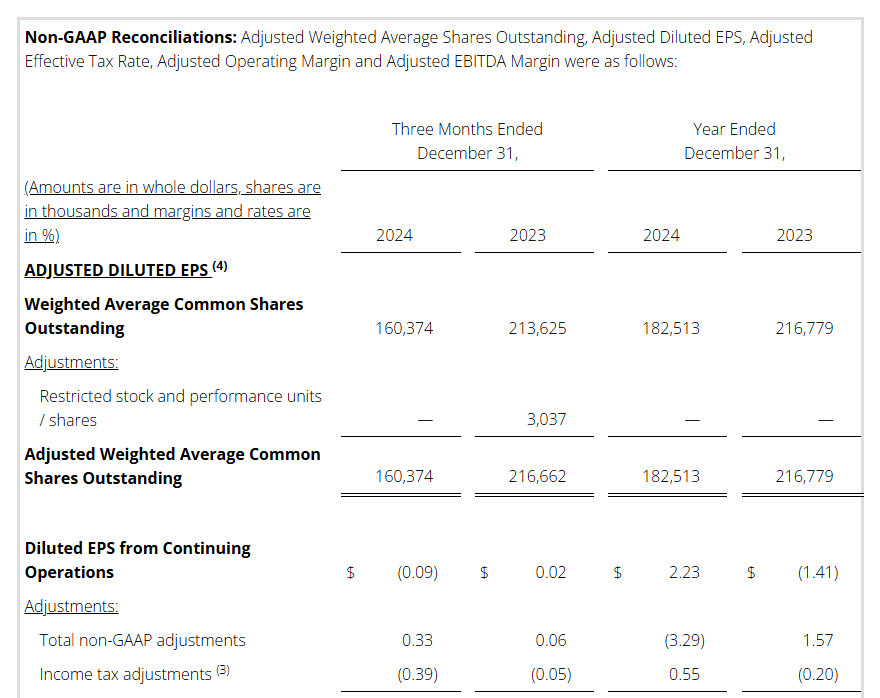

Non-GAAP Financial Measures

We have reported our financial results in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In addition, we have discussed our financial results using non-GAAP measures.

We believe these non-GAAP measures allow investors to better understand the trends in our business and to better understand and compare our results. Accordingly, we believe it is necessary to adjust several reported amounts, determined in accordance with U.S. GAAP, to exclude the effects of certain items as well as their related tax effects. Management believes that these non-GAAP financial measures provide an additional means of analyzing the results of the current period against the corresponding prior period. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, the Company’s reported results prepared in accordance with U.S. GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a substitute for comparable U.S. GAAP measures and should be read only in conjunction with our Consolidated Financial Statements prepared in accordance with U.S. GAAP. Our management regularly uses our non-GAAP financial measures internally to understand, manage and evaluate our business and make operating decisions, and providing such non-GAAP financial measures to investors allows for a further level of transparency as to how management reviews and evaluates our business results and trends. These non-GAAP measures are among the primary factors management uses in planning for and forecasting future periods. Compensation of our executives is based in part on the performance of our business based on certain of these non-GAAP measures.

Management cautions that amounts presented in accordance with Conduent’s definition of non-GAAP financial measures may not be comparable to similar measures disclosed by other companies because not all companies calculate non-GAAP measures in the same manner.

A reconciliation of the following non-GAAP financial measures to the most directly comparable financial measures calculated and presented in accordance with U.S. GAAP are provided below.

These reconciliations also include the income tax effects for our non-GAAP performance measures in total, to the extent applicable. The income tax effects are calculated under the same accounting principles as applied to our reported pre-tax performance measures under Accounting Standards Codification 740, which employs an annual effective tax rate method. The noted income tax effect for our non-GAAP performance measures is effectively the difference in income taxes for reported and adjusted pre-tax income calculated under the annual effective tax rate method. The tax effect of the non-GAAP adjustments was calculated based upon evaluation of the statutory tax treatment and the applicable statutory tax rate in the jurisdictions in which such charges were incurred.

Adjusted Revenue, Adjusted Profit Before Tax, Adjusted Net Income (Loss), Adjusted Diluted Earnings per Share, Adjusted Weighted Average Common Shares Outstanding, and Adjusted Effective Tax Rate

We make adjustments to Revenue, Net Income (Loss) before Income Taxes for the following items, as applicable, to the particular financial measure, for the purpose of calculating Adjusted Revenue, Adjusted Profit Before Tax, Adjusted Net Income (Loss), Adjusted Diluted Earnings per Share, Adjusted Weighted Average Common Shares Outstanding, and Adjusted Effective Tax Rate:

Amortization of acquired intangible assets. The amortization of acquired intangible assets is driven by acquisition activity, which can vary in size, nature and timing as compared to other companies within our industry and from period to period.

Restructuring and related costs. Restructuring and related costs include restructuring and asset impairment charges as well as costs associated with our strategic transformation program.

Goodwill impairment. This represents goodwill impairment charges arising from annual or interim goodwill testing.

(Gain) loss on divestitures and transaction costs, net. Represents (gain) loss on divested businesses and transaction costs.

Litigation settlements (recoveries), net represents settlements or recoveries for various matters subject to litigation.

Loss on extinguishment of debt. This represents write-off related debt issuance costs related to prepayments of debt.

Other charges (credits). This includes Other (income) expenses, net on the Consolidated Statements of Income (loss) and other adjustments.

Divestitures. Revenue and Adjusted EBITDA of divested businesses are excluded.

The Company provides adjusted net income and adjusted EPS financial measures to assist our investors in evaluating our ongoing operating performance for the current reporting period and, where provided, over different reporting periods, by adjusting for certain items which may be recurring or non-recurring and which in our view do not necessarily reflect ongoing performance. We also internally use these measures to assess our operating performance, both absolutely and in comparison to other companies, and in evaluating or making selected compensation decisions.

Management believes that the adjusted effective tax rate, provided as supplemental information, facilitates a comparison by investors of our actual effective tax rate with an adjusted effective tax rate which reflects the impact of the items which are excluded in providing adjusted net income and certain other identified items, and may provide added insight into our underlying business results and how effective tax rates impact our ongoing business.

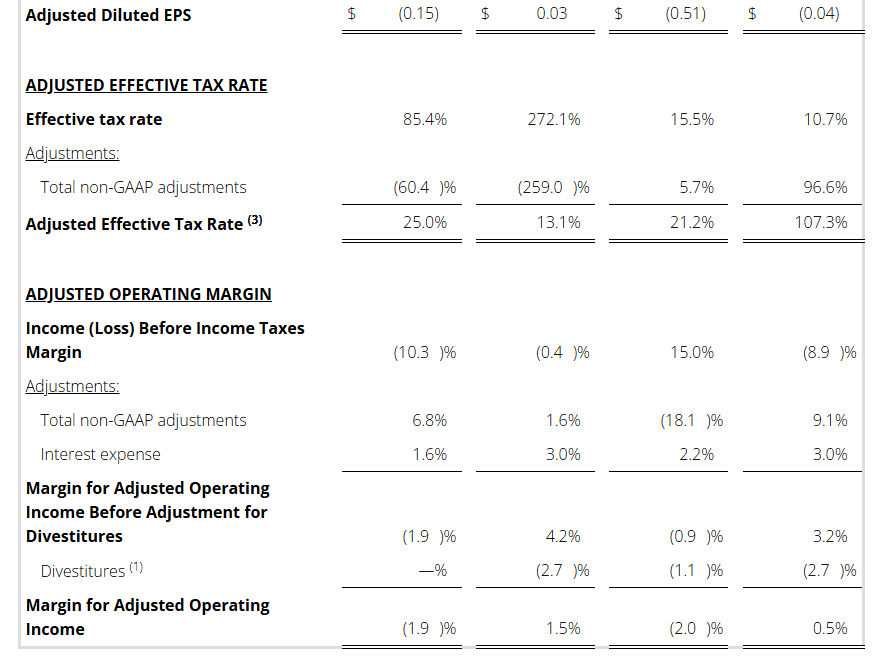

Adjusted Revenue, Adjusted Operating Income and Adjusted Operating Margin

We make adjustments to Revenue, Costs and Expenses and Operating Margin for the following items, as applicable, for the purpose of calculating Adjusted Revenue, Adjusted Operating Income and Adjusted Operating Margin:

Amortization of acquired intangible assets.

Restructuring and related costs.

Interest expense. Interest expense includes interest on long-term debt and amortization of debt issuance costs.

Goodwill impairment.

Loss on extinguishment of debt.

(Gain) loss on divestitures and transaction costs, net.

Litigation settlements (recoveries), net.

Other charges (credits).

Divestitures.

We provide our investors with adjusted revenue, adjusted operating income and adjusted operating margin information, as supplemental information, because we believe it offers added insight, by itself and for comparability between periods, by adjusting for certain non-cash items as well as certain other identified items which we do not believe are indicative of our ongoing business, and may also provide added insight on trends in our ongoing business.

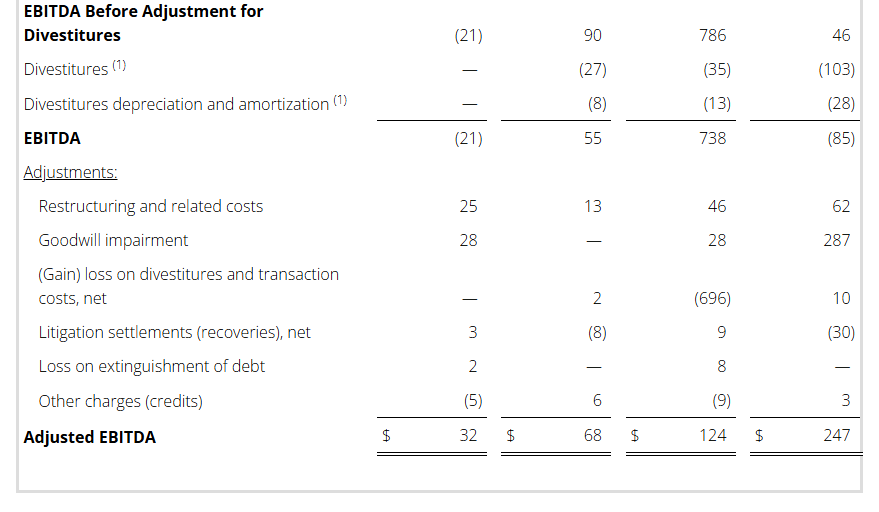

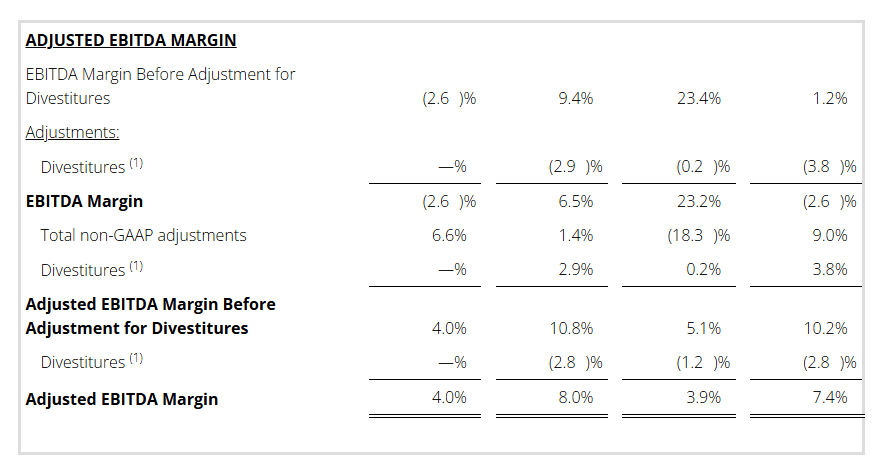

Adjusted EBITDA and EBITDA Margin

We use Adjusted EBITDA and Adjusted EBITDA Margin as an additional way of assessing certain aspects of our operations that, when viewed with the U.S. GAAP results and the accompanying reconciliations to corresponding U.S. GAAP financial measures, provide a more complete understanding of our on-going business. Adjusted EBITDA represents income (loss) before interest, income taxes, depreciation and amortization and contract inducement amortization adjusted for the following items. Adjusted EBITDA Margin is Adjusted EBITDA divided by revenue or adjusted revenue, as applicable.

Restructuring and related costs.

Goodwill impairment.

Loss on extinguishment of debt.

(Gain) loss on divestitures and transaction costs, net.

Litigation settlements (recoveries), net.

Other charges (credits).

Divestitures.

Adjusted EBITDA is not intended to represent cash flows from operations, operating income (loss) or net income (loss) as defined by U.S. GAAP as indicators of operating performance.

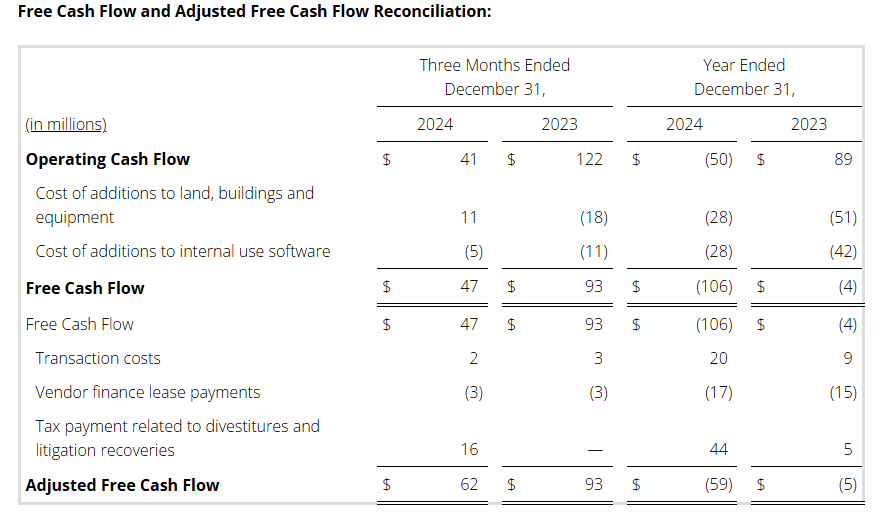

Free Cash Flow

Free Cash Flow is defined as cash flows from operating activities as reported on the consolidated statement of cash flows, less cost of additions to land, buildings and equipment, cost of additions to internal use software, and proceeds from sales of land, buildings and equipment, as applicable. We use the non-GAAP measure of Free Cash Flow as a criterion of liquidity. We use Free Cash Flow as a measure of liquidity to determine amounts we can reinvest in our core businesses, such as amounts available to make acquisitions and invest in land, buildings and equipment and internal use software, after required payments on debt. In order to provide a meaningful basis for comparison, we are providing information with respect to our Free Cash Flow reconciled to cash flow provided by operating activities, which we believe to be the most directly comparable measure under U.S. GAAP.

Adjusted Free Cash Flow

Adjusted Free Cash Flow is defined as Free Cash Flow from above plus adjustments for litigation insurance recoveries, transaction costs, taxes paid on gains from divestitures and litigation recoveries, proceeds from failed sale-leaseback transactions and certain other identified adjustments, as applicable. We use Adjusted Free Cash Flow, in addition to Free Cash Flow, to provide supplemental information to our investors concerning our ability to generate cash from our ongoing operating activities; by excluding these items, we believe we provide useful additional information to our investors to help them further understand our ability to generate cash period-over-period as well as added information on comparability to our competitors. Such as with Free Cash Flow information, as so adjusted, it is specifically not intended to provide amounts available for discretionary spending. We have added certain adjustments to account for items which we do not believe reflect our core business or operating performance, and we computed all periods with such adjusted costs.

Revenue at Constant Currency

To better understand trends in our business, we believe that it is helpful to adjust revenue to exclude the impact of changes in the translation of foreign currencies into U.S. Dollars. We refer to this adjusted revenue as “constant currency.” Currency impact is determined as the difference between actual growth rates and constant currency growth rates. This currency impact is calculated by translating the current period activity in local currency using the comparable prior-year period’s currency translation rate.

Non-GAAP Outlook

In providing the Full Year 2025 outlook for Adjusted EBITDA and Adjusted EBITDA Margin we exclude certain items which are otherwise included in determining the comparable U.S. GAAP financial measure. A description of the adjustments which historically have been applicable in determining Adjusted EBITDA and Adjusted EBITDA Margin is reflected in the table below. We are providing such outlook only on a non-GAAP basis because the company is unable without unreasonable efforts to predict with reasonable certainty the totality or ultimate outcome or occurrence of these adjustments for the forward-looking period, which can be dependent on future events that may not be reliably predicted. Based on past reported results, where one or more of these items have been applicable, such excluded items could be material, individually or in the aggregate, to reported results. We have provided an outlook for Adjusted Revenue only on a non-GAAP basis using foreign currency translation rates as of fiscal year end due to the inability to, without unreasonable efforts, accurately predict foreign currency impact on revenues. Full Year 2025 Outlook for Adjusted Free Cash Flow is provided as a factor of expected Adjusted EBITDA, and such outlook is only available on a non-GAAP basis for the reasons described above. For the same reason, we are unable to provide a GAAP expected adjusted tax rate, which adjusts for our non-GAAP adjustments. Non-GAAP Reconciliations: Adjusted Revenue, Revenue at Constant Currency, Adjusted Net Income (Loss), Adjusted Effective Tax, Adjusted Operating Income (Loss) and Adjusted EBITDA were as follows (see footnotes on last page of Non-GAAP reconciliations):

Key Points: – The Consumer Price Index (CPI) increased 3% year-over-year in January, exceeding expectations and accelerating from December’s 2.9%. – Rising energy costs and food prices, particularly eggs, contributed to the largest monthly headline increase since August 2023. – The Federal Reserve faces challenges in determining interest rate cuts, as inflation remains above its 2% target.

Newly released inflation data for January revealed that consumer prices rose at a faster-than-expected pace, complicating the Federal Reserve’s path forward. The Consumer Price Index (CPI) increased by 3% over the previous year, ticking up from December’s 2.9% annual gain. On a monthly basis, prices climbed 0.5%, marking the largest monthly increase since August 2023 and outpacing economists’ expectations of 0.3%.

Energy costs and persistent food inflation played a significant role in driving the index higher. Egg prices, in particular, surged by a staggering 15.2% in January—the largest monthly jump since June 2015—contributing to a 53% annual increase. Meanwhile, core inflation, which excludes volatile food and energy prices, rose 0.4% month-over-month, reversing December’s easing trend and posting the biggest monthly rise since April 2023.

The stickiness in core inflation remains a concern for policymakers. Shelter and service-related costs, including insurance and medical care, continue to pressure consumers despite some signs of moderation. Shelter inflation increased 4.4% annually, the smallest 12-month gain in three years. Rental price growth also showed signs of cooling, marking its slowest annual increase since early 2022. However, used car prices saw another sharp uptick, rising 2.2% in January after consecutive increases in the prior three months, further fueling inflationary pressures.

Federal Reserve officials have maintained that they will closely monitor inflation data before making any adjustments to interest rates. The central bank’s 2% target remains elusive, and the higher-than-expected January data adds another layer of complexity to future rate decisions. Economists caution that while seasonal factors and one-time influences may have played a role in January’s inflation spike, the persistence of elevated core inflation suggests that rate cuts could be delayed.

Claudia Sahm, chief economist at New Century Advisors and former Federal Reserve economist, described the report as a setback. “This is not a good print,” she said, adding that January’s inflation surprises have been a recurring theme in recent years. She noted that while this does not derail the broader disinflationary trend, it does reinforce the need for patience in assessing future rate adjustments.

The economic outlook is further complicated by recent trade policies. President Donald Trump’s imposition of 25% tariffs on steel and aluminum imports, along with upcoming tariffs on Mexico, Canada, and China, raises concerns about potential cost pressures on goods and supply chains. Market reactions were swift, with traders adjusting expectations for the Fed’s first rate cut and stocks selling off in response.

While the Federal Reserve is unlikely to react to a single month’s data, the latest inflation report suggests that policymakers will need to see consistent progress before considering rate reductions. Analysts now anticipate that any potential rate cuts may be pushed into the second half of the year, dependent on future inflation trends.

Completed Phase 2 enrollment with randomization of 51 subjects into treatment and control arms

Phase 1/2 study (N=60) demonstrated favorable safety and tolerability profile with no serious adverse events related to OCU410, including no cases of ischemic optic neuropathy, vasculitis, intraocular inflammation, endophthalmitis or choroidal neovascularization

Subjects showed considerably slower lesion growth (44%) from baseline in treated eyes versus untreated fellow eyes at 9 months in follow-up data from the Phase 1 study

Clinically meaningful 2-line (10-letter) improvement in visual function (LLVA) in treated eyes compared to untreated eyes was noted in the Phase 1 portion of the trial

Preservation of retinal tissue at 9 months around GA lesions of treated eyes with a single injection of OCU410 in Phase 1 compared favorably to published data on a leading FDA-approved complement inhibitor given monthly or every other month at the same time points

MALVERN, Pa., Feb. 12, 2025 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced that dosing is complete, ahead of schedule in the Phase 2 portion of the Phase 1/2 ArMaDa clinical trial for OCU410—a novel multifunctional modifier gene therapy candidate being developed for geographic atrophy (GA), an advanced stage of dry age-related macular degeneration (dAMD). Age-related macular degeneration (AMD) affects 1 in 8 people 60 years and older. The global prevalence of dAMD is 266 million worldwide and by 2050 more than 5 million Americans may suffer from this incurable condition. Today, GA – the later stage of dAMD – affects approximately 2-3 million people in the United States (U.S.) and Europe.

There are limited options for patients with dAMD in the U.S. and current therapies involve frequent (monthly or every other month) injections and have unwanted side effects that can affect vision. These therapies are not approved in Europe, leaving approximately 2 million patients with no therapeutic option.

“Dosing completion is a major accomplishment for our OCU410 program,” said Dr. Shankar Musunuri, Chairman, CEO, and Co-founder of Ocugen. “Based on the multifunctional effect of our modifier gene therapy, the profound unmet medical need, limited treatment options, and the fact that it is designed as a one and done treatment, we believe OCU410 can be a potential blockbuster therapy and the gold standard for treating GA worldwide. The data from this trial will help us design a future pivotal Phase 3 study planned for 2026 and enable our commercial strategy for Biologics License Application (BLA) and Marketing Authorization Application (MAA) filings as soon as 2028.”

“The preliminary efficacy and safety data from the Phase 1/2 study are highly encouraging, demonstrating the potential of OCU410 to improve both structural and functional outcomes,” said Lejla Vajzovic, MD, FASRS, Director of the Duke Surgical Vitreoretinal Fellowship Program and Professor of Ophthalmology, Pediatrics and Biomedical Engineering with Tenure at Duke University Eye Center. “I look forward to the Phase 2 results and believe a one-time gene therapy could reshape the treatment landscape, offering a transformative option for patients.”

GA is a multifactorial disease with a complex etiology that involves genetic and environmental factors. The current treatment options for GA in the U.S. are limited to those targeting a single mechanism—the complement pathway—requiring frequent intravitreal injections, either monthly or every other month. By contrast, OCU410 is a multifunctional modifier gene therapy, which targets multiple pathways associated with GA.

“Given the safety concerns associated with currently approved GA treatments, the encouraging safety and tolerability profile of OCU410 offers a promising treatment option,” said Dr. Huma Qamar, Chief Medical Officer of Ocugen. “With Phase 2 enrollment now complete, OCU410 has the potential to be a one-time treatment, reducing the burden of frequent injections, improving patient compliance, and ultimately enhancing quality of life.”

In the Phase 2 study, the safety and efficacy of OCU410 in patients with GA secondary to dAMD will be assessed. Fifty-one (51) patients were randomized 1:1:1 into either of two treatment groups (medium or high dose) or a control group. In the treatment groups, subjects received a single subretinal 200-µL administration of 5 x 1010 vector genomes (vg)/mL (medium dose) or 1.5 x 1011 vg/mL (high dose), while the control group remained untreated.

The ArMaDa clinical trial for OCU410 is being performed at 14 leading retinal surgery centers across the U.S.

About the Phase 1/2 ArMaDa clinical trial The ArMaDa Phase 1/2 clinical trial will assess the safety of unilateral subretinal administration of OCU410 in subjects with GA and will be conducted in two phases. Phase 1 is a multicenter, open label, dose-escalation study consisting of three dose levels [low dose (2.5×1010 vg/mL), medium dose (5×1010 vg/mL), and high dose (1.5 ×1011 vg/mL)]. Phase 2 is a randomized, outcome assessor-blinded, dose-expansion study in which subjects were randomized in a 1:1:1 ratio to either the medium dose or high dose OCU410 treatment groups or to an untreated control group.

AboutdAMD and GA dAMD affects approximately 10 million Americans and more than 266 million people worldwide. It is characterized by the thinning of the macula, the portion of the retina responsible for clear vision in one’s direct line of sight. dAMD involves the slow deterioration of the retina with submacular drusen (small white or yellow dots on the retina), atrophy, loss of macular function, and central vision impairment. dAMD accounts for 85-90% of all AMD cases.

AboutOCU410 OCU410 utilizes an adeno-associated virus (AAV) platform for the retinal delivery of the RORA (ROR Related Orphan Receptor A) gene. The RORA protein plays an important role in lipid metabolism, reducing lipofuscin deposits and oxidative stress, and demonstrates an anti-inflammatory role as well as inhibiting the complement system in both in vitro and in vivo (animal model) studies. These results demonstrate the ability of OCU410 to target multiple pathways linked with dAMD pathophysiology. Ocugen is developing AAV-RORA as a one-time gene therapy for the treatment of GA.

AboutOcugen,Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patients’ lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements Thispressreleasecontainsforward-lookingstatementswithinthemeaningofThePrivateSecuritiesLitigationReformActof1995,including,butnot limited to, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines,whicharesubjecttorisksanduncertainties.Wemay,insomecases,usetermssuchas “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including,butnotlimitedto,therisksthatpreliminary,interimandtop-lineclinicaltrialresultsmaynotbeindicativeof,andmaydifferfrom,finalclinical data;the ability of OCU410 to perform in humans in a manner consistent with nonclinical, preclinical or previous clinical study data;thatunfavorablenewclinicaltrialdatamayemergeinongoingclinicaltrialsorthroughfurtheranalysesofexistingclinicaltrialdata;thatearlier non-clinicalandclinicaldataandtestingofmaynotbepredictiveoftheresultsorsuccessoflaterclinicaltrials;andthatthatclinicaltrialdataare subject to differing interpretations and assessments, including by regulatory authorities.Theseandotherrisksanduncertaintiesaremorefully describedinourperiodicfilingswiththeSecuritiesandExchangeCommission(SEC),includingtheriskfactorsdescribedinthesectionentitled“Risk Factors”inthequarterlyandannualreportsthatwefilewiththeSEC.Anyforward-lookingstatementsthatwemakeinthispressreleasespeakonlyas ofthedateofthispressrelease.Exceptasrequiredbylaw,weassumenoobligationtoupdateforward-lookingstatementscontainedinthispress release whether as a result of new information, future events, or otherwise, after the date of this press release.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a global leader in providing augmented reality (“AR”) and artificial intelligence (“AI”) Software-as-a-Service (“SaaS”) solutions to beauty and fashion industries, today announced that it plans to release its financial results for the full year of 2024 before U.S. markets open on Wednesday, February 26, 2025 and to hold a conference call at 7:30 p.m. Eastern Time the same day on February 26, 2025 (or 8:30 a.m. Taipei Standard Time the following day on February 27, 2025).

The Company’s management will discuss the financial results and latest developments during the conference call. For participants who wish to join the call, please complete online registration using the link provided below in advance of the conference call. Upon registration, each participant will receive a participant dial-in number and a unique access PIN, which can be used to join the conference call.

A live and archived webcast of the conference call will also be available at the Company’s investor relations website at https://ir.perfectcorp.com.

About Perfect Corp.

Perfect Corp. (NYSE: PERF) leverages ‘Beautiful AI’ innovations to make our world more beautiful. As a pioneer and leader in the space, Perfect Corp. works with over 650 partners around the globe to empower brands to embrace the digital-first world by transforming shopping journeys through digital tech innovations. Perfect Corp.’s suite of enterprise solutions delivers synergistic, technology-driven experiences that facilitate sustainable, ultra-personalized, and engaging shopping journeys through hyper-realistic virtual try-ons, AI-powered skin analyses, personalized product recommendation tools and many more Beautiful AI innovations. For more information, visit https://ir.perfectcorp.com/.

HOUSTON, Feb. 11, 2025 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (NASDAQ: GLDD) today announced that it will release the financial results for its three and twelve months ended December 31, 2024 on Tuesday, February 18, 2025 at 7:00 a.m. C.S.T. A conference call with the Company will be held the same day at 9:00 a.m. C.S.T.

Investors and analysts are encouraged to pre-register for the conference call by using the link below. Participants who pre-register will be given a unique PIN to gain immediate access to the call. Pre-registration may be completed at any time up to the call start time.

The live call and replay can also be heard at https://edge.media-server.com/mmc/p/oqt4ireo or on the Company’s website, www.gldd.com, under Events on the Investor Relations page. A copy of the press release will be available on the Company’s website.

The Company Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the developing offshore energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 135-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Distribution. Yesterday, MustGrow announced the signing of a five-year exclusive distribution agreement with Adjuvants Plus Inc., in which MustGrow will distribute Adjuvants’ product line across Canada through NexusBioAg. In addition, MustGrow has a First Right of Refusal for the distribution of Adjuvants’ product line in the U.S. market.

Complementing Products. Four key products are being introduced by Adjuvants in the agreement, with a particular focus on EndoFine and EndoGuard. Adjuvants’ patented Clonostachys rosea, a fungus that provides plant health and protection benefits, is in both products, offering an abundance of advantages for various crops in North America, such as corn, soybeans, pulses, canola, and fruits and vegetables. In our view, products such as EndoFine and EndoGuard complement MustGrow’s product line, as both lines target similar crops while offering health and protection benefits.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Opportunity, Opportunity, Opportunity. With the change in Administration and new Congress, CoreCivic is anticipating significant growth opportunities, possibly the most significant growth in the Company’s history, over the next several years. We believe the Company is exceptionally well positioned operationally and financially to meet this expected sharp increase in demand for its services.

Potential. Management has put forth a proposal to ICE for 28,000 beds. If accepted, such a proposal could be worth about $1.5 billion in revenue. Just adding in approximately 15,000 beds from existing idle facilities and the South Texas facility could add $750-$800 million of revenue and some $200-$275 million of adjusted EBITDA. Current proposals by the Administration and Congress support such growth, although funding will be key.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – AbbVie and Xilio Therapeutics announce a partnership to develop innovative tumor-activated immunotherapies, including masked T-cell engagers. – Xilio will receive $52 million upfront and is eligible for up to $2.1 billion in milestone payments and royalties. – The collaboration aims to enhance the effectiveness of immunotherapy while minimizing systemic side effects.

AbbVie and Xilio Therapeutics have entered a strategic collaboration to advance next-generation tumor-activated immunotherapies, a move that could significantly impact the oncology space. The partnership will focus on developing masked T-cell engagers (TCEs), a cutting-edge approach designed to precisely target tumors while reducing the systemic toxicity often associated with immunotherapies.

Under the terms of the agreement, Xilio will receive an upfront payment of $52 million, with the potential to earn up to $2.1 billion in milestone payments and royalties if the collaboration yields successful drug candidates. This deal highlights the growing interest in tumor-selective therapies as biopharmaceutical companies seek to refine cancer treatments for better efficacy and safety.

Immunotherapy has revolutionized cancer treatment over the past decade, with checkpoint inhibitors and CAR-T therapies offering promising results. However, many of these treatments come with serious side effects, such as cytokine release syndrome and immune-related toxicities, which can limit their widespread use. Tumor-activated therapies, like those being developed through the AbbVie-Xilio collaboration, aim to overcome these challenges by ensuring immune system activation occurs predominantly at the tumor site rather than throughout the body.

This strategy aligns with a broader industry trend where major pharmaceutical companies are investing heavily in precision oncology. Companies such as Bristol Myers Squibb, Merck, and Roche are also exploring targeted immune therapies, with some already advancing their own masked TCE platforms.

AbbVie’s decision to partner with Xilio follows similar collaborations between biotech startups and large pharmaceutical firms. Smaller biotech companies often bring innovative drug discovery capabilities, while established players like AbbVie provide the resources and expertise needed to navigate clinical development and regulatory approval.

The move also positions AbbVie competitively in the immuno-oncology space, where it faces increasing competition from global drugmakers. The company has been expanding its oncology pipeline following the success of Imbruvica and Venclexta, and this partnership could strengthen its position in the next generation of cancer therapeutics.

Meanwhile, Xilio Therapeutics, a biotech firm specializing in tumor-selective treatments, stands to gain significant financial backing and research support through this agreement. Its proprietary technology platform, which develops highly potent, tumor-activated biologics, has the potential to redefine immunotherapy approaches for solid tumors.

With oncology continuing to be one of the most lucrative and rapidly evolving fields in biotech, tumor-activated immunotherapies are poised to become a major focus of drug development. The potential to minimize toxicity while enhancing efficacy makes these therapies particularly appealing for both patients and healthcare providers.

If successful, the AbbVie-Xilio collaboration could lead to groundbreaking advancements in cancer treatment, opening doors for future partnerships and expanding the role of tumor-targeted biologics in oncology.

Key Points: – Novartis has agreed to acquire Anthos Therapeutics for up to $3.1 billion, expanding its presence in the cardiovascular space. – Anthos’ lead drug candidate, abelacimab, has demonstrated significant potential in reducing bleeding risks compared to current anticoagulants. – The acquisition highlights the success of Blackstone Life Sciences’ investment strategy in building and scaling innovative biopharmaceutical companies.

Novartis has entered into a definitive agreement to acquire Anthos Therapeutics, a clinical-stage biopharmaceutical company specializing in innovative therapies for cardiometabolic diseases, for up to $3.1 billion. The deal, announced by Blackstone Life Sciences and Anthos, represents a major step forward in the development of abelacimab, a next-generation Factor XI inhibitor designed to prevent strokes and blood clots with superior safety benefits.

Anthos was founded in 2019 as a collaboration between Blackstone Life Sciences and Novartis, securing exclusive global rights from Novartis to develop, manufacture, and commercialize abelacimab. The acquisition reflects Novartis’ confidence in abelacimab’s potential to become a leader in the growing class of Factor XI anticoagulants, which aim to reduce the risk of major bleeding while maintaining strong stroke prevention efficacy.

“Abelacimab has the potential to be an important treatment option for the millions of patients globally with atrial fibrillation at high risk of stroke, and we could not have more conviction in the potential of this asset,” said Bill Meury, Chief Executive Officer of Anthos. “With its deep roots in the cardiovascular space, Novartis is especially well positioned to advance abelacimab’s clinical development and bring this innovative product to healthcare providers and patients.”

The drug has already demonstrated promising results in the AZALEA-TIMI 71 trial, where abelacimab showed a 62% reduction in major bleeding or clinically relevant non-major bleeding compared to rivaroxaban (Xarelto), a 67% reduction in major bleeding, and an 89% reduction in gastrointestinal bleeding. These impressive findings prompted the Independent Data Monitoring Committee to discontinue the study early due to clear clinical benefits. The results were recently published in the New England Journal of Medicine.

Anthos is currently conducting three phase 3 clinical trials for abelacimab: LILAC-TIMI 76 for patients with atrial fibrillation at high risk of stroke or systemic embolism, and ASTER and MAGNOLIA for patients with cancer-associated thrombosis. Data from these trials are expected in the second half of 2026, and Novartis is expected to continue these efforts to bring abelacimab to market.

Blackstone Life Sciences has played a crucial role in Anthos’ growth, investing in its development, assembling a world-class team, and designing the clinical plan. “This transaction is an affirmation of Blackstone Life Sciences’ ownership investment strategy, where we seek to find innovative products and build companies around them to meet unmet patient needs,” said Dr. Nicholas Galakatos, Global Head of Blackstone Life Sciences.

The acquisition deal includes an upfront payment of $925 million, with additional payments contingent on meeting regulatory and commercial milestones. The transaction is expected to close in the first half of 2025, pending regulatory approvals.

Conni will be integrated into multiple Conduent platforms to boost clients’ productivity, enhance quality, and elevate customer experience

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global leader in technology-driven business solutions and services, launches Conni, an innovative GenAI virtual assistant developed as part of the company’s AI initiative. Leveraging Microsoft Azure OpenAI Service, Conni is designed to enhance the quality of results and improve customer experience across Conduent platforms for companies and government agencies.

“We will continue to embed AI and generative AI within our solutions to drive functionality. New features like Conni build on Conduent’s strategy of integrating advanced technologies, such as automation, machine learning, and digitalization to drive better outcomes for our clients,” said Cliff Skelton, President and Chief Executive Officer at Conduent. “In our Human Capital Solutions business, Conni is deployed to help employees navigate their benefits. By enhancing the employee experience, Conni can drive improved satisfaction and help reduce HR-related inquiries.”

The first implementation of Conni is in Conduent’s Life@Work® Connect Experience Platform, a secure closed system, centralized portal for health, wealth, and wellness employee benefits. Life@Work Connect, with its suite of advanced AI-driven features like JellyVision and TALON, consolidates data from various sources, offering interactive content, educational resources and guided recommendations to help employees manage their benefits with a personalized, intelligent experience.

With Conni in Life@Work Connect, employees can:

Use natural, everyday language, avoiding the technical jargon.

Get fast, accurate personalized answers to specific questions about their health and wealth benefits and supplemental benefits.

Easily navigate to resources and transactions for life events, health savings accounts, flexible savings accounts, and other benefits.

Access personalized data and employer program details to make informed decisions.

Use information from all resources on the Life@Work Connect Experience Platform.

Seamlessly transition to live customer support when needed.

DeeAnna Warrington, Principal Research Analyst at NelsonHall and a member of its HR Talent Transformation practice said, “By incorporating generative AI into its client offerings and internal operations, Conduent continues its tradition of delivering advanced technologies and solutions that boost client efficiency, reduce costs, enhance customer experiences, and optimize business processes.”

As an example of how Conni works, in a use case such as an injury requiring physical therapy, Conni can answer questions like, “Where is the best place for physical therapy near me?” and “How much money is in my health savings account to pay for treatment?” Conni uses the employee-specific coverage and elections along with the information available through the health plan to guide the employee and provide fast answers.

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 55,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $100 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com.

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

Brings Over 30 Years of Experience Across World Leading Lighting and Retail Brands

MIAMI, Feb. 11, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a “SKYX Technologies”), a highly disruptive smart platform technology company with over 97 issued and pending patents in the U.S. and globally, and over 60 lighting and home décor websites with a mission to make homes and buildings become smart, safe, and advanced as the new standard announced today that Greg St. John, former head of Home Depot’s indoor lighting category and former CEO of world leading lighting companies such as Eglo, and Cordelia Lighting, has joined SKYX as President of Lighting Fans and Smart Products.

In his new position, St. John will lead SKYX’s growing penetration in lighting, fans, and smart home products, expanding the company’s presence in major retail channels, homebuilders, hotels, and commercial projects. He will also play a pivotal role in strategic collaborations with industry leaders such as Home Depot, and Wayfair among other expected collaborations.

With more than 30 years of experience, St. John has held executive leadership roles in major U.S. and global lighting brands, overseeing product development, sales, and marketing. His deep expertise in merchandising, sourcing, and smart lighting solutions makes him an ideal fit to drive SKYX’s growth and product expansion initiatives.

Rani Kohen, Founder, Inventor and Executive Chairman of SKYX said, “I am very happy to have Greg joining us as he brings vast experience and industry knowledge. His track record with leading companies such as Home Depot among other global lighting brands aligns perfectly with our vision to revolutionize smart, safe living solutions and the lighting industry. “

Greg St. John added, “I am truly excited to join Rani and the SKYX team at such a pivotal time. The company’s plug & play advanced and smart platform technologies are game-changing, and I strongly believe they will set a new standard for lighting, fans, and smart products across homes, buildings, hotels, and commercial spaces. I look forward to leveraging my experience to help drive SKYX’s innovation and expansion in key markets.”

SKYX continues to expand its market presence through product deployments, industry collaborations, and strategic initiatives. The company remains focused on scaling operations and integrating its solutions across key industry sectors.

St. John’s appointment reinforces SKYX’s commitment to advancing lighting, smart home and building technologies while making safety, efficiency, and innovation the new industry standard.

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) (the “Company”), a leading distributor of Medicare insurance policies and owner of a rapidly-growing healthcare services platform, today announced that the Company signed a $350 million strategic investment from funds managed by Bain Capital, Morgan Stanley Private Credit, and Newlight Partners.

The transaction positions the Company to continue growing its healthcare services business, deepening its relationship with carrier partners and providing choice and value for consumers. This investment will allow the Company to recapitalize its balance sheet, to lower its annual cash debt service, and to provide liquidity and increase operating flexibility to fund growth initiatives. The Company’s successful renegotiation of its Senior Secured Credit Facility provides a lower interest rate on the remaining balance.

This investment will accelerate the Company’s effort to optimize its capital structure as it continues to explore accretive, strategic solutions with its insurance carrier partners and to grow its rapidly expanding healthcare services business.

Additionally, SelectQuote is appointing Chris Wolfe of Bain Capital and Srdjan Vukovic of Newlight Partners to the Board of Directors, each bringing over 20 years of investing and healthcare sector experience to the Company. SelectQuote anticipates Mr. Wolfe and Mr. Vukovic will join the Board upon the closing of the transaction, expected to be on February 28, 2025.

SelectQuote CEO Tim Danker commented, “This strategic investment provides the financing we need to capitalize on the robust growth opportunities we foresee in both the senior health insurance and healthcare services marketplaces. While we have more work to do, this deal, on the heels of our 2024 receivables securitization, marks the second meaningful milestone toward our ultimate goal of refinancing the business and significantly deleveraging the balance sheet.”

Mr. Danker continued, “We look forward to benefitting from Chris’s and Srdjan’s valuable growth-oriented healthcare expertise to help augment the Company’s mission to drive long-term value creation.”

Mr. Wolfe is a Managing Director at Bain Capital Insurance, the dedicated insurance investing unit of Bain Capital. Previously, he was a partner at Capital Z Partners and a principal in a series of special purpose acquisition vehicles focused on health insurance and services. Mr. Wolfe has more than 20 years of experience in healthcare and insurance private equity investing.

“SelectQuote pioneered the way consumers approach shopping for insurance by removing barriers and introducing transparency and choice,” added Mr. Wolfe. “I am excited to partner with my fellow board members and the Company’s management team to drive continued growth of its robust insurance sales and healthcare services solutions, which play a crucial role in safeguarding and enhancing the financial well-being and health of its customers.”

Mr. Vukovic is a Partner at Newlight Partners, where he focuses on investments in the healthcare industry. Representative investments include Oak Street Health (acquired by CVS Health) and Zing Health. He has over 20 years of private equity investing experience.

Ashwin Krishnan, Managing Director and Co-Head of North America Private Credit at Morgan Stanley Investment Management stated, “We are pleased to partner with SelectQuote and lead this financing alongside our partners Bain Capital and Newlight. We believe this investment, along with the Company’s recent operating momentum, sets the business up for continued long-term success.”

Jefferies served as Exclusive Financial Advisor to SelectQuote in the transaction. Wachtell, Lipton, Rosen & Katz served as legal advisor to SelectQuote.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; potential litigation and other legal proceedings or inquiries; our existing and future indebtedness; our ability to maintain compliance with our debt covenants; access to additional capital; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in the most recent Annual Report on Form 10-K (the “Annual Report”) and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.