Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Kratos finished 2025 exceeding management’s financial objectives for the fourth quarter, generating approximately 20% year- over-year organic revenue growth, generating a 1.3 to 1.0 book-to-bill ratio on top of the organic growth, having a record backlog of $1.573 billion, and a record opportunity pipeline of $13.7 billion.

4Q25 Results. Fourth quarter revenue of $345.1 million reflected 20% y-o-y organic growth and exceeded our $320 million estimate. Unmanned Systems’ organic revenue growth was 12.1%, while Government Solutions saw 22.2% organic growth. Kratos recorded adjusted EBITDA of $34.1 million, up from $25.2 million a year ago and our $31 million estimate. Adjusted EPS came in at $0.18 versus $0.13 last year and our $0.14 estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. In the fourth quarter, V2X drove record quarterly revenue, adjusted EBITDA, and adjusted cash flow. These results reflect the strength of the Company’s strategy and alignment with national security priorities for readiness and modernization. V2X continues to see momentum across the business coming through contract wins in key growth areas, and we are encouraged by the ongoing demand for the Company’s mission solutions.

4Q25 Results. Revenue increased 5% y-o-y to a record $1.22 billion. Adjusted EBITDA was $88.7 million for the quarter, also a record for the Company. and exceeding management’s expectations. Adjusted net income was $49.3 million and adjusted EPS was $1.56, both representing double-digit year-over-year growth. We were at $1.19 billion, $81 million, and $1.33, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Fourth Quarter 2025 Revenues of $345.1 Million Reflect 21.9 Percent Growth and 20.0 Percent Organic Growth Over Fourth Quarter 2024 Revenues of $283.1 Million

Unmanned Systems Fourth Quarter 2025 Revenues of $68.5 Million Reflect 12.1 Percent Organic Growth Over Fourth Quarter 2024 Revenues of $61.1 Million

Kratos Government Solutions Fourth Quarter 2025 Revenues of $276.6 Million Reflect 22.2Percent Organic Growth Over Fourth Quarter 2024 Revenues of $222.0 Million

Fourth Quarter 2025 Consolidated Book to Bill Ratio of 1.3 to 1 and Bookings of $438.3 Million

Full Year 2025 Consolidated Revenues of $1.347 Billion Reflect 16.6 Percent Organic Growth Over Full Year 2024 Consolidated Revenues of $1.136 Billion

Last Twelve Months Ended December 28, 2025, Consolidated Book to Bill Ratio of 1.1 to 1 and Bookings of $1.475 Billion

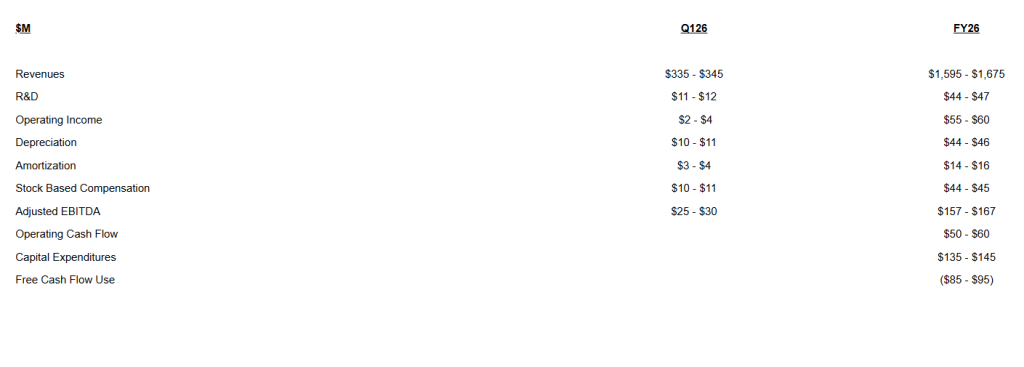

Fiscal 2026 Base Case Revenue Forecast of $1.595 Billion to $1.675 Billion and Adjusted EBITDA Forecast of $157.0 million to $167.0 million or 9.9% to 10.0% of Revenue, including Recently Closed Nomad Global Communication Solutions Acquisition

SAN DIEGO, Feb. 23, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology, Hardware, Products, System and Software Company addressing the Defense, National Security and Commercial Markets, today reported its fourth quarter 2025 financial results, including Revenues of $345.1 million, Operating Income of $8.2 million, Net Income of $5.9 million, Adjusted EBITDA of $34.1 million and a consolidated book to bill ratio of 1.3 to 1.0.

Fourth quarter 2025 Net Income and Operating Income includes non-cash stock compensation expense of $9.1 million, and Company-funded Research and Development (R&D) expense of $9.8 million, including efforts in our Space, Satellite, Unmanned Systems and Microwave Electronic businesses.

Kratos reported in the fourth quarter 2025 GAAP Net Income of $5.9 million and GAAP Net Income per share of $0.03, compared to GAAP Net Income of $3.9 million and GAAP Net Income per share of $0.03, for the fourth quarter of 2024. Adjusted earnings per share (EPS) were $0.18 for the fourth quarter of 2025, compared to $0.13 for the fourth quarter of 2024.

Fourth quarter 2025 Revenues of $345.1 million increased $62.0 million, reflecting 20.0 percent organic growth from fourth quarter 2024 Revenues of $283.1 million. Organic revenue growth was reported in our Unmanned Systems segment of 12.1 percent and in our KGS segment of 22.2 percent. The most notable growth in our KGS Segment was in our Defense Rocket Systems, Microwave Products, and Space, Training and Cyber businesses, with organic revenue growth rates of 47.4 percent, 32.4 percent and 22.7 percent, respectively, compared to the fourth quarter of 2024.

Fourth quarter 2025 Cash Flow Generated by Operations was $12.1 million, primarily reflecting the working capital requirements related to the 21.9 percent revenue growth impacting our receivables, and also including increases in inventory balances related to ramps in production and investments we are making related to certain development initiatives in our Unmanned Systems (KUS) segment, aggregating approximately $51.8 million in working capital use for these items during the quarter. Free Cash Flow Used in Operations for the fourth quarter of 2025 was $0.1 million after funding of $24.2 million of capital expenditures, and net of $12.0 million of proceeds from the sale of Valkyrie units which were previously built as company owned assets and reflected as capital expenditures and therefore the receipt of these sales is reflected in cash flows from investing activities.

For the fourth quarter of 2025, KUS generated Revenues of $68.5 million, compared to $61.1 million in the fourth quarter of 2024, with the increase primarily driven by Valkyrie related activity. KUS’s Operating Income was $1.9 million in the fourth quarter of 2025, compared to an Operating Loss of $0.7 million in the fourth quarter of 2024. KUS’s Adjusted EBITDA for the fourth quarter of 2025 was $6.4 million, compared to $2.6 million for the fourth quarter of 2024, reflecting the impact of the revenue volume and mix. KUS’s book-to-bill ratio for the fourth quarter of 2025 was 1.9 to 1.0 and 1.2 to 1.0 for the twelve months ended December 28, 2025, with bookings of $127.7 million for the three months ended December 28, 2025, and bookings of $358.6 million for the twelve months ended December 28, 2025. Total backlog for KUS at the end of the fourth quarter of 2025 was $361.7 million, compared to $302.5 million at the end of the third quarter of 2025.

For the fourth quarter of 2025, Kratos’ Government Solutions (KGS) segment Revenues of $276.6 million increased from Revenues of $222.0 million in the fourth quarter of 2024, reflecting a 22.2 percent organic growth rate, excluding the impact of the February 2025 acquisition of certain assets of Norden Millimeter, Inc. The increased Revenues includes organic revenue growth across all KGS businesses, with the most notable growth in our Defense and Rocket Support business, Microwave Products business and in our Space, Training and Cyber businesses with organic revenue growth rates of 47.4 percent, 32.4 percent, and 22.7 percent, respectively, over the fourth quarter of 2024.

KGS reported Operating Income of $17.3 million in the fourth quarter of 2025 compared to $11.0 million in the fourth quarter of 2024, primarily reflecting the mix in revenues and increased volume. Fourth quarter 2025 KGS Adjusted EBITDA was $27.7 million, compared to fourth quarter 2024 KGS Adjusted EBITDA of $22.6 million, primarily reflecting the volume and mix in revenues and resources.

KGS reported a book-to-bill ratio of 1.1 to 1.0 for the fourth quarter of 2025, a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended December 28, 2025, and bookings of $310.7 million and $1.117 billion for the three and last twelve months ended December 28, 2025, respectively. KGS’s total backlog was $1.212 billion at the end of the fourth quarter of 2025, compared to $1.178 billion at the end of the third quarter of 2025.

Kratos reported consolidated bookings of $438.3 million and a book-to-bill ratio of 1.3 to 1.0 for the fourth quarter of 2025, and consolidated bookings of $1.475 billion and a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended December 28, 2025. Consolidated backlog was $1.573 billion on December 28, 2025, as compared to $1.480 billion on September 28, 2025. Kratos’ bid and proposal pipeline was $13.7 billion on December 28, 2025, as compared to $13.5 billion at September 28, 2025. Backlog on December 28, 2025, included funded backlog of $1.232 billion and unfunded backlog of $341.4 million.

Full Year 2025 Results

Kratos reported its full year 2025 financial results, including Revenues of $1.347 billion, Operating Income of $25.6 million, Net Income of $22.0 million, Adjusted EBITDA of $119.9 million and a consolidated book to bill ratio of 1.1 to 1.0.

Included in the full year 2025 Net Income and Operating Income is non-cash stock compensation expense of $35.5 million, Company-funded Research and Development (R&D) expense of $40.0 million, including ongoing development efforts in our Space and Satellite Communications business to develop our first to market, virtual, software-based OpenSpace command & control (C2), telemetry tracking & control (TT&C) and other ground system solutions, and ongoing development efforts in our Unmanned Systems and Microwave Products businesses.

Kratos reported full year 2025 GAAP Net Income of $22.0 million and GAAP Net Income per share of $0.13, compared to $16.3 million and GAAP Net per share of $0.11, for the full year 2024. Adjusted earnings per share (EPS) were $0.55 for the full year 2025, compared to $0.49 for the full year 2024.

Full year 2025 Revenues of $1.347 billion increased $210.5 million from 2024, reflecting 18.5 percent growth and 16.6 percent organic growth. Full year 2025 Cash Flow Used in Operations was $42.1 million, reflecting the working capital uses to fund revenue growth resulting primarily in increases in receivables, inventories, prepaid assets and investments in other assets and reduction of deferred revenues or advanced customer payments. Free Cash Flow Used in Operations was $125.4 million after funding $95.3 million of capital expenditures, and net of $12.0 million of proceeds from sale of Valkyrie units which were previously built as company owned assets and reflected as capital expenditures. Full year 2025 capital expenditures were elevated due primarily to the manufacture of the two production lots of Valkyries prior to contract award to meet anticipated customer orders and requirements and due to investments related to the expansion and addition of production facilities.

For full year 2025, KUS generated Revenues of $292.0 million, as compared to $270.5 million in the full year 2024, reflecting 7.9 percent organic growth, primarily reflecting increased Valkyrie and tactical drone activity. KUS’s Operating Income was $2.6 million in full year 2025 compared to $2.9 million in full year 2024. KUS’s Adjusted EBITDA for full year 2025 was $18.1 million, compared to full year 2024 Adjusted EBITDA of $16.3 million, reflecting the increased volume partially offset by increased material and subcontractor costs on multi-year fixed price contracts.

For full year 2025, KGS Revenues of $1.055 billion increased $189.0 million, reflecting 19.3 percent organic growth from Revenues of $865.8 million in full year 2024. The increased Revenues includes organic revenue growth across all of our business units, with the most notable increases in our Defense Rocket Support, Microwave Products, and Space, Training and Cyber businesses, with organic revenue growth rates of 56.3 percent, 17.1 percent and 13.6 percent, respectively.

KGS reported operating income of $60.6 million in full year 2025 compared to $56.6 million in full year 2024, primarily reflecting the increased revenue volume. Full year 2025 KGS Adjusted EBITDA was $101.8 million, compared to full year 2024 KGS Adjusted EBITDA of $89.4 million, primarily reflecting the increased revenue.

Eric DeMarco, Kratos’ President and CEO, said, “We finished 2025 exceeding our financial objectives for the fourth quarter, generating approximately 20 percent Q4 year- over-year organic Revenue growth, generating a 1.3 to 1.0 book to bill ratio on top of this 20 percent organic growth, having a record backlog of $1.573 billion, and a record opportunity pipeline of $13.7 billion, with the opportunity set for Kratos having never been stronger and continuing to increase. Kratos is positioned to achieve our previously communicated 2026 and 2027 financial targets, and similar to 2025, for 2026 we expect our business to accelerate throughout the year, with increasing Revenue volume and Adjusted EBITDA margins, as several new programs, contracts and initiatives begin, ramp and expand.”

Mr. DeMarco continued, “Since our last report, the global National Security opportunity and funding environment for the industry and for Kratos has significantly improved, including the extended U.S. Federal Government shutdown being resolved, the Continuing Resolution being resolved, the 2026 NDAA being signed and the fiscal 2026 Defense Appropriations Bill being signed, bringing the total 2026 National Security related approved spend to approximately $1 trillion. There is a generational recapitalization of the defense industrial base underway due to the geopolitical and related global threat environment, one that we believe that Kratos is uniquely positioned to address. Rapidly manufacturing and delivering affordable military grade hardware, at scale, that must work every time, is hard, and our customers and partners recognize this as one of Kratos’ key differentiators.”

Mr. DeMarcowent on, “We recently announced that our teammate Northrop Grumman received the MUX TACAIR Collaborative Combat Aircraft, or CCA, program award, with Kratos Valkyrie as the CCA aircraft, equipped with Northrop’s mission systems. Additionally, Kratos has now successfully received another tactical drone program of record contract award, and I believe that we are in a sole source position for two additional tactical drone program opportunities, including for Valkyrie. As a result of our progress and based upon expected future customer contractually required delivery schedules, we will be executing a plan in 2026 to increase our rate of production up to approximately 40 Valkyries annually by the end of 2027.”

Mr. DeMarco added, “We now have 120 Kratos Zeus and Oriole solid rocket motors on order, with deliveries of the SRMs to Kratos expected to begin in Q3 of this year and expected to ramp into 2027, and the SRMs are either under customer contract or are directly related to expected hypersonic or “other” vehicle system integration and launch efforts to be performed. Additionally, it was recently announced that Kratos was selected to develop a next generation, highly maneuverable hypersonic missile, with certain other non-traditional vendors. We are also hoping to receive an additional approximate $1 Billion hypersonic program related opportunity by the end of this year, which we believe will be sole source to Kratos as prime. Kratos’ hypersonic franchise is expected to be a primary driver of our expected future revenue growth.”

Mr. DeMarcoconcluded, “We believe that Kratos’ strategy and consistent business plan since inception, including making true internally funded investments ahead of government commitment, for facilities, manufacturing capability and relevant products for the warfighter, while not paying dividends or buying back our stock, are aligned with the current Administration and is an important differentiator for Kratos. I believe that due to the global threat environment, certain customers are out of time, have limited immediate resources, and that the significant investments that Kratos has made to be first-to-market with relevant systems, hardware and software are now invaluable. We believe that the scarcity value of Kratos is clear, and we are laser focused on our balanced business model of making investments, rapidly delivering affordable products and systems to the warfighter at scale, and generating a financial return for our investors.”

Financial Guidance We are providing our first quarter and full year Base Case 2026 guidance, which includes our assumptions, including as related to: current forecasted business mix, expected employee sourcing, hiring and retention; potential manufacturing, production and supply chain disruptions; potential parts shortages and related continued significant cost and price increases in each of these areas, all of which are impacting the industry and Kratos. We are also making significant investments in bid, proposal and other new program opportunity areas, which are currently adversely impacting our profit margins. These investments are expected to continue at least into Kratos’ fiscal 2027, as our opportunity pipeline continues to increase.

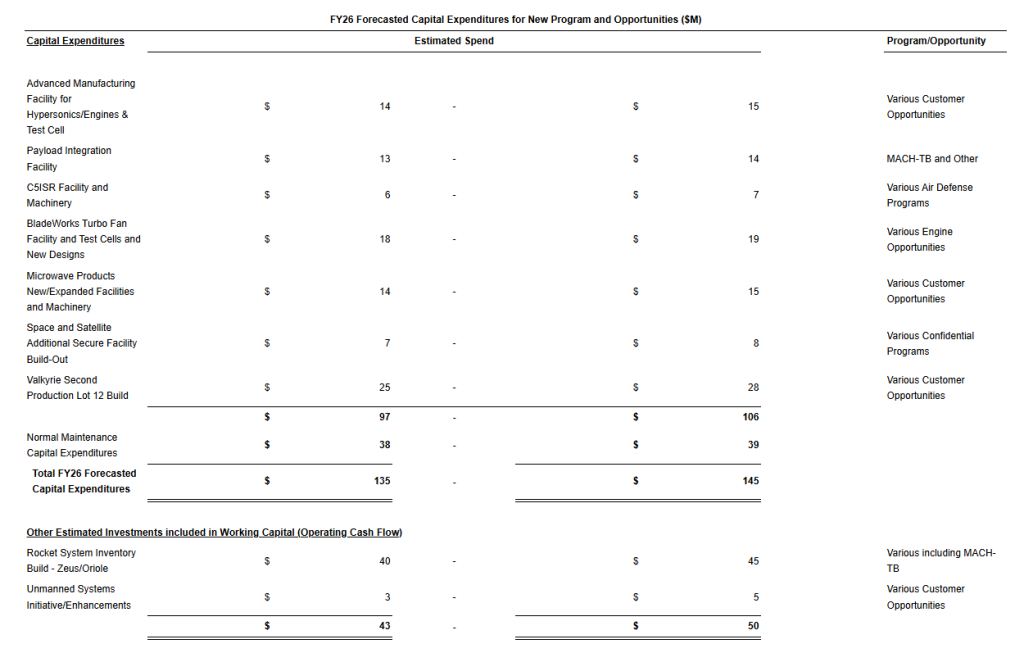

Kratos’ operating cash flow guidance also assumes certain investments in our Rocket Systems and Unmanned Systems businesses, related to the procurement of rocket and related systems and our plan to begin producing approximately 40 Valkyries annually beginning by the end of 2027 as well as the completion of certain of our unmanned systems and related derivatives and vehicles. Additional forecasted investments in 2026 include our funding of the Prometheus joint venture established last year, our Anaconda radar program, our Helios hypersonic and arc chamber program, our Indiana hypersonic integration facility, our Birmingham advanced manufacturing facility for hypersonics, expansion and new microwave electronics facilities in Israel and the US, our GEK and BladeWorks engine facilities, the continued build of our second lot of 12 Valkyrie aircraft, and our Vulcan, Kraken, Elysium, Nemesis, Hermes and other initiatives. In summary, Kratos continues to make the required investments to support the rebuild of the U.S. defense industrial base and related infrastructure, take advantage of the ongoing generational recapitalization of strategic and other weapon and National Security related systems, and generate value for all Kratos stakeholders, including the warfighter and Kratos shareholders.

Our first quarter and full year Base Case 2026 guidance ranges, which includes the recently closed Nomad Global Communication Solutions acquisition, and a summary of the forecasted investments for new programs and opportunities are presented below.

For Kratos’ Base Case fiscal year 2026 forecast, we currently expect the first fiscal quarter to be the lowest in both revenue and Adjusted EBITDA, including as a result of the extended U.S. Federal Government shutdown in the fourth quarter of fiscal 2025, which impacted government contracting, program, administrative and other functions and offices. The impact of the shutdown, we believe, resulted in among other issues, the delay of certain “short turn” contract awards to Kratos, including certain expected software, data related and product sales, which typically generate higher than our normal profit margins. We believe the government shutdown also resulted in a delay in the award of certain longer-term contracts, programs and funding. With the government shutdown now over and the Department of War (DoW) and related Federal Agencies at full function again, we expect to receive these contract and program awards, sales and funding, beginning in our second quarter of 2026. The expected overall lower revenue in our first fiscal quarter is expected to result in lower Adjusted EBITDA, including as a result of the loss of financial leverage on certain of our fixed general, administrative, overhead, infrastructure, bid, proposal and other costs, with a more pronounced impact as we have expanded our infrastructure to support our growing businesses.

Also contributing to our expectation that Kratos second half of fiscal 2026 will have significantly higher Revenue and Adjusted EBITDA than the first half, we expect to begin to receive in the second half of 2026 certain long lead items related to existing customer funded programs, including solid rocket motors and other hardware related to certain hypersonic and other programs, hardware and components related to jet engine and propulsion system development and production, and hardware related to air defense, missile, radar and other National Security system production.

As a result of all of the above, we expect Kratos’ second quarter of fiscal 2026 to have somewhat increased Revenue and Adjusted EBITDA over our fiscal first quarter, and we expect Kratos’ second half of fiscal year 2026 Revenue, Adjusted EBITDA and operating cash flow to be greater than our first half, as our Revenue increases, Adjusted EBITDA margins are expected to expand and contract funding is expected to increase. All financial forecasts provided today include the expected contribution from the recently closed acquisition of Nomad Global Communication Solutions, Incorporated.

We continue to expect Base Case Kratos’ full year 2026 organic revenue growth to be approximately 15 percent to 20 percent above our full year fiscal 2025 revenue financial forecast, which we previously provided in November 2025, and which we exceeded. We continue to expect Kratos’ Base Case full year 2027 organic revenue growth to be approximately 18 percent to 23 percent above the full year fiscal 2026 revenue forecast we provided today. We continue to expect Kratos’ full year 2026 Adjusted EBITDA margin rates to be approximately 100 bps greater than our reported 2025 Adjusted EBITDA margin rates. And we continue to expect our current forecast 2027 Adjusted EBITDA margin rates to increase an additional 100 bps above 2026 Adjusted EBITDA margin rates. Kratos’ Base Case Revenue and Adjusted EBITDA forecasts do not include large scale production of Kratos Valkyrie or other tactical drone production, which will only be included once Kratos receives definitized customer delivery schedules that we can accurately forecast. Additionally, none of the above financial information includes the estimated impact from the pending Orbit Technologies Ltd acquisition, which financial information will only be included once the acquisition closes.

Management will discuss the Company’s financial results at a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, hardware, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field relevant solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as the innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing, which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe our probability of win is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of probability of win is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include, virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, command, control, communication, computing, combat, intelligence surveillance and reconnaissance (C5ISR) and microwave electronic products for missile, radar, air defense, missile defense, space, satellite, counter unmanned aircraft systems (CUAS), directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice RegardingForward–LookingStatements This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its first quarter, second quarter, first half, second half, and full year 2026 revenues, R&D, operating income, depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2026 operating cash flow, capital expenditures, investments, and free cash flow, forecasted company and business unit organic revenue growth, estimated revenue and organic revenue growth for 2026 and 2027, Adjusted EBITDA margins in 2026 and 2027, future initiation of higher margin programs and negotiation of lower margin contracts which are expected to be renewed in the future, expected future investments in property, plant, facilities, and equipment (including expected investments in the Prometheus joint venture and other programs, opportunities, and initiatives), expected future production of Valkyries, the ability of the Company’s customers to respond to industry and market conditions, the impact of acquired companies and businesses on the Company’s operations and financial condition, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, ability to successfully compete and expected new customer awards, the impact of federal government shutdowns on the Company’s operations and financial condition, the availability and timing of government funding for the Company’s offerings, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoW may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will not become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoW Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates; currently unforeseen risks associated with any public health crisis, and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 28, 2025, and in our other filings made with the Securities and Exchange Commission.

Note Regarding Use of Non-GAAP Financial Measures and Other Performance Metrics This news release contains non-GAAP financial measures, including organic revenue growth rates, Adjusted EPS (computed using income before income taxes, excluding depreciation, amortization of intangible assets, amortization of capitalized contract and development costs, stock-based compensation expense, acquisition and restructuring related items and other, which includes, but is not limited to, legal related items, non-recoverable rates and costs, and foreign transaction gains and losses, less the estimated impact to income taxes) and Adjusted EBITDA (which excludes, among other things, acquisition and restructuring related items, stock compensation expense, foreign transaction gains and losses, and the associated margin rates). Additional non-GAAP financial measures include Free Cash Flow from Operations computed as Cash Flow from Operations less Capital Expenditures plus proceeds from sale of assets and Adjusted EBITDA related to our KUS and KGS businesses. Kratos believes this information is useful to investors because it provides a basis for measuring the Company’s available capital resources, the actual and forecasted operating performance of the Company’s business and the Company’s cash flow, excluding non-recurring items and non-cash items that would normally be included in the most directly comparable measures calculated and presented in accordance with GAAP. The Company’s management uses these non-GAAP financial measures, along with the most directly comparable GAAP financial measures, in evaluating the Company’s actual and forecasted operating performance, capital resources and cash flow. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and investors should carefully evaluate the Company’s financial results calculated in accordance with GAAP and reconciliations to those financial results. In addition, non-GAAP financial measures as reported by the Company may not be comparable to similarly titled amounts reported by other companies. As appropriate, the most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to the Company’s financial results prepared in accordance with GAAP are included in this news release.

Another Performance Metric the Company believes is a key performance indicator in our industry is our Book to Bill Ratio as it provides investors with a measure of the amount of bookings or contract awards as compared to the amount of revenues that have been recorded during the period and provides an indicator of how much of the Company’s backlog is being burned or utilized in a certain period. The Book to Bill Ratio is computed as the number of bookings or contract awards in the period divided by the revenues recorded for the same period. The Company believes that the rolling or last twelve months’ Book to Bill Ratio is meaningful since the timing of quarter-to-quarter bookings can vary.

Net income of $22.8 million; adjusted net income1 of $49.3 million, up 16% year-over-year

Adjusted EBITDA1 of $88.7 million; adjusted EBITDA1 margin of 7.3%

Diluted EPS of $0.72; record adjusted diluted EPS1 of $1.56, up 17% year-over-year

Cash flow from operations of $209.5 million

Full-Year Highlights

Revenue of $4.48 billion, up 4% year-over-year

Net income of $77.9 million; adjusted net income1 of $166.8 million, up 20% year-over-year

Adjusted EBITDA1 of $323.3 million, with a margin of 7.2%

Diluted EPS of $2.45; adjusted diluted EPS1 of $5.24, up 21% year-over-year

Cash flow from operations of $182.0 million

Achieved net debt reduction of $116 million and 2.2x net leverage ratio1

2026 Guidance

Establishing full-year 2026 guidance with 6% revenue and adjusted EBITDA1 growth at mid-point

RESTON, Va., Feb. 23, 2026 /PRNewswire/ — V2X, Inc. (NYSE:VVX) today announced financial results for the fourth quarter and full-year 2025 ended December 31, 2025, and established guidance for full-year 2026.

“V2X ended 2025 with another quarter of strong performance, underscoring our team’s successful execution of our strategy,” said Jeremy C. Wensinger, President and Chief Executive Officer. “We are entering 2026 with significant momentum. Our recent awards and alignment to National Security priorities for readiness and modernization are creating tailwinds for continued growth. Additionally, we are continuing to prioritize investments and expand partnerships to deliver innovative solutions that anticipate and fulfill our customers’ requirements. These growth priorities are further supported by the strength of our capital structure. As we look ahead, V2X is well positioned to continue to deliver readiness enabling solutions to support our customers’ evolving requirements, while generating enhanced value for our shareholders.”

Fourth Quarter 2025 Results

In the fourth quarter, V2X reported record revenue of $1.22 billion, which represents 5% year-over-year growth. The Company reported solid topline growth and strong operating performance, yielding double-digit growth in adjusted net income1 and adjusted EPS1. Net income for the quarter was $22.8 million. Adjusted net income1 was $49.3 million, an increase of $6.6 million dollars, or 16%, year-over-year. Fourth quarter GAAP diluted EPS was $0.72. Adjusted diluted EPS1 for the quarter increased 17% year-over-year to $1.56.

V2X delivered record adjusted EBITDA1 of $88.7 million, with a margin of 7.3%, representing an increase of $2.6 million dollars, or 3%, from the prior year.

Fourth quarter net cash provided by operating activities was $209.5 million. Adjusted net cash provided by operating activities1 increased 3% year-over-year to $172.4 million.

At the end of the fourth quarter, net debt for V2X was $758 million, representing an improvement of $116 million year-over-year and achieving its 2.2x net leverage ratio1.

Total backlog as of December 31, 2025 was $11.1 billion. Funded backlog1 was $2.3 billion. Book-to-bill1 in the quarter was approximately 0.7x.

Full-Year 2025 Results

Full-year revenue was $4.48 billion, representing a 4% increase compared to the previous year.

Net income for the year was $77.9 million. Adjusted net income1 was $166.8 million, an increase of $27.9 million dollars, or 20%, year-over-year. Full-year GAAP diluted EPS was $2.45. Adjusted diluted EPS1 for 2025 was $5.24, increasing 21% year-over-year. Full-year adjusted EBITDA1 was $323.3 million with a margin of 7.2%.

Net cash provided by operating activities in 2025 was $182.0 million. Adjusted net cash provided by operating activities1 was $148.3 million.

2026 Guidance

Expectations for the Company’s full year 2026 financial results are as follows:

$ millions, except for per share amounts

2026 Guidance

2026 Mid-Point

Revenue

$4,675

$4,825

$4,750

Adjusted EBITDA1

$335

$350

$343

Adjusted Diluted Earnings Per Share1

$5.50

$5.90

$5.70

Adjusted Net Cash Provided by Operating Activities1

$150

$170

$160

The Company is not providing a quantitative reconciliation with respect to the foregoing forward-looking non-GAAP measures in reliance on the “unreasonable efforts” exception set forth in SEC rules because certain financial information, the probable significance of which cannot be determined, is not available and cannot be reasonably estimated. For example, unusual, one-time, non-ordinary, or non-recurring costs, which relate to M&A, integration and related activities cannot be reasonably estimated. Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Fourth Quarter Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Monday, February 23, 2026. U.S.-based participants may dial in to the conference call at 877-300-8521, while international participants may dial 412-317-6026. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/3do4py9pnRx

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 9, 2026, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10195666.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the company’s website at https://gov2x.com. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

___________________________

1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,200 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management. Forward-looking statements in this press release, include, but are not limited to our future performance and capabilities; all of the statements and items listed under “2026 Guidance” above and other assumptions contained therein for purposes of such guidance; our belief that prior performance provides substantial visibility for future performance; market trends; product development; capital deployment; statements about the benefits and expectations with respect to the strategic acquisition; and our belief that our innovation strategy, visibility, and targeted growth opportunities provide substantial opportunities for value creation.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

PDF VersionJoint team will complete preliminary design of the GEK1500 engine to meet high performance and aggressive cost targets, leveraging GEK800 maturation to accelerate delivery

SAN DIEGO, Feb. 23, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, and GE Aerospace (NYSE: GE), today announced a joint U.S. Air Force contract for $12.4M to design a next generation engine for small Collaborative Combat Aircraft (CCA). The initial phase of the program will complete the preliminary design of the GEK1500 engine to meet demanding performance requirements while achieving aggressive cost targets for affordable mass.

Stacey Rock, President of Kratos Turbine Technologies Division, said, “Building on the success of our GEK800 engine program, the development of the GEK1500 further demonstrates our team’s ability and commitment to deliver high-performance, affordable, jet engines that can be rapidly produced to meet the demands of our defense customers.”

“Lessons learned from recent GEK800 altitude testing are directly informing GEK1500 —improving thrust, power generation, and lifecycle cost — so we can meet CCA requirements without compromising affordability or schedule,” said Steve “Doogie” Russell, Vice President and General Manager of Edison Works at GE Aerospace.

The GEK1500 is a 1,500-lb thrust jet engine that could potentially power unmanned aerial systems (UAS), collaborative combat aircraft (CCAs), and missiles. The design of the GEK1500 leverages the GEK800 cruise missile engine architecture which is successfully completing technical maturation. An additional option on the contract, if exercised, would enable the team to assess key design risks and characterize engine performance under relevant flight and installation conditions for the GEK1500 engine. The Air Force has prioritized the development of high performing and low-cost engines to enable the disruptive capabilities of small CCAs.

GEK1500 Engine (Concept Rendition: Kratos and GE Aerospace)

Recent altitude testing of the GEK800 engine demonstrated critical technologies that will provide future systems increased range, increased thrust, decreased life cycle cost, and increased electrical power. The investments and progress made to date on the GEK800 will reduce the cost and schedule timelines for the GEK1500 and provide enhanced performance for small CCAs.

In June, Kratos and GE Aerospace announced the signing of a formal teaming agreement to advance propulsion technologies for the next generation of affordable unmanned aerial systems and CCA-type aircraft, covering the GEK800 and a framework for partnering on additional engines. The result is another formal teaming agreement covering the GEK1500. This collaboration strengthens the companies’ ongoing partnership and builds on a 2024 Memorandum of Understanding (MOU) to advance the development and production of small, cost-effective engines for unmanned platforms. The teaming agreement expanded on that MOU and provided the framework for the two companies to develop, manufacture, test, and field the GEK800 and additional GEK engines in higher thrust classes.

Kratos brings more than 25 years of experience developing and producing small, affordable engines for UAS, drones, and missile platforms. GE Aerospace adds a century of expertise in propulsion technology and the ability to scale advanced designs into high-rate production, helping bridge the gap from prototype to deployment.

About GE Aerospace GE Aerospace is a global aerospace propulsion, services, and systems leader with an installed base of approximately 49,000 commercial and 29,000 military aircraft engines. With a global team of approximately 53,000 employees building on more than a century of innovation and learning, GE Aerospace is committed to inventing the future of flight, lifting people up, and bringing them home safely. Learn more about how GE Aerospace and its partners are defining flight for today, tomorrow and the future at www.geaerospace.com.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition. In a 424B3 filing, Kratos disclosed that it acquired Nomad Global Communication Solutions, Incorporated, for an initial amount of 972,136 KTOS shares or approximately $100 million. Nomad provides mobile command, control, and communications systems for space and satellite systems, UAVs, counter UAVs, and other systems, with clients including all branches of the U.S. armed forces, Homeland Security, and other Agencies, among others. We expect management to provide additional detail and color on the earnings call.

Drone Dominance. Kratos has been selected to participate in the initial Phase 1 Gauntlet for the Office of the Secretary of War’s Drone Dominance Program. This opportunity seeks to identify and evaluate platforms capable of demonstrating multiple one-way attack missions through a live competition. Upon successful completion of the Gauntlet, participants will be ranked and extended a prototype delivery award based on their performance and placement. The Drone Dominance Program represents a $1.1 billion investment in groundbreaking unmanned systems technologies. The program aims to procure approximately 350,000 units.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In-Depth Modeling, Simulation of Hypersonic Environments Will Lead to a Robust Set of Hypersonic Test Setpoints to Enable Rapid Evaluation, Transition of Various Thermal Protection System Materials

SAN DIEGO, Feb. 18, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, announced today that it has been awarded a contract through the Department of War’s Joint Hypersonics Transition Office to support test and evaluation of thermal protection systems for hypersonic vehicles. For this program, Kratos will leverage decades of expertise in hypersonics to analyze various missions and flight environments to understand appropriate testing conditions. Kratos will establish standard test conditions and techniques to accelerate materials development and can be used as a baseline for other similar aerothermal test facilities.

“The Kratos team is committed to advancing materials for hypersonics through testing and evaluation,” said Ben Dempsey, Kratos SRE Vice President of Programs. “Our focus is on accelerating the development of systems for our warfighter. This begins with increased throughput of our nation’s testing infrastructure, and by making investments in new infrastructure, like the recently awarded Project Helios.”

The test methodologies developed under this program will serve as a model for the hypersonic testing community, accelerating the advancement and deployment of next-generation U.S. hypersonic vehicle technologies. Additionally, Kratos will execute a series of material test campaigns leveraging these procedures that will validate the methodology and mature material solutions.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

RESTON, Va., Feb. 18, 2026 /PRNewswire/ — V2X Inc. (NYSE: VVX) proudly announces its selection for a seat on the Advanced Technology Support Program 5 (ATSP5), a $25 billion multiple-award Indefinite Delivery/Indefinite Quantity (IDIQ) contract. ATSP5, administered by the Defense Microelectronics Activity (DMEA) under the Office of the Secretary of Defense, is one of the Department of Defense’s most comprehensive engineering development and technology transition initiatives.

This contracting vehicle provides federal and state government agencies with streamlined access to V2X’s capabilities in delivering mission-critical solutions. The scope of ATSP5 includes engineering development, from system studies and prototyping to testing, integration, and limited production. It also includes full lifecycle technology support for embedded systems, network-centric warfare systems, large-scale integrations, and standalone systems. The program creates opportunities for modernization, overcoming obsolescence challenges, and extending the lifecycle of aging equipment while advancing cutting-edge technology such as AI-optimized systems and large-scale AI orchestration to address emerging threats.

As an ATSP5 program partner, V2X brings decades of expertise to solving complex engineering challenges through scalable, transformative solutions tailored to defense priorities. Its capabilities address key areas such as rapid acquisition, systems engineering, microelectronics supply assurance, digital prototyping, optimized automated testing, intelligent integration, performance optimization, and the intelligent application of advanced technologies with the aid of AI.

“Winning a position on the ATSP5 enables V2X as a leader in transformative engineering solutions,” said Jeremy C. Wensinger, President and Chief Executive Officer of V2X. “Our selection places us at the forefront of defense modernization, allowing us to deliver advanced capabilities that don’t simply respond to threats and system obsolescence, but anticipate and evolve with them. From AI-powered performance enhancement and autonomous system integration, we are redefining what operational resilience looks like in multi-domain operations. We are honored to contribute to the future of our nation’s warfighter operational superiority.”

In line with the Department of Defense’s most strategic modernization initiatives, V2X’s participation in ATSP5 underscores a commitment to advancing technology-first solutions for critical challenges faced by the warfighter. By deploying intelligent agents for modernizing government systems, advancing innovations, and addressing both traditional and asymmetric challenges, V2X will help ensure readiness and progress in support of the warfighter, while delivering solutions that reflect the highest standards of technical performance, security, and sustainability. V2X ensures unmatched readiness and technological overmatch in defense capabilities

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Media Contact Angelica Spanos Deoudes Director, Corporate Communications Angelica.Deoudes@goV2X.com 571-338-5195

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

End-to-End Ground System Will Maximize the Full Capabilities of Advanced Software-Defined Satellite

SAN DIEGO, Feb. 17, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced that Airbus Defence and Space has awarded Kratos a contract to deliver a ground segment for its customer Space Communication Technologies (SCT) SPC to support the OmanSat-1 software-defined satellite.

With the growing need for mission flexibility to deliver high throughput services, Oman’s national satellite operator, SCT selected Airbus Defence and Space to deliver OmanSat-1, a fully reconfigurable high-throughput OneSat satellite and the associated ground system. Airbus selected Kratos to deliver the integrated ground system to operate the OmanSat-1 software-defined satellite.

Elodie Viau, Senior Vice President of Telecommunication and Navigation for Airbus Defence and Space, said, “The OmanSat-1 satellite uses a flexible OneSat payload architecture that needs a ground system that is just as dynamic to support the reconfiguration of the satellite and the monitoring of the signals to enable troubleshooting and performance reporting. Building on our successful collaboration across multiple OneSat programs, Kratos will deliver the ground system that works in tandem with the OmanSat-1 satellite, enabling SCT to provide high-throughput services while providing extensive flexibility, serving Oman and the region and expanding to access East African and East Asian markets.”

Reinforcing the need for satellites and ground systems to escape legacy silos and work together in tandem, Luke Wyles, an analyst with Analysys Mason explained in a recent white paper that “in order to optimize the resource allocation on the Software-Defined Satellite (SDS), the network must be orchestrated, reconfiguring the space and ground segment in unison to meet changing demands.”

Bruno Dupas, Vice President of Kratos Space, said, “Kratos is integrating the ground system with Airbus’ mission and control platform to manage and monitor the satellite payload while intelligently orchestrating ground resources. This will enable SCT to dynamically plan spectrum, seamlessly coordinate payload configurations with ground assets, and do so far faster and in a more automated fashion than ever before.”

Kratos will deliver the ground segment that will include the capability to configure and monitor the satellite, optimize and setup the payload using integrated Airbus components, monitor the performance of the entire system from the satellite to the ground and orchestrate part of the operations. The implementation will include Ka-Band telemetry, tracking and command (TT&C) antennas, monitor and control and carrier monitoring software, command, control and flight dynamics capabilities and the orchestration system. Leveraging its office in Oman, Kratos will also perform site surveys, install and commission equipment, deliver training and provide support for the delivery.

Kratos has a proven track record of delivering state-of-the-art ground solutions and is at the forefront of developing new capabilities to support today’s software-defined satellites. This includes the recent successful completion of the first factory acceptance test of Kratos’ Epoch command and control (C2) system with Airbus’ OneSat software-defined satellite. Kratos also brings a breadth of experience across the ground segment in areas such as satellite C2; TT&C; payload operations; network management and spectrum monitoring to deliver integrated satellite and ground system solutions.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

SAN DIEGO, Feb. 13, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the fourth quarter and fiscal year 2025 after the close of market on Monday, February 23rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

RESTON, Va., Feb. 11, 2026 /PRNewswire/ — V2X Inc. (NYSE: VVX) was awarded $100 million in classified contracts during the fourth quarter of 2025 to support a broad range of national security missions for multiple U.S. defense and intelligence agencies. The awards include services and solutions in the areas of cyber operations, special systems integration, unique facility solutions and contested logistics.

“These awards demonstrate the trust national security agencies place in V2X and our deep expertise in intelligence and cyber operations,” said Jeremy C. Wensinger, President and Chief Executive Officer of V2X. “We are purposefully growing our presence in this sector and remain dedicated to supporting expanded C5ISR missions.”

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

Media Contact Angelica Spanos Deoudes Director, Corporate Communications Angelica.Deoudes@goV2X.com 571-338-5195

SAN DIEGO, Feb. 10, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a leading technology company in defense, national security, and global markets, announced today that it has been selected to participate in the initial Phase 1 Gauntlet for the Office of the Secretary of War’s Drone Dominance Program. This opportunity seeks to identify and evaluate platforms capable of demonstrating multiple one-way attack missions through a live competition.

“Unmanned systems are redefining the landscape of war. To ensure our superiority, we must equip our warfighter with the tools needed to neutralize adversarial threats, enhance mission success, and ensure operational safety,” said Dave Carter, President of Kratos Defense & Rocket Support Services Division. “Kratos’ small unmanned aerial systems portfolio provides such a platform, enabling mass attritables in the battlefield.”

Upon successful completion of the Gauntlet, participants will be ranked and extended a prototype delivery award based on their performance and placement.