The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 103 facilities totaling approximately 83,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Tracking Device. Yesterday, a new five-year contract was awarded by Santa Clara County, CA to GEO’s subsidiary BI Inc. regarding the Company’s wrist-worn GPS tracking device, VeriWatch. It represents the first ever community corrections contract for the device. No financial details were given for the contract. We believe the contract presents a new opportunity for GEO, and we expect more attention towards the device as the year progresses.

ATD Program. As we have noted, populations under the ATD program dropped in January to 324,554 at the end of the month from 376,031 at the start of the year. Uncertainty surrounding ATD populations drove the wide range of 2023 operating guidance from GEO’s management. Over the course of February, the decline slowed noticeably with populations at 293,167 as of February 25th, the latest data available.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

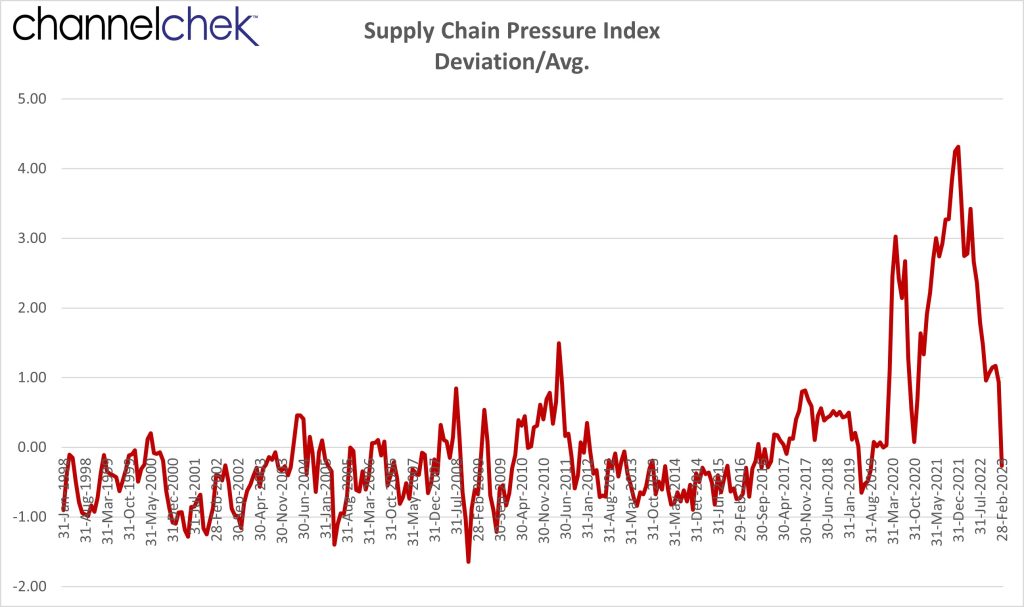

The Supply Chain Part of Inflation Can be Declared Dead, Now What?

New data shows the supply chain is no longer putting meaningful pressure on inflation — will rising prices finally sail off and stay there?

Historically, the Global Supply Chain Pressure Index (GSCPI) is now on the low side. In fact, for the monthly period ending February 28, it’s below its 25-year average. What’s more, is this is the first time the GSCPI has released a below-average reading of supply chain pressure since August of 2019.

This is significant as the supply-chain issues related to the pandemic, would seem to be transitory and are now no longer the issue. From March 2020 until this more recent report, consumers with easier money available, including stimulus checks, drove demand higher for goods. The suddenness of the onslaught of demand for goods caught the modern world’s “just-in-time” inventory management systems off guard. To make that situation much worse, lockdown policies slowed global production, and shipping and transport became entrenched in gridlock due to undermanned loading docks all under some level of new pandemic processes designed for health and safety.

Inflation climbed as the price of shipping was bid up substantially, and shortages of products on shelves caused retailers to lessen demand by hiking prices. Some products, particularly new and used cars, experienced sharp price increases as supply chain-related shortages on automotive components such as computer chips and other parts became difficult to obtain.

Will Inflation Finally Recede?

An 18-month-long period of rampant inflation in goods, including vehicles, electronics, food, and sporting goods, (including bicycles for both indoor and outdoor use became unavailable) began to decompress starting in early 2022. The supply chains had slowly worked through the main causes.

Around this same period in 2022, inflation pressures began to build in services. As price hikes for goods lessened or backtracked, the cost for services, including wages, shot up. This is still fueling inflation today.

Often, the fear or expectation of rising prices drives inflation and vice versa. This may be the reason Fed Chairman Powell used the description “transitory” long past the period that it was obvious that inflation was likely persistent. If the Chair of the US Central Bank had suggested back then that we had a long-term problem, the worst of it may have arrived faster and been worse. Conversely, now that higher-than-target inflation is here, it makes sense for Powell to speak more hawkishly, this helps alter expectations of ongoing high rates of inflation.

With inflation primarily coming from services, the medicine for reducing the demand for human services is lessen demand, or even more difficult, increase the labor force. This is a bitter pill for the economy and creates an issue with the Federal Reserve which has two mandates, one to keep inflation modest and the other to maximize employment.

Take Away

The GSCPI is an indicator that the goods-based part of the economy has normalized. Inflation is still raging in services, which are barely tied to services. The hope is that the Fed can reduce the demand for higher and higher wages or perhaps bring more capable workers into the workforce. Another part of this plan may have nothing to do with tightening credit conditions. Talking publicly about being resolved to squash inflation also has an impact on expectations which will reduce the prices charged for service.

The initial battle, the one that kicked off the price hikes (supply chain), has ended, now we have to see how the rest of the Fed’s fight against inflation, both in policy and psychologically, plays out.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22. Revenue of $1.23 billion was down 1.3% year-over-year (up 0.7% in constant currency). We were at $1.25 billion. Kelly took a $10.3 million asset impairment charge related to its RocketPower acquisition during the quarter. As a result, GAAP EPS loss was $0.02 compared to EPS of $1.80 in 4Q21. Adjusted EPS for the fourth quarter was $0.18 versus $0.65 last year. We had projected adjusted EPS of $0.29.

Quarterly Drivers. Kelly saw top line growth in its SET, Education, and OCG business, and International, if we exclude the sold Russian operations from the y-o-y comparison. Once again, the gross profit rate improved in all five business units, a testament to Kelly’s specialty talent focus.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 103 facilities totaling approximately 83,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. The run of exceeding expectations continued in the fourth quarter. Revenue for the quarter came in at $620.7 million, up from $557.5 million a year ago. Adjusted EBITDA totaled $145.5 million, AFFO was $0.58 per diluted share, EPS was $0.28, and adjusted net income $0.34 per share. In the year ago period, GEO reported $124.1 million, $0.66, $(0.41), and $0.38, respectively. We had forecast $603 million, $133.5 million, $0.54, $0.25, and $0.23, respectively. GEO’s results highlight the resiliency of the business model, in our opinion.

Electronic Monitoring Driving 4Q Results. GEO’s electronic monitoring segment saw revenue jump 89.3% to $149.8 million in the quarter, with segment operating income rising 89.6% to $85.7 million. While electronic monitoring populations have declined since the turn of the year, we believe electronic monitoring will remain a key arrow in government’s quiver to manage undocumented populations given the success of these programs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Image: Student Santiago Andrade interning at Caterpillar

Not Your Grandfathers Nuclear Reactor – Educating the Needed Nuclear Talent Pool

Human infrastructure is critical to any industry. Building the foundations so a new or quickly expanding technology can begin to flourish requires foresight. This forward planning also requires schools to recognize a need, student interest, and old and new industries then understanding that internships are two-way streets that benefit both the young, and also the entrenched. MIT created a unique program for students in the field of nuclear power generation. Below is an article republished from their website on the success of one of their programs. – Paul Hoffman, Channelchek

As nuclear power has gained greater recognition as a zero-emission energy source, the MIT Leaders for Global Operations (LGO) program has taken notice. Two years ago, LGO began a collaboration with MIT’s Department of Nuclear Science and Engineering (NSE) as a way to showcase the vital contribution of both business savvy and scientific rigor that LGO’s dual-degree graduates can offer this growing field.

“We saw that the future of fission and fusion required business acumen and management acumen,” says Professor Anne White, NSE department head. “People who are going to be leaders in our discipline, and leaders in the nuclear enterprise, are going to need all of the technical pieces of the puzzle that our engineering department can provide in terms of education and training. But they’re also going to need a much broader perspective on how the technology connects with society through the lens of business.”

The resulting response has been positive: “Companies are seeing the value of nuclear technology for their operations,” White says, and this often happens in unexpected ways.

For example, graduate student Santiago Andrade recently completed a research project at Caterpillar Inc., a preeminent manufacturer of mining and construction equipment. Caterpillar is one of more than 20 major companies that partner with the LGO program, offering six-month internships to each student. On the surface, it seemed like an improbable pairing; what could Andrade, who was pursuing his master’s in nuclear science and engineering, do for a manufacturing company? However, Caterpillar wanted to understand the technical and commercial feasibility of using nuclear energy to power mining sites and data centers when wind and solar weren’t viable.

“They are leaving no stone unturned in the search of financially smart solutions that can support the transition to a clean energy dependency,” Andrade says. “My project, along with many others’, is part of this effort.”

“The research done through the LGO program with Santiago is enabling Caterpillar to understand how alternative technologies, like the nuclear microreactor, could participate in these markets in the future,” says Brian George, product manager for large electric power solutions at Caterpillar. “Our ability to connect our customers with the research will provide for a more accurate understanding of the potential opportunity, and helps provide exposure for our customers to emerging technologies.”

With looming threats of climate change, White says, “We’re going to require more opportunities for nuclear technologies to step in and be part of those solutions. A cohort of LGO graduates will come through this program with technical expertise — a master’s degree in nuclear engineering — and an MBA. There’s going to be a tremendous talent pool out there to help companies and governments.”

Andrade, who completed an undergraduate degree in chemical engineering and had a strong background in thermodynamics, applied to LGO unsure of which track to choose, but he knew he wanted to confront the world’s energy challenge. When MIT Admissions suggested that he join LGO’s new nuclear track, he was intrigued by how it could further his career.

“Since the NSE department offers opportunities ranging from energy to health care and from quantum engineering to regulatory policy, the possibilities of career tracks after graduation are countless,” he says.

He was also inspired by the fact that, as he says, “Nuclear is one of the less-popular solutions in terms of our energy transition journey. One of the things that attracted me is that it’s not one of the most popular, but it’s one of the most useful.”

In addition to his work at Caterpillar, Andrade connected deeply with professors. He worked closely with professors Jacopo Buongiorno and John Parsons as a research assistant, helping them develop a business model to successfully support the deployment of nuclear microreactors. After graduation, he plans to work in the clean energy sector with an eye to innovations in the nuclear energy technology space.

His LGO classmate, Lindsey Kennington, a control systems engineer, echoes his sentiments: This is a revolutionary time for nuclear technology.

“Before MIT, I worked on a lot of nuclear waste or nuclear weapons-related projects. All of them were fission-related. I got disillusioned because of all the bureaucracy and the regulation,” Kennington says. “However, now there are a lot of new nuclear technologies coming straight out of MIT. Commonwealth Fusion Systems, a fusion startup, represents a prime example of MIT’s close relationship to new nuclear tech. Small modular reactors are another emerging technology being developed by MIT. Exposure to these cutting-edge technologies was the main sell factor for me.”

Kennington conducted an internship with National Grid, where she used her expertise to evaluate how existing nuclear power plants could generate hydrogen. At MIT, she studied nuclear and energy policy, which offered her additional perspective that traditional engineering classes might not have provided. Because nuclear power has long been a hot-button issue, Kennington was able to gain nuanced insight about the pathways and roadblocks to its implementation.

“I don’t think that other engineering departments emphasize that focus on policy quite as much. [Those classes] have been one of the most enriching parts of being in the nuclear department,” she says.

Most of all, she says, it’s a pivotal time to be part of a new, blossoming program at the forefront of clean energy, especially as fusion research grows more prevalent.

“We’re at an inflection point,” she says. “Whether or not we figure out fusion in the next five, 10, or 20 years, people are going to be working on it — and it’s a really exciting time to not only work on the science but to actually help the funding and business side grow.”

White puts it simply.

“This is not your parents’ nuclear,” she says. “It’s something totally different. Our discipline is evolving so rapidly that people who have technical expertise in nuclear will have a huge advantage in this next generation.”

Tokens.com Corp is a publicly traded company that invests in Web3 assets and businesses focused on the Metaverse, NFTs, DeFi, and gaming based digital assets. Tokens.com is the majority owner of Metaverse Group, one of the world’s first virtual real estate companies. Hulk Labs, a wholly-owned Tokens.com subsidiary, focuses on investing in play-to-earn revenue generating gaming tokens and NFTs. Additionally, Tokens.com owns and stakes crypto assets to earn additional tokens. Through its growing digital assets and NFTs, Tokens.com provides public market investors with a simple and secure way to gain exposure to Web3.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First Quarter Results. Total revenue for the quarter was at $151,848, an increase from the prior quarter of $101,235. We will be comparing quarters as Tokens.com has two new revenue streams, leasing and gaming revenue, which both did not occur last year. We estimated revenue at $105,000. Operating loss for Tokens.com was $566,525 versus $879,430 last quarter, and net loss was at $1.7 million, or EPS loss of $0.02, versus the prior quarter loss of $1.8 million, or a $0.02/sh loss.

Market Appreciation. The overall cryptocurrency market has seen an increase in total market cap over the last three months, as total market cap has risen to $1.05 trillion from $843.3 billion on November 15, 2022. This is an increase of $206.1 billion or 24.4%. If sustained, the rebound in the cryptocurrency market will be a positive for Tokens.com, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Will AI Learn to Become a Better Entrepreneur than You?

Contemporary businesses use artificial intelligence (AI) tools to assist with operations and compete in the marketplace. AI enables firms and entrepreneurs to make data-driven decisions and to quicken the data-gathering process. When creating strategy, buying, selling, and increasing marketplace discovery, firms need to ask: What is better, artificial or human intelligence?

A recent article from the Harvard Business Review, “Can AI Help You Sell?,” stated, “Better algorithms lead to better service and greater success.” The attributes of the successful entrepreneur, such as calculated risk taking, dealing with uncertainty, keen sense for market signals, and adjusting to marketplace changes might be a thing of the past. Can AI take the place of the human entrepreneur? Would sophisticated artificial intelligence be able to spot market prices better, adjust to expectations better, and steer production toward the needs of consumers better than a human?

In one of my classes this semester, students and I discussed the role of AI, deep machine learning, and natural language processing (NLP) in driving many of the decisions and operations a human would otherwise provide within the firm. Of course, half of the class felt that the integration of some level of AI into many firms’ operations and resource management is beneficial in creating a competitive advantage.

However, the other half felt using AI will inevitably disable humans’ function in the market economy, resulting in less and less individualism. In other words, the firm will be overrun by AI. We can see that even younger college students are on the fence about whether AI will eliminate humans’ function in the market economy. We concluded as a class that AI and machine learning have their promises and shortcomings.

After class, I started thinking about the digital world of entrepreneurship. E-commerce demands the use of AI to reach customers, sell goods, produce goods, and host exchange—in conjunction with a human entrepreneur, of course.

However, AI—machine learning or deep machine learning—could also be tasked with creating a business-based model, examining the data on customers’ needs, designing a web page, and creating ads. Could AI adjust to market action and react to market uncertainty like a human? The answer may be a resounding yes! So, could AI eliminate the human entrepreneur?

Algorithm-XLab explains deep machine learning as something that “allows computers to solve complex problems. These systems can even handle diverse masses of unstructured data set.” Algorithm-XLab compared deep learning with human learning favorably, stating, “While a human can easily lose concentration, and possibly make a mistake, a robot won’t.”

This statement by Algorithm-XLab challenges the idea that trial and error leads to greater market knowledge and better enables entrepreneurs to provide consumers with what they are willing to buy. The statement also portrays the marketplace as a process where people have perfect knowledge and an equilibrium point, and it implies that humans do not have specialized knowledge of time and place.

The use of AI and its tools of deep learning and language processing do have their benefits from a technical standpoint. AI can determine how to produce hula hoops better, but can it determine whether to produce them or devote energy elsewhere? If entrepreneurs discover market opportunities, they must weigh the advantages and disadvantages of their potential actions. Will AI have the same entrepreneurial foresight?

The acquisition of market knowledge can take humans years to acquire; AI is much faster at it than humans would be. For example, the Allen Institute for AI is “working on systems that can take science tests, which require a knowledge of unstated facts and common sense that humans develop over the course of their lives.” The ability to process unstated, scattered facts is precisely the kind of characteristic we attribute to entrepreneurs. Processes, changes, and choices characterize the operation of the market, and the entrepreneur is at the center of this market function.

There is no doubt that contemporary firms use deep learning for strategy, operations, logistics, sales, and record keeping for human resources (HR) decision-making, according to a Bain & Company article titled “HR’s New Digital Mandate.” While focused on HR, the digital mandate does lend itself to questioning the use of entrepreneurial thinking and strategy conducted within a firm. After AI has learned how to operate a firm using robotic process automation and NLP capacities to their maximum, might it outstrip the human natural entrepreneurial abilities?

AI is used in everyday life, such as self-checkout at the grocery store, online shopping, social media interaction, dating apps, and virtual doctor appointments. Product delivery, financing, and development services increasingly involve an AI-as-a-service component. AI as a service minimizes the costs of gathering and processing customer insights, something usually associated with a team of human minds projecting key performance indicators aligned with an organizational strategy.

The human entrepreneur has a competitive advantage insofar as handling ambiguous customer feedback and in effect creating an entrepreneurial response and delivering satisfaction. We seek to determine whether AI has replaced human energy in some areas of life. Can AI understand human uneasiness or dissatisfaction, or the subjectivity of value felt by the consumer? AI can produce hula hoops, but can it articulate plans and gather the resources needed to produce them in the first place?.

In what, if any, entrepreneurial functions can AI outperform the human entrepreneur? The human entrepreneur is willing to take risks, adjust to the needs of consumers, pick up price signals, and understand customer choices. Could the human entrepreneur soon become an extinct class? If so, would machine learning and natural processing AI understand the differences between free and highly regulated markets? If so, which would it prefer, or which would it create?

Getting to Know ChatGPT: A Shallow Dip into Its Current Functionality and Future Potential

ChatGPT and the underlying AI technology are, as near as anyone can tell, the next-level toolkit for research, communication, idea generation, and a million other uses. If you haven’t introduced yourself to it yet, leave plenty of time – getting started is easy, but getting yourself to stop may not be. Those of us that were around pre-internet may liken the first-time experience to the first time we gained access to the world wide web. The Sudden, much easier access to a world of information, puts one in a place where you don’t know what to try first.

Over the past couple of months, the now-familiar name, ChatGPT has made headlines. It quickly captivated the worlds imagination as an AI product that is likely to disrupt or destroy some industries while enhancing others. Obviously, this is of particular interest to investors. With this in mind, I sat down for an interview with ChatGPT; below are answers to questions that many investors are asking.

Channelchek (PH) – Am I able to interview Chatgpt?

ChatGPT – Hello! As an AI language model, I’m happy to answer any questions you may have. However, it’s important to keep in mind that I don’t have personal experiences or opinions like a human, and I can only provide information based on my training data. So feel free to ask me anything!

Channelchek (PH) – What do most users have ChatGPT to do for them?

ChatGPT – As an AI language model, ChatGPT can be used for a wide range of tasks, including:

Language translation: ChatGPT can be used to translate text from one language to another.

Content creation: ChatGPT can generate text for various types of content, such as articles, blog posts, and product descriptions.

Chatbot development: ChatGPT can be used to develop chatbots that can interact with users and provide information.

Sentiment analysis: ChatGPT can be used to analyze the sentiment of a piece of text, such as a social media post or a product review.

Question-answering: ChatGPT can be used to answer questions on a wide range of topics.

Text summarization: ChatGPT can be used to summarize long pieces of text into shorter, more manageable summaries.

Language modeling: ChatGPT can be used to train new models for specific domains, such as medical or legal language.

These are just a few examples of what ChatGPT can be used for. Its versatility and flexibility make it a powerful tool for many different applications.

Channelchek (PH) – From where do you pull your answers ChatGPT?

ChatGPT – As an AI language model, I don’t have pre-programmed answers. Instead, I generate responses to questions by analyzing patterns in large amounts of text data that I was trained on. Specifically, I was trained on a dataset of billions of words from various sources, including books, articles, websites, and other textual sources. During my training, I was exposed to a wide range of topics and writing styles, which helps me generate responses to many different types of questions.

When you ask me a question, I use natural language processing (NLP) techniques to analyze the question and generate a response based on patterns in the text data that I was trained on. I then use statistical models to determine the most likely response based on the context of the question and the patterns in the training data.

It’s important to note that my responses are only as accurate and reliable as the patterns that I learned during my training. While I strive to provide accurate and helpful information, I may not always get it right, and my responses may not reflect the views or opinions of OpenAI.

Channelchek (PH) – Are you at risk of having the response you generate slanted or biased based on users feedback adjusting your training ChatGPT?

ChatGPT – As an AI language model, I am designed to learn from the data that I am trained on, including the feedback that users provide to adjust my training. However, it’s important to be aware that the feedback that users provide can sometimes introduce biases into my training.

If the feedback is consistently biased in a particular direction, this could affect the accuracy and fairness of my responses. This is why it’s important to carefully monitor and evaluate any feedback that is used to adjust my training, and to ensure that it is representative of a wide range of perspectives.

To address this issue, OpenAI has implemented a number of safeguards to prevent bias and ensure that my training data is as accurate and diverse as possible. For example, the training data is carefully curated to include a wide range of sources and perspectives, and the training process is carefully monitored to ensure that biases are not introduced.

Additionally, OpenAI has implemented a number of techniques to help identify and mitigate any biases that may be present in the training data or feedback. For example, I am periodically evaluated to ensure that my responses are accurate and unbiased, and any issues that are identified are addressed through additional training or other adjustments to the model.

Channelchek (PH) – As an editor I write for Channelchek about stocks, the financial markets, the economy and business climate. Are you a good resource for current events related to these topics ChatGPT?

ChatGPT – As an AI language model, I can certainly provide you with information on current events related to stocks, financial markets, the economy, and the business climate. I have been trained on a vast amount of text data, including news articles and other sources related to these topics, so I can provide you with up-to-date information and insights on current events.

When asking me questions related to these topics, it’s important to provide me with as much context and specificity as possible so that I can provide you with the most accurate and relevant information. For example, if you are looking for information on a particular company or sector, you could provide me with the name of the company or sector, as well as any other relevant details or questions you may have.

However, it’s important to note that my responses are generated based on patterns in the text data that I was trained on, and may not reflect the views or opinions of OpenAI. Additionally, while I can provide you with information on current events and trends, I cannot provide investment advice or make predictions about future market performance. It’s always important to carefully evaluate information and seek the advice of a qualified financial professional before making investment decisions.

Channelchek (PH) – Do users ask you to forecast the stock market direction?

ChatGPT – Yes, users sometimes ask me to forecast the direction of the stock market. However, as an AI language model, I cannot make accurate predictions about future market performance. While I can provide information on current market trends and historical data, predicting the future direction of the stock market is a highly complex task that involves a range of economic, political, and social factors.

It’s important to note that investing in the stock market involves a certain degree of risk, and investors should always carefully evaluate market conditions and seek the advice of a qualified financial professional before making investment decisions. While I can provide general information and insights related to stocks and financial markets, I cannot provide investment advice or predict the future performance of individual stocks or the overall market.

Channelchek (PH) – Are you familiar with Channelchek?

ChatGPT – While I am not specifically programmed to be familiar with individual websites, I may have come across content from Channelchek during my training.

That being said, I can still provide you with general information on what Channelchek is. From my understanding, Channelchek is a financial information platform that provides independent research, analysis, and market commentary on publicly traded companies. It offers a range of tools and resources for investors and financial professionals, including market data, stock quotes, and research reports.

Channelchek’s focus is on providing unbiased and independent information to help investors make informed investment decisions.

Channelchek (PH) – Does your AI technology pose a risk to traditional internet search engines?

ChatGPT – My purpose is not to compete with traditional search engines like Google or Bing, but rather to complement them by providing an additional source of information and assistance to users. While I am capable of providing answers to a wide range of questions and generating responses to open-ended queries, I am not designed to replace traditional search engines or web browsing.

Search engines like Google and Bing are still the primary means by which users navigate the internet and find information, and they use a range of sophisticated algorithms and machine learning techniques to index and rank content on the web. While I am capable of processing natural language queries and generating responses, my training data is based on pre-existing content, which means that my responses are generated based on patterns in the text data that I was trained on, rather than direct access to the vast amounts of data on the internet.

Early Boolean Phrase Search Tool

Overall, AI language models like me are part of a larger ecosystem of tools and technologies that are designed to help users access and navigate the vast amount of information available online. While there may be some overlap between the capabilities of traditional search engines and AI language models, both serve different purposes and can work together to provide users with the most comprehensive and accurate information possible.

Channelchek (PH) – What industries are you likely to disrupt and which are you likely to augment or help build?

ChatGPT – As an AI language model, my capabilities are quite broad, and I have the potential to impact a wide range of industries and areas of society. Here are a few ways in which I could potentially disrupt or augment various industries:

Industries that could be disrupted:

Customer service: AI language models like me are already being used by many companies to automate and improve customer service interactions, and this trend is likely to continue. As AI technology improves, it could potentially replace many human customer service jobs.

Content creation: AI language models have the potential to automate certain types of content creation, such as news articles, product descriptions, and even social media posts. This could have a significant impact on the journalism and writing industries.

Education: AI language models could potentially disrupt the traditional education model by providing personalized learning experiences and automating certain types of teaching and grading.

Industries that could be augmented:

Healthcare: AI language models could help augment healthcare by providing more accurate and personalized diagnoses, and by automating certain types of administrative tasks.

Finance: AI language models could help augment finance by providing more accurate and data-driven investment advice, and by automating certain types of financial analysis.

Research: AI language models could help augment research by processing and analyzing vast amounts of data, and by identifying patterns and insights that might be difficult for humans to spot on their own.

Overall, the impact of AI language models like me on various industries will depend on a wide range of factors, including the development of the technology, the regulatory environment, and societal attitudes toward automation and AI. While there may be some industries that are more susceptible to disruption or augmentation than others, it’s important to approach these developments with a nuanced understanding of the potential benefits and risks.

Channelchek (PH) – Are users using ChatGPT to create social media bots to respond without human intervention likely to flood the internet?

ChatGPT – While it is technically possible for users to use AI language models like ChatGPT to create social media bots that can respond to messages without human intervention, I cannot speculate on whether this is likely to flood the internet.

The use of AI language models like ChatGPT could potentially make it easier and more accessible for users to create more sophisticated chatbots that can mimic human conversation more convincingly.

It’s also important to consider the potential impact of widespread use of social media bots on the quality and authenticity of online interactions. While chatbots can be useful in certain contexts, they can also be used to spread misinformation and propaganda or to manipulate public opinion. As with any technology, it’s important to approach the use of AI language models and chatbots in a responsible and ethical way, and to consider the potential risks and benefits of their use.

Channelchek (PH) – What do you call one that uses ChatGPT?

ChatGPT – There is no specific term for a person who uses ChatGPT or other AI language models, as these tools are designed to be accessible and usable by anyone with an internet connection.

However, a person who uses ChatGPT to create chatbots or other automated tools could be referred to as an AI developer or AI engineer. Similarly, a person who uses ChatGPT to conduct research or analysis in a specific field could be referred to as an AI researcher or analyst.

Channelchek (PH) – How much do you cost?

As an AI language model, I do not have a specific cost as I am not a commercial product. My purpose is to provide information and assistance to users like you, and I am freely accessible through various platforms that integrate my technology, including chatbots, voice assistants, and search engines.

Channelchek (PH) – Should I throw out the encyclopedias on my book shelf and rely instead on ChatGPT?

ChatGPT – Ultimately, whether or not to keep your encyclopedias depends on your personal preferences and how you prefer to access information. While AI language models like ChatGPT are convenient and accessible, they may not always provide the level of detail or accuracy that you require for a specific question or topic. So, it’s always a good idea to consult multiple sources of information to ensure that you have a well-rounded understanding of a given topic.

Channelchek (PH) – How does one get started using ChatGPT for research?

ChatGPT – Getting started with using ChatGPT for research can involve several steps. Here are a few basic steps you can follow:

Identify your research question or topic: Start by identifying the research question or topic you want to investigate. This will help you to focus your search and make the best use of ChatGPT.

Choose a ChatGPT platform: There are several platforms that integrate ChatGPT, including chatbots, voice assistants, and search engines. Choose a platform that best fits your needs and preferences.

Familiarize yourself with the platform: Once you have chosen a platform, take some time to explore and familiarize yourself with its features and capabilities. Many platforms offer tutorials and guides to help you get started.

Start asking questions: Once you are comfortable with the platform, start asking questions related to your research topic. Try to ask open-ended questions that will allow ChatGPT to provide more detailed and relevant answers.

Evaluate the results: As you receive answers from ChatGPT, evaluate the accuracy and relevance of the information. Keep in mind that ChatGPT is not perfect and may not always provide the most accurate or comprehensive information. Be sure to double-check any information you receive with other sources to ensure its accuracy.

Refine your search: If you are not finding the information you need, try refining your search by using more specific keywords or phrases.

Overall, using ChatGPT for research can be a valuable tool for gathering information and conducting preliminary investigations. However, it’s important to keep in mind that it is just one tool in the research process, and should be used in conjunction with other sources of information and research methods.

Wrap Up

It’s easy to comprehend how this technology, which will likely see stronger competition in the coming year, will quickly become something that is used every day to help streamline how we do our jobs, and find information in our personal lives. Unlike an internet search engine, queries produce individual results tailored to the individual question. The same question will recieve different phraseology if asked a minute later. Whereas Google or DuckDuckGo list websites that may provide the answer, ChatGPT responds using its own answer using artificial intelligence.

Getting started is as easy as going to OpenAI.com and navigating to Chat.OpenAI.com and providing an email and verification phone number. Click on my name below and write me, I’d love to hear what you are using it for.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Prepping For an End to Title 42. Once again, during the quarter CoreCivic continued to hire staff in anticipation of an ending of Title 42 and a surge in ICE populations. The additional expense impacted margins. Management did note that without the extra expense, guidance for 2023 would have been in the ballpark of consensus estimates for the year.

Potential New Business? Management again noted increasing interest from various states, both current clients and potential new clients, for solutions as these parties deal with a very tight labor market. With excess bed capacity available and the staff hired, CoreCivic is well positioned to pick up additional business, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

There’s a lot of money being made through the business of professional sports leagues. The NBA, MLB, NHL, all have very profitable business models, and although the businesses are all similar, the NFL leads the other U.S. based leagues in generating revenue. The once tax-exempt entity has a dual business structure with multiple layers of income that continues to expand. Below we cover the multiple ways the NFL, and the months-long drive of more than 30 teams to the Superbowl, ring the register.

In 2015, the National Football League forfeited its tax-exempt status with the IRS. The league had benefitted from the unique status beginning in 1942. The decision was based in part on mounting criticism over its rapidly growing earnings streams.

These streams largely come from the 32 teams that make up the NFL, thirty-one of the ball clubs are privately owned, while just one, the Green Bay Packers, continues to operate under a non-profit public corporation status. The clubs all form a trade association through which funds are directed back to the NFL board, some find their way distributed back to the teams.

This form of entertainment rakes in money on many fronts. In-person attendance, TV viewers, different forms of wagering, and advertising dollars all feed into overall league revenue after costs such as salaries that can $50 million annually.

Tickets to the Super Bowl 2023 event between the Kansas City Chiefs and the Philadelphia Eagles are averaging about $10,000. The higher end seats are in the $40,000 range, about the same as a Tesla Model S.

Tax Exemption of Teams

The team with tax-exempt status is exempt from paying all or some of federal income taxes. This status had been maintained by all NFL teams from 1945 through 2015.

The NFL voluntarily opted to give up its tax-exempt status in 2015 and began paying taxes. Some contend this change avoids further negative public outcry. It seems the economic benefits were not as significant as the public relations disadvantages.

Business Structure

The league separates its income streams into local and national categories. On the national side, the NFL negotiates national merchandise, licensing, and television contracts. The 32 teams receive equal shares of this money, regardless of individual team performance.

Local income is generated through concession sales, ticket sales, and corporate sponsors. This doesn’t nearly cover the cost of fielding a professional football team. Using the Green Bay Packers as a benchmark, the team had expenses totaling $410 million in its fiscal year 2021. Most of this number was attributable to player salaries, with the remainder used for stadium maintenance, advertising, and team and administration expenses.

How Teams Make Money

The majority of any NFL team’s revenue comes from TV arrangements. Ticket revenues, licensing, merchandising agreements, and endorsement deals are additional income sources.

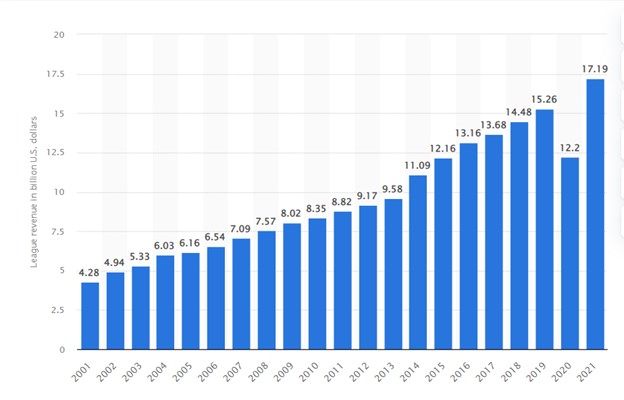

Revenue of All National Football League Teams from 2001 to 2021 (in billion U.S. dollars)

Televised Rights and Deals – The Super Bowl is among the most watched television events in America each year. The regular games broadcast on Sundays, Mondays, and Thursdays throughout the regular season will consistently have the best TV ratings. This is why media corporations pay an above average amount for the right to broadcast them.

The traditional television industry now competes with other video-based programming, all pulling the attention of those seeking entertainment. The NFL audience and draw are not in decline. NFL teams still generate massive local and even international revenue through TV contracts. The individual clubs receive significant amounts from television providers thanks to multibillion-dollar contracts, and there are even more television viewers and broadcasts of games than other programs on set.

Image Credit: Karen (Flickr)

Tickets and Vendor Rental – Far below the rapidly increasing money from TV deals, ticket sales are a large source of income for individual teams. NFL games often sell out, with an estimated average ticket price of $151 and a stadium capacity of roughly 70,000. It’s a nice add-on to broadcast viewership.

NFL teams can also use their stadiums to hold non-football activities, like concerts within local restrictions.

The cash flow on the rental of space to vendors to sell food and drinks at games are also significant in a stadium with 70,000 fans as a captive audience.

Image Credit: RaymondClarkeImages (Flickr)

Official Sponsorships – Corporate sponsors pay NFL teams to put their logos on products, TV transitions, player jerseys, etc. The franchise rights to NFL grounds naming of stadiums are extremely desirable among corporate advertisers.

The naming right to So-Fi Stadium in LA, home of the Los Angeles Rams, is in the neighborhood of $30 million annually, and similar rights to Allegiant Stadium in Las Vegas is estimated at between $20 and $25 million annually.

Gambling Franchises – Some NFL teams take advantage of this method by opening betting platforms in their stadiums, collaborating with well-known casinos, creating online sports betting websites, and other strategies. This is an area of rapid expansion as sports betting becomes legalized across the US and technology provides opportunities for betting on fragments of the game in addition to the more traditional methods. Incremental income from these growing arrangements has expanded income opportunities among teams.

Image Credit: Karen (Flickr)

Costs

Overall, like any business, the NFL will undoubtedly explore all the opportunities for meaningful income that present itself. Of course the overall income is best measured net of expenditures that include marketing, cost of athletes and other entertainers, management, upkeep, and renovations.

Take Away

One of the most financially successful professional sports leagues in the US and across the globe is the NFL. Most of the teams’ revenues are generated from broadcasting and licensing deals. The growth in revenue, with the exception of one year during the pandemic curbs, has been accelerating. Technology has brought new methods to gamble on sports, along with some friendly gaming legislation across the nation. This is additive to the bottom line.

It appears that the trend, which has survived some public relations setbacks, isn’t going to continue as Americans tend to spend many hours during the winter months immersed in the sport of football.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid 4Q22 Operating Results. CoreCivic beat expectations for 4Q22. Reported revenue was $471.4 million, compared to $472.1 million in the year ago period and our estimate of $465 million. Reported net income was $24.4 million, or $0.21 per diluted share, compared to $28 million, or $0.23 per share, last year. We had forecast net income of $14.5 million, or $0.13 per share. Adjusted EBITDA for the quarter was $87.7 million, compared to our $73.1 million estimate, and $103.2 million in 4Q21.

La Palma Normalizing, but Labor Remains a Challenge. CoreCivic substantially completed the transition of inmate populations at La Palma during the quarter, a positive. However, staffing remains a challenge, with temporary incentives, above average wage pressure, and travel costs, all impacting margin, which we anticipate will continue through at least the first quarter of 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

A Journey from Work to Home is about More than Just Getting There – the Psychological Benefits of Commuting that Remote Work Doesn’t Provide

For most American workers who commute, the trip to and from the office takes nearly one full hour a day – 26 minutes each way on average, with 7.7% of workers spending two hours or more on the road.

Many people think of commuting as a chore and a waste of time. However, during the remote work surge resulting from the COVID-19 pandemic, several journalists curiously noted that people were – could it be? – missing their commutes. One woman told The Washington Post that even though she was working from home, she regularly sat in her car in the driveway at the end of the workday in an attempt to carve out some personal time and mark the transition from work to nonwork roles.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Matthew Piszczek, Assistant Professor of Management, Wayne State University, Kristie McAlpine, Assistant Professor of Management, Rutgers University.

As management scholars who study the interface between peoples’ work and personal lives, we sought to understand what it was that people missed when their commutes suddenly disappeared.

In our recently published conceptual study, we argue that commutes are a source of “liminal space” – a time free of both home and work roles that provides an opportunity to recover from work and mentally switch gears to home.

During the shift to remote work, many people lost this built-in support for these important daily processes. Without the ability to mentally shift gears, people experience role blurring, which can lead to stress. Without mentally disengaging from work, people can experience burnout.

We believe the loss of this space helps explain why many people missed their commutes.

One of the more surprising discoveries during the pandemic has been that many people who switched to remote work actually missed their commutes. Gerald Streiter (Flickr)

Commutes and Liminal Space

In our study, we wanted to learn whether the commute provides that time and space, and what the effects are when it becomes unavailable.

We reviewed research on commuting, role transitions and work recovery to develop a model of a typical American worker’s commute liminal space. We focused our research on two cognitive processes: psychological detachment from the work role – mentally disengaging from the demands of work – and psychological recovery from work – rebuilding stores of mental energy used up during work.

Based on our review, we developed a model which shows that the liminal space created in the commute created opportunities for detachment and recovery.

However, we also found that day-to-day variations may affect whether this liminal space is accessible for detachment and recovery. For instance, train commuters must devote attention to selecting their route, monitoring arrivals or departures and ensuring they get off at the right stop, whereas car commuters must devote consistent attention to driving.

We found that, on the one hand, more attention to the act of commuting means less attention that could otherwise be put toward relaxing recovery activities like listening to music and podcasts. On the other hand, longer commutes might give people more time to detach and recover.

In an unpublished follow-up study we conducted ourselves, we examined a week of commutes of 80 university employees to test our conceptual model. The employees completed morning and evening surveys asking about the characteristics of their commutes, whether they “shut off” from work and relaxed during the commute and whether they felt emotionally exhausted when they got home.

Most of the workers in this study reported using the commute’s liminal space to both mentally transition from work to home roles and to start psychologically recovering from the demands of the workday. Our study also confirms that day-to-day variations in commutes predict the ability to do so.

We found that on days with longer-than-average commutes, people reported higher levels of psychological detachment from work and were more relaxed during the commute. However, on days when commutes were more stressful than usual, they reported less psychological detachment from work and less relaxation during the commute.

Creating Liminal Space

Our findings suggest that remote workers may benefit from creating their own form of commute to provide liminal space for recovery and transition – such as a 15-minute walk to mark the beginning and end of the workday.

Our preliminary findings align with related research suggesting that those who have returned to the workplace might benefit from seeking to use their commute to relax as much as possible.

To help enhance work detachment and relaxation during the commute, commuters could try to avoid ruminating about the workday and instead focus on personally fulfilling uses of the commute time, such as listening to music or podcasts, or calling a friend. Other forms of commuting such as public transit or carpooling may also provide opportunities to socialize.

Our data shows that commute stress detracts from detachment and relaxation during the commute more than a shorter or longer commute. So some people may find it worth their time to take the “scenic route” home in order to avoid tense driving situations.

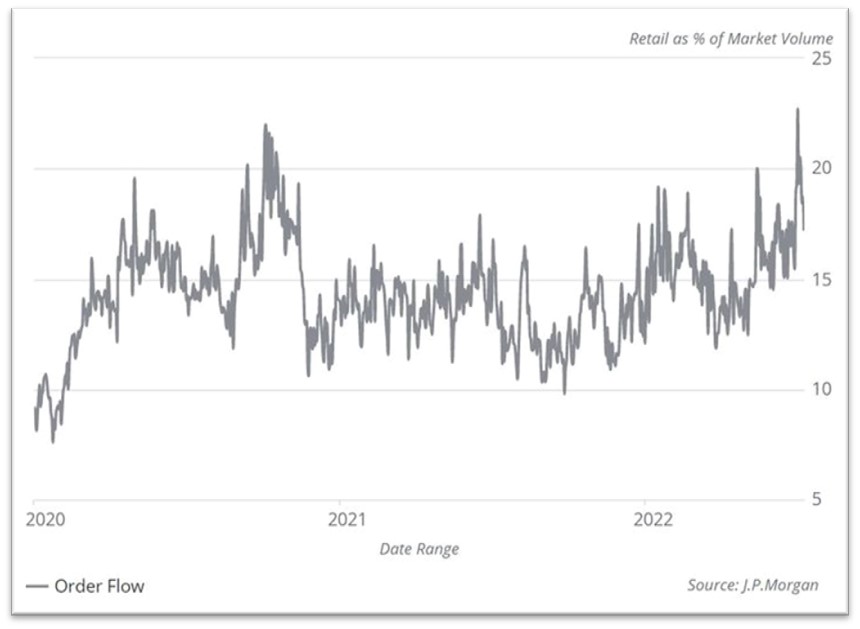

The Percentage Volume of Retail Transactions Has Surpassed 2020’s Level

Retail investors were a strong market force in 2021, and after a hiatus through much of 2022, they may be setting the tone in 2023. As a whole, the investors that fall into this category are watching signs that the US Federal Reserve and other central banks may be near the end of their rate hikes. This, coupled with last year’s sell-off, was taken as a sign to selectively jump back into positions. The positions they have been putting on have been moving the needle in the “risk-on” category; this has sent many of last year’s losers up double digits.

Data from JP Morgan demonstrate retail transactions have recently surpassed the market volume peak reached in the Fall of 2020. The more volume as a percentage of trades, the more influence over price movements any investment group has.

JPMorgan Data Shows Retail’s Market Percentage Has Quickly Grown

Retail Investors as % of Investors (JPM)

What Prices Have They Impacted?

During the last week in January, retail market orders as a percent of market value reached 23%, according to JPMorgan. Comparatively, it got to 22% a few times when GameStop (GME) was confounding institutional money while surging in valuation. As with the increase in retail volume during 2020, the renewed interest in committing to trades can have an outsized impact on sector movements and those of favorite stocks.

During the pandemic lockdown period, many self-directed investors chose to follow groups such as r/WallStreetBets on Reddit and forums on other chatrooms and platforms. One strategy that worked was directed at hedge fund short positions. It involved massive buying of stocks that were heavily shorted. The goal was to force the shorts to cover, which would produce buying and a higher stock price. This was effective enough to have caused significant problems with both institutional investors and the brokerage community settling the trades.

As January came to a close Many of the same risk trades, have gotten attention. AMC Theatres (AMC) is up 70% YTD. Cathie Wood’s ARKK fund, which invests in speculative disruptive companies, has risen nearly 46%. Also in the fund category is an ETF that invests in so-called meme stocks (MEME), this is up 41%.

Bitcoin (BTC.X), which had been presumed on its deathbed toward the end of last year, is up over 42% as it continues to track technology.

Will They Again Score?

“Mark my words, it’s going to end in tears,” was a popular line amongst market pundits back in 2020-2021. The Great Unwashed, the Meme Stock Investors, the market participants Jim Kramer called Robin Hoodies don’t have a long track record. But the track record they do have is worth noting.

According to JP Morgan, as of the first week in February, Tesla (TSLA) was the most sold stock by retail investors. Others that have been sold include those categorized as green and infrastructure stocks tied to EVs and 5G broadband.

The most purchased were Amazon (AMZN) and APPLE (AAPL). The hashtag #MOASS, or Mother of All Short Squeezes, has been trending most days on Twitter. The stock tied to the posts is AMC (AMC, APE), as there has been ongoing news surrounding this classic meme stock. One meme stock that has not attracted that much attention is Bed Bath and Beyond (BBBY). The company, which is trading at $3.20 after having been at $22.80 less than a year ago, is on life support, and closing dozens of stores amongst talk of bankruptcy. For those that were able to withstand the retail short-squeeze in BBBY, they may be able to cash in.

Take Away

If the “risk-on” trend among retail investors continues, discretionary institutional money has learned to pay attention. Self-directed investors should also pay attention to new activity, and any rotation from one cooling sector to one that is heating up.

In addition to following the news on Channelchek, investors can watch the Investor Movement Index (IMX) reported on the last weekend of each month by TDAmeritrade. For additional insight, it is always fun to check in on what the message boards are buzzing about and sorting through the serious and the nonsensical on Reddit and Twitter.