Anfield Energy Inc. (TSX.V: AEC; NASDAQ: AEC; FRANKFURT: 0AD) announced it has entered into a definitive agreement to acquire BRS Inc., a Wyoming-based engineering and consulting firm specializing in uranium and vanadium projects. The transaction represents a strategic step toward strengthening Anfield’s internal technical capabilities as the company advances its portfolio toward near-term production.

BRS has served as a long-standing technical partner to Anfield since 2014, providing engineering, geology, mine development, and construction management services across multiple assets. The firm has authored numerous technical reports, Preliminary Economic Assessments (PEAs), and resource updates for projects including Slick Rock, the West Slope Projects, and the Velvet-Wood Mine. By integrating BRS directly into its operations, Anfield aims to streamline project execution while reducing reliance on third-party consultants.

The acquisition brings decades of specialized expertise in uranium exploration, in-situ recovery (ISR), conventional mining, and mill reactivation directly under Anfield’s corporate umbrella. Douglas L. Beahm, founder of BRS and Anfield’s Chief Operating Officer, will continue in his executive role while serving as principal engineer. Beahm is a Qualified Person under NI 43-101 with more than 50 years of experience in uranium resource development, mine operations, and regulatory permitting seen as critical to Anfield’s growth strategy.

From an operational standpoint, the transaction is expected to improve cost efficiency and shorten development timelines across Anfield’s asset base. Internalizing engineering and technical functions allows the company to move more quickly on resource updates, economic studies, permitting applications, and mine planning activities. This is particularly relevant as Anfield continues efforts toward restarting the Shootaring Canyon mill, which anchors its hub-and-spoke development strategy in the U.S.

Beyond operational efficiencies, the acquisition also creates new growth avenues. BRS is expected to expand its external consulting services with the support of a publicly traded platform, potentially offering turnkey development solutions to third-party toll-mill partners. The expanded technical team may also help Anfield identify and evaluate acquisition opportunities more rapidly, supporting resource expansion and portfolio optimization.

The deal terms include total cash consideration of US$5 million paid to Beahm over a two-year period. An initial payment of US$1.5 million will be made at closing, followed by US$1.5 million after the first anniversary and a final US$2 million payment after the second anniversary. No securities will be issued as part of the transaction, and no finder’s fees are payable. Completion of the acquisition remains subject to customary closing conditions and regulatory approvals.

As a related-party transaction under Multilateral Instrument 61-101, the acquisition qualifies for exemptions from formal valuation and minority shareholder approval requirements, as the total consideration does not exceed 25% of Anfield’s market capitalization.

Anfield Energy is a uranium and vanadium development company focused on building a vertically integrated domestic energy fuels platform. The acquisition of BRS marks a meaningful step toward that goal, enhancing internal technical depth while positioning the company to advance its projects more efficiently amid rising demand for U.S.-based uranium supply.

Crude oil prices sank to their lowest levels in nearly four years this week, underscoring how deeply oversupplied the global energy market has become. Both major benchmarks—Brent and West Texas Intermediate (WTI)—fell below key psychological thresholds, with WTI briefly dipping under $55 a barrel and Brent sliding into the high $50s. The move marks a dramatic reversal from the tight energy markets of recent years and signals mounting pressure across the oil industry.

The selloff reflects what many analysts have been warning about for months: supply has simply outpaced demand. Production growth from OPEC+ and non-OPEC producers alike has overwhelmed consumption, even as global demand remains relatively steady. Since the spring, OPEC+ members have steadily unwound earlier production cuts, adding millions of barrels per day back into the market. Saudi Arabia, in particular, has prioritized regaining market share, even at the expense of lower prices.

Outside the cartel, output has also continued to climb. Producers across parts of the Middle East, Africa, and Asia have increased exports, while U.S. inventories are projected to keep building well into 2026. According to international energy agencies, the imbalance could widen further next year, with excess supply potentially approaching four million barrels per day—an extraordinary figure by historical standards.

One of the clearest signs of the glut is happening offshore. Oil tankers holding crude at sea have surpassed one billion barrels, as sellers struggle to find buyers willing to take delivery at current prices. Storage economics are also shifting, with parts of the oil futures curve slipping into contango. This market structure, where future prices trade above spot prices, typically signals oversupply and encourages traders to store oil rather than sell it immediately.

Pressure is spreading beyond crude itself. Refining margins have narrowed as prices for gasoline, diesel, and jet fuel soften alongside oil. Crack spreads—which measure the profitability of turning crude into refined products—have tightened, removing one of the last pillars of support for energy prices earlier this year.

Wall Street remains firmly bearish. Several major banks now expect oil prices to remain under pressure through 2026, with forecasts clustering in the low-to-mid $50 range and downside risks extending even further. Some analysts warn that if producers fail to curb output, prices could fall into the $40s, levels that would strain balance sheets across the exploration and production sector.

Geopolitics adds another layer of complexity. Sanctions on Russian producers could limit some supply, but discounted barrels often find their way to buyers willing to navigate restrictions. Meanwhile, any breakthrough in peace talks between Russia and Ukraine could ultimately bring more oil back onto the global market, worsening the surplus. Tensions involving Venezuela and U.S. policy decisions also remain wild cards, though none appear strong enough to offset the sheer volume of excess supply.

For energy companies, the implications are sobering. Lower prices threaten drilling activity, investment, and employment, particularly in high-cost regions. While central bank rate cuts and a weaker dollar typically support commodities, oil’s current trajectory is being driven less by macro policy and more by fundamentals. For now, the message from the market is clear: until supply comes back into balance, oil prices are likely to stay under pressure.

Vancouver, British Columbia–(Newsfile Corp. – December 15, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) announces that its Board of Directors has approved grants of incentive restricted share units (“RSU”) and stock options.

Restricted Share Units

Under the Company’s Restricted Share Unit Plan (the “Plan”), RSUs may be granted to directors, employees, and contractors of the Company. At the discretion of the Company’s Board of Directors, the Plan permits the Company to either redeem RSUs for cash or by issuance of Hemisphere’s common shares.

On December 12, 2025, the Company awarded 930,000 incentive RSUs to directors and officers of Hemisphere, all of which will vest one-third annually over a three-year period and will expire on December 15, 2028.

Stock Options

Additionally, in accordance with the Company’s Stock Option Plan, Hemisphere has granted 48,000 incentive stock options to its investor relations service provider on December 15, 2025 at an exercise price of $2.01 per share which will vest quarterly over 12 months and expire on December 15, 2030.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

CALGARY, AB, Dec. 1, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on December 31, 2025, to shareholders of record at the close of business on December 15, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter financial results. Hemisphere reported revenue of C$23.1 million in Q3, down from C$26.7 million in the prior-year period, but slightly above our estimate of C$21.6 million, due to better-than-expected pricing. Net income totaled C$6.9 million, or C$0.07 per share, compared to C$8.6 million, or C$0.09 per share, last year, and in line with our forecast of C$6.9 million, or C$0.07 per share. Average daily production of 3,571 boe/d (99% heavy oil) declined 1% year-over-year due to summer workover downtime, but wasn’t far off from our estimate of 3,606 boe/d. Adjusted funds flow (AFF) from operations was C$10.1 million, or C$0.10 per share, roughly in line with our estimate of C$10.0 million, or C$0.10 per share.

Updating estimates. Reflecting slightly better than expected Q3 results but modestly lower 2025 production guidance of 3,600–3,700 boe/d, we are adjusting our full-year forecasts. We now expect 2025 revenue of C$92.7 million, compared to our prior estimate of C$93.7 million. Our operating cost assumption increased modestly to C$38.1 million from C$37.9 million. We now project 2025 net income of C$26.5 million, or C$0.27 per share, versus our previous forecast of C$27.4 million, or C$0.27 per share. AFF is projected at C$40.0 million, up from our earlier estimate of C$41.0 million. For 2026, we are holding our forecast steady with revenue of C$93.7 million, net income of C$27.7 million, or C$0.29 per share, and AFF of C$39.7 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

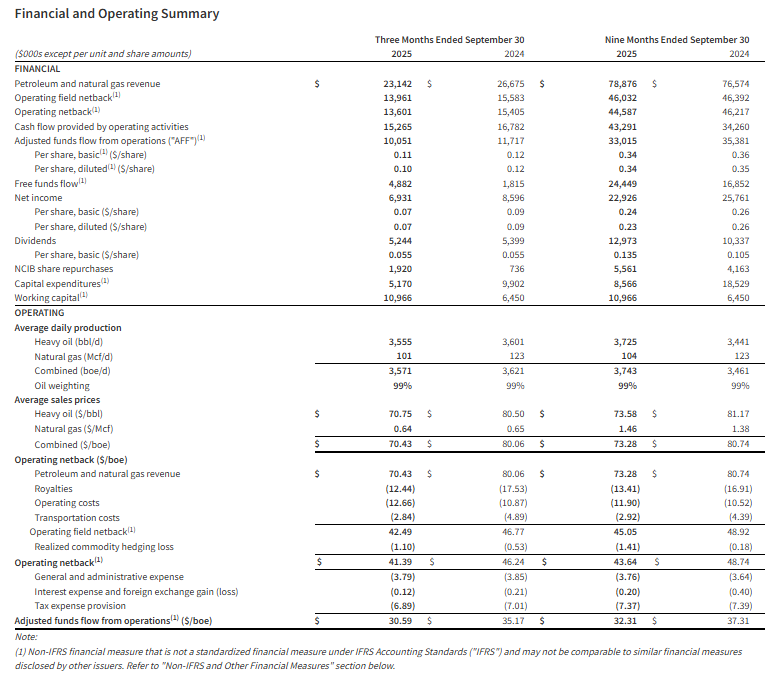

Vancouver, British Columbia–(Newsfile Corp. – November 25, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the three and nine months ended September 30, 2025, declares a quarterly dividend payment to shareholders, and provides an operations update.

Q3 2025 Highlights

Attained quarterly production of 3,571 boe/d (99% heavy oil).

Generated quarterly revenue of $23.1 million.

Achieved total operating and transportation costs of $15.50/boe.

Delivered operating netback1 of $13.6 million or $41.39/boe for the quarter.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.1 million or $30.59/boe.

Initiated a 2025 fall drilling program with $5.2 million in capital expenditures1.

Generated quarterly free funds flow1 of $4.9 million.

Exited the third quarter with a positive working capital1 position of $11.0 million.

Paid a special dividend of $2.9 million ($0.03/share) to shareholders on August 15, 2025.

Paid a quarterly base dividend of $2.4 million ($0.025/share) to shareholders on September 12, 2025.

Purchased and cancelled 1.0 million shares for $1.9 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Renewed the Company’s NCIB.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditures, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited condensed interim consolidated financial statements and related notes, and the Management’s Discussion and Analysis for the three and nine months ended September 30, 2025 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 30, 2025 to shareholders of record as of the close of business on December 9, 2025. The dividend is designated as an eligible dividend for income tax purposes.

With the payment of the fourth quarter dividend, Hemisphere anticipates returning a minimum of $21.6 million to shareholders in 2025, including $9.6 million in quarterly base dividends, $5.8 million in two special dividends, and $6.2 million through NCIB share repurchases and cancellations. Based on the Company’s current market capitalization of $205 million (94.6 million shares issued and outstanding at a market close price of $2.17 per share on November 24, 2025), this represents an annualized yield of 10.5% to Hemisphere’s shareholders.

Operations Update

During the third quarter of 2025, Hemisphere’s production averaged 3,571 boe/d (99% heavy oil), representing a slight decrease of approximately 1% from the same period in 2024. The Company completed a number of workovers during the summer months, which contributed to production downtime during the quarter. However, September production of approximately 3,800 boe/d (99% heavy oil) was back in line with average levels of 3,830 boe/d (99% heavy oil) during the first six months of the year. This performance highlights the stability and low-decline characteristics of Hemisphere’s polymer flood assets in Atlee Buffalo, particularly given that no new wells had been placed on production since the Company’s third-quarter drilling program in 2024.

Throughout 2025, Hemisphere has taken a cautious approach to capital spending amid volatility in the global economy and oil markets, which resulted in delaying its drilling program until later in the year. In September the Company commenced a fall drilling program, which finished in early November. The new wells have just recently been put on production and will continue to be optimized over the coming months.

In October, Hemisphere successfully completed a scheduled facility turnaround and resolved unexpected issues with its power generation and injection systems. Although this short-term disruption will affect overall fourth-quarter production, all systems are now fully operational. November production has averaged approximately 3,800 boe/d (99% heavy oil, field estimate from November 1-22, 2025). Management anticipates fourth-quarter production will range between 3,400 – 3,500 boe/d (99% heavy oil) following this outage.

At the Company’s Marsden, Saskatchewan property, Hemisphere is continuing to evaluate its polymer pilot project. It has been approximately one year since injection commenced, and while an oil production response has not yet been noted, the data being collected is providing insights into reservoir performance. The Hemisphere team plans to advance its pilot project by evaluating the potential effects of producer/injector well spacing, polymer type and injection water, as well as reservoir heterogeneity and composition.

During its fall drilling program, Hemisphere attempted to test a second oil-bearing zone within its Marsden landbase. Unfortunately, drilling challenges prevented Hemisphere from being able to access the reservoir, and the Company is reviewing alternatives for future evaluation of the prospect.

Management anticipates WTI oil prices will average close to US$65 per barrel in 2025 and expects to exceed Hemisphere’s adjusted funds flow guidance estimate of $40 million for this price scenario, while projecting total capital expenditures to be on budget. This outlook holds despite the Company deferring its drilling program until late in the third quarter and experiencing unscheduled production downtime in the second half of the year. As a result, Hemisphere now estimates average annual 2025 production will be approximately 3,600 – 3,700 boe/d (99% heavy oil), compared to its original guidance of 3,900 boe/d (99% heavy oil).

The Company expects to release details on its 2026 guidance in January as part of its forward development planning. Supported by approximately $11 million in working capital, an undrawn credit facility, and strong cash flow from its low-decline production base, Hemisphere is well positioned with a robust balance sheet to pursue potential acquisition opportunities while continuing to deliver shareholder returns.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Ovintiv Inc. (NYSE: OVV) announced a major portfolio transformation on Tuesday, unveiling an agreement to acquire Canadian producer NuVista Energy Ltd. for approximately $2.7 billion (C$3.8 billion) while simultaneously preparing to divest its Anadarko assets in 2026. The twin moves signal a renewed strategic focus on high-return oil and gas production in North America’s Montney region.

Under the deal, Ovintiv will purchase all outstanding NuVista shares not already owned, paying C$18.00 per share in a mix of 50% cash and 50% stock. Ovintiv previously acquired a 9.6% stake in NuVista in a private transaction at C$16 per share. Upon completion, NuVista shareholders will own about 10.6% of the combined company.

The acquisition adds roughly 140,000 net acres—70% of which remain undeveloped—and 100,000 barrels of oil equivalent per day (MBOE/d) of production in Alberta’s oil-rich Montney play. The deal also expands Ovintiv’s drilling inventory by 930 potential well locations, including 620 “premium” sites with projected internal rates of return above 35% at $55 oil.

“This transaction boosts our free cash flow per share by acquiring top-decile rate-of-return assets in the heart of the Montney oil window,” said Brendan McCracken, Ovintiv’s President and CEO. “The NuVista assets were identified as among the highest-value undeveloped oil resources in North America, offering exceptional fit with our existing operations and infrastructure.”

The transaction will also give Ovintiv access to NuVista’s extensive processing and transportation capacity, including 600 MMcf/d of processing rights and 250 MMcf/d of long-term firm transport to markets outside of AECO. This diversification is expected to reduce Ovintiv’s exposure to AECO natural gas pricing from 30% to 25% by 2026.

Financially, the deal is expected to be immediately accretive across all major performance metrics, including free cash flow, return on capital, and earnings per share. Ovintiv anticipates roughly $100 million in annual cost synergies, primarily through reduced capital and operating costs. The company also emphasized that its balance sheet will remain strong, projecting leverage-neutral outcomes at closing and reaffirming its investment-grade credit profile.

To finance the transaction, Ovintiv plans to use a combination of cash on hand, credit facility borrowings, and a potential term loan. The company has temporarily paused its share buyback program for two quarters to prioritize funding but will maintain its base dividend.

Looking ahead, Ovintiv plans to begin the divestiture of its Anadarko Basin assets in early 2026, with proceeds earmarked for debt reduction. The company expects to reduce net debt below $4 billion by year-end 2026, paving the way for increased share repurchases and enhanced shareholder returns.

By consolidating its position in one of North America’s most productive basins while shedding lower-margin assets, Ovintiv is signaling a clear commitment to efficiency and long-term value creation. Once the transaction closes—expected by the end of Q1 2026 pending shareholder and regulatory approvals—Ovintiv’s Montney production will rise to 400,000 barrels of oil equivalent per day, reinforcing its role as one of the leading integrated energy producers in the region.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating third quarter 2025 estimates. While we are maintaining our third-quarter production forecast of 18,695 barrels of oil equivalent per day (boe/d), we lowered our third-quarter 2025 revenue, adjusted funds flow (AFF), and AFF per share estimates to C$86.8 million, C$28.0 million, and C$1.00, respectively, from C$89.3 million, C$38.9 million, and C$1.39. These changes reflect modestly lower commodity pricing, along with higher royalty costs and operating expenses. We expect third-quarter operating expenses to be elevated due to turnaround activity and downtime associated with the recently completed gas plant expansion.

Revising full-year 2025 estimates. For the full year 2025, we forecast revenue of C$301.9 million, AFF of C$116.3 million, and AFF per share of C$4.71, compared to prior estimates of C$306.7 million, C$131.8 million, and C$5.34. These reductions primarily reflect a weaker pricing environment, partially offset by a modest increase in our full-year production forecast to 16,851 boe/d from 16,800, driven by higher fourth quarter production expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter estimate update. We have trimmed our third-quarter revenue and net income estimates to C$21.6 million and C$6.9 million, respectively, from C$23.5 million and C$7.5 million. Additionally, we have lowered our adjusted funds flow (AFF) and AFF per share estimates to C$10.0 million and C$0.10, respectively, from C$10.7 million and C$0.11.

Full-year estimate changes. For the full year 2025, we project revenues and net income of C$93.7 million and C$27.4 million, respectively, compared to our previous estimates of C$97.7 million and C$29.6 million. Moreover, we have lowered our AFF and AFF per share estimates to C$41.0 million and C$0.41, respectively, from C$43.3 million and C$0.43.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Century produces high-purity lithium hydroxide. Century Lithium produced its first samples of lithium hydroxide from lithium carbonate derived from Angel Island’s lithium claystone deposit and treated at its demonstration plant using the company’s patent-pending alkaline leach and direct lithium extraction (DLE) process. Century had previously focused on making lithium carbonate. By producing high-purity lithium hydroxide, Century has demonstrated an ability to produce another major lithium product for the domestic market.

Pursuing a direct lithium conversion process. Lithium hydroxide samples were produced onsite in a batch process using conventional liming conversion with calcium hydroxide to produce lithium hydroxide with a purity level of 99.5% or greater. Century is pursuing a direct lithium conversion (DLC) process to produce lithium hydroxide directly from lithium chloride solution, which would bypass producing lithium carbonate in an intermediate stage to simplify the process and reduce energy consumption and operating costs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Deal positions Bloom as a preferred power provider for Brookfield’s global AI factories and marks Brookfield’s first investment in its dedicated AI Infrastructure strategy

Shares of Bloom Energy (NYSE: BE) surged more than 20% in early trading Monday after the company announced a $5 billion strategic partnership with Brookfield Asset Management (NYSE: BAM, TSX: BAM) to develop and power next-generation AI infrastructure.

Under the agreement, Brookfield will invest up to $5 billion to deploy Bloom’s advanced fuel cell technology as the companies collaborate on the design and construction of “AI factories” — large-scale data centers purpose-built to meet the surging compute and energy demands of artificial intelligence. Bloom Energy will serve as Brookfield’s preferred onsite power provider for these facilities worldwide.

The partnership marks the first phase of a joint AI infrastructure vision and represents Brookfield’s inaugural investment through its newly established AI Infrastructure strategy, which focuses on power, compute, and capital integration for AI data centers. The two companies plan to announce their first European site before the end of the year.

“AI infrastructure must be built like a factory — with purpose, speed, and scale,” said KR Sridhar, Founder, Chairman and CEO of Bloom Energy. “AI factories demand massive power, rapid deployment and real-time responsiveness that legacy grids cannot support. Together with Brookfield, we’re creating a new blueprint for powering AI at scale.”

“Behind-the-meter power solutions are essential to closing the grid gap for AI factories,” added Sikander Rashid, Global Head of AI Infrastructure at Brookfield. “Bloom’s advanced fuel cell technology gives us the unique capability to design and construct modern AI factories with a holistic and innovative approach to power needs.”

A Blueprint for the AI Era

AI data centers are projected to require over 100 gigawatts of power in the U.S. alone by 2035, according to industry estimates. Bloom Energy’s solid oxide fuel cells generate electricity through chemical reactions rather than combustion, providing clean, resilient, and rapidly deployable onsite power — an attractive alternative to traditional grid dependency.

Bloom has already installed hundreds of megawatts of fuel cell systems supporting data centers for American Electric Power, Equinix, and Oracle. The company’s systems can be scaled modularly, reducing construction timelines and improving energy efficiency for high-demand AI applications.

Brookfield, one of the world’s largest alternative asset managers with over $1 trillion in assets under management, has been expanding aggressively into digital and energy infrastructure. Recent commitments include $9.98 billion to develop an AI data center in Sweden and €20 billion for AI projects in France. The firm also holds major stakes in Compass Datacenters, Duke Energy Florida, Colonial Enterprises, and Hotwire Communications, and recently inked a deal to supply Google with up to 3 GW of hydro power in the U.S.

Strategic Implications

The partnership underscores a growing convergence between energy technology and AI infrastructure. As the global race to build AI data centers accelerates, the need for reliable, low-carbon power sources has become a critical bottleneck. Brookfield’s capital and infrastructure expertise, combined with Bloom’s clean power solutions, could provide a scalable model for sustainable AI expansion.

For Bloom Energy, the partnership offers both near-term revenue visibility and long-term positioning at the center of AI-driven energy demand growth. For Brookfield, it establishes a strategic foothold in the AI ecosystem— one that aligns with its global energy transition and infrastructure investment priorities.

Transaction strengthens IsoEnergy’s top-tier uranium portfolio with Toro’s flagship Wiluna Project and expands presence in key global jurisdictions amid rising nuclear demand

IsoEnergy Ltd. (NYSE American: ISOU) and Toro Energy Ltd. (ASX: TOE) have entered into a scheme implementation deed under which IsoEnergy will acquire all issued and outstanding ordinary shares of Toro. The all-stock transaction will create a globally diversified uranium developer with significant resources and near-term production potential across Canada, the United States, and Australia.

Under the terms of the agreement, Toro shareholders will receive 0.036 IsoEnergy shares for each Toro share held, representing a 79.7% premium to Toro’s last traded price and a 92.2% premium to its 20-day volume-weighted average price (VWAP). Upon completion, IsoEnergy and Toro shareholders will own approximately 92.9% and 7.1%, respectively, of the combined company on a fully diluted basis. The deal values Toro at approximately AUD 75 million (CAD 68 million / USD 49 million) and is expected to close in the first half of 2026, subject to shareholder and regulatory approvals.

A Strengthened Uranium Platform

The merger will add Toro’s Wiluna Uranium Project in Western Australia — comprising the Centipede-Millipede, Lake Way, and Lake Maitland deposits — to IsoEnergy’s existing portfolio, which includes the ultra-high-grade Hurricane deposit in Canada’s Athabasca Basin, several past-producing U.S. uranium mines, and other exploration assets across North America and Australia.

The combined resource base will include:

55.2 million pounds U₃O₈ (M&I) and 4.9 million pounds U₃O₈ (Inferred) compliant under NI 43-101

78.1 million pounds U₃O₈ (M&I) and 34.6 million pounds U₃O₈ (Inferred) compliant under JORC standards

Historical resources totaling 154.3 million pounds U₃O₈ (M&I) and 88.2 million pounds U₃O₈ (Inferred)

This creates one of the largest and most geographically diversified uranium portfolios among mid-tier developers.

Strategic and Market Rationale

The merger comes amid growing confidence in the uranium market’s long-term outlook. The World Nuclear Association’s 2025 Fuel Report projects uranium demand to rise roughly 30% by 2030 and more than double by 2040. IsoEnergy’s expanded scale and jurisdictional diversification position it to capture value from this structural supply-demand imbalance.

Australia, home to the Wiluna Project, ranks #1 globally for uranium resources and is among the Top 5 producers worldwide. Western Australia is emerging as a key uranium jurisdiction alongside Cameco’s Kintyre and Yeelirrie projects and Deep Yellow’s Mulga Rock development.

“The acquisition of Toro Energy marks another important step in advancing IsoEnergy’s strategy to build a globally diversified, development-ready uranium platform,” said Philip Williams, CEO and Director of IsoEnergy. “The Wiluna Uranium Project strengthens our portfolio with a large, previously permitted asset in a top-tier jurisdiction at a time when global nuclear demand is accelerating.”

Richard Homsany, Executive Chairman of Toro, added, “This transaction creates significant value for our shareholders and provides an opportunity to participate in a larger, leading uranium company listed on the TSX and NYSE. Toro shareholders will gain exposure to a diverse uranium portfolio with strong growth potential and enhanced access to capital.”

Positioned for Growth

The merged entity will have enhanced balance sheet strength, improved access to global capital markets, and a broader platform for value-accretive growth opportunities across the uranium cycle. Following completion, Toro will be delisted from the Australian Securities Exchange (ASX), while IsoEnergy will remain publicly traded in Toronto and New York.

The deal follows IsoEnergy’s previously announced — and later terminated — plan to acquire Anfield Energy in early 2024, reflecting the company’s continued pursuit of strategic, scale-building opportunities in the uranium sector. Major Toro shareholders, including Mega Uranium Ltd. (12.7%) and its associate Mega Redport Pty Ltd., have indicated their intention to vote in favor of the scheme, provided no superior proposal emerges.

Shares of Lithium Americas (NYSE: LAC) soared nearly 100% on Wednesday after reports that the Trump administration is considering taking a stake in the company as part of a renegotiated federal loan package tied to the development of the Thacker Pass lithium mine in Nevada.

According to Reuters, the administration is seeking as much as a 10% equity stake in the Vancouver-based miner. The proposed arrangement comes as Lithium Americas works through terms of a $2.26 billion loan from the Department of Energy, originally granted during the first Trump administration.

Under the current negotiations, the company has offered the government no-cost warrants for up to 10% of its common stock. At the same time, the administration is reportedly pressing General Motors (NYSE: GM) — which owns a 38% stake in Thacker Pass and has invested $625 million — for purchase guarantees that would help shore up demand for the lithium produced at the site. GM shares ticked higher by more than 2% on the news.

A Strategic Lithium Project

Thacker Pass is expected to play a central role in U.S. energy security. Once operational, the project is projected to be the largest lithium mining operation in the Western Hemisphere. Its first production phase, slated for 2028, is forecast to produce more than 40,000 metric tons of lithium carbonate annually — enough to power batteries for roughly 800,000 electric vehicles.

For perspective, Albemarle’s (NYSE: ALB) Silver Peak mine in Nevada, currently the only operating lithium mine in the U.S., produces fewer than 5,000 metric tons per year. This makes Thacker Pass a significant leap in domestic production capacity at a time when global demand for electric vehicles, battery storage, and clean energy technologies is surging.

China currently dominates the global lithium industry, producing more than 40,000 metric tons per year and refining more than 65% of the world’s supply. By comparison, the U.S. refines less than 3%. This imbalance has made lithium one of the most strategically sensitive commodities in the energy transition.

“Lithium is the new oil,” said one energy analyst, noting that securing supply has become a cornerstone of U.S. industrial policy. “Without it, you can’t scale EV adoption or battery storage, and that makes projects like Thacker Pass crucial to long-term energy independence.”

The government’s interest in Lithium Americas follows similar moves to shore up domestic supply chains for other critical materials. In July, MP Materials (NYSE: MP) announced a multibillion-dollar deal with the Department of Defense that made the government its largest shareholder, boosting MP’s stock more than 50%. Meanwhile, Intel (NASDAQ: INTC) has climbed over 25% since talks of a potential government stake in the chipmaker became public.

This pattern underscores the administration’s strategy of leveraging federal investment to reduce reliance on foreign sources of essential resources, from rare earth elements to semiconductors.

Lithium Americas stock traded at $6.09 as of 2:08 p.m. EDT, up more than 98% on the day. The sharp rally comes despite ongoing weakness in lithium prices, which have fallen over the past year amid oversupply from China. Futures for lithium carbonate are down more than 12%, while lithium hydroxide has dropped more than 4.5%.

Those price pressures have raised concerns about the financial viability of large-scale U.S. mining projects. The administration’s involvement could provide a stabilizing force, ensuring that key projects like Thacker Pass remain on track. The first loan draw is expected this month, with construction at the Nevada site already underway.

For now, investors appear to be betting that federal backing — and a potential government equity stake — could cement Lithium Americas’ role as a cornerstone of America’s clean energy future.