For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fiscal Q1 results better than expected. Total company revenues of $269.1 million, which declined 11.4% from a year earlier, beat our estimate of $249.9 million, driven by better results in each of its operating segments. The revenue decrease represented a significant moderation from the 17.9% decline in its fiscal Q4. The seasonal adj. EBITDA loss of $22.0 million was better than our loss estimate of $27.8 million.

Improving margin outlook still favorable. Gross margins in the latest quarter improved 450 basis points from 33.4% to 37.9% due to lower ocean freight costs, moderating commodity prices, and lower inventory write-offs. While ocean freight prices have returned to near pre-Covid levels, there is still significant margin expansion opportunities as commodity prices moderate. We anticipate that full fiscal year 2024 gross margins should improve from 37.5% in 2023 to 39.3% in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q23 Results. Revenue of $246.7 million was down 1.9% y-o-y, and slightly below our $255 million estimate, mostly due to a COVID related backlog in Asia-Pacific last year that was not repeated this year. Adjusted EBITDA came in at $16.6 million, up 16.1% y-o-y, and in-line with our $17 million estimate. GAAP and adjusted net income was $7.3 million, or $0.22/sh, compared to GAAP $3.6 million, or $0.11/sh, and adjusted $5.1 million, or $0.15/sh, last year. We had forecast net income of $7.2 million, or $0.21/sh.

Segments. Vehicle Solutions revenue was $145.4 million compared to $154 million last year, while operating income was $10.9 million versus $9.6 million. Electrical Systems revenue was $53.9 million versus $46.1 million and operating income grew to $5.9 million from $5.2 million. Aftermarket revenue was $34.4 million, down from $37.1 million and operating income was $4.5 million compared to $5.0 million. Industrial Automation revenue was $13.0 million compared to $14.1 million and segment operating income was $0.7 million compared to an operating loss of $1.0 million last year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The acclaimed culinary chef and Masters of Meat join forces to support military, veteran, and first responder personnel.

Plantation, Fla., Oct. 31, 2023 (GLOBE NEWSWIRE) — Smokey Bones today announces that world-class culinary personality and philanthropist, Chef Robert Irvine, will join the Masters of Meat to introduce a limited-time menu, Robert’s Ribfeast, starting on October 31, 2023. Fans are asked to bring their appetites to try this delicious new menu, which will benefit the Robert Irvine Foundation, dedicated to transforming the lives of service members, veterans, first responders and their families. Smokey Bones has committed to donate 10 percent of sales from “Robert’s Ribfeast” promotion, up to $100,000.

As a Smokey Bones fan and loyalist, particularly of its award-winning ribs, Chef Irvine is working with the brand to share good food with guests while supporting and showing appreciation for the country’s military and veterans. Robert’s Ribfeast includes:

Robert’s Ribfeast for One ($19.99): A half-rack of Smokey Bones’ signature house-smoked St. Louis ribs, two sides, a piece of garlic bread, and choice of appetizer or dessert.

Ribfeast for Two ($29.99): A full rack of St. Louis ribs, four sides, two pieces of garlic bread, and choice of appetizer or dessert.

“We are honored to partner with Chef Irvine, who shares our appreciation for not only our ribs but also for our active-duty military and veterans,” said Cole Robillard, Chief Marketing Officer at Smokey Bones. “Chef Irvine is a frequent guest at Smokey Bones and a natural fit for our brand as he has made a significant impact on both the restaurant industry and military community. We are excited to not only offer guests a terrific deal on his favorite meal, but to bring our communities together to support this important cause.”

Chef Irvine is an acclaimed chef, entrepreneur, and longtime philanthropic supporter of America’s military. He’s also the host of Food Network’s hit show “Restaurant: Impossible,” where he gives struggling restaurateurs a second chance to turn their lives and businesses around.

“We are thankful for the generosity of Smokey Bones in their efforts to support the Robert Irvine Foundation,” said Chef Irvine. “These funds will go towards our Food, Wellness, Community, and Financial-Support programs which impact thousands of service members, veterans and their families. We look forward to kicking off this partnership with the Masters of Meat in supporting America’s heroes.”

Robert’s Ribfeast will be available at all Smokey Bones locations until January 1, 2024, while supplies last.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Smokey Bones, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Smokey Bones

The ‘Masters of Meat,’ Smokey Bones is a full-service restaurant delivering great barbecue, award-winning ribs, crave-worthy cocktails and memorable moments in 61 locations across 16 states. Smokey Bones serves lunch, dinner, and late night every day. Smokey Bones also has a full bar featuring a variety of bourbons and whiskeys; a selection of domestic, import and local craft beers; and signature, handcrafted cocktails. Smokey Bones offers a 10 percent discount to active duty and veterans with ID.

About the Robert Irvine Foundation

The Robert Irvine Foundation was established by chef, entrepreneur and TV personality Robert Irvine. The Robert Irvine Foundation supports and strengthens the physical and mental well-being of our service members, veterans, first responders, and their families. They provide these heroes with life-changing opportunities that unlock the potential in their personal and professional lives through food, wellness, community, and financial support. For more information, please visit: www.robertirvinefoundation.org.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating coverage with Outperform rating and $3.50 price target. Xcel Brands is a fashion apparel company, boasting several well-known and iconic brands, such as Isaac Mizrahi and Halston. In our view, the company is on the cusp of a new, profitable growth era, after its recent business model transformation to an asset-light, brand licensor.

Business model transformation. The new licensing business model is expected to significantly lower the company’s costs, eliminating warehousing and inventory costs as well as capital expenditure needs. We believe this repositioning of the business is a key catalyst for the company to swing towards positive cash flow generation later this year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

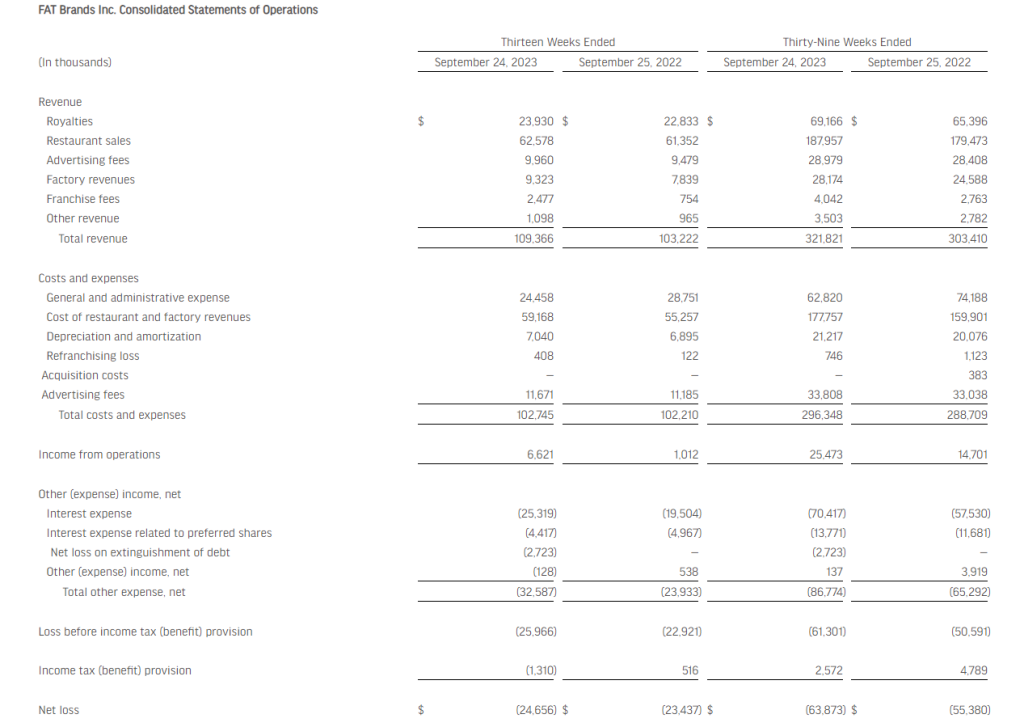

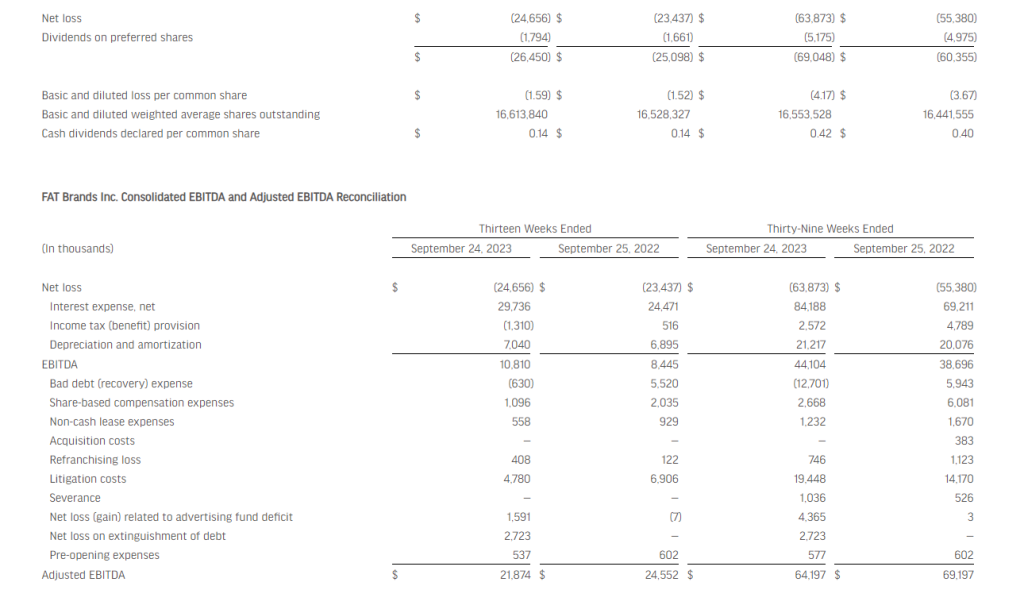

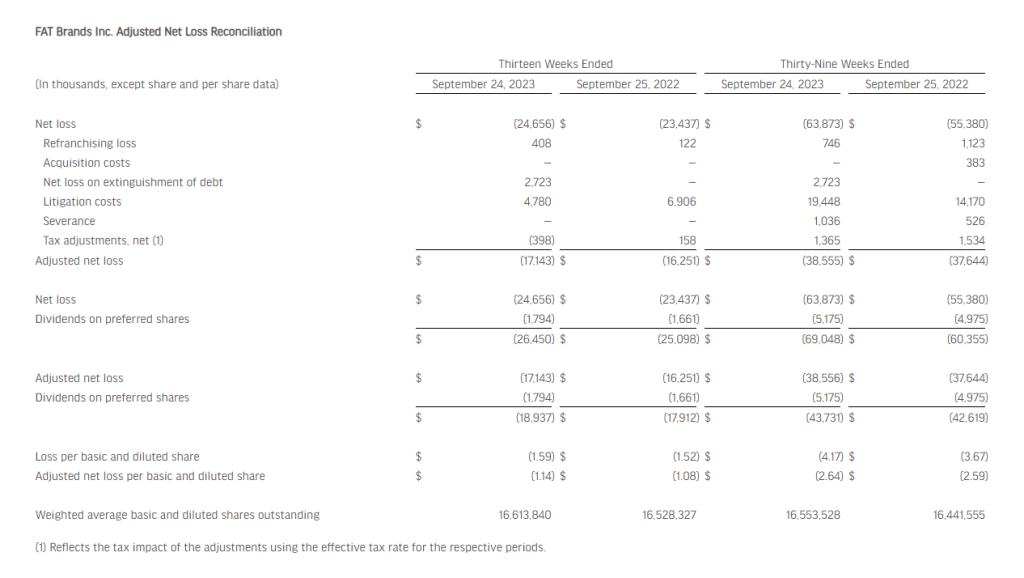

3Q23 Results. FAT Brands reported 3Q23 revenue of $109.4 million, up 6% y-o-y from $103.2 million in the year ago quarter. System-wide sales growth was 0.8%. FAT reported adjusted EBITDA of $21.9 million in the quarter, compared to $24.6 million in 3Q22 (which included $7.2 million of tax credits). Net loss for the quarter was $26.5 million, or $1.59/sh, compared to a net loss of $25.1 million, or $1.52/sh last year. Adjusted net loss for the quarter was $18.9 million, or $1.14/sh, compared to a net loss of $17.9 million, or a loss of $1.08/sh, last year. We had projected revenue of $107 million and a net loss of $28.4 million, or a loss of $1.71/sh.

Ongoing Development. YTD, FAT has opened 96 restaurants, including 30 in 3Q. The Company expects to see 150 openings 2023. YTD, over 200 new franchise agreements have been signed, bringing the total pipeline to over 1,100 signed agreements. This pipeline will add some $60 million to adjusted EBITDA.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

LOS ANGELES, Oct. 26, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”) today reported financial results for the fiscal third quarter ended September 24, 2023.

Andy Wiederhorn, Chairman of FAT Brands, commented, “With the acquisition of Smokey Bones early in the fourth quarter, we have grown the FAT Brands portfolio to 18 iconic restaurant brands with annualized system wide sales of $2.4 billion. Year to date through the third quarter, we have opened 96 restaurants, including 30 that opened in the third quarter, and are on track to open 150 new restaurants in 2023. We are seeing strong franchisee interest in development opportunities, having signed over 200 development agreements in 2023, bringing our total pipeline to over 1,100 units. This represents the potential for over 50% EBITDA growth over the next several years.”

Rob Rosen, Co-Chief Executive Officer of FAT Brands, commented, “While franchise interest remains high across all of our brands, we continue to be focused on the expansion of Twin Peaks. This year, we plan to open 15 to 17 new lodges, of which 11 have been opened so far. We expect to end the year with over 110 lodges, a 35% increase since acquiring the brand in 2021. Our growth pipeline includes over 125 lodges and Smokey Bones’ healthy real estate portfolio provides us with the opportunity to convert over 40 locations into Twin Peaks lodges, with the potential to significantly accelerate the growth of the brand.”

Ken Kuick, Co-Chief Executive Officer of FAT Brands, commented, “We believe there are significant opportunities on the horizon for FAT Brands. Our seasoned leadership team and strong brand management platform allow us to efficiently integrate new brands while maintaining a healthy and evolving pipeline for organic growth. These strengths position us for continued growth in the future, which will help deleverage our balance sheet.”

Fiscal ThirdQuarter 2023Highlights

• Total revenue improved 6.0% to $109.4 million compared to $103.2 million in the fiscal third quarter of 2022

◦ System-wide sales growth of 0.8% in the fiscal third quarter of 2023 compared to the prior year fiscal quarter ◦ Year-to-date system-wide same-store sales growth of 1.3% in the fiscal third quarter of 2023 compared to the prior year ◦ 30 new store openings during the fiscal third quarter of 2023

• Net loss of $24.7 million, or $1.59 per diluted share, compared to $23.4 million, or $1.52 per diluted share, in the fiscal third quarter of 2022 • Adjusted EBITDA(1) of $21.9 million compared to $24.6 million in the fiscal third quarter of 2022 • Adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, compared to adjusted net loss of $16.3 million, or $1.08 per diluted share, in the fiscal third quarter of 2022

(1) EBITDA, Adjusted EBITDA and adjusted net loss are non-GAAP measures defined below, under “Non-GAAP Measures”. Reconciliation of GAAP net loss to EBITDA, adjusted EBITDA and adjusted net loss are included in the accompanying financial tables.

Summary of Fiscal ThirdQuarter 2023Financial Results

Total revenue increased $6.2 million, or 6.0%, in the third quarter of 2023 to $109.4 million compared to $103.2 million in the same period of 2022, driven by a 4.8% increase in royalties, a 2.0% increase in company-owned restaurant revenues, a 228.5% increase in franchise fees and an 18.9% increase in revenues from our manufacturing facility.

Costs and expenses consist of general and administrative expense, cost of restaurant and factory revenues, depreciation and amortization, refranchising net loss and advertising fees. Costs and expenses remained largely unchanged in the third quarter, increasing 0.5% in the third quarter of 2023 compared to the same period in the prior year.

General and administrative expense decreased $4.3 million, or 14.9%, in the third quarter of 2023 compared to the same period in the prior year, primarily due to the recognition of $1.0 million related to Employee Retention Credits during the third quarter of 2023 and lower professional fees related to certain litigation matters.

Cost of restaurant and factory revenues increased $3.9 million, or 7.1%, in the third quarter of 2023 compared to the same period in the prior year, primarily due to Employee Retention Credits recognized during the third quarter of 2022 and higher company-owned restaurant and dough factory revenues.

Depreciation and amortization increased $0.1 million, or 2.1% in the third quarter of 2023 compared to the same period in the prior year, primarily due to depreciation of new property and equipment at company-owned restaurant locations.

Advertising expenses in the third quarter of 2023 increased $0.5 million compared to the prior year period. These expenses vary in relation to advertising revenues.

Total other expense, net, for the third quarter of 2023 and 2022 was $32.6 million and $23.9 million, respectively, which is inclusive of interest expense of $29.7 million and $24.5 million, respectively. Total other expense, net for the third quarter of 2023 also included a $2.7 million net loss on extinguishment of debt.

Adjusted net loss(1) of $17.1 million, or $1.14 per diluted share, compared to adjusted net loss of $16.3 million, or $1.08 per diluted share, in the fiscal third quarter of 2022.

Key Financial Definitions

New store openings – The number of new store openings reflects the number of stores opened during a particular reporting period. The total number of new stores per reporting period and the timing of stores openings has, and will continue to have, an impact on our results.

Same-store sales growth – Same-store sales growth reflects the change in year-over-year sales for the comparable store base, which we define as the number of stores open and in the FAT Brands system for at least one full fiscal year. For stores that were temporarily closed, sales in the current and prior period are adjusted accordingly. Given our focused marketing efforts and public excitement surrounding each opening, new stores often experience an initial start-up period with considerably higher than average sales volumes, which subsequently decrease to stabilized levels after three to six months. Additionally, when we acquire a brand, it may take several months to integrate fully each location of said brand into the FAT Brands platform. Thus, we do not include stores in the comparable base until they have been open and in the FAT Brands system for at least one full fiscal year.

System-wide sales growth – System wide sales growth reflects the percentage change in sales in any given fiscal period compared to the prior fiscal period for all stores in that brand only when the brand is owned by FAT Brands. Because of acquisitions, new store openings and store closures, the stores open throughout both fiscal periods being compared may be different from period to period.

Conference Call and Webcast

FAT Brands will host a conference call and webcast to discuss its fiscal third quarter 2023 financial results today at 4:30 PM ET. Hosting the conference call and webcast will be Andy Wiederhorn, Chairman of the Board, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call can be accessed live over the phone by dialing 1-844-826-3035 from the U.S. or 1-412-317-5195 internationally. A replay will be available after the call until Thursday, November 16, 2023, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 10183290. The webcast will be available at www.fatbrands.com under the “Investors” section and will be archived on the site shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Smokey Bones, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses and franchises and owns approximately 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the future financial and operating results of the Company, estimates of future EBITDA, the timing and performance of new store openings, future reductions in cost of capital and leverage ratio, our ability to conduct future accretive acquisitions and our pipeline of new store locations. Forward-looking statements generally use words such as “expect,” “foresee,” “anticipate,” “believe,” “project,” “should,” “estimate,” “will,” “plans,” “forecast,” and similar expressions, and reflect our expectations concerning the future. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other risks and uncertainties that could cause our actual results to differ materially from our current expectations and from the forward-looking statements contained in this press release. We undertake no obligation to update any forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Non-GAAP Measures (Unaudited)

This press release includes the non-GAAP financial measures of EBITDA, adjusted EBITDA and adjusted net loss.

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. We use the term EBITDA, as opposed to income from operations, as it is widely used by analysts, investors, and other interested parties to evaluate companies in our industry. We believe that EBITDA is an appropriate measure of operating performance because it eliminates the impact of expenses that do not relate to business performance. EBITDA is not a measure of our financial performance or liquidity that is determined in accordance with generally accepted accounting principles (“GAAP”), and should not be considered as an alternative to net loss as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP.

Adjusted EBITDA is defined as EBITDA (as defined above), excluding expenses related to acquisitions, refranchising loss, impairment charges, and certain non-recurring or non-cash items that the Company does not believe directly reflect its core operations and may not be indicative of the Company’s recurring business operations.

Adjusted net loss is a supplemental measure of financial performance that is not required by or presented in accordance with GAAP. Adjusted net loss is defined as net loss plus the impact of adjustments and the tax effects of such adjustments. Adjusted net loss is presented because we believe it helps convey supplemental information to investors regarding our performance, excluding the impact of special items that affect the comparability of results in past quarters to expected results in future quarters. Adjusted net loss as presented may not be comparable to other similarly titled measures of other companies, and our presentation of adjusted net loss should not be construed as an inference that our future results will be unaffected by excluded or unusual items. Our management uses this non-GAAP financial measure to analyze changes in our underlying business from quarter to quarter based on comparable financial results.

Reconciliations of net loss presented in accordance with GAAP to EBITDA, adjusted EBITDA and adjusted net loss are set forth in the tables below.

With more than 60 units, RCI Hospitality Holdings, Inc., through its subsidiaries, is the country’s leading company in adult nightclubs and sports bars/restaurants. Clubs in New York City, Chicago, Dallas-Fort Worth, Houston, Miami, Minneapolis, Denver, St. Louis, Charlotte, Pittsburgh, Raleigh, Louisville, and other markets operate under brand names such as Rick’s Cabaret, XTC, Club Onyx, Vivid Cabaret, Jaguars Club, Tootsie’s Cabaret, Scarlett’s Cabaret, Diamond Cabaret, and PT’s Showclub. Sports bars/restaurants operate under the brand name Bombshells Restaurant & Bar.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Modification. RCI announced the Company modified $15.7 million in debt due October 2024 through extending maturities of the notes to free up more cash to buy back shares. The notes will continue to be unsecured at 12% interest, with $9.1 million due October 1, 2026, interest-only payable monthly, and $6.6 million due November 1, 2027, with monthly payments of interest and principal based on a 10-year amortization.

Buying Up Shares. With the modification in place for the debt, the Company has over $15 million to buy back shares. Using the Company’s closing price on October 26 of $52.70, RCI can purchase up to 297,912 shares. If the Company were to do so, this lowers the Company’s outstanding shares to roughly 9.1 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

BOCA RATON, Fla.–(BUSINESS WIRE)–Oct. 25, 2023– The ODP Corporation (NASDAQ:ODP) (“ODP,” or the “Company”), a leading provider of business services, products and digital workplace technology solutions to businesses and consumers, will announce third quarter 2023 financial results before the market open on Wednesday, November 8th, 2023. The ODP Corporation will webcast a call with financial analysts and investors that day at 9:00 am Eastern Time which will be accessible to the media and the general public.

To listen to the conference call via webcast, please visit The ODP Corporation’s Investor Relations website at investor.theodpcorp.com. A replay of the webcast will be available approximately two hours following the event. A copy of the earnings press release, supplemental financial disclosures and presentation will also be available on the website.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products and services through an integrated business-to-business (B2B) distribution platform and omnichannel presence, which includes world-class supply chain and distribution operations, dedicated sales professionals, a B2B digital procurement solution, online presence and a network of Office Depot and OfficeMax retail stores. Through its operating companies Office Depot, LLC; ODP Business Solutions, LLC; Veyer, LLC; and Varis, Inc., The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

ODP and ODP Business Solutions are trademarks of ODP Business Solutions, LLC. Office Depot is a trademark of The Office Club, LLC. OfficeMax is a trademark of OMX, Inc. Veyer is a trademark of Veyer, LLC. Varis is a trademark of Varis Inc. Grand&Toy is a trademark of Grand & Toy, LLC in Canada. Any other product or company names mentioned herein are the trademarks of their respective owners.

Legendary Chains Merge for the First Time to Serve Up Burgers and Pizzas Under One Roof in Lantana, Texas

LOS ANGELES, Oct. 25, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger, Round Table Pizza, and 16 other restaurant concepts, announces that it has officially opened its first-ever co-branded Fatburger and Round Table Pizza location in Dallas. Situated in the vibrant Lantana neighborhood, the 3,500 sq. foot restaurant offers a full-service, full-bar casual dining experience great for game day. It is the first of four co-branded Fatburger and Round Table Pizza locations planned for the greater Dallas area operated by SNM Management Group.

“We are beyond thrilled to introduce our first co-branded Fatburger and Round Table Pizza concept to Dallas,” says Taylor Wiederhorn, Chief Development Officer of FAT Brands. “This new restaurant will allow guests to enjoy the best of both brands in one space, creating a seamless experience that caters to a range of tastes. With the success Fatburger has seen co-branding with Buffalo’s Cafe and Express, we’re eager to see this new venture with Round Table Pizza flourish.”

Ever since the first Fatburger opened in Los Angeles 70 years ago, the chain has been known for its delicious, grilled-to-perfection and cooked-to-order burgers. Founder Lovie Yancey believed that a big burger with everything on it is a meal in itself; at Fatburger “everything” is not just the usual roster of toppings. Burgers can be customized with everything from bacon and eggs to chili and onion rings. In addition to its famous burgers, the Fatburger menu also includes Fat and Skinny Fries, sweet potato fries, scratch-made onion rings, Impossible™ Burgers, turkeyburgers, hand-breaded crispy chicken sandwiches, and hand-scooped milkshakes made from 100 percent real ice cream.

Since its founding, Round Table Pizza has been recognized as “Pizza Royalty™” for its homemade dough, signature three-cheese blend, and gold-standard ingredients topped to the edge. Customers can enjoy the chain’s proprietary handmade pizzas, salads, baked-to-perfection Garlic Parmesan Twists, classic and boneless wings, and more.

The new co-branded Fatburger and Round Table Pizza location is located at 3701 FM 407 Suite 600, Bartonville, Texas 76226. It is open Sunday to Thursday, 11 a.m. to 10 p.m., and Fridays and Saturdays 11 a.m. to 12 a.m. – perfect for late-night cravings.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Smokey Bones, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Fatburger

An all-American, Hollywood favorite, Fatburger is a fast-casual restaurant serving big, juicy, tasty burgers, crafted specifically to each customer’s liking. With a legacy spanning 70 years, Fatburger’s extraordinary quality and taste inspire fierce loyalty amongst its fan base, which includes a number of A-list celebrities and athletes. Featuring a contemporary design and ambiance, Fatburger offers an unparalleled dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1952 – The Last Great Hamburger Stand™. For more information, visit www.fatburger.com.

About Round Table Pizza

Inspired by the honor, valor, and revelry of the Knights of the Round Table, Round Table Pizza’s® superior pizza and commitment to quality and authenticity have earned the reputation of “Pizza Royalty™” for over 60 years. With more than 410 restaurants across the United States, Round Table celebrates community, family, and making merry. For more information, visit www.roundtablepizza.com.

Pixar | Vera Bradley Toy Story Collection Now Available Nationwide

FORT WAYNE, Ind., Oct. 24, 2023 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) today announced that Vera Bradley, its iconic American bag and luggage lifestyle brand, has collaborated with Disney and Pixar to launch its first-ever collection inspired by the beloved Toy Story franchise.

Celebrating the magic of childhood, friendship and adventure with more than 60 lighthearted styles made especially for new adventures with special friends, the Pixar | Vera Bradley Toy Story Collection includes four new patterns—Andy’s Room, Festive Toy Story, Toy Chest, and Toy Story Sketch—featuring Pixar’s Woody, Buzz Lightyear and the entire Pixar Toy Story gang.

“The Vera Bradley brand came to life more than 40 years ago thanks to the friendship of co-founders Barbara Bradley Baekgaard and Patricia R. Miller, so we are especially excited to celebrate the power of friendship with our new Pixar | Vera Bradley Toy Story Collection,” noted Alison Hiatt, CMO of Vera Bradley, Inc. “Fans of the Disney and Pixar Toy Story franchise are sure to love the colorful, fun and festive patterns and embroidered motifs featuring their favorite Toy Story characters.”

Pixar | Vera Bradley Toy Story Collection styles range in price from $15 to $160 and are perfect for holiday gift-giving. Shop the collection now in Vera Bradley Full Line Stores, participating Vera Bradley retailers and online at www.verabradley.com/disney. Follow @verabradley for updates and to learn more.

ABOUT VERA BRADLEY

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace. Visit www.verabradley.com and follow @verabradley to learn more.

NEW ALBANY, Ohio, Oct. 23, 2023 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI) will hold its quarterly conference call on Thursday, November 2, 2023, at 10:00 a.m. ET, to discuss third quarter 2023 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (888) 259-6580 using conference code 93330617. International participants dial (416) 764-8624 using conference code 93330617. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

A telephonic replay of the conference call will be available until November 16, 2023. To access the replay, toll-free callers can dial (877) 674-7070 using access code 330617.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group [email protected]

LOS ANGELES, Oct. 23, 2023 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 13 other restaurant concepts, today announced that the Company will host a conference call to review its third quarter 2023 financial results on Thursday, October 26, 2023 at 4:30 PM ET. A press release with third quarter 2023 financial results will be issued prior to the conference call that day.

The conference call can be accessed live over the phone by dialing 1-844-826-3035 from the U.S. or 1-412-317-5195 internationally. A replay will be available after the call until Thursday, November 16, 2023, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 10183290. Hosting the call will be Andy Wiederhorn, Chairman, and Ken Kuick, Co-Chief Executive Officer and Chief Financial Officer.

The conference call will also be webcast live from the corporate website at www.fatbrands.com, under the “Investors” section. A replay of the webcast will be available through the corporate website shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 18 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Smokey Bones, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Asset sale-leaseback. On October 19, the company completed the sale-leaseback of 38 bowling centers across 17 states to Vici Properties in exchange for $432.9 million. Notably, the agreement is structured as a 25 year lease with an initial annual rent of $31.6 million. In our view, the favorable transaction should allow for an acceleration of company growth initiatives and debt reduction.

Terms of the agreement. The 25 year lease will increase from the initial amount of $31.6 million by a minimum of 2% and a maximum of 2.5% annually, equating to an acquisition cap rate of 7.3%. The lease agreement stipulates the lessee pays all expenses of the property in addition to rent, and should be treated as a long-term lease, which should have no impact on EBITDA.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.