Tesla shares moved sharply higher Monday after confirmation that the company has begun testing its Robotaxi service without a safety driver, a milestone that investors and analysts see as a major step toward fully autonomous transportation.

The rally followed social media footage showing a Tesla Robotaxi operating in Austin, Texas with no human driver inside the vehicle. The video quickly gained traction after Ashok Elluswamy, who leads Tesla’s AI and autonomous driving efforts, acknowledged the clip with a brief but telling comment: “And so it begins.” Tesla CEO Elon Musk later confirmed the development, stating that testing is underway with no occupants in the car.

Shares of Tesla rose roughly 4% following the confirmation, pushing the stock closer to its prior all-time highs and reinforcing renewed optimism around the company’s long-promised autonomy strategy. The move lends credibility to Musk’s recent claim that Tesla is only weeks away from unsupervised robotaxi operations.

Austin has emerged as the proving ground for Tesla’s Robotaxi ambitions, with limited deployments already underway using safety drivers. The latest test suggests the company is moving closer to removing that final safeguard, a critical hurdle before broader commercial expansion. Musk has previously said Tesla plans to expand Robotaxi testing beyond Austin and the San Francisco Bay Area into markets such as Phoenix and Nevada.

Wall Street bulls were quick to seize on the news. Wedbush analyst Dan Ives reiterated his long-standing optimism on Tesla, describing the development as the beginning of the company’s “autonomous chapter.” In a note to clients, Ives said 2026 could be a defining year for Tesla as autonomous driving and robotics move from concept to scale.

According to Ives, Tesla is on track for an accelerated Robotaxi rollout across the U.S., with volume production of the company’s purpose-built Cybercab expected to begin in the spring. The futuristic two-seat vehicle, unveiled last year without a steering wheel or pedals, has become central to Tesla’s long-term autonomous strategy.

Early feedback on Tesla’s latest Full Self-Driving software has also added fuel to the rally. Automotive reviewers and journalists who have tested the newest version report smoother driving behavior and fewer required interventions compared with prior iterations. While competitors like Alphabet-backed Waymo still lead in publicly reported safety metrics, the gap appears to be narrowing.

The market reaction highlights a broader shift in how investors are valuing Tesla. Rather than focusing solely on vehicle deliveries and margins, attention is increasingly turning to software, AI, and recurring revenue opportunities tied to autonomy. Wedbush maintains an Outperform rating on the stock and a $600 price target, arguing that autonomous driving could unlock a path toward a multi-trillion-dollar valuation.

Still, challenges remain. Regulatory approval, public trust, and demonstrable safety performance will be essential before Tesla can scale Robotaxi services nationwide. But for the first time in years, tangible evidence appears to support Tesla’s autonomy narrative.

For investors, the confirmation of driverless Robotaxi testing marks more than just a technical achievement — it signals that Tesla’s long-awaited autonomous future may finally be arriving.

For the first time in more than two years, U.S. home prices have dipped into negative territory, slipping 1.4% in just the last three months. High-frequency data from Parcl Labs shows a modest decline nationally, but the shift carries more weight than the numbers suggest. After a long stretch of rising prices fueled by pandemic demand, extremely low inventory, and a surge in relocation activity, the market is now feeling the effects of high mortgage rates, slower buyer activity, and a consumer who is becoming increasingly cautious. For small-cap investors, this change in the housing landscape serves as a valuable indicator of broader economic sentiment.

The housing market has been wrestling with affordability pressures since mortgage rates spiked in 2022 and 2023, with the 30-year fixed rate jumping from under 4% to more than 7%. That rapid climb priced out large segments of buyers and forced sellers to adjust their expectations. While inventory is still historically low, active listings have risen 13% year over year, and many sellers are pulling their homes off the market entirely due to low demand. That type of hesitation reflects real-time consumer behavior—people are slowing down major purchases, reevaluating budgets, and becoming more selective. Housing tends to reveal economic shifts early, and the current softness mirrors the same cautious tone we’ve been seeing in certain pockets of the small-cap market.

Regionally, the data is even more telling. Markets like Austin are down 10% year over year, with Denver, Tampa, Houston, Atlanta, and Phoenix also showing notable declines. Meanwhile, cities like Cleveland, Chicago, New York, Philadelphia, and Boston are still posting price gains. This split environment is a reminder that the national average rarely tells the full story—both in real estate and in equities. Small-cap stocks behave the same way: some regions and sectors weaken sharply while others show surprising strength. Investors who learn to spot these patterns early often outperform.

Another challenge is the lack of updated government housing reports due to the recent federal shutdown. Without fresh data on housing starts, permits, or new home sales, analysts are relying heavily on private data, builder sentiment, and earnings commentary. Homebuilders themselves describe a market with weak demand and ongoing incentives, and their sentiment remains deep in negative territory. That combination—soft demand, cautious consumers, and uneven regional performance—is exactly the kind of environment where small caps tend to lag temporarily before outperforming when conditions improve.

Mortgage rates have barely moved in the last three months, even after the Fed’s recent rate cut, suggesting that home prices may hover around zero growth for some time. But for small-cap investors, this stability isn’t a bad thing. When markets pause, opportunities emerge. Historically, when housing cools without collapsing, it often sets the stage for strong small-cap recoveries once rates drift lower and consumer confidence finds its footing.

Home prices turning slightly negative isn’t a crisis—it’s a signal. It tells us the economy is recalibrating after years of aggressive tightening, and that consumers are adapting. For disciplined small-cap investors, this environment is a chance to study balance sheets, identify undervalued companies, and prepare for the next move higher. Economic resets don’t punish prepared investors—they reward them.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 Results. The company reported Q3 revenue of $85.1 million, beating our estimate of $80.0 million by 6.4%. Adj. EBITDA of $6.5 million, strongly outperformed our estimate of $1.7 million by 289%. The strong operating results were driven by growth in the wholesale and direct-to-consumer channels, its e-commerce platform, and by effective tariff mitigation strategies.

Digital momentum. Notably, the company’s e-commerce platform experienced triple-digit traffic growth late in the quarter, creating a strong backdrop for the launch of its dropship initiative. While the initiative currently offers only footwear, the company highlighted encouraging early results and plans to expand product offerings, leveraging its partnership with Authentic Brands. In our view, the dropship strategy provides the company with a capital-efficient way to broaden product offerings while gathering customer insight.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NobleCon21. On December 3rd, management presented at NobleCon21 at Florida Atlantic University (FAU) in Boca Raton, Florida. The presentation, conducted by Jeff Walker, CEO, highlighted the company’s record financial performance, dominant wholesale distribution platform, and favorable growth initiative in authenticated collectibles. A replay of the presentation can be viewed here.

Dominant wholesale platform. As the largest wholesale distributor of physical entertainment in the U.S., the company’s scaled, automated logistics operations provide a significant competitive moat. Furthermore, it serves as the category manager and primary fulfillment partner for major retailers like Walmart, Target, and Amazon, managing both in-store inventory and direct-to-consumer e-commerce shipments.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (Nasdaq: VNCE) (“VNCE” or the “Company”), a global contemporary retailer, today reported its financial results for the third quarter ended November 1, 2025.

Brendan Hoffman, Chief Executive Officer of VNCE said, “We are extremely proud of our third quarter performance, delivering healthy sales growth across all channels while exceeding expectations for both top and bottom line results. Our direct-to-consumer segment is showing broad-based strength benefiting from enhancements we have made to the customer experience. This includes the store renovations from earlier this year, as well as an e-commerce site refresh, increased marketing support, and the launch of drop-ship capabilities expanding the breadth and depth of our assortment online in the third quarter. This momentum has continued into the fourth quarter with a record holiday sales weekend in direct-to-consumer. As we look ahead, I’m more confident than ever in our trajectory as we successfully balance disciplined execution with strategic reinvestment to position the Vince Holding Corp. platform for sustained long-term profitable growth.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures and Exhibit 3 and Exhibit 4 to this press release for a reconciliation of GAAP measures to such non-GAAP measures.

For the third quarter ended November 1, 2025:

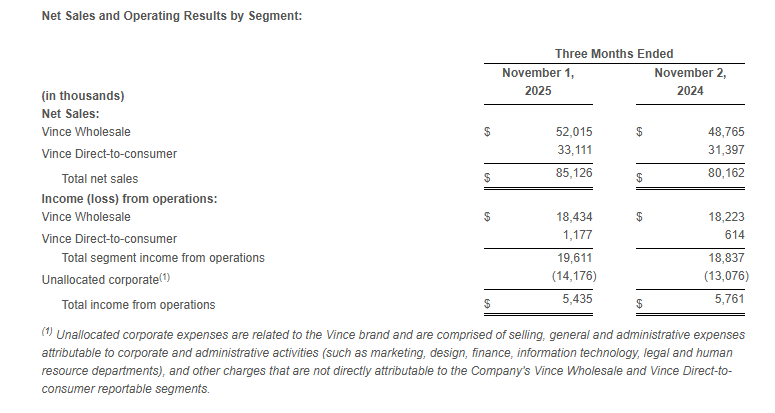

Total Company net sales increased 6.2% to $85.1 million compared to $80.2 million in the third quarter of fiscal 2024. The year-over-year increase was driven by a 6.7% increase in the wholesale segment and a 5.5% increase in direct-to-consumer segment.

Gross profit was $41.9 million, or 49.2% of net sales, compared to gross profit of $40.1 million, or 50.0% of net sales, in the third quarter of fiscal 2024. The decrease in gross margin rate was primarily driven by approximately 260 basis points due to the unfavorable impact of higher tariffs and approximately 100 basis points due to increased freight costs, partially offset by a 140 basis points increase due to the favorable impact of lower product costing and higher pricing, and approximately 110 basis points due to the favorable impact of lower discounting.

Selling, general, and administrative expenses were $36.5 million, or 42.8% of sales, compared to $34.3 million, or 42.8% of sales, in the third quarter of fiscal 2024. The increase in SG&A dollars was primarily driven by compensation and benefits and marketing and advertising costs.

Income from operations was $5.4 million compared to income from operations of $5.8 million in the same period last year.

Income tax expense was $2.0 million compared to an income tax expense of $0 in the same period last year. The increase is due to the impact of applying the Company’s estimated annual effective tax rate to the year-to-date ordinary pre-tax income. In the prior comparative period, the Company had year-to-date ordinary pre-tax losses for the interim period and as such, the Company did not record any tax expense.

Net income was $2.7 million or $0.21 per diluted share compared to net income of $4.3 million or $0.34 per diluted share in the same period last year.

Adjusted EBITDA* was $6.5 million compared to $7.4 million in the same period last year.

The Company ended the quarter with 60 company-operated Vince stores, a net decrease of 1 store since the third quarter of fiscal 2024.

Third Quarter Review

Net sales increased 6.2% to $85.1 million as compared to the third quarter of fiscal 2024.

Wholesale segment sales increased 6.7% to $52.0 million compared to the third quarter of fiscal 2024.

Direct-to-consumer segment sales increased 5.5% to $33.1 million compared to the third quarter of fiscal 2024.

Income from operations excluding unallocated corporate expenses was $19.6 million compared to income from operations of $18.8 million in the same period last year.

Balance Sheet

At the end of the third quarter of fiscal 2025, total borrowings under the Company’s debt agreements totaled $36.1 million and the Company had $47.3 million of excess availability under its revolving credit facility.

Net inventory at the end of the third quarter of fiscal 2025 was $75.9 million compared to $63.8 million at the end of the third quarter of fiscal 2024. The year-over-year increase in inventory includes approximately $4.2 million of higher inventory carrying value due to tariffs.

During the quarter ended November 1, 2025, the Company issued and sold 370,878 shares of common stock under the Virtu At-the-Market Offering for aggregate net proceeds of $1,291 at an average price of $3.55 per share. The Company continues to have shares available under the program to exercise with proceeds to be used as sources, along with cash from operations, to fund future growth.

Outlook

For the fourth quarter of fiscal 2025 the Company expects the following:

Net sales to increase approximately 3% to 7% compared to the prior year period.

Adjusted operating income as a percentage of net sales to be approximately 0% to 2%.

Adjusted EBITDA as a percentage of net sales to be approximately 2% to 4%.

For fiscal 2025 the Company expects the following:

Net sales to increase approximately 2% to 3% compared to the prior year.

Adjusted operating income as a percentage of net sales to be approximately 2% to 3%.

Adjusted EBITDA as a percentage of net sales to be approximately 4% to 5%.

The above guidance for the fourth quarter of fiscal 2025 assumes $4 million to $5 million in expected incremental tariff costs, of which the Company expects to continue to partially offset through its mitigation strategies.

Strategic Partnership with Authentic Brands Group

On May 25, 2023, the Company announced that it completed the previously announced transaction (the “Authentic Transaction”) with Authentic Brands Group (“Authentic”).

In connection with the Authentic Transaction, VNCE entered into an exclusive, long-term license agreement (the “License Agreement”) with Authentic for usage of the contributed intellectual property for VNCE’s existing business in a manner consistent with the Company’s current wholesale, retail and e-commerce operations. The License Agreement contains an initial ten-year term and eight ten-year renewal options allowing VNCE to renew the agreement.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three and nine months ended November 1, 2025 and November 2, 2024, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, capitalized cloud computing amortization, ERC benefit, and gain on sale of Rebecca Taylor, Inc. and its wholly owned subsidiary (“Gain on Sale of Subsidiary”). For the three and nine months ended November 1, 2025 and November 2, 2024, respectively, the Company has provided adjusted income from operations, adjusted income (loss) before income taxes and equity in net income of equity method investment, adjusted income before equity in net income of equity method investment, adjusted net income, and adjusted earnings per share, which are non-GAAP measures, in order to eliminate the effect of the ERC benefit, Discrete Tax Effect Associated with ERC benefit, and Gain on Sale of Subsidiary.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 and Exhibit 4 to this press release.

Conference Call

A conference call to discuss the third quarter results will be held today, December 9, 2025, at 8:30 a.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (833) 470-1428, conference ID 579552. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail company that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 46 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Seasoned Technology Executive to Drive AI, Digital Commerce, and Cybersecurity Innovation

JERICHO, N.Y., Dec. 8, 2025 /PRNewswire/ — Today, 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of thoughtful expressions designed to help inspire customers to express and connect, announced the appointment of Alexander Zelikovsky as Chief Information Officer. Zelikovsky’s appointment accelerates the company’s ongoing transformation strategy under CEO Adolfo Villagomez.

As Chief Information Officer, Zelikovsky will lead an enterprise-wide technology strategy to accelerate the company’s digital transformation. His responsibilities include IT applications and platforms, data architecture, data management, cybersecurity, and business intelligence. Zelikovsky will also support the organization’s AI and business optimization efforts by ensuring the technology, data, and platforms are in place to help these initiatives succeed — strengthening the company’s ability to deliver exceptional customer-centric experiences and drive omnichannel growth. He will report directly to 1-800-FLOWERS.COM, Inc. CEO Adolfo Villagomez.

“Alex is a visionary technology leader with proven expertise leading digital transformation initiatives at scale,” said Adolfo Villagomez, CEO of 1-800-FLOWERS.COM, Inc. “His ability to position technology to fuel business growth, enhance operational efficiency, and deliver personalized customer experiences is all critical to driving our transformation strategy forward. His experience in enterprise modernization, AI, and cybersecurity will be instrumental in accelerating growth and innovation across our portfolio. We are thrilled to have Alex join the organization.”

Zelikovsky brings more than 25 years of technology leadership experience, transforming traditional businesses into digital enterprises at global scale. Most recently, he served as Executive Vice President and Global CIO at Pitney Bowes. Prior to that, he held divisional CIO and Head of Digital Technology roles at Kimberly-Clark for both the EMEA and Latin America regions, where he executed comprehensive IT transformation strategies that drove significant business turnarounds and operating profit growth.

“I’m excited to join 1-800-FLOWERS.COM at such a pivotal time in the company’s transformation,” said Zelikovsky. “Adolfo’s vision for building a consumer-centric organization resonates deeply with my approach to technology leadership. The company has built an exceptional portfolio of brands and understands the importance of delivering meaningful and personalized customer experiences. I look forward to partnering with the leadership team to harness technology, data, and innovation to deepen customer relationships, drive operational excellence, and accelerate growth across the business.”

Before joining Kimberly-Clark, Zelikovsky drove the development and execution of Bed Bath & Beyond’s omnichannel technology strategy and was instrumental in building out their multibillion-dollar digital commerce business. His journey into digital technology began at Amazon.com, where he was part of the team that pioneered Amazon’s global distribution network. He has also held senior technology and operations roles at Procter & Gamble and Sephora/LVMH.

Zelikovsky holds an MBA from the University of Chicago’s Booth School of Business and a bachelor’s degree from Brooklyn College, City University of New York. He is the author of “Achieving Stretch Goals Efficiently” and has served as an adjunct professor at Purdue University’s Krannert School of Management, where he developed and taught a graduate course in e-Commerce Strategy and Operations.

About 1-800-FLOWERS.COM, Inc. 1-800-FLOWERS.COM, Inc. is the premier destination for meaningful gifting, helping people express and connect through thoughtful giving. As an omnichannel retailer, the company’s portfolio includes more than 18 premium brands, such as 1-800-Flowers.com®, Harry & David®, PersonalizationMall.com®, and Things Remembered®. 1-800-FLOWERS.COM, Inc. also supports local community businesses nationwide through BloomNet®, its network of local florists and merchants, that enables same-day delivery. The company also operates Napco®, a leading resource for floral gifts and seasonal décor, and DesignPac Gifts, LLC, a manufacturer of gift baskets and towers

Netflix’s landmark $72 billion acquisition of Warner Bros.’ studios and HBO Max marks one of the most transformative moments in modern entertainment history — a move that not only reshapes Hollywood’s power structure but also sends meaningful ripple effects through the small- and micro-cap media and technology ecosystem.

Announced Friday, the agreement gives Netflix control of Warner Bros.’ iconic film and TV library, including franchises like Harry Potter, DC, The Sopranos, Game of Thrones, and Friends, along with the HBO Max streaming platform. The deal is expected to close following Warner Bros. Discovery’s plan to spin off its Global Networks division in 2026, creating a new publicly traded entity housing CNN and its linear cable assets.

The acquisition is historic for Netflix, a company that has primarily built its empire through original content rather than mergers. As of Q3, nearly two-thirds of its content library consists of originals, with no single show representing more than 1% of viewership. This diversification insulated Netflix from industry consolidation — but the streaming landscape has changed dramatically.

With HBO Max, Paramount+, and Peacock all struggling to scale, analysts widely believe only a handful of global players will survive. Securing Warner Bros.’ intellectual property may not just be strategic — it may be defensive, ensuring that no rival streaming service gains control of one of Hollywood’s deepest content vaults.

The Small & Micro-Cap Effect: Why This Deal Matters Down the Ladder

While mega-cap giants are the headline story, the implications for small and micro-cap entertainment, production, and streaming-adjacent companies could be significant.

This consolidation wave often results in:

• Increased demand for independent content: As major studios merge, they frequently trim internal production pipelines. This opens opportunities for small-cap and micro-cap production houses, animation studios, and niche content creators that can sell or license projects to fill larger platforms’ volume needs.

• Rising valuations for niche streaming and IP owners: Micro-streamers, genre-focused platforms, and specialty content IP holders often benefit from industry shakeups. With the “big three” fighting for subscriber retention, specialty libraries — from horror to anime to sports archives — tend to gain acquisition interest or licensing deals.

• Technology spillover: Cloud providers, AI-driven media startups, captioning tech, localization companies, and compression software developers — many of which fall in the micro-cap category — may see increased demand as larger platforms race to integrate and scale newly combined content libraries.

• Greater pressure on small-cap competitors: Independent media companies without premium IP or distribution scale could feel heightened pressure. Some may become acquisition targets; others may need to pivot toward niche verticals to remain competitive.

In essence, mega-mergers at the top often spark a wave of secondary deals at the bottom.

Regulatory Uncertainty Still Looms

Like other bidders, Netflix will face intense regulatory scrutiny given its global scale. Analysts note that Paramount would have had the cleanest approval path. Meanwhile, competitor pressure may persist — both Paramount and Comcast could re-engage or attempt to challenge the deal’s fairness.

Still, Netflix ultimately prevailed thanks to one key advantage: liquidity. The final agreement provides each WBD shareholder $23.25 in cash and $4.50 in Netflix stock, demonstrating Netflix’s willingness to pay up to secure long-term streaming dominance.

A New Era of Entertainment

If approved, the acquisition unites a century of Warner Bros. storytelling with the world’s largest streaming platform — a fusion that could define the next chapter of global content.

For small and micro-cap players, the message is clear: Another consolidation wave is here, and the companies able to adapt quickly — or strategically position themselves as acquisition targets — stand to benefit the most.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Debt Acceleration. In an 8-K filing, FAT Brands disclosed on November 17, 2025, that the Company received notices of acceleration from UMB with respect to Securitization Notes issued by FAT Brands GFG Royalty I, LLC, FAT Brands Royalty I, LLC, FAT Brands Fazoli’s Native I, LLC, and Twin Hospitality I, LLC. The Acceleration Notices basically state that all amounts outstanding under the Notes are immediately due and payable. FAT Brands does not have the capital to repay all amounts due under the Notes.

Past Negotiations. In a November 14th 8-K filing, FAT Brands reported “cleansing material” related to the negotiations to modify the outstanding debt. In our view, there appears to be significant agreement on many issues, with key differences being the timing of certain items, certain payments to management and/or outside parties, and parties to receive certain reports.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile application. Codere currently operates in its core markets of Spain, Italy, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence in the region.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 Results. The company reported Q3 revenue of €51.6 million, essentially flat with the prior year period and below our estimate of €56.0 million. Adj. EBITDA of €2.9 million was modestly better than our estimate of €2.6 million. Notably, when excluding the impact of the Mexican Peso devaluation in Q3, revenue was up roughly 3% over the prior year period.

Solid fundamentals. Notably, while the company benefited from an 11% increase in monthly active customers, it was largely offset by a 10% decrease in monthly average spend, primarily attributed to the Mexican Peso devaluation. Moreover, the company recorded 85,000 first-time deposit customers in Q3, a 26% y-o-y. Importantly, the company’s cost per acquisition was €167, which is its lowest since Q1 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, Nov. 24, 2025 (GLOBE NEWSWIRE) — Xcel Brands, Inc. (NASDAQ: XELB), an industry-leading media and consumer products company specializing in building influencer-driven brands through social commerce and livestreaming, is proud to announce a new partnership between Longaberger and Shannon Doherty, creator of At Home with Shannon. Together, they will introduce a new collection designed to bring warmth, style, and functionality to every home.

With Longaberger’s long-standing tradition of American craftsmanship and Shannon’s approachable, family-centered lifestyle brand, this partnership blends heritage with heart. The collaboration celebrates the beauty of everyday living and reimagines the home as a place for connection, creativity, and comfort.

“I believe that home is where we build our memories and Longaberger has always represented the kind of home I try to create – warm, intentional and filled with heart. I am honored to bring my vision to a brand with such a beautiful legacy; and together, design pieces that help families celebrate those everyday moments,” said Shannon Doherty, founder of At Home with Shannon.

Robert W. D’Loren, Chairman and CEO of Xcel Brands, said, “Shannon’s authenticity and the genuine connection she has built with her community make her an ideal partner for Longaberger. Together, we are creating a vision for the modern home that honors tradition while celebrating how families live today.”

From cozy entertaining pieces to functional storage and timeless accents, each item will embody Longaberger’s handcrafted quality paired with Shannon’s signature warmth and approachability. This partnership continues Xcel Brands’ commitment to developing innovative, creator-led brands that connect deeply with today’s consumers through authenticity, design, and storytelling. For more information, visit www.longaberger.com or www.xcelbrands.com

About Xcel Brands Xcel Brands, Inc. (NASDAQ: XELB) is a media and consumer products company engaged in the design, licensing, marketing, live streaming, and social commerce sales of branded apparel, footwear, accessories, fine jewelry, home goods and other consumer products, and the acquisition of dynamic consumer lifestyle brands. Xcel was founded in 2011 with a vision to reimagine shopping, entertainment, and social media as social commerce. Xcel owns the Halston, Judith Ripka, and C. Wonder brands, as well as the co-branded collaboration brands Towerhill by Christie Brinkley, Trust. Respect. Love by Cesar Millan, GemmaMade by Gemma Stafford, and a brand in development with Coco Rocha and also holds noncontrolling interests or long-term license agreements in the Isaac Mizrahi brand, Orme Live, and Mesa Mia by Jenny Martinez. Xcel also owns and manages the Longaberger brand through its controlling interest in Longaberger Licensing, LLC. Xcel is pioneering a true modern consumer products sales strategy which includes the promotion and sale of products under its brands through interactive television, digital live-stream shopping, social commerce, brick-and-mortar retailers, and e-commerce channels to be everywhere its customers shop. The company’s brands have generated in excess of $5 billion in retail sales via livestreaming in interactive television and digital channels alone, and over 20,000 hours of content production time in live-stream and social commerce. The brand portfolio reaches in excess of 43 million social media followers with broadcast reach into 200 million households. Headquartered in New York City, Xcel Brands is led by an executive team with significant live streaming, production, merchandising, design, marketing, retailing, and licensing experience, and a proven track record of success in elevating branded consumer products companies. For more information, visit www.xcelbrands.com.

About Longaberger Longaberger, founded by Dave Longaberger in 1973, is an American home collectibles brand known for artisanal handcrafted products. For generations, Longaberger has manufactured handmade maple baskets and home products that are collected by a loyal community of customers. In 2019, Xcel Brands acquired The Longaberger Company and launched with a new digital social selling business model, offering timeless and modern décor products that inspire a highly engaged community. For more company information, visit the website at longaberger.com or on social media at @longaberger, #longaberger and #thelongabergerfamily.

About Shannon Doherty Shannon Doherty is the founder and voice behind At Home with Shannon, a lifestyle platform rooted in her life as a mom of four. She shares décor ideas, simple DIYs, family routines, and cooking inspiration through her social channels, reaching millions who appreciate real, heart-led content. Her approach to home is grounded in authenticity, accessibility, and joy.

US consumer sentiment weakened again in November, underscoring the growing strain households feel from higher prices, softer income growth, and persistent anxiety about job security. Despite a modest improvement after the government shutdown ended, consumers remain broadly pessimistic and increasingly concerned about their financial future.

According to the University of Michigan’s final November reading, overall sentiment ticked up slightly to 51 after briefly plunging earlier in the month. But even with the rebound, confidence remains well below October’s level and sits nearly 30% lower than a year ago. For many Americans, the temporary resolution of the government funding crisis brought some short-term relief, but not enough to offset the everyday pressure of rising costs and weaker purchasing power.

One major factor weighing on households is continued inflation. While expectations for year-ahead inflation edged down to 4.5%, most consumers say they still feel the squeeze from higher prices for essentials like food, rent, utilities, and healthcare. The anticipated jump in health insurance premiums heading into 2026 has added another layer of financial worry, especially for families already stretched thin.

Incomes are another pain point. Many workers report that their earnings aren’t keeping up with rising costs, leading to a decline of about 15% in consumers’ assessments of their current financial situation. Even individuals who felt secure earlier in the fall have grown more cautious as the economic outlook becomes increasingly uncertain.

Labor-market concerns are also accelerating. The unemployment rate is higher than a year ago, and layoffs across several industries have heightened anxiety. Nearly seven out of ten consumers now expect unemployment to rise over the next year — more than double the share from this time in 2024. Many also feel more vulnerable personally, with the perceived likelihood of job loss rising to its highest point since 2020.

The mood among younger adults is even more troubling. For Americans aged 18 to 34, expectations around job loss over the next five years have climbed to their highest level in more than a decade. Younger workers, many of whom are early in their careers or managing student loan burdens, are increasingly uneasy about their career stability and long-term financial prospects.

Even wealthier households are not immune. Consumers with large stock holdings initially saw sentiment improve earlier in November, but market declines wiped out those gains. Volatile markets combined with the broader economic uncertainty have contributed to renewed caution among investors and higher-income earners.

Overall, the November data paints a picture of an economy where the shutdown may have ended, but its psychological impact lingers. With government funding only secured through January, uncertainty about future disruptions remains. Households are preparing for the possibility of more instability at a time when budgets are already strained.

The combination of stubborn inflation, weakening income growth, elevated recession fears, and unstable policy conditions continues to erode Americans’ confidence. While the economy has avoided a sharp downturn so far, consumers appear increasingly doubtful that the months ahead will bring meaningful improvement.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 Results. The company reported Q3 revenue of $1.1 million and an adj. EBITDA loss of $0.7 million, both of which were modestly lower than our estimates of $1.6 million and a loss of $0.2 million, respectively, as illustrated in Figure #1 Q3 Results. Notably, sales for C. Wonder and Christie Brinkley’s TWRHLL were disrupted by tariff-related vendor issues and HSN’s studio transition during Q3, which have since been resolved.

Strategic partnerships. The company’s new influencer brands, with Jenny Martinez, Gemma Stafford, Cesar Millan, and Coco Rocha, are expected to launch in Q1 2026. Notably, these celebrity partnerships drove the increase in the company’s social media following from 5 million at the start of the year to its current following of 46 million. In our view, the company is well positioned to reach its goal of 100 million social media followers in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition. Twin Hospitality has entered into a letter of intent to acquire eight Twin Peaks franchised restaurants in Florida from DMD Ventures, LLC for approximately $47 million in cash. We view this strategic transaction as an opportunistic investment in a key growth market, even as the Company’s long-term focus remains on franchise driven expansion.

Details. The acquisition will bring the following Florida locations to Company ownership: Davie, Fort Myers, West Palm Beach, Pembroke Pines, Hollywood, Cypress Creek, Doral and Naples. Upon completion, the transaction is expected to contribute approximately $76-$77 million in annual revenue and $9-$10 million in additional annual EBITDA, representing an EV/Sales multiple of 0.6x and an EV/EBITDA multiple of approximately 5x, a discount to TWNP’s current trading multiples.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")