Ayala Pharmaceuticals, Inc. is a clinical-stage oncology company focused on developing and commercializing small molecule therapeutics for patients suffering from rare and aggressive cancers, primarily in genetically defined patient populations. Ayala’s approach is focused on predicating, identifying and addressing tumorigenic drivers of cancer through a combination of its bioinformatics platform and next-generation sequencing to deliver targeted therapies to underserved patient populations. The company has two product candidates under development, AL101 and AL102, targeting the aberrant activation of the Notch pathway with gamma secretase inhibitors to treat a variety of tumors including Adenoid Cystic Carcinoma, Triple Negative Breast Cancer (TNBC), T-cell Acute Lymphoblastic Leukemia (T-ALL), Desmoid Tumors and Multiple Myeloma (MM) (in collaboration with Novartis). AL101, has received Fast Track Designation and Orphan Drug Designation from the U.S. FDA and is currently in a Phase 2 clinical trial for patients with ACC (ACCURACY) bearing Notch activating mutations. AL102 is currently in a Pivotal Phase 2/3 clinical trials for patients with desmoid tumors (RINGSIDE) and is being evaluated in a Phase 1 clinical trial in combination with Novartis’ BMCA targeting agent, WVT078, in Patients with relapsed/refractory Multiple Myeloma. For more information, visit www.ayalapharma.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First AL012 RINGSIDE Data Presented At ESMO. Ayala presented first data the from the Phase 2/3 RINGSIDE trial testing AL102 in desmoid tumors, a rare tumor of the connective tissue. The data was from Part A, designed to test three dosing intervals for tolerability, safety, and select a dosing schedule for the double-blind, placebo-controlled Part B. Patients receiving drug at intervals of either 1.2 mg daily, 2 mg for 2 days then 5 days rest, or 4 mg for 2 days then 5 days rest. The 1.2mg daily dose was chosen for Part B.

The Stock Fell On The News. We attribute the stock price decline to the selection of the lower dose given daily rather than one of the higher doses given in cycles. The data from the daily dosing arm also had partial responses, rather than complete responses, although the effect improved over time. We point out that Part A was designed to determine tolerability and select the dose for Part B, and the upcoming Part B with 156 patients will determine efficacy and approvability.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Federal Reserve (the Fed) will be holding a two-day Federal Open Market Committee (FOMC) meeting next week that ends on September 21. After the FOMC meeting, it is the current practice for the Fed to announce what the target Fed Funds range will be. That is, make the public aware of what overnight bank loan rate the Federal Reserve will work to maintain through open market operations.

Open market operations is the Federal Reserve buying and selling securities on the open market. The purchases are restricted to debt or debt-backed securities so that interest rates are impacted. It’s through controlling interest rates that the Fed works to maintain a sound banking system, keep inflation under control, and help maximize employment. Purchasing securities through its account puts money into the economy, which lowers rates and helps stimulate economic activity. Selling securities takes cash out of circulation. This tightens money’s availability and can also be accomplished by letting the financial instrument mature and then not replacing them with an equal purchase.

Quantitative Easing

If the Federal Reserve hadn’t put money into the economy, they’d have nothing to sell or allow to mature (roll-off). With this in mind, the natural position of the Federal Reserve Bank is stimulative.

Currently, the Fed owns about a third of the U.S.Treasury and mortgage-backed-securities (MBS) that have been issued and are still outstanding. Much of these holdings are a result of its emergency asset-buying to prop up the U.S. economy during the Covid-19 efforts.

Two years of quantitative easing (QE) doubled the central bank’s holdings to $9 trillion. This amount approximates 40% of all the goods and services produced in the U.S. in a year (GDP). By putting so much money in the economy, the cost of the money went down (interest rates), and the excess money, without much of an increase in how many stocks, bonds, or houses there are, made it easier for people to bid prices up for investible assets. For non-investments, the combination of easy money while lockdowns slowed production became a recipe for inflation.

Inflation

Inflation is now a concern for the average household. The Fed, which is supposed to keep inflation slow and steady, needs to act, so they are changing the current mix. It is making these changes by taking out a key inflation ingredient, easy money. This same easy money has been a contributor to the ever-increasing market prices for stocks, bonds, and real estate.

The overnight lending rate the Fed is likely to alter next week is the policy that will create headlines. These headlines may cause kneejerk market reactions that are often short-lived. It is the extra trillions being methodically removed from the economy that will have a longer-term impact on markets. These don’t have much impact on overnight rates, their maturities average much longer, so they impact longer rates, and of course spendable and investible cash in circulation.

Quantitative Tightening

The central bank has only just started to shrink its holdings by letting no more than $30 billion of Treasuries and $17.5 billion of MBS, roll off (cash removed from circulation). They did this in July and again in August. The Fed then has plans to double the amount rolling off this month (most Treasuries mature on the 15th and month-end).

This pace is more aggressive than last time the Fed experimented with shrinking its balance sheet.

Will this lower the value of stocks, crash the economy, and make our homes worth the same as 2019? A lot depends on market expectations, which the Fed also helps control. If the markets, which knows the money that was quickly put in over two years, is now coming back out at a measured pace, and trusts the Fed to not hit the brake pedal too hard, the means exist to succeed without being overly disruptive. If instead the forward-looking stock market believes it sees disaster, an outcome that feels like a disaster increases in likelihood. For bonds, if the Fed does it correctly, rates will rise, which makes bonds cheaper. You’d rather not hold a bond that has gotten cheaper for the same reason that you don’t want to hold a stock that has gotten cheaper. However, buying a cheaper bond means you earn a higher interest rate. This is attractive to conservative investors but also serves as an improved alternative for those deciding to invest in stocks or bonds.

Houses are regional, don’t trade on an exchange and unlike securities, are each unique. They are often purchased with a long-term mortgage. Higher interest rates increase payment costs on the same amount of principal. In order to keep those payments affordable, home purchasers may demand a lower price, thereby causing real estate values to decline.

Take Away

The Fed has told us to expect tightening. They were honest when they promised to ease more than two years ago; there is no reason not to plan for higher rates and tighter money. The overnight rate increases get most of the attention. Further, out on the yield curve, the way quantitative tightening plays out depends on trust in the Fed and a lot of currently unknowns.

The Reasons Biotech is Gaining Ground on the Field

Similar to their watching a horse race, with a sense that their horse is starting to come from behind and may even be moving toward the front of the pack, biotech investors are leaning over the rail, watching their sector’s increased pace. This week biotechs, as measured by the ETF $XBI, crossed above its 200-day moving average – only last week the biotech sector’s momentum took it above its 50-day moving average. Does this technical indicator demonstrate the growing strength will continue, or does this indicate that it may be approaching overbought?

Technical analysis is not usually clear on this; below, we look for clues in the sector’s fundamentals to better handicap its chances.

In 2021, the overall healthcare sector experienced record merger and acquisition activity. The first half of 2022 also had significant activity; however, at $92.4 billion in value and 481 deals announced, the pace of activity was down 51% from the same period in 2021. This may feel slow but is well ahead of the pre-pandemic pace for these companies. For example, it’s a 37% increase from the first half of 2020. This could be seen as fundamentally positive for a sector that is trading below its 2021 levels and even below the second half of 2020.

One catalyst for this continued high pace of deals which may even help accelerate it, is that big pharmacies are flush with cash. This cash serves them best if invested in the next generation of medicine or valuable patent. Fortunately for big pharma, small and mid-sized biotech companies are more likely now to form financial partnerships, agree to merger arrangements, or be outright purchased in order to help with their need for cash to continue operations.

This dynamic is easy to understand; there is less money flowing into the smaller incubator-type companies than the big pharmaceutical companies that have had money pouring in from generous pandemic-related government contracts. These small companies, many working on what may be life-changing science, rarely have sizeable sales. Sales and revenue come after the final phase of testing, FDA approval, and marketing. A small biotech company that sees its research and development possibly making a difference a few years from now, but is currently burning through capital at a pace where it may only last another 12 months, might welcome partnership or acquisition talks with a cash-rich suitor.

News of any injection of cash or capital in these smaller biotechs is usually an event that pushes the price up by percentage points in a short period of time. A full buyout can do much more.

XBI provides exposure to US biotech stocks, as defined by GICS, from a universe that invests across the market-cap spectrum. The fund equal-weights its portfolio, which in turn emphasizes small- and micro-caps and greatly reduces single-name risk. Thus, the weighted-average market-cap is much smaller than some competitors. Unlike other funds in this segment, XBI is a pure biotech play, with relatively small pharma overlap. The index is rebalanced quarterly. – FactSet

Put yourself in the position of big pharma in 2022 into 2023. Your firm may now be sitting on a huge war chest thanks to the pandemic. This is now being eroded by high inflation. Management’s role is to use resources to provide value to shareholders. In the meantime, biotech is well-priced and motivated to talk.

And then the clock is always ticking on patent cliffs for big pharma. They may be very amenable to shop for acquisition targets as they look out at the expiration of patent rights and the exclusive protection those patents provide. Analysts estimate the top-ten pharmaceutical manufacturers have more than 46 percent of their revenues at risk between 2022 and 2030. Behemoths like Bristol Myers Squibb, Pfizer and Merck will be among the most exposed over the next decade.

Take Away

Watching a thoroughbred that was lagging behind the pack find an opening and begin to gain ground on those around it is exciting. When you have money on the horse, it’s even more enjoyable. The performance of the biotech sector was far behind other industries for much of this year. Moving into fall it has been outperforming its own average and many other investment areas.

There are fundamentals in play that could keep this strength going. What’s more is that these factors have little to do with the overall market, which many now fear

This challenge may catalyze M&A in the industry as large firms look to recoup lost revenue streams and invest in patents.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Cocrystal Has Reported Progress In Its Influenza Program. Cocrystal has reported Phase 1 data and plans for a Phase 2a trial for CC-42344, its oral drug for seasonal and pandemic influenza. The drug is an inhibitor of the enzyme PB2 (polymerase basic 2), a subunit of the RNA polymerase required for the replication cycle of the virus. This early point of action could make it effective against all strains of influenza.

Phase 1 Data Confirmed Once-Daily Dosing. In July 2022, Cocrystal announced pharmacokinetic data from its Phase 1 trial. The single ascending-dose stage met its goals, confirming administration on a once-daily basis. Patient enrollment continues in the multiple ascending dose portion. The company plans to present the study data at a medical meeting later in the year.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Non-deal roadshow highlights. Last week, Direct Digital President, Keith Smith, and CFO, Susan Echard hosted meetings for investors in St. louis. This report highlights some of the key takeaways from the roadshow.

Re-iterated guidance. Management noted that the company remains on track to reach its upwardly revised full year 2022 revenue target of$70-$75 million. We are forecasting revenue of $70 million and adj. EBITDA of $8.4 million, for the full year.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

GABY Inc. is a California-focused retail consolidator and the owner of Mankind Dispensary, one of the oldest licensed dispensaries in California. Mankind is a well-known, and highly respected dispensary with deep roots in the California cannabis community operating in San Diego, California. GABY curates and sells a diverse portfolio of products, including its own proprietary brands, Lulu’s™ and Kind Republic™ through Mankind, manufactures Kind Republic, and distributes all its proprietary brands through its wholly owned subsidiary, GABY Manufacturing. A pioneer in the industry with a multi-vertical retail foundation, and a strong management team with experience in retail, consolidation, and cannabis, GABY is poised to grow its retail operations both organically and through acquisition.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q22 Revenue. Note: GABY switched to the U.S. dollar for reporting purposes this quarter from the Canadian dollar previously. All figures are now in U.S. $, unless noted. Reported second quarter revenue fell 44% to $5.2 million, from $9.2 million reported last year, although adjusted for the closure of the wholesale distribution business, revenue was down 26%. On a sequential basis, revenue declined 10.4%. A still difficult operating environment due to lower pricing and reduced demand, combined with increased competition, impacted results.

But GM Held. In spite of the decline in revenue, gross margin was stable. 2Q22 GM was 43.2% versus 44.4% sequentially and 35.0% in the year ago period. Higher sales of proprietary products, control over supplier costs, and overall cost controls contributed to the stable GM. GABY reported a net loss of $3.0 million, or breakeven EPS for the quarter, compared to a net loss of $1.3 million, or breakeven EPS, in 2Q21.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

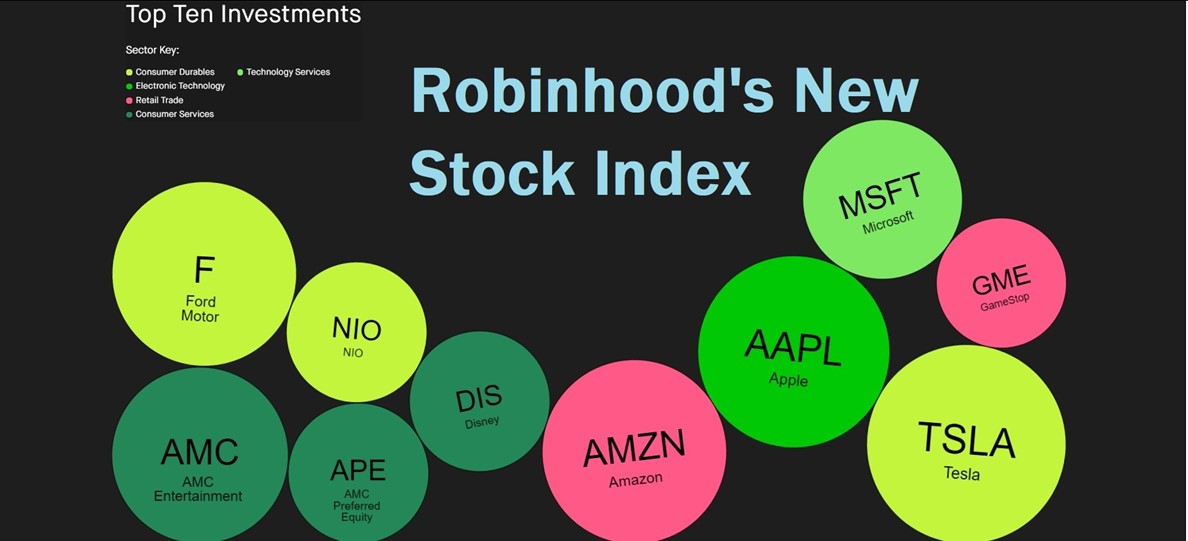

Robinhood’s Latest Step Could Increase the Influence of its Customers

Robinhood made an exciting announcement at the close of business last week that went largely unnoticed. It is creating an index consisting of the most held stocks by its customers. For Robinhood ($HOOD) users and everyone else, this unique index will be useful intelligence to help serve as a barometer as to what top stocks users of the brokerage app are adding and which they are paring down. The Robinhood Investor Index will be based on the top 100 most owned stocks and is unique in how it is configured and weighted.

About the Index

The Robinhood Investor Index presents an aggregate view of its customers’ top 100 most owned investments (does not account for shorts) and tracks the performance of those investments. Unlike the S&P 500 or Nasdaq 100, the index isn’t weighted by the size of the company but instead by the “conviction” of the 20+ million investors using the app.

Robinhood will take a monthly snapshot of holdings of each ticker and look at the percentage each comprises of each customer portfolio. They’ll ensure that all customers are equally included by averaging the conviction for each investment across all customers. In this way, whether clients have $500 or $500,000 in their account, it is the weighting per account percentage, not shares or dollar value.

Robinhood plans to update the index once a month and will share the valuable insights reflecting where its customers are allocating their assets in the index. Robinhood says its data tells them that customers invest in the companies they’re passionate about, and the Robinhood Investor Index aims to make this known.

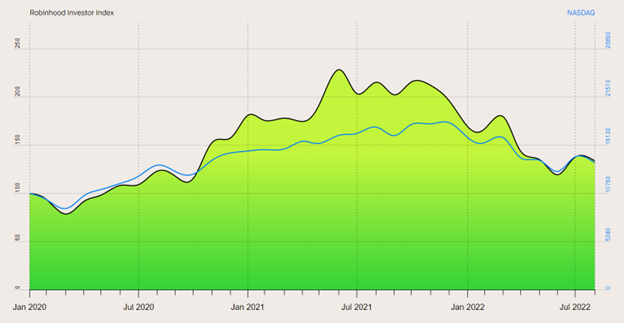

The index weights are re-calculated at the beginning of each new month, using data from the last trading day of the previous month. These monthly updates are expected to be published on a dedicated site within five trading days after the first trading day of each month. The index inception date for performance measurement is January 2020.

Performance

Robinhood says its customers tend to invest in what they know, entertainment, technology, and non-obscure staples in most of their lives.

For comparison, below is a look back to the beginning of 2020 (index inception date) comparing the Nasdaq 100 (NDX) in blue to the Robinhood Investor Index (RII) in green. Robinhood has shared that the evolution of its customer’s portfolios have shown an increased conviction to growth in electric vehicles with Tesla at the top, and growth in Ford and NIO, which has moved these holdings up the ranking system. Entertainment is also well represented, with Disney and AMC consistently among the top stocks. The sector representation, is diversified, also spanning financial services, energy and healthcare.

Overall, the RII leans towards large cap stocks with 75% in large-cap, 16% in midcap and 9% in small-cap.

The Nasdaq Composite Index is a market capitalization-weighted index of more than 3,600 stocks listed on the Nasdaq stock exchange. The index is constructed on a modified capitalization methodology. This modified method uses individual weights of included companies according to their market capitalization. Similar methods are used for other often quoted market indices. The holdings captured in the Robinhood index are directly invested in by its users and weighted in the proportion weighted in each of the user accounts.

The sectors are defined using the FactSet Revere Business and Industry Classification System (RBICS). Sectors may be excluded if they are not among the holdings with the highest conviction.

Market capitalization evaluation is broken into three categories, large-cap (greater than $10 billion), midcap (between $2 and $10 billion), and small-cap (between $300 million and $2 billion). The RII does not include securities considered microcap (below $300 million).

Take Away

This new index could be of interest to financial professionals and other traders that monitor the activities of retail investors as a factor behind stock-market moves. The average age of Robinhood account holders is 32, this demographic has become an increasingly powerful driver of movement and it will be worth monitoring its trends.

Channelchek reports on index changes that we believe impact our readers. The Robinhood Investor Index, now in its infancy, will certainly be reported on in its early stages.

Sign-up for Channelchek news and research free to your inbox each day.

The Ethereum Merge Could Kick Off a Transformation in Crypto’s Battered Reputation

Cryptocurrencies might still be a very long way from their highs of 2021, but some of the major ones have staged some decent recoveries in the past couple of months. Notably ether (ETH), the second largest cryptocurrency after bitcoin, is trading at almost $US1,700 (£1,463) at the time of writing, having dropped as low as $US876 in mid-June.

Ether, which was created by Canadian/Russian programmer Vitalik Buterin, is the cryptocurrency used for transactions on Ethereum, the leading platform on which developers can applications using blockchain technology.

Blockchains are online ledgers that run without been controlled by any single company. Much of these applications revolve around smart contracts, which are automated contracts that remove the need for intermediaries such as lawyers and are seen as having huge potential for the future.

One of the main catalysts for ether’s rebound has been the Ethereum merge, a huge project to change the way the underlying blockchain operates. Where transactions on Ethereum are currently validated using an energy-intensive system known as proof-of-work (PoW), in which lots of very powerful computers compete to solve complex mathematical puzzles, from around September 15 it will shift to a new system known as proof of stake (PoS).

PoS basically means that transactions on the blockchain will be validated not by all these computations but by a network of investors whose commitment is demonstrated by the fact that they own at least 32 ether (yours for about $US54,000).

The idea is that this gives them an economic incentive to enhance the security of the network, and are therefore very unlikely to try and sabotage it. Whereas bitcoin transactions all depend on PoW, lots of newer cryptocurrencies use PoS, including Ethereum rivals such as Solana and Cardano.

Going Green

When the Ethereum merge takes place, power consumption on the blockchain will be reduced by 99%. Since it is currently the most used blockchain in terms of transactions, this will save a huge amount of electricity each year, corresponding to Chile’s power consumption.

As a result of the merge, some analysts expect ether to overtake bitcoin as the leading crypto in terms of the total value of all the coins (in crypto circles this is referred to as the “flippening”). Ether is currently worth just over US$204 billion, while bitcoin is worth US$396 billion.

Until now, cryptocurrencies and bitcoin in particular have suffered from a bad reputation. Bitcoin was initially conceived with the egalitarian goal of allowing investors access to a financial system with no need for banks and with money that isn’t controlled by countries. It has been championed for its ability to enable billions of people without bank accounts to transact online, and to facilitate things like microfinance and ultra-cheap cross-border trading.

Yet bitcoin has come to be associated with environmental degradation and criminal activities. The mainstream media has endlessly linked the leading cryptocurrency – and by extension the whole space – with money laundering, online drug dealing, Ponzi schemes and exchange hacking.

Netflix documentaries have further reinforced this negative public image. Recent scandals in the crypto world, such as the fall of Ethereum rival Luna and the bankruptcy of Celsius and other crypto lenders, have not helped either.

One major consequence has been that major financial institutions like investment banks and pension funds have been cautious of ploughing money into this space, despite the leap forward in technology that blockchains represent.

But if the most widely adopted crypto platform successfully shifts to PoW in the coming days, many believe that this will overcome the biggest institutional objection and see much more money flowing into the space (there are already early signs, such as Fidelity’s new crypto fund for retail investors). This is likely to accelerate the global regulatory framework that would minimise undesirable activities.

By closing down the environmental objections to crypto, other advantages to ether are likely to come to the fore. The merge will offer a return to investors in the form of rewards in exchange for locking up their money for a period of time (“staking”).

Although you need to stake 32 ether to become one of the network’s validators, numerous companies have set up systems to enable smaller investors to pool their money so that they can participate. For example, Binance, the world’s largest crypto exchange, offers investors 6% annual percentage yield for pooled staking on ether.

Staking will therefore create a win-win situation with guaranteed returns and a very liquid system that makes it easy for people to move their money in and out of ether. This will further enhance the appeal of ether and PoS cryptos in general.

This could help to accentuate other positives around crypto, another of which is humanitarian donations. When Russia invaded Ukraine, for instance, the Ukrainian government called for donations in bitcoin and ether to support its efforts against invaders. This quickly attracted substantial amounts of money.

Tonga was similarly successful with a campaign after its volcanic eruption earlier this year. By being able to cross borders easily and cheaply, cryptocurrencies are the ideal vehicle for international donations.

Lingering Uncertainties

All that said, it is uncertain how the Ethereum blockchain will function after the merge in terms of transaction speeds and costs. One major problem with Ethereum in the past has been that transactions have been ludicrously expensive, sometimes running to thousands of US dollars at peak times in 2021.

The developers of the Ethereum Foundation do not expect the merge to make a big difference in these respects (currently “gas” fees are averaging between $US1 and $US4 per transaction depending on which platform you are using). Much more important is likely to be another shift in ethereum’s journey to “Ethereum 2.0” known as sharding, which is due to happen in 2023.

We will also have to wait and see how smooth the merge is. Synchronisation and update bugs could see problems such as validators disconnected from the blockchain. Negative stories like these could see investors staying away for fear of instability. But on the whole, while the merge will not be a miraculous event, it could help improve the image of cryptocurrencies and attract institutional and retail investors. At a time when sustainable investing is increasingly high priority, the ether merge and its attractive returns have the potential to put ether at the top of the list.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Jean-Philippe Serbera, Senior Lecturer in Banking And Financial Markets, Sheffield Hallam University.

September 11, a Retrospective Account of Investment Fallout and Recovery

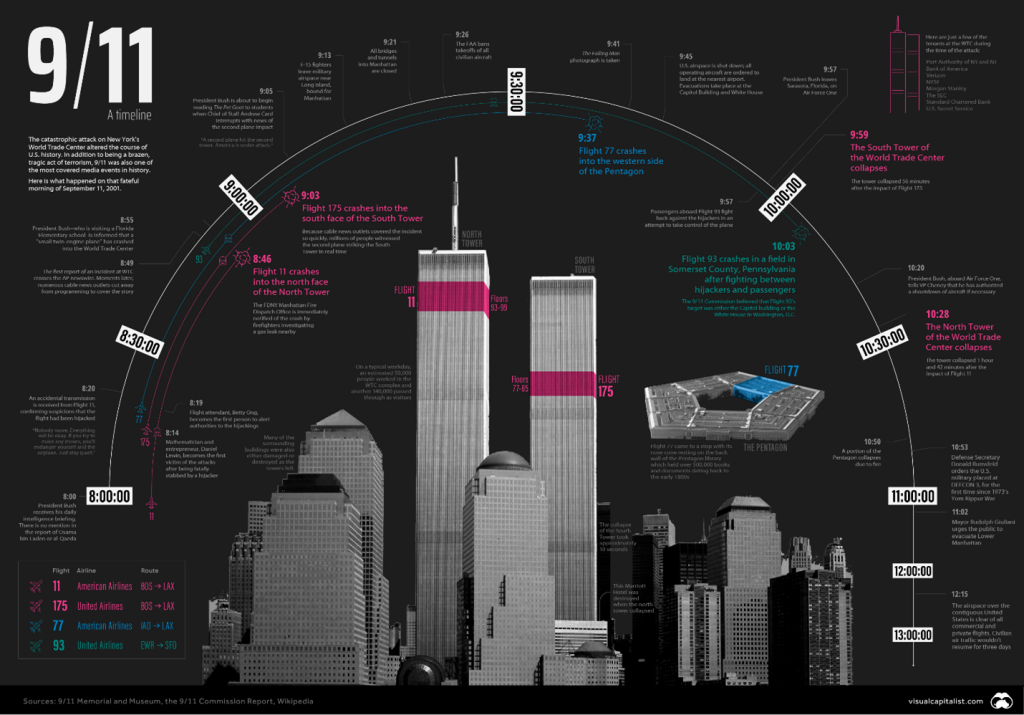

I wasn’t in New York City on September 11, 2001. Just prior to 911, I had taken a position as CIO for a major Wall Street firm headquartered in lower Manhattan; however, the trading floor I was responsible for was about 50 miles east of ground zero. I took the position outside NYC to be closer to my home and family – the benefit of my decision became apparent all at once, at 8:45 am that Tuesday morning, then reinforced 18 minutes later.

Twenty-one years have passed since then, the children of the deceased are now adults, and financial activity is spread much further than one small area in lower Manhattan. Although much has changed, it’s important to look back and recognize how the investment markets handle devastation and, at the same time, recognize how humans here and around the world will band together when others need help.

The opening bells at the New York Stock Exchange (NYSE) and Nasdaq were silent at 9:30 that morning. They remained silent until September 17, as traders and investors feared what their positions would be worth upon the reopening of the financial markets after the longest close on record.

Once reopened, the Dow Jones fell 7.1% or 684 points, setting a record at the time for the highest one-day loss in the exchange’s history. By Friday, the NYSE had experienced the greatest one-week decline in its history. The Dow 30 was down more than 14%, the S&P 500 plunged 11.6%, and the Nasdaq dropped 16%. In all, about $1.4 trillion in wealth disappeared during the five trading days. Since then, this record has only been surpassed once at the early stages of the pandemic.

In hindsight, the industries most negatively impacted make sense. Airlines and the insurance sectors lost tremendous value. A flight to quality made gold popular as the price per ounce leaped 6% to $287.

Gas and oil prices quickly rose as fears that oil imports from the Middle East would be slowed or stopped altogether. Those fears lasted about a week; then, after no new attacks and a clearer understanding of the intentions of government officials, index levels returned to near their pre-911 levels.

The sectors that experienced major gains after the attacks include technology companies and certainly defense and weapons contractors. Investors anticipated a huge increase in government borrowing and spending as the country prepared to root out terror around the world. Stock prices also spiked for communications and pharmaceutical companies.

On the U.S. options exchanges, volatility in the markets caused put and call volume to increase. Put options, designed to allow an investor to profit if a specific stock declines in price, were purchased in large numbers on airline, banking, and publicly traded insurance companies. Call options, designed to allow an investor to profit from stocks that go up in price, were purchased on defense and military-related companies. Short-term profits were made by investors who were quick to execute.

The terrorism of September 11 will, doubtless, have significant effects on the U.S. economy over the short term. An enormous effort will be required on the part of many to cope with the human and physical destruction. But as we struggle to make sense of our profound loss and its immediate consequences for the economy, we must not lose sight of our longer-run prospects, which have not been significantly diminished by these terrible events. – Fed Chairman Alan Greenspan, September 20, 2001

Since September 11

Over the following 21 years, the major U.S. stock exchanges have taken steps to make physical disruption of trading more difficult. This includes dramatically increasing the percentage of trading that is electronic. While this has made the U.S. markets less vulnerable to physical attacks, it is feared that there is increased potential for cyberattacks. “As we have digitized our lives, which has generally been a great blessing, we have sown the seeds for even greater destruction in terms of the ability to hack into our systems,” said former Securities and Exchange Commission Chairman Harvey Pitt, who led the agency on Sept. 11, 2001. “That is today’s equivalent of a 9/11 attack. There is a potential ‘black swan’ event every single day.”

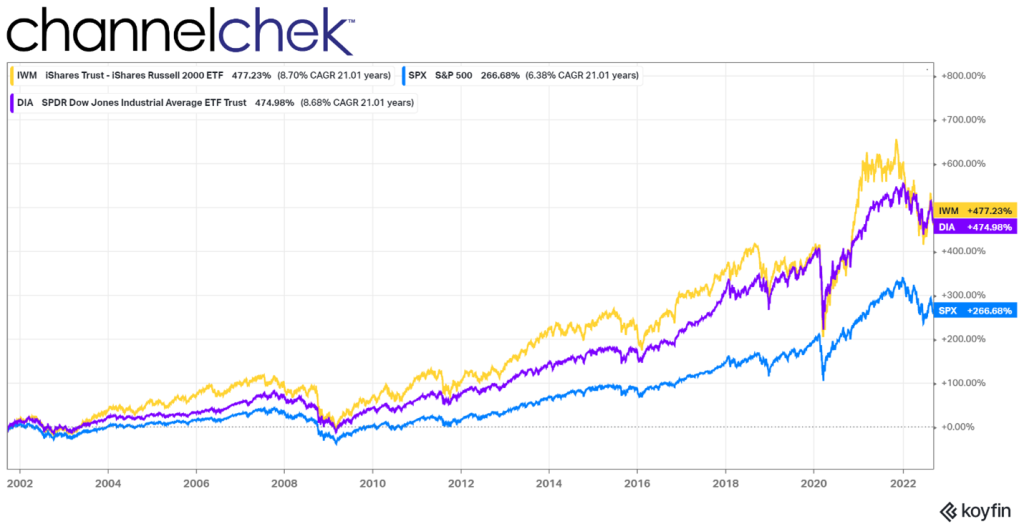

Major Market Indices Since September 11, 2001 (Source: Koyfin)

The investment markets have enjoyed above-average upward movement, despite the negative short-term impact of the black swan event. In the nearly 20 years since Sept. 11, the S&P 500, Nasdaq 100, and Russell 2000 Small-Cap index has risen more than four-fold. The bond market has also been strong (persistent low rates) despite increased borrowing to fund defense operations to finance America’s 911 response.

The U.S. economy itself has had long periods of expansion since 2021, even with the mortgage market crisis from December 2007 to June 2009, and the economic challenges from the response to the COVID-19 pandemic.

The costs, however, are likely to continue to be borne by taxpayers for generations. Interest-related costs alone on debt which financed military operations, including the long Afghanistan war, which was resolved last year when the U.S. withdrew after 20 years, and the protracted conflict in Iraq from 2003 to 2011, are high. The economic drag of these costs, while not fully measurable, are real.

The U.S. government financed the wars with debt, not taxes. Interest rates have been low, but taxpayers have already helped pay approximately $1 trillion in interest costs on the debt incurred to finance the two wars. These interest costs are expected to balloon to $2 trillion by 2030 and to $6.5 trillion by 2050 (according to the Watson Institute at Brown University). This places upward pressure on interest rates and places downward pressure on economic activity. One reason is that taxes used to fund interest costs take money from the economy without providing any stimulus or new material benefit.

Off Wall Street

September 11 radically changed the national mood and political environment. Polls and surveys taken just before the 911 attacks found Americans growing less certain about the direction of the country as a recession began to weigh down the ability to be optimistic. A full 44 percent of the country thought it was headed in on the wrong direction, according to the August 29-30, 2001 New Models survey.

Logic might suggest that after a successful attack, people’s attitudes toward the direction of the country would trend toward a worse future. Reporters, politicians, and spokespeople all predicted a terrible economic shock; their forecast seemed supported by the first week’s plunge in markets. But the events of that day seemed to give citizens purpose. In fact, statistics that indicated the “direction of the country” showed that optimism surged. An October 25-28 CBS/NY Times survey reported that people felt the country was headed in the right direction by a two-to-one margin. A sense of pride in who we are as a country and as individuals overcame negative economic news in an unprecedented way.

Take Away

It has been over two decades since what many of us think of as recent. The truth is, children born on September 11, 2021 or before are now of drinking age. But history can prepare us for new events. The market’s first reaction to tragic news is always down; when proven temporary, bargain hunters come in, then the market has always resumed its historical growth trend upward.

The markets now trade more digitally with almost no need for runners in lower Manhattan and far less open-outcry and paper jockeying by masses of people working for companies in one small section of Manhattan island. But the new threats are also real, a cyber attack on electronic records or transactions could be devastating in its own way.

Challenges even those caused by tragedy provide opportunity and even purpose. September 11, and its aftermath are proof of this.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent drill results. Labrador Gold released results from recent drilling associated with its 100,000-meter drill program at its 100%-owned Kingsway gold project targeting the Appleton Fault Zone over a 12-kilometer strike length.A total of 52,648 meters have been drilled to date with assays pending for samples from approximately 3,343 meters of core. The company has four drill rigs operating, including two at the Big Vein target, one rig at the Golden Glove target, and one at the CSAMT target. Till sampling and prospecting continues to generate new drill targets along the Appleton Fault Zone and the gabbro trend north and south of Midway. Drilling on these targets will commence once initial drilling at the CSAMT target is complete.

Big Vein results continue to impress. At the Big Vein target, Hole K-22-177 returned 2.02 grams of gold per tonne over 32 meters from 134 meters depth that included 18.08 grams of gold per tonne over 0.63 meters and 11.42 grams of gold per tonne over 1.05 meters. It represents the longest mineralized intersection on the property to date. Hole K-22-187 at Big Vein southwest intersected 12.84 grams of gold per tonne over 0.8 meters from 341 meters depth.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ark Invest’s Cathie Wood Finds the Federal Reserve Quixotic

On Wall Street, staying with the herd guarantees average gains or losses. Wandering far from the herd adds two more possibilities. You may still have average performance, you may exceed the averages, or you may get slaughtered. ARK Invest’s Cathie Wood likes to explore her own field in which to graze, far from the herd. This preference shows in her funds performance. At times her returns have far exceeded competing hedge funds, and at other times they fall well below the pack.

In October of 2021, before Fed Chairman Powell changed his thinking that inflation may not be transitory, the renowned hedge fund manager, and market guru, Cathie Wood began sounding alarm bells about her fear of deflationary pressures. At the same time, she warned of job losses due to displacement as technology would reduce costs and the need for the current skill sets in the labor force.

For months renowned investor Cathie Wood has said that the Federal Reserve should stop raising interest rates, that the economy is seeing deflation rather than inflation, and that it is in a recession.

Even as others in the”transitory” camp have come more in line with the official position of the Fed on inflation, she has remained steadfast to her idea that new technology will solve supply issues. Supply is an important inflation input, and that innovation may oversupply to a point where the economy may struggle with falling prices.

This week she tweeted a few reasons for her forecast and shared her thoughts on Jerome Powell’s address at the Jackson Hole Economic Symposium.

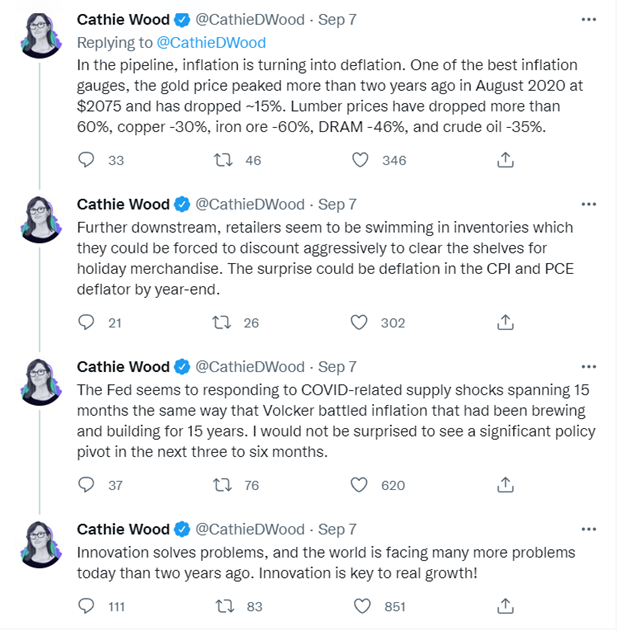

Her view is that the Fed has overshot the target. Wood, who was already working on Wall Street during the high inflation 1970’s, tweeted her reasons for this belief. High on her list is the price of gold (expressed in dollars) which she says is one of the best inflation gauges. Gold, she tweeted, “peaked more than two years ago.”

She also reminded followers of the price movements of other commodities, all down. These include lumber’s price decrease of 60%, iron ore 60%, oil 35%, and copper 30%. Much closer to final consumer prices, she highlighted that retailers are flush with inventories that don’t match the selling season. They’re discounting to clear shelves which could result in a deflation print in one of the more popular inflation gauges.

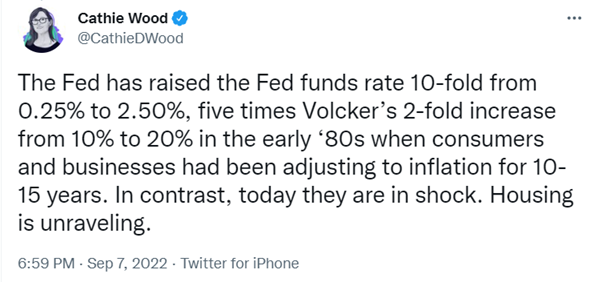

The Fed chairman who last fought inflation with unblinking resolve is Paul Volcker. Ms. Wood reminded her Twitter followers that the inflation he was battling had been “brewing and building for 15 years.” In comparison, she said inflation under Jay Powell’s watch is only 15 months old and Covid-related. She thinks the current Fed Chair has gone too far, and “I wouldn’t be surprised to see a significant policy pivot over the next three to six months,” Wood said.

A Quixotic Fed?

Powell and his colleagues are looking at the wrong data, Wood tweeted. “The Fed is basing monetary policy decisions on backward indicators: employment and core inflation,” she tweeted. “Inflation is turning into deflation,” she said in another tweet.

Wood said, comparing the two Fed chairpersons, Powell invoked Volcker’s name four times in the Jackson Hole speech. Her tweets explained inflation was much higher in Volker’s era. “Until Volker took over [of the Fed] In 1979, 15 years after the start of the Vietnam War and the Great Society, did the Fed launch a decisive attack on inflation,” Wood detailed.

“Conversely, in the face of two-year supply-related inflationary shocks, Powell is using Volker’s sledgehammer and, I believe, is making a mistake.”

Take Away

Without different opinions and different investment holding periods, there would be no market. We’d all speculate on the same things, and they’d continue upward until the last dollar was invested.

Ark Invest’s flagship Arc Innovation ETF (arkk) has fallen 55% this year, more than double the fall-off of the indexes. When discussing current performance Wood has defended her strategy by reminding others that she has an investment horizon of five years. As of Sept. 7, Arc Innovation’s five-year annualized return was 5.81%.

Cathie Wood has continued an almost year-long campaign warning of deflation and saying the Federal Reserve should stop raising interest rates, and that the economy is in a recession. If she is right and has selected the investments that benefit from being correct, then those invested in her funds will be glad they placed some of their investment funds away from the herd.

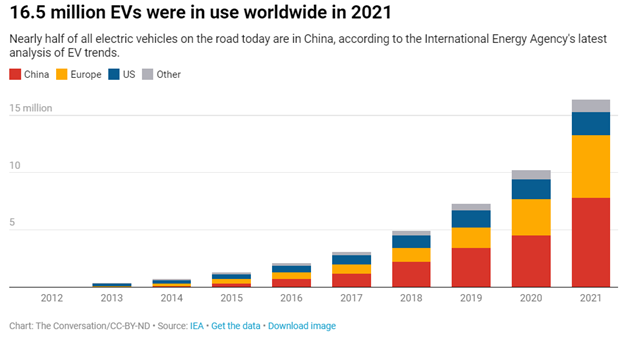

Making EVs Without China’s Supply Chain is Hard, But Not Impossible – 3 Supply Chain Experts Outline a Strategy

Two electrifying moves in recent weeks have the potential to ignite electric vehicle demand in the United States. First, Congress passed the Inflation Reduction Act, expanding federal tax rebates for EV purchases. Then California approved rules to ban the sale of new gasoline-powered cars by 2035.

The Inflation Reduction Act extends the Obama-era EV tax credit of up to US$7,500. But it includes some high hurdles. Its country-of-origin rules require that EVs – and an increasing percentage of their components and critical minerals – be sourced from the U.S. or countries that have free-trade agreements with the U.S. The law expressly forbids tax credits for vehicles with any components or critical minerals sourced from a “foreign entity of concern,” such as China or Russia. That’s not so simple when China controls 60% of the world’s lithium mining, 77% of battery cell capacity and 60% of battery component manufacturing. Many American EV makers, including Tesla, rely heavily on battery materials from China.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It was written by and represents the research-based opinions of Ho-Yin Mak, Associate Professor in Operations & Information Management, Georgetown University – Christopher S. Tang, Professor of Supply Chain Management, University of California, Los Angeles – Tinglong Dai, Professor of Operations Management & Business Analytics, Carey Business School, Johns Hopkins University.

The U.S. needs a national strategy to build an EV ecosystem if it hopes to catch up. As experts in supply chain management, we have some ideas.

Why the EV Industry Depends Heavily on China

How did the U.S. fall so far behind?

Back in 2009, the Obama administration pledged $2.4 billion to support the country’s fledgling EV industry. But demand grew slowly, and battery manufacturers such as A123 Systems and Ener1 failed to scale up their production. Both succumbed to financial pressure and were acquired by Chinese and Russian investors.

China took the lead in the EV market through an aggressive mix of carrots and sticks. Its consumer subsidies raised demand at home, and Beijing and other major cities set licensing quotas mandating a minimum share of EV sales.

China also established a world-dominating battery supply chain by securing overseas mineral supplies and heavily subsidizing its battery manufacturers.

Today, the U.S. domestic EV supply chain is far from adequate to meet its goals. The new U.S. tax credits are designed to help turn that around, but building a resilient EV supply chain will inevitably entail competing with China for limited resources.

A comprehensive national strategy entails measures for the short, medium and long term.

Short-Term: What Can be Done Now?

Six of the 10 best-selling EV models in 2022 are already assembled in the U.S., fulfilling the Inflation Reduction Act’s final assembly location clause. The Hyundai-Kia alliance, which has three of the other four bestsellers, plans to open an EV assembly line in Georgia. Volkswagen has also started assembling its ID.4 electric SUV in Tennessee.

The challenge is batteries. Besides the Tesla-Panasonic factories in Nevada and planned in Kansas, U.S.-based battery manufacturers trail their Chinese counterparts in both size and growth.

For the U.S. to scale up its own production, it needs to rely on strategic partners overseas. The Inflation Reduction Act allows imports of critical minerals from countries with free trade agreements to still qualify for incentives, but not imports of battery components. This means overseas suppliers like Korea’s “Big Three” – LG Chem, SK Innovation and Samsung SDI – which supply 26% of the world’s EV batteries, are shut out, even though the U.S. and Korea have a free trade agreement.

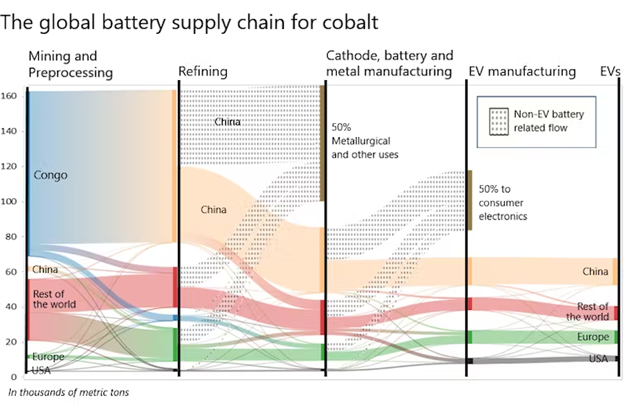

The bulk of the world’s cobalt is mined in the Democratic Republic of Congo but processed and turned into lithium-ion battery components by Chinese companies. This chart shows the pathways from mining to EVs.

The Korea Automobile Manufacturers Association has asked Congress to make an exception for Korean-made EVs and batteries.

In the spirit of “friend-shoring,” the Biden administration could think of a temporary waiver as a stopgap measure that makes it easier for Korean battery makers to move more of their supply chain to the U.S., such as LG’s planned battery plants in partnerships with GM and Honda.

The 2021 Infrastructure Act also provided $5 billion to expand charging infrastructure, which surveys show is critical to bolstering demand.

Medium-Term: Diversifying Lithium and Cobalt Supplies

A strong and concerted effort in trade and diplomacy is necessary for the U.S. to secure critical mineral supplies.

As EV sales rise, the world is expected to face a lithium shortage by 2025. In addition to lithium, cobalt is needed for high-performance battery chemistries.

The problem? The Democratic Republic of the Congo is where 70% of the world’s cobalt is mined, and Chinese companies control 80% of that. The distant second-largest producer is Russia.

The Biden administration’s “friend-shoring” vision has a chance only if it can diversify the lithium and cobalt supply chains.

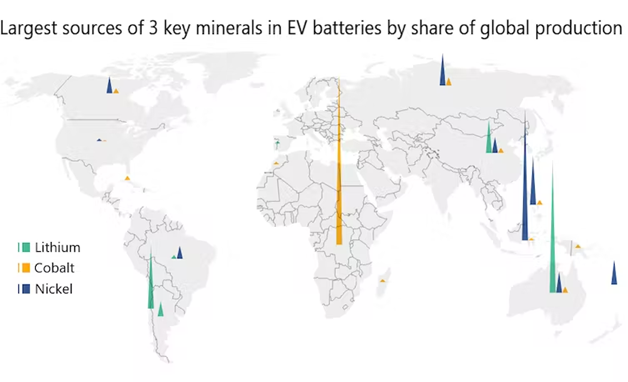

Lithium, cobalt and nickel are critical components in many EV batteries. The largest 2021 production sources included the Democratic Republic of Congo for cobalt; Australia, Chile and China for lithium; and Indonesia, the Philippines and Russia for nickel.

The “Lithium Triangle” of South America is one region to invest in. Also, Australia, a key U.S. ally, leads the world in lithium production and possesses rich cobalt deposits. Waste from many of Australia’s copper mines also contains cobalt, lowering the cost. GM has reached an agreement with the Australian mining giant Glencore to mine and process cobalt in Western Australia for its Ohio battery plant with LG Chem, bypassing China.

A way to avoid cobalt altogether also exists: lithium-iron-phosphate batteries are about 30% cheaper to make because they use minerals that are easy to find and plentiful. However, LFP batteries are heavier and have less power and range per unit.

For years, Chinese companies like CATL and BYD were the only ones making LFP batteries. But the patent rights associated with LFP batteries expire this year, opening up an important opportunity for the U.S.

Since not everyone needs a high-end electric supercar, affordable EVs powered by LFP batteries are an option. In fact, Tesla now offers Model 3s with LFP batteries that can travel about 270 miles on a charge.

The 2021 Bipartisan Infrastructure Law set aside $3.16 billion to support domestic battery supply chains. With the Inflation Reduction Act’s emphasis on supporting more affordable EVs – it has price caps for vehicles to qualify for incentives – these funds will be needed to help scale up domestic LFP manufacturing.

Long-Term: US Critical Mineral Production

Replacing overseas critical materials with domestic mining falls under long-term planning.

The scale of current domestic mining is minuscule, and new mining operations can take seven to 10 years to establish because of the lengthy permitting process. Lithium deposits exist in California, Maine, Nevada and North Carolina, and there are cobalt resources in Minnesota and Idaho.

Finally, to build an industrial commons for EVs, the U.S. must continue to invest in research and development of new battery technologies.

Pools of brine containing lithium carbonate stretch across a lithium mine in the Atacama Desert of Chile. Local opposition can be a challenge to mining proposals. Nuno Luciano (Flickr)

Also, end-of-life battery recycling is essential to the sustainability of EVs. The industry has been kicking the can down the road on this, as recycling demand has been minuscule thus far given the longevity of batteries. Yet, as a proactive step, the Inflation Reduction Act specifically permits battery content recycled in North America to qualify for the critical mineral clause.

To make this happen, the federal and state governments could use takeback legislation similar to producer responsibility laws for electronic waste enacted in more than 20 states, which stipulate that producers bear the responsibility for collecting, transporting and recycling end-of-cycle electronic products.

What’s Ahead

With the new law, the Biden administration has set its sights on a future transportation system that is built in the U.S. and runs on electricity. But there are supply chain obstacles, and the U.S. will need both incentives and regulations to make it happen.

California’s announcement will help. Under the Clean Air Act, California has a waiver that allows it to set policies more strict than federal law. Other states can choose to follow California’s policies. Seventeen other states have adopted California’s emissions standards. At least three, New York, Washington and Massachusetts, have already announced plans to also phase out new gas-powered cars and light trucks by 2035.

MALVERN, Pa., Sept. 08, 2022 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that the Company’s Chief Scientific Officer, Arun Upadhyay, PhD, will be among the featured speakers at the 3rd Annual Gene Therapy for Ophthalmic Disorders conference, which is being held Sept. 13-16 in Danvers, Massachusetts.

Details regarding Dr. Upadhyay’s presentation are as follows:

Event:

3rd Annual Gene Therapy for Ophthalmic Disorders Conference

Topic:

Highlighting the Modifier Gene Therapy Approach for the Treatment of Retinitis Pigmentosa

Date:

September 14, 2022

Time:

9:15 a.m. ET

Location:

DoubleTree by Hilton Boston North Shore, Danvers, Mass.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Contact: Tiffany Hamilton Head of Communications IR@ocugen.com