Image: Rendering of folate receptors on a cancer cell

Understanding ImmunoGen’s Great Performance, and Related Stocks

Discovering a company developing a novel and more effective mechanism or method of doing something, and then investing in shares, is one reason investors pay attention to small-cap stocks. Innovations that improve results of any kind are valuable and usually rewarded. Nowhere is this more true than in biotech or biopharma stocks. After all, better treatments for frightening diseases will always be in demand. However, the big difference between the biotech industry and say, computer technology, is the approval process. FDA requirements are many and approval is slow and uncertain – overall, it’s a high bar to overcome.

Is it Worth it for Investors?

Over the past two days, ImmunoGen (IMGN:Nasdaq) a U.S. based clinical-stage biotech company, has had the kind of moonshot trajectory that investors dream about. The company reported promising topline phase III data and overall survival benefits in folate receptor alpha (FRα)-positive platinum-resistant ovarian cancer patients. Immunogen plans to submit the drug for full approval in the U.S. and Europe. The company’s therapy is a is a first-in-class ADC comprising folate receptor alpha-binding antibody. The stock during the first four days of this week is up over 145%. The reason for the sudden moonshot is the company announced that it expects full FDA approval of one of its ADC candidates (Elahere). ADC, or antibody-drug conjugates, are a very targeted way to treat some solid tumor cancers, and seem to represent the “more effective mechanisms or method of doing something” mentioned above as sought after by small-cap investors.

Excitement Over ADC

An antibody-drug conjugate consists of an antibody that targets a specific antigen or receptor on cancer cells, it carries with it an impactful anticancer drug. The antibody which is linked to a toxin such as a chemotherapy drug, is found by folate receptors on the cancer cells; they will bind with the receptors on the cancer cells, the toxic payload is then delivered to the cells, which internalize it. Once in the cancer cell, the toxin is released. This therapy is designed to result in the selective killing of cancer cells while minimizing damage to healthy cells. ADCs have continued to show promising results in treating various types of cancer and are an active area of research by a few publicly traded small-cap biotechs developing alternatives in oncology.

Stock Market Behavior

As with other industries, the stocks of the peer group will often respond to news of the other. This was the case this week for the subgroup of stocks that are in various stages of researching ADC therapies against cancer.

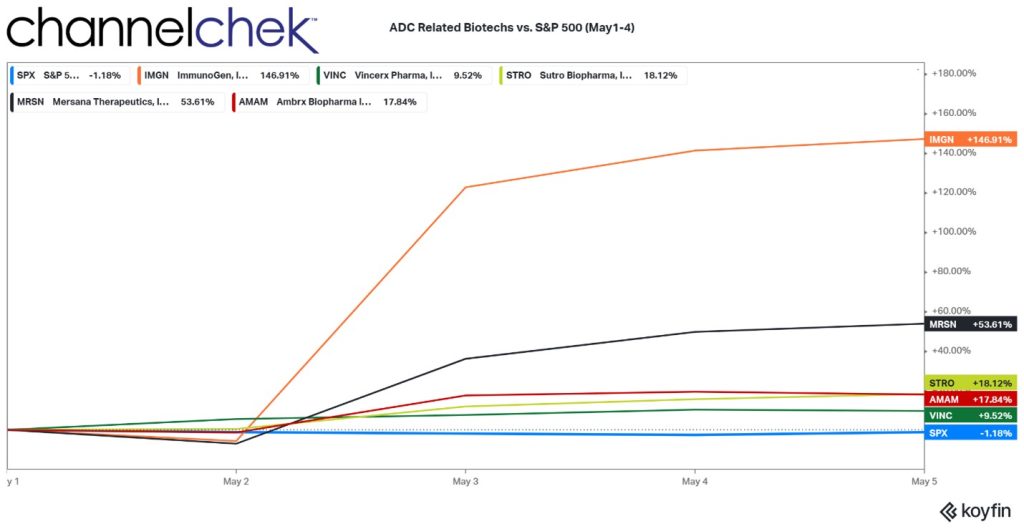

As the chart below indicates, since May 1, the S&P 500 sank by more than 1.00%, yet cancer research biotech, which is not highly correlated to the overall market, rewarded investors in companies working with ADC technology for better cancer outcomes.

Among the stocks that seemed to have gotten a boost from Immunogen’s good news are:

Ambrx Biopharma (AMAM:Nasdaq) is a clinical-stage biologics company. The company’s lead product candidate is ARX788, an anti-HER2 antibody-drug conjugate (ADC), which is being investigated in various clinical trials for the treatment of breast cancer, gastric/gastroesophageal junction cancer, and other solid tumors.

Mersana Therapeutics (MRSN:Nasdaq) is a clinical-stage biopharmaceutical company developing antibody-drug conjugates (ADC) for cancer patients with unmet needs.

Vincerx Pharma (VINC:Nasdaq) is a four-year-old clinical-stage biopharmaceutical company. VIP236, a small molecule drug conjugate that is in Phase 1 clinical trials to treat solid tumors. The company’s preclinical stage product candidates include VIP943 and VIP924 for the treatment of hematologic malignancies.

Sutro Biopharma (STRO:Nasdaq) is a clinical-stage oncology company that develops site-specific and novel-format antibody-drug conjugates (ADC). The company’s candidates include STRO-001, an ADC directed against the cancer target CD74 for patients with multiple myeloma and non-Hodgkin lymphoma, an ADC directed against folate receptor-alpha for patients with ovarian and endometrial cancers, which is in Phase 1 clinical trials.

As these biotech companies that are focused on ADC cancer treatment move their products through clinical trials, each success (or failure) is likely to impact the group. Not yet in the publicly traded group, but also being watched by those involved with ADC cancer stocks is OS Therapies.

OS Therapies (OSTX) is a U.S.-based biotech company that is developing therapies to treat specific cancers. The company completed its filing with the SEC last month to go public through an initial public offering (IPO). The biotech company hopes to list its shares on the NYSE American and trade under the symbol OSTX. It is a clinical-stage phase II biopharmaceutical company focused on the identification, development, and commercialization of treatments for Osteosarcoma (OS) and other solid tumors. There have not been any new treatments approved by the FDA for Osteosarcoma for more than 40 years.

The lead core product candidates OS Therapies is researching are OST-HER2 and the OST-Tunable Drug Conjugate (OST-TDC) platform. The company says it intends to expand its pipeline beyond osteosarcoma into solid tumors. The OST-Tunable Drug Conjugate (OST-TDC) platform could deliver the next-generation ADC technology with the intent of providing a more potent drug and better efficacy with an improved safety profile, a potential “Best-in-Class”. Importantly, OS Therapies lead ADC drug will target folate receptor alpha-binding utilizing a small molecule ligand the same druggable target to Immunogen’s (IMGN) folate receptor alpha-binding site which is something that could become extremely notable to investors and larger pharmaceutical companies. Immunogen has now proved that folate receptor alpha-binding site can work.

The next generation ADC, according to the company filing, will be targeting ovarian, lung and pancreatic cancers. “Tunable” is a term used in drug development that refers to the properties that can be influenced by chemical modifications, and “antibody-drug conjugate.”

An IPO date for OS Therapies has not yet been confirmed.

Take Away

Stocks tend to trade up or down depending on the mood of the market. The current mood is that the overall market may still be overpriced. As such, 2023 has been marked by the bulls and bears duking it out – without any clear direction.

Biotech stocks tend to be far less correlated to what is going on in other areas of the market. This makes the sector and various peer groups worth a visit in bad markets. For example, when the pandemic began to unfold, many biotech stocks rocketed during the same period the overall market was crashing.

Within biotech, companies those working on the production of related technology typically trade in rough tandem with each other. Biotech stocks developing ADC, presumed to be a breaktrough in treating many types of cancers, have gotten a lift in anticipation of the imminent success of one of their peers.

To do a deeper dive into small-cap names, scroll up to the search bar found next to the Channelchek logo, then enter a company name, ticker, or other keyword.

MELVILLE, N.Y. – May 4, 2023– Comtech (NASDAQ: CMTL) announced today that Aarna Networks, a leading provider of network automation and orchestration solutions, will become the Company’s latest publicly revealed EVOKE technology partner.

As the fourth publicly announced EVOKE technology partner, Aarna Networks will work with Comtech to create new integrated cloud-native solutions for emerging commercial and government use cases. By combining Aarna Networks technologies with Comtech’s Dynamic Cloud Platform (DCP), the companies will enable customers to easily add and manage a variety of open architecture cloud-based applications across private, hybrid, and public networks, in both terrestrial and non-terrestrial environments.

“By working with Aarna Networks as an EVOKE technology partner, we will open the door to new cloud-based applications that will support the convergence of communications infrastructures and empower individuals, communities, businesses, and governments by providing access to new technologies,” said Ken Peterman, President and CEO, Comtech. “As connectivity services expand into new global markets, the need for innovative cloud applications will continue to grow. By integrating Aarna Networks zero-touch edge orchestration technologies with Comtech’s DCP offerings, we will multiply the value our cloud-native solutions can bring to 5G, satellite communications, and edge computing customers around the world.”

Comtech’s DCP is designed to be infrastructure, cloud, and application agnostic. Comtech’s DCP also unlocks the availability of new third-party cloud-based applications across current and future computing environments.

Aarna Network’s software, and software as a service (SaaS) solutions, leverage open source, cloud native, and DevOps methodologies to provide zero-touch edge and 5G service orchestration and management (SMO) services.

“Aarna Networks is thrilled to be an EVOKE technology partner and to integrate with Comtech’s DCP,” said Amar Kapadia, Co-founder and CEO, Aarna Networks. “This allows us to bring edge and 5G services orchestration to diverse infrastructures and management systems for a broad set of industry use cases. Our open source, vendor neutral Open Radio Access Network (O-RAN) SMO offering is important for a variety of customers segments across global markets.”

EVOKE is Comtech’s Innovation Foundry, which is led by the company’s Chief Growth Officer, Anirban Chakraborty, and is dedicated to creating and accelerating transformational changes across the global technology landscape. EVOKE engages with customers, partners, and suppliers to push the boundaries of technologies that will lay the foundation of connectivity as well as shape future societies and ecosystems.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 9-1-1 emergency services, satellite and space communications technologies, and cloud-native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

About Aarna Networks

Aarna Networks solves enterprise edge and 5G management complexity through zero-touch edge orchestration at scale. We’re on a mission to help enterprises and network operators unlock previously unimagined new services and drastically slash operational costs and improve time to market. Aarna’s software and SaaS solutions leverage open source, cloud native, and DevOps methodologies to provide zero-touch edge and 5G service orchestration and management services. Visit us at https://www.aarnanetworks.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results and performance could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

FLORHAM PARK, N.J., May 04, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced that the Company will release financial results for the first quarter of 2023 on Monday, May 15, 2023, before the market opens. Following the release, management will host a conference call to review the financial results and provide a business update.

Monday, May 15, 2023, 8:00 AM ET Domestic: 877-407-3088 International: 201-389-0927 Conference ID: 13738216 Webcast: PDS Biotech Earnings Webcast

After the live webcast, the event will be archived on PDS Biotech’s website for six months.

About PDS Biotechnology PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce and shrink tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16- associated cancers in multiple Phase 2 clinical trials and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Multiple Additional Indications Possible, Including Autoimmune Diseases: Pipeline within a Product

Published Non-Human Primate Studies Show TNX-1500 Prolongs Renal and Heart Allograft Survival

Phase 1 Clinical Trial of TNX-1500 Expected to Start Third Quarter 2023

CHATHAM, N.J., May 04, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced the U.S. Food and Drug Administration (FDA) has cleared the Investigational New Drug (IND) application to support a Phase 1 clinical trial with TNX-1500 (anti-CD40L monoclonal antibody [mAb]). The first indication Tonix is seeking for TNX-1500 is the prevention of organ rejection in patients receiving a kidney transplant. The Company expects to initiate enrollment in the Phase 1 study in the third quarter of 2023.

The IND application for TNX-1500 was supported by preclinical allotransplantation studies conducted at the Massachusetts General Hospital (MGH), led by principal investigators Tatsuo Kawai, MD, PhD, A. Benedict Cosimi Chair in Transplant Surgery, MGH and Professor of Surgery, Harvard Medical School (HMS), and Richard N. Pierson III, M.D., scientific director of the Center for Transplantation Sciences in the Department of Surgery at MGH and Professor of Surgery at HMS.

“This is an important milestone as we advance TNX-1500 into clinical development,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Despite advancements in the field of solid organ transplantation, there remains a significant need for new treatments with improved activity and tolerability to prevent organ transplant rejection. Our primary focus of early development will be allotransplantation in which the donor organ comes from another human. However, in the longer term we hope to develop TNX-1500 for xenograft transplantation in which the donor organ comes from a genetically engineered pig.”

Dr. Lederman continued, “We view TNX-1500 as a pipeline within a product, because of its potential to treat a number of autoimmune diseases. Anti-CD40L mAbs have demonstrated activity and tolerability in autoimmune diseases like systemic lupus erythematosus and Sjögren’s Syndrome. An anti-CD40L mAb is also in development for multiple sclerosis. CD40L is a member of the TNFα super gene family. Other TNFα super gene members have been the targets of successful mAb therapeutics: TNFα and RANKL for autoimmune diseases and osteoporosis, respectively. Still other TNFα super gene family members are targeted by mAbs in development including TNF-like ligand 1A (TL1A) and CD30L for ulcerative colitis and Ox40L for atopic dermatitis.”

TNX-1500 is a third generation anti-CD40L mAb that has been designed by protein engineering to decrease FcγRIIA binding and to therefore reduce the potential for thrombosis. Preclinical studies in non-human primates demonstrated that TNX-1500 showed activity in preventing allograft organ rejection and was well tolerated1,2.

About TNX-1500

TNX-1500 (Fc-modified anti-CD40L mAb) is a humanized monoclonal antibody that interacts with the CD40-ligand (CD40L), which is also known as CD154. TNX-1500 is being developed for the prevention of allograft and xenograft rejection, for the treatment of autoimmune diseases and for the prevention of graft-versus-host disease (GvHD) after hematopoietic stem cell transplantation (HCT). A Phase 1 study of TNX-1500 is expected to be initiated in the third quarter of 2023. Two articles have recently published in the American Journal of Transplantation that demonstrate TNX-1500 prolongs non-human primate renal and heart allograft survival1,2.

1Lassiter, G., et al. (2023). TNX-1500, a crystallizable fragment–modified anti-CD154 antibody, prolongs non-human primate renal allograft survival. American Journal of Transplantation. April 3, 2023. https://doi.org/10.1016/j.ajt.2023.03.022

2Miura, S., et al. (2023) TNX-1500, a crystallizable fragment–modified anti-CD154 antibody, prolongs non-human primate cardiac allograft survival. American Journal of Transplantation. April 6, 2023. https://doi.org/10.1016/j.ajt.2023.03.025

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with topline data expected in the fourth quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Enrollment in a Phase 2 study has been completed, and topline results are expected in the third quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), in development for chronic migraine, is currently enrolling with topline data expected in the fourth quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets), a once-daily formulation being developed as a treatment for major depressive disorder (MDD), is also currently enrolling with interim data expected in the fourth quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the third quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the third quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox, for which a Phase 1 study is expected to be initiated in the second half of 2023. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases. The infectious disease portfolio also includes TNX-3900 and TNX-4000, classes of broad-spectrum small molecule oral antivirals.

*All of Tonix’s product candidates are investigational new drugs (IND) or biologics and have not been approved for any indication. TNX-801, TNX-2900, TNX-3900 and TNX-4000 are in pre-IND stage of development and have not been approved for any indication.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

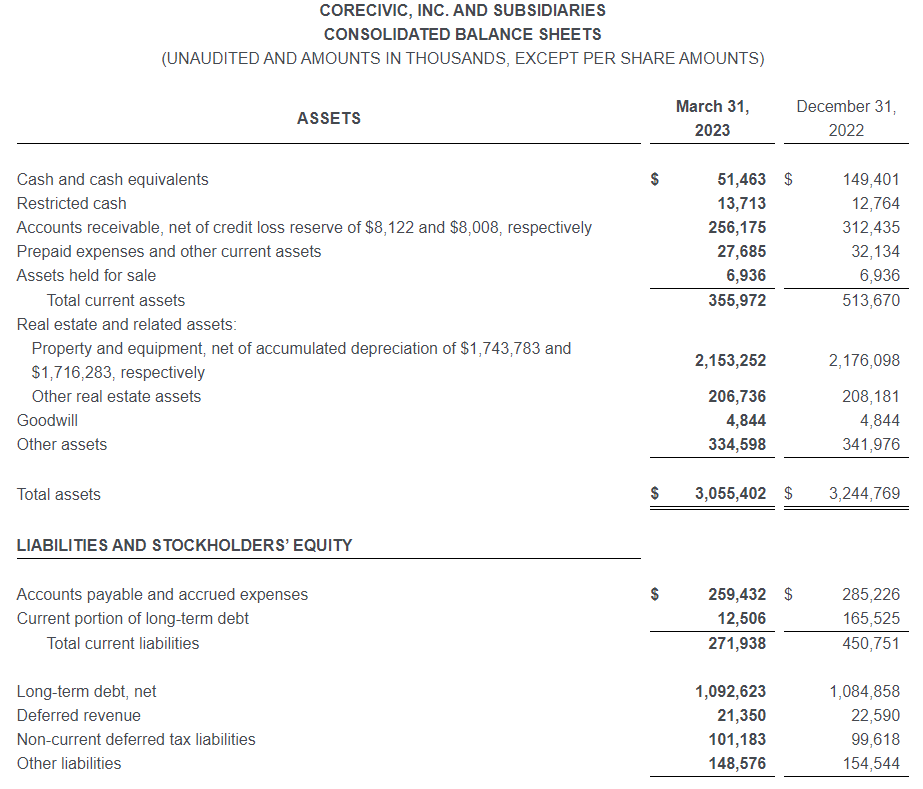

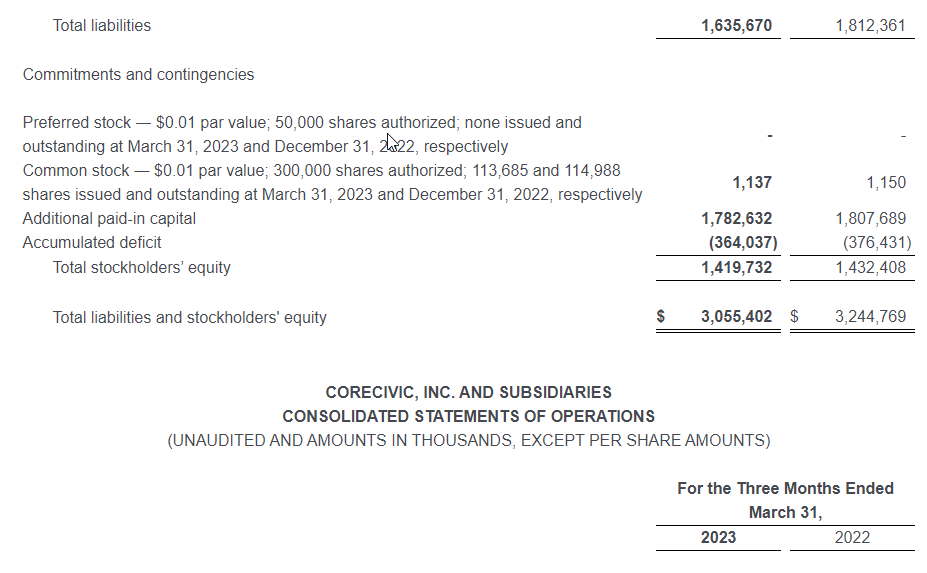

BRENTWOOD, Tenn., May 03, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today its financial results for the first quarter of 2023.

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, said, “We are pleased to report first quarter results that were in line with our expectations, while we continue to operate through a challenging labor market and execute on our long-term capital allocation strategy. During the first quarter, we generated $73.7 million of EBITDA that, along with existing liquidity, enabled us to repay in full the $153.8 million outstanding balance of our 4.625% Senior Notes that were scheduled to mature on May 1, 2023. We also continued to execute on our share repurchase program during the quarter by repurchasing 2.5 million shares, representing an additional 2% of our outstanding shares, at a total cost of $24.9 million.

Hininger continued, “We’re also proud to have recently released our fifth Environmental, Social and Governance (ESG) Report. The ESG report details the ways we delivered reentry and vocational programming designed to prepare those in our care for long-lasting success upon reentry to their communities during 2022, a mission that our organization has been carrying out for more than 40 years. I hope you have an opportunity to review our latest ESG report to learn more about CoreCivic and the important services we provide. We are proud of our history and our accomplishments that truly help individuals in our care change their lives for the better primarily through the strength and volume of our evidence-based programs.”

Financial Highlights – First Quarter 2023

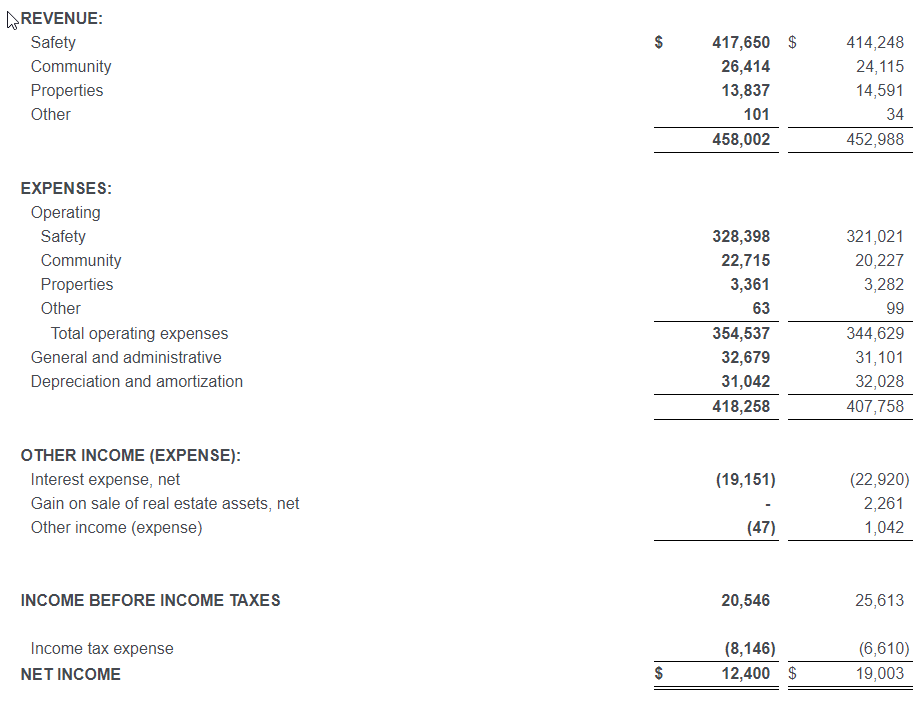

Total revenue of $458.0 million

CoreCivic Safety revenue of $417.7 million

CoreCivic Community revenue of $26.4 million

CoreCivic Properties revenue of $13.8 million

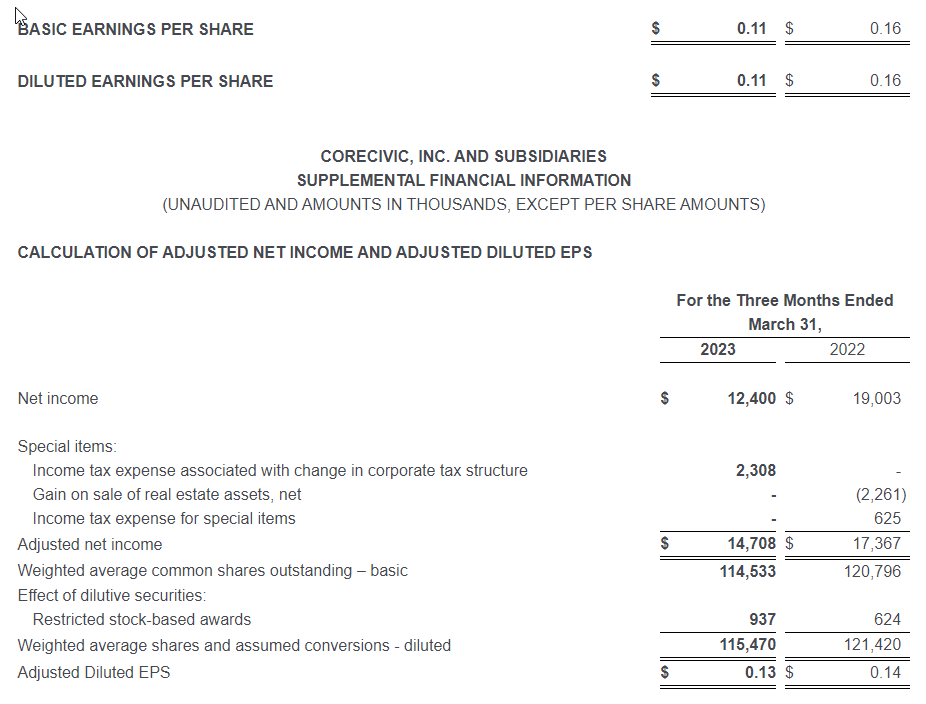

Net Income of $12.4 million

Diluted earnings per share of $0.11

Adjusted Diluted EPS of $0.13

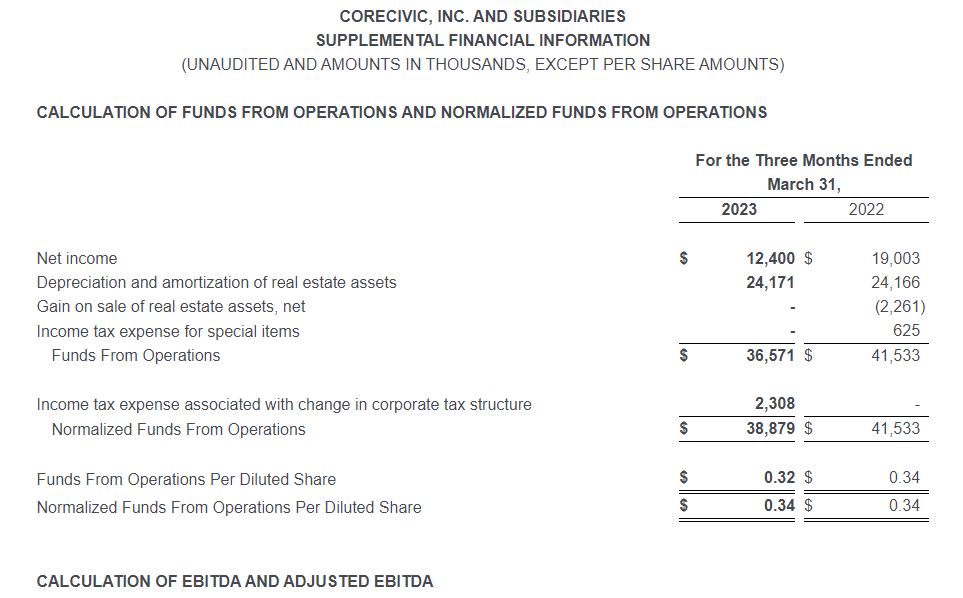

Normalized Funds From Operations per diluted share of $0.34

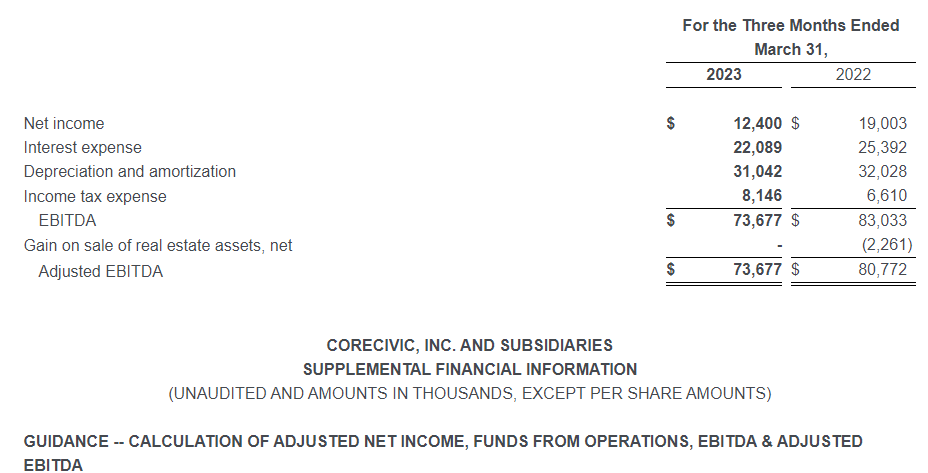

EBITDA of $73.7 million

First Quarter 2023 Financial Results Compared With First Quarter 2022

Net income in the first quarter of 2023 totaled $12.4 million, or $0.11 per diluted share, compared with net income in the first quarter of 2022 of $19.0 million, or $0.16 per diluted share. Adjusted for special items, adjusted net income in the first quarter of 2023 was $14.7 million, or $0.13 per diluted share (Adjusted Diluted EPS), compared with adjusted net income in the first quarter of 2022 of $17.4 million, or $0.14 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The $0.01 per share decline in Adjusted Diluted EPS occurred despite transitioning to the previously announced contract with the state of Arizona at our 3,060-bed La Palma Correctional Center in Arizona, the expiration of our contract with the Federal Bureau of Prisons (BOP) at the McRae Correctional Facility on November 30, 2022, and ongoing labor market pressures, including above average wage inflation. We substantially completed the transition of inmate populations at the La Palma facility by the end of 2022, but we continued to incur elevated operating expenses during the first quarter of 2023 due to ongoing efforts to attract and retain local staff at the facility. Despite the expiration of the contract with the BOP at the McRae facility, a facility we sold to the state of Georgia in 2022, our renewal rate on owned and controlled facilities remains high at 94% over the previous five years. We believe our renewal rate on existing contracts remains high due to a variety of reasons including the aged and constrained supply of available beds within the U.S. correctional system, our ownership of the majority of the beds we operate, the value our government partners place in the wide range of recidivism-reducing programs we offer to those in our care, and the cost effectiveness of the services we provide.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $73.7 million in the first quarter of 2023, compared with $83.0 million in the first quarter of 2022. Adjusted EBITDA was $73.7 million in the first quarter of 2023, compared with $80.8 million in the first quarter of 2022. Adjusted EBITDA of $80.8 million in the prior year quarter excludes a net gain on sale of real estate assets. Adjusted EBITDA decreased from the prior year quarter primarily due to the previously mentioned transition of offender populations at our La Palma Correctional Center, which resulted in a reduction in EBITDA of $7.4 million, and the expiration of our BOP contract at the McRae Correctional Facility in November 2022, which resulted in a reduction in EBITDA of $2.3 million from the first quarter of 2022 to the first quarter of 2023. Due to an improving labor market, we achieved higher staffing levels in the first quarter of 2023 than in the prior year quarter; however, we incurred higher wage rates than in the prior year quarter in order to attract and retain facility staff in the challenging labor market. We also incurred higher travel expenses in order to augment staffing levels at multiple facilities. We believe these investments in staffing are positioning us to manage the increased number of residents we anticipate at our facilities once the remaining occupancy restrictions attributable to COVID-19 are removed, most notably Title 42, a policy that denies entry at the United States border to asylum-seekers and anyone crossing the border without proper documentation or authority in an effort to contain the spread of COVID-19. Title 42 is currently scheduled to end in May 2023. Despite the difficult labor market, we have been able to reduce certain labor-related expenses, such as registry nursing and temporary incentives, which moderated during the first quarter of 2023 compared with the first quarter of 2022.

Funds From Operations (FFO) was $36.6 million, or $0.32 per diluted share, in the first quarter of 2023, compared to $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO, which excludes special items, was $38.9 million, or $0.34 per diluted share, in the first quarter of 2023, compared with $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Asset Dispositions and Assets Held for Sale

During the third quarter of 2022, we began marketing for sale our Roth Hall Residential Reentry Center and the Walker Hall Residential Reentry Center, both of which are located in Philadelphia, Pennsylvania and reported in our CoreCivic Properties segment. The properties were classified as held for sale as of March 31, 2023 and December 31, 2022. A purchase and sale agreement for these two Philadelphia properties was executed in March 2023 and the properties were sold on May 2, 2023, generating net sales proceeds of $5.8 million, which approximated the carrying value of the properties. We are also marketing for sale a residential reentry center in Denver, Colorado with a carrying value of $1.2 million and reported in our CoreCivic Community segment, which was also classified as held for sale as of March 31, 2023.

Share Repurchases

On May 12, 2022, our Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $150.0 million of our common stock. On August 2, 2022, our Board of Directors authorized an increase in our share repurchase program of up to an additional $75.0 million in shares of our common stock, or a total of up to $225.0 million. During the first quarter of 2023, we repurchased 2.5 million shares of our common stock at an aggregate purchase price of $24.9 million, excluding fees, commissions and other costs related to the repurchases. Since the share repurchase program was authorized, through March 31, 2023, we have repurchased a total of 9.1 million shares at an aggregate price of $99.4 million under this share repurchase program.

As of March 31, 2023, we had $125.6 million remaining under the share repurchase program authorized by the Board of Directors. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time.

Debt Repayments

On December 22, 2022, we delivered an irrevocable notice to the trustee of the holders of the 4.625% Senior Notes that we elected to redeem in full the 4.625% Senior Notes that remained outstanding on February 1, 2023. The 4.625% Senior Notes were redeemed on February 1, 2023 at a redemption price equal to 100% of the principal amount of the outstanding 4.625% Senior Notes, which amounted to $153.8 million, plus accrued and unpaid interest to, but not including, the redemption date. We used a combination of cash on hand and available capacity under our Revolving Credit Facility to fund the redemption. During the first quarter of 2023, we reduced our total debt balance by $146.2 million, or by $48.2 million net of the change in cash. Following the redemption of the 4.625% Senior Notes, we have no debt maturities until 2026.

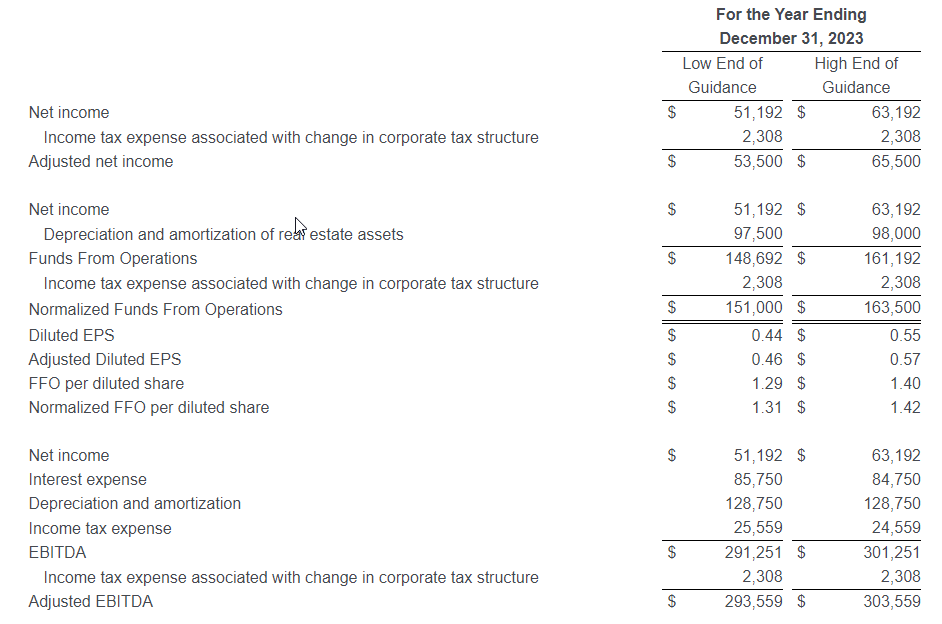

2023 Financial Guidance

Based on current business conditions, we are providing the following update to our financial guidance for the full year 2023:

Guidance Full Year 2023

Prior Guidance Full Year 2023

Net income

$51.2 million to $63.2 million

$58.0 million to $75.0 million

Adjusted net income

$53.5 million to $65.5 million

$58.0 million to $75.0 million

Diluted EPS

$0.44 to $0.55

$0.50 to $0.65

Adjusted Diluted EPS

$0.46 to $0.57

$0.50 to $0.65

FFO per diluted share

$1.29 to $1.40

$1.35 to $1.50

Normalized FFO per diluted share

$1.31 to $1.42

$1.35 to $1.50

EBITDA

$291.3 million to $301.3 million

$298.5 million to $313.5 million

Adjusted EBITDA

$293.6 million to $303.6 million

$298.5 million to $313.5 million

Financial guidance has been updated to reflect a favorable $0.01 per share variance to our internal forecast for the first quarter of 2023, offset by $0.04 per share to reflect the non-renewal of our lease with the state of Oklahoma at our North Fork Correctional Facility expiring June 30, 2023, which we previously disclosed on April 24, 2023. In addition, we continue to negotiate in good faith with the state of Oklahoma for the renewal of our contract to manage our Davis Correctional Facility, which also expires June 30, 2023, and operated at a loss during 2022 and the first quarter of 2023. However, we have not yet been able to reach acceptable terms. Our updated guidance was further reduced by $0.03 per share to reflect the potential transition of inmate populations out of the Davis Correctional Facility during the second quarter of 2023 and idle operations during the second half of the year, which we did not contemplate in our previous forecast. If we are able to reach acceptable terms on a new agreement, the $0.03 per share reduction will be avoided, as we would exceed our forecast by approximately $0.02 per share during the second quarter by avoiding the transition, and we would further exceed our guidance during the second half of 2023, the magnitude of which would depend on the terms of a new agreement.

During 2023, we expect to invest $64.0 million to $67.0 million in capital expenditures, consisting of $36.0 million to $37.0 million in maintenance capital expenditures on real estate assets, $25.0 million to $26.0 million for maintenance capital expenditures on other assets and information technology, and $3.0 million to $4.0 million for other capital investments. These capital expenditure amounts are unchanged from our previous guidance.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the first quarter of 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the second quarter of 2023. Written materials used in the investor presentations will also be available on our website beginning on or about May 19, 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, May 4, 2023, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page.

To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BI6394fffe952b47d497a2735e53d08f32. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice, or DOJ, not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, or the Private Prison EO, impacting utilization primarily by the BOP and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) the duration of the federal government’s denial of entry at the United States southern border to asylum-seekers and anyone crossing the southern border without proper documentation or authority in an effort to contain the spread of COVID-19, a policy known as Title 42 (Title 42 is expected to end May 11, 2023, when President Biden has decided to lift the public health emergency for COVID-19, although its termination may be subject to ongoing litigation, the outcome of which is unclear. Most recently, on December 27, 2022, the Supreme Court granted a stay on the cessation of Title 42, while it considers an appeal by a group of states to continue the expulsions.); (vii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (viii) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

NOTE TO SUPPLEMENTAL FINANCIAL INFORMATION

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share metrics are non-GAAP financial measures. The Company believes that these measures are important operating measures that supplement discussion and analysis of the Company’s results of operations and are used to review and assess operating performance of the Company and its properties and their management teams. The Company believes that it is useful to provide investors, lenders and security analysts disclosures of its results of operations on the same basis that is used by management.

FFO, in particular, is a widely accepted non-GAAP supplemental measure of performance of real estate companies, grounded in the standards for FFO established by the National Association of Real Estate Investment Trusts (NAREIT). NAREIT defines FFO as net income computed in accordance with GAAP, excluding gains (or losses) from sales of property and extraordinary items, plus depreciation and amortization of real estate and impairment of depreciable real estate and after adjustments for unconsolidated partnerships and joint ventures calculated to reflect funds from operations on the same basis. As a company with extensive real estate holdings, we believe FFO and FFO per share are important supplemental measures of our operating performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs and other real estate operating companies, many of which present FFO and FFO per share when reporting results. EBITDA, Adjusted EBITDA, and FFO are useful as supplemental measures of performance of the Company’s properties because such measures do not take into account depreciation and amortization, or with respect to EBITDA, the impact of the Company’s tax provision and financing strategies. Because the historical cost accounting convention used for real estate assets requires depreciation (except on land), this accounting presentation assumes that the value of real estate assets diminishes at a level rate over time. Because of the unique structure, design and use of the Company’s properties, management believes that assessing performance of the Company’s properties without the impact of depreciation or amortization is useful. The Company may make adjustments to FFO from time to time for certain other income and expenses that it considers non-recurring, infrequent or unusual, even though such items may require cash settlement, because such items do not reflect a necessary or ordinary component of the ongoing operations of the Company. Normalized FFO excludes the effects of such items. The Company calculates Adjusted Net Income by adding to GAAP Net Income expenses associated with the Company’s debt repayments and refinancing transactions, and certain impairments and other charges that the Company believes are unusual or non-recurring to provide an alternative measure of comparing operating performance for the periods presented.

Other companies may calculate Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO differently than the Company does, or adjust for other items, and therefore comparability may be limited. Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO and, where appropriate, their corresponding per share measures are not measures of performance under GAAP, and should not be considered as an alternative to cash flows from operating activities, a measure of liquidity or an alternative to net income as indicators of the Company’s operating performance or any other measure of performance derived in accordance with GAAP. This data should be read in conjunction with the Company’s consolidated financial statements and related notes included in its filings with the Securities and Exchange Commission.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2QFY23 Results. DLH reported revenue of $99.4 million compared to $68.9 million the year prior, excluding FEMA contract contribution. GRSi contributed $32.6 million of revenue, indicating the core DLH business saw revenue decline $2.1 million y-o-y. Net income was reported at $0.8 million, or $0.06 per diluted share, versus $7.2 million, or $0.50, last year. EBITDA was at $10.5 million compared with $12.1 million last year, or $6.6 million excluding FEMA.

Focusing In. Although revenue came in lower than our expected $104 million, we believe this to be more a function of some business moving to the right and the challenge in estimating the recently acquired GRSI business. We do not believe the “miss” indicates a deterioration of the core business. We continue to believe the new DLH has significant growth opportunities. The Company has noted multiple cross selling opportunities, with a recent example being the award given by the National Cancer Institute’s Center for Biomedical Informatics and Information Technology for IT services.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Results Below Expectations. Revenue totaled $458 million, up from $453 million a year ago, but below our $469 million projection. Consensus was $471 million. Adjusted EBITDA was $73.7 million, down from $80.8 million in 1Q22. We were at $76.4 million. CXW reported net income of $12.4 million, or $0.11/sh, compared to $19 million, or $0.16/sh last year and our $16.3 million, or $0.14/sh estimate.

Labor, Arizona Remain Challenges. CoreCivic substantially completed the transition of inmate populations at the La Palma facility by the end of 2022, but continued to incur elevated operating expenses during the first quarter of 2023. This is due to ongoing efforts to attract and retain local staff at the facility, as well as other facilities to position the Company for the increased number of residents anticipated at facilities once the remaining occupancy restrictions attributable to COVID-19 are removed.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor webinar. Comstock recently hosted a virtual investor meeting to provide a business update, including a discussion of first quarter financial results and upcoming milestones. Executing a license agreement(s) associated with its biorefining technologies and commencing development of commercial scale projects remains the most significant revenue opportunity in 2023. Within its mining segment, Comstock expects to publish preliminary economic assessments for the Lucerne and Dayton resource areas. Within its lithium-ion battery recycling segment, the company expects to advance the technology readiness for broader material recycling, including photovoltaics.

Sale of battery recycling facility enhances financial flexibility. Comstock’s LINICO subsidiary is advancing the sale of its battery recycling facility in the Tahoe Reno Industrial Center and associated assets to American Battery Technology Corporation (OTCQX: ABML) for a gross price of $27.6 million. As of April 21, Comstock has received $18 million in cash and 10 million restricted shares of American Battery Technology Corporation stock with the guarantee that Comstock will receive additional cash and/or shares if the proceeds for the shares are less than $6.6 million. Comstock expects to receive an additional $3.0 million in cash on or before May 12, 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

The Strategy is Working. Posting record quarterly revenue and improved margins for the quarter indicates management’s growth strategy is working. We believe CVG is at an inflection point for improved growth and margins. The Company is well on its way to achieving its 2027 goal of $1.5 billion in revenue and 9% adjusted EBITDA margin, in our view.

Volume, Price Driving Top Line. Record first quarter revenue was driven by a combination of volume and price, with volume contributing about 60% of top line growth in the quarter and price the other 40%. CVG spent considerable energy in 2022 seeking out more favorable pricing to reflect current operating realities. The final major contract was redone in the first quarter of 2023 and began contributing at the beginning of April.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. Alliance reported first quarter EBITDA and earnings per unit (EPU) of $270.9 million and $1.45, respectively, compared to $154.6 million and $0.28 during the prior year period and $293.9 million and $1.63 during the fourth quarter of 2022. We had forecast EBITDA and EPU of $251.0 million and $1.25. While revenue of $662.9 million was modestly above our estimate of $661.1 million, operating expenses of $338.7 million were well below our estimate of $367.1 million.

Updated guidance. Alliance provided updated 2023 guidance which we have incorporated into our estimates as detailed in the body of this note. While total coal sales volume is still expected to be 36.0 million to 38.0 million tons, coal sales price per ton was reduced to a range of $65 to $67 from $67 to $69 driven by lower pricing expectations for ARLP’s uncontracted coal tonnage position. As a partial offset, segment adjusted EBITDA expense per ton sold was also lowered to $39 to $42 from $40.25 to $42.25. Importantly, Alliance increased the midpoint of its full year guidance for oil and gas volumes on a barrel of oil equivalent basis by approximately 9% due to strong performance on all of its acreage exceeding initial expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Can Biden and McCarthy Avert a Calamitous Debt Default? Three Evidence-Backed Leadership Strategies that Might Help

The U.S. is teetering toward an unprecedented debt default that could come as soon as June 1, 2023.

In order for the U.S. to borrow more money, Congress needs to raise the debt ceiling – currently $31.4 trillion. President Joe Biden has refused to negotiate with House Republicans over spending, demanding instead that Congress pass a stand-alone bill to increase the debt limit. House Speaker Kevin McCarthy won a small victory on April 26 by narrowly passing a more complex bill with GOP support that would raise the debt ceiling but also slash spending and roll back Biden’s policy agenda.

Biden recently invited congressional leaders, including GOP leader McCarthy, to the White House on May 9 to discuss the situation but insisted he isn’t willing to negotiate.

Rather than leading the nation, Biden and McCarthy seem to be waging a partisan political war. Biden likely doesn’t want to be seen as giving in to Repubicans’ demands and diminishing legislative wins for his liberal constituency. McCarthy, with his slim majority in the House, needs to appease even the most hard-line members of his party.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Wendy K. Smith, Professor of Business and Leadership, University of Delaware.

Having studied leadership for over 25 years, I would suggest that their leadership styles are polarized, oppositional, short-term and highly ineffective. Such combative leadership risks a debt default that could send the U.S. into recession and potentially lead to a global economic and financial crisis.

While it may seem almost impossible in the current political climate, Biden and McCarthy have an opportunity to turn around this crisis and leave a positive and lasting legacy of courageous leadership. To do so, they need to put aside partisanship and adopt a different approach. Here are a few evidence-backed strategies to get them started.

Moving From a Zero-Sum Game to a More Holistic Approach

Political leaders often risk being hijacked by members of their own party. McCarthy faces a direct threat by hard-line conservative members of his coalition.

For example, back in January, McCarthy agreed to let a single lawmaker force a vote for his ouster to win enough votes from ultraconservative lawmakers to become speaker. That and other concessions give the most extreme members of his party a lot of control over his agenda and limit McCarthy’s ability to make a compromise deal with the president.

Biden, who just announced he’s running for reelection in 2024, is betting his first-term accomplishments – such as unprecedented climate investments and student loan forgiveness – will help him keep the White House. Negotiating any of that away could cost him the support of key parts of his base.

My research partner Marianne W. Lewis and I label this kind of short-term, one-sided leadership as “either/or” thinking. That is, this approach assumes that leadership decisions are a zero-sum game – every inch you give is a loss to your side. We argue that this kind of leadership is limited at best and detrimental at worst.

Instead, we find that great leadership involves what we call “both/and” thinking, which involves seeking integration and unity across opposing perspectives. History offers examples of how this more holistic leadership style has achieved substantial achievements.

President Lyndon B. Johnson and fellow Democrats were struggling to get a Senate vote on the Civil Rights Act of 1964 and needed Republican support. Despite his initial opposition, Republican Sen. Everett McKinley Dirksen – then the minority leader and a staunch conservative – led colleagues in crossing party lines and joining Democrats to pass the historic legislation.

Another example came in 1990, when South Africa’s then-President Frederik Willem de Klerk freed opponent Nelson Mandela from prison. The two erstwhile political enemies agreed to a deal that ended apartheid and paved the way for a democratic government – which won them both the Nobel Peace Prize. Mandela became president four years later.

This integrative leadership approach starts with a shift of mindset that moves away from seeing opposing sides as conflicting and instead values them as generative of new possibilities. So in the case of the debt ceiling situation, holistic leadership means, at the least, Biden would not simply put up his hands and refuse to negotiate over spending. He could acknowledge that Republicans have a point about the nation’s soaring debt load. McCarthy and his party might recognize they cannot just slash spending. Together they could achieve greater success by developing an integrative plan that cuts costs, increases taxes and raises the debt ceiling.

Champion a Long-Term Vision Over Short-Term Goals

What we call “short-termism” plagues America’s politics. Leaders face pressure to demonstrate immediate results to voters. Biden and McCarthy both have strong incentives to focus on a short-term victory for their side with the presidential and congressional elections coming soon. Instead, long-term thinking can help leaders with competing agendas.

In a 2015 study, Natalie Slawinski and Pratima Bansal studied executives at five Canadian oil companies who were dealing with tensions between keeping costs low in the short term while making investments that could mitigate their industry’s environmental impact over the long run. The two scholars found that those who focused on the short term struggled to reconcile the two competing forces, while long-term thinkers managed to find more creative solutions that kept costs down but also allowed them to do more to fight climate change.

Likewise, if Biden and McCarthy want to avert a financial crisis and leave a lasting legacy, they would benefit from focusing on the long term. Finding points of connection in this shared long-term goal, rather than stressing their significant differences about how to get there, can help shift away from their standoff and toward a solution.

Be Adaptive, Not Assured

Voters often praise political leaders who act swiftly and with confidence and self-assurance, particularly at a moment of economic uncertainty.

Yet finding a creative solution to America’s greatest challenges often requires leaders to put aside the swagger and adapt, meaning they take small steps to listen to one another, experiment with solutions, evaluate these outcomes and adjust their approach as needed.

In a study of business decisions at a Fortune 500 technology company, I spent a year following the senior management teams in charge of six units – each of which had revenues of over $1 billion. I found that the team leaders who were most innovative tended to be good at adaptation. They constantly explored whether they had made the right investment and made changes if needed.

Small steps are also necessary to build unlikely relationships with political foes. In his 2017 book, “Collaborating With the Enemy,” organizational consultant Adam Kahane describes how he facilitated workshops to help former enemies take small steps toward reconciliation, such as in South Africa at the end of apartheid and in Colombia amid the drug wars. Such efforts helped South Africa become a successful multiracial democracy and Colombia end decades of war with a guerrilla insurgency.

This kind of leadership requires small steps toward connection rather than large political leaps. It also requires that both sides let go of their positions and consider where they are willing to compromise.

Biden and McCarthy could learn from two former Tennessee governors, Democrat Phil Bredesen and Republican Bill Haslam. Though they oppose each other on almost every political issue, including gun control, the two former leaders have built a constructive relationship over the years. Rather than tackle the big divisive issues, they started with identifying the small points where they agreed with each other. Doing so led them to build greater trust and continue to look for connections.

So when a gunman killed six people at a school in Nashville recently, the two former governors were able to move beyond political finger-pointing and focus on how their respective parties could work together on meaningful gun reform.

Of course, it’s easier to do this once you’re out of office and the pressure from voters and parties goes away. And although current Tennessee Gov. Bill Lee agreed on the need for gun reform, his fellow Republicans in the state Legislature balked.

A Long Shot, But …

And that’s why I know this is a long shot. The two main political parties are as polarized as ever. The odds of a breakthrough that leads to anything more than a last-second deal that kicks the debt ceiling can down the road remain pretty low – and even that seems in doubt.

But this is about more than the debt ceiling. The U.S. faces a long list of problems big and small, from high inflation and a banking crisis to the war in Ukraine and climate change.

Americans need and deserve leaders who will tackle these issues by working together toward a more creative outcomes.

Stock options, sometimes referred to as derivatives, are a tool for managing risk when combined with a related equity holding, or as a means to amplify return on moves made by a stock or index. There are also related income strategies investors should know about. Newer investors often learn they could have benefited from options after it’s too late. Below we talk about stock options, what they are and how they are used to fill some investor knowledge gaps they may not even be aware they have. This discussion includes understanding what options are, why they are used, the different types of options available, and how you can use them to hedge against the market moving in the wrong direction. You’ll also discover how options can be used to amplify portfolio results.

What are Options?

Options are contracts that give the buyer the right, but not the obligation, to buy or sell an underlying asset at a specified price and date(s). The underlying asset can be anything from stocks, bonds, commodities, or even currencies, for the purpose of this article, we focus on stocks and stock indices.

There are two types of stock options: call options and put options. A call option gives the buyer the right, but not the obligation, to buy the underlying stock at a specified price and date. A put option gives the buyer the right, but not the obligation, to sell the underlying stock at a specified price and date.

When an investor buys an option, they are said to be “long” the option. When they sell an option, they are said to be “short” the option. Being long a call option is similar to being long the stock, as the investor profits if the stock rises. Being long a put option is similar to being short the stock, as the investor profits if the stock price falls.

Why Are Options Used?

Options are used for various reasons, such as speculation, hedging, and income generation. Speculators implement strategies to bet on the direction of the options underlying stock. For example, an investor that expects a stock price may rise will buy a call option. It they believe it will fall, they could get short exposure by going long a put option.

Options can also serve investors to hedge (protect) their holdings and offset potential losses in the underlying position. For example, if an investor owns XYZ Stock, they can buy a put option to protect against a potential drop in XYZ Stock. If the stock price falls, the put option will increase in value; depending on the shares controlled by the option, it can offset the decline in the stock.

Income generation using stock options is growing in usage. The scenario where this works is when an investor sells a call option against a stock they own, as part of the sale, they collect a premium for the option. If the stock price remains below the strike price of the call option, the investor keeps the premium and the stock. If the stock price rises above the strike price, the investor must sell the stock at the strike price, but still keeps the premium. This works best in a flat or declining market.

Using Options as a Hedge Against Losses

Options can be used as a hedge against the market moving against a stock position. For example, if an investor owns 100 shares of ABC Stock, currently trading at $50 per share. And the investor is concerned that the stock price may fall, but does not want to sell the stock and miss out on potential gains if the stock price rises, or in some cases, create a tax situation.

To hedge against a potential drop in ABC’s stock price, the investor may decide to buy a put option with a strike price of $45, expiring in three months, for a premium (cost) of $2 per share. If the stock price falls below $45, the put option will increase in value, offsetting the losses in the stock. If the stock price remains above $45, the put option will expire worthless, and the investor keeps the stock and the premium.

Time Decay, Intrinsic Value, and Extrinsic Value

So far, the use of options described here have been fairly straightforward. But there are considerations that might help keep this portfolio tool in the toolbox until it is most needed. The considerations are time decay, intrinsic value, and extrinsic value. Here is what is important to understand about these realities.

Time Decay:

Time decay, also known as theta, refers to the decrease in the value of an option as it approaches its expiration date. Options have a limited lifespan, and as time passes, the likelihood of the option ending up in the money decreases. Therefore, the time value of an option decreases as it approaches its expiration date, resulting in a decrease in the option premium.

Intrinsic Value:

Intrinsic value is the amount by which an option is in the money. In other words, it is the difference between the current market price of the stock and the strike price of the option. For example, if a call option has a strike price of $50 and the underlying stock is currently trading at $60, the intrinsic value of the option is $10 ($60 – $50).

Intrinsic value only applies to in-the-money options, as options that are out-of-the-money or at-the-money have no intrinsic value. The intrinsic value of an option is important because it represents the profit that an option holder would realize if they exercised the option immediately.

Extrinsic Value:

Extrinsic value, also known as time value, is the portion of an option’s premium that is not attributed to its intrinsic value. Extrinsic value is the amount that investors are willing to pay for the time left until expiration and the possibility of the underlying asset moving in their favor.

Extrinsic value is affected by several factors, including the time left until expiration, and the volatility of the underlying stock. As the expiration date approaches, the extrinsic value of an option decreases, and the option premium decreases as well.

Options Premium:

The options premium is the price that the buyer pays to purchase an option. The options premium is determined by various factors, including the current market price of the underlying asset, the strike price, the expiration date, and the level of volatility in the stocks price.

The options premium is made up of intrinsic value and extrinsic value. The intrinsic value represents the portion of the premium that is directly attributable to the difference between the current market price of the underlying asset and the strike price of the option. The extrinsic value represents the portion of the premium that is not attributable to the intrinsic value and is based on the time left until expiration, the level of volatility in the market, and other factors.

Understanding time decay, intrinsic value, and extrinsic value is crucial when it comes to trading stock options. Time decay affects the value of an option as it approaches its expiration date, while intrinsic value and extrinsic value make up the options premium. By understanding these concepts, investors can better understand their costs and make more enlightened decisions.

Take Away

Stock investors transact in stock options for various reasons. These include portfolio protection, income generation for an existing portfolio, and speculating on the direction of an asset. There are considerations associated with holding options beyond any commission or bid/offer spread. These are intrinsic premium costs for in-the-money trades, extrinsic as they relate to value and decay on the position as it approaches its expiration date.

Adding risk management using options to your investment tools to call upon when appropriate can reduce stress; speculating with the help of derivatives can be very rewarding but may have the impact of increasing portfolio swings in value along the way.

DENVER, May 3, 2023 /CNW/ – Medicine Man Technologies operating as Schwazze, (OTCQX: SHWZ) (NEO: SHWZ) (“Schwazze” or the “Company”), will hold a first quarter earnings webcast on May 10, 2023, at 5:00 pm ET.

Investors and stakeholders may participate in the conference call by dialing 416-764-8650 or by dialing North American toll free 1-888-664-6383 or listen to the webcast from the Company’s website at https://ir.schwazze.com The webcast will be available on the Company’s website and on replay until May 17, 2023, and may be accessed by dialing 416-764-8677 or North American toll free 1-888-390-0541 / 613777 #.

Following their prepared remarks, Management will answer investor questions. Investors may submit questions in advance or during the conference call itself through the weblink: https://app.webinar.net/8JdExl9XLGb This weblink has been posted to the Company’s website and will be archived on the website. All Company SEC filings can also be accessed on the Company website at https://ir.schwazze.com/sec-filings

About Schwazze Schwazze (OTCQX:SHWZ, NEO:SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices. Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc.

Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth.