Research News and Market Data on HMENF

Vancouver, British Columbia–(Newsfile Corp. – November 21, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the three and nine months ended September 30, 2024, declare a quarterly dividend payment to shareholders, and provide an operations update.

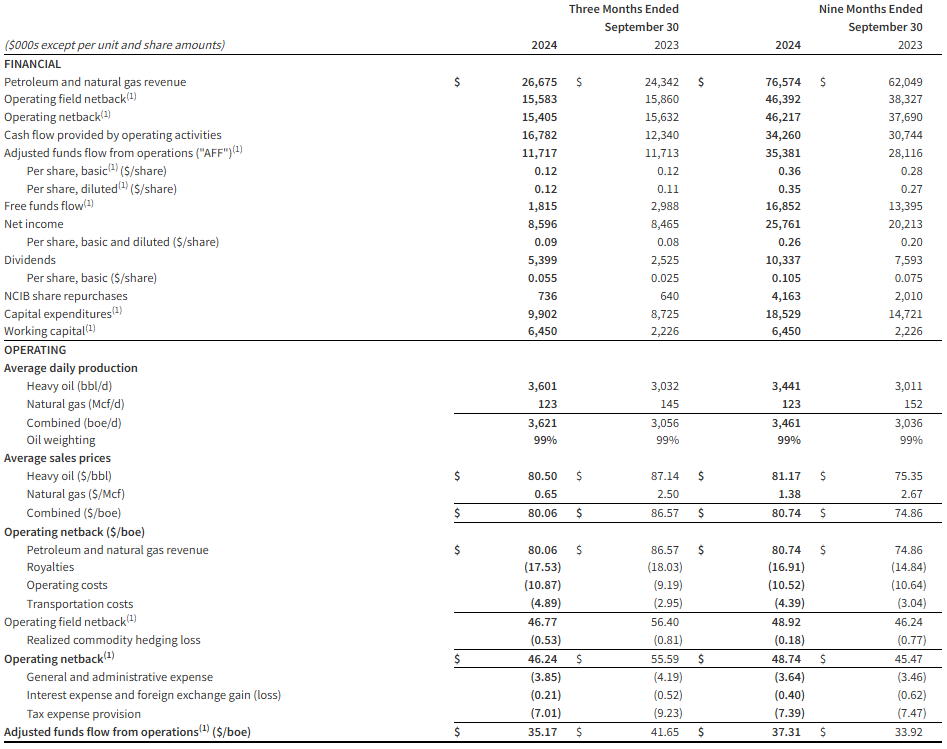

Q3 2024 Highlights

- Achieved quarterly production of 3,621 boe/d (99% heavy oil), an 18% increase over the same quarter last year.

- Attained quarterly revenue of $26.7 million, a 10% increase from the third quarter of 2023.

- Delivered operating netback1 of $15.4 million or $46.24/boe for the quarter.

- Realized quarterly adjusted funds flow from operations (“AFF”)1 of $11.7 million or $35.17/boe.

- Executed a $9.9 million capital expenditure program to drill eight successful wells in Atlee Buffalo, Alberta and construct a new multi-well battery and polymer injection facility in Marsden, Saskatchewan.

- Exited the third quarter with a positive working capital1 position of $6.5 million.

- Paid a special dividend of $2.9 million ($0.03/share) to shareholders on July 26, 2024.

- Paid a quarterly base dividend of $2.5 million ($0.025/share) to shareholders on September 13, 2024.

- Announced a special dividend of $0.03/share to shareholders that was paid subsequent to the quarter on October 25, 2024.

- Renewed the Company’s Normal Course Issuer Bid (“NCIB”).

- Purchased and cancelled 756,400 shares under the Company’s NCIB.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditures, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited consolidated interim financial statements and related notes, and the Management’s Discussion and Analysis for the three and nine months ended September 30, 2024 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Financial and Operating Summary

Quarterly Dividend and Shareholder Return

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 27, 2024 to shareholders of record as of the close of business on December 13, 2024. The dividend is designated as an eligible dividend for income tax purposes.

A minimum of $21 million is anticipated to be returned to Hemisphere’s shareholders in 2024, inclusive of $9.8 million in quarterly base dividends, $5.9 million in two special dividends, and $5.3 million in NCIB share repurchases and cancellations. Based on the Company’s current market capitalization of $179 million (97.5 million shares issued and outstanding at market close price of $1.84 per share on November 20, 2024), this represents an annualized yield of 11.7% to Hemisphere’s shareholders.

Operations Update

Hemisphere’s polymer floods in Atlee Buffalo continue to perform well, with third quarter production up 18% from the same period of 2023. During the third quarter of 2024, Hemisphere drilled eight new horizontal wells into its Atlee Buffalo pools, of which three are in the F pool and five in the G pool. All but one of these wells were brought online subsequent to the end of the quarter, although at least two will ultimately be converted into injectors to continue to build reservoir pressure and sweep oil to producers in the pool.

The Company is currently adding another treater to its G pool battery to handle the additional volumes from these wells. At the same time, vessel inspection and overall maintenance is being completed across the G pool battery. Due to this downtime, management anticipates lower corporate production during the first half of the fourth quarter, with overall expectations for annual 2024 production to be in line with guidance.

In its Marsden, Saskatchewan property, Hemisphere continues to evaluate its new polymer pilot project and is awaiting source well regulatory approval in order to increase injection rates. At this time no significant production is budgeted from the area.

The Hemisphere team is currently working on development plans for next year and expects to release details on its 2025 guidance in January.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, low decline conventional heavy oil assets through polymer flood enhanced recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer

Telephone: (604) 685-9255

Email: info@hemisphereenergy.ca

Website: www.hemisphereenergy.ca

Forward-looking Statements

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a quarterly dividend will be paid December 27, 2024 to shareholders of record as of the close of business on December 13, 2024; that a minimum of $21 million is anticipated to be returned to shareholders in 2024; that at least two of Hemisphere’s new wells will be converted into injectors; that management anticipates lower corporate production during the first half of the fourth quarter, with overall expectations for annual 2024 production to fall in line with guidance; and that Hemisphere expects to release details on its 2025 guidance in January.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the perspectivity of recently acquired properties and the timing and manner to explore and develop the same; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, free funds flow, capital expenditures, operating field netback, operating netback, and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered more meaningful than IFRS measures in evaluating the Company’s performance.

a) Adjusted funds flow from operations (“AFF”) (Non-IFRS Financial Measure and Ratio if calculated on a per share or boe basis): The Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period.

Click Here for Full Report