V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Refresh. V2X’s Board recently elected to increase the size of the Board from 7 members to 10 members and appointed Nicole B. Theophilus, Gerard A. Fasano, and Ross S. Niebergall, effective immediately, as new members of the Board to serve as Class I, Class II, and Class III Directors, respectively.

Theophilus. Ms. Theophilus currently serves as EVP and Chief Administrative Officer of Wabtec Corporation, a global provider of equipment, systems, digital solutions, and value-added services, since July 2024. She previously served as Wabtec’s EVP and Chief Human Resources Officer from August 2020 to March 2024. She was also the EVP and Chief Human Resources Officer for West Corporation from April 2016 to February 2018 and for ConAgra Foods from November 2009 to August 2015.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

SAN DIEGO, Jan. 08, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, today expressed strong support for President Trump’s announcement of policies that prioritize reinvestment in national defense capabilities over stock buybacks by defense contractors.

Kratos has long operated under a fundamentally different capital allocation philosophy than much of the publicly traded defense market. The company does not have a practice of conducting stock buybacks or paying dividends, choosing instead to reinvest capital directly into the development, production, and fielding of affordable, mission-ready technologies for the warfighter.

“At Kratos, every dollar we earn is viewed through the lens of readiness and capability,” said Eric DeMarco, President and CEO of Kratos. “Since our inception as a defense company, we have aggressively self-funded development to be first-to-market with relevant systems that can be affordably produced in large quantities to deter and, if necessary, defeat our adversaries, and we have reinvested in people, facilities, inventory, and real technologies that can be delivered at speed and scale to support today’s and tomorrow’s warfighter.”

Kratos’ reinvestment-first approach has enabled the company to self-fund and be first-to-market with critical capabilities across unmanned systems, hypersonics, propulsion, space, and defense electronics—taking on development and production risk ahead of customer funding or becoming formal programs of record. This model supports faster innovation cycles, strengthens the U.S. defense industrial base, and helps ensure that advanced capabilities are available when needed, not years later.

The company’s strategy aligns with growing emphasis across government and the Department of War on accelerating both production and acquisition, expanding industrial capacity, delivering affordable systems in quantity, and ensuring readiness and lethality for the warfighter. By maintaining inventory on the shelf, investing in infrastructure, and scaling production-ready technologies, Kratos continues to demonstrate how disciplined reinvestment can translate directly into operational advantage.

DeMarco added, “Our mission is not financial engineering, but delivering value to all Kratos stakeholders, including most importantly the warfighter, and delivering capability now – affordable, scalable, and real – so the United States and its allies are prepared. That is where we believe defense capital should go.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

SAN DIEGO, Jan. 08, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, today announced that Northrop Grumman (NYSE: NOC) was competitively awarded the U.S. Marine Corps’ Marine Air-Ground Task Force Uncrewed Expeditionary Tactical Aircraft (MUX TACAIR) Collaborative Combat Aircraft (CCA). This award combines Northrop Grumman’s uncrewed capabilities and autonomous leadership with Kratos’ Valkyrie uncrewed aerial system to work alongside crewed fighters to provide air dominance in high-threat environments.

Northrop Grumman will develop and rapidly deliver platforms that include:

Advanced Mission Kit: Northrop Grumman’s cost-effective mission kit is inclusive of sensors and software-defined technologies designed specifically for uncrewed aircraft. The mission kit’s flexible technology can perform various kinetic and non-kinetic effects, making the platform a combat-ready asset.

Open Architecture Autonomy Software: Northrop Grumman’s open architecture autonomy software package – known as Prism – will manage the aircraft’s operations autonomously.

Valkyrie Uncrewed Aerial System from Kratos Defense and Security Solutions: Fully equipped for a variety of missions that will include conventional takeoff and landing capabilities, enhanced runway flexibility with a modular airframe and payload bays for customizable effects.

This agile solution integrates Northrop Grumman’s proven mission systems with Kratos’ mature Valkyrie. (Photo Credit: U.S. Marine Corps)

This agile solution integrates Northrop Grumman’s proven mission systems with Kratos’ mature Valkyrie. (Photo Credit: U.S. Marine Corps)

Experts: Krys Moen, vice president, advanced mission capabilities, Northrop Grumman: “Northrop Grumman remains at the forefront of advanced sensing capabilities, delivering innovative solutions that meet the needs of the warfighter with unmatched speed and reliability. This enhanced capability set ensures optimal performance for both crewed and uncrewed platforms.”

Steve Fendley, president Kratos Unmanned Systems Division: “The integration of the Kratos Valkyrie aircraft system configured with the world’s best multifunction mission systems from Northrop Grumman results in a high-capability CCA at a price point that enables the uncrewed systems to be deployed in mass with crewed aircraft.”

Details: Northrop Grumman has packaged its sensors and other mission capabilities into a smaller envelope, resulting in a more cost-effective solution that is compatible with an uncrewed platform. Combining existing product lines and proven capabilities, Northrop Grumman, Kratos, and commercial partners developed a missionized CCA that includes survivability, connectivity, lethality and supportability elements. With more than 20 successful flight demonstrations in operationally relevant environments, Northrop Grumman and Kratos are offering the U.S. Marine Corps a low risk, expedited path to MUX TACAIR mission capability and persistent joint crewed and uncrewed expeditionary operations.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

DMEA ATSP. V2X subsidiary Vertex Aerospace has been named as an awardee to the Defense Microelectronics Activity (DMEA) Advanced Technology Support Program (ATSP), according to the daily Department of War contract award activity. With multi-billion dollar potential, this award caps a strong year for V2X. The Company has won places on multiple billion dollar contracts, which bode well for the future.

Details. DMEA ATSP is an ID/IQ contract with a $23.357 billion ceiling. This multiple award contract has a base ordering period of five years with two option periods, three years and two years respectively, to establish a 10 year ordering period. There are a total of 10 awardees, including Vertex. As an ID/IQ, Vertex will need to compete for each award, but we are confident the Company will receive its fair share of wins under the contract.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

SAN DIEGO, Dec. 29, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, announced today that it has recently received approximately $30 million in Air Defense and C5ISR system national-security-related, military-grade custom hardware production contracts. Kratos is an industry leader in the development, engineering, design, and large-scale production of military-grade hardware and integrated systems for missile, radar, counter-UAS, hypersonic, directed energy, satellite communication, and other complex systems. Work performed under the recent contract awards will be performed in secure Kratos manufacturing facilities.

Tom Mills, President of Kratos’ C5ISR Division, said, “Our entire team is honored to have our customers’ confidence in our ability to engage early in the systems’ design phase to collaborate with our customers on system-level engineering and design, provide highly engineered custom systems and solutions, large-scale manufacturing, at an affordable cost, for these urgent, relevant, and mission critical systems. Kratos is the recognized industry leader in delivering military-grade hardware and systems in direct support of America’s National Security requirements.”

Eric DeMarco, President and CEO of Kratos, said, “Delivering relevant, military-grade hardware on time, on schedule, and that works every time is hard, and Kratos’ demonstrated capability to continuously do so is a differentiator for our Company to our customers and partners. Kratos is currently in high volume, mass production on multiple hypersonic, counter-UAS, missile, radar and other systems, and we are proud to be the clear industry leader in our mil-spec hardware areas of expertise.”

Due to competitive, security related and other considerations, no additional information will be provided.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

PDF VersionKratos Zeus SRMs Are Specifically Designed for Affordable, Rapid, Full-Rate Production, to Enable National Security Customers to Fly More Often, Faster and Farther, Using Fewer Stages, at a Substantially Reduced Cost

SAN DIEGO, Dec. 23, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, announced today that it has issued a letter of intent to L3Harris Technologies (LHX: NYSE) for an order of 40 Zeus 1 and 20 Zeus 2 hypersonic motors. The large Zeus SRM acquisition by Kratos is representative of the existing under contract, expected future hypersonic and other system launch manifest(s), as Kratos continues to execute its longstanding strategy of making internally funded investments to move fast, and be first to market with affordable, relevant systems for U.S. National Security.

The Zeus 1 and Zeus 2 are high-performance, 32.5-inch diameter solid rocket motors (SRMs) providing substantial performance improvements over similar legacy rockets. They are purposely designed to be fully compatible with existing payloads and launch infrastructure, to enable rapid integration of new technologies and advanced payloads, including those currently under development by Kratos. These and other key attributes will provide Kratos and our customers, including the MACH-TB 2.0 program, with opportunities to fly more often, faster and farther, using fewer stages, and at a substantially reduced cost.

“This strategic purchase of Zeus hypersonic rocket motors is a direct reflection and result of Kratos’ long-standing approach: investing our own capital to build capability, capacity, and inventory ahead of customer need,” said Eric DeMarco, President and CEO of Kratos. “By putting real product on the shelf and delivering real, ready-now systems at scale, we are fully aligned with Secretary Hegseth’s acquisition reform priorities to accelerate delivery, put our own skin in the game, and equip the warfighter faster and more affordably. We have a number of additional, low-cost hypersonic systems and products, certain of which are flying today, as we are committed to being the go-to, low cost, hypersonic system and hardware provider for the United States.”

Kratos developed the Zeus family of SRMs in direct response to the need for affordable commercial launch vehicle stages for hypersonic test, ballistic missile targets, scientific research, sounding rocket and special customer missions. Kratos applied its significant rocket launch experience to establish the Zeus 1 and Zeus 2 motor specifications in close coordination with respective customer and user communities. Kratos internally funded development of the Zeus SRMs which are designed and manufactured to Kratos’ specifications by key merchant supplier and partner, L3Harris.

The Zeus SRM family is designed with versatility and affordability in mind as a complement to Kratos’ other internally funded investments such as the Erinyes hypersonic test “flyer” that debuted in June 2024. Kratos’ investments in hypersonic and other relevant mission areas create a versatile family of test and evaluation products that offer complete systems. With the Zeus SRMs, the Erinyes, and other Kratos front end systems, Kratos is one of the only companies boasting both launcher and flyer systems within one organization, providing unmatched innovation, disruptive capabilities, mission responsiveness and affordability to the customer.

This order further demonstrates Kratos’ steadfast commitment to supporting the Department of War customer by investing in systems and inventory. This investment, along with Kratos’ recent order for 60 22-inch diameter Oriole solid rocket motors, is ensuring that rapid and relevant flight test platforms are available as needed to accelerate hypersonic research and deliver capability to our warfighters.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

RESTON, Va., Dec. 17, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) announced it has been awarded a $72 million contract to provide support and engineering services for the Gateway Mission Router (GMR).

The GMR is a cyber-hardened solution that enhances air-to-ground operations and adapts to evolving mission needs through open-standard interfaces. By intelligently routing datalinks and platform capabilities, the GMR enables a unified common operating picture that merges situational awareness and command-and-control data across multiple formats.

The system’s versatility supports the Department of War, also known as the Department of Defense’s, Combined Joint All Domain Command and Control initiative, which aims to connect systems across domains into a unified network for faster, data-driven decision-making.

“This award represents an important milestone as we continue to advance and expand the Gateway Mission Router and our C6ISR work,” said Richard Caputo, Senior Vice President of Aerospace Systems at V2X. “The GMR has broad applicability across numerous aviation and ground platforms, and we see strong potential for growth beyond this award. We remain committed to investing in the solution to deliver greater processing capability at reduced size, weight, and power for critical missions.”

This award builds upon a previous $49 million contract as V2X continues to advance the GMR program and expand its use across the U.S. military’s mission systems. The contract has an estimated completion date of June 25, 2030.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Media Contact Angelica Spanos Deoudes Director, Corporate Communications Angelica.Deoudes@goV2X.com 571-338-5195

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

SAN DIEGO, Dec. 05, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, today announced the opening of its new state‑of‑the‑art 10,000 square foot facility for PT6A and PT6T engine overhaul in Vancouver, British Colombia—a significant milestone in the company’s continued growth and innovative support of the PT6A and PT6T engine market. This modern space has been designed to enhance operational efficiency, foster collaboration, and provide the infrastructure needed to meet the evolving demands of the industry. The expansion underscores Kratos’ commitment to delivering cutting‑edge solutions and ensuring that its teams have the resources required to drive excellence across all areas of operation.

The new facility also strengthens Kratos’ Bristow, Oklahoma operations, enabling expanded capabilities and improved service delivery for Canadian operators. By investing in advanced technology and increased capacity, Kratos’ Consolidated Turbines divisions in Canada and Oklahoma are better positioned to support its partners with greater responsiveness, reliability, and scalability. This move reflects the company’s dedication to building strong international relationships and providing unmatched support to operators across North America, reinforcing its role as a trusted leader in the PT6T and PT6A industry.

“This move will create seemingly endless possibilities with regards to expansion, employment and in-house capabilities. We are fortunate to have many long-standing Bell Medium customers in Canada, which operate the PT6T model engines. Our goal is to add the fixed wing version (PT6A models) to our quiver in the near future,” said Dave Wark, Director of Kratos MRO Canada.

CTS Canada started 20 years ago to support PT6 maintenance, repair, and overhaul in Langley, BC. Now a Kratos business, the company has grown significantly with its third expansion in less than ten years that provides the opportunity to support customers better than ever before, a testament to Kratos’ great team that works tirelessly to keep customers flying.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

RESTON, Va., Dec. 3, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) has been awarded a position on the Automated Test Systems Division’s (ATS) Multiple Award indefinite delivery, indefinite quantity (IDIQ) contract by the Air Force Life Cycle Management Center at Warner Robins Air Force Base in Georgia.

V2X will provide rapid, full lifecycle support for ATS used to sustain critical warfighter operations worldwide. These systems support a wide array of aircraft platforms, including fighter jets, bombers, cargo/airlift/tanker aircraft, unmanned aerial vehicles, and helicopters. Users include the U.S. Air Force, Air Force Reserve, Air National Guard, F-35 Joint Strike Fighter program, Foreign Military Sales customers, amongst others.

“This award reflects our team’s continued commitment to delivering mission-critical solutions that supports operational readiness,” said Jeremy C. Wensinger, President and Chief Executive Officer at V2X. “We are honored to contribute to the sustainment of vital test systems supporting the U.S. and allied partners around the world.”

The IDIQ contract provides flexible support for both legacy and future ATS requirements, with a base ordering period of five years and an option to extend for an additional five years. V2X will maintain and sustain both commercial and noncommercial products across the ATS Division’s portfolio.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

Media Contact Angelica Spanos Deoudes Director, Corporate Communications Angelica.Deoudes@goV2X.com 571-338-5195

RESTON, Va., Dec. 1, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX), announced it has been awarded a 10-year, $425 million indefinite-delivery, indefinite-quantity contract to modernize and upgrade cockpit displays for the U.S. Air Force F-16 fleet.

Under the contract, V2X will provide center display units (CDU’s) full kits, line-replaceable units, shop-replaceable units, and related support hardware for the combat jet.

“This is a great example of how smart modernization can deliver immediate mission enhancement,” said Jeremy C. Wensinger, President and Chief Executive Officer at V2X. “By upgrading the F-16 cockpit display at a significantly lower cost than full replacement, we are strengthening the digital backbone of the aircraft and enhancing operational effectiveness for decades to come.”

The award builds on past orders and represents the largest award we have received for the F-16 CDU program. V2X’s approach to cockpit modernization delivers cost-effective technology insertion with minimal retrofit, ensuring enhanced combat effectiveness while reducing overall lifecycle costs.

Work will be performed at V2X’s facility in Indianapolis, Indiana, and is expected to be completed by September 2035.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Media Contact Angelica Spanos Deoudes Director, Corporate Communications Angelica.Deoudes@goV2X.com 571-338-5195

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Awards. With the Federal government once again open, contract awards are once again being announced by the Department of War. VVX’s award momentum continues, providing the Company with a solid base of business going into 2026, in our view.

Iraq F-16. On November 20th, subsidiary Vectrus Systems LLC. was awarded a $252.1 million cost-plus fixed-fee indefinite contract action for base support services in support of the Iraq F-16 program. Recall, this is one of the major $1 billion-plus contracts V2X has recently won. This contract provides for base operating support, base life support, and security services at the Martyr BG Ali Flaih Air Base in Iraq, and is expected to be complete by September 24, 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

State-of-the-art clean rooms enable accelerated development of microwave products

SAN DIEGO, Nov. 17, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, today announced the relocation of the Jerusalem branch of its Microwave Electronics Division to a new purpose-built facility within the Gav Yam Group high-tech complex, adjacent to the Hebrew University of Jerusalem. The new facility encompasses approximately 60,000 square feet, including 20,000 square feet of clean-room space dedicated to precision assembly, testing, and production of qualified microwave assemblies and subsystems.

The move represents a major investment in Kratos’ international infrastructure and reflects the company’s long-term commitment to advancing high-performance microwave and RF technologies for applications across missiles, radars, satellites, electronic warfare, and other missions.

“This new Jerusalem facility marks an exciting milestone for our team and for Kratos,” said Yonah Adelman, President of Kratos’ Microwave Electronics Division. “With expanded space, advanced clean-room capabilities, and close proximity to the academic and technology talent at Hebrew University, we are positioned to deliver solutions for the next generation of microwave and RF systems faster and more efficiently than ever before. This investment underscores Kratos’ commitment to Israel as a key center of innovation and excellence.”

“Our expansion in Jerusalem reflects Kratos’ commitment to global partnerships and sovereign-capable production,” said Eric DeMarco, President & CEO of Kratos Defense & Security Solutions. “Our long-standing presence in the region gives us a strong base from which to deliver readiness through advanced microwave and digital technologies.”

This Jerusalem facility announcement follows Kratos’ recently announced acquisition of Orbit Technologies Ltd., further enhancing the company’s microwave and digital subsystem capabilities and its team within Israel. By integrating Orbit’s leading RF and satellite communications expertise with Kratos’ global manufacturing reach, Kratos will be better equipped than ever to support customers worldwide.

The new site will serve as a cornerstone for Kratos’ growing microwave and digital subsystem production capacity, supporting both defense and commercial space programs. With its enhanced clean-room infrastructure and advanced testing facilities, Kratos is positioned to meet accelerating demand for reliable, high-volume RF and microwave assemblies in support of international defense readiness.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

SAN DIEGO, Nov. 13, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a leading technology company in the defense, national security, and global markets, today announced the opening of a new Propulsion Manufacturing Facility in Auburn Hills, Michigan to fulfill upcoming demand for Kratos’ Spartan engines, a family of high-quality, low-cost, military grade turbojet engines, a key enabler in the affordable mass problem set.

This state-of-the-art 22,500-square-foot facility with office, manufacturing, assembly and test areas allows for concurrent production of all four engines in the Spartan family and quantities of 50,000 plus per year. The Spartan line of engines consists of four propulsion systems ranging in thrust from 30 to over 200 lbf.

Kratos’ investment in the new facility demonstrates our commitment to advancing affordable mass inventory levels, producing a large number of military-grade, affordable turbojet engines while expanding crucial infrastructure needed to accelerate propulsion system inventory levels as a part of the US defense industrial base.

To support concurrent production and test of the multiple engine types, Kratos has configured the new facility and optimized inventory systems, production flow, and manufacturing ramp plans to enable isolation of key elements such as inventory while enabling shared use for incoming and outgoing inspection, as well as the multi-station test cell.

Kratos’ Auburn Hills Engine Manufacturing, Assembly, and Test Facility

With an investment in infrastructure, personnel, and equipment, Kratos’ Auburn Hills facility is designed for rapid, affordable manufacturing of low-cost turbojet engines to significantly boost critical inventory levels.

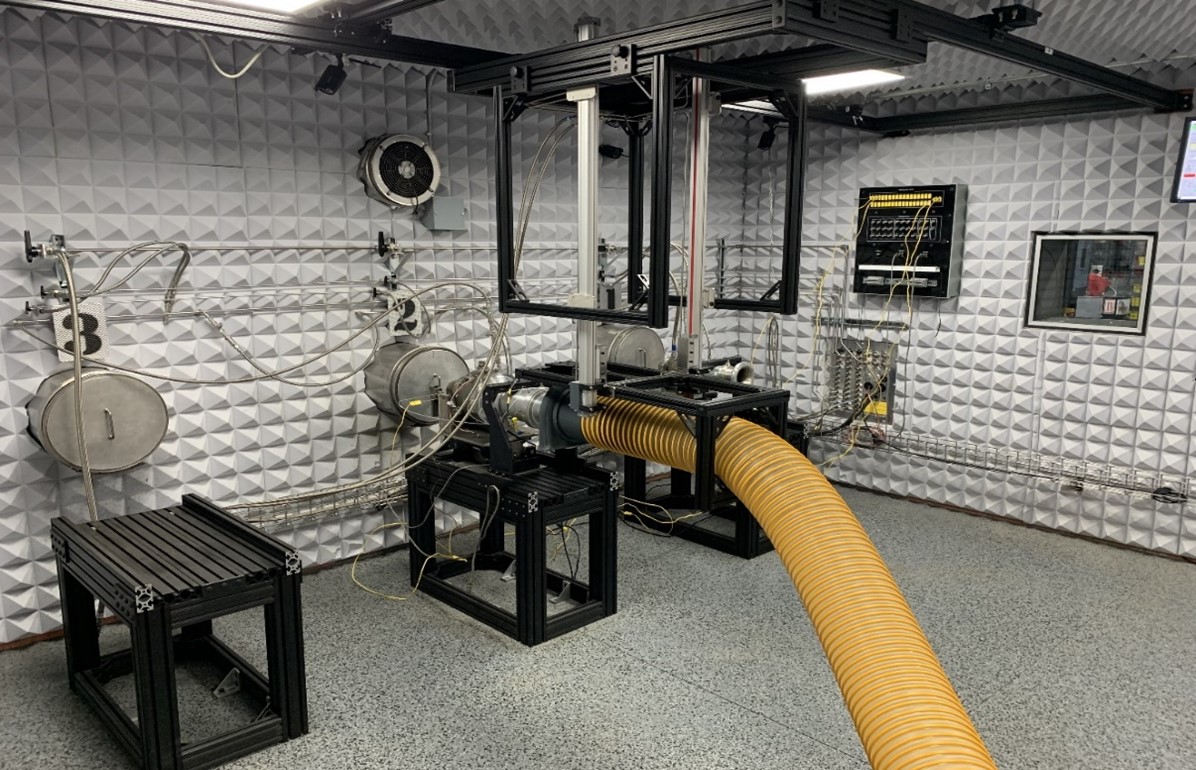

Image of Kratos’ fully attenuated engine test cell that supports running engine tests for acceptance, and full system, missile, aircraft body, analysis, verification, and validation.

Steve Fendley, President of Kratos Unmanned Systems Division, said, “Achieving affordable mass requires effective planning and management at all levels—from supply chain to military customer delivery aligned and optimized for cost, capacity, and resilience. Our production-first mindset has been key to our success in realizing high-reliability, military-grade engines with key operational features that can be produced affordably and delivered at high rates. This is a result of our focus on producibility and cost right from the start, rather than the traditional performance first, manufacturability and cost second approach.”

For more information on Kratos and the Spartan Line of Engines, visit www.kratosdefense.com. ###

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Kratos’ Auburn Hills Engine Manufacturing, Assembly and Test Facility

Kratos’ Auburn Hills Engine Manufacturing, Assembly and Test Facility

Image of Kratos’ Fully attenuated engine test cell that supports running engine tests for acceptance, and full system, missile, aircraft body, analysis, verification, and validation

Image of Kratos’ Fully attenuated engine test cell that supports running engine tests for acceptance, and full system, missile, aircraft body, analysis, verification, and validation