Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results. Great Lakes reported total revenue of $117.2 million, a decrease from $158.4 million the prior year and below our estimate of $137 million. Gross margin was 7.7% compared to 2.4%, but lower than our projection of 8.8%. Net loss was at $6.2 million, or $0.09 per diluted share compared to $9.9 million last year, or $0.15. We projected a net loss of $6 million, or $0.09 per share. Adjusted EBTIDA totaled $5.3 million versus $1.3 million in the previous year.

Backlog. Great Lakes ended the quarter record backlog of $1.03 billion, up from $327.1 million at 1Q23, not including approximately $50.0 million of performance obligations related to offshore wind contracts. In addition, the Company ended the quarter with $225 million in low bids and options pending award. Significantly, 71% of backlog was capital projects work, which will help drive margins higher going forward.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q23 Results. Record revenue of $1.0 billion was up 4.5% y-o-y, and above our $965 million forecast. Adjusted EBITDA came in at $64.7 million, versus $79 million in 3Q22 and our $64 million estimate. Adjusted diluted EPS was $0.73 compared to $1.33 last year and our $0.90 estimate.

Some Headwinds. 3Q23 results were impacted by a couple items, including contract mix and performance on certain integrated electronic security programs. In addition, the strong 2Q23 benefitted from the pull forward of some business that was expected to occur in the just completed quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q Results. Revenue totaled $483.7 million, up 4.2% year-over-year and up 4.3% sequentially, driven by higher populations and increased per diems. Net income was $13.9 million, or $0.12/sh versus $68.3 million, or $0.58 per share last year. Adjusted EPS was $0.14 for 3Q23 versus $0.08 for 3Q22. Adjusted EBITDA was $75.2 million, up from $68.4 million last year.

ICE Populations. Since the ending of Title 42 on May 11th, overall ICE populations are up 66% through the end of September. CoreCivic ICE populations are up by 4,729, or 84% over the same time frame. We believe this has been driven by management’s foresight in adding staff in anticipation of higher population levels. Reportedly, ICE populations have continued to rise.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q23 Results. Partially helped by one extra week, third quarter results came in above expectations. Revenue totaled $274.6 million, up 20.1% y-o-y. Adjusted EBITDA came in at $27.7 million, up from $20 million in 3Q22. GAAP EPS loss was $0.01 and adjusted EPS was $0.12, compared to a EPS loss of $0.06 and adjusted EPS of $0.08, respectively, a year ago. We had forecasted $250 million, $20.5 million, breakeven, and $0.09, respectively.

Organic Growth Again the Driver. Kratos generated 20.1% overall organic growth in the quarter. The Government Solutions Segment saw overall revenue increase 22% organically to $217.9 million. The Unmanned Systems segment saw 13.4% organic revenue growth, with revenue of $56.7 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Eagle Bulk Shipping Inc. (“Eagle”) is a US-based drybulk owner-operator focused on the Supramax/Ultramax mid-size asset class, which ranges from 50,000 and 65,000 deadweight tons in size; these vessels are equipped with onboard cranes allowing for the self-loading and unloading of cargoes, a feature which distinguishes them from the larger classes of drybulk vessels and provides for greatly enhanced flexibility and versatility- both with respect to cargo diversity and port accessibility. The Company transports a broad range of major and minor bulk cargoes around the world, including coal, grain, ore, pet coke, cement, and fertilizer. Eagle operates out of three offices, Stamford (headquarters), Singapore, and Hamburg, and performs all aspects of vessel management in-house including: commercial, operational, technical, and strategic.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Eagle Bulk Shipping 2023-3Q revenues and earnings were in line with recently updated projections. Eagle reported an average TCE rate of $11,482/day down from $14,367/day in the previous quarter. Eagle continues to command a premium to index rates due to its fleet of newer, scrubber-installed ships.

Management indicated it locked in 68% of 2023-4Q shipping days at a favorable rate of $15,655/day. Guidance for costs per day were largely unchanged from the recently reported quarter. The upcoming jump in TCE rates should result in an improvement in cash flow. Management indicated it will likely use free cash flow to pay down debt. The company fixed additional debt with swaps during the quarter and now estimates that 75% of its debt has been fixed at a rate of 5.2%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Selling A Piece. Kelly Services is selling its European Staffing Business to Gi Group Holdings S.P.A. The sale is for cash consideration of €100 million (about $106 million at current exchange rates) with a €30 million earnout based on a multiple of adjusted 2023 EBITDA and payable in 2Q24. The transaction is expected to close in 1Q24.

But Not All. The deal includes Kelly’s European Staffing business across 14 European countries. Notably, Kelly will maintain its global footprint and continue to provide higher margin, higher growth potential MSP, RPO, and FSP solutions to customers in the EMEA region through KellyOCG. As a leading global vendor-neutral provider of talent supply chain strategies and workforce solutions, KellyOCG leverages a network of 3,000 suppliers – including Gi – spanning 140 countries to connect customers across North America, Asia Pacific, and EMEA with top talent.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EPS of $0.22, up 100% year-over-year Adjusted EBITDA of $16.6 million, up 16.1% year-over-year Our strategy continues to favorably impact our results as Electrical Systems revenues were up 16.8% year-over-year

NEW ALBANY, Ohio, Nov. 01, 2023 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its third quarter ended September 30, 2023.

Third Quarter 2023Highlights(Compared with prior year, where comparisons are noted)

Revenues of $246.7 million, down 1.9% due primarily to higher revenue in the prior year as a result of a COVID backlog in Asia-Pacific which offset an increase in revenue in Electrical Systems in 2023.

Operating income of $12.4 million, up 30.5%; adjusted operating income of $12.5 million, up 17.9%. Improved operating income was driven primarily by improved pricing and cost management, partially offset by volume decreases.

Net income and adjusted net income were both $7.3 million, or $0.22 per diluted share, compared to net income of $3.6 million, or $0.11 per diluted share and adjusted net income of $5.1 million, or $0.15 per diluted share.

Adjusted EBITDA of $16.6 million, up 16.1% with an adjusted EBITDA margin of 6.7%, up from 5.7%.

New business wins year-to-date are expected to be approximately $140 million when fully ramped. The majority of the new business awards continue to be in the Electrical Systems segment.

Strong free cash flow and debt pay down reduced our leverage ratio down to 1.5x from 2.7x.

Robert Griffin, Chairman of the Board and Interim President and Chief Executive Officer, said, “CVG continues to execute on its strategic long-term plan, which again delivered year-over-year bottom line improvements in the quarter. Electrical Systems remains a key growth area for the Company, as evidenced by the strong revenue growth compared to last year and the successful start-up at our new Electrical Systems facilities in Aldama, Mexico, and Tangier, Morocco, which has gone very well. As always, I would like to thank our global CVG teams for their hard work, dedication, and commitment as we continue to execute our strategic goals.”

Andy Cheung, Chief Financial Officer, added, “CVG continued executing on our strategy, delivering strong year-over-year improvements in profitability during the quarter. Despite the strong performance, revenues declined slightly year-over-year against a tough comparable base year in 2022, when our Asia-Pacific business benefited from a post-COVID increase in backlogged sales orders. We also had improved earnings and generated strong free cash flow of $12.5 million during the quarter, further strengthening our financial foundation, and reduced our leverage to 1.5x from 2.7x in the third quarter last year.”

“Going forward, we remain committed to driving strong free cash flow, paying down debt, and investing to support our growing, diverse portfolio of businesses.”

Third Quarter Financial Results (amounts in millions except per share data and percentages)

ThirdQuarter

2023

2022

$ Change

% Change

Revenues

$

246.7

$

251.4

$

(4.7

)

(1.9)%

Gross profit

$

33.9

$

26.8

$

7.1

26.5%

Gross margin

13.7

%

10.7

%

Adjusted gross profit 1

$

34.0

$

27.4

$

6.6

24.1%

Adjusted gross margin 1

13.8

%

10.9

%

Operating income

$

12.4

$

9.5

$

2.9

30.5%

Operating margin

5.0

%

3.8

%

Adjusted operating income 1

$

12.5

$

10.6

$

1.9

17.9%

Adjusted operating margin 1

5.1

%

4.2

%

Net income

$

7.3

$

3.6

$

3.7

102.8%

Adjusted net income 1

$

7.3

$

5.1

$

2.2

43.1%

Earnings per share, diluted

$

0.22

$

0.11

$

0.11

100.0%

Adjusted earnings per share, diluted 1

$

0.22

$

0.15

$

0.07

46.7%

Adjusted EBITDA 1

$

16.6

$

14.3

$

2.3

16.1%

Adjusted EBITDA margin 1

6.7

%

5.7

%

1 See Appendix A for GAAP to Non-GAAP reconciliation

Consolidated Results

Third Quarter 2023 Results

Third quarter 2023 revenues were $246.7 million, compared to $251.4 million in the prior year period, a decrease of 1.9%. The overall decrease in revenues was due to higher revenue in the prior year as a result of a COVID backlog in Asia-Pacific. Foreign currency translation also favorably impacted third quarter 2023 revenues by $2.0 million, or 0.8%.

Operating income in the third quarter 2023 was $12.4 million compared to $9.5 million in the prior year period. The increase in operating income was attributable to improved pricing and cost management, partially offset by volume decreases. Third quarter 2023 adjusted operating income was $12.5 million, excluding special charges.

Interest associated with debt and other expenses was $2.6 million and $2.8 million for the third quarter 2023 and 2022, respectively.

Net income was $7.3 million, or $0.22 per diluted share, for the third quarter 2023 compared to net income of $3.6 million, or $0.11 per diluted share, in the prior year period.

On September 30, 2023, the Company had $5.0 million of outstanding borrowings on its U.S. revolving credit facility and $4.1 million outstanding on its China credit facility, $46.3 million of cash and $152.0 million of availability from the credit facilities, resulting in total liquidity of $198.3 million.

Third Quarter 2023 Segment Results

Vehicle Solutions Segment

Revenues were $145.4 million compared to $154.0 million for the prior year period, a decrease of 5.6%, due to higher revenue in the prior year as a result of a COVID backlog in Asia-Pacific.

Operating income was $10.9 million, compared to $9.6 million in the prior year period, an increase of 14.0%, primarily attributable to price increases, material and freight cost reduction improvements, partially offset by volume decreases.

Electrical Systems Segment

Revenues were $53.9 million compared to $46.1 million in the prior year period, an increase of 16.8%, primarily resulting from increased sales volume, pricing and favorable foreign exchange.

Operating income was $5.9 million compared to $5.2 million in the prior year period, an increase of 13.7%. The increase in operating income was primarily attributable to increased sales volume and pricing, partially offset by startup costs related to new facilities.

Aftermarket & Accessories Segment

Revenues were $34.4 million compared to $37.1 million in the prior year period, a decrease of 7.4%, primarily resulting from decreased sales volume.

Operating income was $4.5 million compared to $5.0 million in the prior year period, a decrease of 9.1%. The decrease in operating income was primarily attributable to cost inflation, partially offset by increased pricing.

Industrial Automation Segment

Revenues were $13.0 million compared to $14.1 million in the prior year period, a decrease of 7.8%, primarily due to lower sales volume due to decreased customer demand.

Operating income was $0.7 million compared to an operating loss of $1.0 million in the prior year period. The increase in operating income was primarily attributable to profit reported from the liquidation of certain excess inventories. Adjusted operating income was $0.8 million.

2023 Demand Outlook

According to ACT Research, the 2023 North American Class 8 truck production levels are expected to be at 336,000 units, compared to approximately 315,000 units in 2022. Class 8 estimates from FTR for 2023 are 327,000 units, slightly lower than ACT Research for Class 8 truck builds. Class 5-7 production levels are expected to be at 266,000 units in 2023. The 2024 forecast Class 8 truck builds according to ACT Research is approximately 274,000 units.

According to Transparency Market Research Inc, the global commercial and automotive vehicle wire harness market is growing at approximately 5% per year.

According to Interact Analysis, the Global Off-Highway vehicle market is expected to increase approximately 5% in 2023. Beyond 2023, the Off-Highway vehicle market is expected to grow in the 4-5% range.

According to MacKay and Company, North American aftermarket truck parts are expected to see at least 4% growth in 2023. Compounded annual growth of at least 4% is forecasted for 2023-2027.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Thursday, November 2, 2023, at 10:00 a.m. ET. Management intends to reference the Q3 2023 Earnings Call Presentation during the conference call. To participate, dial (888) 259-6580 using conference code 93330617. International participants dial (416) 764-8624 using conference code 93330617.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (877) 674-7070 using access code 051647 and international callers can dial (416) 764-8692 using access code 051647.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction equipment business, the Company’s prospects in the wire harness, warehouse automation and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

COMMERCIAL VEHICLE GROUP, INC. AND SUBSIDIARIES CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS Three Months and Nine Months Ended September 30, 2023 and 2022 (Unaudited) (Amounts in thousands, except per share amounts)

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Revenues

$

246,687

$

251,412

$

771,590

$

746,635

Cost of revenues

212,763

224,570

664,056

672,531

Gross profit

33,924

26,842

107,534

74,104

Selling, general and administrative expenses

21,476

17,304

64,498

49,955

Operating income

12,448

9,538

43,036

24,149

Other expense

383

1,924

488

2,798

Interest expense

2,614

2,813

8,308

6,892

Loss on extinguishment of debt

—

—

—

921

Income before provision for income taxes

9,451

4,801

34,240

13,538

Provision for income taxes

2,161

1,250

8,110

3,520

Net income

$

7,290

$

3,551

$

26,130

$

10,018

Earnings per Common Share:

Basic

$

0.22

$

0.11

$

0.79

$

0.30

Diluted

$

0.22

$

0.11

$

0.78

$

0.30

Weighted average shares outstanding:

Basic

33,100

32,460

33,010

32,950

Diluted

33,350

32,922

33,408

33,645

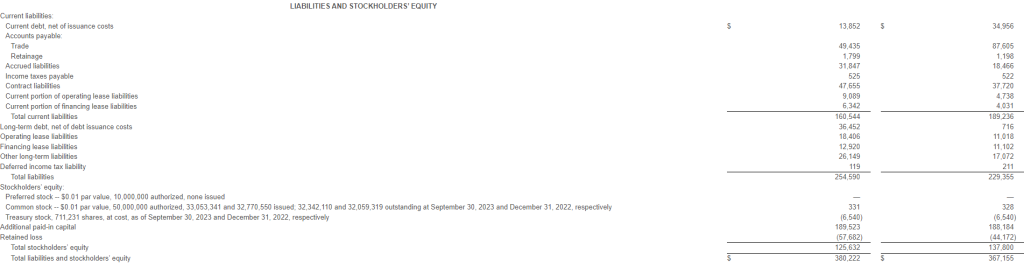

COMMERCIAL VEHICLE GROUP, INC. AND SUBSIDIARIES CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited) (Amounts in thousands, except per share amounts)

ASSETS

September 30, 2023

December 31, 2022

Current assets:

Cash

$

46,293

$

31,825

Accounts receivable, net

159,863

152,626

Inventories

128,192

142,542

Other current assets

29,892

12,582

Total current assets

364,240

339,575

Property, plant and equipment, net

71,554

67,805

Intangible assets, net

12,041

14,620

Deferred income taxes

11,181

12,275

Other assets, net

37,026

35,993

Total assets

$

496,042

$

470,268

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities:

Accounts payable

$

105,110

$

122,091

Accrued liabilities and other

52,999

42,809

Current portion of long-term debt and short-term debt

18,331

10,938

Total current liabilities

176,440

175,838

Long-term debt

135,573

141,499

Pension and other post-retirement benefits

9,325

8,428

Other long-term liabilities

28,150

24,463

Total liabilities

$

349,488

$

350,228

Stockholders’ equity:

Preferred stock

$

—

$

—

Common stock

330

328

Treasury stock

(15,322

)

(14,514

)

Additional paid-in capital

263,641

261,371

Retained deficit

(69,465

)

(95,595

)

Accumulated other comprehensive loss

(32,630

)

(31,550

)

Total stockholders’ equity

146,554

120,040

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY

$

496,042

$

470,268

COMMERCIAL VEHICLE GROUP, INC. AND SUBSIDIARIES BUSINESS SEGMENT FINANCIAL INFORMATION (Unaudited) (Amounts in thousands)

Three Months Ended September 30,

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

2023

2022

2023

2022

2023

2022

2023

2022

2023

2022

2023

2022

Revenues

$

145,393

$

154,024

$

53,862

$

46,129

$

34,412

$

37,143

$

13,020

$

14,116

$

—

$

—

$

246,687

$

251,412

Gross profit

17,661

13,839

7,881

6,210

6,605

6,389

1,777

404

—

—

33,924

26,842

Selling, general & administrative expenses

6,761

4,279

2,018

1,055

2,104

1,436

1,087

1,371

9,506

9,163

21,476

17,304

Operating income (loss)

$

10,900

$

9,560

$

5,863

$

5,155

$

4,501

$

4,953

$

690

$

(967

)

$

(9,506

)

$

(9,163

)

$

12,448

$

9,538

Nine Months Ended September 30,

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

2023

2022

2023

2022

2023

2022

2023

2022

2023

2022

2023

2022

Revenues

$

458,707

$

436,966

$

172,236

$

133,350

$

108,870

$

99,530

$

31,777

$

76,789

$

—

$

—

$

771,590

$

746,635

Gross profit

58,035

35,657

26,524

16,857

21,620

13,341

1,355

8,249

—

—

107,534

74,104

Selling, general & administrative expenses

19,609

18,269

6,932

3,998

6,017

4,636

3,588

4,242

28,352

18,810

64,498

49,955

Operating income (loss)

$

38,426

$

17,388

$

19,592

$

12,859

$

15,603

$

8,705

$

(2,233

)

$

4,007

$

(28,352

)

$

(18,810

)

$

43,036

$

24,149

COMMERCIAL VEHICLE GROUP, INC. AND SUBSIDIARIES Appendix A: Reconciliation of GAAP to Non-GAAP Financial Measures (Unaudited) (Amounts in thousands, except per share amounts and percentages)

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Gross profit

$

33,924

$

26,842

$

107,534

$

74,104

Restructuring

70

607

1,443

2,958

Adjusted gross profit

$

33,994

$

27,449

$

108,977

$

77,062

% of revenues

13.8

%

10.9

%

14.1

%

10.3

%

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Operating income (loss)

$

12,448

$

9,538

$

43,036

$

24,149

Restructuring

70

647

1,501

3,387

Deferred consideration purchase accounting

—

103

—

341

Executive transition

—

329

—

329

Total operating income adjustments

70

1,079

1,501

4,057

Adjusted operating income

$

12,518

$

10,617

$

44,537

$

28,206

% of revenues

5.1

%

4.2

%

5.8

%

3.8

%

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Net income

$

7,290

$

3,551

$

26,130

$

10,018

Operating income adjustments

70

1,079

1,501

4,057

Pension settlement

—

1,116

—

1,116

Loss on extinguishment of debt

—

—

—

921

Hryvnia fair value adjustments on forward exchange contracts

—

(153

)

—

98

Adjusted provision for income taxes1

(18

)

(511

)

(375

)

(1,548

)

Adjusted net income

$

7,342

$

5,082

$

27,256

$

14,662

Diluted EPS

$

0.22

$

0.11

$

0.78

$

0.30

Adjustments to diluted EPS

$

—

$

0.04

$

0.04

$

0.14

Adjusted diluted EPS

$

0.22

$

0.15

$

0.82

$

0.44

Reported Tax Provision adjusted for tax effect of special charges at 25%

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Net income

$

7,290

$

3,551

$

26,130

$

10,018

Interest expense

2,614

2,813

8,308

6,892

Provision for income taxes

2,161

1,250

8,110

3,520

Depreciation expense

3,639

3,749

10,615

11,043

Amortization expense

847

851

2,544

2,563

EBITDA

$

16,551

$

12,214

$

55,707

$

34,036

% of revenues

6.7

%

4.9

%

7.2

%

4.6

%

EBITDA adjustments

Restructuring

$

70

$

647

$

1,501

$

3,387

Deferred consideration purchase accounting

—

103

—

341

Loss on extinguishment of debt

—

—

—

921

Hryvnia fair value adjustments on forward exchange contracts

—

(153

)

—

98

Executive transition

—

329

—

329

Pension settlement

—

1,116

—

1,116

Adjusted EBITDA

$

16,621

$

14,256

$

57,208

$

40,228

% of revenues

6.7

%

5.7

%

7.4

%

5.4

%

Three Months Ended September 30, 2023

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

Operating income (loss)

$

10,900

$

5,863

$

4,501

$

690

$

(9,506

)

$

12,448

Restructuring

—

—

—

70

—

70

Adjusted operating income (loss)

$

10,900

$

5,863

$

4,501

$

760

$

(9,506

)

$

12,518

% of revenues

7.5

%

10.9

%

13.1

%

5.8

%

5.1

%

Nine Months Ended September 30, 2023

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

Operating income (loss)

$

38,426

$

19,592

$

15,603

$

(2,233

)

$

(28,352

)

$

43,036

Restructuring

423

8

—

1,070

—

1,501

Adjusted operating income (loss)

$

38,849

$

19,600

$

15,603

$

(1,163

)

$

(28,352

)

$

44,537

% of revenues

8.5

%

11.4

%

14.3

%

(3.7

)%

5.8

%

Three Months Ended September 30, 2022

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

Operating income (loss)

$

9,560

$

5,155

$

4,953

$

(967

)

$

(9,163

)

$

9,538

Restructuring

66

445

136

$

647

Deferred consideration purchase accounting

—

—

—

103

—

103

Executive transition

—

—

—

—

329

329

Adjusted operating income (loss)

$

9,626

$

5,155

$

5,398

$

(728

)

$

(8,834

)

$

10,617

% of revenues

6.2

%

11.2

%

14.5

%

(5.2

)%

4.2

%

Nine Months Ended September 30, 2022

Vehicle Solutions

Electrical Systems

Aftermarket and Accessories

Industrial Automation

Corporate/Other

Total

Operating income (loss)

$

17,388

$

12,859

$

8,705

$

4,007

$

(18,810

)

$

24,149

Restructuring

270

571

1,440

800

306

3,387

Deferred consideration purchase accounting

—

—

—

341

—

341

Executive transition

—

—

—

—

329

329

Adjusted operating income (loss)

$

17,658

$

13,430

$

10,145

$

5,148

$

(18,175

)

$

28,206

% of revenues

4.0

%

10.1

%

10.2

%

6.7

%

3.8

%

Three Months Ended

Nine Months Ended

September 30, 2023

September 30, 2022

September 30, 2023

September 30, 2022

Cash flows from operating activities

$

18,468

$

38,301

$

29,990

$

33,794

Purchases of property, plant and equipment

(6,017

)

(3,925

)

(15,196

)

(12,541

)

Free cash flow

$

12,451

$

34,376

$

14,794

$

21,253

Use of Non-GAAP Measures

This earnings release contains financial measures that are not calculated in accordance with U.S. generally accepted accounting principles (“GAAP”). In general, the non-GAAP measures exclude items that (i) management believes reflect the Company’s multi-year corporate activities; or (ii) relate to activities or actions that may have occurred over multiple or in prior periods without predictable trends. Management uses these non-GAAP financial measures internally to evaluate the Company’s performance, engage in financial and operational planning and to determine incentive compensation.

Management provides these non-GAAP financial measures to investors as supplemental metrics to assist readers in assessing the effects of items and events on the Company’s financial and operating results and in comparing the Company’s performance to that of its competitors and to comparable reporting periods. The non-GAAP financial measures used by the Company may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies.

The non-GAAP financial measures disclosed by the Company should not be considered a substitute for, or superior to, financial measures calculated in accordance with GAAP. The financial results calculated in accordance with GAAP and reconciliations to those financial statements set forth above should be carefully evaluated.

NEW ALBANY, Ohio, October 30, 2023 (Newswire.com) – Commercial Vehicle Group (CVG) (NASDAQ:CVGI), a global leader in the design and manufacturing of electrical systems, mechanical components, and vehicle accessories, announced today that Corinne Ross has been appointed President, Aftermarket & Accessories. Ross will oversee CVG’s global aftermarket and accessories business segment.

Ross comes to CVG after 16 years with German-based Freudenberg Sealing Technologies, a leading sealing technology company, where she served as Vice President, Corteco North America, Aftermarket Division. In that role, she led regional sales; marketing; supply chain management and operations; and product development and category

management. She began her career in human resources and served in a variety of HR roles of increasing responsibility in both corporate and manufacturing environments.

Ross will be responsible for both the strategic development and tactical execution of the annual and long-term business plans for Aftermarket & Accessories. She will lead the development and execution of commercial, operational, and product management strategies and action plans, and she will work closely with customers and focus on new business development. Ross will also have oversight of product innovation, design, development, and planning activities for the entire Aftermarket product portfolio.

“Corinne is a strong strategic leader who brings a unique blend of business and product aptitude, customer centricity, a big-picture vision and the ability to deliver results,” said Bob Griffin, Interim President and CEO and Chairman of the Board at CVG. “I am confident that she will be a strong strategic thought partner to our executive leadership team.”

“The Aftermarket business is poised for global growth with great potential for additional sales of existing and new products,” said Corinne. “I am excited to join CVG and accelerate growth in the Aftermarket segment.”

Ross holds a bachelor’s degree in business management and an MBA, both from the University of Findlay.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating 3Q23 Estimates. On the heels of Orion Group’s release late last week, we are adjusting our third quarter 2023 projections for Great Lakes downward. On its earnings call, Orion management noted the ongoing sluggishness in Army Corps of Engineers dredging awards. As a result, competition for business has increased. We suspect Great Lakes has been impacted to some degree by the market conditions.

Updated Projections. On the revenue side, we are lowering our estimate to $137 million from a prior $145 million. With reduced utilization, we also are decreasing our gross margin estimate. Net net, our projected quarterly net loss projection is now $6 million, or a loss of $0.09 per share, compared to a previous estimated loss of $3.0 million, or a loss of $0.04 per share. Our adjusted EBITDA estimate declines to $8 million from $11.5 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

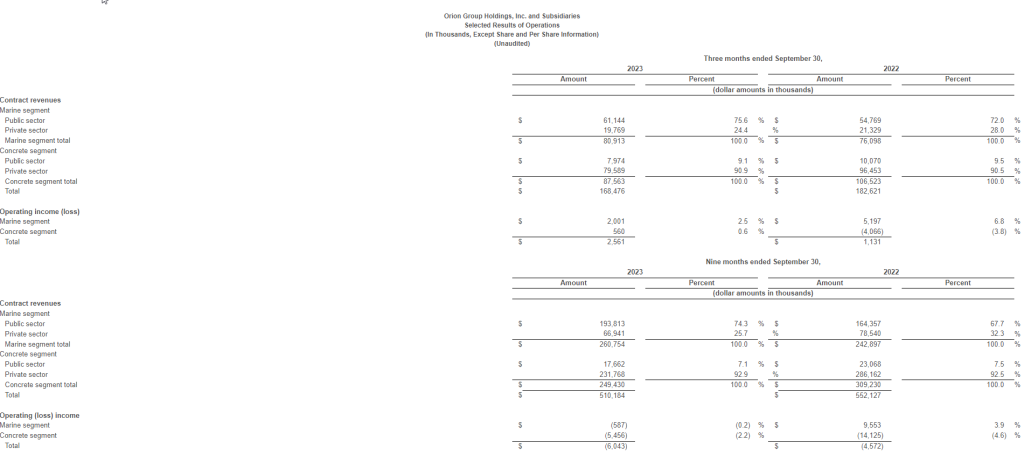

Momentum. While top line in the third quarter was impacted by a more measured pace of award roll-out and the withdrawal from the Central Texas market, operating momentum continued, driven by implementation of management’s operating plan and an increasing mix of higher margin projects. We expect the momentum to continue going forward.

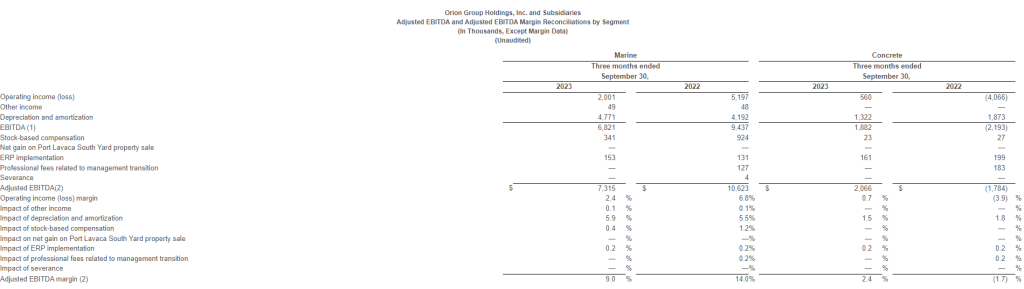

Marine Segment. Marine segment revenue was up 6.3% y-o-y driven by the Hawaii contract. Partly due to recognition of outstanding claims in the year-ago quarter, segment operating profit fell to $2.0 million, or a 2.5% margin, from $5.2 million, or a 6.8% margin last year. Orion is winning new awards in the segment at higher margins, but the Army Corps continues to award business at a slower than historical rate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

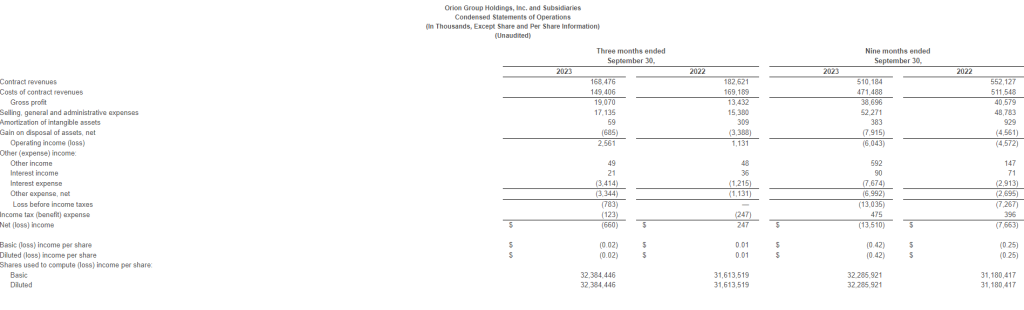

HOUSTON, Oct. 25, 2023 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, today reported its financial results for the third quarter ended September 30, 2023.

Highlights for the quarter ended September 30, 2023:

Contract revenues of $168.5 million

GAAP net loss was $0.7 million or $0.02 per diluted share

Adjusted net income was $0.8 million or $0.02 per diluted share

Adjusted EBITDA was $9.4 million

Signed contract valued over $100 million with Grand Bahama Shipyard Limited (GBSL) for the turnkey design-build of the Grand Bahama Shipyard Dry Dock Replacement Project

Other recently awarded new contracts in both the Concrete and Marine segments for a combined total of approximately $121 million

Backlog and contracts awarded subsequent to quarter end totaled $920 million

See definitions and reconciliation of non-GAAP measures elsewhere in this release.

Management Commentary

“As CFO Scott Thanisch and I marked our first anniversary with Orion, we are incredibly proud of how our people have worked collaboratively to embrace change and deliver positive results,” said Travis Boone, Chief Executive Officer of Orion Group Holdings. “Backlog is a key metric and indicator of the health of the business. As of September 30, backlog stood at $878 million compared with backlog of $549 million in the prior year period. We have won several prestigious projects including the $435 million contract to build a dry dock at Pearl Harbor for the US Navy and a contract valued over $100 million with the Grand Bahama Shipyard Limited (GBSL) for the turnkey design-build of the Grand Bahama Shipyard Dry Dock Replacement Project.”

“Last quarter we told you that we expected continued improvement in profitability through the back half of the year, and we are delivering on that promise. Third-quarter Adjusted EBITDA was $9.4 million versus $3.7 million in the second quarter of 2023. While our third quarter revenue of $169 million is down year-over-year due to our exit from the Central Texas concrete business, the higher quality of our revenue is delivering improved profitability.”

“Since March, our Concrete business has been profitable and improving on an Adjusted EBITDA basis. Adjusted EBITDA margin increased from negative 1.7% to positive 2.4% year-over-year. In addition, the Concrete business was operating income positive on an unconsolidated basis in the third quarter. In Marine, we have a lot of momentum with projects won and potential future projects. There’s a tremendous amount of pent-up demand that we think will be a significant tailwind for us well into 2024 and 2025.”

“As we look ahead to the fourth quarter and beyond, we are optimistic. Our investments in business development are paying off, and we have sufficient capacity and a more disciplined approach to optimize our people and assets. We will see continued improvement in our margins and benefit from operating leverage as we grow the top line. We are excited to build on our success this year and continue growing profitably in 2024,” concluded Boone.

Third Quarter 2023 Results

Contract revenues of $168.5 million decreased 7.7% from $182.6 million in the third quarter last year, primarily due to our decision to exit the unprofitable concrete business in central Texas, partially offset by an increase in marine segment revenue related to the Pearl Harbor, Hawaii drydock project (the “Pearl Harbor Project”).

Gross profit was $19.1 million or 11.3% of revenue up from $13.4 million or 7.4% of revenue in the third quarter of 2022. The increase in gross profit dollars and margin was primarily driven by margin improvements in both segments stemming from higher quality projects and improved execution, partially offset by lower equipment and labor utilization in our dredging business.

Selling, general and administrative (“SG&A”) expenses were $17.1 million, up 11.4% from $15.4 million in the third quarter of 2022. As a percentage of total contract revenues, SG&A expenses increased to 10.2% from 8.5%, primarily due to lower revenues and an increase in SG&A in the third quarter. The increase in SG&A dollars reflected an increase in IT and business development spending and higher legal costs related to customer claims.

Net loss for the third quarter was $0.7 million or $0.02 per diluted share compared to net income of $0.2 million or $0.01 per diluted share in the third quarter of 2022.

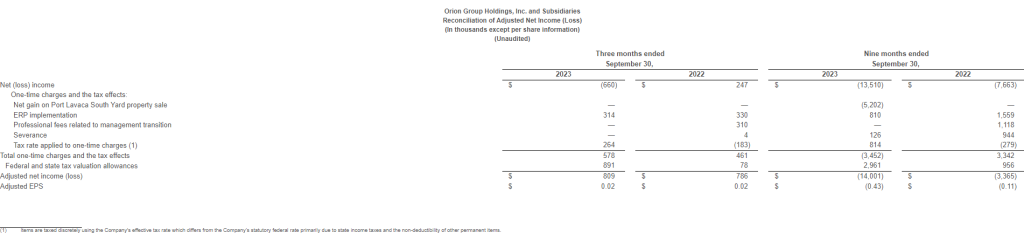

The third quarter 2023 net loss included $1.5 million ($0.04 diluted income per share) of non-recurring items. Third quarter 2023 adjusted net income was $0.8 million ($0.02 diluted income per share).

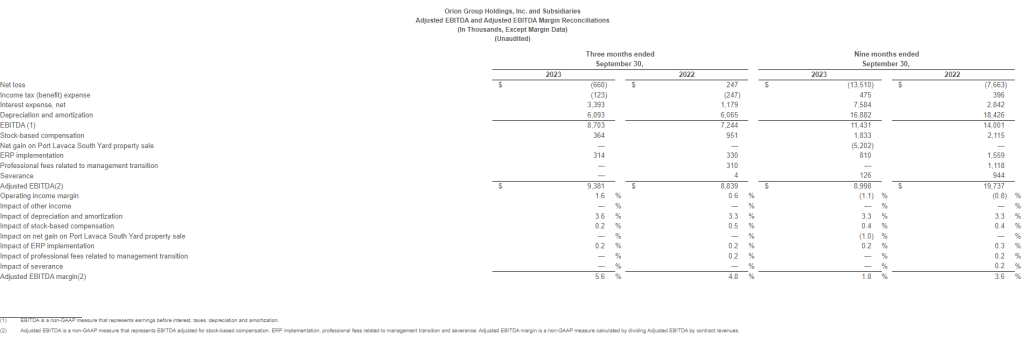

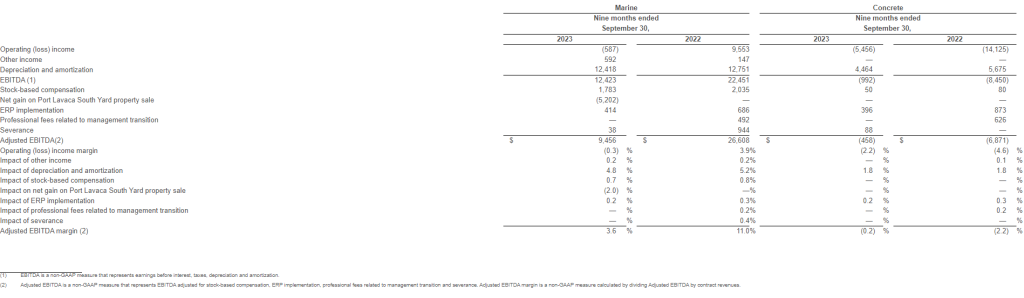

EBITDA for the third quarter of 2023 was $8.7 million, representing a 5.2% EBITDA margin, as compared to EBITDA of $7.2 million, or a 4.0% EBITDA margin in the third quarter last year. Adjusted for non-recurring items, EBITDA for the third quarter of 2023 was $9.4 million, representing a 5.6% adjusted EBITDA margin, as compared to adjusted EBITDA for the third quarter of 2022 of $8.8 million, representing a 4.8% adjusted EBITDA margin.

Backlog

Total backlog at September 30, 2023 was $877.5 million, compared to $818.7 million at June 30, 2023 and $548.6 million at September 30, 2022. Backlog for the Marine segment was $699.9 million, compared to $614.9 million at June 30, 2023 and $280.2 million at September 30, 2022. Backlog for the Concrete segment was $177.6 million, compared to $203.8 million at June 30, 2023 and $268.4 million at September 30, 2022. In addition, the Company has been awarded $43 million in new project work subsequent to the end of the quarter ended September 30, 2022 that is not included in backlog at the end of the quarter.

Recent Wins

On September 22, the Company entered into a design-build contract valued over $100 million for its Marine and Engineering business. The contract was awarded by Grand Bahama Shipyard Limited (GBSL) for the turnkey design-build of the Grand Bahama Shipyard Dry Dock Replacement Project, situated in Grand Bahama, Bahamas. In addition, the Company was recently awarded other new contracts in both its concrete and marine segments for a combined total of approximately $121 million.

Safety Award

Orion Group Holdings, Inc. was presented with the Company Award for Leadership in Safety from the Council of Dredging and Marine Construction Safety (CDMCS). The award, presented at the 2023 CDMCS Annual Awards Dinner in Washington, D.C. on September 28, recognizes outstanding safety leadership in the dredging and marine construction industry.

Orion Group Holdings was recognized for advancing a safety-first culture through safety-conscious policies and procedures in the workplace, mentoring others in safety, training on identifying and properly controlling hazards, and placing high personal value on collaborative and proactive work toward improving safety.

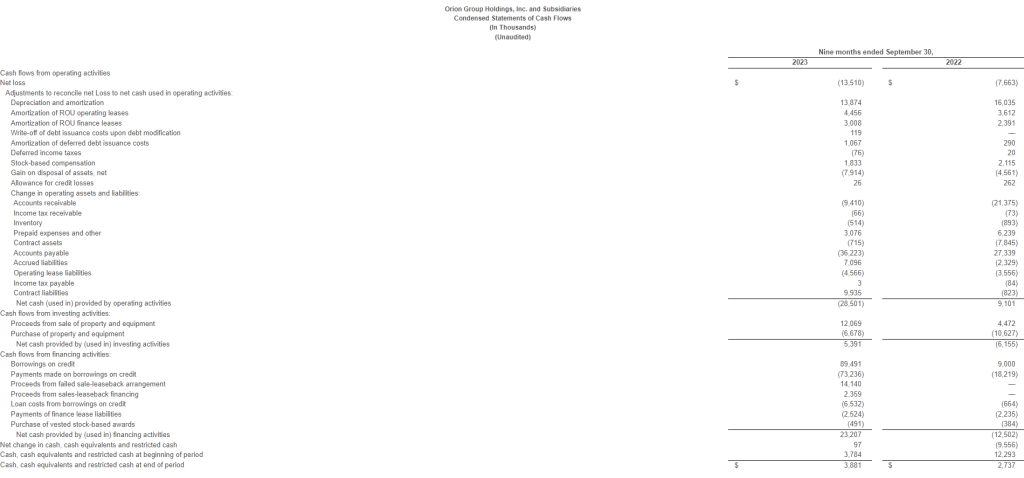

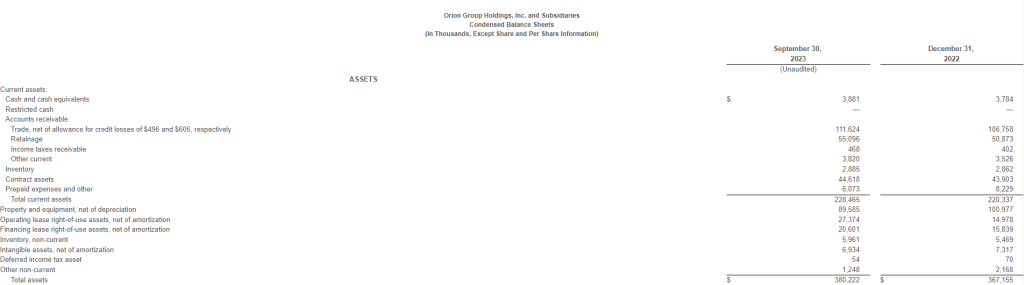

Balance Sheet Update

As of September 30, 2023, current assets were $228.5 million, including unrestricted cash and cash equivalents of $3.9 million. Total debt outstanding as of September 30, 2023 was $50.3 million. At the end of the quarter, the Company had $13.5 million in outstanding borrowings under its revolving credit facility.

Conference Call Details

Orion Group Holdings will host a conference call to discuss results for the third quarter 2023 at 9:00 a.m. Eastern Time/8:00 a.m. Central Time on Thursday, October 26, 2023. To participate, please dial (800) 715-9871 and ask for the Orion Group Holdings Conference Call. A live audio webcast of the call will also be available on the Investor Relations section of Orion’s website at https://www.oriongroupholdingsinc.com/investor/ and will be archived for replay.

About Orion Group Holdings

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Hawaii, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design and specialty services. Its concrete segment provides turnkey concrete construction services including place and finish, site prep, layout, forming, and rebar placement for large commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices throughout its operating areas. The Company’s website is located at: https://www.oriongroupholdingsinc.com.

Backlog Definition

Backlog consists of projects under contract that have either (a) not been started, or (b) are in progress but are not yet complete. The Company cannot guarantee that the revenue implied by its backlog will be realized, or, if realized, will result in earnings. Backlog can fluctuate from period to period due to the timing and execution of contracts. The typical duration of the Company’s projects ranges from three to nine months on shorter projects to multiple years on larger projects. The Company’s backlog at any point in time includes both revenue it expects to realize during the next twelve-month period as well as revenue it expects to realize in future years.

Non-GAAP Financial Measures

This press release includes the financial measures “adjusted net income/loss,” “adjusted earnings/loss per share,” “EBITDA,” “Adjusted EBITDA” and “Adjusted EBITDA margin.” These measurements are “non-GAAP financial measures” under rules of the Securities and Exchange Commission, including Regulation G. The non-GAAP financial information may be determined or calculated differently by other companies. By reporting such non-GAAP financial information, the Company does not intend to give such information greater prominence than comparable GAAP financial information. Investors are urged to consider these non-GAAP measures in addition to and not in substitute for measures prepared in accordance with GAAP.

Adjusted net income/loss and adjusted earnings/loss per share should not be viewed as an equivalent financial measure to net income/loss or earnings/loss per share. Adjusted net income/loss and adjusted earnings/loss per share exclude certain items that management believes impairs a meaningful evaluation of the Company’s financial performance. The Company believes these adjusted financial measures are a useful supplement to earnings/loss calculated in accordance with GAAP because they better inform our common stockholders as to the Company’s operational trends and performance relative to other companies. Generally, items excluded are one-time items or items whose timing or amount cannot be reasonably estimated. Accordingly, any guidance provided by the Company generally excludes information regarding these types of items.

Orion Group Holdings defines EBITDA as net income/loss before net interest expense, income taxes, depreciation and amortization. Adjusted EBITDA is calculated by adjusting EBITDA for certain items that management believes impairs a meaningful comparison of operating results. Adjusted EBITDA margin is calculated by dividing Adjusted EBITDA for the period by contract revenues for the period. The GAAP financial measure that is most directly comparable to EBITDA and Adjusted EBITDA is net income, while the GAAP financial measure that is most directly comparable to Adjusted EBITDA margin is operating margin, which represents operating income divided by contract revenues. EBITDA, Adjusted EBITDA and Adjusted EBITDA margin are used internally to evaluate current operating expense, operating efficiency, and operating profitability on a variable cost basis, by excluding the depreciation and amortization expenses, primarily related to capital expenditures and acquisitions, and net interest and tax expenses. Additionally, EBITDA, Adjusted EBITDA and Adjusted EBITDA margin provide useful information regarding the Company’s ability to meet future debt service and working capital requirements while providing an overall evaluation of the Company’s financial condition. In addition, EBITDA is used internally for incentive compensation purposes. The Company includes EBITDA, Adjusted EBITDA and Adjusted EBITDA margin to provide transparency to investors as they are commonly used by investors and others in assessing performance. EBITDA, Adjusted EBITDA and Adjusted EBITDA margin have certain limitations as analytical tools and should not be used as a substitute for operating margin, net income, cash flows, or other data prepared in accordance with GAAP, or as a measure of the Company’s profitability or liquidity.

Forward-Looking Statements

The matters discussed in this press release may constitute or include projections or other forward-looking statements within the meaning of the “safe harbor” provisions of Section 27A of the Securities Exchange Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, of which provisions the Company is availing itself. Certain forward-looking statements can be identified by the use of forward-looking terminology, such as ‘believes’, ‘expects’, ‘may’, ‘will’, ‘could’, ‘should’, ‘seeks’, ‘approximately’, ‘intends’, ‘plans’, ‘estimates’, or ‘anticipates’, or the negative thereof or other comparable terminology, or by discussions of strategy, plans, objectives, intentions, estimates, forecasts, outlook, assumptions, or goals. In particular, statements regarding future operations or results, including those set forth in this press release, and any other statement, express or implied, concerning future operating results or the future generation of or ability to generate revenues, income, net income, gross profit, EBITDA, Adjusted EBITDA, Adjusted EBITDA margin, or cash flow, including to service debt, and including any estimates, forecasts or assumptions regarding future revenues or revenue growth, are forward-looking statements. Forward-looking statements also include project award announcements, estimated project start dates, anticipated revenues, and contract options which may or may not be awarded in the future. Forward-looking statements involve risks, including those associated with the Company’s fixed price contracts that impacts profits, unforeseen productivity delays that may alter the final profitability of the contract, cancellation of the contract by the customer for unforeseen reasons, delays or decreases in funding by the customer, levels and predictability of government funding or other governmental budgetary constraints, and any potential contract options which may or may not be awarded in the future, and are at the sole discretion of award by the customer. Past performance is not necessarily an indicator of future results. In light of these and other uncertainties, the inclusion of forward-looking statements in this press release should not be regarded as a representation by the Company that the Company’s plans, estimates, forecasts, goals, intentions, or objectives will be achieved or realized. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company assumes no obligation to update information contained in this press release whether as a result of new developments or otherwise, except as required by law.

Please refer to the Company’s 2022 Annual Report on Form 10-K, filed on March 16, 2023, which is available on its website at www.oriongroupholdingsinc.com or at the SEC’s website at www.sec.gov, for additional and more detailed discussion of risk factors that could cause actual results to differ materially from our current expectations, estimates or forecasts.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third Quarter Results. Revenue for Orion was $168.5 million, a 7.7% decrease from $182.6 million last year reflecting the exit of the Central Texas concrete market. Adjusted net income for the quarter was $0.8 million, or diluted EPS of $0.02, flat with last year. Adjusted EBTIDA was $9.4 million compared to $8.8 million in the previous year.

Better Margins. Although revenue decreased year-over-year, Orion showcased better margin improvement in its gross and adjusted EBITDA margins through taking higher quality projects and better execution. Gross margin improved to 11.3% from 7.4% last year and adjusted EBITDA to 5.6% from 4.8%. We believe margin improvement can continue as the Company further implements its current strategy and executes it, and puts another feather in the Company’s cap heading into the new year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Key Metrics. Yesterday, DLH Holdings released some key metrics for the fiscal year ended September 30, 2023. The Company expects to release full audited financial results on December 6th. We will update our models following the full release.

Revenue. The preliminary 4Q23 revenue estimate is $100 million, which would be below our $103 million estimate and the $104 million consensus estimate, up from $67.2 million in 4Q22. The increase was driven by the GRSi acquisition. The legacy contract portfolio grew modestly. We believe the slow roll out of work under recently won ID/IQs negatively impacted quarterly revenue growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.