Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Family. The saga between Lifeway CEO Julie Smolyansky and her brother, Edward, and mother, Ludmila, continues, with each side claiming the other breached the Proxy settlement reached last July. While the legal battle continues to unfold, the most recent Court decisions determined, “… no basis in law or fact that remains as to the invalidity of Mr. Smolyansky’s nomination of an alternate slate of directors and such nomination is void ab initio and is not a valid solicitation,” according to the Company.

The Twist. In a twist, David Kanen of Kanen Wealth Management issued a letter sent to Julie Smolyansky and the Board of Directors. According to the letter, Mr. Kanen owns approximately 4.1% of the outstanding LWAY shares and intends to vote his shares in support of the recent slate nominated by Edward and Ludmila Smolyansky.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1QFY24 Revenue Light. Net revenue of $94.4 million was below our and consensus estimates of $99 million and $99.7 million, respectively. The revenue miss was driven by some traffic weakness at factory stores during March, although subsequent months have shown improvement. However, Pura Vida showed its first y-o-y sales improvement in five quarters, while Vera Bradley full line and e-comm produced solid results.

But Margins Improved. Gross margin expanded 150 basis points to 54.8% reflecting lower freight costs and inventory sell through while SG&A fell to 58.9% of revenue from 60.3% (both non-GAAP) last year reflecting strong cost control. GAAP EPS loss was $0.15, while adjusted EPS loss was $0.09, compared to EPS loss of $0.21 and $0.18, respectively, in 1QFY23, and our $0.19 EPS loss estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Net loss totaled ($4.7) million, or ($0.15) per diluted share; non-GAAP net loss totaled ($2.6) million, or ($0.09) per diluted share

Balance sheet remains strong, with cash and cash equivalents of $25.3 million, no debt, and year-over-year inventories down 11.8%

Management increases guidance for fiscal year

FORT WAYNE, Ind., June 07, 2023 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) today announced its financial results for the first quarter ended April 29, 2023.

In this release, Vera Bradley, Inc. or “the Company” refers to the entire enterprise and includes both the Vera Bradley and Pura Vida brands. Vera Bradley on a stand-alone basis refers to the Vera Bradley brand.

First Quarter Comments

Jackie Ardrey, Chief Executive Officer of the Company, noted, “We are pleased that meaningful gross margin expansion and diligent expense control led to significant year-over-year improvement in bottom-line performance for the quarter.

“On the revenue side, Vera Bradley factory stores experienced challenging traffic trends in March and April that led to weaker-than-expected performance for the quarter. This was partially offset, however, by several positive highlights in other areas of our business.

“First, we experienced our first positive quarterly revenue performance in five quarters at Pura Vida, primarily driven by non-comparable retail store sales. We also saw improved year-over-year sales trends in both our Pura Vida wholesale and e-commerce channels. Second, we delivered strong Vera Bradley e-commerce performance and solid Vera Bradley full-line store revenues. Vera Bradley Indirect revenues declined, as expected, due to a non-recurring key account order that took place in last year’s first quarter, but the underlying business remains healthy.”

“We are building a collaborative team with the mindset of generating long-term revenue increases, expanding gross margin, and ensuring strong financial discipline and cost control, which we expect will drive long-term profitable growth,” Ardrey continued. “The team is working hard and taking strategic, proactive steps to steadily grow Pura Vida’s revenues and to reverse the trends in Vera Bradley’s factory channel through the expansion of successfully tested targeted marketing programs designed to drive traffic and average order size.”

Ardrey added, “The hard work on Project Restoration began in the first quarter, which is focused on four key pillars of the business for each brand – Consumer, Brand, Product, and Channel – to drive this long-term profitable growth. To support Project Restoration and lay the foundation for our success, we made additional corporate changes and announced $12 million in incremental annualized cost reductions, including the elimination of approximately 25 corporate positions as part of an overall plan to further right-size the expense structure of the Company.”

Michael Schwindle joined the Company as Chief Financial Officer on May 8, 2023. “His track record of driving profitable growth, along with his passion for retail and operational excellence, will be instrumental as the Company executes Project Restoration and in the years beyond,” Ardrey noted. The Company also made several organizational changes in the Marketing, E-commerce, Product Design, and Product Development areas that flattened and streamlined the organizational structure to improve execution; make faster decisions; and provide support for the four pillars of Project Restoration. These most recent organizational changes and non-payroll expense reductions are expected to produce annualized savings of approximately $12 million, on top of the Company’s Fiscal 2023 cost reductions.

“We are committed to delivering improved value to our shareholders,” Ardrey continued. “These efforts will allow us to simplify our structure, be a more agile organization, and reset our expense base, so we can focus fully on Project Restoration and on delivering both healthy top- and bottom-line growth in the future.”

Summary of Financial Performance for the First Quarter

Consolidated net revenues totaled $94.4 million compared to $98.5 million in the prior year first quarter ended April 30, 2022.

For the current year first quarter, Vera Bradley, Inc.’s consolidated net loss totaled ($4.7) million, or ($0.15) per diluted share. These results included $2.0 million of net after tax charges, comprised of $1.4 million of severance charges, $0.5 million for the amortization of definite-lived intangible assets, and $0.1 million of consulting and professional fees primarily associated with cost saving and strategic initiatives. On a non-GAAP basis, Vera Bradley, Inc.’s consolidated first quarter net loss totaled ($2.6) million, or ($0.09) per diluted share.

For the prior year first quarter, Vera Bradley, Inc.’s consolidated net loss totaled ($7.0) million, or ($0.21) per diluted share. These results included $0.9 million of net after tax charges, comprised of $0.4 million of intangible asset amortization and $0.4 million of impairment charges, and $0.1 million of consulting fees associated with cost savings initiatives. On a non-GAAP basis, Vera Bradley, Inc.’s consolidated first quarter net loss totaled ($6.0) million, or ($0.18) per diluted share.

Non-GAAP Numbers

The current year non-GAAP first quarter income statement numbers referenced below exclude the previously outlined severance charges, intangible asset amortization, and consulting and professional fees. The prior year non-GAAP first quarter income statement numbers referenced below exclude the previously outlined intangible asset amortization, impairment charges, and consulting fees.

First Quarter Details

Current year first quarter Vera Bradley Direct segment revenues totaled $58.9 million, a 4.4% decrease from $61.6 million in the prior year first quarter. Comparable sales declined 3.3% in the first quarter, primarily due to weakness in the factory channel. The Company permanently closed 19 full-line and two factory outlet stores and opened five factory outlet stores over the last twelve months.

Vera Bradley Indirect segment revenues totaled $15.4 million, a 9.4% decrease from $17.0 million in the prior year first quarter. Prior year revenues reflected a large one-time key account order that was not repeated in the current year.

Pura Vida segment revenues totaled $20.1 million, a 1.2% increase over $19.8 million in the prior year first quarter, primarily driven by new store growth resulting in non-comparable retail store sales.

First quarter consolidated gross profit totaled $51.7 million, or 54.8% of net revenues, compared to $52.5 million, or 53.3% of net revenues, in the prior year first quarter. The current year gross profit rate was favorably impacted by lower year-over-year inbound and outbound freight expense and the sell-through of previously-reserved inventory, partially offset by an increase in promotional activity.

Consolidated SG&A expense totaled $58.5 million, or 62.0% of net revenues, for the quarter, compared to $60.9 million, or 61.9% of net revenues, for the prior year first quarter. On a non-GAAP basis, consolidated SG&A expense totaled $55.6 million, or 58.9% of net revenues, for the current quarter, compared to $59.4 million, or 60.3% of net revenues, for the prior year first quarter. Vera Bradley’s current year non-GAAP SG&A expenses were lower than the prior year primarily due to cost reduction initiatives and a reduction in variable-related expenses related to lower sales volume.

The Company’s first quarter consolidated operating loss totaled ($6.4) million, or (6.8%) of net revenues, compared to an operating loss of ($8.2) million, or (8.4%) of net revenues, in the prior year first quarter. On a non-GAAP basis, the consolidated operating loss totaled ($3.5) million, or (3.7%) of net revenues, compared to ($6.7) million, or (6.8%) of net revenues, in the prior year.

By segment:

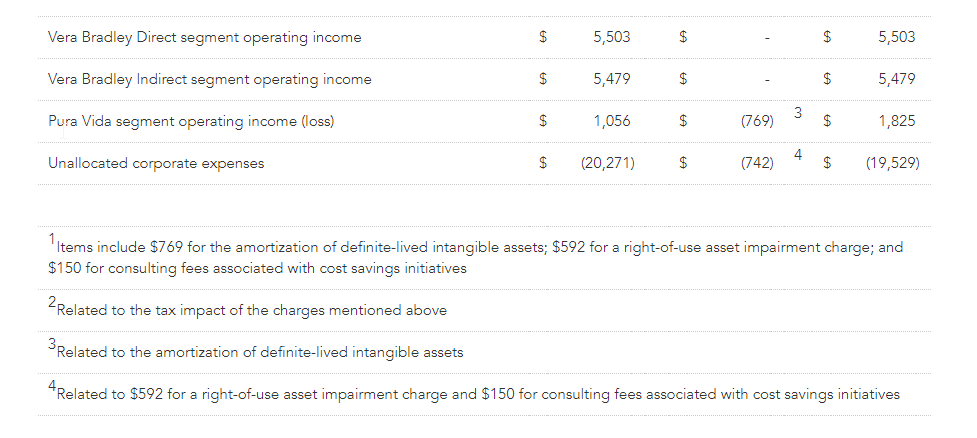

Vera Bradley Direct’s first quarter operating income was $7.3 million, or 12.5% of Direct net revenues, compared to operating income of $5.5 million, or 8.9% of Direct net revenues, in the prior year. On a non-GAAP basis, Vera Bradley Direct’s current year first quarter operating income was $7.7 million, or 13.0% of Direct net revenues, compared to $5.5 million, or 8.9% of Direct net revenues, in the prior year.

Vera Bradley Indirect’s first quarter operating income was $4.7 million, or 30.6% of Indirect net revenues, compared to $5.5 million, or 32.3% of Indirect net revenues, in the prior year.

Pura Vida’s first quarter operating income was $1.6 million, or 7.8% of Pura Vida net revenues, compared to $1.1 million, or 5.3% of Pura Vida net revenues, in the prior year. On a non-GAAP basis, Pura Vida’s current year first quarter operating income was $2.3 million, or 11.4% of Pura Vida net revenues, compared to $1.8 million, or 9.2% of Pura Vida net revenues, in the prior year.

Balance Sheet

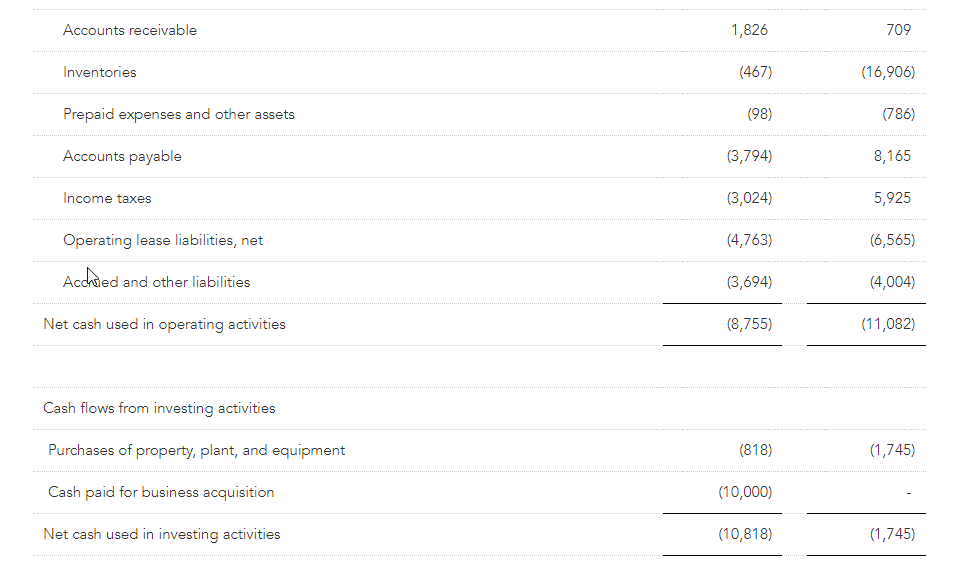

Net capital spending for the first quarter totaled $0.8 million compared to $1.7 million in the prior year.

Cash and cash equivalents as of April 29, 2023 totaled $25.3 million compared to $46.6 million at fiscal year end. The Company had no borrowings on its $75 million ABL credit facility at quarter end.

Total quarter-end inventory was $142.7 million, compared to $161.8 million at the end of the first quarter last year.

During the first quarter, the Company repurchased approximately $0.7 million of its common stock (approximately 0.1 million shares at an average price of $5.71). $27.0 million remains under the Company’s $50.0 million repurchase authorization that expires in December 2024.

Forward Outlook

Management is updating guidance for the fiscal year ending February 3, 2024 (“Fiscal 2024”) based on first quarter performance, Company initiatives underway, and current macroeconomic trends and expectations.

Excluding net revenues, all forward-looking guidance numbers referenced below are non-GAAP. The prior year income statement numbers exclude the previously disclosed charges for goodwill and intangible asset impairment; net inventory and purchase order-related adjustments; severance, retention, and stock-based retirement compensation; consulting and professional fees primarily associated with cost savings initiatives, the CEO search, and strategic initiatives; amortization of definite-lived intangible assets; store and right-of-use asset impairment charges; new CEO sign-on bonus and relocation; and goodMRKT exit costs. Current year guidance excludes any similar charges.

For Fiscal 2024, the Company’s expectations are as follows:

Consolidated net revenues of $490 to $510 million. Net revenues totaled $500.0 million in Fiscal 2023. Both Vera Bradley and Pura Vida revenues are expected to be approximately flat on a year-over-year basis.

A consolidated gross profit percentage of 52.8% to 53.8% compared to 51.4% in Fiscal 2023. The Fiscal 2024 gross margin rate is expected to be favorably impacted by lower year-over-year freight expense, cost reduction initiatives, and the sell-through of previously-reserved inventory, partially offset by an increase in promotional activity.

Consolidated SG&A expense of $237 to $247 million compared to $245.3 million in Fiscal 2023. An expected decline in SG&A expense is being driven by Company-wide cost reduction initiatives, partially offset by restoring short-term and long-term incentive compensation to more normalized levels and incremental marketing investment intended to accelerate customer file growth.

Consolidated operating income of $24 to $28 million compared to $12.3 million in Fiscal 2023.

Free cash flow of between $35 and $40 million compared to a cash usage of $21.7 million in Fiscal 2023.

Consolidated diluted EPS of $0.57 to $0.67 based on diluted weighted-average shares outstanding of 30.7 million and an effective tax rate of approximately 28%. Diluted EPS totaled $0.24 last year.

Net capital spending of approximately $5 million compared to $8.2 million in the prior year, reflecting investments associated with new Vera Bradley Factory stores and technology and logistics enhancements.

Disclosure Regarding Non-GAAP Measures

The Company’s management does not, nor does it suggest that investors should, consider the supplemental non-GAAP financial measures in isolation from, or as a substitute for, financial information prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). Further, the non-GAAP measures utilized by the Company may be unique to the Company, as they may be different from non-GAAP measures used by other companies.

The Company believes that the non-GAAP measures presented in this earnings release, including (cash usage) free cash flow; gross profit; selling, general, and administrative expenses; operating loss; net loss; net loss attributable and available to Vera Bradley, Inc.; and diluted net loss per share available to Vera Bradley, Inc. common shareholders, along with the associated percentages of net revenues, are helpful to investors because they allow for a more direct comparison of the Company’s year-over-year performance and are consistent with management’s evaluation of business performance. A reconciliation of the non-GAAP measures to the most directly comparable GAAP measures can be found in the Company’s supplemental schedules included in this earnings release.

Call Information

A conference call to discuss results for the first quarter is scheduled for today, Wednesday, June 7, 2023, at 9:30 a.m. Eastern Time. A broadcast of the call will be available via Vera Bradley’s Investor Relations section of its website, www.verabradley.com. Alternatively, interested parties may dial into the call at (888) 394-8218, and enter the access code 9903988. A replay will be available shortly after the conclusion of the call and remain available through June 21, 2023. To access the recording, listeners should dial (844) 512-2921, and enter the access code 9903988.

About Vera Bradley, Inc.

Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

The Company has three reportable segments: Vera Bradley Direct (“VB Direct”), Vera Bradley Indirect (“VB Indirect”), and Pura Vida. The VB Direct business consists of sales of Vera Bradley products through Vera Bradley Full-Line and Factory stores in the United States, www.verabradley.com, www.verabradley.ca, Vera Bradley’s online outlet site, and the Vera Bradley annual outlet sale in Fort Wayne, Indiana. The VB Indirect business consists of sales of Vera Bradley products to approximately 1,700 specialty retail locations throughout the United States, as well as select department stores, national accounts, third party e-commerce sites, and third-party inventory liquidators, and royalties recognized through licensing agreements related to the Vera Bradley brand. The Pura Vida segment consists of sales of Pura Vida products through the Pura Vida websites, www.puravidabracelets.com, www.puravidabracelets.eu, and www.puravidabracelets.ca; through the distribution of its products to wholesale retailers and department stores; and through its Pura Vida retail stores.

Website Information

We routinely post important information for investors on our website www.verabradley.com in the “Investor Relations” section. We intend to use this webpage as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor the Investor Relations section of our website, in addition to following our press releases, SEC filings, public conference calls, presentations and webcasts. The information contained on, or that may be accessed through, our webpage is not incorporated by reference into, and is not a part of, this document.

Investors and other interested parties may also access the Company’s most recent Corporate Responsibility and Sustainability Report outlining its ESG (Environmental, Social, and Governance) initiatives at https://verabradley.com/pages/corporate-responsibility.

Vera Bradley Safe Harbor Statement

Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. Risks, uncertainties, and assumptions also include the possibility that Pura Vida acquisition benefits may not materialize as expected and that Pura Vida’s business may not perform as expected. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 28, 2023. We undertake no obligation to publicly update or revise any forward-looking statement. Financial schedules are attached to this release.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Twin Peaks IPO. FAT Brands announced plans to pursue an initial public offering of its Twin Peaks restaurant business. Management previously had indicated the significant value creating potential of Twin Peaks for FAT Brands’ shareholders, although the timing is sooner than we had expected. FAT expects to retain a majority ownership.

The Business. Twin Peaks recently opened its 100th location and should end the year with approximately 115 lodges, an almost 40% increase in unit count since the acquisition. The brand also has a committed development pipeline for an additional 109 franchise locations. Over the next several years, Twin Peaks plans to double its unit count to more than 200 lodges with about 80% franchised. The planned unit growth is expected to increase systemwide sales to approximately $1.0 billion. Over the next three years, Twin Peaks’ contribution to FAT Brands adjusted EBITDA should increase from $40 million to $60 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Reliable Data, Not Emotions, are Pointing to a Growing U.S. Economy

In roughly one month, we will be halfway through 2023. While many point to the Fed’s pace of tightening and the downward sloping yield curve, as a reason to run around like Chicken Little warning of a coming recession, a fresh read of the economic tea leaves tells a different story. Just today, May 23, the PMI Output Index (PMI) rose to its highest reading in over a year. Home sales figures were also reported to show that new homes in May sold at the highest rate in over a year. These are both reliable leading indicators that point to growth in both services and manufacturing.

U.S. Composite PMI Output Index

Business activity in the U.S. increased to a 13-month high in May due in large part to strong growth in the services sector. This is a reliable indication that economic expansion has growing momentum. Despite the negative talk of those that are concerned that the Fed has lifted interest rates closer to historical norms and that the yield curve is still inverted, in part due to Covid era Fed yield-curve-control, the numbers suggest less caution might be warranted.

S&P Global said on Tuesday (May 23) its flash U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, rose to a reading of 54.5 this month. It indicates the highest level since April 2022 and is up from a reading of 53.4 in April. A reading above 50 indicates growth, this is the fourth consecutive month it has been above 50. The consensus among economists was only 52.6.

Home Sales

One sector that is directly impacted by interest rates is real estate. However, new home sales rose in April, this is a clear sign that prospective buyers are making deals with builders.

New homes in April were sold at a seasonally-adjusted annual rate of 683,000, Its the highest rate since March 2022. The April data represents a 4.1% gain from March’s revised rate of 656,000,. The report was from the Census and Department of Housing and Urban Development and was reported Tuesday May 23. Economists had expected new home sales to decline to 670,000 from a March rate of 683,000. It was the largest month-over-month increase since December 2022.

Leading Indicators

PMI is forward-looking as it surveys purchasing managers’ expectations and intentions for the coming months. By capturing their sentiment on future orders, production plans, and hiring intentions, PMI offers insights into economic trends that have yet to be reflected in other after-the-fact indicators.

Home sales are considered a leading indicator because they can serve as a measure of other needs and broader economic trends. Home sales have a significant impact on related sectors, such as construction, home improvement, finance, and consumer spending. Changes in home sales can influence economic activity and indicate shifts in consumer confidence, employment levels, and overall economic health.

While many economic reports offer rear-view mirror data, these reports are true indicators of business behavior as it plans for future expectations, and consumer behavior as it is confident that it will have the resources available to purchase and outfit a new home.

The upbeat reports prompted the Atlanta Federal Reserve to raise its second-quarter gross domestic product estimate to a 2.9% annualized rate from a 2.6% pace. The economy grew at a 1.1% rate in the first quarter.

Take Away

Many economists are negative about the economic outlook later this year. Market participants have been positioning themselves with the notion that there may be a late year recession. Is the notion misguided? Recent data suggests there may be buying opportunities for those willing to go against the tide of pundits preaching recession.

No one has a crystal ball. In good markets and bad, there is no replacement for good research before you put on a position, and then for as long as the position remains in your portfolio.

Channelchek is a great resource for information to follow the companies not likely being reported in traditional outlets. Turn to this online free resource as you evaluate small and microcap stocks.

LOS ANGELES, May 22, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”) announced today that it will be presenting at the 13th Annual LD Micro Invitational at the Luxe Sunset Boulevard Hotel, Los Angeles, California on June 6th-8th, 2023. The event is expected to feature 150+ companies, presenting in half-hour increments, as well as private 1:1 meetings.

FAT Brands is scheduled to present on Tuesday, June 6th at 4:30 pm PT. Andy Wiederhorn, Chairman of the Board, and Ken Kuick, Co-CEO and Chief Financial Officer, will be leading the presentation.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About LD Micro

LD Micro, a wholly owned subsidiary of Freedom US Markets, was founded in 2006 with the sole purpose of being an independent resource in the micro-cap space. Whether it is the Index, comprehensive data, or hosting the most significant events annually, LD’s sole mission is to serve as an invaluable asset for all those interested in finding the next generation of great companies. For more information on LD Micro, visit www.ldmicro.com.

Jenn Johnston Assumes Chief Marketing OfficerRole, New Brand Presidents to Lead Round Table Pizza, Great American Cookies, Marble Slab Creamery, and PretzelmakerConcepts

LOS ANGELES, May 18, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. announces the elevation of Jenn Johnston to the role of Chief Marketing Officer. Since the acquisition of Global Franchise Group in July 2021, Ms. Johnston has held the role of President of the Quick-Service Division at FAT Brands, overseeing brands including Round Table Pizza, Great American Cookies, Marble Slab Creamery, and Pretzelmaker. With Ms. Johnston’s promotion to Chief Marketing Officer, Allison Lauenstein and David Pear will assume Brand President roles.

Ms. Lauenstein will serve as Brand President of Great American Cookies, Marble Slab Creamery, and Pretzelmaker. Ms. Lauenstein brings over a decade of experience working with the respective brands, having previously served as Executive Vice President of Brand Operations and Marketing at Global Franchise Group. Ms. Lauenstein successfully launched several initiatives during her tenure, including the unlimited mix-ins platform at Marble Slab Creamery, the co-branded model of Great American Cookies and Marble Slab Creamery, and the Fresh Twist menu concept for Pretzelmaker. Prior to joining Global Franchise Group, Ms. Lauenstein spent 13 years at Dunkin’ and Baskin-Robbins Brands in various leadership positions.

With over 20 years of strategic and operational restaurant leadership experience, Mr. Pear will assume the role of Brand President at Round Table Pizza. Mr. Pear most recently served as Vice President of Strategic Initiatives at Desert De Oro Foods, a multi-unit franchise organization with 360 restaurants, including Taco Bell, KFC, Pizza Hut, Whataburger, Dickey’s Barbecue Pit, and Dave’s Hot Chicken. Prior to that, Mr. Pear served as Senior Vice President of Operations at Del Taco, where he played a key role in consistently increasing same-store sales and driving overall unit growth. Mr. Pear also brings experience from his time at Yum! Brands’ Taco Bell and Domino’s Pizza, where he led operational transformation through a combination of key initiatives focused on culture, continuous improvement of operational elements, and elevation of the guest experience.

“As FAT Brands continues to evolve and grow, we saw an opportunity to expand Jenn’s role to impact the larger organization,” said Thayer Wiederhorn, Chief Operating Officer of FAT Brands. “Her unique marketing and operations background will enable us to develop impactful campaigns that increase brand visibility and drive profitable sales across our 17 concepts. We are also pleased to welcome Allison and David to the team. Allison has a great track record with Great American Cookies, Marble Slab Creamery, and Pretzelmaker. We expect a seamless integration into her new role and immediate value to the brands. On the other hand, David brings exciting insights from his outside experience, which we also expect will bring immediate results. We are fortunate to have them both join our talented management team.”

About FAT (Fresh. Authentic. Tasty.) Brands FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

MEDIA CONTACT: Erin Mandzik, FAT Brands [email protected] 860-212-6509

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. The momentum exhibited in 2022 carried over into 2023 as Lifeway reported its 14th consecutive quarter of topline expansion. Higher pricing, accelerating kefir unit volume, and additional distribution drove the top line. Gross margin increased by 530 basis points y-o-y, reflecting higher pricing and volumes as well as favorable milk pricing.

1Q23 Results. Revenue totaled $37.9 million, up 11.2% year-over-year. Gross profit margin was 21.7%, compared to 16.4% in 1Q22. Lifeway reported net income of $830,000, or EPS of $0.06 per share, versus a net loss of $895,000, or a loss of $0.06/sh last year. We had forecast revenue of $36 million, gross margin of 22.2%, and net income of $1.26 million, or EPS of $0.08/sh.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

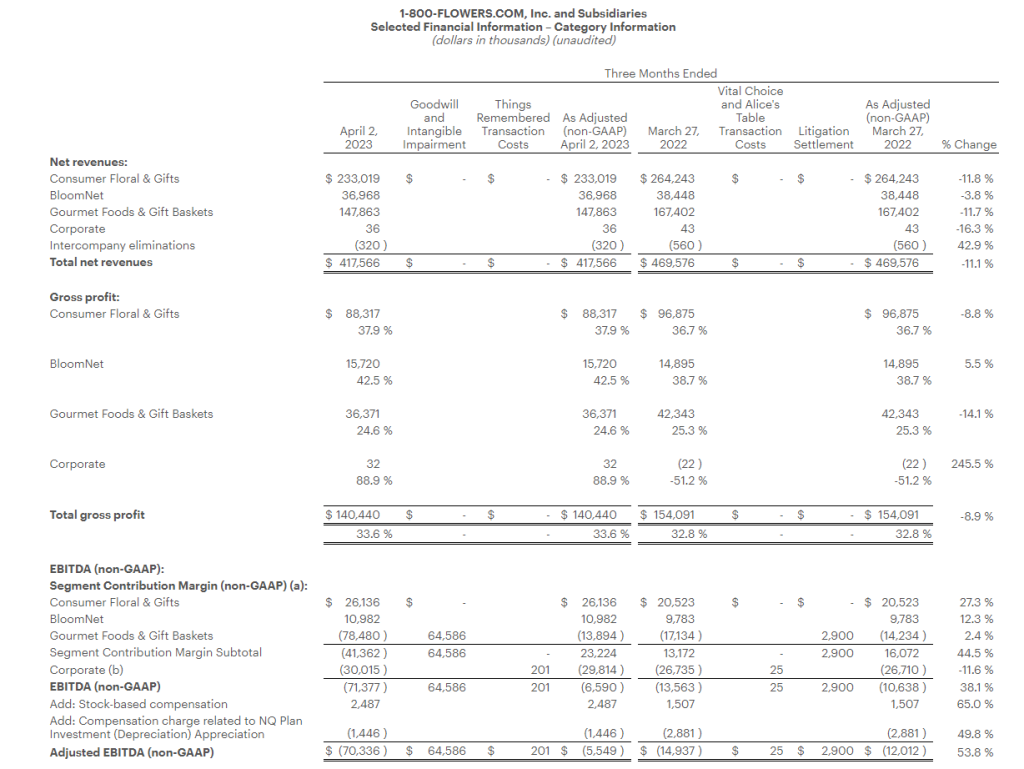

Margins improve. The company reported $417.6 million in revenue, 1.9% below our estimate of $425.8 million. But, importantly, adj EBITDA in the quarter was negative $5.5 million, beating our estimate of a loss of $13.1 million by 57.5%. Improved margins in the quarter were attributed to reduced ocean freight costs and some commodity price decreases.

Raises fiscal 2023 adj. EBITDA guidance. Management provided full year fiscal 2023 guidance of revenue down 8% and adj. EBITDA to be in the range of $85 million to $90 million, an increase from its previous guidance of $75 million to $80 million. In addition, the company reiterated that it will exceed $75 million in free cash flow.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FatburgerGains Momentum,Great American Cookies, Marble Slab Creamery,Buffalo’s Express Make Debut

LOS ANGELES, May 11, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger, Buffalo’s Express, Great American Cookies, Marble Slab Creamery, and 13 other restaurant concepts, announces a new development deal to open 22 new franchised locations in Iraq. In partnership with Global Vita USA LLC, 12 co-branded Fatburger and Buffalo’s Express locations will open throughout the country outside of the Kurdistan region over the next five years with the first units set to open in 2024. Ten co-branded Great American Cookies and Marble Slab Creamery units will also arrive throughout the country, opening in the next five years with the first locations set to open in 2024.

“With four units already operating in the Kurdistan region, Fatburger has established a strong following in the country,” said Taylor Wiederhorn, Chief Development Officer of FAT Brands. “Now, as we look to further expand the brand with Global Vita USA, we can reach even more fans that crave our all-American, custom-built burgers. This is new territory for Great American Cookies, Marble Slab Creamery, and Buffalo’s Express, however, the brands have had a presence in the Middle East for some time, so this is a natural progression for the concepts to strengthen their foothold in the region.”

Ever since the first Fatburger opened in Los Angeles 70 years ago, the chain has been known for its delicious, grilled-to-perfection and cooked-to-order burgers. Founder Lovie Yancey believed that a big burger with everything on it is a meal in itself; at Fatburger “everything” is not just the usual roster of toppings. Burgers can be customized with everything from bacon and eggs to chili and onion rings. In addition to its famous burgers, the Fatburger menu also includes Fat and Skinny Fries, sweet potato fries, scratch-made onion rings, Impossible™ Burgers, turkeyburgers, hand-breaded crispy chicken sandwiches, and hand-scooped milkshakes made from 100% real ice cream.

A perfect complement to Fatburger, Buffalo’s Express menu includes delicious bone-in and boneless chicken wings accompanied by a range of original sauces. All of Buffalo’s Express’ wings are accompanied by celery, carrots, and blue cheese, ranch or honey mustard dressing.

For nearly 40 years, Marble Slab Creamery has been an innovator in the ice cream space, dreaming up the frozen slab technique and offering homemade, small-batch ice cream with free unlimited mix-ins, shakes in a variety of flavors, and ice cream cakes.

Since 1977, Great American Cookies has baked up a reputation for not only being the creator of the Original Cookie Cake, but also for its famous chocolate chip cookie recipe. Other crave-able menu items include brownies and Double Doozies™, delectable icing sandwiched between two cookies.

About FAT (Fresh. Authentic. Tasty.) Brands FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Fatburger

An all-American, Hollywood favorite, Fatburger is a fast-casual restaurant serving big, juicy, tasty burgers, crafted specifically to each customer’s liking. With a legacy spanning 70 years, Fatburger’s extraordinary quality and taste inspire fierce loyalty amongst its fan base, which includes a number of A-list celebrities and athletes. Featuring a contemporary design and ambience, Fatburger offers an unparalleled dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1952 – The Last Great Hamburger Stand™.

About Buffalo’s Express

Founded in 1985 in Roswell, Georgia, Buffalo’s Express is a fast-casual chain known for its world-famous chicken wings and proprietary wing sauces. Co-branded with over 100 Fatburger restaurants to date, Buffalo’s Express’ significant growth can be attributed to its high-quality menu offerings and unparalleled dining experience. Featuring a contemporary design and ambience, whether guests are dining-in or having take-out/delivery, Buffalo’s Express offers friends and families the flexibility to enjoy their world-famous chicken wings however they prefer. Buffalo’s Express – Where Everyone is Family™.

About Great American Cookies

Founded on a family chocolate chip cookie recipe in 1977, Great American Cookies believes that pure, simple delight is part of living a full life. Serving the Original Cookie Cake, fresh baked cookies in a variety of flavors, brownies, and Double Doozies™, we promise to treat you to bites of bliss that prove how sweet life can be. With more than 370 bakeries across the country and internationally in Bahrain, Guam, Saudi Arabia, and treats available to ship right to your door, the sweet spot is always close to home. For more information, visit www.greatamericancookies.com.

About Marble Slab Creamery Since dreaming up the frozen slab technique and serving fresh homemade, small-batch ice cream in-store since 1983, Marble Slab Creamery has always known how to dream big. We sprinkle our customers with imagination and promise to inspire with infinite ice cream possibilities to feed your curiosity and capture cravings. With our free unlimited mix-in philosophy, delicious ice cream and shakes in a variety of flavors, hand-rolled waffle cones, and ice cream cakes, imagination has no limits. Today, Marble Slab Creamery is enjoyed by consumers across the globe with locations in Bahrain, Bangladesh, Canada, Kuwait, Pakistan, Saudi Arabia, Guam, Puerto Rico, and the United States. For more information, visit www.marbleslab.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings. Forward-looking statements reflect expectations of FAT Brands Inc. (“we”, “our” or the “Company”) concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies, including but not limited to uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

MEDIA CONTACT: Erin Mandzik, FAT Brands [email protected] 860-212-6509

Generates Net Revenues of $417.6 million and a Net Loss of $71.0 million, which Net Loss Includes an After-Tax, Non-Cash Goodwill and Intangible Asset Impairment Charge of $53.1 million

Adjusted Net Loss(1) Improves to $17.8 million, Compared with an Adjusted Net Loss of $21.0 million in the Prior Year Period

Adjusted EBITDA(1)Loss Improves to $5.5 million, Compared with an Adjusted EBITDA Loss of $12.0 million in the Prior Year Period, as Gross Margin Improvement and Operating Efficiencies Mitigate Revenue Decline

Updates Fiscal 2023 Outlook

(1) Refer to “Definitions of Non-GAAP Financial Measures” and the tables attached at the end of this press release for reconciliation of non-GAAP results to applicable GAAP results.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today reported results for its fiscal 2023 third quarter, ended April 2, 2023.

Fiscal 2023 Third Quarter Highlights

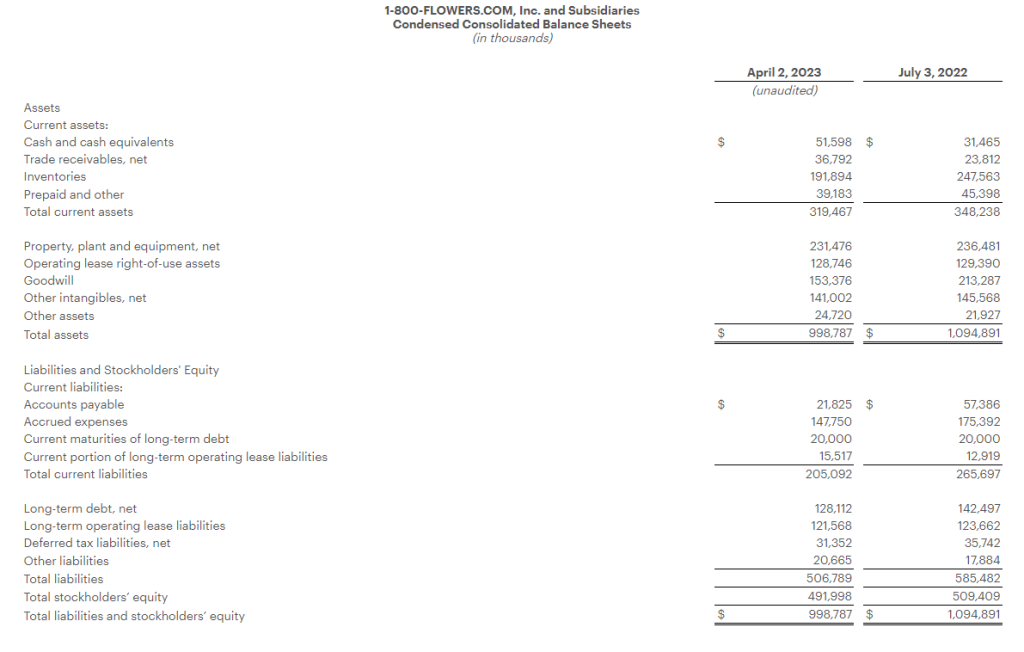

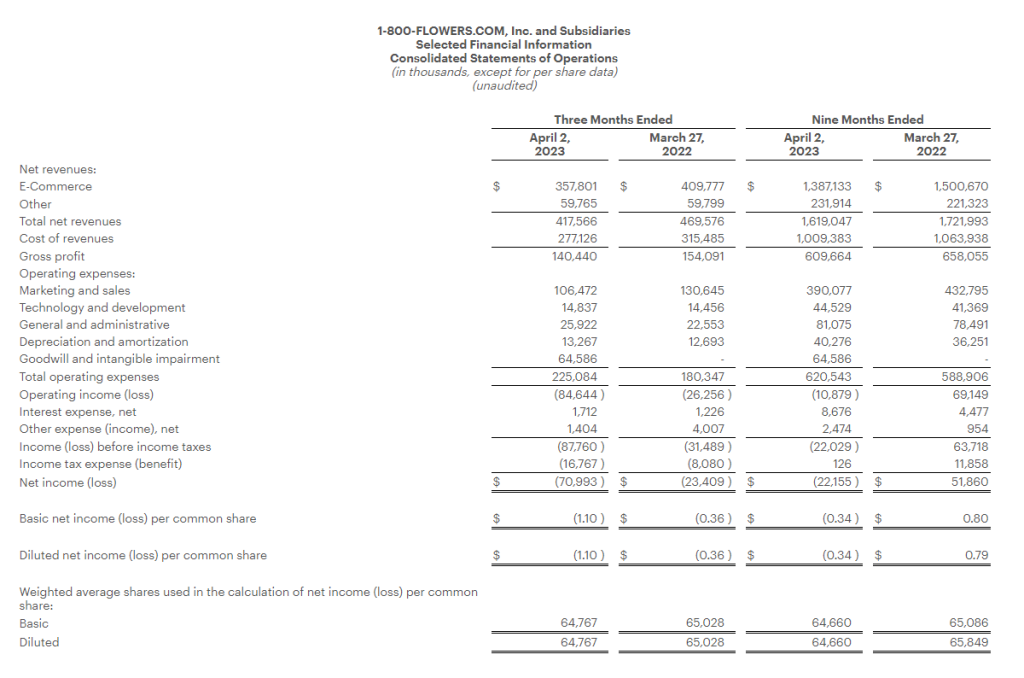

Total consolidated revenues decreased 11.1% to $417.6 million, compared with total consolidated revenues of $469.6 million in the prior year period.

Gross profit margin for the quarter increased 80 basis points to 33.6%, compared with 32.8% in the prior year period.

Operating expenses increased $44.7 million from the prior year period, including a $64.6 million non-cash goodwill and intangible assets impairment charge. Excluding the impact of this charge, operating expenses declined $19.8 million or 11.0%, as compared with the prior year period.

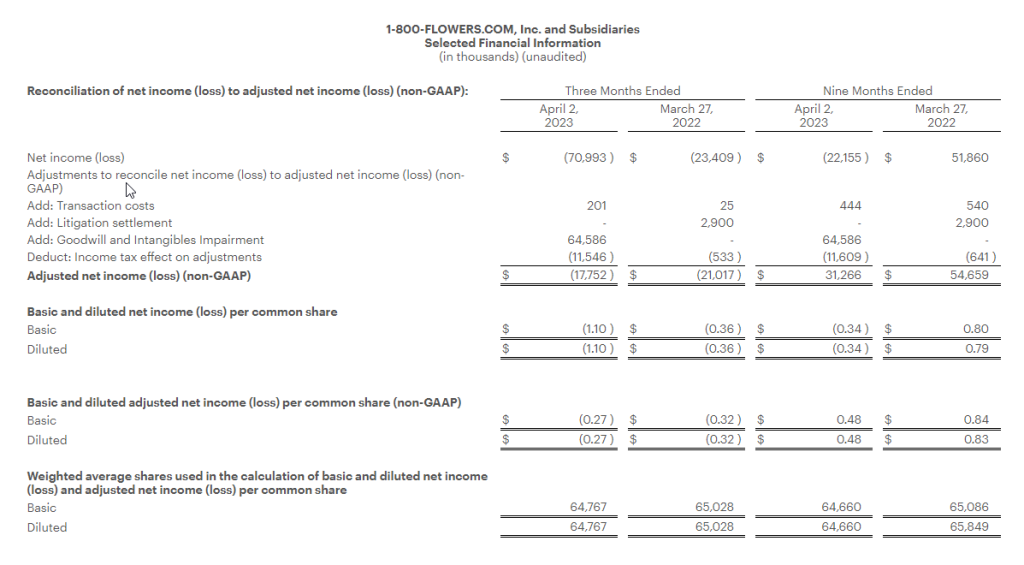

Net loss for the quarter was $71.0 million, or $1.10 per share, which includes an after-tax non-cash goodwill and intangible assets impairment charge of $53.1 million or $0.82 per share. Adjusted Net Loss1 was $17.8 million, or $0.27 per share.

Adjusted EBITDA1 for the quarter was a loss of $5.5 million, as compared with an Adjusted EBITDA1 loss of $12.0 million in the prior year period.

Chris McCann, CEO of 1-800-FLOWERS.COM, Inc., said “Our third quarter results reflect a continuation of the trends that we have experienced throughout this fiscal year. In this challenging consumer environment, we are executing on our strategy to invest in and develop stronger customer relationships, while continuing to identify operating efficiencies to reduce expenses. As a result of our expense optimization efforts, combined with improving gross margin, we exceeded our Adjusted EBITDA1 expectations for the quarter and are raising our full year Adjusted EBITDA1 guidance.”

McCann added, “We will continue to optimize operating expenses in this environment, while simultaneously investing in the long-term growth of our business, as evidenced by the recent acquisitions of Things Remembered® and SmartGift®. We believe these efforts position us well once the broader consumer environment improves and reinforce our company as a premier gifting destination that helps our customers connect with the important people in their lives.”

Third Quarter 2023 Financial Results

Total consolidated revenues decreased 11.1% to $417.6 million, as compared with total consolidated revenues of $469.6 million in the prior year period.

Gross profit margin for the quarter was 33.6%, increasing 80 basis points from the prior year period led by the Consumer Floral and Gifts and BloomNet® segments. Operating expenses, excluding the impairment charge noted above, stock-based compensation, appreciation-or-depreciation of investments in the Company’s non-qualified compensation plan, and the costs associated with a legal settlement in the prior year period, were 38.1% of total sales, or flat with the prior year period, as lower advertising and labor costs were offset by higher depreciation and amortization due to our capital investments in technology and automation.

As a result, the Company generated a net loss of $71.0 million, or ($1.10) per share, and an Adjusted Net Loss1 of $17.8 million, or ($0.27) per share, compared with a net loss of $23.4 million, or ($0.36) per share, and an Adjusted Net Loss1 of $21.0 million, or ($0.32) per share, in the prior year period.

Adjusted EBITDA1 for the quarter was a loss of $5.5 million, as compared with an Adjusted EBITDA1 loss of $12.0 million in the prior year period.

Segment Results

The Company provides selected financial results for its Gourmet Foods and Gift Baskets, Consumer Floral and Gifts, and BloomNet segments in the tables attached to this release and as follows:

Gourmet Foods and Gift Baskets: Revenues for the quarter decreased 11.7% to $147.9 million, compared with $167.4 million in the prior year period. Gross profit margin was 24.6%, compared with 25.3% in the prior year period, declining on continued higher commodity costs, increased promotional activity and overhead cost deleveraging. Segment contribution margin1 without the impairment charge was a loss of $13.9 million, compared with an adjusted loss1 of $14.2 million a year ago.

Consumer Floral and Gifts: Revenues decreased 11.8% to $233.0 million, compared with $264.2 million in the prior year period. Gross profit margin increased to 37.9%, compared with 36.7% in the prior year period, on strategic pricing initiatives and lower cost of merchandise in part due to lower ocean freight costs. Segment contribution margin1 was $26.1 million, compared with $20.5 million the prior year.

BloomNet: Revenues for the quarter decreased 3.8% to $37.0 million, compared with $38.4 million in the prior year period. Gross profit margin increased to 42.5%, compared with 38.7% in the prior year on strategic pricing initiatives and lower ocean freight costs. Segment contribution margin1 was $11.0 million, compared with $9.8 million in the prior year period.

Company Guidance

Based on its third quarter performance and outlook for the balance of the year, the Company is updating its Fiscal 2023 guidance. This outlook includes a continuation of the challenging consumer environment, which is expected to be mitigated by the Company’s expense management efforts.

The Company expects:

total revenues to decline approximately 8% as compared with the prior year;

adjusted EBITDA1 to be in a range of $85 million to $90 million; and

Free Cash Flow1 to exceed $75 million.

Conference Call

The Company will conduct a conference call to discuss the above details and attached financial results today, Thursday, May 11, at 8:00 a.m. (ET). The conference call will be webcast from the Investors section of the Company’s website at www.1800flowersinc.com. A recording of the call will be posted on the Investors section of the Company’s website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) today through May 18, 2023, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID #: 4785326.

Definitions of non-GAAP Financial Measures:

We sometimes use financial measures derived from consolidated financial information, but not presented in our financial statements prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). Certain of these are considered “non-GAAP financial measures” under the U.S. Securities and Exchange Commission rules. Non-GAAP financial measures referred to in this document are either labeled as “non-GAAP” or designated as such with a “1”. See below for definitions and the reasons why we use these non-GAAP financial measures. Where applicable, see the Selected Financial Information below for reconciliations of these non-GAAP measures to their most directly comparable GAAP financial measures. Reconciliations for forward-looking figures would require unreasonable efforts at this time because of the uncertainty and variability of the nature and amount of certain components of various necessary GAAP components, including, for example, those related to compensation, tax items, amortization or others that may arise during the year, and the Company’s management believes such reconciliations would imply a degree of precision that would be confusing or misleading to investors. For the same reasons, the Company is unable to address the probable significance of the unavailable information. The lack of such reconciling information should be considered when assessing the impact of such disclosures.

EBITDA and Adjusted EBITDA:

We define EBITDA as net income (loss) before interest, taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA adjusted for the impact of stock-based compensation, Non-Qualified Plan Investment appreciation/depreciation, and for certain items affecting period-to-period comparability. See Selected Financial Information for details on how EBITDA and Adjusted EBITDA were calculated for each period presented. The Company presents EBITDA and Adjusted EBITDA because it considers such information meaningful supplemental measures of its performance and believes such information is frequently used by the investment community in the evaluation of similarly situated companies. The Company uses EBITDA and Adjusted EBITDA as factors to determine the total amount of incentive compensation available to be awarded to executive officers and other employees. The Company’s credit agreement uses EBITDA and Adjusted EBITDA to determine its interest rate and to measure compliance with certain covenants. EBITDA and Adjusted EBITDA are also used by the Company to evaluate and price potential acquisition candidates. EBITDA and Adjusted EBITDA have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. Some of the limitations are: (a) EBITDA and Adjusted EBITDA do not reflect changes in, or cash requirements for, the Company’s working capital needs; (b) EBITDA and Adjusted EBITDA do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on the Company’s debts; and (c) although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future and EBITDA does not reflect any cash requirements for such capital expenditures. EBITDA and Adjusted EBITDA should only be used on a supplemental basis combined with GAAP results when evaluating the Company’s performance.

Segment Contribution Margin and Adjusted Segment Contribution Margin

We define Segment Contribution Margin as earnings before interest, taxes, depreciation, and amortization, before the allocation of corporate overhead expenses. Adjusted Contribution Margin is defined as Contribution Margin adjusted for certain items affecting period-to-period comparability. See Selected Financial Information for details on how Segment Contribution Margin and Adjusted Segment Contribution Margin were calculated for each period presented. When viewed together with our GAAP results, we believe Segment Contribution Margin and Adjusted Segment Contribution Margin provide management and users of the financial statements meaningful information about the performance of our business segments. Segment Contribution Margin and Adjusted Segment Contribution Margin are used in addition to and in conjunction with results presented in accordance with GAAP and should not be relied upon to the exclusion of GAAP financial measures. The material limitation associated with the use of Segment Contribution Margin and Adjusted Segment Contribution Margin is that they are an incomplete measure of profitability as they do not include all operating expenses or non-operating income and expenses. Management compensates for this limitation when using these measures by looking at other GAAP measures, such as Operating Income and Net Income.

Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share:

We define Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share as Net Income (Loss) and Net Income (Loss) Per Common Share adjusted for certain items affecting period-to-period comparability. See Selected Financial Information below for details on how Adjusted Net Income (Loss) Per Common Share and Adjusted or Comparable Net Income (Loss) Per Common Share were calculated for each period presented. We believe that Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share are meaningful measures because they increase the comparability of period-to-period results. Since these are not measures of performance calculated in accordance with GAAP, they should not be considered in isolation of, or as a substitute for, GAAP Net Income (Loss) and Net Income (Loss) Per Common share, as indicators of operating performance and they may not be comparable to similarly titled measures employed by other companies.

Free Cash Flow:

We define Free Cash Flow as net cash provided by operating activities less capital expenditures. The Company considers Free Cash Flow to be a liquidity measure that provides useful information to management and investors about the amount of cash generated by the business after the purchases of fixed assets, which can then be used to, among other things, invest in the Company’s business, make strategic acquisitions, strengthen the balance sheet, and repurchase stock or retire debt. Free Cash Flow is a liquidity measure that is frequently used by the investment community in the evaluation of similarly situated companies. Since Free Cash Flow is not a measure of performance calculated in accordance with GAAP, it should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. A limitation of the utility of Free Cash Flow as a measure of financial performance is that it does not represent the total increase or decrease in the Company’s cash balance for the period.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, Stock Yards® and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com or follow @1800FLOWERSInc on Twitter.

FLWS–COMP FLWS-FN

Special Note Regarding Forward Looking Statements:

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements represent the Company’s current expectations or beliefs concerning future events and can generally be identified using statements that include words such as “estimate,” “expects,” “project,” “believe,” “anticipate,” “intend,” “plan,” “foresee,” “forecast,” “likely,” “will,” “target” or similar words or phrases. These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of the Company’s control, which could cause actual results to differ materially from the results expressed or implied in the forward-looking statements, including, but not limited to, statements regarding the Company’s ability to achieve its guidance for the full Fiscal year; the Company’s ability to leverage its operating platform and reduce its operating expense ratio; its ability to sell through existing inventories; its ability to successfully integrate acquired businesses and assets; its ability to successfully execute its strategic initiatives; its ability to cost effectively acquire and retain customers; the outcome of contingencies, including legal proceedings in the normal course of business; its ability to compete against existing and new competitors; its ability to manage expenses associated with sales and marketing and necessary general and administrative and technology investments; its ability to reduce promotional activities and achieve more efficient marketing programs; and general consumer sentiment and industry and economic conditions that may affect levels of discretionary customer purchases of the Company’s products. The Company undertakes no obligation to publicly update any of the forward-looking statements, whether because of new information, future events or otherwise, made in this release or in any of its SEC filings. Consequently, you should not consider any such list to be a complete set of all potential risks and uncertainties. For a more detailed description of these and other risk factors, refer to the Company’s SEC filings, including the Company’s Annual Reports on Form 10-K and its Quarterly Reports on Form 10-Q.

Note: The following tables are an integral part of this press release without which the information presented in this press release should be considered incomplete.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

CEO Stepping Down. Yesterday, CVG announced CEO Harold Bevis is resigning from his role as President and CEO, as well as a Board member, effective May 19th to become CEO of another company. The Company noted Mr. Bevis’ resignation did not result from any disagreement with the Company on any matter.

Interim CEO. Current Chairman of the Board Robert Griffin will step into an interim CEO role. On the Board since 2005, Mr. Griffin worked closely with Mr. Bevis in designing and implementing the Company’s strategy. Mr. Griffin has an extensive financial background, including as Head of Investment Banking for Barclays Capital. Other Board members with a more operational and manufacturing background will assist Mr. Griffin. CVG will be in good hands during the transition, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Results. FAT Brands reported 1Q23 revenue of $105.7 million, up 8.5% y-o-y from $97.4 million in the year ago quarter. System-wide sales growth was 9.9%. Same Store Sales were up 4.3%. FAT reported adjusted EBITDA of $19.2 million in the quarter, up from $15.1 million in 1Q22. Adjusted net loss for the quarter was $23.5 million, or a loss of $1.43 per share, compared to a net loss of $18.5 million, or a loss of $1.13 per share, last year. We had projected revenue of $105 million and a net loss of $17.3 million, or a loss of $1.04 per share.

Organic Growth. Organic growth at FAT Brands remains strong. A total of 41 new units were opened during 1Q and plans are to open 45 additional units in 2Q. For the full year, a total of 175 new units are expected to open, representing over 25% growth from last year. The pipeline remains robust with development agreements for more than 1,000 new locations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.