Deal Enhances Social Mobile’s Position in Enterprise Mobility and Expands Carrier Channel Reach

In a strategic move to strengthen its leadership in the enterprise mobility space, Social Mobile announced it has entered into a definitive agreement to acquire the assets and liabilities of Sonim Technologies (NASDAQ: SONM). The all-cash transaction is valued at $20 million, including a $5 million potential earn-out, and is expected to close in the fourth quarter of 2025, pending customary closing conditions.

The acquisition aligns with Social Mobile’s long-term strategy to expand its footprint in the purpose-built enterprise mobility market. Sonim Technologies, known for its rugged mobile solutions trusted by first responders, government agencies, and Fortune 500 companies, brings a complementary product portfolio and proven expertise in mission-critical communications to Social Mobile’s custom enterprise offerings.

“This acquisition creates a powerful synergy between Sonim’s durable, field-tested devices and Social Mobile’s scalable, custom mobility solutions,” said a spokesperson for Social Mobile. “Together, we are better positioned to deliver innovative, secure, and tailored mobility ecosystems that meet the evolving needs of our global clients.”

Sonim’s Board of Directors has approved the agreement.

Founded in 1999, Sonim Technologies has established itself as a leading U.S. provider of ultra-rugged phones, wireless data devices, and accessories, with a distribution footprint across North America, EMEA, and Asia-Pacific. The company’s products are widely adopted in industries where durability, security, and performance are non-negotiable.

For Social Mobile, a Google-certified Android Enterprise Gold Partner, this acquisition not only enhances its enterprise-grade product suite but also significantly expands its sellable addressable market, particularly through carrier channels where Sonim has longstanding relationships.

Social Mobile specializes in developing custom mobility solutions for clients across healthcare, transportation, retail, and defense. With over 15 million devices distributed globally, the company offers end-to-end services from design and deployment to lifecycle management, ensuring product availability and operational efficiency at scale.

As enterprise mobility demand continues to rise, the combined capabilities of Social Mobile and Sonim are expected to unlock new revenue opportunities and deliver greater value to customers looking for rugged, reliable, and custom-built mobile solutions.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Support Services. According to the daily Department of Defense contract announcements, V2X subsidiary Vectrus Systems has been awarded an $118 million cost-plus-fixed-fee undefinitized contract for base support services in support of the Iraq F-16 program. This is another in a long line of recent wins for V2X, demonstrating the V2X value proposition and confirming the significant traction on near-term Foreign Military and International opportunities previously highlighted by management.

Details. The contract provides for base operating support, base life support, and security services. Work will be performed at Martyr BG Ali Flaih Air Base, Iraq, and is expected to be completed by Nov. 30, 2026. This contract involves Foreign Military Sales (FMS) to Iraq. This contract was a sole source acquisition. FMS funds in the amount of $57.8 million are being obligated at the time of award.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mixed Environment. Steelcase continues to face a mixed environment, both on a vertical basis and a geographical basis. The key large corporate customer cohort is doing well, driven by a number of factors such as return to office, but education and government have been hit by funding uncertainties. Germany and France remain sluggish in the key small-to-mid-sized business, but India and China are doing better.

International Actions. Steelcase is taking steps to implement additional cost reduction efforts in Europe, given the weak macroeconomic factors and lower demand in France and Germany. A goal of these actions is to get the International segment back to profitability.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

News. Bit Digital released a flurry of news over the past two days, including a strategic shift in its business strategy, the potential IPO of its WhiteFiber subsidiary, and a $150 million equity offering. Needless to say, a lot to digest. If completed, the announced shifts would result in a significant change to Bit Digital.

Ethereum Focus. Operationally, Bit Digital will exit the bitcoin mining business and transition to become a pure-play Ethereum staking and treasury company. Given the economics of bitcoin mining versus Ethereum staking, we see the rationale in the move. The Company has commenced a strategic alternatives process for the Bitcoin mining operations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increase in the quarterly cash dividend. AZZ announced a 17.6% increase in the quarterly cash dividend to $0.20 per share, or $0.80 on an annualized basis, from $0.17 per share, or $0.68 on an annualized basis. The dividend is payable on July 31 to shareholders of record as of the close of business on July 10. In our view, the dividend increase reflects management’s confidence in the company’s near- and long-term outlook.

First Quarter FY 2026 financial results. AZZ will release its first quarter financial results after the market close on Wednesday, July 9. Management will host an investor conference call and webcast on Thursday, July 10, at 11:00 am ET. We look forward to an update regarding the company’s new aluminum coil coating facility in Washington, Missouri, that is ramping up production, along with a review of market fundamentals and the company’s capital allocation priorities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Demand for rare earth elements expected to grow. Demand for rare earth elements is expected to grow meaningfully through 2030 and beyond, driven by electric vehicles, wind turbines, grid upgrades, and advanced defense technologies. According to the IEA, global rare earth demand could double by 2050 under a net-zero scenario, underscoring the growing strategic relevance in the global energy transition.

China dominates the REE market. According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves, while accounting for most of the midstream and downstream capacity. While mining activity is gradually diversifying, the refining stage remains concentrated. This level of concentration poses a risk to both the U.S. supply chain and national security.

U.S. policymakers seek to reduce dependence on China. U.S. policymakers are increasingly focused on reducing dependence on China for rare earth elements, viewing it as a national security and industrial resilience issue. Recent actions include invoking the Defense Production Act, funding domestic processing projects, and expanding international partnerships through initiatives like the Minerals Security Partnership. Legislative efforts and strategic investments are aimed at reshoring supply chains and building alternative capacity in allied countries such as Canada and Australia.

Necessity is the mother of invention. While the Trump Administration is taking appropriate action and policy momentum is growing, the path to increasing rare earth supply chain independence is complex and will take time. Policymakers may need to work with allies, such as Canada, to promote a North American supply chain that encompasses all aspects of the REE value chain, including upstream, midstream, and downstream. In addition to supportive public policy, private industry will likely need financial support from governments to kick start the effort.

Metals and Mining Spotlight: Rare Earth Elements

Rare earth elements (REEs) are comprised of 15 elements in the lanthanum series, along with scandium and yttrium. While not lanthanides, scandium and yttrium are classified as rare earth elements because they occur within the same ore deposits and share similar chemical properties. While the actual elements may not be rare, it is often difficult to find them in sufficient concentrations for economic extraction, and they require extensive processing. Cerium, lanthanum, neodymium, praseodymium, and promethium are considered light rare earth elements. Europium, gadolinium, and samarium are often referred to as medium rare earth elements, while dysprosium, erbium, holmium, lutetium, terbium, thulium, and ytterbium are considered heavy rare earth elements. We do not classify scandium (Sc) or yttrium (Y) as light, medium, or heavy. Below is a table summarizing the elements and their symbols.

Figure 1: Rare Earth Elements and Atomic Number and Symbol

Source: Noble Capital Markets, Inc.

One of the many uses of rare earth elements is in the production of permanent magnets which are critical components in electric vehicles, wind turbines, and other communication and defense technologies. Neodymium and praseodymium are critical materials in the manufacturing of neodymium-iron-boron (NdFeB) magnets, which have among the highest magnetic strength among commercially available magnets and promote high energy density and efficiency in energy technologies. They are often referred to as NdPr magnets because they generally contain about one-third neodymium, of which some of that can be replaced by praseodymium. While REEs are used for a variety of applications, the highest value REEs are neodymium and praseodymium, which currently drive the value of mixed rare earth concentrates and precipitates. By economic value, neodymium-praseodymium (NdPr) is the largest segment of the REE market. NdPr is primarily used in neodymium-iron-boron (NdFeB) permanent magnets for electric machines, such as electric vehicle (EV) traction motors, wind power generators, drones, robotics, electronics, and other applications. Given the wide-ranging uses of these component materials in critical infrastructure essential for national security and economic growth, the U.S. government has taken an interest in industry concentration.

Figure 2: Rare Earth Applications

Source: National Energy Technology Laboratory

According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves. Conversely, the United States accounted for 12.2% of rare earth mineral production in 2023 and 1.6% of rare earth mineral reserves.

Figure 3: Rare Earth Metals Production and Reserves

Source: Energy Institute Statistical Review of World Energy 2024

Supply Chain and Pricing Overview

The supply chain for rare earths includes upstream, midstream, and downstream components.

Figure 4: Rare Earth Element Supply Chain

Source: Critical Materials Rare Earths Supply Chain: A Situational White Paper, U.S. Department of Energy, Office of Energy Efficiency & Renewable Energy, April 2020

As illustrated in Figure 4, concentration or beneficiation is an extractive metallurgy process that upgrades the value of mineral ores that contain raw REEs by removing low value minerals and resulting in a higher-grade product such as rare-earth concentrate.

Separation is the process of separating individual REEs from one another in the rare earth oxide (REO) concentrates. Separation of REEs is chemically intensive because the REEs are chemically similar. Processing refers to the conversion of REOs to rare earth metals, such as neodymium metal which can then be used to form alloys. China controls most of the midstream separating and processing capacity.

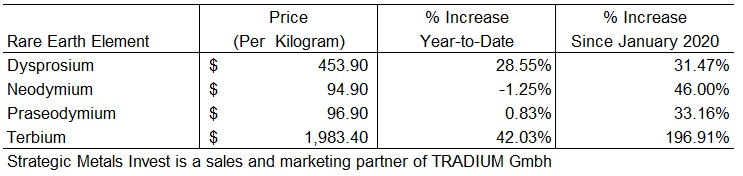

There is no single price for REEs collectively, but numerous prices for REE oxides and compounds individually. Pricing information for rare earths is opaque and generally available by paid subscription. Public information is generally not comprehensive and generally does not provide detailed information as to quality and origin, which makes comparisons difficult. Below we have provided a pricing sample of the most valuable elements as of June 11, 2025.

Figure 5: Pricing Data for Select Rare Earth Elements (REE)

Source: Strategic Metals Invest

U.S. Rare Earth Element Market

According to the U.S. Department of the Interior, the estimated value of rare-earth compounds and metals imported by the United States in 2023 was $190 million, down 7% from $208 million in 2022. Catalysts represented the leading domestic end use for rare earths, followed by applications in ceramics and glass, metallurgical alloys, polishing, and embedded permanent magnets in finished goods. While rare earth recycling is expected to grow in the coming years, current recovery rates from sources such as batteries and permanent magnets remain limited. The table below provides some statistics associated with the rare earths market in the United States.

Figure 6: United States REE Market Statistics

Source: Mineral Commodity Summaries 2024, U.S. Department of the Interior, U.S. Geological Survey

Given the United States’ reliance on imports, we think Canadian producers stand to benefit from a shift away from sources in China. As processing capabilities are developed, the U.S. could be an important destination for Canada sourced materials.

Key REE Market Participants

The global rare earth industry remains defined by a limited number of dominant players, most of which are concentrated in China. China Northern Rare Earth Group (SHH: 600111), and China Minmetals are the largest vertically integrated producers, with strong government alignment and control over both upstream mining and midstream separation capacity. These firms benefit from large-scale infrastructure, domestic demand, and preferential access to processing technology that remains restricted from foreign use.

Outside China, Lynas Rare Earths (ASX: LYC, OTC: LYSDY), in Australia is the largest fully integrated producer, with upstream operations at Mount Weld and a separation plant in Malaysia. Lynas is expanding into heavy rare earth processing in Texas through a strategic partnership with the U.S. Department of Defense.

MP Materials, the most significant rare earth materials producer in the United States, completed a business combination with Fortress Value Acquisition Corp., a special purpose acquisition company and began trading on the New York Stock Exchange on November 18, 2020, under the ticker MP. MP Materials owns and operates the Mountain Pass rare earth mine and processing facility in California which opened in 1952 as a uranium producer, pivoted to one of the largest suppliers of rare earth minerals, but closed in 2002 as environmental restrictions and imports made it difficult to compete. The facility underwent various ownership changes and reopened in 2017 under MP Materials’ ownership. It is North America’s only active and scaled rare earth production site and now has a market capitalization of $4.1 billion as of June 11, 2025.

The Mountain Pass mine in California and is the only active rare-earth mine in the United States. The company has restarted oxide production and is building refining and alloying capacity in Texas. MP has signed multi-year offtake agreements with original equipment manufacturers (OEMs), including General Motors, aimed at creating a vertically integrated domestic supply chain. However, the company still relies on China to assist in the separation process for some of its output, underscoring the current U.S. capabilities gap.

Additional participants working to expand non-Chinese supply chains include Iluka Resources (ASX: ILU, OTC: ILKAF) and Arafura Rare Earths (ASX: ARU, OTC: ARAFF), both based in Australia. Iluka is building a new facility with support from the Australian government, aimed at handling all stages of rare earth production. Arafura is also developing a new project with backing from international lenders, focused on supplying materials used in magnets for electric motors and other technologies. On the downstream side, magnet production is dominated by firms such as Shin-Etsu (TSE: 4063, OTC: SHECY), Hitachi Metals, and JL MAG (SZSC: 300748, OTC: JMREY), with capacity heavily skewed toward Asia. Efforts among U.S. and allied countries to establish domestic magnet manufacturing are progressing but remain in the early stages.

China dominates the production of many critical minerals, including rare earth elements. There appears to be an awakening among U.S. policy makers of the dangers of dependence on foreign sources for critical minerals, especially those that are adversarial to the United States. We believe a shift is underway to source REEs from countries that are friendly to the United States, including Canada. As part of its strategy to ensure secure and reliable supplies of critical minerals, the U.S. Department of the Interior identified 35 critical minerals, including the rare earth elements group. The U.S. Government is planning to fund rare earths projects to reduce reliance on China. In January 2022, bipartisan legislation was introduced, the Restoring Essential Energy and Security Holdings Onshore for Rare Earths Act, to protect the U.S. from the threat of rare-earth element supply disruptions, encourage domestic production, and reduce reliance on China. REEs are found in mineral deposits such as bastnaesite and monazite, the two largest sources of REEs. Bastnaesite, a carbonate-fluoride mineral, typically contains cerium, lanthanum, neodymium, and praseodymium. Monazite, a phosphate mineral, typically contains cerium, lanthanum, neodymium, and samarium. Rare earths are mined domestically in the United States. Bastnaesite is extracted at the mine in Mountain Pass, California.

Since January 2025, the Trump administration has significantly expanded its strategic focus on rare earth supply chain security. In April, an executive order initiated an investigation into whether U.S. dependence on foreign sources of rare earths constitutes a national security threat. An additional order opened up new offshore exploration zones for critical minerals, including seabed areas believed to contain rare earth and battery metals.

Furthermore, the administration has invoked the Defense Production Act to allocate capital and permit support to midstream and downstream segments of the rare earth supply chain. MP Materials began producing rare earth metals at its Texas facility, while Lynas advanced its U.S. processing plant with support from the Department of Defense. These efforts are part of a broader strategy to rebuild U.S. capabilities across the rare earth value chain.

International partnerships have also gained momentum. The U.S. is advancing cooperation with Australia, Canada, and Ukraine to secure alternative sources of supply and coordinate project financing through the Minerals Security Partnership. A bilateral agreement with Ukraine is expected to facilitate exploration and development of new deposits, while Australia remains a primary ally for both upstream mining and technical collaboration.

Outlook

The rare earth industry is entering a period of strong growth and growing strategic relevance. According to the International Energy Agency (IEA), magnet-grade rare earth demand could double by 2050, and mining projects could rise by 52% by 2040, under current policy (IEA, Critical Minerals Report, 2024). These forecasts are driven by growth in electric vehicle drivetrains, offshore wind development, and precision defense systems, all of which rely heavily on rare earth magnets for performance, efficiency, and miniaturization. As a result, rare earths have transitioned from niche industrial inputs to core strategic resources.

Figure 7: REE Demand Outlook and Mining Requirements (kt REE)

Source: Global Critical Minerals Outlook 2024, International Energy Agency (IEA)

We note that the IEA’s forecasts are based on three scenarios. These include: 1) the Stated Policies Scenario (STEPS), 2) the Announced Pledges Scenario (APS), and 3) the Net Zero Emissions by 2050 Scenario (NZE). The Stated Policies Scenario is based on current policy settings. The Announced Pledges Scenario assumes that governments will meet all climate-related commitments they have announced, including net zero emissions targets. The Net Zero Emissions by 2050 Scenario represents a pathway for the global energy sector to achieve net zero carbon dioxide emissions by 2050. These are summarized, of course, and readers may consult the IEA’s report for a more detailed description.

In the short term, challenges will continue to shape how supply chains evolve outside of China. Most new projects in Western countries face long approval timelines due to environmental reviews, local opposition, and infrastructure gaps. While government funding and procurement support are improving, the limited availability of midstream processing remains a key constraint.

In our view, rare earths are evolving from niche industrial inputs to foundational resources for advanced economies. Although the industry currently operates at a scale that lags its growing strategic importance, recent policy momentum and expanded investment across allied nations are setting the stage for meaningful transformation. Looking ahead, we expect a more balanced and resilient global supply chain to emerge—anchored by deepening cooperation between the United States, Canada, Australia, and European partners. While China will remain a major player in the near term, the diversification of supply chains is gaining traction, signaling a shift toward greater self-sufficiency and long-term security among like-minded nations.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest

Watch the replays from the Noble Capital Markets Emerging Growth Virtual Equity Conference. Replays are available to Channelchek registered members. Registration is free and easy. Simply click the Join button in the upper right to get started.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Industry dynamics. The QVC Group recently announced that it is laying off 900 employees as part of its effort to become a live social shopping company. Notably, while we don’t anticipate QVC will stop live selling on traditional TV, the increased focus on social commerce is illustrative of changing consumer viewing habits. In our view, XCEL Brands is well positioned to benefit from shift in viewing habits toward streaming alternatives.

Valuable expertise. XCEL Brands is a veteran in the live selling space and has extensive experience working with celebrities to help bring their products to market and help them sell. In our view, the company is well positioned to provide celebrities with expertise both in traditional TV and social commerce selling, or live streaming.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Noble Capital Markets’ Emerging Growth Virtual Equity Conference – June 3-4, 2026

Set to be an immersive experience, bringing together investors, industry leaders, and experts from middle market public companies across all sectors. Featuring:

Corporate presentations with Fireside-style Q&A session proctored by Noble’s analysts and bankers

Scheduled 1×1 meetings with qualified investors

Up to 50 presenting companies, representing a wide array of sectors.

Noble’s investor base extends beyond traditional institutions to include family offices, money managers, and high-net-worth individuals who actively engage in smaller cap, open market transactions.

Noble’s investors crave the undervalued investment idea.

And not just investors that attend the live event. Channelchek will host replays of the corporate presentations and Q&A sessions right here, for all investors to view, free of charge, for the rest of the year.

Participation in conferences, both in-person and virtually, has proven to help in boosting awareness and liquidity. And Noble’s service offerings extend well beyond the conference circuit; our events are an extension of the year-round investor access we provide.

Ready to Register to Present? Click the link below:

Key Points: – Alumis and ACELYRIN have agreed to an all-stock merger, creating a well-capitalized biopharmaceutical company focused on advancing immunology treatments. – The combined company will have approximately $737 million in cash and securities, supporting multiple clinical trial readouts and operations into 2027. – Alumis will retain its name and leadership team, with an expanded board including two ACELYRIN members, and the merger is expected to close in Q2 2025.

Alumis Inc. (NASDAQ: ALMS) and ACELYRIN (NASDAQ: SLRN) have announced a definitive merger agreement, combining the two clinical-stage biopharmaceutical companies in an all-stock transaction aimed at advancing immunology treatments and optimizing clinical outcomes.

Strategic Rationale and Financial Position

The merger will create a strongly capitalized company with a combined cash, cash equivalents, and marketable securities position of approximately $737 million as of year-end 2024. This financial strength is expected to support the advancement of the companies’ combined pipeline through multiple key clinical data readouts and fund operating expenses and capital expenditures into 2027.

The combined company will leverage its track record in research and development and a proprietary data and analytics platform to drive innovation in immune-mediated diseases.

Martin Babler, President, CEO, and Chairman of Alumis, stated: “Through this combination with ACELYRIN, Alumis will have the financial flexibility and runway to advance an expanded late-stage pipeline, now including lonigutamab, and build commercial capabilities. Since completing our IPO, Alumis has operated with speed and rigor, and the multiple development milestones expected in 2025 and 2026, coupled with potential additional indications for ESK-001, represent exciting breakthroughs for our patients and value-driving opportunities for the combined company’s stockholders. As we move forward together, we will maintain financial discipline and a flexible capital allocation strategy with the goal of maximizing the value of our highly differentiated portfolio.”

Pipeline Highlights

Alumis’ ESK-001: A next-generation, allosteric TYK2 inhibitor, currently in Phase 3 ONWARD trials for moderate-to-severe plaque psoriasis (PsO) and Phase 2b LUMUS trials for systemic lupus erythematosus (SLE). Key Phase 2 52-week updates expected in 2025, with Phase 3 topline data in H1 2026.

Alumis’ A-005: A CNS-penetrant allosteric TYK2 inhibitor, targeting neuroinflammatory and neurodegenerative diseases like multiple sclerosis (MS) and Parkinson’s Disease. A Phase 2 trial is set to begin in H2 2025.

ACELYRIN’s Lonigutamab: A subcutaneous anti-IGF-1R therapy with best-in-class potential for thyroid eye disease (TED), currently under Phase 2 evaluation.

Transaction Terms & Leadership Structure

Exchange Ratio: ACELYRIN stockholders will receive 0.4274 shares of Alumis common stock for each ACELYRIN share owned.

Leadership: The combined company will operate under the Alumis name and be led by Alumis’ executive team, strengthened by key ACELYRIN professionals and medical experts.

Board Expansion: The board will grow to nine members, including two from ACELYRIN.

Closing Timeline: The transaction is expected to close in Q2 2025, subject to regulatory and shareholder approvals.

This merger brings together two companies dedicated to transforming immunology treatments, strengthening their pipeline, and delivering long-term value to patients and investors alike.

Key Points: – January job growth slowed to 143,000, falling below expectations and marking a sharp decline from December’s revised 307,000 gain. – Wage growth increased by 4.1% over the past year, outpacing inflation but continuing to pose affordability challenges for consumers. – The Federal Reserve and markets are closely monitoring labor trends, while rising trade policy uncertainty and potential economic shifts under President Trump add to financial volatility.

The U.S. labor market saw weaker-than-expected job growth in January, with nonfarm payrolls increasing by 143,000, below the Dow Jones forecast of 169,000 and down from a revised 307,000 in December. Meanwhile, the unemployment rate declined to 4.0%, showing continued resilience in the job market despite the slowdown in hiring.

Key Takeaways from the January Jobs Report

Weaker Job Growth: January’s 143,000 job gain marks a sharp decline from December and falls below expectations.

Downward Revisions: Total payroll numbers for 2024 were revised downward by 589,000 over the trailing 12-month period ending in March 2024.

Sector Performance:

Healthcare: +44,000 jobs

Retail: +34,000 jobs

Government: +32,000 jobs

Labor Force Participation: Increased 0.1% from December to 62.6%.

2024 Job Growth Trend: The monthly average for job growth in 2024 stood at 166,000 per month.

Wage Growth: Average hourly earnings rose 4.1% over the past year, partly due to minimum wage hikes in parts of the country.

Affordability Challenges: Wage growth continues to outpace recent inflation rates, but many consumers still face affordability challenges.

Market and Federal Reserve Reactions

Markets showed little reaction to the report in early trading, as investors had largely anticipated a slowdown in job creation. Federal Reserve officials are closely monitoring labor market data as they consider future monetary policy moves. The Fed cut its benchmark interest rate by a full percentage point in late 2024, and today’s report may influence their next steps regarding interest rate adjustments. President Trump recently stated that the Fed’s decision last week to hold rates steady was well-advised, despite previously criticizing the move.

Broader Economic and Political Context

Some indicators, such as hiring rates, suggest slower movement in the job market. Meanwhile, business executives remain optimistic that Trump’s policies—such as tax cuts and deregulation—will boost economic growth. However, Trump’s recent tariff decisions have rattled markets, adding to economic uncertainty. Rising trade policy uncertainty could further heighten financial market volatility in the coming months.

The Historical Importance of Jobs Reports

The monthly jobs report is one of the most closely watched economic indicators, providing insights into labor market health, consumer spending power, and broader economic momentum. Historically, strong job growth has been associated with economic expansion, while sluggish reports can indicate slowdowns or even recessions. Policymakers, investors, and businesses use these reports to make critical decisions on interest rates, hiring strategies, and economic forecasts. In the current environment, sustained job growth and wage pressures suggest a resilient labor market, even as broader economic uncertainties loom.

With job growth slowing but unemployment remaining stable, policymakers will weigh the need for further economic stimulus against concerns of overheating the labor market. The upcoming months will be crucial in determining whether this slowdown is temporary or indicative of a broader labor market trend.

Key Points: – TPG Rise Climate will acquire Altus Power for $5.00 per share in a $2.2 billion deal, taking the company private to accelerate clean energy expansion. – Altus Power’s Board of Directors unanimously approved the transaction, which represents a 66% premium to its October 2024 stock price and is expected to close in Q2 2025. – This acquisition aligns with TPG Rise Climate’s strategy to scale climate solutions, leveraging its expertise in clean energy infrastructure to support Altus Power’s growth.

Altus Power, the largest owner of commercial-scale solar in the U.S., has announced that it has entered into a definitive agreement to be acquired by TPG through its TPG Rise Climate Transition Infrastructure strategy. Under the terms of the agreement, TPG will acquire Altus at $5.00 per share, valuing the company at approximately $2.2 billion, including outstanding debt. Upon completion of the transaction, Altus Power will become a privately held company.

Strategic Rationale and Market Impact

On October 15, 2024, Altus Power initiated a formal review of strategic alternatives. Today’s purchase price represents a 66% premium to Altus’ closing price on that date. The company expects this acquisition to bolster its ability to provide greater value to both commercial and Community Solar customers while expanding access to clean electric power.

“This transaction represents a pivotal moment for Altus Power,” said Gregg Felton, CEO of Altus Power. “We are incredibly excited to partner with TPG Rise Climate to continue to build our position as the leading commercial-scale provider of clean electric power to businesses and households from coast to coast. TPG Rise Climate’s deep expertise in the clean energy sector, investment-oriented mindset, and value-driven approach to infrastructure development align perfectly with our vision. This partnership strengthens our ability to serve both our Community Solar and commercial clients with clean electric power at a time when demand for power is expected to grow substantially. As a private company, Altus Power will be better positioned for continued long-term growth, which we believe will allow us to scale our operations, drive innovation, and enhance the value we deliver to our customers. Together with TPG Rise Climate, we believe we are poised to accelerate clean energy adoption and ensure more businesses and communities have access to the power they need for a sustainable future.”

Transaction Details

The Board of Directors of Altus has unanimously approved the transaction and recommends that Altus stockholders vote to adopt the merger agreement.

The deal is contingent upon majority approval by Class A stockholders.

The transaction is expected to close in Q2 2025.

About TPG Rise Climate

TPG Rise Climate is the dedicated climate investing platform of TPG, a leading global alternative asset management firm. With dedicated pools of capital across private equity, transition infrastructure, and the Global South, TPG Rise Climate focuses on climate-related investments that benefit from the expertise of TPG’s investment professionals and its global network of executives, advisors, and corporate partners. As part of TPG’s $25 billion global impact investing platform, TPG Rise Climate invests broadly in the climate sector, emphasizing clean electrons, clean molecules and materials, and negative emissions.

About Altus Power

Altus Power is a leader in commercial-scale solar energy, providing clean, renewable energy solutions for businesses and communities across the U.S. The company is currently traded on the New York Stock Exchange under the ticker symbol AMPS.

Key Points: – Above Food Ingredients Inc. (NASDAQ: ABVE) has signed a Letter of Intent to acquire Palm Global Technologies Ltd. in a $180 million share exchange, expanding into Agri-Tech, FinTech, and carbon credit securitization. – Palm Global’s proprietary AI, blockchain, and decentralized finance technologies will enhance Above Food’s vertically integrated food systems, supporting sustainable agriculture and economic empowerment for millions of farmers. – Following the acquisition, Palm Global’s Peter Knez will become Chairman and CEO of the combined companies, with definitive agreements expected to be finalized and closed in the near term.

Above Food Ingredients Inc. (NASDAQ: ABVE), a leader in sustainable, vertically integrated food systems, has signed a Letter of Intent (LOI) to acquire Palm Global Technologies Ltd., a next-generation innovator in technology, sustainability, and global food markets. The acquisition is expected to strengthen Above Food’s position in Agri-Tech, FinTech, and carbon credit securitization, further advancing its commitment to sustainable food production and innovation.

Strategic Rationale and Industry Impact

The transaction will integrate Above Food’s vertically integrated food systems with Palm Global’s groundbreaking technologies, alliances, and global reach. Palm Global’s proprietary AI, blockchain, and decentralized finance technologies are designed to drive economic empowerment, education, and sustainable growth, particularly in underserved markets, benefiting tens of millions of farmers worldwide.

“This transformative acquisition positions Above Food to redefine global agriculture and sustainability while unlocking a number of significant opportunities in high-growth markets,” said Lionel Kambeitz, Founder and CEO of Above Food. “Palm Global’s innovative technologies, combined with its mission to drive economic empowerment, align perfectly with our vision for sustainable food solutions worldwide.”

Palm Global’s Technological and Strategic Contributions

AI, Blockchain, and DeFi Technologies – Palm Global’s solutions enhance efficiency, security, and accessibility in the global food supply chain.

Partnerships with Governments and Institutions – Palm Global collaborates with entities like the Peace for Life Foundation, IIMSAM, and global institutions to accelerate technology adoption among farmers.

Strategic Global Alliances – The acquisition allows Above Food to leverage Palm Global’s extensive partnerships to develop, utilize, and maximize R&D capabilities in agronomy and genomics.

The newly combined entity will enable innovative initiatives such as regenerative agriculture and grow-to-order food solutions, creating customized approaches to meet evolving consumer and agricultural needs.

Transaction Details and Leadership Transition

The LOI outlines a share exchange valuing Palm Global at approximately $180 million.

Definitive agreements are expected this month, with approvals and closing anticipated soon after.

Peter Knez, currently on Palm Global’s Board of Directors, will assume the role of Chairman and CEO of the combined companies.

Future Outlook

This merger is set to enhance global food security, promote sustainable agriculture, and create economic opportunities in underserved markets through technological innovation and strategic partnerships. By combining resources, Above Food and Palm Global aim to drive the next wave of transformation in sustainable food production and agricultural technology.