SKYX Positions to Advance its Market Penetration with the AI Native E-Commerce Platform Designed to Elevate B2B and B2C Experiences Through its Innovative and Smart Product Line

SKYX Continues to Grow its Builder Segment Through Direct Sales Channels and Intends to Utilize the New AI Driven Software to Enhance and Support its Builder and Pro Segments

E-Commerce Continues to Lead All Sectors as the Fastest-Growing Sales Channel for Businesses Worldwide

MIAMI, Nov. 05, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become smart and safe as the new standard, today announced it will be launching a new AI driven software for its e-commerce platform of 60 websites for lighting, home décor, and smart technologies. When fully integrated the new AI native driven software is expected to increase website conversion rates and sales by 30%.

As SKYX continues to grow its builder segment through direct sales channels, it intends to utilize the advantages of the new AI driven software platform to enhance and support its builder and pro segments. The software is expected to grow both B2B and B2C segments including SKYX’s advanced and smart home technologies.

SKYX’s E-commerce platform Belami, is led by CEO, Huey Long, and Executive Chairman, Todd Johnson.

Long, formerly Director of Amazon E-Commerce, Senior Vice President of Walmart, and Executive Vice President at Ashley Furniture, spearheaded the development of Amazon Basics, the company’s first private brand initiative. He has also served as Senior Vice President at Walmart Stores Inc., and Executive Vice President at Ashley Furniture.

Huey Long, CEO of Belami, said; “The next decade of retail growth will be driven by eCommerce and AI-powered innovation. By unifying our platform and data architecture, we can significantly accelerate revenue across more than 60 high-intent specialty sites and marketplaces while expanding into new B2B and professional segments. This new unified AI native software platform positions us to capture more share in large, fragmented home improvement markets — and to deliver measurable value for customers, vendors, and shareholders.”

Rani Kohen, Founder and Executive Chairman of SKYX Platforms, said; “This new AI-powered software reflects SKYX’s commitment to continuous innovation and growth. We are leveraging AI to maximize efficiency, scale our e-commerce operations, and create an intelligent ecosystem that supports our vision of making smart and safe living the global standard.”

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Powered by Microsoft Azure OpenAI, new solution automates reportable event detection for Pharma & Life Sciences companies across every customer channel

FLORHAM PARK, N.J. — Conduent Incorporated (Nasdaq: CNDT), a global technology-driven business solutions and services company, today announced the launch of a new GenAI-powered reportable event detection solution that dramatically improves the identification of events and empowers healthcare companies to uphold the highest standards of patient safety, both of which are critically important.

Built on Microsoft Azure OpenAI, Conduent’s reportable event detection solution enhances the speed, accuracy, and consistency to identify incidents that must be provided to the Food & Drug Administration (FDA) for compliance. These events include adverse reactions, product complaints, and usability issues that could arise across millions of customer interactions.

Why It Matters

Pharma and Life Science companies handle countless interactions with customers every day via emails, chats, voice calls, texts, faxes, and social and digital platforms, and within these interactions is vital information that potentially must be reported to the FDA.

Real-world examples of reportable events

A patient emailing about unexpected dizziness after taking a prescribed medication.

A caregiver calling to report a child’s rash after using a topical cream.

A customer texting that their insulin pen malfunctioned during use.

A chatbot conversation revealing confusion over dosage instructions.

A social media post describing a broken inhaler or packaging defect.

Setting New Standard for Compliance

Quality control to ensure the highest standards of quality, accuracy, and compliance are met is typically a manual process that can only randomly evaluate a small percentage of customer interactions. This new GenAI-powered solution can review nearly 100% of interactions across all channels, using GenAI to analyze language, context, and compliance rules to revolutionize the identification of reportable events.

“Patient assistance programs and medical information engagements are complex and data-rich, which is perfect for GenAI,” said Kimberly Marshall, Head of Commercial Solutions and Account Management at Conduent. “By combining AI with deep compliance expertise, we’re helping clients report faster, more accurately, and more consistently while saving time and money.”

This solution integrates GenAI with logical reasoning, AI-driven search, client-specific rules, training materials, and regulatory framework, backed by Conduent’s infrastructure, to automate the capture and classification of reportable events.

Key Benefits:

Enhanced Efficiency : Streamlines the process of identifying reportable events, saving time and reducing manual efforts.

Quality and Consistency: Understands the variability of consumer language to better identify potential reportable events and product quality complaints, and provides consistent, high-quality reporting.

Regulatory Compliance : Enables adherence to FDA regulations and other compliance standards, minimizing the risk of penalties. Life Science companies can use the data to enhance their marketing strategies, product packaging and user experiences while ensuring compliance with FDA regulations.

The Conduent reportable event detection tool is another collaboration where Conduent leverages Microsoft Azure OpenAI to drive quality, improve customer experience, and save cost.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 56,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $85 billion in government payments annually, enabling 2.3 billion customer service interactions annually, empowering millions of employees through HR services every year and processing nearly 13 million tolling transactions every day. Learn more at www.conduent.com.

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

DENVER–(BUSINESS WIRE)– The ONE Group Hospitality, Inc. (“The ONE Group” or the “Company”) (Nasdaq: STKS) today announced that Emanuel “Manny” Hilario, President and Chief Executive Officer, and Nicole Thaung, Chief Financial Officer, will host a conference call and webcast to discuss third quarter 2025 financial results on Thursday, November 6, 2025 at 4:30 PM ET. A press release containing the third quarter 2025 financial results will be issued after market close that same afternoon.

The conference call can be accessed live over the phone by dialing 203-518-9708. To enter the call, the conference ID is ONEG3Q25. A replay will be available after the call and can be accessed by dialing 412-317-6671; the passcode is 11159955. The replay will be available until Thursday, November 20, 2025.

The webcast can be accessed from the Investor Relations tab of The ONE Group’s website at http://www.togrp.com/ under “News / Events”.

About The ONE Group

The ONE Group Hospitality, Inc. (Nasdaq: STKS) is an international restaurant company that develops and operates upscale and polished casual, high-energy restaurants and lounges and provides hospitality management services for hotels, casinos and other high-end venues both in the U.S. and internationally. The ONE Group is recognized as one of “America’s Greatest Companies” (NEWSWEEK, 2025) and Benihana honored as Forbes Best Brands for Value . The ONE Group’s focus is to be the global leader in Vibe Dining, and its primary restaurant brands and operations are:

STK, a modern twist on the American steakhouse concept with restaurants in major metropolitan cities in the U.S., Europe and the Middle East, featuring premium steaks, seafood and specialty cocktails in an energetic upscale atmosphere.

Benihana, an interactive dining destination with highly skilled chefs preparing food right in front of guests and served in an energetic atmosphere alongside fresh sushi and innovative cocktails. The Company franchises Benihanas in the U.S., Caribbean, Central America, and South America.

Samurai, an interactive dining experience located in sunny Miami, FL, provides a distinctive dining experience where skilled personal chefs masterfully perform the ancient art of teppanyaki right before your eyes.

Kona Grill, a polished casual, bar-centric grill concept with restaurants in the U.S., featuring American favorites, award-winning sushi, and specialty cocktails in an upscale casual atmosphere.

Salt Water Social is your gateway to the seven seas, featuring an array of signature and unique fresh seafood items, complemented by the highest quality beef dishes and elegant, delicious cocktails.

Benihana Express, a small footprint casual concept showcasing the best of Benihana but without teppanyaki tables or bar.

RA Sushi, a Japanese cuisine concept that offers a fun-filled, bar-forward, upbeat, and vibrant dining atmosphere with restaurants in the U.S. anchored by creative sushi, inventive drinks, and outstanding service.

ONE Hospitality, The ONE Group’s food and beverage hospitality services business develops, manages and operates premier restaurants and turnkey food and beverage services within high-end hotels and casinos currently operating venues in the U.S. and Europe.

Additional information about The ONE Group can be found at www.togrp.com.

Led by new BODi Super Trainer Waz Ashayer, P90X Generation Next will reignite the most popular extreme home fitness program in February 2026

ASRV, Core Home Fitness, Hyperice, and Reebok bring next-level innovation to the program

EL SEGUNDO, Calif.–(BUSINESS WIRE)– BODi (NASDAQ: BODI), today announced the highly anticipated new installment of one of the most transformative fitness programs ever created, P90X, with the launch of “P90X Generation Next,” scheduled for release on February 3, 2026. Originally developed by Super Trainer Tony Horton, this next chapter of P90X will be led by Waz Ashayer, one of Equinox Fitness Club’s most dynamic and in-demand lead instructors, where he has built a reputation for creating unparalleled training experiences that consistently draw sold-out classes and inspire a dedicated community. His leadership and intensity marks an exciting new era for the iconic P90X brand.

“P90X Generation Next” will be led by Waz Ashayer. His leadership marks an exciting new era for the iconic P90X brand.

“P90X remains one of the most powerful names in fitness, and with ‘P90X Generation Next,’ we’ve redesigned it from the bottom up to use the latest in functional program design for extreme transformation and performance,” said Carl Daikeler, CEO and co-founder of BODi. “It will have the intensity and grit that made P90X a cultural phenomenon, now with the latest science-backed methods to help people achieve results they never thought possible. With Waz Ashayer at the helm, we’re introducing the next generation to true extreme home fitness.”

Before stepping into his leading role at Equinox Fitness Club, Ashayer built his foundation in London at the prestigious boxing gym BXR, where he quickly earned recognition for his ability to drive peak performance. He went on to manage group fitness at Equinox in London, sharpening his leadership in one of the industry’s most competitive arenas. Expanding his reach to the U.S., he launched Raise x Takeoff, a series of high-intensity bootcamps in New York City and the Hamptons, solidifying his reputation as a fitness innovator with a passionate following. Today, Ashayer’s proven expertise in group training and his ability to motivate at scale make him the perfect driving force behind this new 90-day program, “P90X Generation Next”.

“Fitness has always been about unlocking inner strength and pushing past limits,” said Waz Ashayer, BODi Super Trainer and lead for P90X Generation Next. “Carrying the P90X legacy forward is an incredible honor. I’m dedicated to inspiring people to exceed their own expectations because this program isn’t just about workouts, it’s about igniting the fire of transformation.”

“P90X Generation Next” will be complemented by a roster of distinguished brand partners that are at the forefront of performance and innovation, including ASRV, Core Home Fitness, Hyperice and Reebok. Together, these partnerships underscore the P90X promise to deliver the most complete extreme home fitness experience available.

BODi will also debut a line of P90X supplements and nutrition products, engineered for fast-acting performance and to accelerate results. Developed by experts and backed by the latest innovations in performance nutrition science, the lineup is created to help high achievers get the most from their training. The full assortment will be available on BODi.com and select retail partners in early 2026.

Consumers can get ready to start “P90X Generation Next” in early 2026 by subscribing to BODi now and exploring the original P90X programs or any of BODi’s 140+ step-by-step workout and nutrition plans. BODi subscriptions start at $19 per month or $179 annually. For more information and to subscribe, go to BODi.com.

About BODi and The Beachbody Company

BODi, formerly known as Beachbody, has been a pioneer in structured, step-by-step home fitness and nutrition programs for nearly three decades, with iconic programs like P90X, INSANITY, 21 Day Fix and the original premium superfood supplement, Shakeology. Since its inception, BODi has helped more than 30 million people reach life-changing results. Today, BODi continues to evolve with a simple mission: help people achieve their goals and lead healthy, fulfilling lives, especially busy, time-strapped people who want to fit healthy habits into everyday life with proven solutions. The BODi community empowers millions to stay motivated and accountable, supporting healthy weight management, improved metabolic function, increased mental and physical well-being, better sleep, as well as evidence-based habits that enhance healthspan and longevity.

Third Quarter Revenue of $1.6 Billion with GAAP EPS of $0.72; Adjusted EPS of $1.14

GAAP Operating Income of $34 Million; Net Income of $23 Million; Operating Cash Flow of $90 Million

Adjusted EBITDA of $62 Million; Adjusted Free Cash Flow of $89 Million

Previously Announced Transaction Expected to Close by Year-End 2025

BOCA RATON, Fla.–(BUSINESS WIRE)–Nov. 5, 2025– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the third quarter ended September 27, 2025.

Consolidated (in millions, except per share amounts)

3Q25

3Q24

YTD25

YTD24

Selected GAAP and Non-GAAP measures:

Sales

$1,625

$1,780

$4,911

$5,367

Sales change from prior year period

(9)%

(8)%

Operating income

$34

$102

$11

$143

Adjusted operating income (1)

$38

$41

$117

$141

Net income (loss) from continuing operations

$23

$68

$(6)

$95

Diluted earnings (loss) per share from continuing operations

$0.72

$2.04

$(0.21)

$2.65

Adjusted net income from continuing operations (1)

$36

$24

$83

$94

Adjusted earnings per share from continuing operations (fully diluted) (1)

$1.14

$0.71

$2.71

$2.61

Adjusted EBITDA (1)

$62

$62

$184

$210

Operating Cash Flow from continuing operations

$90

$81

$163

$125

Free Cash Flow (2)

$78

$58

$118

$51

Adjusted Free Cash Flow (3)

$89

$68

$147

$90

Third Quarter 2025 Summary(1)(3)

Total reported sales of $1.6 billion, down 9% versus the prior year period on a reported basis. The decrease in reported sales is largely related to lower sales in its Office Depot Division, primarily due to 63 fewer retail locations in service compared to the previous year and reduced retail and online consumer traffic, as well as lower sales in its ODP Business Solutions Division.

GAAP operating income of $34 million and net income from continuing operations of $23 million, or $0.72 per diluted share, versus $102 million and $68 million, respectively, or $2.04 per diluted share, in the prior year period

Adjusted operating income of $38 million, compared to $41 million in the third quarter of 2024; adjusted EBITDA of $62 million in both the third quarter of 2025 and 2024. Adjusted operating income in the third quarter of 2024 excludes $70 million of income related to legal matter monetization where the Company was engaged in legal proceedings as a plaintiff

Adjusted net income from continuing operations of $36 million, or adjusted diluted earnings per share from continuing operations of $1.14, versus $24 million or $0.71, respectively, in the prior year period. Adjusted net income from continuing operations in the third quarter of 2024 excludes $70 million of income, or $51 million net of tax, related to legal matter monetization where the Company was engaged in legal proceedings as a plaintiff

Operating cash flow from continuing operations of $90 million and adjusted free cash flow of $89 million, versus $81 million and $68 million, respectively, in the prior year period

$730 million of total available liquidity including $182 million in cash and cash equivalents at quarter end

Consolidated Results

Reported (GAAP) Results Total reported sales for the third quarter of 2025 were $1.6 billion, a 9% decrease compared to the same period last year, primarily reflecting lower sales in both the consumer and business-to-business (B2B) divisions. The decline in the consumer division, Office Depot, was mainly driven by 63 fewer stores in operation due to planned closures, as well as reduced retail and online consumer traffic. On a comparable store basis, sales declined 7%, representing an improvement over the 10% decrease in the prior year period. In the ODP Business Solutions Division, sales declined 6% year-over-year, primarily reflecting ongoing macroeconomic headwinds and softer enterprise customer spending. Veyer continued to deliver strong logistical support for both the ODP Business Solutions and Office Depot divisions despite lower internal sales volume, while also advancing its growth strategy by providing supply chain and procurement solutions to third-party customers and driving increases in external revenue.

The Company reported GAAP operating income of $34 million in the third quarter of 2025, down compared to $102 million in the prior year period. Operating results in the third quarter of 2025 included $4 million of charges primarily related to $8 million in transaction and integration expenses associated with the Merger (as defined below), $5 million in non-cash asset impairments of operating lease right-of-use (“ROU”) assets associated with the Company’s retail store locations, $2 million related to the impairment of operating lease ROU assets associated with the Company’s supply chain facilities, and $1 million related to the impairment of fixed assets. These charges were partially offset by $12 million in restructuring income primarily associated with the Optimize for Growth restructuring plan. Net income from continuing operations was $23 million, or $0.72 per diluted share in the third quarter of 2025, down compared to net income from continuing operations of $68 million, or $2.04 per diluted share in the third quarter of 2024.

Adjusted (non-GAAP) Results(1) Adjusted results for the third quarter of 2025 exclude charges and credits totaling $4 million as described above and the associated tax impacts.

Third quarter 2025 adjusted EBITDA was $62 million, flat with the prior year period. This included adjusted depreciation and amortization of $24 million in both the third quarter of 2025 and 2024

Third quarter 2025 adjusted operating income was $38 million, down compared to $41 million in the third quarter of 2024

Third quarter 2025 adjusted net income from continuing operations was $36 million, or $1.14 per diluted share, compared to $24 million, or $0.71 per diluted share, in the third quarter of 2024, an increase of 61% on a per share basis

Division Results

ODP Business Solutions Division Leading B2B distribution solutions provider serving small, medium and enterprise level companies with an annual trailing-twelve-month revenue of $3.4 billion.

Reported sales for the third quarter of 2025 were $862 million, a decrease of 6% year-over-year. This result reflects an improvement in revenue trends compared to the prior year period, despite ongoing macroeconomic challenges and continued softness in enterprise demand. Year-over-year revenue trends improved by about 200 basis points, driven by ODP Business Solutions’ success in onboarding new customers, executing targeted sales initiatives, and generating incremental growth in hospitality sector

Total adjacency category sales, including cleaning and breakroom, furniture, technology, and copy and print, were 45% of total ODP Business Solutions’ sales, representing an increase over the same period last year

Drove accelerated sales growth in Operating, Supplies & Equipment (OS&E) categories within the hospitality business and expanded presence in new markets helping drive increased demand for traditional product categories. Onboarded more than 600 new hotel properties as customers under the Company’s existing hospitality agreement. Made meaningful progress on potential new agreements with several leading hospitality management companies

Operating income was $14 million in the third quarter of 2025, down compared to $28 million in the same period last year on a reported basis

Office Depot Division Leading provider of retail consumer and small business products and services distributed via Office Depot and OfficeMax retail locations and eCommerce presence.

Reported sales were $749 million in the third quarter of 2025, down 13% year-over-year, reflecting an improvement over prior year trends. Sales were impacted by 63 fewer retail locations due to planned store closures, lower demand in certain product categories, and reduced online sales. Comparable store sales declined 7%, an improvement versus the 10% decrease in the prior year period, as targeted, profitable sales strategies gained traction. The Company closed 12 retail stores during the quarter, ending with 822 retail locations

Store and online traffic were lower year-over-year due to macroeconomic factors. However, targeted sales promotions resulted in higher average order volumes and sales per shopper, which supported top-line results and margins

Operating income was $31 million in the third quarter of 2025, compared to $23 million during the same period last year on a reported basis. As a percentage of sales, operating income was 4%, increase of 140 basis points from the same period last year

Veyer Division Nationwide supply chain, distribution, procurement and global sourcing operation supporting Office Depot and ODP Business Solutions, as well as third-party customers. Veyer’s assets and capabilities include 7 million square feet of infrastructure through a network of distribution centers, cross-docks, and other facilities throughout the United States; a global sourcing presence in Asia; and business next-day delivery capabilities to 98.5% of U.S. population.

In the third quarter of 2025, Veyer provided support for its internal customers, ODP Business Solutions and Office Depot, as well as its third-party customers, generating reported sales of $1.1 billion

Reported operating income was $12 million in the third quarter of 2025, compared to $9 million in the prior year period

In the third quarter of 2025, sales generated from third-party customers increased by 64% compared to the same period last year, resulting in sales of $23 million. EBITDA generated from third-party customers was $7 million in the quarter

Balance Sheet and Cash Flow

As of September 27, 2025, ODP had total available liquidity of $730 million, consisting of $182 million in cash and cash equivalents and $548 million of available credit under the Fourth Amended Credit Agreement. Total debt was $148 million.

For the third quarter of 2025, cash provided by operating activities of continuing operations increased to $90 million, which included $10 million in restructuring spend, compared to $81 million in the third quarter of the prior year, which included $10 million in restructuring spend. The year-over-year increase in operating cash flow is primarily related to operational discipline including strong cash conversion, as well as prudent working capital management helping to offset the impact of lower sales.

Capital expenditures were $12 million in the third quarter of 2025 versus $22 million in the prior year period, as the Company continued to prioritize capital investments towards B2B growth opportunities supporting its supply chain operations, distribution network, and digital capabilities. Adjusted Free Cash Flow(3) was $89 million in the third quarter of 2025, up compared to $68 million in the prior year period.

“Optimize for Growth” B2B Revenue Acceleration Plan

In the third quarter of 2025, the Company advanced its “Optimize for Growth” restructuring plan, an initiative aimed at reducing fixed-cost infrastructure while leveraging core strengths to accelerate growth in B2B market segments. This includes expansion into new enterprise verticals such as hospitality, healthcare, and other adjacent sectors.

As part of this plan in the third quarter of 2025, the Company recognized $13 million of restructuring income primarily related to a $17 million gain on disposal of an owned distribution facility. The Company closed 12 retail stores, 15 satellite locations and one distribution facility. In total, over the multi-year life of the plan, the Company expects to incur costs in the range of $185 million to $230 million, which we anticipate will generate approximately $380 million in EBITDA improvement and generate over $1.3 billion in total value.

Transaction Update

As previously announced on September 22, 2025, the Company entered into a definitive agreement to be acquired, via merger (the “Merger”), by an affiliate of Atlas Holdings. The Company’s Board of Directors has unanimously approved the Merger, which the Company continues to expect will be completed by the end of 2025. The Merger is subject to customary closing conditions, including regulatory approvals and approval by the Company’s shareholders. In light of the pending Merger, the Company will not hold an earnings conference call or provide forward-looking guidance.

(1)

As presented throughout this release, adjusted results represent non-GAAP financial measures and exclude charges or credits not indicative of core operations and the tax effect of these items, which may include but not be limited to merger integration, restructuring, acquisition costs, asset impairments, and $70 million in operating income related to legal matter monetization where the Company was engaged in legal proceedings as a plaintiff. Reconciliations from GAAP to non-GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(2)

As used in this release, Free Cash Flow is defined as cash flows from operating activities less capital expenditures and changes in restricted cash. Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

(3)

As used in this release, Adjusted Free Cash Flow is defined as Free Cash Flow excluding cash charges associated with the Company’s restructuring programs, and related expenses. Adjusted Free Cash Flow is a non-GAAP financial measure and reconciliations from GAAP financial measures can be found in this release as well as on the Company’s Investor Relations website at investor.theodpcorp.com.

About The ODP Corporation

The ODP Corporation (NASDAQ:ODP) is a leading provider of products, services and technology solutions through an integrated business-to-business (B2B) distribution platform and omni-channel presence, which includes supply chain and distribution operations, dedicated sales professionals, online presence, and a network of Office Depot and OfficeMax retail stores. Through its operating companies ODP Business Solutions, LLC; Office Depot, LLC; and Veyer, LLC, The ODP Corporation empowers every business, professional, and consumer to achieve more every day. For more information, visit theodpcorp.com.

This communication contains statements that constitute “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 27A of the Securities Act of 1933, as amended. All statements that are not statements of historical fact are forward-looking statements. Without limitation, when we use the words “believe,” “estimate,” “plan,” “expect,” “intend,” “anticipate,” “continue,” “may,” “project,” “probably,” “should,” “could,” “will” and similar expressions in this communication, we are identifying forward-looking statements (as such term is defined in the Private Securities Litigation Reform Act of 1995). These statements appear in a number of places in this communication and include statements regarding the intent, belief, or current expectations of the Company, its directors, or its officers with respect to, among other things, the Company’s acquisition by an affiliate of Atlas Holdings, trends affecting the Company’s financial condition or results of operations, the Company’s ability to achieve its strategic plans, including the benefits related to Optimize for Growth, Project Core and other strategic restructurings or initiatives, liquidity, suppliers, consumers, customers, and employees, disruptions or inefficiencies in our supply chain, uncertainties arising from conflicts including the conflicts in Russia-Ukraine and in the Middle East, and macroeconomic drivers and their effect on the U.S. economy, changes in trade policy and tariffs, changes in worldwide and U.S. economic conditions including higher interest rates that materially impact consumer spending and employment and the demand for our products and services, and the outcome of contingencies such as litigation and investigations. Readers are cautioned that any forward-looking statements are not guarantees of future performance and involve risks and uncertainties. More information regarding these risks, uncertainties and other important factors that could cause actual results to differ materially from those in the forward-looking statements is set forth in our discussion of “Risk Factors” within Other Key Information in our Annual Report on Form 10-K filed on February 26, 2025 (the “2024 Form 10-K”) with the SEC and within Other Information in our Quarterly Reports on Form 10-Q filed for any subsequent fiscal quarters.

VIRGINIA CITY, Nev., November 05, 2025 (GLOBE NEWSWIRE) — Comstock Inc. (NYSE: LODE) (“Comstock” and the “Company”) and Comstock Metals LLC (“Comstock Metals”), a leader in the responsible recycling of end-of-life solar panels with the only certified, north American, zero-landfill solution, announced today that it has received its notification of eligibility for a Written Determination Permit from the Nevada Division of Environmental Protection – Bureau of Sustainable Materials Management (NDEP-BSMM), subject to certain normal compliance conditions and public notice periods, for the processing of waste solar panels and photovoltaics for its industry-scale materials recovery facility located in Silver Springs, NV. This timely approval keeps our scale up plans for commissioning our first industry-scale facility in Silver Springs, NV, right on schedule.

Comstock Metals expects the receipt of a similar notification of approval for the Air Quality control permit in the next few weeks, also with the normal conditions and public notice period. These permits, once final, represent the complete scope of required regulatory approvals for commissioning the scale up of a facility designed for processing over 3 million panels per year from one, continuous production line, representing up to 100,000 tons per year of waste materials being processed. This facility integrates technologies for efficiently crushing, conditioning, extracting, and recycling metal concentrates from photovoltaics. The Company previously ordered all of the equipment and expects deliveries by year end, so that it can commence installation, testing, and commissioning of the industry-scale facility during the first quarter of 2026.

“We appreciate BSMM’s collaborative efforts in issuing this first solar panel recycling Written Determination permit and enabling the only Nevada-based, zero-landfill, end-of-life solar panel solution serving this broad region and keeping these critical materials out of our landfills,” said Dr. Fortunato Villamagna, President of Comstock Metals. “Our original expectations for the receipt of these permits were for the end of October, so these notifications keep us right on schedule. This is a true testament to the strong working relationship we have with our regulators and the successful efforts of a complex process.”

Most of the U.S. solar panels have been deployed in the southwestern U.S., primarily California, Arizona, and Nevada, with decommissioning of these solar panels occurring now, accelerating supply and increasing the demand for environmentally responsible end-of-life solutions. Comstock has positioned itself to ensure the safe deconstruction and productive reuse of these important materials. Establishing our platform in Nevada establishes the leading solar recycling position over more than half the U.S. market for end-of-life panels and establishes a platform for rapid expansion across the rest of the United States.

“We are receiving waste panels continuously into our facility and very much look forward to commencing our commissioning activities. We are receiving more and more customer inquiries as waste panels are becoming rapidly available from many different sources, directly enabling and supporting our ramp up efforts” stated Dr. Villamagna.

“We have quickly established a leadership position in this readily available, and rapidly growing photovoltaic market,” stated Corrado De Gasperis, Comstock’s Executive Chairman and CEO. “Our metals team is already assessing additional sites for our industry scale solution and an expanded storage capability, as we look to capitalize and expand our lead in this rapidly growing end-of-life solar dilemma. Comstock Metals is the leading zero-landfill, end-of-life solution for these wasted solar panels.”

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 ir@comstockinc.com

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future market conditions; future explorations or acquisitions; divestitures, spin-offs or similar distribution transactions, future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, divestitures, spin-offs or similar distribution transactions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; business opportunities, growth rates, future working capital, needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; operational or technical difficulties in connection with exploration, metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious and other metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; challenges to, or potential inability to, achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology and efficacy, quantum computing and generative artificial intelligence supported advanced materials development, development of cellulosic technology in bio-fuels and related material production; commercialization of cellulosic technology in bio-fuels and generative artificial intelligence development services; ability to successfully identify, finance, complete and integrate acquisitions, spin-offs or similar distribution transactions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Phase 2/3 OCU410ST GARDian3 pivotal confirmatory trial is progressing toward 1H 2027 Biologics License Application (BLA) filing with 50% enrollment completed to date

European Medicines Agency (EMA) provided acceptability of a single U.S.-based trial for submission of a Marketing Authorization Application (MAA)

Executed licensing agreement with Kwangdong Pharmaceutical for exclusive rights in South Korea to OCU400

Sales milestones of $1.5 million for every $15 million of sales in South Korea, projected to reach $180 million or more in first 10 years of commercialization and royalties equaling 25% of net sales

Closed $20 million registered direct offering of common stock and accompanying premium warrants

The Company will receive $30 million of additional gross proceeds if the warrants are exercised in full

MALVERN, Pa., Nov. 05, 2025 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a pioneering biotechnology leader in gene therapies for blindness diseases, today reported third quarter 2025 financial results along with a general business update.

“With two late-stage modifier gene therapies on track to meet 2026 and 2027 BLA/MAA filings, it’s remarkable to look back and recognize we only began dosing the first patient in the Phase 1/2 OCU400 clinical trial in 2022,” said Dr. Shankar Musunuri, Chairman, CEO, and Co-founder of Ocugen. “The OCU410ST Phase 2/3 GARDian3 pivotal confirmatory trial is following close behind the OCU400 Phase 3 liMeLiGhT clinical trial, and with 50% enrollment completed to date, we believe recruitment will be completed in the first quarter of 2026. This progress not only reinforces our commitment to file three BLAs in the next three years, but it also brings us closer to addressing the incredible unmet medical needs that exist for patients facing vision loss.”

In September, Ocugen announced its exclusive licensing agreement with Kwangdong Pharmaceutical Co., Ltd. (Kwangdong) for the rights to OCU400 in South Korea. Under the agreement, the Company will receive up to $7.5 million in upfront and development milestone payments, plus sales milestones of $1.5 million for every $15 million of sales in South Korea, projected to reach $180 million or more in the first 10 years of commercialization. The Company will also earn a 25% royalty on net sales generated by Kwangdong and will be responsible for manufacturing and supplying OCU400. A regional approach preserves Ocugen’s rights to larger geographies to maximize total patient reach while also generating a potential return for shareholders.

Enrollment in the OCU400 Phase 3 liMeliGhT clinical trial is nearing completion, and the program remains on track for BLA and MAA submissions in 2026. This is the only known broad retinitis pigmentosa (RP) gene-agnostic trial to address multiple genetic mutations and multiple disease pathways with a single therapeutic approach. There are approximately 300,000 people in the U.S. and Europe combined living with RP, which affects greater than 100 genes. Ocugen’s gene-agnostic approach has the potential to treat multiple gene mutations associated with RP with a one-time subretinal injection.

The Phase 2/3 GARDian3 pivotal confirmatory trial for OCU410ST for Stargardt disease is well underway and in August the Company announced that the Committee for Medicinal Products for Human Use (CHMP) of the EMA provided acceptability of a single U.S.-based trial for submission of an MAA. Stargardt disease affects approximately 100,000 people in the U.S. and Europe combined, and approximately 1 million globally. Currently, there is no FDA-approved treatment available for Stargardt disease.

Also in August, Ocugen closed a registered direct offering pursuant to a securities purchase agreement with Janus Henderson Investors for the purchase and sale of 20,000,000 shares of common stock and warrants to purchase up to an aggregate of 20,000,000 shares of common stock at a purchase price of $1.00 per share and accompanying warrant at a premium exercise price of $1.50 per share. The gross proceeds to the Company were approximately $20 million, which Ocugen anticipates will extend the Company’s cash runway into the second quarter of 2026. The Company will receive $30 million of additional gross proceeds if the warrants are exercised in full extending runway into 2027.

“We will continue to pursue financing opportunities along with strategic business development to fund the Company into commercialization,” said Dr. Musunuri. “We have engaged with potential funding and business partners during various investor and global conferences. I look forward to additional substantive conversations between now and the end of the year.”

Upcoming inflection points for Ocugen’s novel modifier gene therapy platform include OCU410 (Geographic Atrophy) Phase 2 full data release expected in the first quarter of 2026, OCU410ST (Stargardt disease) interim data on 50% of patients at eight months of treatment expected mid-year 2026, and OCU400 (RP) Phase 3 top line data expected in the fourth quarter of 2026. The Company looks forward to providing the market and key stakeholders with near-term catalysts supporting Ocugen’s strong path forward.

OCU400 – Enrollment in the Phase 3 liMeliGhT clinical trial is nearing completion. The Company secured an exclusive licensing agreement with Kwangdong for rights to OCU400 in South Korea and will continue to pursue regional partnerships. Intend to initiate BLA rolling submission in the first half of 2026 and release Phase 3 top-line data in the fourth quarter of 2026.

OCU410ST – Pivotal confirmatory Phase 2/3 trial is ahead of schedule. CHMP of the EMA provided acceptability of a single U.S.-based trial for submission of an MAA. Intend to release interim data (50% of patients at 8 months of treatment) mid-year 2026.

OCU410 – Intend to release full data from the Phase 2 clinical trial in the first quarter of 2026 and begin Phase 3 in 2026.

Ophthalmic Biologic Product

OCU200 – Intend to complete enrollment in the Phase 1 clinical trial in 4Q 2025.

Third Quarter 2025 Financial Results

With the recent $20 million financing in the third quarter, we expect our current cash position provides sufficient runway to operate through 2Q 2026.

The Company’s cash, cash equivalents and restricted cash totaled $32.9 million as of September 30, 2025, compared to $58.8 million as of December 31, 2024.

Total operating expenses for the three months ended September 30, 2025 were $19.4 million and included research and development expenses of $11.2 million and general and administrative expenses of $8.2 million. This compares to total operating expenses for the three months ended September 30, 2024 of $14.4 million that included research and development expenses of $8.1 million and general and administrative expenses of $6.3 million.

Conference Call and Webcast Details

Ocugen has scheduled a conference call and webcast for 8:30 a.m. ET today to discuss the financial results and recent business highlights. Ocugen’s senior management team will host the call, which will be open to all listeners. There will also be a question-and-answer session following the prepared remarks.

Attendees are invited to participate on the call or webcast using the following details:

Dial-in Numbers: (800) 715-9871 for U.S. callers and (646) 307-1963 for international callers Conference ID: 3029428 Webcast: Available on the events section of the Ocugen investor site

A replay of the call and archived webcast will be available for approximately 45 days following the event on the Ocugen investor site.

About Ocugen, Inc. Ocugen, Inc. is a pioneering biotechnology leader in gene therapies for blindness diseases. Our breakthrough modifier gene therapy platform has the potential to address significant unmet medical need for large patient populations through our gene-agnostic approach. Unlike traditional gene therapies and gene editing, Ocugen’s modifier gene therapies address the entire disease—complex diseases that are potentially caused by imbalances in multiple gene networks. Currently we have programs in development for inherited retinal diseases and blindness diseases affecting millions across the globe, including retinitis pigmentosa, Stargardt disease, and geographic atrophy—late stage dry age-related macular degeneration. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, including, but not limited to, strategy, business plans and objectives for Ocugen’s clinical programs, plans and timelines for the preclinical and clinical development of Ocugen’s product candidates, including the therapeutic potential, clinical benefits and safety thereof, expectations regarding timing, success and data announcements of current ongoing preclinical and clinical trials, the ability to initiate new clinical programs, Ocugen’s financial condition and expected cash runway into the second quarter of 2026, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines,and Ocugen’s projections under its license agreement with Kwangdong Pharmaceutical Co., Ltd., which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including, but not limited to, the risks that preliminary, interim and top-line clinical trial results may not be indicative of, and may differ from, final clinical data; that unfavorable new clinical trial data may emerge in ongoing clinical trials or through further analyses of existing clinical trial data; that earlier non-clinical and clinical data and testing of may not be predictive of the results or success of later clinical trials; and that that clinical trial data are subject to differing interpretations and assessments, including by regulatory authorities. These and other risks and uncertainties are more fully described in our annual and periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Atlanta, GA – November 4, 2025 – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing multi-antigen vaccines and immunotherapies for infectious diseases and cancer, today announced that it will report its financial results for the quarter ended September 30, 2025, after the close of U.S. markets on Thursday, November 13, 2025. Following the release, management will host a live conference call and audio webcast at 4:30 p.m. ET to review results and provide a business update.

Conference Call Details

To access the live conference call, participants may register in advance here (https://edge.media-server.com/mmc/p/u86rmdmb/). The live audio webcast of the call will be available via the “Events & Presentations” section of the Company’s Investor Relations website at www.geovax.com/investors. To participate via telephone, please register using the link above; registrants will receive a confirmation email with dial-in information, a unique passcode, and access instructions. Although registration is not required, participants are encouraged to join ten minutes prior to the scheduled start. An archive of the webcast will be available on the Company’s website approximately two hours after the conclusion of the call and will remain available for at least 90 days.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel vaccines against infectious diseases and therapies for solid tumor cancers. The Company’s lead clinical program is GEO-CM04S1, a next-generation COVID-19 vaccine currently in three Phase 2 clinical trials, being evaluated as (1) a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, (2) a booster vaccine in patients with chronic lymphocytic leukemia (CLL) and (3) a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. In oncology the lead clinical program is evaluating a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, having recently completed a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax is also developing a vaccine targeting Mpox and smallpox and, based on recent EMA regulatory guidance, anticipates progressing directly to a Phase 3 clinical evaluation, omitting Phase 1 and Phase 2 trials. GeoVax has a strong IP portfolio in support of its technologies and product candidates, holding worldwide rights for its technologies and products. For more information about the current status of our clinical trials and other updates, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

VANCOUVER, B.C., November 4, 2025 – Nicola Mining Inc. (TSX.V: NIM)(FSE: HLI) (OTCQB: HUSIF), (the “Company” or “Nicola”) is pleased to announce that it has completed work at Dominion for 2025 and has completed all mine development for the 10,000 bulk sample, which is planned to recommence in July of 2026. Initially, the Company had planned to ship up to 2000 tonnes to the Nicola mill in 2025 for processing, but opted to wait until next year for two reasons:

Weather: Abnormally high rainfall during August and September would likely degrade the haul road from overuse.

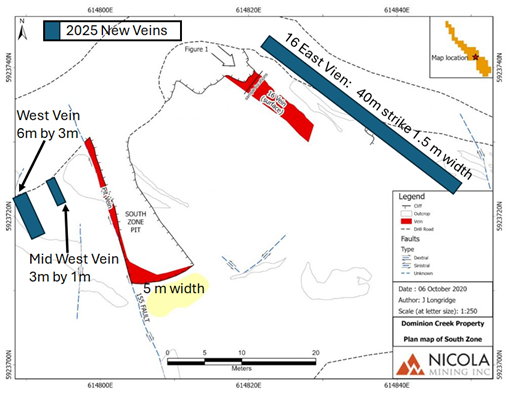

Project Size: During the mine development phase (“Development Phase”), which commenced in August following completion of haul road upgrades, a landing area (“Landing”) was constructed to provide access for vein extraction. The Development Phase included lowering the entire Landing by approximately 6 metres to create a face suited for vein extraction. While developing the Landing, three additional veins were discovered.

Dominion Map Higlighting 2025 Work and Vein Discoveries

Figure 1. Map showing the locations of 3 new veins discovered in 2025. Note: The map is from 2020 due diligence with additional of veins uncovered in 2025 indicated.

Historically Known Veins:

South Pit Vein: Historically known vein from which previously chip samples were taken in 2020 Link. Samples taken were comprised of two South Pit Samples and two 16 Vein Samples. During 2025, the Company commenced vein extraction in the South Pit Zone, having moved the Landing down and working into the vein approximately 2 metres. Approximately 20 metres from the entrance, the vein expands to approximately 5 metres in width.

16 Vein: This historically known vein is located approximately 20 metres from the South Pit Vein. Chip samples and grab samples were taken from the vein during the October 14, 2020 due diligence process.

Newly Exposed Veins:

Mid-West Vein: Located 13 metres from the South Pit Vein. The vein is approximately 1 metre wide and exposed over 3 metres.

West Vein: Located 12 metres from the Mid-West Vein. The vein is approximately 3 metres wide and exposed over 6 metres.

16 East Vein: Located 1.5-2 metres east of the 16 Vein. It is approximately 1.5 metres wide and exposed over 40 metres.

Samples from the newly exposed veins were taken by site crew and brought to Paragon Geochemical for analysis. Paragon Geochemical is an ISO 17025:2017 accredited geochemical testing laboratory providing analytical services to the mining industry. Results will be released upon receipt.

Figure 6. Mid-West Vein

Mr. Peter Espig, CEO of Nicola Mining Inc., commented, “We have been pleasantly surprised with the work at Dominion, which clearly indicates that the project is larger than initially anticipated. For the 2026 Program, we now have 5 open faces that are accessible from the Landing to give approximately 6 metres of strike length for extraction. These exposed veins also represent attractive exploration targets as they are open at depth.”

Qualified Person

The scientific and technical disclosures included in this news release have been reviewed and approved by Will Whitty, P.Geo., who is the Qualified Person as defined by NI 43-101. Mr. Whitty is Vice President of Exploration for the Company.

DOMINION CREEK PROPERTY HISTORY

The Dominion Creek Property consists of 9 mineral claims (55 units) totaling approximately 1,058 hectares. The property was acquired from the prospector N. Kencayd by Noranda Exploration Company Ltd. in 1986. Noranda subsequently conducted geological, geochemical, and geophysical surveys which culminated in an increase in their land position. Between 1987 and 1990, Noranda’s exploration program included a small (20 samples) geochemical silt sample survey. Encouraged by those results, a larger soil geochemical survey (3,399 samples) was conducted. Noranda drilled a total of 53 shallow diamond drill holes, totaling 3,483.86 meters (average depth of approximately 65.7 meters). Trenching of several coincident Pb, Zn, Cu, Ag and Au soil geochemistry anomalies resulted in the discovery of several mineralized quartz veins.

Drilling in the South Zone covered an area of approximately 300 meters by 200 meters. Limited drilling in the North Zone covered two small areas (approximately 50 meters by 60 meters) 300 meters apart. The drill targets were selected using the soil geochemistry survey data and outcrop sampling from trenches and the drill access road data. Noranda subsequently returned the property to N. Kencayd, who sold it to A. Raven in 1989.

A Technical Report[1] on the Dominion Creek Project was completed by Geospectrum Engineering on August 22, 2003.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high grade gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a high-grade copper property, which covers an area of 10,913 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

[1] Makepeace, D. K., 2003. Dominion Creek Project Technical Report for XMP Mining Ltd. Geospectrum Engineering, August 22.

The information in these press releases is historical in nature, has not been updated, and is current only to the date indicated in the particular press release. This information may no longer be accurate and therefore you should not rely on the information contained in these press releases. To the extent permitted by law, Nicola Mining Inc. and its employees, agents and consultants exclude all liability for any loss or damage arising from the use of, or reliance on, any such information, whether or not caused by any negligent act or omission.

Planning to initiate an open-label Phase 2 study of TNX-1500 under an investigator-initiated IND to evaluate safety and activity in the first half of 2026

Novel immunomodulatory regimen designed to reduce calcineurin inhibitor exposure and improve outcomes

Dimeric Fc-modified mAb TNX-1500 selectively targets cell-associated CD40L with once-monthly dosing

CHATHAM, N.J., Nov. 04, 2025 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully-integrated, commercial biotechnology company, today announced a collaboration with Massachusetts General Hospital (MGH), a founding member of Mass General Brigham (MGB) to conduct a Phase 2 clinical trial evaluating monoclonal antibody (mAb) TNX-1500 in kidney transplant recipients. The investigator-initiated study will be led by Ayman Al Jurdi, M.D., at MGH and is designed to assess the safety, tolerability and activity of Fc-modified anti-CD40L mAb TNX-1500 in preventing kidney transplant rejection while significantly minimizing the dose of conventional immunosuppressive drugs, which are associated with infection, cancer, cardiovascular side effects and various metabolic derangements. The CD40 ligand (CD40L) is also known as CD154. Study initiation is contingent on institutional review board (IRB) approval and FDA clearance of an investigator-initiated investigational new drug application (IND).

“TNX-1500 represents a differentiated approach that is designed to block the function of cell-associated CD40L,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Collaborating with MGH, one of the nation’s leading transplant research centers, allows us to advance this promising candidate in patients who need safer therapies with better long-term outcomes. The Fc-modified TNX-1500 has shown activity and has been well tolerated in animals1,2 and in a Phase 1 pharmacodynamic (PD) and pharmacokinetic (PK) study that supports monthly dosing. Ultimately, our goal is to establish TNX-1500 as a monotherapy, with the potential to transform the landscape of organ transplant management.”

“The ability to modulate the immune system without the toxicities associated with prolonged standard dose CNIs is one of the most pressing unmet needs in transplantation,” said Ayman Al Jurdi, M.D., Principal Investigator at MGH. “Studying TNX-1500 in this Phase II trial will allow us to explore its potential to improve long-term outcomes for kidney transplant recipients.”

Pending IRB approval and IND clearance, the open-label, single-center study will enroll five adult kidney transplant recipients at MGH. Patients will receive induction therapy with anti-thymocyte globulin, TNX-1500, tacrolimus, and corticosteroids. The corticosteroids will be tapered and discontinued by Day 33 post-transplant. TNX-1500 will be continued for 12 months (to the primary endpoint) with an option to continue treatment beyond 12 months. Tacrolimus at standard dose will be continued for six months, at which point tacrolimus will be decreased to low dose with the expectation of discontinuing tacrolimus after 12 months. The primary endpoint is the incidence of adverse and serious adverse events at 12 months. Secondary endpoints include graft survival, renal function, biopsy-proven acute rejection, and incidence of donor-specific antibodies. The study is expected to be initiated in the first half of 2026.

About TNX-1500

TNX-1500 (Fc-modified humanized anti-CD40L mAb) is a humanized monoclonal antibody that interacts with the CD40-ligand (CD40L), also known as CD154. TNX-1500 is being developed for the prevention of allograft and xenograft rejection, for the prevention of graft-versus-host disease (GvHD) after hematopoietic stem cell transplantation (HCT) and for the treatment of autoimmune diseases. The first-in-human Phase 1 PD/PK study of TNX-1500 was completed and topline reported in first quarter 2025 to support dosing in a planned Phase 2 trial in kidney transplant recipients. The primary objective of the Phase 1 trial was to assess the safety, tolerability, PD and PK of single-dose intravenous (i.v.) TNX-1500 at 3 mg/kg, 10 mg/kg, and 30 mg/kg. Two published articles in the peer-reviewed American Journal of Transplantation demonstrate TNX-1500 prevents rejection, prolongs survival and preserves graft function as a single agent or in combination with other drugs in animal renal and heart allografts.1,2

1Lassiter G, et al. Am J Transplant. 2023;23(8):1171-1181. 2Miura S, et al. Am J Transplant. 2023;23(8):1182-1193.

Tonix Pharmaceuticals Holding Corp.

Tonix Pharmaceuticals is a fully-integrated commercial biotechnology company with marketed products and a pipeline of development candidates. Tonix has received FDA approval for Tonmya™ (cyclobenzaprine HCl sublingual tablets), a first-in-class, non-opioid analgesic medicine for the treatment of fibromyalgia, a chronic pain condition that affects millions of adults. This marks the first approval for a new prescription medicine for fibromyalgia in more than 15 years. Tonix also markets two treatments for acute migraine in adults. Tonix’s development portfolio is focused on central nervous system (CNS) disorders, immunology, immuno-oncology, rare disease and infectious disease. TNX-102 SL (cyclobenzaprine HCl sublingual tablets) is being developed to treat acute stress reaction and acute stress disorder under a Physician-Initiated IND at the University of North Carolina in the OASIS study funded by the U.S. Department of Defense (DoD). TNX-102 SL is also in development for major depressive disorder. Tonix’s rare disease portfolio includes TNX-2900, intranasal potentiated oxytocin with magnesium, in development for Prader-Willi syndrome. Tonix’s infectious disease portfolio includes TNX-801, a vaccine in development for mpox and smallpox, as well as TNX-4800, a monoclonal antibody for the seasonal prevention of Lyme Disease. Finally, TNX-4200 for which Tonix has a contract with the U.S. DoD’s Defense Threat Reduction Agency (DTRA) for up to $34 million over five years, is a small molecule broad-spectrum antiviral agent targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, Md.

* Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements