Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Look-in on Programs. Yesterday, MustGrow announced the update on the Company’s biological programs with various partners Sumitomo, Bayer, Janssen PMP, and NexusBioAg. The update includes the soil biofumigation, postharvest food preservation, and bioherbicide of the Company’s mustard-derived technology.

Soil Biofumigation. Data regarding efficacy continue to remain positive, as the Company recently extended the program with Sumitomo that we highlighted in August. Sumitomo is working with MustGrow and the EPA in the registration approval process in the U.S. along with registration in Mexico. In Chile, the country approved an Experimental Use permit and registration work has commenced. Bayer has shown positive results in laboratory and greenhouse studies, and has new trials underway and further studies planned for Europe, Asia, and Africa.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Lee Enterprises, Incorporated provides local news, information, and advertising primarily in midsize markets in the United States. It publishes 49 daily newspapers, as well as offers 300 weekly newspapers and specialty publications in 23 states. The company also provides online advertising and services; and online infrastructure and online publishing services for approximately 1,500 daily and weekly newspapers and shoppers. In addition, it offers commercial printing services. The company has a strategic alliance with Yahoo!, Inc. to provide its classified employment advertising customer base the opportunity to post job listings and other employment products on Yahoo!�s HotJobs national platform. Lee Enterprises, Incorporated was founded in 1890 and is based in Davenport, Iowa.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transferring pension liabilities. The company announced in its latest 8-K that it has agreed to purchase annuities from an insurance company with a portion of its pension plan assets, whereby it will transfer roughly $86 million in pension liabilities off the balance sheet.

A cleaner balance sheet. We view this development favorably, as it is a move to de-risk the balance sheet. Notably, the pension plan, which was already overfunded by roughly $1 million, is expected to increase the over funded amount by several million. The pension obligations are expected to decrease as interest rates rise, but this move de-risks the company from funding should interest rates fall.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

U.S. Department of Energy grant application. Comstock filed a grant application with the U.S. Department of Energy (DOE) to build a pre-pilot scale system to demonstrate one of its methods to produce renewable diesel, sustainable aviation fuel, gasoline, and marine fuel from woody biomass utilizing Comstock’s technology and processes leading to greater yield, efficiency, and cost relative to other methods.

An impressive roster of grant participants. Comstock’s grant application is supported by an impressive roster of collaborators, including Marathon Petroleum Company LP, Topsoe Inc., Novozymes, Xylome Corporation, RenFuel K2B AB, Emerging Fuels Technology Inc., the University of Nevada, Reno, the University of Minnesota Duluth’s Natural Resources Research Institute, and the State University of New York College of Environmental Science and Forestry.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bowlero Corp. is the worldwide leader in bowling entertainment, media, and events. With more than 300 bowling centers across North America, Bowlero Corp. serves more than 26 million guests each year through a family of brands that includes Bowlero, Bowlmor Lanes, and AMF. In 2019, Bowlero Corp. acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero Corp., please visit BowleroCorp.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Reports a strong year. The company reported another strong quarter. Q4 revenue of $267.7 million increased a strong 68% from year earlier levels and an impressive 42% above our estimate of $188.3 million. The strong revenue was attributed to favorable “walk-in” revenue. Adj. EBITDA was well above our estimate at $82.4 million, 45% higher than our forecast of $56.8 million.

The COVID bounce continues. Management noted the strong performance was driven in large part by a continuation of the COVID recovery. This is perhaps best illustrated by Group Event revenue which was $46 million, up 140% from the prior year period. Notably, the recovery of Event revenue will likely get an additional boost over the upcoming holiday season as year earlier results reflected lingering Covid issues.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARPA-H: High-Risk, High-Reward Health Research is the Mandate of New, Billion-Dollar US Agency

A new multibillion-dollar federal agency was created with a goal of supporting “the next generation of moonshots for health” in science, logistics, diversity and equality. And the agency now has it’s first leader, as President Joe Biden announced Renee Wegrzyn as director of the Advanced Research Projects Agency for Health, or ARPA-H, on Sept. 12, 2022.

Since the announcement of the intention to establish ARPA-H two years ago, this new agency has sparked interest and questions within both academia and industry.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Tong Sun, Assistant Dean of Translational Health Sciences, University of Washington.

I have been a director of innovation-driven health institutes for decades and have worked with many of the government agencies that fund science. I and many of my colleagues hope ARPA-H will become an agency that can quickly turn scientific discoveries into real-world advances to detect, prevent and treat diseases like cancer, diabetes and Alzheimer’s. But questions still remain surrounding how it will work and what makes it different from other government-funded agencies such as the National Institutes of Health and the National Science Foundation.

What is ARPA-H?

ARPA-H is the newest entity established within the National Institutes of Health. ARPA-H was explicitly set up as an independent agency within NIH, in theory allowing it to benefit from the NIH’s vast scientific and administrative expertise and resources while still being nimble and forward-thinking.

ARPA-H was inspired by and modeled after the Defense Advanced Research Projects Agency, or DARPA, to rapidly develop cutting-edge technologies. DARPA is small compared to other federal research and development agencies, but has long been hugely successful. It played a critical role in spawning many technologies ranging from the internet to GPS, and even funded Moderna to develop mRNA vaccine technology in 2013.

ARPA-H is not the only DARPA spinoff. In 2006, the federal government created the Intelligence Advanced Research Projects Activity to tackle difficult challenges in the intelligence community, and in 2009, the Advanced Research Projects Agency for Energy was launched. Though its budget is small compared to the Department of Energy, ARPA-E has been incredibly effective in funding ambitious research into fighting climate change. By funding ambitious mid- and long-term projects, IARPA, ARPA-E and now ARPA-H are meant to operate in between slow, government-funded basic research and short-term, profit-driven private sector venture capital.

ARPA-H is modeled after the Defense Advanced Research Projects Agency, which played a key role in developing many modern technologies, including personal computers. Tim Colegrove (Wikimedia Commons)

How Will the Agency Function?

Biden wants ARPA-H to replicate the success of DARPA, but in the health care realm, by providing “leadership for high-risk, high-reward biomedical and health research to speed application and implementation of health breakthroughs equitably.”

Established federal agencies like the NIH and the National Science Foundation prefer to fund more basic research and less risky projects compared to the high-risk, high-reward, applied science approach of DARPA. If ARPA-H wants to achieve the success of its predecessor, it will need to operate differently from NIH and NSF.

DARPA employs about 100 program managers who are “borrowed” from academia or industry for three to five years. These managers travel across the nation to meet with scientists and experts in different fields in order to generate ideas and start projects. These managers make funding decisions and work closely with their funded teams to overcome problems, but will cut funding if teams cannot deliver promised milestones on time. Many DARPA projects don’t produce spectacular successes, yet they pushed the boundaries of science and technology.

Many years ago, I had the privilege of working with a DARPA program manager alongside numerous experts in various scientific and medical fields. After several months of meetings, the program manager came up with the idea to develop “fracture putty” – a puttylike material that could be applied to the shattered bones of a wounded soldier in the battlefield. The material would support weight, prevent infection, expedite healing and bone regeneration and eventually dissolve away. The program launched in 2008, and our team of chemists, nanomaterials experts, bioengineers, mathematical modelers and surgeons was one of the funded teams in this program.

President Joe Biden appointed Renee Wegrzyn, a former DARPA project manager and biotech industry expert, to lead ARPA-H. Image: Renee Wegrzyn (@rwegrzyn)

Who is the New Director?

Wegrzyn holds a Ph.D. in molecular biology and bioengineering from Georgia Tech. She is currently a vice president of business development at Ginkgo Bioworks, a U.S. biotech company. Wegrzyn spent four and half years as a program manager in DARPA’s Biological Technologies Office, where she managed projects that focused on using genetic engineering and gene editing for biosecurity and public health. She also worked for another DARPA-inspired agency, Intelligence Advanced Research Projects Activity.

At this moment, we don’t know yet the exact plan and progress in hiring APPA-H program managers and where APAR-H’s headquarters will be located. Several cities have expressed interest.

What Should People Look for as ARPA-H Gets Started?

DARPA is driven by talented, ambitious and risk-taking program managers. They are the ones who generate ideas and turn lofty goals into executable projects. It will be interesting to see how many and what kind of program managers ARPA-H hires in its early days, as these decisions will give an indication of which areas within health care the agency will be prioritizing.

I’ll also be watching to see how well ARPA-H and its program managers work within the NIH, which has an unbelievable depth of resources and expertise in all health care related fields that ARPA-H can tap into. But the NIH has very different funding mechanisms and culture from DARPA.

The final question is money. Biden wants US$6.5 billion in funding for ARPA-H, and he’s only gotten $1 billion from Congress so far. This is its first, biggest challenge. Finding political unity for funding may have to be this new agency’s first big breakthrough if it is to reach its goals.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

NDRS. We hosted Great Lakes CEO & President Lasse Petterson and CFO Scott Kornblau for a series of investor meetings in New York City on Tuesday. Following are some highlights from the meetings.

Improving Bid Environment. Management noted the bid environment has improved dramatically from 1H22 and it looks like the recent momentum will continue into the fourth quarter. If trends continue, the overall 2022 bid market could end up exceeding the strong 2021 bid market.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

What is Proof-of-Stake? A Computer Scientist Explains a New Way to Make Cryptocurrencies, NFTs and Metaverse Transactions

Proof-of-stake is a mechanism for achieving consensus on a blockchain. Blockchain is a technology that records transactions that can’t be deleted or altered. It’s a decentralized database, or ledger, that is under no one person or organization’s control. Since no one controls the database, consensus mechanisms, such as proof-of-stake, are needed to coordinate the operation of blockchain-based systems.

While Bitcoin popularized the technology, blockchain is now a part of many different systems, enabling interesting applications such as decentralized finance platforms and non-fungible tokens, or NFTs.

The first widely commercialized blockchain consensus mechanism was proof-of-work, which enables users to reach consensus by solving complex mathematical problems. For solving these problems, users are commonly provided stake in the system. This process, dubbed mining, requires large amounts of computing power. Proof-of-stake is an alternative that consumes far less energy.

At its core, blockchain technology provides three important properties:

Decentralized governance and operation – the people using the system get to collectively decide how to govern and operate the system.

Verifiable state – anyone using the system can validate the correctness of the system, with each user being able to ensure that the system is currently working as expected and has been since its inception.

Resilience to data loss – even if some users lose their copy of system data, whether through negligence or cyberattack, that data can be recovered from other users in a verifiable manner.

The first property, decentralized governance and operation, is the property that controls how much energy is needed to run a blockchain system.

Voting in Blockchain Systems

Blockchain systems use voting to decentralize governance and operation. While the exact mechanisms for how voting and consensus are achieved differ in each blockchain system, at a high level, blockchain systems allow each user to vote on how the system should work, and whether any given operation – accepting a new block into the chain, for example – should be approved.

Traditionally, voting requires that the identity of the people casting ballots can be known and verified to ensure that only eligible people vote and do so only once. Some blockchain systems allow users to present a digital ID to prove their identity, enabling voting with negligible energy usage.

However, in most blockchain systems, users are anonymous and have no digital ID that can prove their identity. What, then, stops an individual from pretending to be many individuals and casting many votes? There are several different approaches, but the most used is proof-of-work.

In proof-of-work, users get votes based on the amount of computational power they have in proportion to other users. They demonstrate their ownership of this computational power by solving difficult mathematical problems. If one user can solve twice as many problems as another user, they have twice the computational power as other users and get twice as many votes.

However, solving these mathematical problems is extremely energy intensive, leading to complaints that proof-of-work is not sustainable.

Proof-of-Stake

To address the energy consumption of proof-of-work, another way to validate users is needed. Proof-of-stake is one such method. In proof-of-stake, users validate their identities by demonstrating ownership of some asset on the blockchain. For example, in Bitcoin, this would be ownership of bitcoins, and in Ethereum, it is ownership of Ether.

Though this does require users to temporarily lock their assets in the blockchain for a period of time, it is far more efficient because it requires negligible energy expenditure. By the company’s estimation, moving from proof-of-work to proof-of-stake will reduce Ethereum’s energy consumption by 99.95%.

Ethereum’s ‘Merge’

This improved energy efficiency is why many blockchain systems intend to transition away from proof-of-work to proof-of-stake. Ethereum plans to make this change during the week of Sept. 15, 2022. This is known as the Merge. During this merge, operations will shift from being voted on using proof-of-work to being voted on using proof-of-stake. At the completion of the merge, only proof-of-stake will be used to vote on transactions.

The hope is that this will set up Ethereum to be sustainable for the foreseeable future.

This article was republished with permission from The Conversation, anews site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Scott Ruoti, Assistant Professor of Computer Science, University of Tennessee

Increased Take Home Pay in 2023 Thanks to the IRS (and Inflation)

If two negatives make a positive, what do you get when you cross inflation with the IRS?

In addition to receiving much higher COLA increases on Social Security payments, and earning an interest rate in excess of 9% on US Savings Bonds, those making an income in 2023 are likely to see more take-home pay. This should happen whether or not they get a raise. An IRS calculation devised to prevent bracket creep is to thank for this. While high inflation is destructive, at least there are a few things that are put in place that will automatically adjust and help ease the pain.

The adjustment to tax brackets typically has had a minimal impact on workers paychecks. But the tax formulas that are law and the persistent inflation through 2022 point to significant impact on workers 2023 tax bill. Next year when income tax thresholds and the standard deductions are raised, if all else is unchanged, there will be more money in the income earners’ pockets, and less going to the government.

How Much More?

According to an accounting professor at Northern Illinois University named Jim Young, a single taxpayer with $100,000 in adjusted gross income in 2023 could experience a tax savings of about $500, or $42 each month.

Contribution maximums are also expected to be raised where tax-advantaged savings for retirement could also help reduce tax burdens in the coming years. Estate and gift tax thresholds would also automatically be increased by as much as $2 million more for a couple.

The IRS makes the adjustments based on formulas and inflation data spelled out in the tax code. This is different than the headline CPI-U which is most often reported.

The inflation measure used for the tax and contribution adjustments is the Chained Consumer Price Index (C-CPI-U), which takes into account the substitutions customers make when costs rise. The average of the chained CPI from September 2021 through August 2022 is used to calculate the 2023 adjustments, which the IRS will announce next month. These ultimately affect tax returns for the 2023 tax year filed in early 2024.

Price increases eroding purchasing power are running at the most rampant pace in forty years. Based on the current average of the C-CPI-U, here are estimates on what to expect, according to the American Enterprise Institute:

Tax levels and other tax bracket thresholds and breakpoints will increase by around 7% over 2022. The 2022 increase over 2021 was around 3%, which was the largest percentage increase in four years. For the tax year 2023, income earners will see the breakpoints moved by the most in 35 years.

The top federal income tax threshold in 2023 is expected to rise by nearly $50,000 next year for married couples, and that 37% rate will apply to income above $693,750. For individuals, the top tax bracket will start at $578,125.

The standard deduction for married couples is expected to be $27,700 for 2023, up from $25,900 this year, and $13,850 for individuals, up from $12,950. This is the amount that those who do not itemize deductions can reduce their W-2 federal income by before being subject to income tax.

The federal estate tax exclusion amount, what a person can protect from estate taxes, is $12.06 million this year. That’s expected to rise to $12.92 million by 2023, meaning a married couple can shield nearly $26 million from estate taxes.

The annual tax-free gift limit is expected to rise from $16,000 this year to $17,000 by 2023.

The maximum contribution amount for an individual retirement account is expected to jump to $6,500 for 2023, up from $6,000, where it has been since 2019. The maximum contribution allowed for a flexible health account is expected to increase to $3,050 in 2023, up from $2,850 this year.

The maximum contribution amount for a 401(k) or similar workplace retirement plan is governed by yet another formula that uses September inflation data. It is estimated that the contribution limit will increase to $22,500 in 2023 from $20,500 this year and the catch-contribution amount for those age 50 or more will rise from $6,500 to at least $7,500.

The child tax credit under current law is $2,000 per child is not adjusted for inflation. But the additional child tax credit, which is refundable and available even to taxpayers that have no tax liability, is adjusted for inflation. It is expected to increase from $1,500 to $1,600 in 2023.

For those that look forward to capping out payments to Social Security, there is bad news. This has also increased. According to the 2022 Social Security Trustees Report, the wage base tax rate is projected to increase 5.5% from $147,000 to $155,100 in 2023.

Costs are rising, but so are deductions. It’s improbable that the reduced taxes will offset skyrocketing inflation, but at least there is one financial category that is helped by the increases.

Newrange is focused on district-scale exploration for precious metals in the prolific Red Lake District of northwestern Ontario. The past-producing high-grade Argosy Gold Mine is open to depth, while the adjacent North Birch Project offers additional blue-sky potential. Focused on developing shareholder value through exploration and development of key projects, the Company is committed to building sustainable value for all stakeholders. Further information can be found on our website at www.newrangegold.com .

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New flagship project. Newrange signed a non-binding Letter of Intent (LOI) with Great Panther Mining Limited (NYSE American, GPL) to acquire a 100% interest in the past-producing Coricancha mine in central Peru. Management expects to sign a definitive agreement shortly. Coricancha is a high-grade, narrow-vein, gold-silver-copper-lead-zinc underground mine in the Central Polymetallic Belt of Peru. It is 90 kilometers east of Lima and includes a 600-tonne per day processing plant, dry-stack tailings storage facility and requisite surface and underground infrastructure.

Acquisition terms. Newrange has agreed to make a single cash payment of US$750,000 to Great Panther upon closing and the transaction will be on an “as-is” basis. Shareholder approval is not required. Because the acquisition is subject to financing, Newrange is considering a “one new for six old” share consolidation and subsequent name change to be effective upon closing. Closing is subject to certain conditions, including the completion of a definitive agreement, financing by Newrange, and receipt of all necessary third-party approvals.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Any Rail Strike Would Surely Cause Transitory Inflation

There is something I taught myself years ago as a young trader on Wall Street. I appreciate this “skill” less and less as the years go on, but it has served me well. When news breaks, my mind shifts to asking, “for what sectors is this bullish and for what sectors is this bearish?” No attachment except money movement. There will be time for personal involvement with the event after the market closes. The news of a train strike that may begin on Friday is a good example. My investor mind was quick to try and determine what companies would benefit and also which could be hurt. I have no control over whether or not it happens, but I may be able to add to portfolio returns from it. Meanwhile, at home, I’m stocking up on a few of the items often shipped by rail.

Below is some helpful information about this segment of the freight and shipping industry.

Background

Rail workers may go out on strike as early as Friday, September 16.

In the U.S. the Rail network runs almost 140,000 miles. Freight rail is an $80-billion industry operated by seven Class I railroads (railroads with operating revenues of $490 million or more), and 22 regional and 584 local/short line railroads.

More than 167,000 are employed across the U.S. It’s a safer and often more efficient means of shipping as it uses less energy and rides on a more cost-effective and safer infrastructure than trucking.

Heavy freight such as coal, lumber, metals, and liquids going long distances are likely to travel by rail or some combination of truck, rail, water, or pipeline. The rail network accounts for approximately 28% percent of U.S. freight movement by ton-miles (the distance and weight freight travels). So, by weight, 28% of what is shipped within the U.S. may get stalled in the event of a strike. This would significantly add to any supply chain issues currently being experienced.

Unlike roadways, U.S. freight railroads are owned by private organizations that are responsible for their own maintenance and improvements.

What Would be Impacted

In all, 52 percent of rail freight cars carry bulk commodities such as agriculture and energy products, automobiles and components, construction materials, chemicals, equipment, food, metals, minerals, paper, and pulp. The remaining 48 percent onboard is generally being shipped in packaging that allows it to easily be moved onboard a plane, van, or other non-bulk carrier.

Source: Federal Railroad Administration

A rail strike would stop a high percentage of the transportation of food, lumber, coal, oil and other goods across the U.S.

Current Status

Rail stocks like Union Pacific ($UNP) and CSX ($CSX) are underperforming the market this week as rail workers’ unions continue to negotiate for higher pay and benefits. The unionized workers have the legal go-ahead to strike at the end of the week if no agreement is reached. This could impact all major U.S. railroads and cripple the supply chain on many raw materials until the dispute is settled. An immediate but temporary impact would be material shortages that would push prices up, largely at the producer level. These shortages should be resolved when the strike ends as increased price pressures should come back down. But the short-lived inflation will be additive to final goods prices for a period of time.

Eight of 12 labor unions have reached tentative agreements with railroad carriers. However, there are still disagreements over vacation, sick days, and attendance policies.

A “cooling off” period expires Friday, at which time workers can strike.

A freight rail shutdown would be expected to cost the U.S. economy around $2 billion per day, according to the Association of American Railroads. It would especially hit the energy sector hard as rail is the number one mode of transportation used by coal producers, according to the Energy Information Administration (EIA).

Take Away

A rail strike would hit multiple sectors as it could stop the transportation of food, lumber, coal, and other goods across the country. Much of what is shipped by train can’t easily be shipped by the already overburdened trucking industry.

A strike, if any, would put upward pressure on lumber, energy, and food prices. Assuming the strike gets resolved, these transit-related higher price pressures should prove to be transitory. As individuals, whether or not there is a strike is beyond our ability to change. If there is an industry sector or company that stands to improve earnings or a sector that may suffer losses, there should be no investor guilt in positioning investments in a way where the investor may prosper.

AMC Diversified into Mining Last Winter – The Prospects Look Good

They should make a movie about the CEO of AMC Theaters, Adam Aron. But they ought to wait because it seems his story and that of AMC Theaters ($AMC) have a few more plot twists left. Yesterday AMC Shareholders struck gold. That is, the 22% of a gold mining operation in Nevada that AMC purchased in March returned extremely positive results as to the amount and quality of the yellow metal found in recent tests.

Let’s Rewind

In mid-March of this year AMC Theaters, coupled with Natural Resources Guru Eric Sprott, had taken a large stake in a gold and silver mining company. The company, Hycroft Mining Holdings ($HYMC), has a 71,000-acre gold mine in Northern Nevada. AMC’s stake was 22%. It invested $27.9 million in cash in Hycroft in exchange for 23.4 million warrant units, with each unit consisting of one common share of Hycroft and one common share purchase warrant. The units were priced at $1.193 a share, while each purchase warrant was priced at about $1.07 and carried a five-year term. HYMC had been trading in the $0.30 to $0.33 range when the deal was executed, as of September 14, the mining company was trading for $0.84 per share. AMC also was granted the right to appoint someone to Hycroft’s board.

Eric Sprott’s investment was made through a holding company for Sprott, not the alternative investment manager owned by Mr. Sprott, Sprott Inc. The holding company will make an equal investment in Hycroft with the same terms. Together, AMC and Sprott invested $56 million in the mining company.

So Far, So Good

The large stake taken by a completely unrelated business was ridiculed by many. One Seeking Alpha author called it a “Horror Story.” But the run-up in AMC’s stock from the short-squeeze in 2021 and its foresight to set aside capital for growth and diversification may have been smart. As of yesterday, the 22% stake in the uncorrelated business (Leisure vs Natural Resources) makes the CEO presiding over the popular meme-stock look like a hero.

According to a press release from Hycroft Mining, initial drill results from the test they conducted in different areas of the the property more than confirmed their expectations.

Alex Davidson, Vice President, Exploration at Hycroft commented, “These initial drill results confirm the higher-grade opportunities identified in the 2021 drill program. While we have only just begun investigating the planned targets of our 2022-23 drill program, these results are very encouraging and further confirm the importance of additional drilling to explore the untapped potential of the Hycroft deposit. Importantly, we are observing the high-grade zones are more continuous than previously interpreted in addition to seeing silver and gold grades significantly higher than the average grade at the Hycroft deposit.”

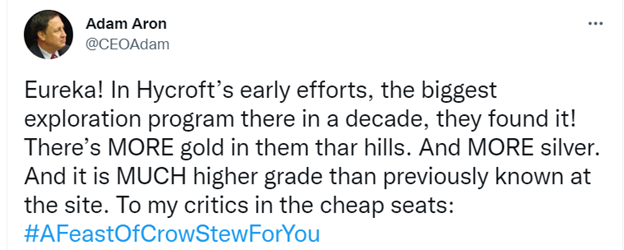

Adam Aron tweeted dramatically yesterday after the results were made public, exclaiming, “Eureka, In Hycroft’s early efforts, the biggest exploration program there in a decade, they found it! There’s MORE gold in them thar hills. And MORE silver. And it’s MUCH higher grade than previously known at the site. To my critics in the cheap seats: #AFeast of CrowStewForYou.

Take Away

The AMC story, so far this decade, is full of so many plot twists and unexpected events that it confounds even the most veteran market watchers.

High-level research and analysis for many natural resource producers is regularly posted on Channelchek, along with information on stocks within the leisure sector. Watch for continued updates on this story by signing up for Channelchek emails.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

10-Q Filing. Last week, Vera Bradley filed the 10-Q for the fiscal second quarter of 2023 ended July 30th and we had an opportunity to review. While the big picture remains the same from the August 31st earnings release, the 10-Q does provide some additional detail regarding the quarter’s performance.

VB Direct Comparable Sales. The overall 13.8% comp sales decline included a 20.1% decrease in comparable store sales, partially offset by a 3.1% increase in e-commerce sales. Non-comp stores contributed $2.6 million of revenue. The Company permanently closed eight full-line stores and opened six factory outlet stores in the last twelve months.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation. Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in two Phase 1 dose-escalation and expansion studies. These trials are currently underway in the United States and China. Onconova’s product candidate rigosertib is being studied in an investigator-sponsored study program, including in a dose-escalation and expansion Phase 1/2a investigator-sponsored study with oral rigosertib in combination with nivolumab for patients with KRAS+ non-small cell lung cancer.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Data Shows Efficacy After Treatment Failures. Onconova presented positive interim data from its Phase 1/2a trial testing rigosertib at the European Society for Medical Oncology (ESMO). The Investigator-sponsored trial tested the combination of rigosertib with nivolumab, an anti-PD1 checkpoint inhibitor, in non-small cell lung cancer patients that had progressive non-small cell lung cancer (NSCLC) following treatment with checkpoint inhibitor therapies.

Patients Showed Both Complete and Partial Responses. The interim data reported was for 14 out of 19 patients enrolled in the study. Four of the 14 (29%) showed disease control responses, including 1 complete response, 2 partial responses, and 1 stable disease. Mean survival for these responders was 6.75 months, compared with 1-2 months for the non-responders. Each responding patient had a different mutation in the KRAS gene, showing activity against multiple variants.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.